Embed Size (px)

Citation preview

Lux Redux: reshaping the Luxury sector Jean-Marc Bellaiche

May 1st, 2013

1 Luxury Redux-LuxuryRoundtable-1May13.pptx

What is luxury?

American Heritage

"Something inessential but conductive to pleasure and comfort. Expensive and hard to obtain"

Larousse

"Caractère de ce qui est couteux, raffiné, somptueux. Plaisir couteux qu'on s'offre sans vraie necessité" what is costly, refined and sumptuous. Expensive pleasure one can buy without true necessity

Wikipedia.it

"Abitudine a consumi di elevata gamma qualitativa e di coste. Spesso, superflui, destinati ad ornare il proprio corpo o la propria abitazione" Habit to consume high quality and expensive range. Rare, non-necessary products to ornate own body or home "必要な程度をこえて、物事に金銭や物などを使うこと。金銭や物などを惜しまないこと。 " To use money or things for a certain purpose above the necessary level. Not to spare money nor things Daijisen

"Indulgence in rich and sumptuous living" Collins

"внешнее великолепие, богатство, пышность . излишество в жизненных удобствах и удовольствиях, сопровождаемая расточительством изобилие, пышность"

External splendor, wealth, opulence. Extravagance in living comfort and pleasure, with a wasteful abundance ru.wiktionary. org

" ومتطورة المعيشة غالء من مكلفة االمور من تتكون التي البيئة " Environment which consists of expensive cost of living and sophisticated things

Baheth

"挥霍浪费钱财,过分追求享受" Extravagant waste of money, excessive pursuit of enjoyment

ZDIC

2 Luxury Redux-LuxuryRoundtable-1May13.pptx

The market as defined by consumers: 1.1T€

1,200

900

600

300

0 Total

~1,100

Travel , hotels,

yachting

300

Alcohol and food

60

Technology

110

Home & Furniture

60

Arts

65

Luxury cars

270

Cosmetic

35

Watch and jewellery

85

Leather goods and

accessories

50

Apparel

Estimation of market size in €B

50

1. Luxury car category not included in the survey. BCG estimate Source: IPSOS market research 2009–2011 (sample of 1000+ individuals from top 50% revenue quintile in mature countries (US, Japan, France, Italy, Germany, UK, Spain) and top 10% revenue quintile in emerging countries (China, Brazil, India, Russia...)

3 Luxury Redux-LuxuryRoundtable-1May13.pptx

Two main drivers of growth

1. High net worth individuals (investable assets > US $ 1 Mio.) Source: Dr. Ziems, Concept M; BCG analysis

New money

"The Loan Trader" The Russian

climber"

Old money

"The Noble Italian Entrepreneur"

7.5 M people 2.5 M people

30-35% of luxury market

10-15% of luxury market

Growth of number of Millionaires1

Rising middle class

"The proud business woman"

~ 70M people

25-27% of luxury market

Emergence of a middle class

Aspirational masses

"The trendy metropolitan"

~ 330 M people

25-27% of luxury market

4 New world of luxury-9Nov11-JMB-Par.pptx

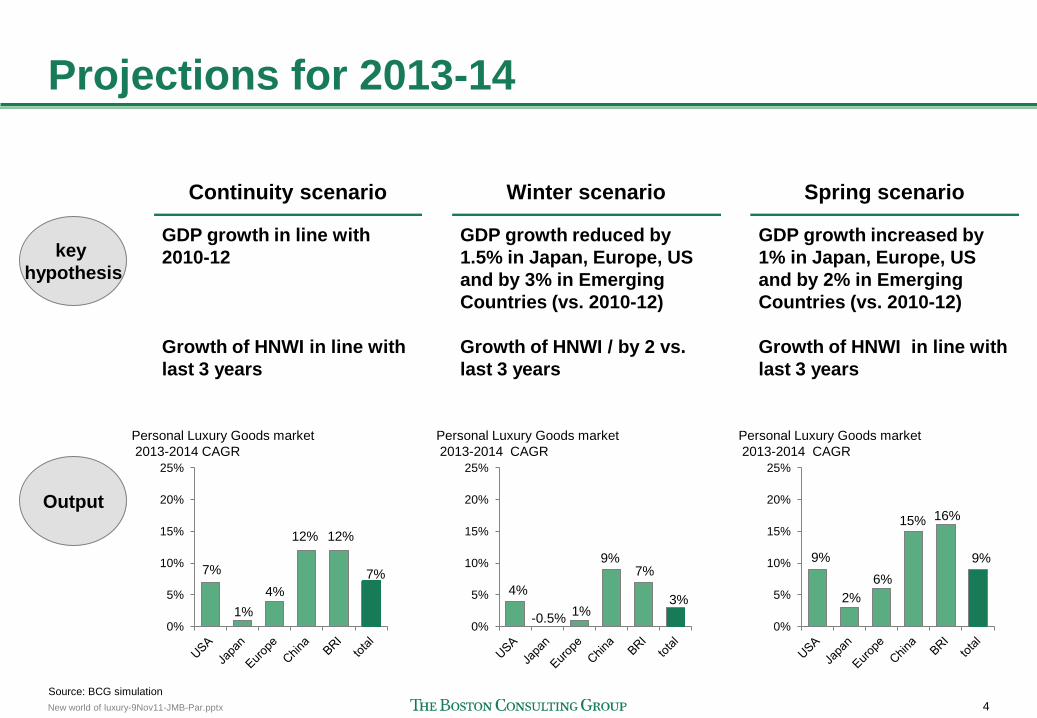

Projections for 2013-14

Continuity scenario

GDP growth in line with 2010-12 Growth of HNWI in line with last 3 years

Winter scenario

GDP growth reduced by 1.5% in Japan, Europe, US and by 3% in Emerging Countries (vs. 2010-12) Growth of HNWI / by 2 vs. last 3 years

Spring scenario

GDP growth increased by 1% in Japan, Europe, US and by 2% in Emerging Countries (vs. 2010-12) Growth of HNWI in line with last 3 years

key hypothesis

Output

0%

5%

10%

15%

20%

25%

Personal Luxury Goods market 2013-2014 CAGR

7%

0%

5%

10%

15%

20%

25%

Personal Luxury Goods market 2013-2014 CAGR

3%

0%

5%

10%

15%

20%

25%

Personal Luxury Goods market 2013-2014 CAGR

9% 7%

1% 4%

12% 12%

4%

-0.5% 1%

9% 7%

9%

2% 6%

15% 16%

Source: BCG simulation

5 Luxury Redux-LuxuryRoundtable-1May13.pptx

New rules of the game New World of Luxury

The new world of luxury Key trends that are changing the rules of the game

New consumer values: from "having" to "being"

from extrinsic to intrinsic, from conspicuous to meaningful

... and more segmented views

New epicenters of Luxury: Major rise of emerging

markets... and continuous potential

in mature ones

New business models (licenses, co-branding,

new retail formats...)

New platforms multiplication of

touchpoints, digitalization of the

brands

1

2

3 4

6 Luxury Redux-LuxuryRoundtable-1May13.pptx

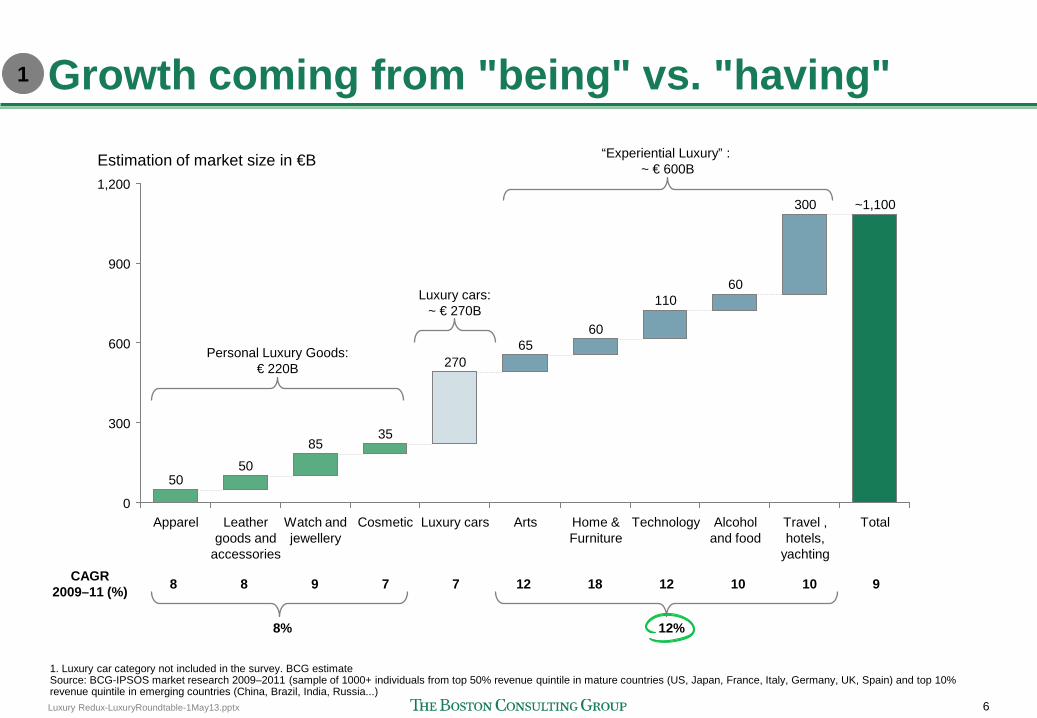

Growth coming from "being" vs. "having"

1. Luxury car category not included in the survey. BCG estimate Source: BCG-IPSOS market research 2009–2011 (sample of 1000+ individuals from top 50% revenue quintile in mature countries (US, Japan, France, Italy, Germany, UK, Spain) and top 10% revenue quintile in emerging countries (China, Brazil, India, Russia...)

1,200

Estimation of market size in €B

900

600

300

0 Total

~1,100

Travel , hotels,

yachting

300

Alcohol and food

60

Technology

110

Home & Furniture

60

Arts

65

Luxury cars

270

Cosmetic

35

Watch and jewellery

85

Leather goods and

accessories

50

Apparel

50

CAGR 2009–11 (%) 8 9 7 7 12 18 12 10 10

8% 12%

“Experiential Luxury” : ~ € 600B

Personal Luxury Goods: € 220B

Luxury cars: ~ € 270B

9 8

1

7 Luxury Redux-LuxuryRoundtable-1May13.pptx

Fundamental differences between luxury goods and luxury experiences

Experiential luxury Personal goods luxury

Having

For self only

Usually visible to other

For the mid-long term

Being

Often with others

Not always visible

Instant pleasure

Character-istics

Examples

Hybrid

• iPad • High-end kitchen • High end furniture • ....

Source: Internet research

• Luxury hotel or resorts

• High-end restaurant

• Spas...

• Watches with diamonds

• Jewelry • Bags, apparel • ...

1

8 Luxury Redux-LuxuryRoundtable-1May13.pptx

-40 8

-16 16 -16 13 -12 19

-12 19 -10 21

-18 23 -14 18 -10 21

-9 21 -11 17

-4 25 -6 24

-11 18 -9 20 -28 12 -6 32 -5 39 -20 16 -4 28 -6 27 -7 36 -3 35 -3 34

-6 33 -3 37

-4 40 -6 41 -3 47

Luxury values clearly challenged

More im

portant 1 Less im

portant 1

1. Than two years ago 2. Survey question: Below is a list of terms and values. For each, please indicate if this is something that you would see as being more or less important to you than it was two years ago 3. Respondents who ranked the term as equally important as two years ago have been excluded. Note: Graph excludes answer "no change"; EU includes EU Big5 (Germany, UK, Spain, Italy and France); Developing markets include Brazil, China, India, Russia; Bottom income quartile cut and sample reweighed to represent real income distribution in each country Source: BCG Global consumer sentiment survey 2011

US Japan EU 5

% of respondents2,3

-36 8 Bright colors -21 9

Conviviality -21 12 Altruism -14 13

Excitement -15 14 Professional success -22 19

Wealth -18 20 Change -10 20

Convenience -12 22 Local communities -7 22

Naturalness -8 22 Authenticity 3 24

Tradition -6 26 Craftsmanship -5 27

Religion -13 29 Education -11 30

Environment -9 32 Spirituality -10 33

Friends -3 34 Ethics -3

Luxury

Locally grown products -6 37 Calm -2 37

My home -3 38 Wellness -1 47

Family

36

48 Stability -1 52

Saving -2 58 Value for money -1 59

-50 5

Status

-1

-30 23 -8 48 -18 30

-11 39 -13 36 -12 37 -12 45

-7 52 -11 38

-5 48 -14 34

-9 37 -12 35 -10 36

39 -12 33

-7 44 -5

59

-5 56

29 -16 32

-7 56 -7 48 -8 42 -9

-19

42 -8

-2 62 -6 45 -5 57 -6 48

BRIC

25 0

-35 4 -12 9

-2 18 -8 20 -4 15

-8 16 -17 14 -1 33

-7 11 -4 21 -3 19 -3 25

0 31 -5 11

-9 12 -13

-1 44

-9

36

19 -1 30

-14 9 -3 24 -2 17 -3

5

23 -1 38 -3 25

0 55 -1 35 -1 39

-2

1

9 Luxury Redux-LuxuryRoundtable-1May13.pptx

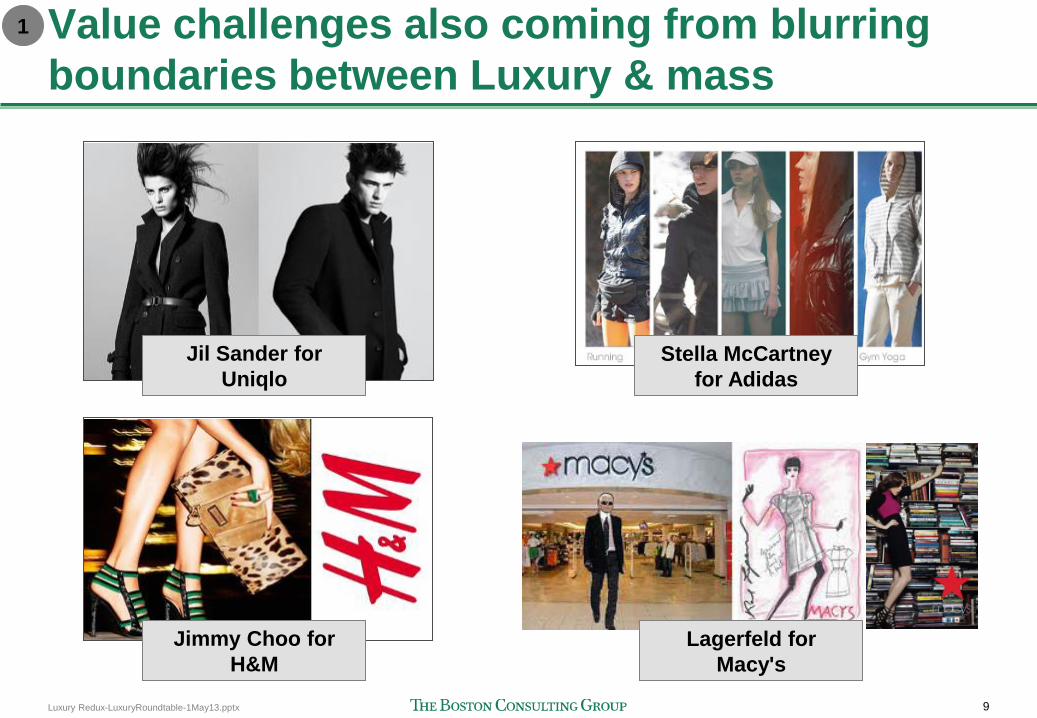

Value challenges also coming from blurring boundaries between Luxury & mass

Stella McCartney for Adidas

Jil Sander for Uniqlo

Jimmy Choo for H&M

Lagerfeld for Macy's

1

10 Luxury Redux-LuxuryRoundtable-1May13.pptx

Luxury brands adapting to new values: is it enough?

From sex to craftsmanship From extra-luxury to intro-luxury

Dior Couture, 2009-10 Dior Couture, 2002

Chanel N°5, 2001

Chanel N°5, 2009-10

LV, 2007

LV, 2009-10

Gucci, 2001

Gucci, 2009-10

Source: Press

1

11 Luxury Redux-LuxuryRoundtable-1May13.pptx

What new sense of purpose for Luxury? Improving every day's life of people Aesthetic/ art, quest for the beauty Craftsmanship, preservation of know-how Well-being and pleasure quest

Heritage, be part of the history

Performance, pushed to the limit

Learning/ cultural quest

Green (?)

1

LuxuryOutlook2012-China-21Feb13-NO-v2.pptx 12

Draft—for discussion only

Cop

yrig

ht ©

201

3 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Chinese Luxury consumption accounts for 120-130B€, heavily skewed towards "having"

Personal Luxury Goods

Cars

Experiential Luxury

Total

Chinese consumption (in and outside China)

~45 B€

~50B€

~30B€

~125 B€

Share of total market

20%+

20%

5%

12%

2

13 Luxury Redux-LuxuryRoundtable-1May13.pptx

More than 330 "Shanghais" in 10 yrs in China

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

# of cities

2020 city disposable income per capita vs. 2010 Shanghai level

RMB (2020 UDI/capita – 2010 Shanghai UDI/capita)

2020 Shanghai UDI/capita (RMB 38,024)

318 cities

332 cities

Source: BCG 2010 Urban Income Forecast Model

2010 Shanghai disposable income per capita (RMB 23,492)

2

14 Luxury Redux-LuxuryRoundtable-1May13.pptx

Very different segments of luxury consumers in China : Illustration of 3 segments

The successful entrepreneur

Mostly men 30-45 High assets, high income (e.g. >150k RMB) All cities Ostentatious, status oriented Low education on / knowledge of luxury brands Big spender Travel a lot Watches Cars Bags Self-purchase and gifts

The new comers

Men and Women All age Medium income (e.g. 60k RMB) Tier 3 and 4 cities Ostentatious, status oriented Low education on / knowledge of luxury, go for big brands Low tickets Do not travel much Cosmetics Accessories

The "Sugar 2" generation

Men and Women Younger High assets (inherited), income irrelevant (can be low) Tier 1 and 2 cities (mostly) Discernment, knows luxury brands, will go for niches Still status oriented, want to show Big spender Very hooked on the internet Travel a lot All categories including fashion, jewelry and more experiential categories (travel...)

Demographics

Luxury attitude

Main categories

2

15 Luxury Redux-LuxuryRoundtable-1May13.pptx

Uncontrolled licenses can hurt the brand 3

16 Luxury Redux-LuxuryRoundtable-1May13.pptx

Breaking compromises between Control and Openness

3

Openness

Control High Low

High

Low

17 Luxury Redux-LuxuryRoundtable-1May13.pptx

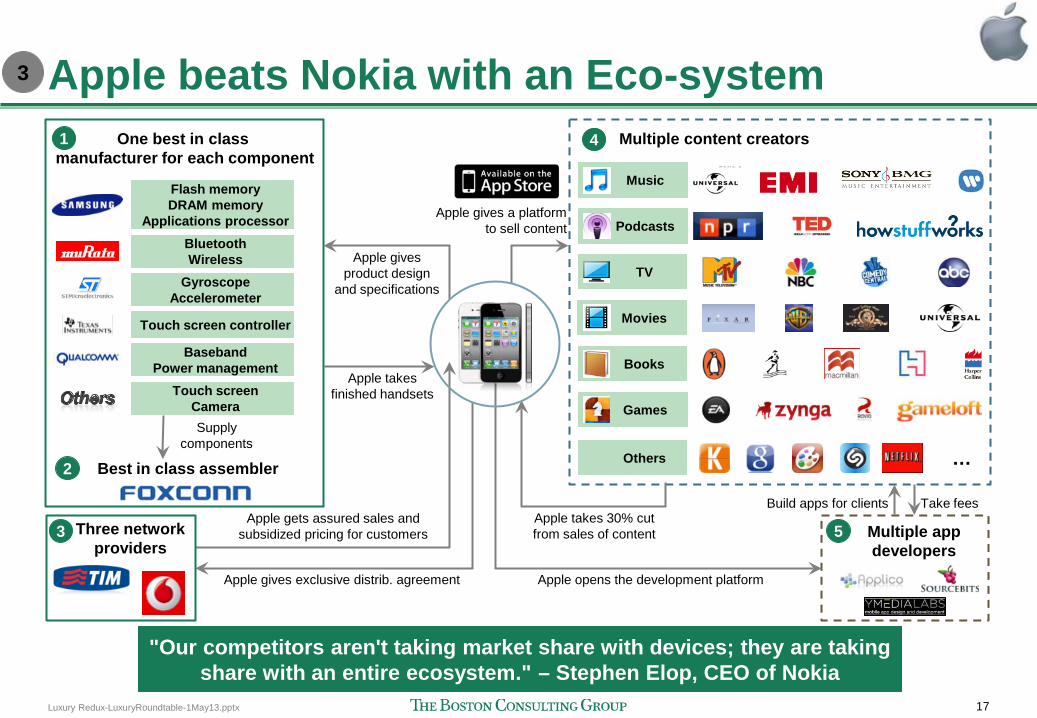

1

Flash memory DRAM memory

Applications processor Bluetooth Wireless

Gyroscope Accelerometer

Touch screen controller

Baseband Power management

Touch screen Camera

2

4

Music

Podcasts

TV

Movies

Books

Games

Others …

Multiple app developers

Apple gives product design

and specifications

One best in class manufacturer for each component

Apple takes finished handsets

Best in class assembler

Supply components

Apple gives exclusive distrib. agreement

Apple gets assured sales and subsidized pricing for customers

Multiple content creators

Apple opens the development platform

Build apps for clients Take fees

Apple gives a platform to sell content

Apple takes 30% cut from sales of content 5 3 Three network

providers

Apple beats Nokia with an Eco-system

"Our competitors aren't taking market share with devices; they are taking share with an entire ecosystem." – Stephen Elop, CEO of Nokia

3

18 Luxury Redux-LuxuryRoundtable-1May13.pptx

Examples of collaboration 3

Core processes

Product design Manuf. Sales Marketing/

Opinion building

Post sales/ CRM

Industria- lization

19 Luxury Redux-LuxuryRoundtable-1May13.pptx

Ecommerce and luxury: already a reality

Sales 2011(%)

100

0

Offline sales

Online sales

Estee Lauder(e)

Lancome US(e)

Coach(e) Tiffany Sephora

25

Macy’s1

9

Nordstrom

8

Neiman Marcus

16

Saks

25

80

60

40

20

Tory Burch(e)

1. Includes Bloomingdale's Source: Internet retailer, BCG Estimates

4

7-15%

20 Luxury Redux-LuxuryRoundtable-1May13.pptx

The best websites address the 3C's Example: New Sephora.com

Commerce

• Aesthetically pleasing with trendy homepage • Equipped with advanced product finder • Clear description of products and customer reviews • Layout easy to navigate, quick to buy products • Free shipping with purchases over $50 • Selection of three samples with every purchase • Products easy to return (online and offline)

Content

• Purchase history available • Product discussion forums • 'The Sephora Glossy' online magazine • 'Beauty Talk' forum with instant peer & professional advice • Sephora TV introducing & educating on new F&B products

• 'Beauty and the Blog' update on new products

Community

• On demand advice from peers and professionals • Active consumer forums linked to product reviews • 'Beauty Insider' membership community • Updated rich in content social media platforms

(e.g., Twitter, Facebook, Youtube, Pinterest, Instagram) • Pinterest pin button to easily pin products and images

Source: Sephora website, Retail interviews

4

21 Luxury Redux-LuxuryRoundtable-1May13.pptx

New competition between Brands & Dept Stores

...but Saks utilizes online technology to engage the customer with the product

Ralph Lauren presents the product authentically...

Women size guide

addresses potential hesitation to shop

online

Detailed product

description aids product positioning

Product reviews button enable

opinion seekers to engage and gather more information

Video and zoom used

to display product from all sides

Suggests additional Ralph

Lauren products to complete the silhouette

Clear display of

product brand

Limited viewing

options

No additional product

suggestions

Standard size

chart Short product

description

4

22 Luxury Redux-LuxuryRoundtable-1May13.pptx

New competition wit Amazon as well 4

+500 Cartier watches on sale on Amazon

Many reviews

Real price difference vs Cartier (-10 to 25%) Real price difference

vs Cartier (-10 to 25%)

Incomplete name of the product

1 click

Free shipping (prime)

Up to 9 e-retailers in the marketplace (Jomashop, WatchSaving,

Finebrand, PricePro, Certified Watch Store, Swiss Luxury...)

23 Luxury Redux-LuxuryRoundtable-1May13.pptx

Call for actions to our luxury clients 1. Don't consider it is back to normal. Things have changed in depth

2. Expand into new experiential categories vs traditional personal goods; boost

experiences as part of traditional offering

3. Reinvent new codes vs mass players, make sure you deliver a unique luxury value added and in product and experience

4. Stretch your pricing accordingly!

5. Invest to understand the aspirations /frustrations of various consumer segments

6. Attack specific segment e.g. women self-purchaser or senior segment

7. Do not forget to farm in mature countries while hunting in emerging ones. Chase the globetrotters from China, Brazil etc Build fully international executive teams (with senior talent from China)

8. Consider new business models, consider licenses and co-branding, while maintaining control; Develop new distribution format, create surprises at POS

9. Increase your bond with consumers; Develop more intimacy/ CRM

10.Create a real web presence for the brand (ecommerce, branding, blogs an social media etc); digitalize your brand! Up your ambition level online.