Embed Size (px)

Citation preview

FIN 673 Mergers and Acquisitions

Professor Robert B.H. Hauswald

Kogod School of Business, AU

2/16/2011 M&A © Robert B.H. Hauswald 2

M&A: Doing the Deal

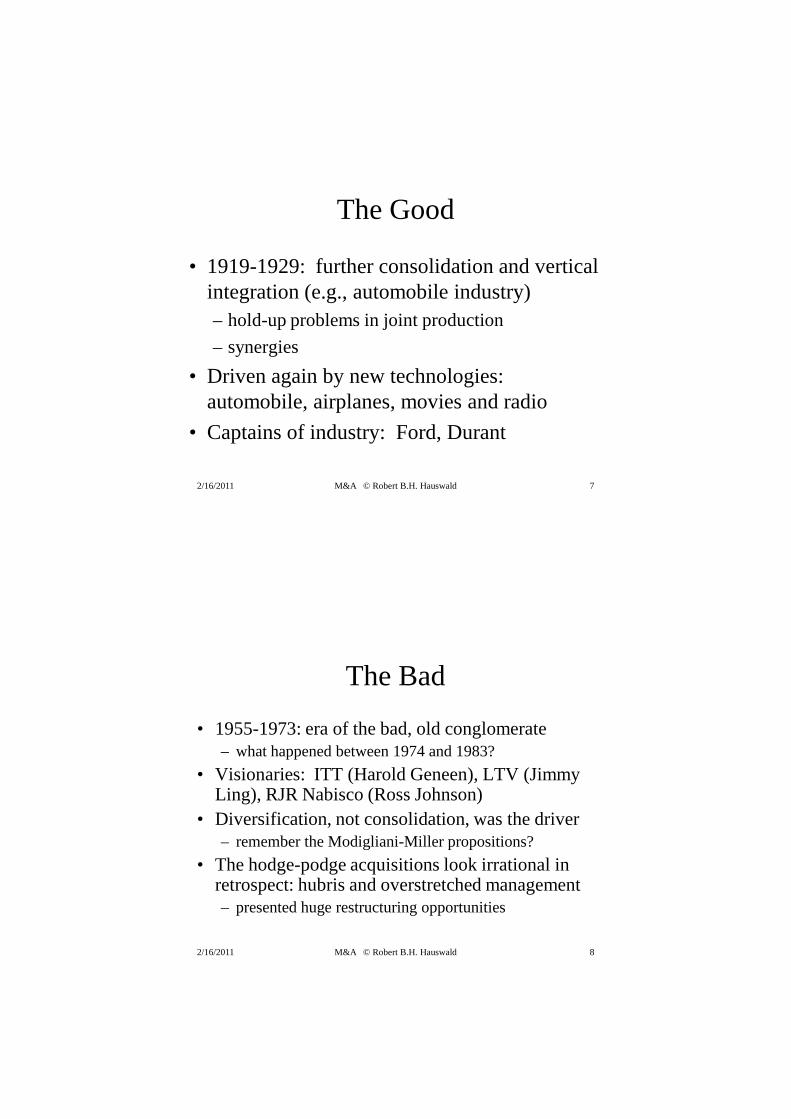

• There are three basic legal procedures that one firm can use to acquire another firm:– Merger– Acquisition of Stock– Acquisition of Assets

• Takeover: imprecise term– acquisition of other firms– hostile or friendly

• Grand tour of issues in M&A: usual topics– mechanics, valuation, evidence

2/16/2011 M&A © Robert B.H. Hauswald 3

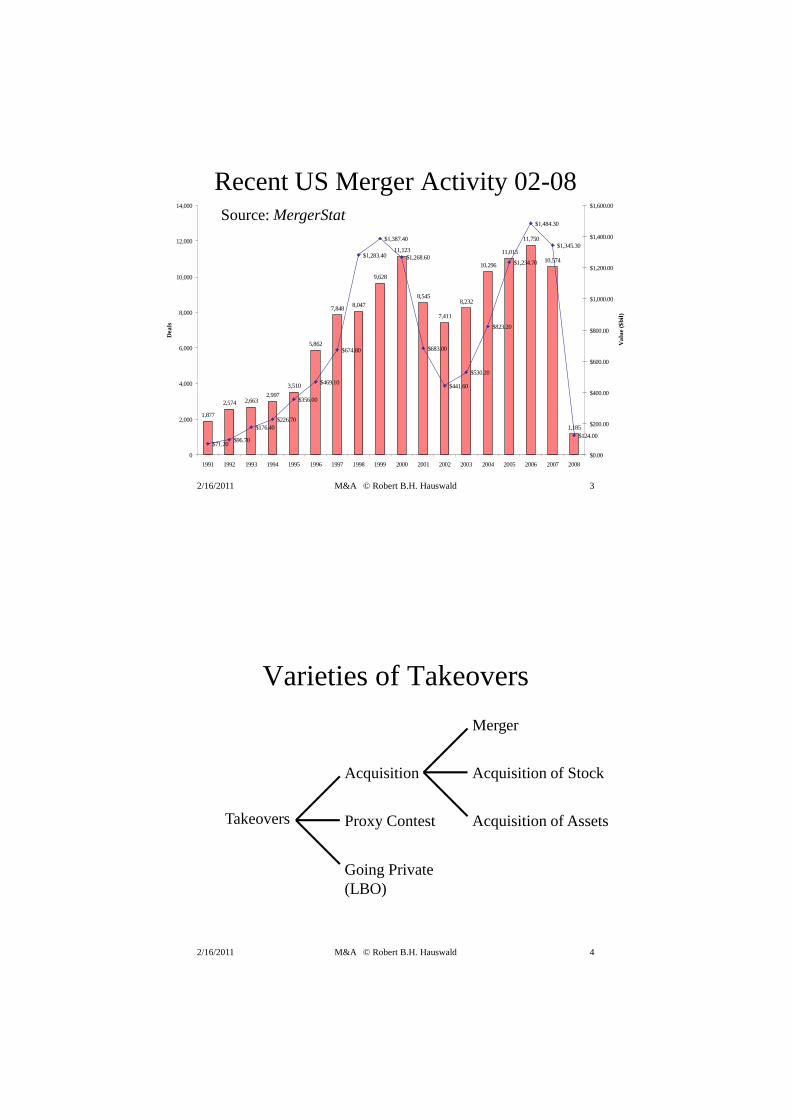

Recent US Merger Activity 02-08Source: MergerStat

1,877

2,574 2,6632,997

3,510

5,862

7,848 8,047

9,628

11,123

8,545

7,411

8,232

10,296

11,013

11,750

10,574

1,185

$71.20$96.70

$176.40$226.70

$356.00

$469.10

$674.80

$1,283.40

$1,387.40

$1,268.60

$683.00

$441.60

$530.20

$823.20

$1,234.70

$1,484.30

$1,345.30

$124.00

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Dea

ls

$0.00

$200.00

$400.00

$600.00

$800.00

$1,000.00

$1,200.00

$1,400.00

$1,600.00

Va

lue

($bi

l)

2/16/2011 M&A © Robert B.H. Hauswald 4

Varieties of Takeovers

Takeovers

Acquisition

Proxy Contest

Going Private(LBO)

Merger

Acquisition of Stock

Acquisition of Assets

2/16/2011 M&A © Robert B.H. Hauswald 5

Forms of Acquisition

• The Tax Forms of Acquisitions– If it is a taxable acquisition, selling shareholders need to

figure their cost basis and pay taxes on any capital gains.– If it is not a taxable event, shareholders are deemed to have

exchanged their old shares for new ones of equivalent value.

• Accounting for Acquisitions: recent changes?– The Purchase Method: the source of much “goodwill”

• purchase accounting is now generally used under recent regulation

– Pooling of Interests: generally used when the acquiring firm issues voting stock in exchange for at least 90 percent of the outstanding voting stock of the acquired firm.

2/16/2011 M&A © Robert B.H. Hauswald 6

The Early Times

• 1893-1904: consolidation of railroads, oil, steel, and other basic industries– Robber barons: Rockefeller, Vanderbilt, Carnegie

• Motivated in large part by new technologies

• Consolidation of fragmented industries (e.g., railroads) into “Trusts:” monopolization

• Fueled by foreign money (instituted by J. P. Morgan): financing “restructuring”

2/16/2011 M&A © Robert B.H. Hauswald 7

The Good

• 1919-1929: further consolidation and vertical integration (e.g., automobile industry)– hold-up problems in joint production

– synergies

• Driven again by new technologies: automobile, airplanes, movies and radio

• Captains of industry: Ford, Durant

2/16/2011 M&A © Robert B.H. Hauswald 8

The Bad

• 1955-1973: era of the bad, old conglomerate– what happened between 1974 and 1983?

• Visionaries: ITT (Harold Geneen), LTV (Jimmy Ling), RJR Nabisco (Ross Johnson)

• Diversification, not consolidation, was the driver– remember the Modigliani-Miller propositions?

• The hodge-podge acquisitions look irrational in retrospect: hubris and overstretched management– presented huge restructuring opportunities

2/16/2011 M&A © Robert B.H. Hauswald 9

The Ugly• 1980’s: growth of LBO’s, financial buyers, MBO’s,

hostile takeovers, break-up LBO’s– undoing the damage of the previous merger wave– trimming fat: restructuring gains– who is in charge? – realigning management and shareholder interests: focus

on shareholder value vs. mangerial entrenchment• Spurred in large part by sophisticated financing and

leverage: the charm of debt– bred its own excesses: debt crisis in the early 1990s

• The raiders: I. Boesky, M. Milken, T. Boone Pickens, KKR, Perelman, Carl Icahn, K. Kerkorian

2/16/2011 M&A © Robert B.H. Hauswald 10

The Irrational

• 1993-2000: dotcom bubble and merger mania– Fueled by the “Irrational Exuberance” of Stock

Market Valuations: Vivendi-Universal

• Motivated by the internet – Deregulation (Banks, Broadcasting, …etc.)

– Relaxation of Antitrust Restraints

– Technology

– Foreign Investment and Cheap Money

– Globalization and its

2/16/2011 M&A © Robert B.H. Hauswald 11

Merger Drivers

• Bruce Wasserstein’s five “pistons” for M&A:– Technological Developments

– Drive for Scale

– Regulatory and Political Change

– Leadership Style

– Fluctuations in the Financial Markets

• Incompetence or worse– restructuring gains, missed opportunities

2/16/2011 M&A © Robert B.H. Hauswald 12

Corporate Strategies in M&A

Exploit market power, economies of scale & scope,

and market inefficiencies

Same industry/Same market- Consolidation

Related industries- Horizontal

Same industry/Different market- InternationalSuppliers

- Vertical

Customers- Vertical

2/16/2011 M&A © Robert B.H. Hauswald 13

M&A Timeline

3 8 11 13 17+Weeks

3 weeks

Preparation

ExecutedAgreement

Contact Buyers/Sellers

Marketing

5 weeks

Preparation Indicationsof Interest

Potential Buyer Due Diligence

3 weeks

Final Bids

Negotiations

2 weeks

Closing

4–8 weeks

Transaction Closed

2/16/2011 M&A © Robert B.H. Hauswald 14

1

Company Evaluation

Weeks

Conduct due diligence

Understand / assess financial and strategic objectives

Develop financial models

Develop positioning strategy

Draft descriptive selling memorandum

Develop potential acquiror list

Find agreement on all elements of process

2

Preparation and Research

3

Executive

Marketing

Strategy

4

Screening and Due Diligence

5

Execution and Closing

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Contact potential acquirors

Execute confidentiality agreements

Distribute descriptive selling memorandum

Prepare management presentation

Personal visits

Schedule visits by potential acquirors

Initial due diligence

Discuss feedback with management

Evaluate proposals

Select final candidates

Negotiate agreement in principle

Conduct final due diligence

Negotiate definitive merger or purchase agreement

Announcement of transaction

Close transaction

17+

Phase

Using an Executive Summary as the principal “selling document” will sometimes help to compress the preparatory phases of the sale process . Additionally, the preemptive bid approach may expedite the screening and buyer diligence phases.

M&A Process

2/16/2011 M&A © Robert B.H. Hauswald 15

Alternative Mechanisms

Contact most logical potential buyer

Mechanism

Price Competition

Confidentiality

Process Flexibility

Minimize Business

Disruption

ConsiderationsRisk of unsuccessful sale and suboptimal valuation

Privately contact a limited number of potential buyers (10–25 buyers)

Likely to elicit optimal valuation

Make public announcement and contact broad universe of potential buyers (30+ buyers)

Reluctance of potential buyers to participate in auctions

Exclusive Negotiation Private Auction Public Auction

+

+

+

+

2/16/2011 M&A © Robert B.H. Hauswald 16

Critical Terms of a Transaction1. Price

2. Consideration — cash or stock or cash & stock

3. Transaction structure

4. Registration rights

5. Timetable/speed

6. Management roles/employment contracts/retention agreements

7. Board composition

8. Exclusivity/no shop

9. Break-up fee/fiduciary out

10. Escrow amounts/earn-outs

11. Conditions to closing

12. Representations and warranties

2/16/2011 M&A © Robert B.H. Hauswald 17

Hostility Is Back!

• 62% of hostile bids in 2001 involved high-tech companies– hostile deals in HT used to be avoided because of the

fear that human capital would walk; but– fewer options for HC in down market: more comfort in

purchasing in hostile fashion

• New hostility has also initiated another wave of defensive tactics (e.g., 35% increase in Poison Pill adoption in 2001); but– such measures now appear to be used to leverage up

offers (36% vs. 32% premiums) rather than scuttle them

2/16/2011 M&A © Robert B.H. Hauswald 18

Human Assets

2/16/2011 M&A © Robert B.H. Hauswald 19

Determining the Synergy from an Acquisition

• Most acquisitions fail to create value for the acquirer

• The main reason why they do not lies in failures (or unwillingness?) to integrate two firms after a merger– intellectual capital often walks out the door when

acquisitions aren't handled carefully

– M&A as real options on synergies: often out-of-the money

– acquisitions deliver value when they allow for scale economies or market power, better products and services in the market, or learning from the new firms

2/16/2011 M&A © Robert B.H. Hauswald 20

Problems in Corporate Cooperation

• The role of management as– facilitators

– complicators

2/16/2011 M&A © Robert B.H. Hauswald 21

Sources of Synergy from Acquisitions

• Revenue Enhancement– cross-fertilization: technology, bundling, etc.

• Cost Reduction– eliminating overlap; also– replacing ineffective managers.

• Tax Gains – Net Operating Losses– Unused Debt Capacity

• The Cost of Capital– Economies of Scale in Underwriting.

2/16/2011 M&A © Robert B.H. Hauswald 22

M&A Synergies

• Valuing synergies from an acquisition

– total greater than sum of the parts– synergistic cash flows:

where

• Revenueenhancement– strategic benefits and technological monopoly

• Cost reduction– economies of scale– economies of scope: cross-fertilization

• Management inefficiencies: cuts both ways

( ) 0Synergy >+−= BAAB VVV

( )∑= +

∆=T

tt

t

r

C

1 1Synergy

ttttt ∆CapExp∆Taxes∆Costs∆Rev∆C −−−=

2/16/2011 M&A © Robert B.H. Hauswald 23

“Bad” Reasons for Mergers

• Earnings Growth– Only an accounting illusion.

• Diversification– Shareholders who wish to diversify can do so at much

lower cost with one phone call to their broker than can management with a takeover

• Hubris and governance failures: wrong objectives“Corporate executives in general and CEOs in particular are accustomed to winning and, as a result, define “success” in M&A as closing the deal”

Soter, 2001, “M&A – Why Most Winners Lose”

– this means what if you were to buy a house?

2/16/2011 M&A © Robert B.H. Hauswald 24

A Cost to Stockholders from Reduction in Risk

• The Base Case– If two all-equity firms merge, there is no transfer of

(financing) synergies to bondholders, but if…

• One Firm has Debt– The value of the levered shareholder’s call option falls

– recall that equity with leverage = call option

• How Can Shareholders Reduce their Losses from the Coinsurance Effect?– Retire debt pre-merger.

2/16/2011 M&A © Robert B.H. Hauswald 25

M&A Valuation Principles

• Perspective– target valuation proceeds from the perspective of

acquiring company’s shareholders– NPV of acquisition is the “value of the target to

acquirer” minus the “effective cost”

• Value of the target to the acquirer is made up of:– Stand alone value of the target plus– Value of improvements at target made by acquirer

management plus– Value of pure synergies between target and acquirer

2/16/2011 M&A © Robert B.H. Hauswald 26

Calculating the Value of the Firm after an Acquisition

• Avoiding Mistakes– Do not Ignore Market Values– Estimate only Incremental Cash Flows– Use the Correct Discount Rate– Don’t Forget Transactions Costs

• The NPV of a Merger– Typically, a firm would use NPV analysis when making

acquisitions: why might this approach be wrong?– The analysis is straightforward with a cash offer, but

gets complicated when the consideration is stock.

2/16/2011 M&A © Robert B.H. Hauswald 27

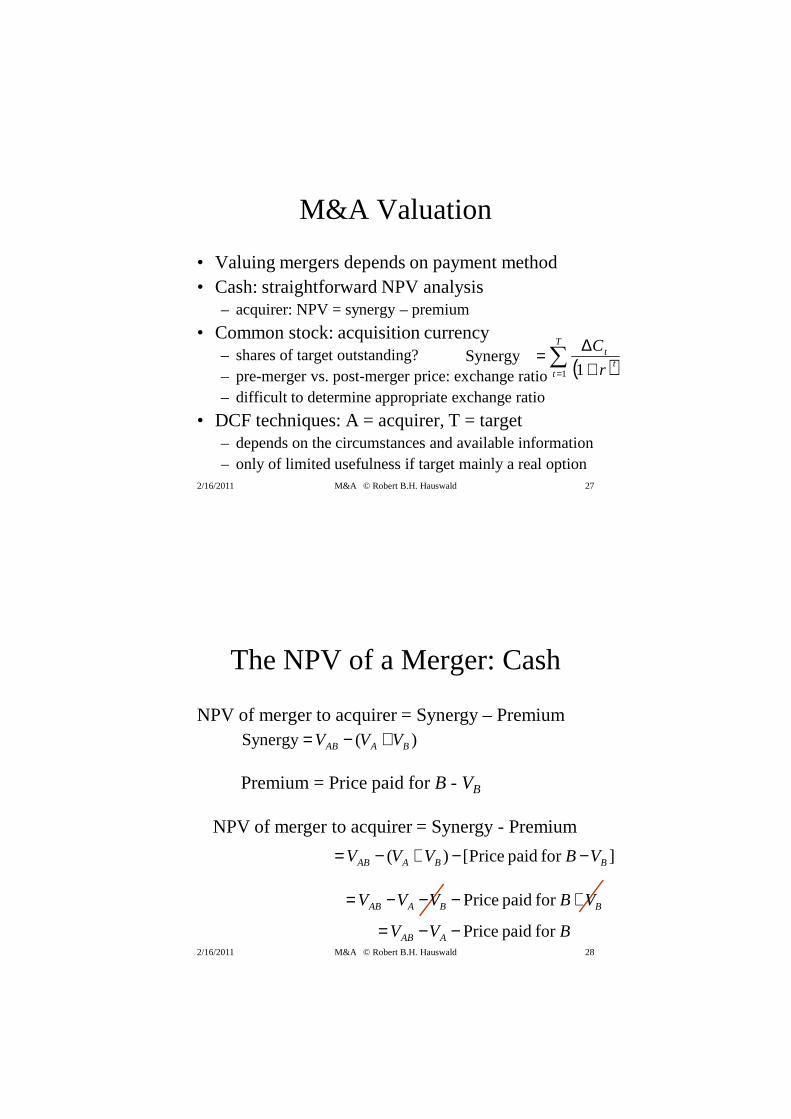

M&A Valuation

• Valuing mergers depends on payment method• Cash: straightforward NPV analysis

– acquirer: NPV = synergy – premium

• Common stock: acquisition currency– shares of target outstanding? – pre-merger vs. post-merger price: exchange ratio– difficult to determine appropriate exchange ratio

• DCF techniques: A = acquirer, T = target– depends on the circumstances and available information– only of limited usefulness if target mainly a real option

( )∑= +

∆=T

tt

t

r

C

1 1Synergy

2/16/2011 M&A © Robert B.H. Hauswald 28

The NPV of a Merger: Cash

NPV of merger to acquirer = Synergy – Premium )(Synergy BAAB VVV +−=

Premium = Price paid for B - VB

NPV of merger to acquirer = Synergy - Premium

]for paid Price[)( BBAAB VBVVV −−+−=

BBAAB VBVVV +−−−= for paid Price

BVV AAB for paid Price−−=

2/16/2011 M&A © Robert B.H. Hauswald 29

Stand-alonevalue oftarget firm

(Value of firmwithout anytakeoverpremium)

Value of

synergies,etc.

Transactioncosts

Grossvalue oftarget firmto acquirer

Price paidincludingpremium

Net valuegained foracquirer

Valueof

debt

Gross value ofequity oftarget toacquirer

Cash Acquisition Valuation: Old (Mature) Firm

2/16/2011 M&A © Robert B.H. Hauswald 30

Stand-alonevalue of

target's equity(without anytakeoverpremium)

Value of

synergies,etc.

Transactioncosts

Grossvalue ofequity oftarget toacquirer

Price paidincludingpremium

Net valuegained foracquirer

Cash Acquisition Valuation: New (Young) Firm

2/16/2011 M&A © Robert B.H. Hauswald 31

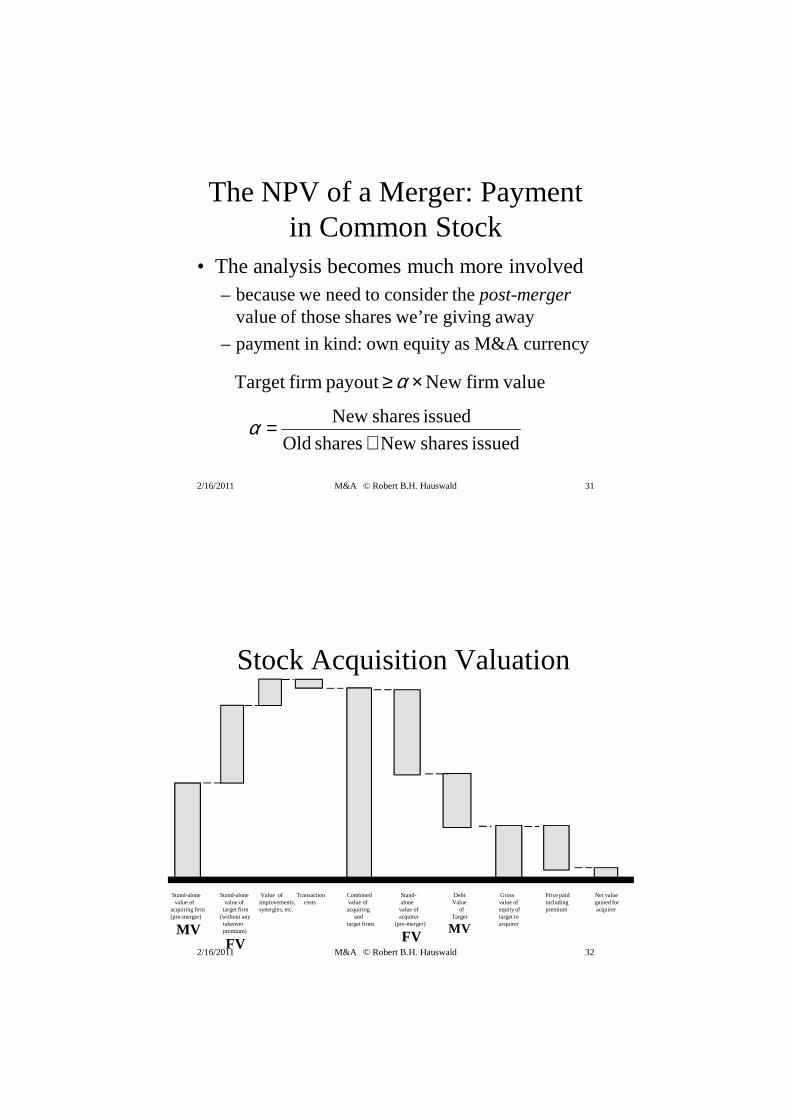

The NPV of a Merger: Payment in Common Stock

• The analysis becomes much more involved – because we need to consider the post-merger

value of those shares we’re giving away

– payment in kind: own equity as M&A currency

valuefirm Newpayout firmTarget ×≥ α

issued shares Newshares Old

issued shares New

+=α

2/16/2011 M&A © Robert B.H. Hauswald 32

Stand-alonevalue of

acquiring firm(pre-merger)

MV

Stand-alonevalue oftarget firm

(without anytakeoverpremium)

FV

Value of improvements, synergies, etc.

Transactioncosts

Combinedvalue ofacquiring

and target firms

Stand-alonevalue ofacquirer

(pre-merger)

FV

Grossvalue ofequity oftarget toacquirer

Price paidincludingpremium

Net valuegained for acquirer

DebtValue

ofTarget

MV

Stock Acquisition Valuation

2/16/2011 M&A © Robert B.H. Hauswald 33

Cash versus Common Stock

• Overvaluation– If the target firm shares are too pricey to buy with cash,

then go with stock.

• Taxes– Cash acquisitions usually trigger taxes.

– Stock acquisitions are usually tax-free.

• Sharing Gains from the Merger– With a cash transaction, the target firm shareholders are

not entitled to any downstream synergies.

2/16/2011 M&A © Robert B.H. Hauswald 34

Fixed Shares vs. Fixed Value

Fixed Shares• Number of shares issued is

certain, but value of the deal fluctuates between announcement and close of deal

• Conseco acquires Green Tree Financial

• 1 GTF share=0.9165 Conseco share

• Conseco pre-announcement share price=$57.75

• Close-of-deal share price=$48• Post-acquisition share price=$30

Fixed Value• Number of shares issued depends on

prevailing share price at close of deal• Buyer’s share price at close=$76• Buyer issues 52.6 million shares to

purchase Seller for $4 billion value• Buyer’s shareholders have only 48.7%

of combined company, while Seller’s shareholders now own 51.3%

• Pre-acquisition, Buyer shareholders bear all price risk

• Post-acquisition, Seller shareholders have more to gain or lose since they own the majority of the company

2/16/2011 M&A © Robert B.H. Hauswald 35

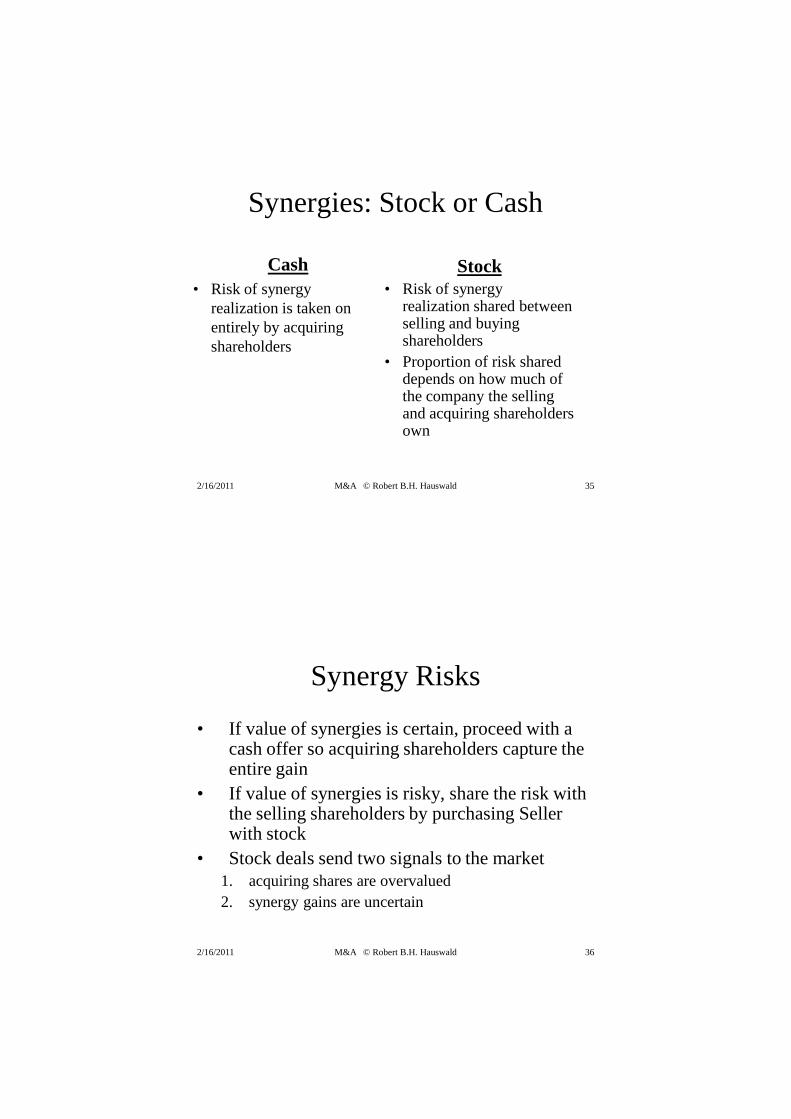

Synergies: Stock or Cash

Stock• Risk of synergy

realization shared between selling and buying shareholders

• Proportion of risk shared depends on how much of the company the selling and acquiring shareholders own

Cash• Risk of synergy

realization is taken on entirely by acquiring shareholders

2/16/2011 M&A © Robert B.H. Hauswald 36

Synergy Risks

• If value of synergies is certain, proceed with a cash offer so acquiring shareholders capture the entire gain

• If value of synergies is risky, share the risk with the selling shareholders by purchasing Seller with stock

• Stock deals send two signals to the market1. acquiring shares are overvalued2. synergy gains are uncertain

2/16/2011 M&A © Robert B.H. Hauswald 37

Pre-closing Market Risk

• Research shows that markets respond favorably when acquirers bear more pre-closing market risk– signals confidence by acquirer

• Fixed-share offer decreases seller’s compensation if acquirer’s shares fall– could offer a fixed-share deal with a floor and a ceiling

• Fixed-value offer sends confident signal since acquirers bear entire pre-closing market risk– floors and ceilings can be established in a fixed-value

offer, too

2/16/2011 M&A © Robert B.H. Hauswald 38

Example

(in millions except share prices) Buyer SellerOutstanding Shares 50 40Share Price $100 $70Market Capitalization $5,000 $2,800

Synergy Value Expected $1,700Offer Price per share $100Seller value to buyer $4,000Premium over market cap $1,200Shareholder Value Added $500

Cash Transaction Stock TransactionBuyer SVA $500 Combined company shares 90Seller SVA 0 Proportion owned by buyer 55.6%

Proportion owned by seller 44.4%Buyer SVA $277.8Seller SVA $222.2

2/16/2011 M&A © Robert B.H. Hauswald 39

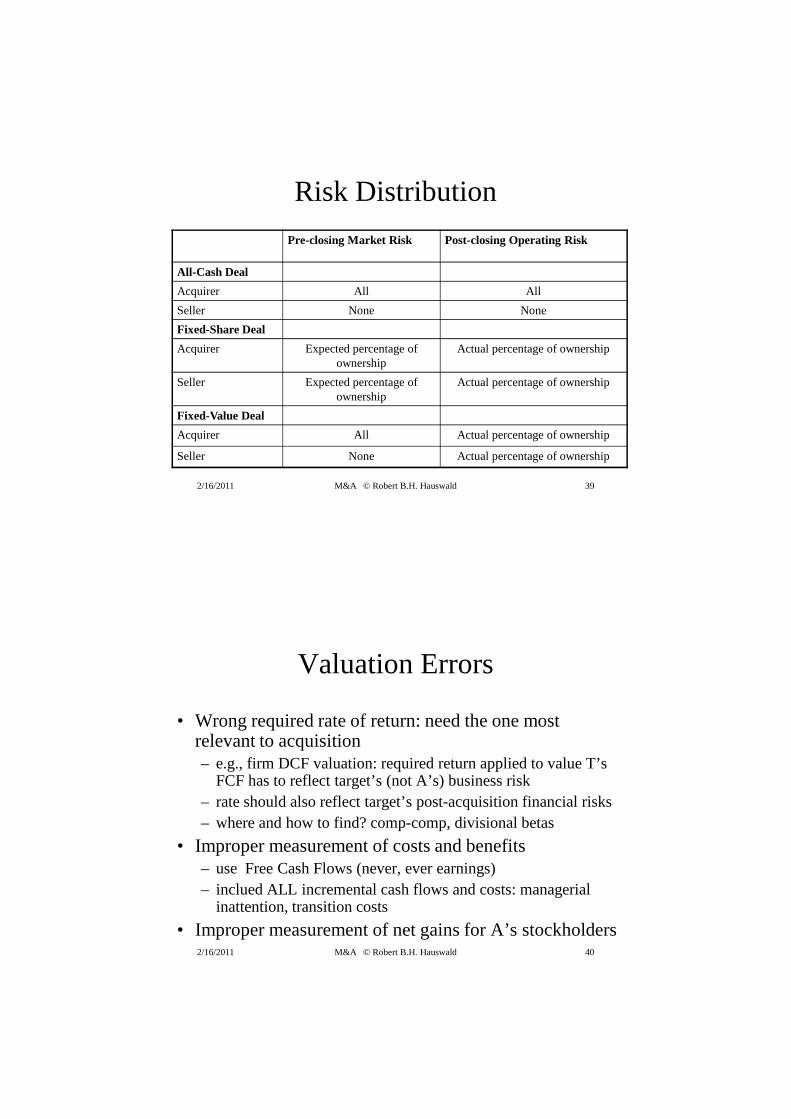

Risk Distribution

Pre-closing Market Risk Post-closing Operating Risk

All-Cash Deal

Acquirer All All

Seller None None

Fixed-Share Deal

Acquirer Expected percentage of ownership

Actual percentage of ownership

Seller Expected percentage of ownership

Actual percentage of ownership

Fixed-Value Deal

Acquirer All Actual percentage of ownership

Seller None Actual percentage of ownership

2/16/2011 M&A © Robert B.H. Hauswald 40

Valuation Errors

• Wrong required rate of return: need the one most relevant to acquisition– e.g., firm DCF valuation: required return applied to value T’s

FCF has to reflect target’s (not A’s) business risk– rate should also reflect target’s post-acquisition financial risks– where and how to find? comp-comp, divisional betas

• Improper measurement of costs and benefits– use Free Cash Flows (never, ever earnings)– inclued ALL incremental cash flows and costs: managerial

inattention, transition costs

• Improper measurement of net gains for A’s stockholders

2/16/2011 M&A © Robert B.H. Hauswald 41

Faulty Acquisition “Analysis”

• Management wants “to do the deal”– why?– sign of what?

• How to justify “the deal”– strategic objectives: problems?– synergies: problems?

• Irrational exuberance: everywhere– cook the numbers– torture synergies until they confess: Worldcom

• Rational exuberance: why?

2/16/2011 M&A © Robert B.H. Hauswald 42

Defensive Tactics

• Target-firm managers frequently resist takeover attempts.– start with press releases and mailings to shareholders

that present management’s viewpoint and escalate to legal action.

• Management resistance may represent the pursuit of self interest at the expense of shareholders– sign of what?

• Resistance may benefit shareholders in the end if it results in a higher offer premium from the bidding firm or another bidder

2/16/2011 M&A © Robert B.H. Hauswald 43

Divestitures

• The basic idea is to reduce the potential diversification discount associated with commingled operations and to increase corporate focus

• Divestiture can take three forms:– Sale of assets: usually for cash– Spinoff: parent company distributes shares of a subsidiary

to shareholders. Shareholders wind up owning shares in two firms. Sometimes this is done with a public IPO.

– Issuance if tracking stock: a class of common stock whose value is connected to the performance of a particular segment of the parent company.

2/16/2011 M&A © Robert B.H. Hauswald 44

The Corporate Charter

• The corporate charter establishes the conditions that allow a takeover.– very often Delaware law intervenes

• Target firms frequently amend corporate charters to make acquisitions more difficult.

• Examples– Staggering the terms of the board of directors.

– Requiring a supermajority shareholder approval of an acquisition

2/16/2011 M&A © Robert B.H. Hauswald 45

Repurchase Standstill Agreements

• In a targeted repurchase the firm buys back its own stock from a potential acquirer, often at a premium.– Critics of such payments label them greenmail.

• Standstill agreements are contracts where the bidding firm agrees to limit its holdings of another firm. – These usually leads to cessation of takeover attempts.– When the market decides that the target is out of play, the

stock price falls.

• Exclusionary Self-Tenders– The opposite of a targeted repurchase.– The target firm makes a tender offer for its own stock while

excluding targeted shareholders.

2/16/2011 M&A © Robert B.H. Hauswald 46

Going Private and LBOs

• If the existing management buys the firm from the shareholders and takes it private.

• If it is financed with a lot of debt, it is a leveraged buyout (LBO)– analyzed as cash deals: NPV

• The extra debt provides a tax deduction for the new owners, while at the same time turning the pervious managers into owners– incentive benefits: reduces the agency costs of equity– provides powerful effort incentives for management

2/16/2011 M&A © Robert B.H. Hauswald 47

Other Devices and the Jargon of Corporate Takeovers

• Golden parachutes are compensation to outgoing target firm management.

• Crown jewels are the major assets of the target. If the target firm management is desperate enough, they will sell off the crown jewels.

• Poison pills are measures of true desperation to make the firm unattractive to bidders. They reduce shareholder wealth.– One example of a poison pill is giving the shareholders

in a target firm the right to buy shares in the merged firm at a bargain price, contingent on another firm acquiring control.

2/16/2011 M&A © Robert B.H. Hauswald 48

M&A Advice from a Wall Street Veteran“Life all comes down to a few moments. This is one of them.”

2/16/2011 M&A © Robert B.H. Hauswald 49

Summary and Outlook

• Synergies drive M&A and corporate cooperation– synergies are as uncertain as everything else– an acquisition is an OPTION on synergies– subsequent investments to make the deal work: might

not make sense with hindsight – who is to blame?

• Model synergies as real options– examples: WebTV, AOL-Time Warner, HP-Compaq

• The record: who wins, who loses in M&A?– what would you expect?– what mergers are fool-proof?