Embed Size (px)

Citation preview

März 2002 © Michael Klemen / Private Page 1

m-business .... what works, what not ....

Globalisierung und m-Business:

mobile commerce... wireless enabled business

Michael KlemenKrems, 07.03.2002

März 2002 © Michael Klemen / Private Page 2

m-business .... what works, what not ....

• M-commerce - an emerging business force that will drive £75 billion global revenue by 2005 of which Europe’s share will be £40 billion and the multiple players who want to capture this revenue

• Austria – where are we

• Trends impacting m-commerce and factors for consideration in capturing m-commerce value - how to understand the landscape and the challenges for both Business and Technology.

• Examples / first experiences enable already certain solutions and why it is important to understand geographic differences when creating solutions.

• What value 3G will provide and the challenges it faces as m-commerce applications evolve.

Introduction1.

März 2002 © Michael Klemen / Private Page 3

m-business .... what works, what not ....

• The mobile market worldwide is …… moving... (booming?)

• Is the market potential for m-commerce significant - £75 billion by 2005 - Europe’s share will be £40 billion Merrill Lynch, Wireless Internet, June 2000

• how much revenue will m-commerce capture from/through mobile data

• Multiple players are trying to capture this potential

• There are challenges which must be overcome before this value is realised and mass market adoption is achieved -There have been some successes to date but real business value is yet to be proven

• 2.5 and 3G will impact m-commerce but there are some issues

• Technology is not the only driving force

Introduction1.

März 2002 © Michael Klemen / Private Page 4

m-business .... what works, what not ....

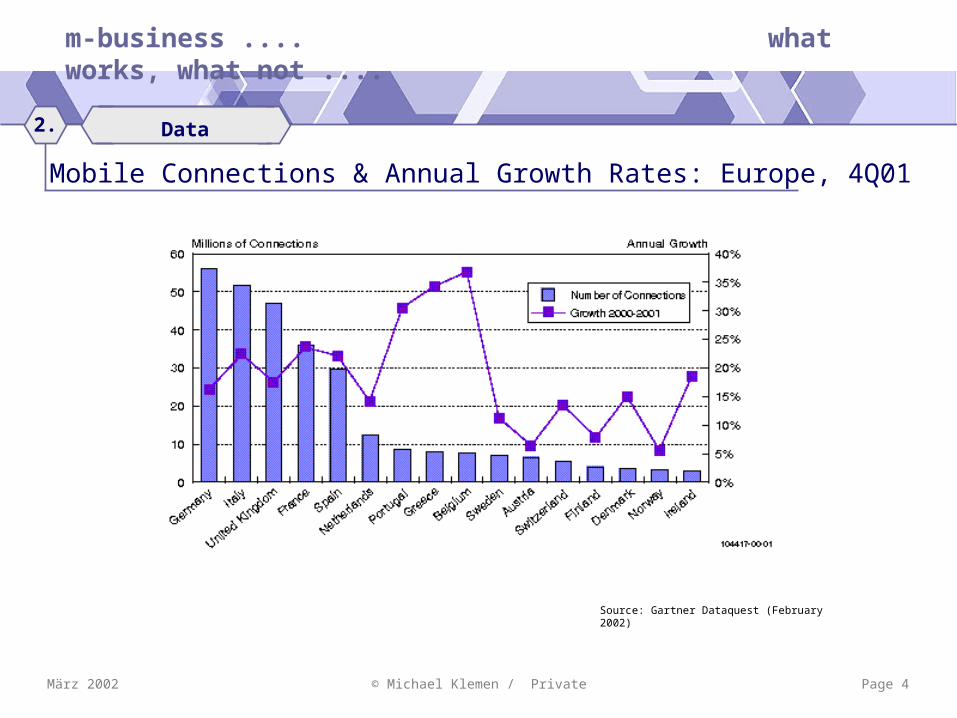

Source: Gartner Dataquest (February 2002)

Mobile Connections & Annual Growth Rates: Europe, 4Q01

Data2.

März 2002 © Michael Klemen / Private Page 5

m-business .... what works, what not ....

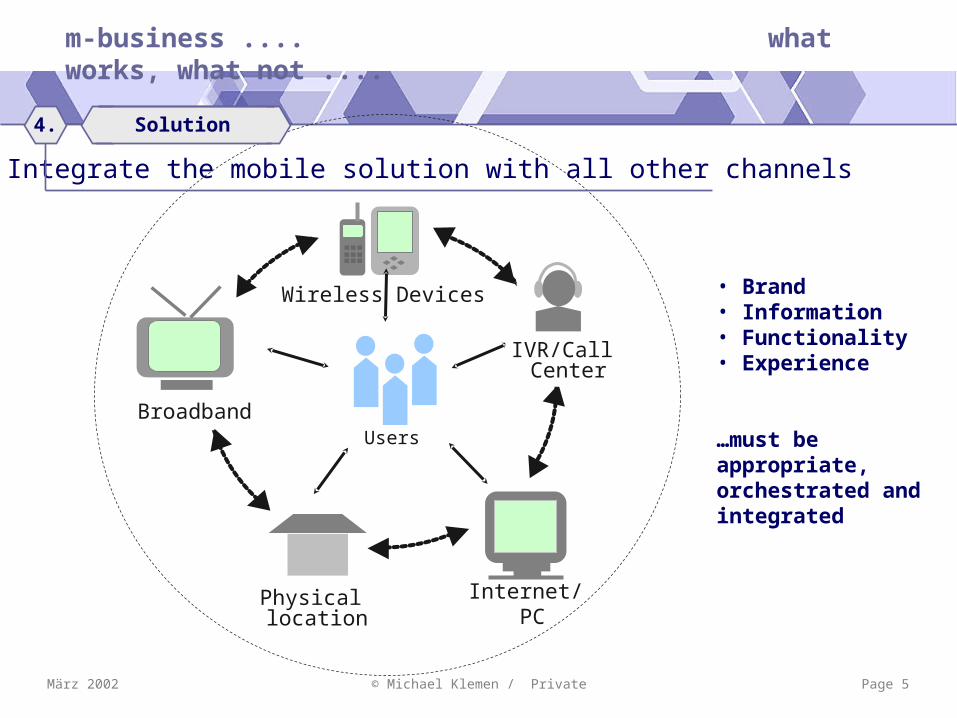

Integrate the mobile solution with all other channels

Users

Internet/ PC

Wireless Devices

Broadband

Physical location

IVR/Call Center

• Brand• Information• Functionality• Experience

…must be appropriate,orchestrated and integrated

Solution4.

März 2002 © Michael Klemen / Private Page 6

m-business .... what works, what not ....

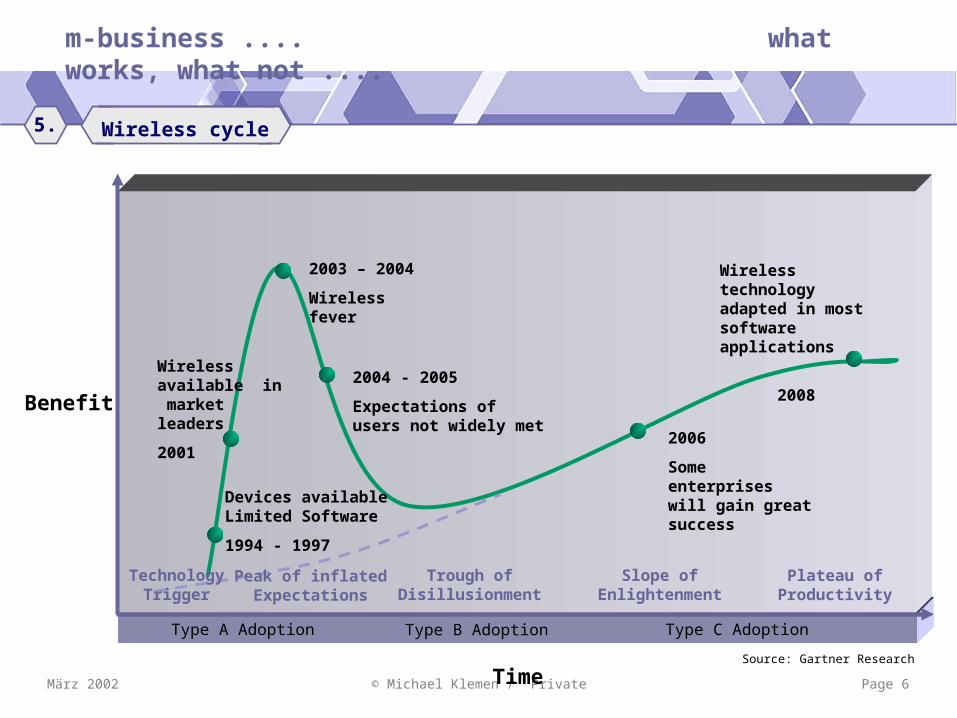

Type A Adoption Type B Adoption Type C Adoption

Benefit

TimeSource: Gartner Research

Wireless cycle5.

Peak of inflatedExpectations

Slope ofEnlightenment

TechnologyTrigger

Trough ofDisillusionment

Plateau ofProductivity

Wireless available in market leaders

2001

Devices available Limited Software

1994 - 1997

2003 – 2004

Wireless fever

2004 - 2005

Expectations of users not widely met

2006

Some enterprises will gain great success

Wireless technology adapted in most software applications

2008

März 2002 © Michael Klemen / Private Page 7

m-business .... what works, what not ....

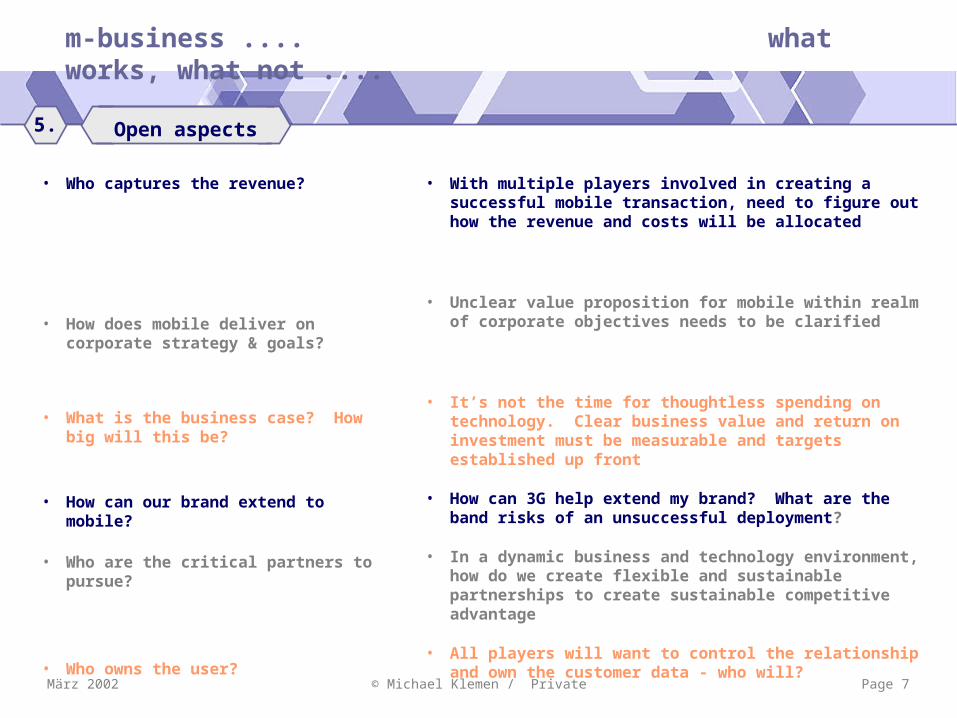

• With multiple players involved in creating a successful mobile transaction, need to figure out how the revenue and costs will be allocated

• Unclear value proposition for mobile within realm of corporate objectives needs to be clarified

• It’s not the time for thoughtless spending on technology. Clear business value and return on investment must be measurable and targets established up front

• How can 3G help extend my brand? What are the band risks of an unsuccessful deployment?

• In a dynamic business and technology environment, how do we create flexible and sustainable partnerships to create sustainable competitive advantage

• All players will want to control the relationship and own the customer data - who will?

• Who captures the revenue?

• How does mobile deliver on corporate strategy & goals?

• What is the business case? How big will this be?

• How can our brand extend to mobile?

• Who are the critical partners to pursue?

• Who owns the user?

Open aspects5.

März 2002 © Michael Klemen / Private Page 8

m-business .... what works, what not ....

Technology

März 2002 © Michael Klemen / Private Page 9

m-business .... what works, what not ....

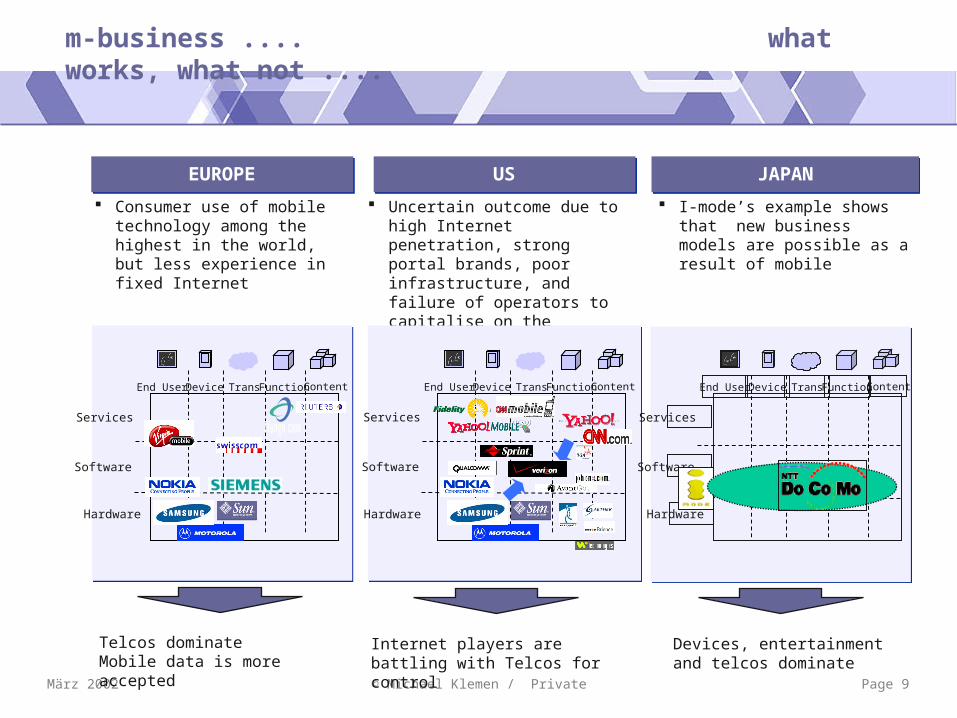

US JAPANEUROPE

I-mode’s example shows that new business models are possible as a result of mobile

Uncertain outcome due to high Internet penetration, strong portal brands, poor infrastructure, and failure of operators to capitalise on the Internet

Consumer use of mobile technology among the highest in the world, but less experience in fixed Internet

Software

Hardware

Services

DeviceEnd User FunctionTrans Content

Devices, entertainment and telcos dominate

Internet players are battling with Telcos for control

Software

Hardware

Services

DeviceEnd User FunctionTrans Content

Telcos dominateMobile data is more accepted

Software

Hardware

Services

DeviceEnd User FunctionTrans Content

März 2002 © Michael Klemen / Private Page 10

m-business .... what works, what not ....

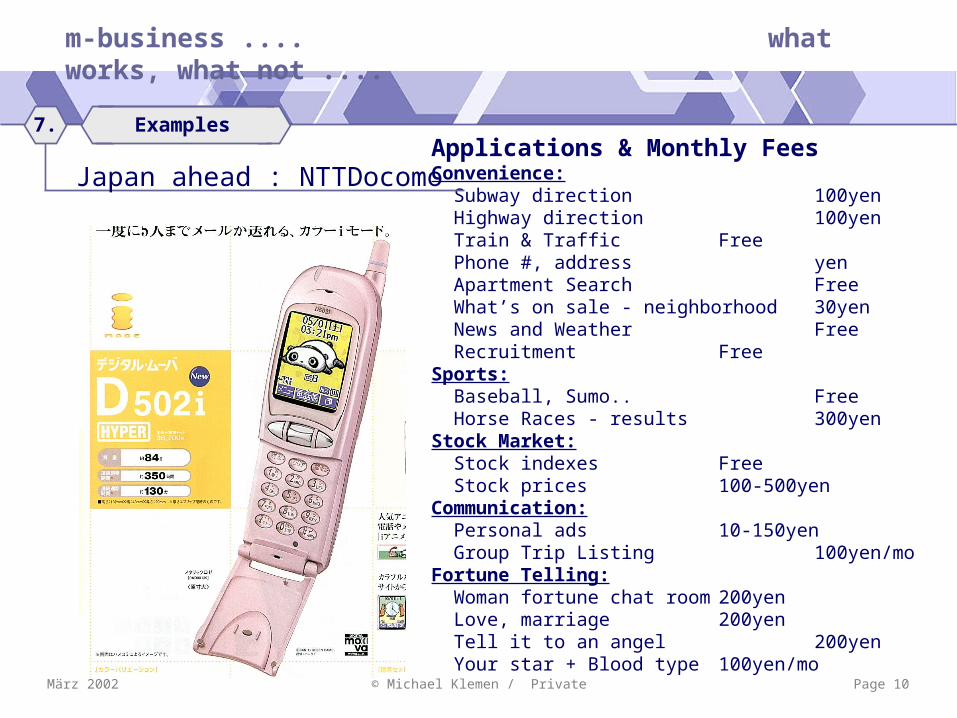

Applications & Monthly FeesConvenience: Subway direction 100yen Highway direction 100yen Train & Traffic Free Phone #, address yen Apartment Search Free What’s on sale - neighborhood 30yen News and Weather Free Recruitment FreeSports: Baseball, Sumo.. Free Horse Races - results 300yenStock Market: Stock indexes Free Stock prices 100-500yenCommunication: Personal ads 10-150yen Group Trip Listing 100yen/moFortune Telling: Woman fortune chat room 200yen Love, marriage 200yen Tell it to an angel 200yen Your star + Blood type 100yen/mo

Japan ahead : NTTDocomo

Examples7.

März 2002 © Michael Klemen / Private Page 11

m-business .... what works, what not ....

März 2002 © Michael Klemen / Private Page 12

m-business .... what works, what not ....

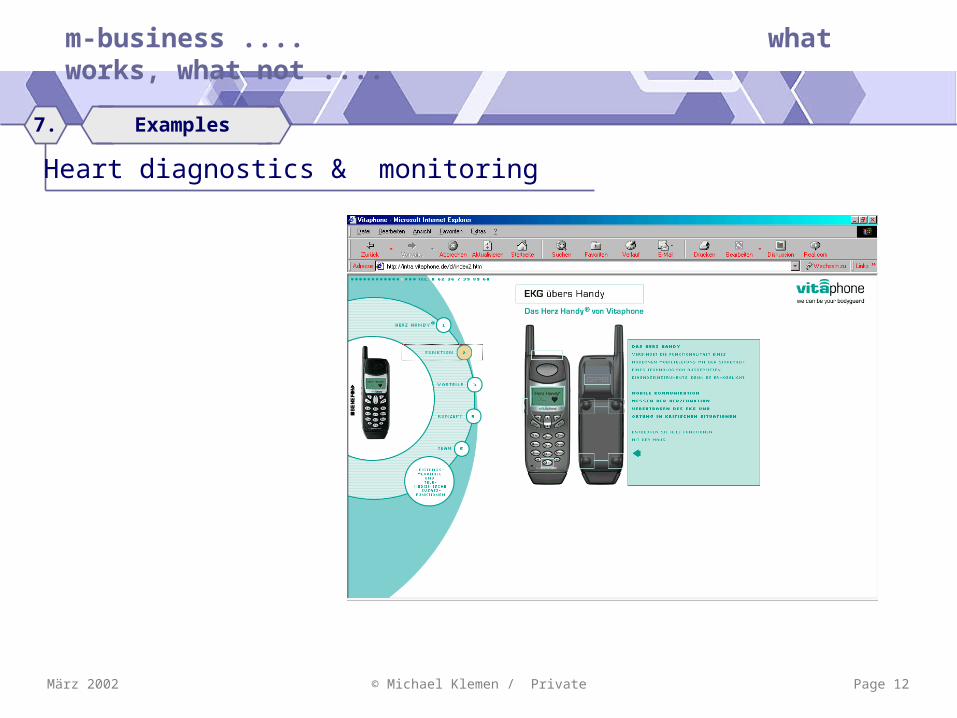

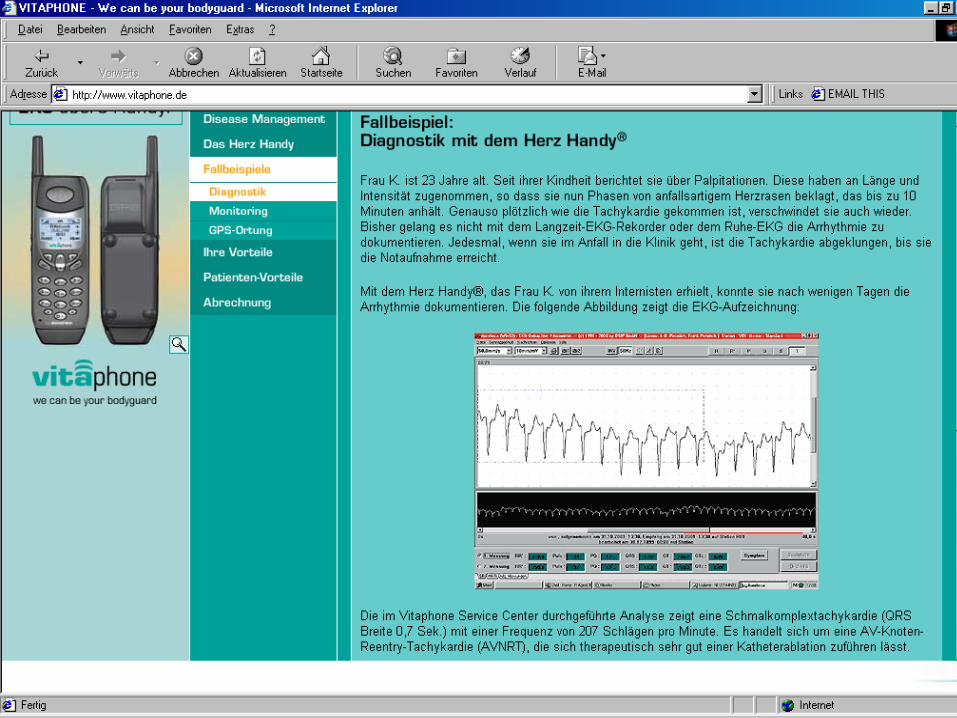

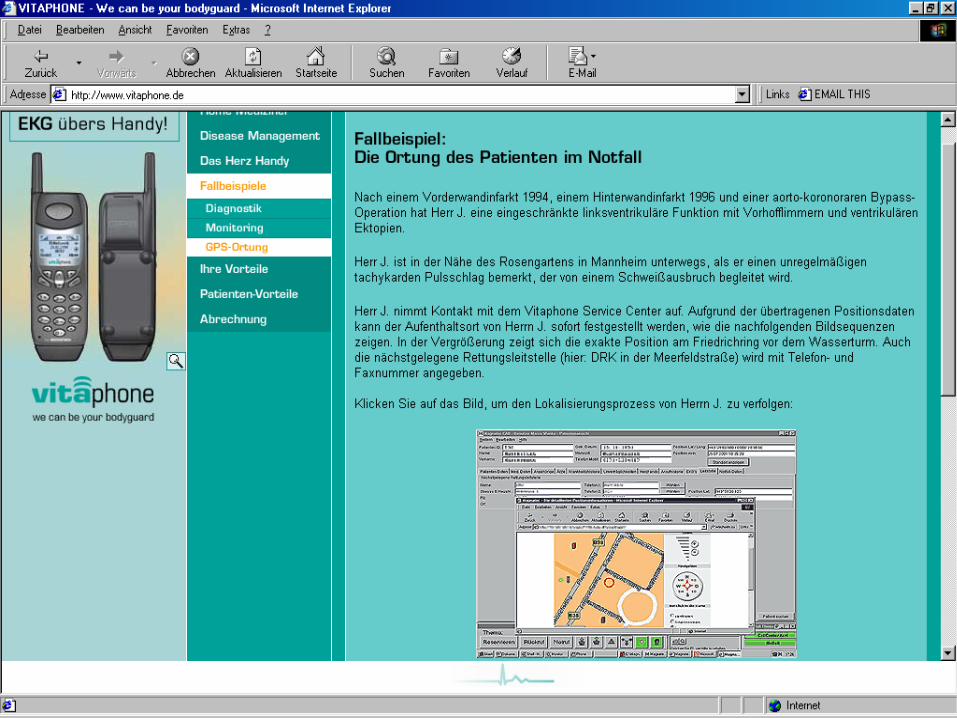

Heart diagnostics & monitoring

Examples7.

März 2002 © Michael Klemen / Private Page 13

m-business .... what works, what not ....

März 2002 © Michael Klemen / Private Page 14

m-business .... what works, what not ....

März 2002 © Michael Klemen / Private Page 15

m-business .... what works, what not ....

Conclusions

März 2002 © Michael Klemen / Private

m-business .... what works, what not ....

• Which user segments can best benefit?

• What user situations, tasks, problems can mobile improve?

• Which services should be applied to which device?

• Will users trust the services?

• Who will the user call when there is a problem?

• How does mobile deliver on corporate strategy & goals?

• What’s the business case? How big will this be?

• How can our brand extend to mobile?

• Who are the critical partners to pursue?

• Which technologies (HW & SW) are most suitable?

• What are the implications for back-end systems?

• Which vendors are best? How should they be evaluated?

• In-house vs. ASP?

• How can security be maintained?

Page 16

Users

Business

Technology

Conclusions9.

März 2002 © Michael Klemen / Private Page 17

m-business .... what works, what not ....

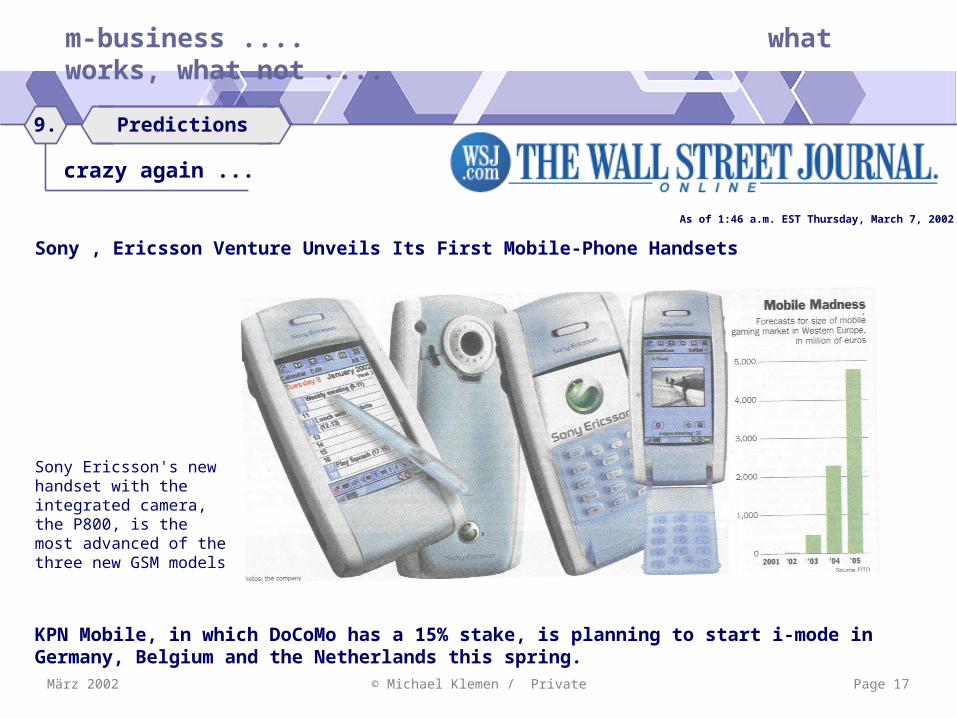

KPN Mobile, in which DoCoMo has a 15% stake, is planning to start i-mode in Germany, Belgium and the Netherlands this spring.

Sony Ericsson's new handset with the integrated camera, the P800, is the most advanced of the three new GSM models

Sony , Ericsson Venture Unveils Its First Mobile-Phone Handsets

Predictions9.

crazy again ...

As of 1:46 a.m. EST Thursday, March 7, 2002

März 2002 © Michael Klemen / Private Page 18

m-business .... what works, what not ....

Danke schön

![What Is Globalization?...Beck, Ulrich, 1944-[Was ist Globalisierung? English] What Is globalization? / Ulrich Beck; translated by Patrick Camiller. p. cm. Includes bibliographical](https://img.pdfslide.us/doc/110x75/60e156dac5cb390c48686bb3/what-is-globalization-beck-ulrich-1944-was-ist-globalisierung-english.jpg)