Embed Size (px)

Citation preview

M&A handbookiberian market

2013

An analysis of transactions in 2012, including M&A, private equiy and venture capital

www.TTRecord.com

M&A handbookiberian market

2013

Note from the Authors:The M&A HANDBOOK is a result of local research and market analysis by TTR’s Research

and Business Intelligence team. Our team follows the transactional markets analysed in this Handbook at a local level, in local language, and on a daily basis – researching transactional and financial data by contacting market players, collecting their input and crosschecking and analysing the data throughout the year.

For full access to all of the transactional data on Latin America and the Iberian market (spanning Mergers and Acquisitions, Equity Capital Markets, Acquisition Finance and Project Finance) visit TTR at www.TTRecord.com.

INTRODUCTIONDEFINITIONSTRANSACTIONS

HIGH-END MARKET Spain

MID-MARKET Spain

SMALLER MARKET Spain

PRIVATIZATIONS Portugal

HIGH-END MARKET Portugal

MID-MARKET Portugal

SMALLER MARKET Portugal

ENTITIES

BANKS AND SAVINGS BANKS Spain

PRIVATE EQUITY / VENTURE CAPITAL Spain

LEGAL ADVISERS Spain

CONSULTANCY FIRMS / FINANCIAL ADVISERS Spain

BANKS Portugal

PRIVATE EQUITY / VENTURE CAPITAL Portugal

LEGAL ADVISER Portugal

CONSULTANCY FIRMS / FINANCIAL ADVISERS Portugal

SECTORS AND SUBSECTORS

ENERGY AND RENEWABLE ENERGIES Spain

INDUSTRY Spain

INFRASTRUCTURE Spain

REAL STATE AND CONSTRUCTION Spain

MILITARY AND STATE DEFENSE Spain

NATURAL RESOURCES Spain

SERVICES AND DISTRIBUTION Spain

TECHNOLOGY AND TELECOMS Spain

ENERGY AND RENEWABLE ENERGIES Portugal

INDUSTRY Portugal

INFRASTRUCTURE Portugal

REAL ESTATE AND CONSTRUCTION Portugal

MILITARY AND STATE DEFENSE Portugal

NATURAL RESOURCES Portugal

SERVICES AND DISTRIBUTION Portugal

TECHNOLOGY AND TELECOMS Portugal

IBERIAN TRANSACTIONS

Spain

Portugal

CORPORATE PROFILESACKNOWLEGEMENTSINDEX OF ENTITIES

11

13

15

127

183

231

237

291

293

16

34

56

80

88

100

116

129

132

149

159

171

173

175

181

232

234

185

189

193

195

197

198

199

208

215

217

220

222

223

224

225

229

CONTENTS

El editor no se hace responsable de las opiniones recogidas, comentarios y manifestaciones vertidas por los autores. La presente obra recoge exclusivamente la opinión de su autor como manifestación de su derecho de libertad de expresión.

Reservados todos los derechos. El contenido de esta publicación no puede ser reproducido, ni en todo ni en parte, ni transmitido, ni registrado por ningún sistema de recuperación de información, en ninguna forma ni por ningún medio, sin el permiso preTvio, por escrito, de Editorial Aranzadi, SA.

TTR - Transactional Track Record y el logotipo TTR son marcas de Zuvi Nova, S.A.

Thomson Reuters y el logotipo de Thomson Reuters son marcas de Thomson Reuters Aranzadi es una marca de Thomson Reuters (Legal) Limited

© 2013 [Thomson Reuters (Legal) Limited / Mercedes García Ordaz] Editorial Aranzadi, SA Camino de Galar, 15 31190 Cizur Menor (Navarra)

Imprime: Rodona Industria Gráfica, SL Polígono Agustinos, Calle A, Nave D-11 31013 - Pamplona

Depósito Legal: NA 1067/2013

ISBN: 978-84-470-4428-3

Printed in Spain. Impreso en España

First edition, May 2013

TRANSACTIONSHIGH-END MARKET (> EUR 500M)

HIGHLIGHTED DEALS

OTHER HIGHLIGHTED DEALS

PRIVATE EQUITY

INVESTMENTS

EXITS

MID-MARKET (> EUR 100M)HIGHLIGHTED DEALS

OTHER HIGHLIGHTED DEALS

PRIVATE EQUITY

INVESTMENTS

EXITS

SMALLER MARKET (< EUR 100M)HIGHLIGHTED DEALS

OTHER HIGHLIGHTED DEALS

PRIVATE EQUITY / VENTURE CAPITAL

INVESTMENTS

EXITS

ENTITIESBANKS AND SAVINGS BANKS

PRIVATE EQUITY / VENTURE CAPITAL

LEGAL ADVISERS

CONSULTANCY FIRMS / FINANCIAL ADVISERS

SECTORS AND SUBSECTORSENERGY AND RENEWABLE ENERGIES

INDUSTRY

INFRASTRUCTURE

REAL ESTATE AND CONSTRUCTION

MILITARY AND STATE DEFENSE

NATURAL RESOURCES

SERVICES AND DISTRIBUTION

TECHNOLOGY AND TELECOMS

IBERIAN TRANSACTIONSSPANISH TARGET

TRANSACTIONSPRIVATIZATIONS

PRIVATIZATIONS IN 2012

OTHER PRIVATIZATIONS IN 2012

HIGH-END MARKET (> EUR 250M) HIGHLIGHTED DEAL

PRIVATE EQUITY

INVESTMENTS

EXITS

MID-MARKET (> EUR 15M)HIGHLIGHTED DEALS

OTHER HIGHLIGHTED DEALS

PRIVATE EQUITY

INVESTMENTS

EXITS

SMALLER MARKET (< EUR 15M)HIGHLIGHTED DEALS

PRIVATE EQUITY / VENTURE CAPITAL

INVESTMENTS

EXITS

ENTITIESBANKS

PRIVATE EQUITY / VENTURE CAPITAL

LEGAL ADVISERS

CONSULTANCY FIRMS / FINANCIAL ADVISERS

SECTORS AND SUBSECTORSENERGY AND RENEWABLE ENERGIES

INDUSTRY

INFRASTRUCTURE

REAL ESTATE AND CONSTRUCTION

MILITARY AND STATE DEFENSE

NATURAL RESOURCES

SERVICES AND DISTRIBUTION

TECHNOLOGY AND TELECOMS

IBERIAN TRANSACTIONS PORTUGUESE TARGET

CONTENTS BY COUNTRY

SPAIN PORTUGAL

185

189

193

195

197

198

199

208

215

217

220

222

223

224

225

229

129

132

149

159

171

173

175

181

56

69

70

70

75

116

124

124

124

34

46

48

48

53

100

112

113

113

114

16

28

30

31

33 88

89

89

89

80

80

232

234

INTRODUCTION

TTR -Transactional Track Record presents the second edition of its M&A HANDBOOK 2013, which organizes and analyses all M&A data, involving the Iberian market, in 2012.The M&A HANDBOOK and its contents have been graphically laid out in a way that enables the reader to quickly access all the necessary details of a specific transaction, as well as the year’s most active industry sectors, companies, financial entities, consultancy firms, financial advisers and legal advisers.

Highlights in the Iberian M&A market in 2012 include:

The Iberian M&A market sector recorded a decrease both in investment volume in number of closed deals, compared to 2011. In fact, the total number of deals decreased by 10% and the investment dropped by approximately 15%.The main obstacles in the M&A sector: the financing conditions, with a limited access to credit, and company’s delicate economic situation. Highlighted M&A sectors: financial, food, consultancy, and technology.Private equity in Spain and Portugal, throughout the year, suffered a 20% decrease, with respect to 2011. The total number of deals also decreased between 5% - 10%. The high-end marked suffered the most, whereas the mid-market remained stable.Private equity funds, venture capital and Business angels showed an increasing activity in the technology-related areas, which represents an increasing investment in start-ups.Cross-border deals were particularly relevant. Highlights include divestments by Spanish groups abroad to balance their financial statements. Also noteworthy were the Spanish companies’ investments in Latin America and some players in Spain. In 2012, the number of deals involving legal and/or financial advisers decreased slightly compared to previous year. Deals involving company’s internal teams increased.

•

•

• •

•

•

•

11TTR - Transactional Track Record - (www.TTRecord.com)

DEFINITIONS

M&A TRANSACTIONS

TTR considers Iberian M&A deals to include any acquisition of shares, both of public and private companies headquartered in Spain or in Portugal, or of any other company worldwide by a Spanish or Portuguese entity.

For the purpose of this Handbook, the acquisition of assets or any other corporate acquisition that does not imply the acquisition of shares is not considered a M&A transaction. The acquisition of shares in a target company which configures a mere stock market transac-tion (namely, through a broker or any type of intermediary) is also not considered to be a M&A transaction.

PRIVATE EQUITY TRANSACTIONS

All investments or divestments carried out by private equity firms and/or funds under management are registered as private equity deals. When the purchase or sale of a specific target company is carried out through one of the private equity firms’/funds’ subsidiaries, the deal will only be considered a private equity deal if the subsidiary is controlled by the referred to private equity/fund.

VENTURE CAPITAL DEALS

Investments carried out by private funds which concentrate their activity on companies in a start up phase, including seed capital, early stage and expansion.

HIGH-END MARKET

Spain: All M&A deals which total deal value is in excess of EUR 500m. Portugal: All M&A deals which total deal value is in excess of EUR 250m.

MID-MARKET

Spain: All M&A deals which total deal value is in excess of EUR 100m. Portugal: All M&A deals which total deal value is in excess of EUR 15m.

SMALLER MARKET

Spain: All M&A deals which total deal value is less than EUR 100m. Portugal: All M&A deals which total deal value is less than EUR 15m.

13TTR - Transactional Track Record - (www.TTRecord.com)

Transactions

Spain

16

34

56

High-end Market (> EUR 500m)Largest deals Additional deals in this segment Private equity / Venture capital Investments Exits

Mid-Market (> EUR 100m)Largest deals Additional deals in this segment Private equity / Venture capital Investments Exits

Smaller Market (< EUR 100m)Largest deals Additional deals in this segment Private equity / Venture capital Investments Exits

1716 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

Largest deals in 2011

Largest deals in 2012

TARGET COUNTRY SUBSECTOR BUYER SELLER AMOUNT (EUR m)

Cono Sur Participaciones Spain Financial and

insurances Enersis Chile Endesa 4.501,74

Bankia (fusión Caja Madrid y Bancaja); Banco Financiero

y de Ahorros

Spain Financial and insurances

Fondo de Reestructuración

Ordenada Bancaria (FROB)

- 4.456

Brisa Portugal Roads and Highways Tagus Holdings AbertisPrivate shareholders 1.404,54

Banco Pastor Spain Financial and insurances Banco Popular - 1.362

China Unicom China Telecoms China United Network Communications Telefónica International 1.154,35

Heathrow Airport Holdings (BAA) UK Transports, Aviation

and Logistics Qatar Holding

Ferrovial; Britannia Airport Partners

GIC (Government of Singapore Investment

Corporation)

1.105,38

Atento Spain Telecoms Bain Capital Telefónica 1.051

Banco Santander Colombia Colombia Financial and

insurances CorpBanca Banco Santander 984,14

Banca Cívica Spain Financial and insurances

CaixaBank (Criteria CaixaCorp) - 977

Abertis Spain Roads and Highways OHL Admirabilia 875,3

TARGET COUNTRY SUBSECTOR BUYER SELLER AMOUNT (EUR m)

Bank Zachodni Poland Financial and insurances Banco Santander Private shareholders

AIB Group 4.293

Garanti Bankasi Turkey Financial and

insurances BBVA General Electric Company Dogus Group 4.200

Cepsa Spain Oil and Gas IPIC Private shareholders;Total 3.966

British AirwaysIberia UK Transports, Aviation

and Logistics - - 3.700

Talecris USAFarmacéutico, Parafarmacia y Cosmética

Grifols Private shareholdersCerberus 2.800

Repsol YPF Spain Oil and Gas Repsol YPF

Citibank España; ING Bank; Natixis; Société

Générale Group; Crédit Agricole; Banco Santander;

Sacyr Vallehermoso;Bankia (merger Caja Madrid y Bancaja)

2.572

Elektro Brazil ElectricIberdrola; Energia

do Brasil EPC - Empresa Paranaense

Ashmore Energy International 1.636

Vidacaixa - Adeslas Seguros

Generales

Spain Financial and insurances

Mutua Madrileña Automovilista

CaixaBank (Criteria CaixaCorp) 1.075

Capio España SpainHealthcare, Hygiene and

Medical AestheticsCVC Capital Partners Capio; Nordic Capital;

Apax Partners 900

Mivisa Spain Industrial Machinery, Metals

Private shareholders; Blackstone; N+1

Private Equity Fund ICVC Capital Partners 900

Source: www.TTRecord.com

Source: www.TTRecord.com

High-end Market

In 2012, the high-end transactional market was slightly less active than in the previous year. The number of deals decreased. In fact, seven deals were closed with values superior to EUR 1.000m, compared to nine in 2011. Furthermore, we registered eight deals with values superior to EUR 500m, while in 2011, thirteen had been closed.

Similar to 2011, most deals in this segment had a cross-border component. Highlights include the divestment conducted by Endesa, a Spain-based electricity multinational, of Cono Sur Participaciones, a company that groups Endesa’s assets and stakes in Latin America, to Enersis (Chile), a company held by Endesa (60,62%). The deal value was USD 5.963m, some EUR 4.501,74m. Furthermore, Telefónica, through Telefónica International, sold a 4,56% stake in China Unicom to China United Network Communications, the group’s controlling company. The deal value was HKD 10.963m, some EUR 1.128,9m. Previously, Telefónica held a 9,6% stake in China Unicom, and with this sale this percentage will decrease to 5,01%.

The most active sector in this segment was the financial and insurance. Banco Financiero y de Ahorros, a merger of seven savings banks headed by Caja Madrid and Bancaja, submitted a conversion request to the Spanish Government for EUR 4.460m in preference shares of FROB (Fondo de Reestructuración Ordenada) a bank restructuring fund, into equity. With this deal, FROB enters, directly, Banco Financiero y de Ahorros’s share capital, and indirectly its subsidiary Bankia (fusión Caja Madrid y Bancaja) with 45% of the capital. As a result, the ministry of Economy recognizes the Government’s control over the bank.

On the other hand, Banco Popular launched a public takeover offer to acquire Banco Pastor, and merge the two banks. The deal value was EUR 1.362m. Banco Popular will pay through new issued shares to all Banco Pastor’s share-holders that participated in the takeover. In fact, Banco Popular offered 1,11 new shares for each share of Banco Pastor, and 30,9 shares for each of Banco Pastor's mandatory convertible bonds.

1918 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

AdvisersIn this deal, Endesa appointed Mediobanca, J.P. Morgan and Celfin Capital as financial

advisers, and used its internal team as legal adviser.

COUNTRY: SpainCono Sur Participaciones

Endesa, a Spain-based electricity multinational, sold Cono Sur Participa- ciones, a company that groups Endesa’s assets and stakes in Latin America, to Enersis (Chile), held by Endesa (60,62%). The deal value was USD 5.963m, approximately EUR 4.501,74m.

This transaction was part of a capital increase conducted by Enersis (Chile) for USD 8.020m. With this deal, Endesa aims to improve its shareholding structure and change Enersis (Chile) into a company that operates in all Latin American countries.

This year, Endesa also sold Endesa Ireland to UK-based Scottish & Southern Energy (SSE). The deal value was EUR 286m.

Founded in 1944, Endesa is a Spain-based company that operates in the electric and gas sector. Since 2009, and after a lengthy public offering, Enel, an Italy-based power company holds a 92% stake in Endesa’s share capital.

Endesa is the largest utility company in Spain and a leading multinational energy company in Latin America. The company also operates in Portugal and is present in Morocco, with a thermal plant in Tahaddart. Endesa began its expansion as a producer and carrier of electricity in Latin America during 1990’s, focusing mainly in Argentina, Chile and Venezuela. Later the utility company entered Brazil, Colombia and Peru, where it is one of the major electricity carriers in number of customers.

Endesa has in excess of 25 million customers worldwide, with an installed capacity of 45.095 MW and a production of 138.714 GWh, by 31 December 2011. Its net profits were EUR 2.12m, this same year.

Enersis is one of the largest private electricity multinationals in Latin America. Currently, the company has direct and indirect control over the generation, transmission and distribution of electric energy and related areas. Enersis operates in Argentina, Brazil, Chile, Colombia and Peru. Its installed capac-ity exceeds 15.171 MW, and through its distributors the company supplies electricity to some 14,2 million customers. Source: www.TTRecord.com

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: Cono Sur ParticipacionesDESCRIPTION: Company that groups Endesa’s assets and stakes in Latin America.

SELLER %

Endesa 100

Total sold 100

BUYER %

Enersis Chile 100

Total acquired 100

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues - -

EBITDA 8,60 x 8,60 x

DEAL VALUE Payment

EUR 4.501,74m (Cash) EUR 4.501,74m

TARGET (EUR million)

Revenues - 2011 -

EBITDA - 2011 535,59

Enterprise value 4.501,74

Equity value 4.501,74

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Endesa MediobancaJ.P. Morgan

Celfin CapitalIn-house -

2120 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

AdvisersIn this deal, Fondo de Reestructuración Ordenada Bancaria (FROB) appointed law firm

Garrigues as legal adviser.

COUNTRY: Spain

COUNTRY: SpainBanco Financiero y de Ahorros

Bankia (merger Caja Madrid y Bancaja)

Banco Financiero y de Ahorros, a merger of seven savings banks headed by Caja Madrid and Bancaja, submitted a conversion request to the Spanish Government for EUR 4.460m in preference shares of FROB (Fondo de Reestructuración Ordenada), a bank restructuring fund, into equity. With this deal, FROB enters, directly, Banco Financiero y de Ahorros’s share capital, and indirectly its subsidiary Bankia (merger Caja Madrid and Bancaja) with 45% of the capital.

Bankia (merger of Caja Madrid and Bancaja) is the largest bank in Spain, with a total of EUR 272.000m in assets and EUR 12.000m inequity. Following this transaction, Banco Finaciero y de Ahorros stated its financial needs were of EUR 19.000m. Up until now , the bank only received EUR 4.500m from banking bailout, in addition to EUR 4.665m received, in 2010, from Fondo de Reestructuración Ordenada (FROB), a banking bailout and recon-struction program.

Bankia (merger of Caja Madrid and Bancaja) is the result of restructur-ing process savings banks’ system promoted by Banco de España through a financial system called Sistema Institucional de Protección (SIP), a protection system for institutions. Banco Financiero y de Ahorros was created in 2010, jointly by Caja Madrid and Bancaja. Later, a few other entities merged: La Caja de Canarias, Caixa Laietana, Caja Rioja, Caja Ávila and Caja Segovia. This transaction, known in financial terms as ‘cold merger’, is controlled by Caja Madrid, a bank that manages EUR 340.000m in assets. In addition, Caja Madrid will receive support from FROB of approximately EUR 4.465m.

In March 2011, the board of directors of the seven savings banks that con-stitute Banco Financiero y de Ahorros, approved to transfer all their assets and liabilities to Bankia (merger of Caja Madrid and Bancaja), keeping the name, its social work, and a number of buildings considered historical. The entity carried out an initial public offering, on 20 July 2011. The price was of EUR 3,75 per share, totaling EUR 3.092m.

Source: www.TTRecord.com

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: Banco Financiero y de Ahorros; Bankia (merger Caja Madrid and Bancaja)DESCRIPTION: Financial institution

SELLER %

- -

Total sold -

BUYER %

Fondo de Reestructuración Ordenada Bancaria (FROB) 45

Total acquired 45

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues - -

EBITDA - -

DEAL VALUE Payment

EUR 4.456m (Cash) EUR 4.456m

TARGET (EUR million)

Revenues - 2011 770,65

EBITDA - 2011 -297,26

Enterprise value 9.902,22

Equity value 9.902,22

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED

FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Fondo de Reestructuración Ordenada Bancaria (FROB) - Garrigues -

2322 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

AdvisersIn this deal, Arcus Infrastructure Partners hired law firms Campos Ferreira, Sá Carneiro

Advogados and Linklaters as legal advisers. While José de Mello Holding hired Vieira de

Almeida Advogados as legal adviser; and Brisa hired law firm Sérvulo Advogados.

Tagus concluded a public takeover offer to acquire Brisa’s shares, which it did not yet hold, offering EUR 2,76 per share. Tagus is held by Portuguese group José de Mello Holding (55%) and UK-based Arcus Infrastructure Partners (45%), which jointly hold a 49,57% stake in Brisa.

With this offer, Tagus acquired a 35,23% stake in Brisa, a highway conces-sions company. In fact, Abertis sold 15,02% of the capital, and several private shareholders sold the remaining 20,21%, equivalent to 508,89 million shares. As a result Tagus will hold a 84,8% stake in Brisa’s share capital. The total deal value is EUR 1.404,54m.

Brisa is the largest highway concessions management company in Portugal. The company was founded in 1972 and also operates in other countries, such as United States and The Netherlands. As a result of this transaction, Brisa will leave the main Portuguese Stock Exchange index PSI-20.

At the beginning, Abertis voted against this takeover, but changed its decision later. Brisa’s market value at the time of this transaction was some EUR 1.500m, relatively far from EUR 6.300m, as of December 2007. Abertis, a Spain-based concessionary, estimates that the impact on cash flow of this deal will be EUR 312m, while the impact on its income statement will be EUR 97m.

COUNTRY: PortugalBrisa

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Tagus Holdings Caixa BI

Espírito Santo Investment - BESiMillennium IB

- -

Arcus Infrastructure Partners -

Campos Ferreira, Sá Carneiro Advogados;

Linklaters -

José de Mello Holding - Vieira de Almeida

Advogados -

Brisa - Sérvulo Advogados -

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues - -

EBITDA - -

DEAL VALUE Payment

EUR 1.404,54m EUR 1.404,54m

TARGET (EUR million)

Revenues - 2011 -

EBITDA - 2011 -

Enterprise value 3.986,77

Equity value 3.986,77

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIES TARGET: Brisa

DESCRIPTION: Highway concessions management company

SELLER %

Private shareholders 20,21

Abertis 15,02

Total sold 35,23

BUYER %

Tagus Holdings (José de Mello Holding;

Arcus Infrastructure Partners)35,23

Total acquired 35,23

FINANCING

FINANCING BANKS

AMOUNT(EURm)

PERCENTAGE (%)

FINANCIAL ADVISERS LEGAL ADVISERS

Millennium BCP - - - Morais Leitão, Galvão Teles, Soares da Silva Advogados

CGD Caixa Geral de Depósitos - - - Morais Leitão, Galvão Teles,

Soares da Silva Advogados

Banco Espirito Santo - BES - - - Morais Leitão, Galvão Teles,

Soares da Silva Advogados

Source: www.TTRecord.com

2524 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

AdvisersIn this deal, Banco Popular hired Morgan Stanley as financial adviser and law firm

Cuatrecasas, Gonçalves Pereira as legal adviser. While Goldman Sachs was Banco Pastor’s

financial adviser and law firm Pérez-Llorca was its legal adviser.

COUNTRY: SpainBanco Pastor

Banco Popular launched a takeover offer to acquire Banco Pastor and merge the two entities. The deal value was EUR 1.362m, paid through exchange of new issued shares to all Banco Pastor’s shareholders who participated. In fact, Banco Popular offered 1,11 new shares for each share of Banco Pastor, and 30.9 shares for each of Banco Pastor's mandatory convertible bonds.

This deal was announced at the end of 2011, although it was only closed on 18 January 2012, once it was approved by the shareholders’ boards of both companies and by regulatory authorities.

Banco Popular uses this name since 1947, although it was founded in 1926 under the denomination Banco Popular de los Previsores del Porvenir. Currently, the bank is constituted by Targobank (Banco Popular Español and French group Crédit Mutuel), Banco Popular Portugal, Bancopopular-e (online bank), Popular Banca Privada (Banco Popular Español and Dexia), and TotalBank (Miami). In addition the bank has offices in Belgium, Chile, Germany, Hong-Kong, Colombia, Morocco, The Netherlands, Switzerland, Venezuela, Turkey and United Kingdom.

Source: www.TTRecord.comSource: www.TTRecord.com

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: Banco Pastor DESCRIPTION: Financial institution

SELLER %

- -

Total sold -

BUYER %

Banco Popular 100

Total acquired 100

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues 1,31 x 1,31 x

EBITDA - -

DEAL VALUE Payment

EUR 1.362m (Cash) EUR 1.362m

TARGET (EUR million)

Revenues - 2011 1.039,72

EBITDA - 2011 -

Enterprise value 1.362

Equity value 1.362

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED

FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Banco Popular Morgan Stanley Cuatrecasas, Gonçalves Pereira -

Banco Pastor Goldman Sachs Pérez-Llorca -

2726 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

AdvisersIn this deal, China United Network Communications hired Freshfields as legal adviser,

while Telefónica International hired Clifford Chance as legal adviser.

COUNTRY: ChinaChina Unicom

Telefónica, through Telefónica International, sold a 4,56% stake in China Unicom to China United Network Communications, the group’s controlling company. The deal value was HDK 10.963m. Previously, Telefónica held a 9,6% stake in China Unicom, and with this deal this percentage will drop to 5,01%.

The deal does not include management changes in China Unicom. César Alierta will remain a member and China Unicom’s president, Chang Xiaobing will remain a member of Telefónica’s board of directors.

In 2010, Telefónica and China Unicom signed an agreement through which the Chinese company acquired a 0,9% stake in Telefónica, and Telefónica in turn increased its stake from 5,4% to 8% in China Unicom. This transaction meant a disbursement of EUR 700m by each company.

In 2011, China Unicom and Telefónica strengthened the agreement signed in 2009. In fact, the new agreement was signed on 23 January 2011 and includes new cross investments between both companies valued at USD 500m (some EUR 375m). Once this deal is finalized, Telefónica will hold a 9,6% stake in China Unicom, while the Chinese company will hold a 1,37% stake in Telefónica.

Source: www.TTRecord.com

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: China Unicom DESCRIPTION: Telecommunications operator

SELLER %

Telefónica International 4,56

Total sold 4,56

BUYER %

China United Network Communications 4,56

Total acquired 4,56

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues 0,95 x 0,95 x

EBITDA 3,12 x 3,12 x

DEAL VALUE Payment

EUR 1.154,35m (Cash) EUR 1.154,35m

TARGET (EUR million)

Revenues - 2011 25.636,98

EBITDA - 2011 7.771,98

Enterprise value 25.314,75

Equity value 25.314,75

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED

FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

China United Network Communications - Freshfields -

Telefónica International - Clifford Chance -

2928 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

In 2012, we registered some twenty deals in Spain in this market segment, which includes deals superior to EUR 500m. This means a decrease in number of deals. Thirty deals were registered in 2011.

The five largest deals this year were detailed above, although several others were also relevant. These include various divestments by Spanish multinationals such as Ferrovial and Banco Santander.

In 2012, Ferrovial sold a 10,62% stake in FGP Topco, controlling company of Heathrow Airport Holdings (BAA), to Qatar Holding, a Arab Emirates-based investment fund. The deal value was EUR 607m. Furthermore, and part of this trans-action, Qatar Holding acquired a 9,38% stake in Heathrow Airport Holdings (BAA), held by Britannia Airport Partners (5,63%) and by GIC (3,75%). With this deal, Qatar Holding attains a 20% stake in Heathrow Airport Holdings (BAA). The deal value was EUR 1.144m.

With this deal, Ferrovial reduces its stake in Heathrow Airport Holdings (BAA) to 39,37%. This divestment is part of Ferrovial’s assets valorization strategy and investment diversification. Ferrovial will use these resources to improve its liquidity and gain flexibility for new investments in infrastructure projects and services

In this transaction, Britannia Airport Partners was advised by Fasken Martineau Dumoulin, while Ferrovial received legal advice from Freshfields.

Banco Santander also divested abroad. The bank sold Banco Santander Colombia to CorpBanca, a Chile-based bank. The deal value was USD 1.229m (approx. EUR 910m). With this deal, Banco Santander will receive profits valued at EUR 615m, to strengthen its financial statements.

In this deal, CorpBanca used its internal team as financial and legal advisers, as well as Posse, Herrera & Ruiz Abogados for legal advice. On the other hand, Banco Santander hired Uría Menéndez and Colombia-based Prieto & Carrizosa.

Highlights, in 2012, also include other financial entities. Caixabank (Criteria CaixaCorp) and Banca Cívica, a bank created through a merger of Caja Navarra, Cajasol, Caja Burgos and Caja Canarias, approved the terms for their merger. The deal value was EUR 977m. With this merger, a new banking group was created with EUR 342.618m under management.

In this deal, CaixaBank (Criteria CaixaCorp) hired AZ Capital as financial adviser.

As we can see, most of the high-end market deals have a cross-border component. Another relevant deal, in 2012, was the acquisition by OHL of an additional stake in Abertis. In fact, construction company ACS sold a 10,04% stake in Abertis to OHL and to Abertis itself. The deal value was EUR 875,3m. With

Other highlighted deals

this transaction OHL attains a 15% of the capital. On the other hand Abertis acquired a 5,3% of its own shares, to subsequently sell to OHL. In exchange for this 15% stake, OHL integrates in Abertis, OHL’s highway concessions in Brazil and Chile. This transaction was executed through a swap of Participes en Brasil, an investment vehicle owner of a 60% stake in OHL Brasil, in exchange for a 10% stake in Abertis. In addition, Abertis will assume EUR 504,1m of liabilities from OHL Concesiones’s Brazilian business Partícipes en Brasil, plus a payment of EUR 10,7m. After this deal, OHL will hold a 15% stake in Abertis. The swap value to acquire its concession assets in Chile was EUR 204m, which will be partially financed by local banks.

In this deal, Abertis hired Citigroup as financial advisers, and Freshfields as legal advisers, while ACS hired Mediobanca as financial advisers. On the other hand, OHL appointed Linklaters and Lefosse Advogados as legal advisers. In addition, Deloitte was appointed to conduct the due diligence.

Furthermore, Procter & Gamble acquired a 50% stake in Arbora & Ausonia. With this deal, Agrolimen, a group held by the Carulla family, exits the com-pany’s share capital, and Procter & Gamble attained 100%. The deal value was EUR 814m. Agrolimen’s divestment is part of its efforts to focus on its three core businesses: food group Gallina Blanca Star, catering group The Eat Out Group, and animal feed manufacturer Affinity Pet Care.

In this deal, Procter & Gamble hired Uría Menéndez and Garrigues as legal advisers. Agrolimen received legal advice from Cuatrecasas, Gonçalves Pereira. In addition, Inforpress was the communications consultant.

3130 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

Source: www.TTRecord.com

TARGET SUBSECTOR BUYER SELLER AMOUNT (EUR m)

Atento Telecoms Bain Capital Telefónica 1.051

Kemble Water Water and Sanitation

China Investment Corporation (CIC)

Santander Private EquityFinpro 600

TARGET SUBSECTOR BUYER SELLER AMOUNT (EUR m)

CapioHealthcare, Hygiene

and Medical Aesthetics

CVC Capital PartnersCapio

Nordic CapitalApax Partners

900

MivisaIndustrial Production,

Industrial Machinery, Metals

Private shareholdersN+1 Private Equity Fund I

BlackstoneCVC Capital Partners 900

Swissport Transports, Aviation and Logistics PAI Partners Ferrovial 880

Central Termosolar Andasol I;

Central Termosolar Andasol II

Solar Antin Infrastructure Partners RREEF Infrastructure Grupo Cobra 830

Santander Consumer USA

Financial and insurances

Dundon DFSSponsor Auto Finance Holdings Santander Consumer 828,35

Parque Eólico Tesosanto;

Parque Eólico Sierra de Carbas;

La Caldera Energía Burgos;Parque Eólico

La Boga;Parque Eólico

Marmellar

Wind Bridgepoint ACS 636,30

Largest private equity investments in 2011

Largest private equity investments in 2012

Source: www.TTRecord.com

Private Equity

In 2012, we registered two private equity deals in the Spanish high-end market, which includes deals superior to EUR 500m. Venture capital fund Bain Capital acquired Atento, held by Telefónica, for EUR 1.051m. In addition, Santander Private Equity sold, jointly with Portugal-based Finpro, a 8,68% stake in Kemble Water to China Investment Corporation. The deal value was some EUR 600m.

These values are clearly inferior to those registered last year. In 2011, six deals were recorded totaling EUR 4.974,65m. The deal volume in 2012 is thus similar to 2010, where there was only one deal with value superior to EUR 500m.

Atento

Telefónica closed the sale of Atento to a Group of companies held by venture capital fund Bain Capital. The deal value was EUR 1.051m. With this deal Bain Capital enters the Spanish market. Payment includes a deferred installment of EUR 110m subject to the company’s future performance, and bank loan for another EUR 110m. This sale was initiated in March 2012 and received three offers from venture capital funds Bain Capital, Apollo Capital and Permira. None of these materialized, and Telefónica cancelled the process, in September 2012. In October 2012, Telefónica reopened the sale.

Atento is based in Madrid with offices in the United States, Colombia, Brasil, Uruguay, Argentina, Mexico, and others in Latin America, and Morocco. The company registered, in 2011, a turnover of EUR 1.082m (+8.4%) and EBITDA of EUR 101m.

With this divestment, Telefónica accelerates its divestment strategy of non-strategic assets, to cope with its debt of EUR 58.000m.

AdvisersIn this deal, Telefónica hired HSBC Bank and Morgan Stanley as financial advisers, and

Ramón y Cajal and KPMG Abogados as legal advisers. On the other hand, Bain Capital

appointed Goldman Sachs and Santander Global Banking & Markets as financial advisers,

and law firms Uría Menéndez, Kirkland & Ellis, Marval O´Farrel & Mairal, Souza, Cescon,

Barrieu & Flesch Advogados, Carey & Allende, Brigard & Urrutia Abogados, and González

Calvillo Abogados as legal advisers. Atento received legal advice from law firms Houthoff

Buruma, Posse, Herrera & Ruiz Abogados, Miranda & Amado Abogados, Larraín Rencoret

Lackington & Urzúa Abogados, Tauil & Chequer Advogados, Consortium Centro América

Abogados, Nader Hayaux & Goebel Abogados, Cabanellas, Etchebarne, and Kelly &

Dell´oro Maini Abogados. Finally, Deloitte was appointed to carry out the due diligence.

3332 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

HIG

H-EN

D M

ARKET >

EUR 500m

HIG

H-E

ND

MA

RKET

> E

UR

500m

AdvisersIn this deal, Santander Private Equity hired Clifford Chance as legal adviser.

Kemble Water

Spain-based fund Santander Private Equity and Portugal-based Finpro sold, jointly, a 8,68% stake in Kemble Water to China Investment Corporation. The deal value was some EUR 600m. This was the first investment by the Chinese group in Europe. This deal took place after a visit from the British authorities to China with the objective of showing the country’s strengths. Santander Private Equity entered Thames Water’s share capital in December 2006, with a EUR 38,9m investment. The deal was executed jointly with a consortium headed by Australia-based Macquarie Group.

TARGET SUBSECTOR BUYER SELLER AMOUNT (EUR m)

No private equity investments were registered in this market segment in 2012

TARGET SUBSECTOR BUYER SELLER AMOUNT (EUR m)

CapioHealthcare, Hygiene

and Medical Aesthetics

CVC Capital PartnersCapio

Nordic CapitalApax Partners

900

MivisaIndustrial Production,

Industrial Machinery, Metals

Private shareholders;N+1 Private Equity Fund I

BlackstoneCVC Capital Partners 900

Swissport Transports, Aviation and Logistics PAI Partners Ferrovial 880

BioVex Biotechnology Amgen

MVM Life Science Partners;

Crédit Agricole Private Equity;

Morningside Venture;Ysios BioFund I

730

Jimmy Choo Luxury goods and Services Labelux

Private shareholders;Gala Capital;Towerbrook;

Capital Partners

600

Largest private equity exits in 2011

Source: www.TTRecord.com

Source: www.TTRecord.com

Largest private equity exits in 2012

3534 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

Largest deals in 2011

Largest deals in 2012

TARGET COUNTRY SUBSECTOR BUYER SELLER AMOUNT (EUR m)

Stahlwerk ThüringenGallardo Sections Germany

Industrial Production, Industrial Machinery,

MetalsCSN Steel Grupo Alfonso Gallardo 482,5

Repsol Butano Chile Chile Oil and Gas Larraín VialPrivate shareholders

Repsol (former Repsol YPF) 438,42

Groupama Seguros (España) Spain Financial and

insurances

InocsaGrupo Catalana

OccidenteGroupama 404,5

Eutelsat Communications France Telecoms China Investment

Corporation (CIC) Abertis telecom 385,2

BBVA Securities of Puerto Rico;

BBVA PR HoldingPuerto Rico Financial and

insurances Oriental Financial Group BBVA 379,42

USP Hospitales SpainHealthcare, Hygiene

and Medical Aesthetics

Doughty Hanson

Barclays Bank;Private shareholders

RBS - The Royal Bank of Scotland;

355

Gasmedi SpainHealthcare, Hygiene

and Medical Aesthetics

Air Liquide MercapitalPrivate shareholders 330

FGP Topco UK Financial and insurances

Stable Investment Corporation Ferrovial 319,3

Endesa Ireland Ireland Electric Scottish Southern Energy (SSE) Endesa 286

Esmalglass SpainGlass, Ceramic, Paper, Plastics,

Wood and TimberInvestcorp Private shareholders

3i (España) 280

TARGET COUNTRY SUBSECTOR BUYER SELLER AMOUNT (EUR m)

Opodo Spain Internet PermiraAXA Private Equity Amadeus 500

Telvent Spain Technology Schneider Electric Abengoa 421

Jantus Spain Wind CPFL Comercialização Brasil Private shareholders 420

MBNA España Spain Financial and insurances Apollo Capital Bank of America

Merrill Lynch 400

Guascor Spain Solar Dresser-Rand

Axis Participaciones Empresariales; Diana Capital;

Private shareholders

375

Compañía Logística de

Hidrocarburos (CLH)

Spain Oil and Gas AXA Private Equity Disa 360

Bond Air Services UK Transports, Aviation

and Logistics Inaer Private shareholders 340

Telecable de Asturias Spain Telecoms Carlyle

Prensa Ibérica; Liberbank (Merger Cajastur, Caja de Extremadura and

Caja Cantabria)

340

BAA UK Airports Alinda Capital Partners Ferrovial 325

Saba Infraestructuras Spain Parkings

ProA Capital; Torreal; CaixaBank (Criteria

CaixaCorp)

Abertis ; CVC Capital Partners 311,5

Source: www.TTRecord.com

Source: www.TTRecord.com

Mid-market

In 2012, the Spanish mid-market transactional activity, which includes deals ranging between EUR 100m and EUR 500m, had a slight decrease compared to previous year, in as far as number of deals as well and also volume invested. In fact, forty deals were registered, 15 of these with values superior to EUR 250m.

Cross-border deals were significant in the mid-market, mainly due to Spanish companies’ divestments of their subsidiaries abroad. Grupo Alfonso Gallardo sold German companies Gallardo Sections y Stahlwerk Thüringen. Repsol sold Repsol Butano Chile, and Banesto sold Atuka to US-based venture capital fund Centerbridge Partners.

On the other hand, some Spanish companies showed interest in continuing their growth plans abroad, mainly towards emerging markets and Latin American countries. Highlights include the acquisition by Enagás of a 40% stake in Chile-based GNL Quintero, held by British Gas Group.

Spain is facing a difficult situation due to the economic crisis, which is influ-encing significantly the M&A market over the last few years. Nevertheless, this is also generating opportunities for international groups that chose to invest in Spain aiming to expand their businesses, due to the know-how and experience of Spanish teams. Highlights include the acquisition made by Air Liquide of Gasmedi, a Spain-based company that offers home respiratory therapies, held by Mercapital (75%) and by the Fierro family (25%). The deal value was EUR 330m. Furthermore, France-based group Elior acquired a 50% stake in Spain-based Áereas Iberoamericana and its controlling company Áreas, held by Emesa. With this deal Elior attained 100% of the capital. The deal value was EUR 150m.

Also noteworthy was the acquisition of ZIV Aplicaciones y Tecnología by India-based Crompton Greaves, through CG International. The Spanish company was held by its management teams (62,75%) and Dinamia Capital Privado, a company managed by N+1 Capital Privado (37,25%). The deal value was EUR 150m. From this amount, Dinamia will receive EUR 40,7m, which corresponds to 3,5 times the initial investment cost made in 2007.

3736 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

COUNTRY: Germany

COUNTRY: Germany

AdvisersIn this deal, Grupo Alfonso Gallardo hired BBVA Corporate Finance and Mediobanca as

financial advisers and Cuatrecasas, Gonçalves Pereira as legal adviser. CSN Steel received

financial advice from Santander Global Banking & Markets and legal advice from Uría

Menéndez. Ernst & Young carried out the due diligence.

Stahlwerk Thüringen

Gallardo Sections

Brazilian company CSN, through its subsidiary CSN Steel, acquired German companies Gallardo Sections and Stahlwerk Thüringen. The deal value was EUR 482,5m.

With this divestment, Gupo Alfonso Gallardo strengthens its financial capacity, taking into account the debt reduction of some EUR 4885m. In addition the group will close negotiations with its creditors and continue to develop future projects.

CSN Steel received an external loan, for an undisclosed amount, from BBVA, Banco Santander, Banesto, Bankia (merger of Caja Madrid and Bancaja), Banco Popular, Banco Caixa Geral Brasil, Caixa BI and CaixaBank (Criteria CaixaCorp).

Grupo Alfonso Gallardo will maintain a strong presence in the steel sector, with its factories: Siderúrgica Balboa, Alfonso Gallardo, Ferromallas, Galvacolor (Jerez de los Caballeros, Badajoz); Corrugados Getafe y Ferralca (Madrid); Corrugados Azpeitia y Corrugados Lasao (Guipúzcoa). The group also maintains its steel distributors Eusebio Calvo and Marceliano Martín with warehouses throughout Spain; in the cement sector, Cementos Balboa (Alconera, Badajoz); in the paper sector, Papresa (Guipúzcoa); as well as the sectors of media, and renewable energies.

In September 2011, Grupo Alfonso Gallardo agreed with Brazil-based CSN the sale of Cementos Balboa, Corrugados Azpeitia and Corrugados Lasao, and Germany-based Gallardo Sections and Stahlwerk Thüringen. Initially, this agreement was of EUR 543m, but the transaction did not materialize. A few months later the Spanish and Brazilian groups reached a new agreement in which the three Spanish plants were not included.

FINANCING

FINANCING BANKS AMOUNT(EURm)

(%) FINANCIAL ADVISERS LEGAL ADVISERS

BBVA - - - Clifford Chance

Banco Santander - - - Clifford Chance

Banesto - - - Clifford Chance

Bankia (fusión Caja Madrid y Bancaja) - - - Clifford Chance

Banco Popular - - - Clifford Chance

Banco Caixa Geral Brasil - - - Clifford Chance

Caixa BI - - - Clifford Chance

CaixaBank (Criteria CaixaCorp) - - - Clifford Chance

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Grupo Alfonso Gallardo

BBVA Corporate FinanceMediobanca

Cuatrecasas, Gonçalves Pereira -

CSN Steel Santander Global Banking & Markets España Uría Menéndez -

Stahlwerk Thüringen - - Ernst & Young (España)

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues - -

EBITDA - -

DEAL VALUE Payment

EUR 482,50m (Aprox.) (Cash) EUR 482,50m (Aprox.)

TARGET (EUR million)

Revenues - 2011 -

EBITDA - 2011 -

Enterprise value -

Equity value -

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: Stahlwerk Thüringen / Gallardo SectionsDESCRIPTION: Plant for the manufacture of steel / Steel manufacturing company

SELLER %

Grupo Alfonso Gallardo 100

Total sold 100

BUYER %

CSN Steel (CSN) 100

Total acquired 100

Source: www.TTRecord.com

3938 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

COUNTRY: Chile

AdvisersIn this deal, Larraín Vial received legal advice from its internal team, and hired Claro y

Cia. Abogados as legal adviser. Repsol appointed Goldman Sachs as financial adviser,

and Prieto y Cía Abogados as legal adviser. On the other hand, Empresas Lipigas hired

Philippi, Yrarrázaval, Pulido & Brunner as legal adviser.

Repsol Butano Chile

Repsol (former Repsol YPF), a Spain-based oil company, sold Repsol Butano Chile to a group of Chilean investors headed by Larraín Vial, a brokerage company, and Empresas Lipigas. The deal value was USD 540m. With this deal, Repsol continues its divestment strategy of non-strategic assets, and will receive a profit valued at USD 170m. In addition, Repsol will reduce its debt up to USD 317m. Repsol’s strategic plan for 2012-2016, estimates divestments of EUR 4.500m. Repsol has already reached EUR 1.850m, which includes Repsol Butano Chile’s sale.

The strategic plan includes the sale of Repsol Francia GLP to Totalgaz, a subsid-iary of French oil group Total. The deal value may be EUR 14,5m, approximately.

By mid-2012, Repsol (former Repsol YPF) faced a complicated situation, when the Argentinean Republic decided to expropriate a 51% stake in oil com-pany YPF, after declaring it was of public interest. The nationalized percentage involved most of Repsol’s stake in YPF. With this transaction, the Argentinean Government retained 51% of the capital, and the remaining 49% was transferred to ten hydrocarbon-producing provinces. As a result, the Argentinean Government will hold 26,01% of the capital and governors will hold 24,99%. Argentinean group Petersen, held by the Eskenazi family, will retain a 25% stake in YPF, while Repsol reduces its stake to 6,43% (previously held 57,43%).

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Larraín Vial In-House Claro y Cía. Abogados -

Repsol (extinguida Repsol YPF) Goldman Sachs Prieto y Cía Abogados -

Empresas Lipigas - Philippi, Yrarrázaval, Pulido & Brunner -

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues - -

EBITDA - -

DEAL VALUE Payment

EUR 438,42m (Cash) EUR 438,42m

TARGET (EUR million)

Revenues - 2011 -

EBITDA - 2011 -

Enterprise value 438,42

Equity value 438,42

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: Repsol Butano ChileDESCRIPTION: Butane gas exploration and production company

SELLER %

Repsol (extinguida Repsol YPF) 100

Total sold 100

BUYER %

Larraín Vial -

Private shareholders -

Empresas Lipigas -

Total acquired 100

Source: www.TTRecord.com

4140 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

COUNTRY: Spain

AdvisersIn this deal, Groupama hired Morgan Stanley as financial adviser and Garrigues as legal

adviser. On the other hand, Grupo Catala Occidente appointed BNP Paribas as financial

adviser and law firm Cuatrecasas, Gonçalves Pereira as legal adviser.

Groupama Seguros (España)

Catalana Occidente acquired Groupama Seguros (España) held by France-based Groupama, for EUR 404,5m. With this deal, Grupo Catalana Occidente acquired a 49% stake in Groupama Seguros (España) and Inocsa (which holds a 56,71% stake in Grupo Catalana Occidente) acquired the remaining 51% of the capital.

Furthermore, Grupo Catalana Occidente obtained an option to acquire shares held by Inocsa three years after this transaction. Groupama Seguros (España) has a staff of 1.000 employees, and in 2011, it registered profits of EUR 33m, 16% more than in 2010. The company’s turnover was EUR 940m, with a market share of 1,51%. The largest insurance line is the automobile with revenues of EUR 342m, followed by life with EUR 143m, and the pension fund with EUR 11m.

In 2012, Catalana Occidente also acquired a 6,48% stake in Atradius, a The Netherlands-based credit insurance company, held by Inocsa, for EUR 99,88m. With this deal, Catalana Occidente exercised its option to acquire Inocsa’s stake in Atradius, which was agreed in 2010 when the company acquired a 26,66% stake of the capital. As a result, the Catalan-based insurance company attained a 33,14% stake in Atradius’ share capital.

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Groupama Morgan Stanley Garrigues -

Grupo Catalana Occidente BNP Paribas Cuatrecasas, Gonçalves

Pereira -

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues 0,43 x 0,43 x

EBITDA - -

DEAL VALUE Payment

EUR 404,5m (Cash) EUR 404,5m

TARGET (EUR million)

Revenues - 2011 940

EBITDA - 2011 -

Enterprise value 404,5

Equity value 404,5

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: Groupama Seguros (España)DESCRIPTION: Insurance company

SELLER %

Groupama 100

Total sold 100

BUYER %

Grupo Catalana Occidente 51

Inocsa 49

Total acquired 100

Source: www.TTRecord.com

4342 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

COUNTRY: France

AdvisersIn this deal, Abertis telecom hired Linklaters as legal adviser.

Eutelsat Communications

Abertis telecom, held by Abertis Infraestructuras, sold a 7% stake in France-based Eutelsat Communications, to fund China Investment Corporation (CIC). The deal value was EUR 385,2m.

Eutelsat Communications, registered a turnover of EUR 1.222,2m, this year ending on 30 June, which represents a 4,6% increase, with EBITDA of EUR 957,2m. It also generated a profit of EUR 237m, which represents an IRR of 13%. This transaction occurred after Abertis’ acquisition of a 16% stake in Eutelsat Communications, in a private placement offering to qualified investors. Abertis retaied a 8,53% stake in Eutelsat Communications.

In compliance with the terms agreed by Abertis in this recent placement, CIC agreed not to dispose of the acquired shares (“lock-up”) during the period that remains from the initial 6 months agreement.

With this sale, Abertis continues its assets reorganization process, and focuses on those projects in which it can take an industry leadership role and a greater financial consolidation.

On the other hand, on 28 December 2012, after receiving an approval from the Spanish Government, Abertis acquired through its subsidiary Abertis telecom, a 7,2% stake in Hispasat, held by Telefónica de Contenidos. The deal value was EUR 68m.

The agreement terms were modified after Hispasat’s second shareholder, Eutelsat Communications, exercised its option to acquire the stake Telefónica intended to sell Abertis. Both companies had announced, on 21 February 2012, an agreement over a 13,23% stake in Hispasat, for EUR 124m. Finally Abertis acquired a 7,2% of the capital and Eutelsat Communications acquired the remaining 6,03%.

With this deal, Abertis becomes Hispasat’s major shareholder; its stake increases from 33,37% to 40,6%.

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Abertis telecom - Linklaters -

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues 4,50 x 4,50 x

EBITDA 5,75 x 5,75 x

DEAL VALUE Payment

EUR 385,2m (Cash) EUR 385,2m

TARGET (EUR million)

Revenues - 2011 1.222,2

EBITDA - 2011 957,2

Enterprise value 5.502,8

Equity value 5.502,8

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: Eutelsat CommunicationsDESCRIPTION: Company that develops and operates a satellite-based telecommunications

SELLER %

Abertis telecom 7

Total sold 7

BUYER %

China Investment Corporation (CIC) 7

Total acquired 7

Source: www.TTRecord.com

4544 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

COUNTRY: Puerto Rico

COUNTRY: Puerto Rico

AdvisersIn this deal, Oriental Finacial Group hired Jefferies Internaltional as financial adviser, and

Cleary Gottlieb Steen & Hamilton and McConnel Valdés as legal advisers. On the other

hand, BBVA appointed BBVA Corporate Finance as financial adviser.

BBVA PR Holding

BBVA Securities of Puerto Rico

BBVA is one of the Spanish financial entities that chose to divest to restructure its business and cope with the financial crisis in Spain. The plan was to sell some of its assets in Latin America and focus on international expansion in the United States. BBVA’s plan for 2013, is to sell several pension funds in Latin America, possibly Colombia and Peru.

In 2012, BBVA sold BBVA PR Holding and BBVA Securities of Puerto Rico, its subsidiaries in Puerto Rico, to local financial institution Oriental Financial Group. The deal value was USD 500m, representing a price-earnings ratio of 14.7 times.

Thus far, BBVA’s activity in Puerto Rico was ranked as the seventh, out of eight financial entities in the country. The bank has 37 offices and a staff of 950 employees. BBVA PR Holding and BBVA Securities of Puerto Rico’s assets, on 31 March, were USD 5.200m, with deposits of USD 3.300m, and a market share of 5,9%, on 30 June 2011.

Oriental Financial Group offers financial services in Puerto Rico and Florida through four subsidiaries: Oriental Bank and Trust, Oriental Financial Services Corp, Oriental Insurance, and Caribe Pensiones Consultants. The company is based in San Juan and has a staff of 520 employees. With this deal, it becomes one of the largest financial groups in Puerto Rico.

ADVISERS & DUE DILIGENCEFINANCIAL DATAPARTIES

PARTY ADVISED FINANCIAL ADVISERS LEGAL ADVISERS DUE

DILIGENCE

Oriental Financial Group Jefferies International

Cleary Gottlieb Steen & Hamilton;

McConnel Valdés-

BBVA BBVA Corporate Finance - -

PARTIES ADVISERS & DUE DILIGENCEFINANCIAL DATA

MULTIPLES

Enterprise value Equity value

Revenues - -

EBITDA - -

DEAL VALUE Payment

EUR 379,42m (Cash) EUR 379,42m

TARGET (EUR million)

Revenues - 2011 -

EBITDA - 2011 -

Enterprise value 379,42

Equity value 379,42

FINANCIAL DATA ADVISERS & DUE DILIGENCEPARTIESTARGET: BBVA PR Holding y BBVA Securities of Puerto RicoDESCRIPTION: Financial institutions

SELLER %

BBVA 100

Total sold 100

BUYER %

Oriental Financial Group 100

Total acquired 100

Source: www.TTRecord.com

4746 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

Similarly to 2011, in Spain, most of the highlighted mid-market deals had a cross-border component. Spanish multinationals chose to divest their subsidiaries abroad, and several Spain-based companies set their sights on emerging countries to continue their growth plans.

Also noteworthy were several private equity deals registered in this market segment. The creditors of USP Hospitales, RBS -The Royal Bank of Scotland and Barclays Bank, its founder Gabriel Masfurroll and the management team, sold the hospital group to private equity fund Doughty Hanson. So far, RBS -The Royal Bank of Scotland and Barclays Bank held a 65% of the capital, Gabriel Masfurroll and the management team held 25%, and the remaining 10% was held by John de Zuleta. Doughty Hanson paid EUR 355m, which represents 10,3 times USP’s EBITDA in 2011, and 9 times EBITDA estimated for 2012.

Regarding divestments by Spanish companies, highlights include the sale by Ferrovial, an infrastructure management company, of a 5,7% stake in FGP Topco, the management company of Heathrow airport, to Stable Investment Corporation, a subsidiary of China Investment Corporation (CIC). The deal value was EUR 319,3m. With this deal, Ferrovial will indirectly hold a 44,27% stake in Heathrow Airport Holdings.

Furthermore, Bankia (merger of Caja Madrid and Bancaja) sold a 10,36% stake in Mapfre América to Mapfre. The deal value was EUR 244m, which represents a profit of EUR 102m. Bankia (merger of Caja Madrid and Bancaja) exercised its sale option, agreed in 2005 by both companies. Mapfre América groups the direct insurance business of Mapfre in Latin America. The group is pres-ent in 18 countries and is the leading company in life insurance. Corporación Financiera Caja de Madrid acquired a 10,36% in Mapfre América in 1998. The bank was integrated in BFA as a result of the merger of Caja Madrid and six other savings banks with Bankia (merger of Caja Madrid and Bancaja).

In addition, Italy-based Enel, through Endesa, sold Endesa Ireland to UK-based Scottish & Southern Energy (SSE). The deal value was EUR 286m. Endesa Ireland owns electric power plants with a total capacity of 1.068MW. The deal value was EUR 361m, and includes the company’s net financial position. Moreover, Scottish & Southern Energy (SSE) will invest EUR 137m to finish the construction of a combined cycle turbine, capable of generating 460MW, in wind farm located in Great Island, Wexford.

Other highlighted deals

Enel does not consider Ireland a strategic market, and expects the sale to have a positive impact on its debt of some EUR 382m.

On the other hand, regarding Spanish companies investing abroad, high-lights include Enagás’ acquisition of a 40% stake in GNL Quintero, held by British Gas Group. The deal value was EUR 272m, paid in two equal installments. Enagás acquires a 20% stake for each installment of EUR 136m. The first stage was closed on 13 September 2012, after receiving the appropriate authorizations. The remaining 20% is still pending. After this first stage, GNL Quintero’s share capital is divided between ENAP, Endesa Chile, Metrogas y BG Group, with a 20% stake each. As for the second stage, it is estimated that Enagás will acquire a 40% stake jointly with another shareholder. In this manner, Enagás would hold 51% and the other partner would retain 49% of the capital.

Other highlighted transactions, in this market segment this year, include financial and insurance companies. CaixaBank acquired a 50% stake in Caja Burgos Vida, Compañía de Seguros de Vida, Caja Navarra Seguros y Banca Cívica, and Vida y Pensiones, held by Aegon España, a subsidiary of Dutch company Aegon. The deal value was EUR 190m. With this transaction, which means the end of current joint venture agreements, CaixaBank acquires the insurance business held by the Dutch group in Banca Cívica. On 31 July 2012, Banca Cívica and CaixaBank closed a merger agreement, in the middle of the restructuring process taking place in Spanish financial sector.

4948 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

TARGET SUBSECTOR BUYER SELLER AMOUNT (EUR m)

USP Hospitales Healthcare, Hygiene and Medical Aesthetics Doughty Hanson

Barclays Bank; Private shareholders; RBS - The Royal Bank of Scotland

355

EsmalglassGlass, Ceramic, Paper, Plastics,

Wood and TimberInvestcorp 3i (España)

Accionistas particulares 280

Maxam (antigua Unión Española de Explosivos)

Chemical and Chemical Materials

Advent International España

Vista Capital Portobello Capital 230

Euskaltel Telecoms InvestindustrialTrilantic Capital Partners

Gobierno Vasco; Corporación Mondragón; Endesa; Iberdrola; Kutxabank

(merger BBK, Kutxa y Vital)

198

Panamericana Solar, Tacna Solar Solar

CAF - Corporación Andina de Fomento;

Conduit Capital Partners

Corporación GestampSolarpack 164,9

USP Hospitales; Grupo Hospitalario Quirón

Healthcare, Hygiene and Medical Aesthetics Doughty Hanson 160

BanBajío Financial and insurances Ion Investment Private shareholders Banco Sabadell 156

Flightcare Transports, Aviation and Logistics

Swissport Handling (controlada por PAI Partners)

FCC Versia 135

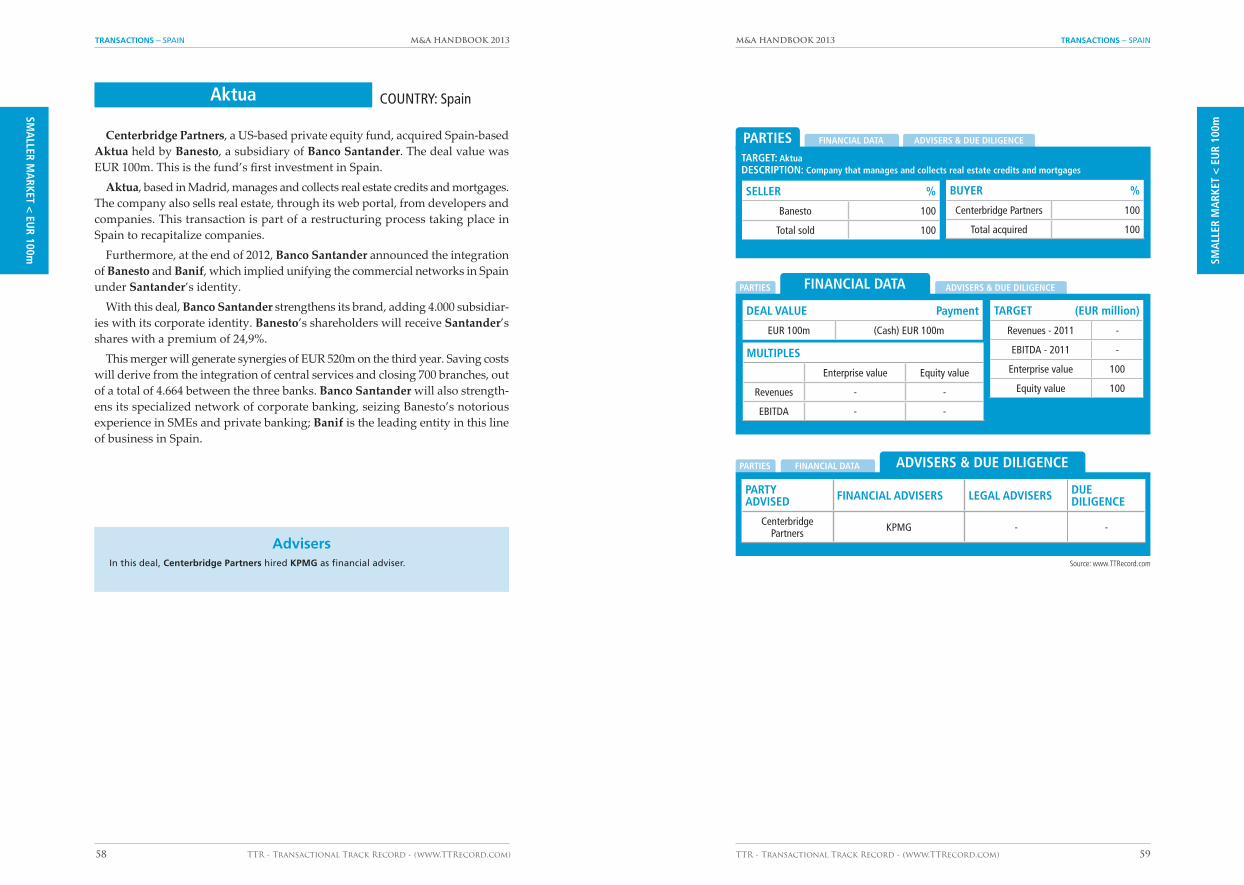

Aktua Financial and insurances Centerbridge Partners Banesto 100

TARGET SUBSECTOR BUYER SELLER AMOUNT (EUR m)

Opodo Internet PermiraAXA Private Equity Amadeus 500

MBNA España Financial and insurances Apollo Capital Bank of America

Merrill Lynch 400

Bond Air Services Transports, Aviation and Logistics Inaer Private shareholders 340

Telecable de Asturias Telecoms Carlyle

Prensa Ibérica; Liberbank (Fusión entre Cajastur, Caja de Extremadura,

Caja Cantabria)

340

Saba Infraestructuras Parkings Torreal

ProA Capital;CaixaBank (Criteria CaixaCorp)

CVC Capital Partners Abertis 311,5

Panasa FoodPrivate shareholders

MercapitalDeyá Capital

Private shareholders 300

Unión Fenosa Deocsa - Deorsa Electric Actis Gas Natural Fenosa 241

Grupo Hospitalario Adeslas (Unión

Médica Regional)

Healthcare, Hygiene and Medical Aesthetics

Goodgrower CaixaBank (Criteria CaixaCorp) 190

Compañía Logística de Hidrocarburos (CLH) Oil and Gas AXA Private Equity Disa 180

Acciona Parkings Parkings EQT Infrastructure Acciona 140

Highlighted private equity investments 2011

Highlighted private equity investments 2012

Source: www.TTRecord.com

Source: www.TTRecord.com

Private Equity

The private equity segment, in 2012, registered a slight decrease compared to 2011, in as far as number of deals in all the market segments, and also in invest-ment volume. The mid-market in particular, decreased slightly with 15 deals registered (nine investments and three divestments) compared to 17 in 2011 (fourteen investments and three divestments). In 2011, the two largest deals in this segment totalized EUR 90m, while in 2012 the two largest deals totalized EUR 635m. Doughty Hanson acquired USP Hospitales, for EUR 355m; and Investcorp acquired Esmalglass held by 3i Group, for EUR 280m.

USP Hospitales

The creditors of USP Hospitales, RBS - The Royal Bank of Scotland and Barclays Bank, its founder Gabriel Masfurroll and its management team, sold the hospital group to private equity fund Doughty Hanson. So far, RBS -The Royal Bank of Scotland and Barclays Bank held a 65% of the capital, Gabriel Masfurroll and the management team held 25%, and the remaining 10% was held by John de Zuleta. Doughty Hanson paid EUR 355m, which represents 10,3 times USP’s EBITDA in 2011 and 9 times EBITDA estimated for 2012.

Other groups showed interest in the acquisition of USP Hospitales: consor-tiums PAI Partners-Grupo Hospital de Madrid and Blackstone-Hospiten. Some companies made offers, such as CVC Capital Partners, through Capio España; Bridgepoint and KKR, jointly with Grupo Hospitalario Quirón. In 2006, USP Hospitales decided to reconvert its debt, of EUR 500m, into shares. As a result its creditors, RBS - The Royal Bank of Scotland y Barclays Bank, acquired a 65% stake of the capital. The management team retained 25%, while Cinven with 64%, Portugal-based Caixa Geral with 10%, and Fundación Alex with 1%, reduced their stake to 10% in USP Hospitales. The remaining 10% will be retained by John de Zulueta.

USP Hospitales has a staff of 7.000 employees and a network with 35 health centers in Spain, Portugal and Morocco. In 2010, USP Hospitales registered a turnover of EUR 319,3m and profits of EUR 6,5m

AdvisersDoughty Hanson hired Rothschild and BBVA Corporate Finance as financial advisers and

Ashurst as legal adviser and also to carry out the due diligence. On the other hand, the

sellers appointed Allen & Overy as legal adviser, while Deloitte carried out the due dili-

gence for USP Hospitales.

5150 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

Esmalglass

Arab group Investcorp acquired Esmalglass, a manufacturer of ceramic colors and enamels, through Goromar XXI. The company was held by private equity fund 3i España and the company’s management team, headed by the Baigorri family, which will retain a minority stake. The deal value was approximately EUR 280m.From this amount, EUR 105m will be paid by ICG (Intermediate Capital Group). Furthermore, Banco Santander and BBVA also supported this deal’s funding. The sale process began in mid-2011, and attracted interest from Mercapital and Ergon, although neither of these firms presented a binding offer. Esmalglass registered a turnover of EUR 270m, in 2010. The firm owns factories in Italy, Brazil, China, Indonesia, United Kingdom and Russia. In 2002, 3i España acquired a 49% stake in Esmalglass, marking its entry the company’s share capital. The deal was executed through a MBO, and the remaining 51% of the capital was retained by the management team. The deal value was EUR 230m. From this amount, EUR 80m were paid by 3i Group, EUR 25m by the management team, the rest was a loan granted by BNP Paribas, for EUR 125m.

Maxam (antigua Unión Española de Explosivos)

Advent International España acquired a 49,9% stake in Maxam, held previ-ously by Portobello Capital and Vista Capital. The deal value is estimated at EUR 230m.

Both funds entered the company’s share capital in 2006, with the acquisition of a 27,37% and a 22,62% stake, respectively. The remaining 50,1% will be retained by the management team, headed by José F. Sanchez-Junco. Portobello Capital y Vista Capital registered profits in this deal; its investment in Maxam, in 2006, was EUR 66m.

Maxam is the third operator of civil explosives in the world. The company registered a turnover of some EUR 800m in 2010, and EBITDA of EUR113m.

AdvisersIn this deal, 3i España hired BNP Paribas as financial adviser and Cuatrecasas, Gonçalves

Pereira as legal adviser. On the other hand, Esmalglass received legal advice from

Deloitte Abogados.

Portobello Capital is firm created in 2010, by five former partners of Inversiones Ibersuizas. The new firm retained 15 subsidiaries as part of its portfolio, and among them was Maxam.

Euskaltel

US-based private equity fund Trilantic Capital Partners and Italy-based fund Investindustrial acquired a 48,1% stake in Euskaltel, for EUR 198m. As a result the following companies will exit Euskaltel’s share capital: Endesa (10,64%), Corporación Mondragón (2%) and the Basque Government (7,5%). Kutxabank and Iberdrola will have their stake reduced to 49,9% and 2% respectively. Euskaltel is a telecommunications company that operates in the Basque Country. In 2011, the company registered a turnover of EUR 334m, with EBITDA of EUR 131m and profits of EUR 38,4m. Euskaltel’s debt is valued at EUR 440m.

This transaction was executed through a capital increase of EUR 68m. The resources will be used to pay the Basque Government for the public telecom-munications network, which up until now was leased by Euskaltel. Subsequently the funds will pay the remaining EUR 198m and recompose the shareholding structure

Panamericana Solar y Tacna Solar

AdvisersAdvent International España hired N+1 as financial adviser and law firms Uría Menéndez,

Clifford Chance and Garrigues as legal advisers. Moreover, Advent International España

appointed The Boston Consulting Group for the sectorial and market analysis and KPMG

España and Aon España to execute the due diligence.

On the other hand, Portobello Capital and Vista Capital appointed CMS Albiñana &

Suárez de Lezo as legal advisers and to carry out the due diligence for both. Maxam (for-

mer Unión Española de Explosivos) hired Linklaters as legal adviser. The real estate due

diligence was carried out by Tinsa and the environment due diligence by Environ Iberia.

AdvisersIn this deal, Kutxabank (merger of BBK, Kutxa and Vital) hired Citigroup as financial adviser

and Deloitte to carry out the due diligence. On the other hand, Investindustrial hired GBS

Finanzas as financial adviser and Garrigues as legal adviser, a law firm which also advised

Trilantic Capital Partners. Euskaltel appointed Uría Menéndez as legal adviser and KPMG to

carry out the due diligence.

5352 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

US-based private equity fund Conduit Capital Partners and CAF - Corpora- ción Andina de Fomento acquired a 81% stake in Tacna Solar and Panamericana Solar, two Peru-based companies that manage and develop photovoltaic plants with capacity of 20 MW each. The deal value was USD 210m. In addition the firms will share the plant’s management with Spain-based companies Solarpack (9,5%) and Corporación Gestamp (9,5%). Currently, Tacna Solar is already built and its operations began recently, while Panamericana Solar is still under construction.

AdvisersConduit Capital Partners hired Estudio Echecopar y Clifford Chance as legal advisers. On

the other hand, Solarpack appointed its own internal team, and law firms Rodrigo, Elías &

Medrano Abogados and Jones Day as legal advisers. Corporación Gestamp, received legal

advice from its own team, as well as from law firms Rodrigo, Elías & Medrano Abogados

and Jones Day.

TARGET SUBSECTOR BUYER SELLER AMOUNT (EUR m)

Gasmedi Healthcare, Hygiene and Medical Aesthetics Air Liquide Mercapital

Private shareholders 330

Controladora Milano Distribution and Retail Kaltex Comercial Advent International Valanza 268,28

Amobee Marketing y Publicidad SingTel (Singapore Telecommunications)

Sequoia Capital Accel Partners

Telefónica240

ZIV Aplicaciones y Technology Technology Crompton Greaves Dinamia

Private shareholders 150

Highlighted private equity exits 2011

Highlighted private equity exits 2012

TARGET SUBSECTOR BUYER SELLER AMOUNT (EUR m)

Saba Infraestructuras ParkingsTorreal

ProA Capital; CaixaBank (Criteria CaixaCorp)

CVC Capital Partners Abertis 311,5

Restauravia Tourism, Hostels and Restaurants Amrest Corpfin Capital 198

Dress for less Internet Privalia Palamon Capital Partners 160

Source: www.TTRecord.com

Source: www.TTRecord.com

5554 TTR - Transactional Track Record - (www.TTRecord.com)TTR - Transactional Track Record - (www.TTRecord.com)

M&A HANDBOOK 2013 TRANSACTIONS – SPAINTRANSACTIONS – SPAIN M&A HANDBOOK 2013

MID

-MA

RKET

> E

UR

100m

MID

-MA

RKET > EU

R 100m

Gasmedi