Embed Size (px)

Citation preview

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 1/13

Insights from Exploring Mobile FinancingIndustry of Bangladesh

Prepared for

Sheikh Morshed Jahan

Course Instructor: Business Strategy

Prepared by

Saif Bin Rashid ZR-62Tasnima Iqbal RH-65

Kazi Noman Ahmed ZR-74

Tasnima Haque Orin RH-75

Abdullah Al Rezwan ZR- 80

Nur Hasan Arko ZR- 83

Mazharul Islam Bin Towhid ZR- 89

Radiyah M. Salim RH- 92

Ahnaf Mohsin ZR-99

Maleeha Tarannum RH- 106

September 24, 2013

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 2/13

Table of Contents

1. Macro-Economic View of Mobile Financing in Bangladesh ............................................................ 1

1.1. Regulations of Mobile Financing ............................................................................................. 2

2. Mobile Financial Services and Service Providers: The Status Quo ................................................. 3

3. Exploring M-Financing in Bangladesh ............................................................................................. 5

3.1. Stakeholder Analysis of M-Financing ...................................................................................... 5

3.2. Industry Life Cycle ................................................................................................................... 6

3.3. PESTEL Analysis of M-Financing in Bangladesh....................................................................... 7

3.4. Porter’s Five Forces Model for Mobile Financing ................................................................... 7

3.5. Dynamics of Competition ........................................................................................................ 8

Number of Operators ...................................................................................................................... 8

Service Charges ............................................................................................................................... 9

Accessibility of Service Outlets ....................................................................................................... 9

Services ........................................................................................................................................... 9

3.6. Porter’s Competitive Diamond Model .................................................................................... 9

4. Challenges and Opportunities Ahead for M-Financing ................................................................. 10

4.1. Challenges for M-Financing .................................................................................................. 10

4.2. Potentials for M-Financing .................................................................................................... 10

Works Cited ........................................................................................................................................... 11

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 3/13

1

1. Macro-Economic View of Mobile Financing in BangladeshIn Bangladesh, about half of the adult population is unbanked (48.49 percent) in terms of deposit

accounts in the banks (Islam &Mamun, 2011). Though Bangladesh is not a very big geographical

country to reach, in 2010, there were only 2.221 Banking Branches and 1.443 ATM Booths in per 100

square kilometre (Bangladesh Bank, 2011). That also reflects in the fact that there are only 5.28

Banking Branches and 1.28 ATM Booths for per 100,000 people in Bangladesh (Bangladesh Bank,

2011). This results in lower Financial Inclusion of Bangladesh. Financial inclusion or inclusive

financing is the delivery of financial services, at affordable costs, to sections of disadvantaged and

low income segments of society.

However, it is very inefficient for Banks to expand its operation by rapidly increasing its branch

network as it involves high cost and very low return (Chowdhury, 2010). Globally, e banking services

usage is at a sharp rise due to responsive and convenient nature. In order to reach the unbanked

population and give the customers a more convenient experience, the mobile financial services have

been playing a major role. (BTRC, 2012)Of them, Mobile Banking, popularly known as M-banking has

become extremely popular in emerging markets, especially in developing countries (Khan, 2012). To

provide banking and financial services, such as cash-in, cash out, merchant payment, utility payment,

salary disbursement, foreign remittance, government allowance disbursement, ATM money

withdrawal through mobile technology devices, i.e. Mobile Phone, is called Mobile Banking

(Wikimedia Foundation, 2012).

Figure 1 Mobile Banking Statistics of Bangladesh Source: (Islam I. , 2011)

In 2011, the Central Bank issued Mobile Financial Service Guidelines which both clarified mobilebanking opportunities for banks, defined clear roles, and signalled support for banking innovation.

Mobile Banking Insights of Bangladesh

Population: 150 Million

Urban/rural split: Urban: 28%, Rural: 72%

GDP (PPP): $305 billion

GDP per capita (PPP): $2000

Literacy rate: 56.8%

Remittance (% of GDPP): 11.4%

Agriculture generates over 17% ofGDP, and has become increasinglyimportant as policy makersgrapple with climate change andspikes in global and domesticfood prices.

There is a shift underway totransition from subsistence tocommercial agriculture.

The Banking Sector hasresponded to the agriculturalneeds, with increased products(notably cards and greenfinancing) to supportdevelopment of agriculture (andsustainable agriculture).Opportunity to examine mobile

channel applications.

Banking penetration:36%

Mobile phonepenetration: 65.77%

The MFI sector continues to grow,but with slower uptake amongstwomen entrepreneurs andincreasing uptake with SMEs – demonstrating market saturationin one area, and marketdiversification in another.

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 4/13

2

Through these guidelines, mobile banking will be bank-led. Since 2011, two clear leaders have

emerged – BRAC/bKash and Dutch Bangla Bank/ DBBL. Both have extensive partnerships with the

MNOs. BRAC/bKash alone has access to 98% of mobile subscribers, and a vast agent network – an

agent in almost every other Bangladesh village. Some more recent estimates note that bKash has

over 2 million subscribers (IFC, 2013), a notable leader in this field.

Despite these early advances a number of key issues still remain as it relates to access, usage, and

diversification. A number of surveys indicated that awareness of the service is still relatively low ,

and trust/credibility of the service is preventing adoption. Those who do register for an account are

using the service only once, and not deepening their usage or diversification of services.

1.1. Regulations of Mobile Financing

Bangladesh Bank is the central bank in Bangladesh, overseeing all monetary policies and

regulation of the financial sector.

Banking, payment, and identification rules and guidelines have been updated in the last 10

years. Consumer protection laws do not apply to the financial sector, though are touched

upon in the Payment and Settlement System Guidelines, and the Mobile Financial Service

Guidelines. (Bangladesh Bank, 2011)

Mobile Financial Service Guidelines were released in September 2011 (Boakye, Scott, &

Smyth, 2011) (and updated in December 2011). Through these guidelines, mobile financial

services are to be bank-led through licensed banks. Banks leverage a network of agents, and

are accountable for ensuring that mobile accounts are indeed set up, and compliance with

KYC protocol.

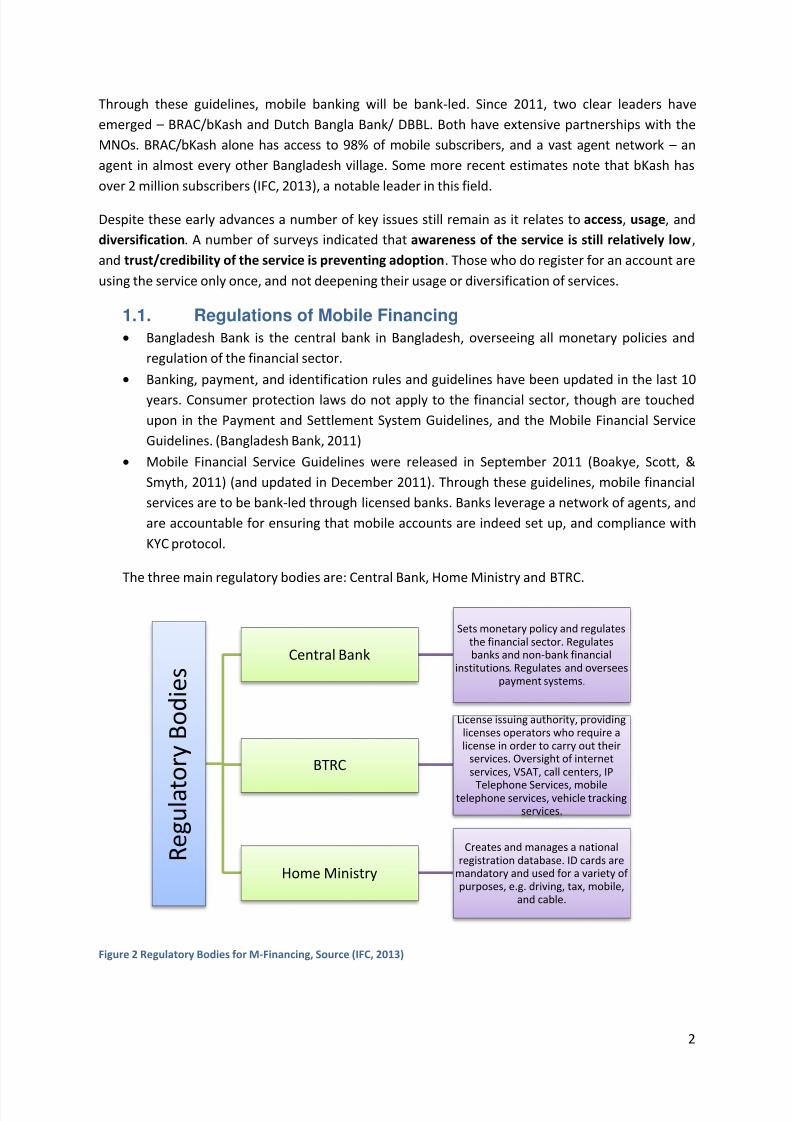

The three main regulatory bodies are: Central Bank, Home Ministry and BTRC.

Figure 2 Regulatory Bodies for M-Financing, Source (IFC, 2013)

R e g u l a t

o r y

B o d i e s

Central Bank

Sets monetary policy and regulatesthe financial sector. Regulatesbanks and non-bank financial

institutions. Regulates and overseespayment systems.

BTRC

License issuing authority, providinglicenses operators who require alicense in order to carry out their

services. Oversight of internetservices, VSAT, call centers, IP

Telephone Services, mobiletelephone services, vehicle tracking

services.

Home Ministry

Creates and manages a nationalregistration database. ID cards are

mandatory and used for a variety ofpurposes, e.g. driving, tax, mobile,

and cable.

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 5/13

3

Areas Regulations

Mobile Money

Issuers

Guidelines for Mobile Financial Services for Banks, 2011

Deposit Taking Banking Companies Act, 1991

Bangladesh Payment and Settlement

Systems Regulations, 2009

Retail Agents Bangladesh Payment and Settlement Systems, 2009

Operating Rules and Procedures of Bangladesh, Automated Cheque

Processing Systems

Bangladesh Electronic Fund Transfer

Network (BEFTN) Rules

BEFTN Risk Management Guideline

Customer

Acquisition

Guidelines for Mobile Financial Services forBanks, 2011

KYC/ AML

Requirements

Money Laundering Prevention Act, 2002

Guidance Notes on the Prevention of Money Laundering

Guidelines for Mobile Financial Services for Banks, 2011Table 1 Regulations of M-Financing in Bangladesh Source (Islam I. , 2011)

The law which directs mobile financing services in Banlgadesh primarily is Guidelines for Mobile

Financial Services for Banks, 2011.

2. Mobile Financial Services and Service Providers: The Status

QuoBanks have been providing mobile financial services to 5 million people through around 117,000

agents across the country and the number of transaction every day is around 4.5 lac. Around BDT

112 Crore (Boakye, Scott, & Smyth, 2011) is being transacted through mobile banking services in

the country every day on an average, helping the economy grow further by transferring money from

urban to rural areas. (Islam & Mamun, 2011)

Following are the names of the companies who were granted permission to provide mobile banking

services by Bangladesh Bank:

Table 2: Mobile Financial Service Permission Granted by Bangladesh Bank

Full Mobile Financial Services Permission International Remittance Only Bangladesh Commerce Bank AB Bank

Bank Asia Citi N.A bKash (BRAC Bank) Dhaka Bank Dutch Bangla Bank Eastern Bank First Security Islami Bank Jamuna Bank IFIC Bank NCCBL Islami Bank Premier Bank Janata Bank Southeast Bank

Mercantile Bank Standard Bank

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 6/13

4

One Bank Prime Bank

Sonali Bank Trust Bank

UCBL (Karim, Islam, & Alam, 2012)

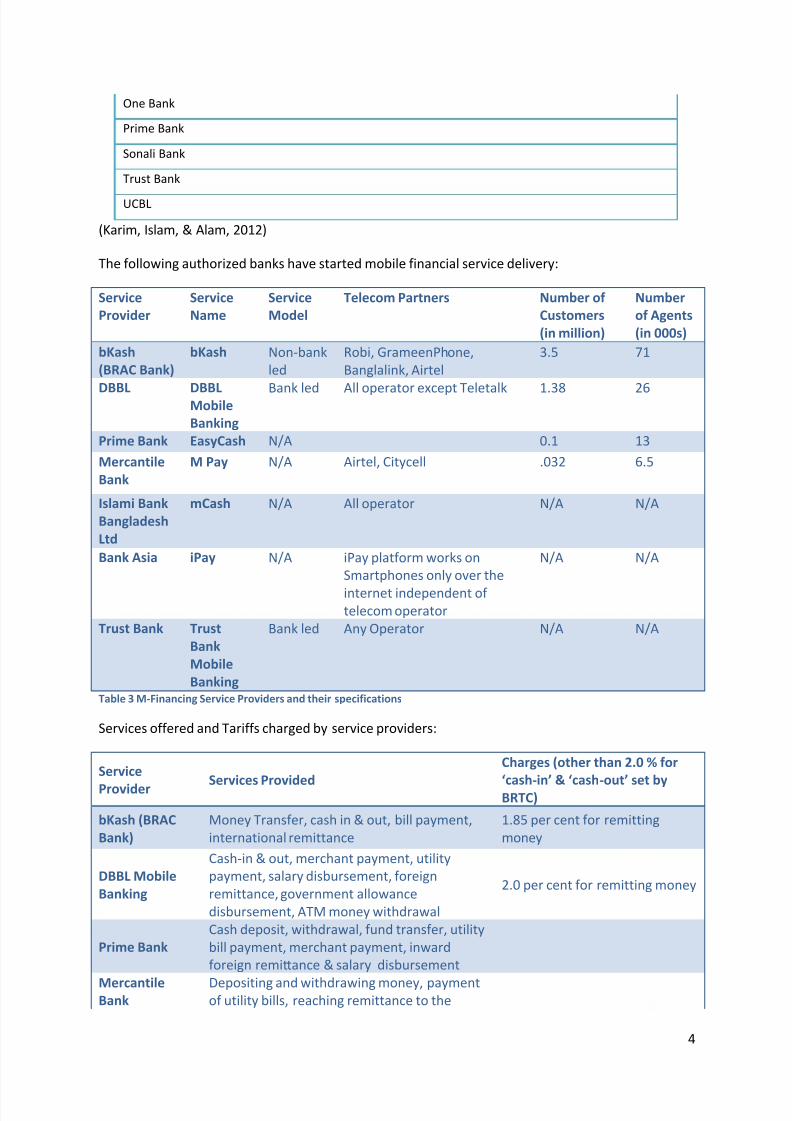

The following authorized banks have started mobile financial service delivery:

Service

Provider Service

Name Service

Model Telecom Partners Number of

Customers

(in million) Number

of Agents

(in 000s) bKash

(BRAC Bank) bKash Non-bank

led Robi, GrameenPhone,

Banglalink, Airtel 3.5 71 DBBL

DBBLMobile

Banking Bank led

All operator except Teletalk

1.38

26

Prime Bank EasyCash N/A 0.1 13 Mercantile

Bank M Pay N/A Airtel, Citycell .032 6.5 Islami Bank

Bangladesh

Ltd mCash N/A All operator N/A N/A

Bank Asia iPay N/A iPay platform works on

Smartphones only over the

internet independent oftelecom operator

N/A N/A

Trust Bank Trust

Bank

Mobile

Banking

Bank led Any Operator N/A N/A

Table 3 M-Financing Service Providers and their specifications

Services offered and Tariffs charged by service providers:

Service

Provider Services Provided Charges (other than 2.0 % for

‘cash-in’ & ‘cash-out’ set byBRTC)

bKash (BRAC

Bank) Money Transfer, cash in & out, bill payment,

international remittance 1.85 per cent for remitting

money DBBL Mobile

Banking Cash-in & out, merchant payment, utility

payment, salary disbursement, foreign

remittance, government allowance

disbursement, ATM money withdrawal 2.0 per cent for remitting money

Prime Bank Cash deposit, withdrawal, fund transfer, utility

bill payment, merchant payment, inward

foreign remittance & salary disbursement MercantileBank Depositing and withdrawing money, payment

of utility bills, reaching remittance to the

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 7/13

5

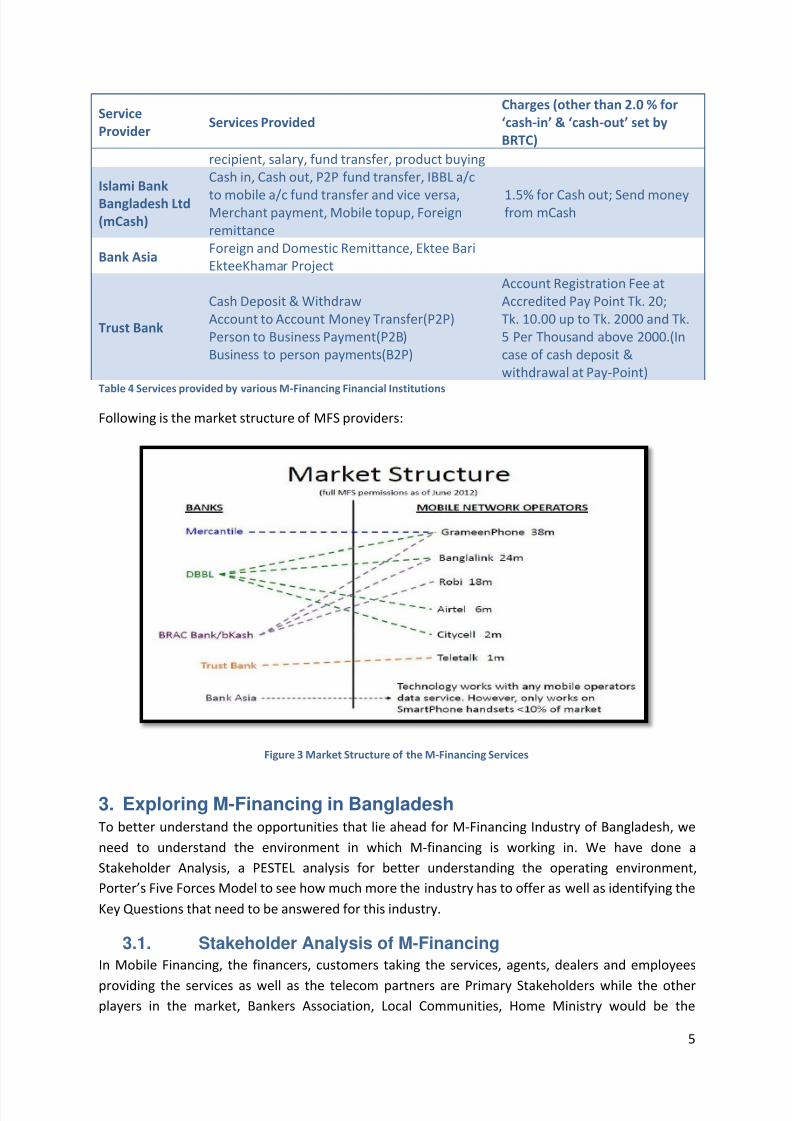

Service

Provider Services Provided Charges (other than 2.0 % for

‘cash-in’ & ‘cash-out’ set by

BRTC) recipient, salary, fund transfer, product buying

Islami Bank

Bangladesh Ltd

(mCash) Cash in, Cash out, P2P fund transfer, IBBL a/c

to mobile a/c fund transfer and vice versa,Merchant payment, Mobile topup, Foreign

remittance 1.5% for Cash out; Send moneyfrom mCash

Bank Asia Foreign and Domestic Remittance, Ektee Bari

EkteeKhamar Project

Trust Bank Cash Deposit & Withdraw Account to Account Money Transfer(P2P)

Person to Business Payment(P2B)

Business to person payments(B2P)

Account Registration Fee at Accredited Pay Point Tk. 20;

Tk. 10.00 up to Tk. 2000 and Tk.

5 Per Thousand above 2000.(In

case of cash deposit &

withdrawal at Pay-Point) Table 4 Services provided by various M-Financing Financial Institutions

Following is the market structure of MFS providers:

Figure 3 Market Structure of the M-Financing Services

3. Exploring M-Financing in BangladeshTo better understand the opportunities that lie ahead for M-Financing Industry of Bangladesh, we

need to understand the environment in which M-financing is working in. We have done a

Stakeholder Analysis, a PESTEL analysis for better understanding the operating environment,

Porter’s Five Forces Model to see how much more the industry has to offer as well as identifying the

Key Questions that need to be answered for this industry.

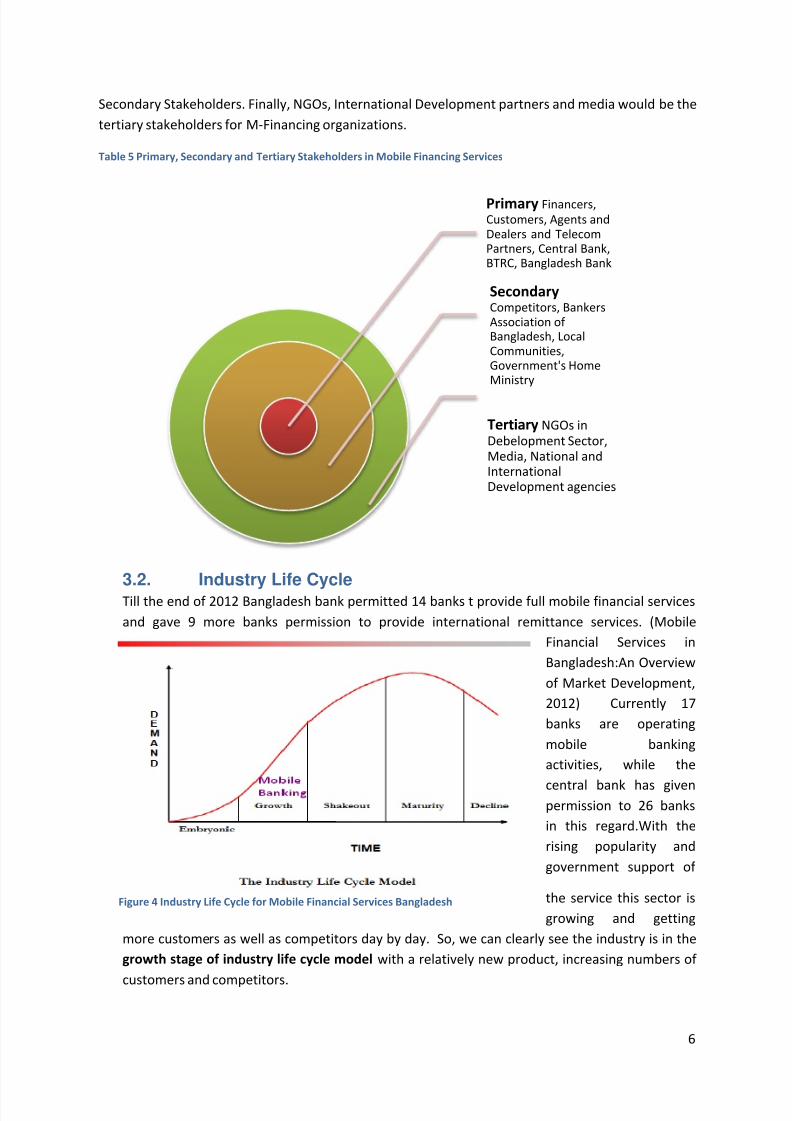

3.1. Stakeholder Analysis of M-FinancingIn Mobile Financing, the financers, customers taking the services, agents, dealers and employees

providing the services as well as the telecom partners are Primary Stakeholders while the other

players in the market, Bankers Association, Local Communities, Home Ministry would be the

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 8/13

6

Secondary Stakeholders. Finally, NGOs, International Development partners and media would be the

tertiary stakeholders for M-Financing organizations.

Table 5 Primary, Secondary and Tertiary Stakeholders in Mobile Financing Services

3.2. Industry Life CycleTill the end of 2012 Bangladesh bank permitted 14 banks t provide full mobile financial services

and gave 9 more banks permission to provide international remittance services. (Mobile

Financial Services in

Bangladesh:An Overview

of Market Development,

2012) Currently 17

banks are operating

mobile banking

activities, while the

central bank has givenpermission to 26 banks

in this regard.With the

rising popularity and

government support of

the service this sector is

growing and getting

more customers as well as competitors day by day. So, we can clearly see the industry is in the

growth stage of industry life cycle model with a relatively new product, increasing numbers of

customers and competitors.

Primary Financers,Customers, Agents andDealers and TelecomPartners, Central Bank,BTRC, Bangladesh Bank

Secondary Competitors, BankersAssociation ofBangladesh, LocalCommunities,Government's HomeMinistry

Tertiary NGOs inDebelopment Sector,Media, National andInternationalDevelopment agencies

Figure 4 Industry Life Cycle for Mobile Financial Services Bangladesh

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 9/13

7

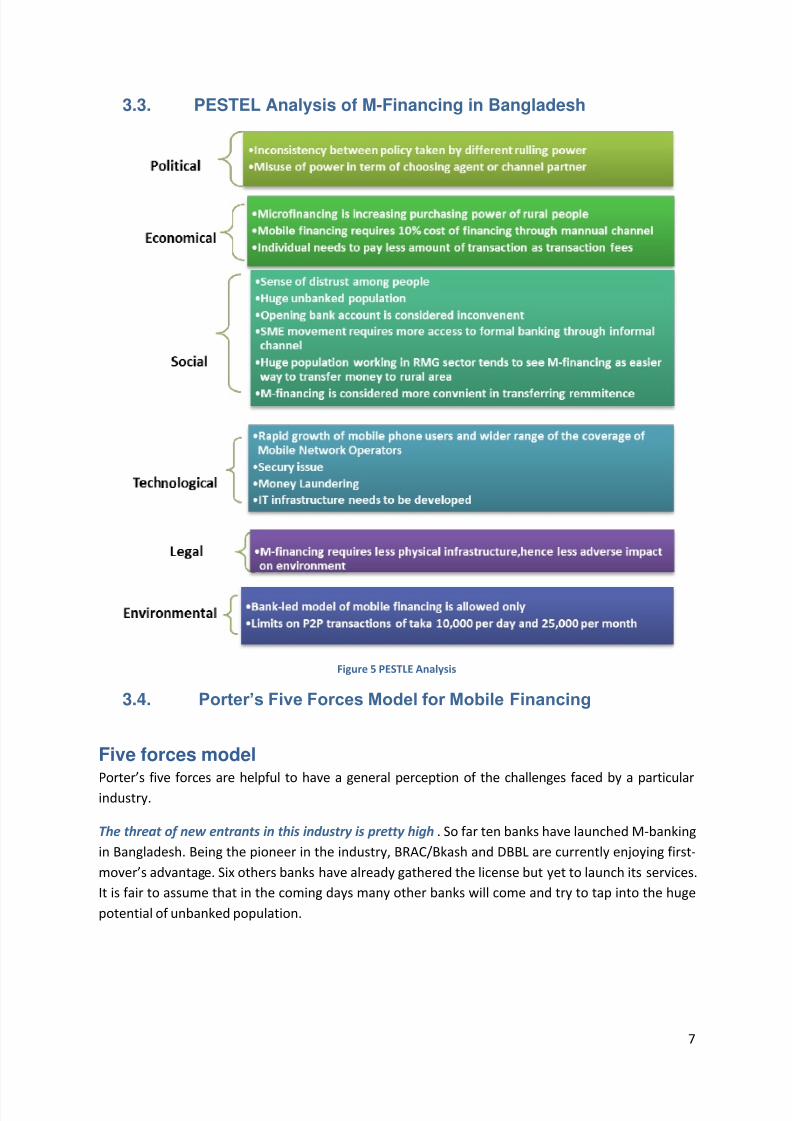

3.3. PESTEL Analysis of M-Financing in Bangladesh

Figure 5 PESTLE Analysis

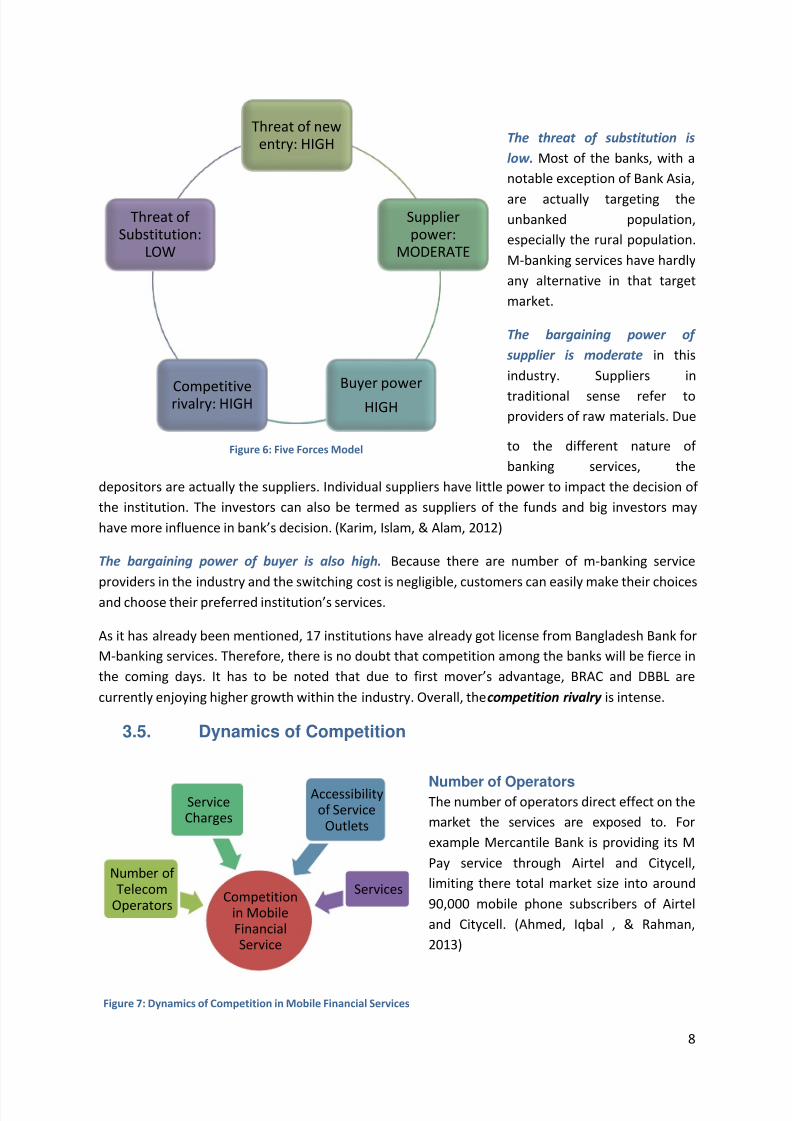

3.4. Porter’s Five Forces Model for Mobile Financing

Five forces modelPorter’s five forces are helpful to have a general perception of the challenges faced by a particular

industry.

The threat of new entrants in this industry is pretty high . So far ten banks have launched M-banking

in Bangladesh. Being the pioneer in the industry, BRAC/Bkash and DBBL are currently enjoying first-

mover’s advantage. Six others banks have already gathered the license but yet to launch its services.

It is fair to assume that in the coming days many other banks will come and try to tap into the huge

potential of unbanked population.

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 10/13

8

The threat of substitution is

low. Most of the banks, with a

notable exception of Bank Asia,

are actually targeting theunbanked population,

especially the rural population.

M-banking services have hardly

any alternative in that target

market.

The bargaining power of

supplier is moderate in this

industry. Suppliers in

traditional sense refer to

providers of raw materials. Due

to the different nature of

banking services, the

depositors are actually the suppliers. Individual suppliers have little power to impact the decision of

the institution. The investors can also be termed as suppliers of the funds and big investors may

have more influence in bank’s decision. (Karim, Islam, & Alam, 2012)

The bargaining power of buyer is also high. Because there are number of m-banking service

providers in the industry and the switching cost is negligible, customers can easily make their choices

and choose their preferred institution’s services.

As it has already been mentioned, 17 institutions have already got license from Bangladesh Bank for

M-banking services. Therefore, there is no doubt that competition among the banks will be fierce in

the coming days. It has to be noted that due to first mover’s advantage, BRAC and DBBL are

currently enjoying higher growth within the industry. Overall, the competition rivalry is intense.

3.5. Dynamics of Competition

Number of OperatorsThe number of operators direct effect on the

market the services are exposed to. For

example Mercantile Bank is providing its M

Pay service through Airtel and Citycell,

limiting there total market size into around

90,000 mobile phone subscribers of Airtel

and Citycell. (Ahmed, Iqbal , & Rahman,

2013)

Threat of newentry: HIGH

Supplierpower:

MODERATE

Buyer power

HIGHCompetitiverivalry: HIGH

Threat ofSubstitution:

LOW

Competitionin MobileFinancialService

Number ofTelecom

Operators

ServiceCharges

Accessibilityof Service

Outlets

Services

Figure 6: Five Forces Model

Figure 7: Dynamics of Competition in Mobile Financial Services

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 11/13

9

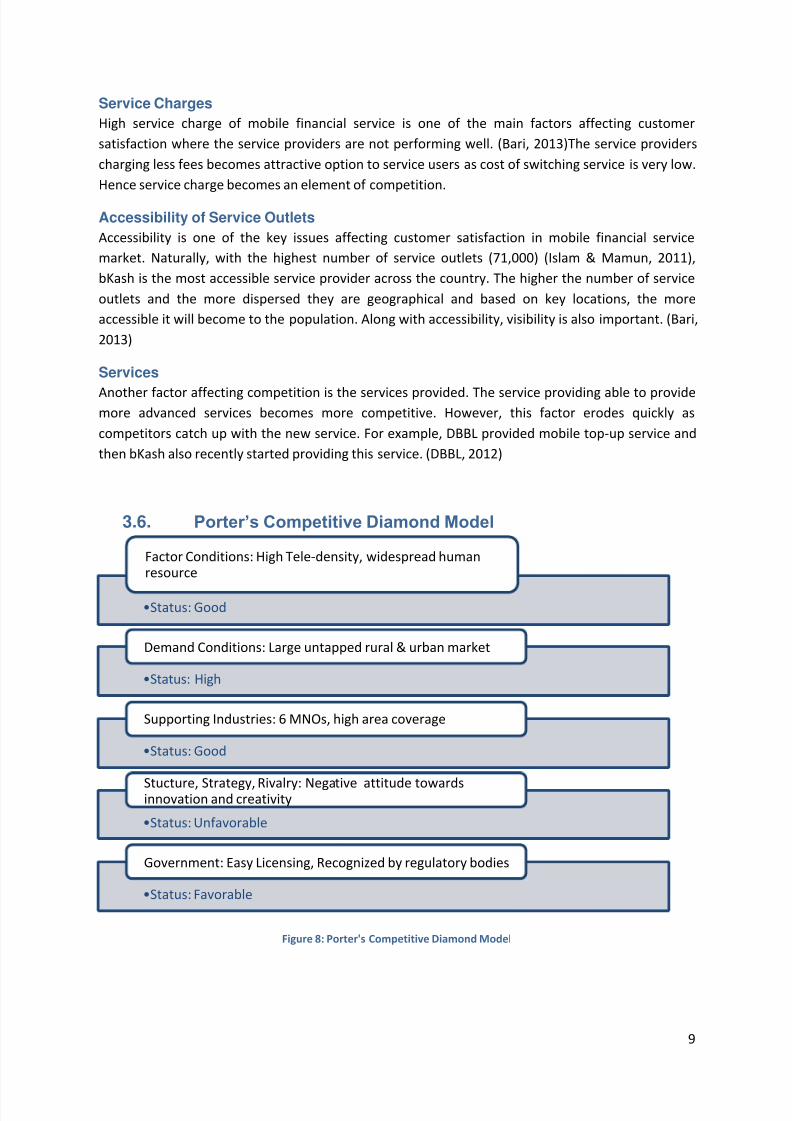

Service Charges

High service charge of mobile financial service is one of the main factors affecting customer

satisfaction where the service providers are not performing well. (Bari, 2013)The service providers

charging less fees becomes attractive option to service users as cost of switching service is very low.

Hence service charge becomes an element of competition.

Accessibility of Service Outlets

Accessibility is one of the key issues affecting customer satisfaction in mobile financial service

market. Naturally, with the highest number of service outlets (71,000) (Islam & Mamun, 2011),

bKash is the most accessible service provider across the country. The higher the number of service

outlets and the more dispersed they are geographical and based on key locations, the more

accessible it will become to the population. Along with accessibility, visibility is also important. (Bari,

2013)

Services

Another factor affecting competition is the services provided. The service providing able to providemore advanced services becomes more competitive. However, this factor erodes quickly as

competitors catch up with the new service. For example, DBBL provided mobile top-up service and

then bKash also recently started providing this service. (DBBL, 2012)

3.6. Porter’s Competitive Diamond Model

Figure 8: Porter's Competitive Diamond Model

•Status: Good

Factor Conditions: High Tele-density, widespread humanresource

•Status: High

Demand Conditions: Large untapped rural & urban market

•Status: Good

Supporting Industries: 6 MNOs, high area coverage

•Status: Unfavorable

Stucture, Strategy, Rivalry: Negative attitude towardsinnovation and creativity

•Status: Favorable

Government: Easy Licensing, Recognized by regulatory bodies

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 12/13

10

4. Challenges and Opportunities Ahead for M-FinancingIn short, the Mobile Financing sector of Bangladesh looks promising if the companies can evaluate

the environment and deliver their value in that manner. Some of the challenges and opportunities

ahead have been identified:

4.1. Challenges for M-Financing1. Channelling the Services through the agents and the telecom partners gives them power

and banks are highly dependent on them. Since banks are highly dependent upon these

other parties, their cost remains higher and the profit margin lower.

2. Through the non-bank led approach, customer identification and transaction monitoring is in

the hands of the agents. This poses a safety threat, because there is hardly any way of

determining who the wrongdoer is should there be any crime such as money laundering or

terrorist financing committed with this service.

3. The profits have to be shared between the bank, the agents and the telecommunication

partners. The agents receive 50%, the banks 25% and the telecommunication partners25%. (Bari, 2013)

4. Infrastructural Development issues for some organizations like DBBL, who alone invested

around BDT 10 crore in mobile banking technology.

5. Bangladesh Bank Regulations limiting transactions up to BDT 25,000 can be transferred

each day by a single mobile-banking account.

4.2. Potentials for M-Financing1. There is an untapped banking market of more than 9 crore to be reached through mobile

banking. (Islam & Mamun, 2011)

2. Mobile banking can be a development tool for NGOs.3. Mobile financing is very convenient, affordable, secure and speedy access to financial

services across the country.

4. The average customer growth rate of the industry is on average 15%. (Huq, 2013)

5. The operators can come up with more value added services keeping the convenience of

customers in mind for example DPS, insurance, bill payment, insurance, micro-loan etc.

6. Carrying Foreign Remittance through mobile financing

7. The RMG sector workers present a huge potential group of customers. 86% of the garments

workers do not use mobile banking, which can be an effective market.

8. Promotes entrepreneurship, as m-financing has become a profitable source of income to

the agents. Each of these operators earns at least BDT 18,000 month, encouraging SME

businesses.

8/13/2019 M-Finance Industry Overview 1.0

http://slidepdf.com/reader/full/m-finance-industry-overview-10 13/13

11

Works CitedAhmed, A., Iqbal , T., & Rahman, M. (2013). Study on Mobile Financing Services: Problems and

Prospects. Dhaka.

Bangladesh Bank. (2011). Amendment of Guidelines on Mobile Financial Services for the Banks.

Bangladesh Bank.

Bari, A. S. (2013, June 4). Mobile Banking Scenario in Bangladesh. (K. N. Ahmed, & A. Ahmed,

Interviewers)

Boakye, K., Scott, N., & Smyth, C. (2011). Mobile For Development. United Nations.

BTRC. (2012, Sep 18). Mobile Money Transfer . Retrieved Sep 21, 2013, from BTRC:

www.btrc.gov.bd/index.php?option=com_content&view=article&id=285&Itemid=745

DBBL. (2012, June 12). Mobile Banking Agents and Merchants. Retrieved June 9, 2013, from Dutch

Bangla Bank Limited: http://www.dutchbanglabank.com/DBBLWeb/mobileagents.jsp

Huq, M. M. (2013, June 5). Head of Mobile Banking, DBBL. (T. Iqbal, Interviewer)

IFC. (2013). IFC Mobile Money Scoping Report . Dhaka: International Finance Corporation.

Islam, D. M., & Mamun, M. S. (2011). Working Paper Series: WP1101, Financial Inclusion: The Role of

Bangladesh Bank. Dhaka: Research Department, Bangladesh Bank.

Islam, I. (2011). The Bangladesh Telecoms Sector: Challenges and Opportunitites. Dhaka: Asian Tiger

Capital Partners.

Islam, M. S., & Chowdhury, I. A. (2012). An Evaluation of the Trade Relations of Bangladesh with

ASEAN: Justification of Being a future member. European Journal of Business and Management .

Karim, A., Islam, S., & Alam, R. (2012). Mobile Financial Services in Bangladesh:An Overview of

Market Development.

(2012). Mobile Financial Services in Bangladesh:An Overview of Market Development. Dhaka:

Bangladesh Bank.

Page, M. (2013). The Mobile Economy. GSMA.