Embed Size (px)

Citation preview

Lunch and Learn

February 10, 2004

Crop Insurance UpdateGeorge Patrick

Crop Insurance Update

Topics1. Review of crop insurance

2. Risk management crop insurance and pre-harvest

pricing3. Crop insurance for hogs

Crop Insurance Alternatives

• Multiple Peril (Yield Insurance)– Actual Production History (APH)– Group Risk Plan (GRP)

• Multiple Peril and Price (Revenue Ins.)– Crop Revenue Coverage (CRC)– Revenue Assurance (RA)– Income Protection Plan (IPP)– Group Risk Income Protection (GRIP)

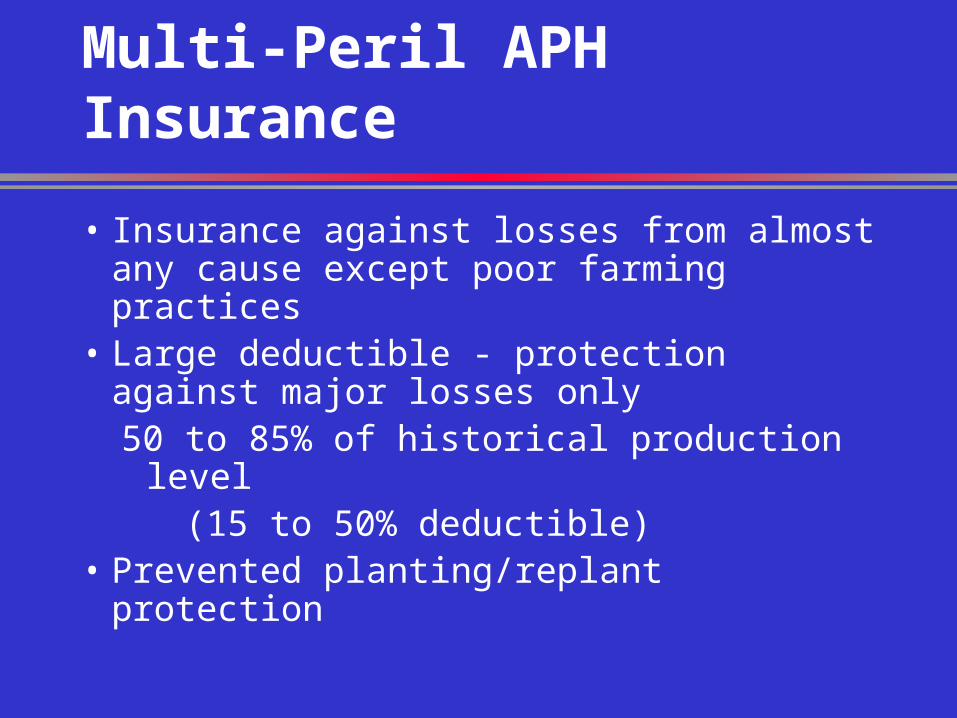

Multi-Peril APH Insurance

• Insurance against losses from almost any cause except poor farming practices

• Large deductible - protection against major losses only50 to 85% of historical production level (15 to 50% deductible)

• Prevented planting/replant protection

Multi-Peril APH Insurance

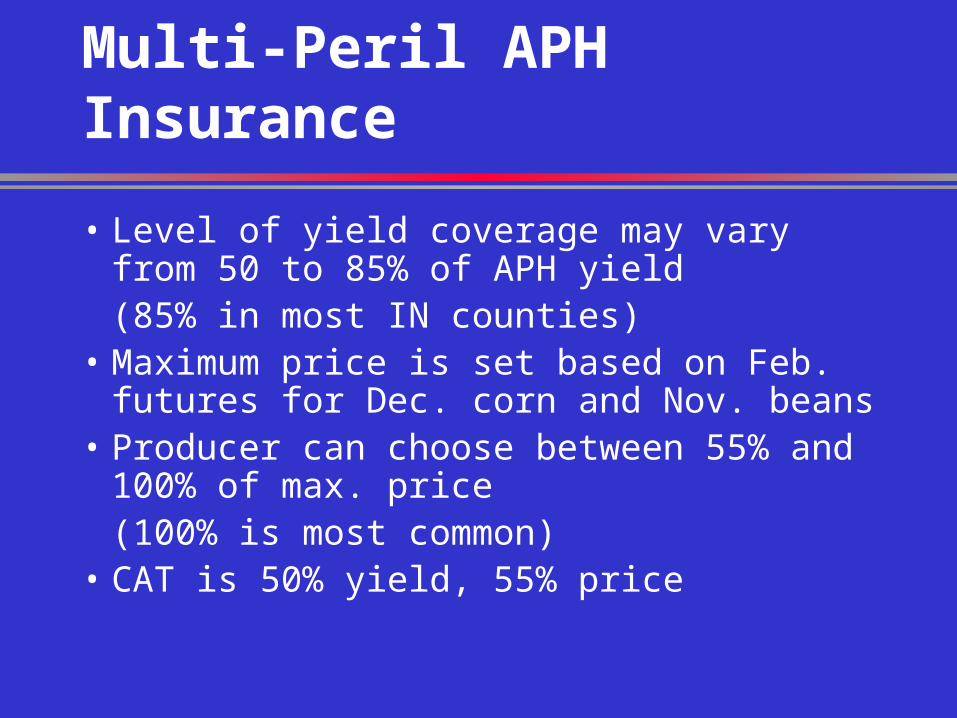

• Level of yield coverage may vary from 50 to 85% of APH yield

(85% in most IN counties)• Maximum price is set based on Feb.

futures for Dec. corn and Nov. beans• Producer can choose between 55% and

100% of max. price (100% is most common)

• CAT is 50% yield, 55% price

Multi-Peril Crop Insurance

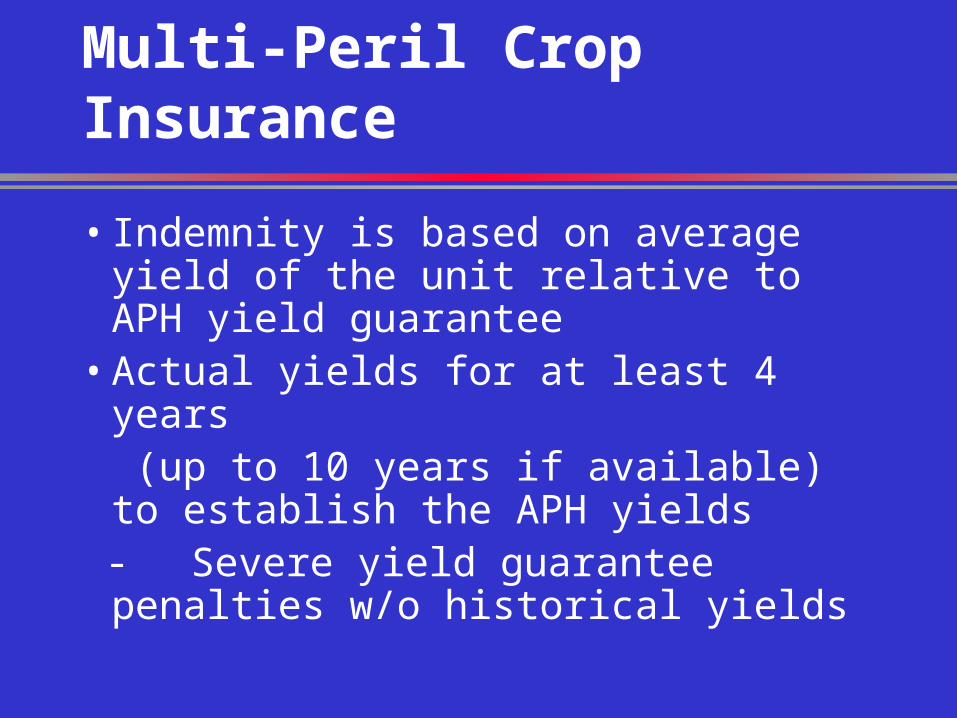

• Indemnity is based on average yield of the unit relative to APH yield guarantee

• Actual yields for at least 4 years (up to 10 years if available) to establish the APH yields

-Severe yield guarantee penalties w/o historical yields

Multi-Peril Crop Insurance

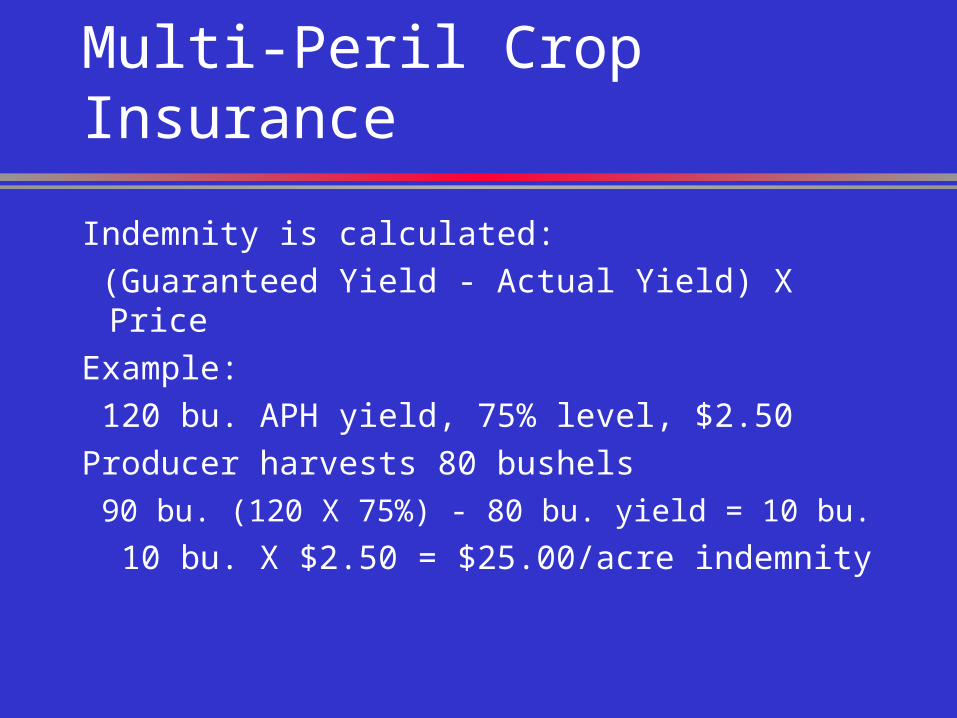

Indemnity is calculated:

(Guaranteed Yield - Actual Yield) X Price

Example:

120 bu. APH yield, 75% level, $2.50

Producer harvests 80 bushels

90 bu. (120 X 75%) - 80 bu. yield = 10 bu.

10 bu. X $2.50 = $25.00/acre indemnity

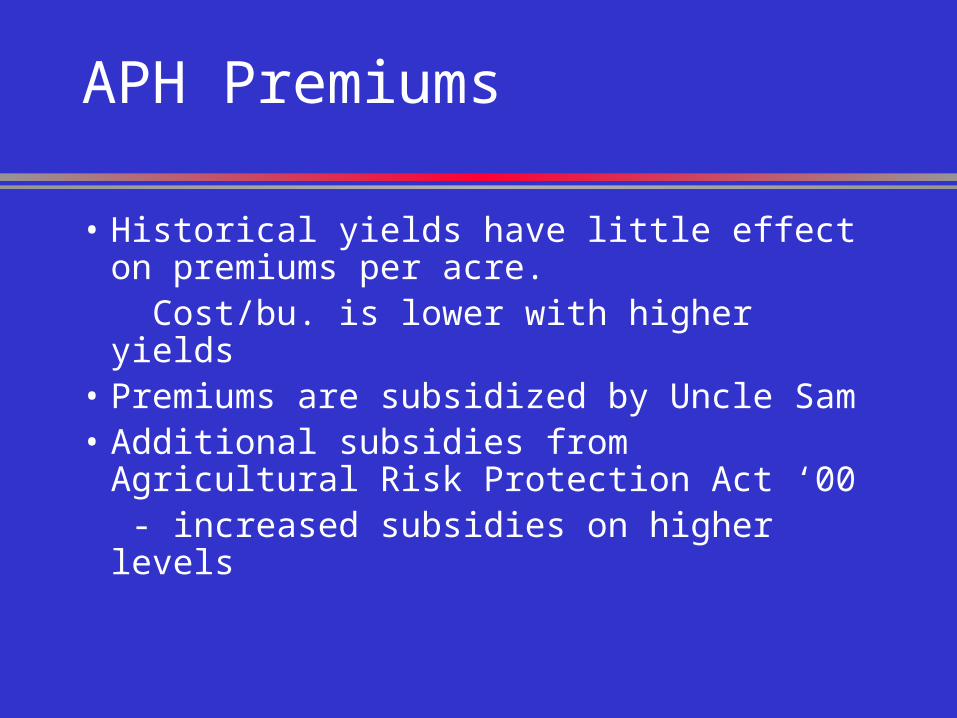

APH Premiums

• Historical yields have little effect on premiums per acre.

Cost/bu. is lower with higher yields

• Premiums are subsidized by Uncle Sam• Additional subsidies from Agricultural

Risk Protection Act ‘00 - increased subsidies on higher levels

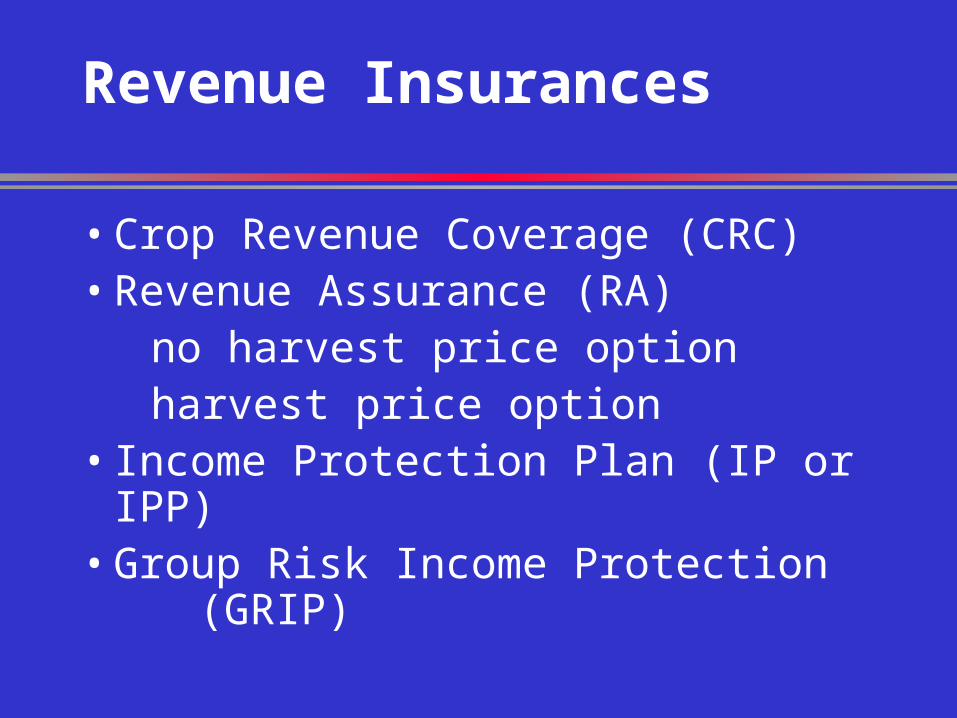

Revenue Insurances

• Crop Revenue Coverage (CRC)• Revenue Assurance (RA)

no harvest price optionharvest price option

• Income Protection Plan (IP or IPP)• Group Risk Income Protection

(GRIP)

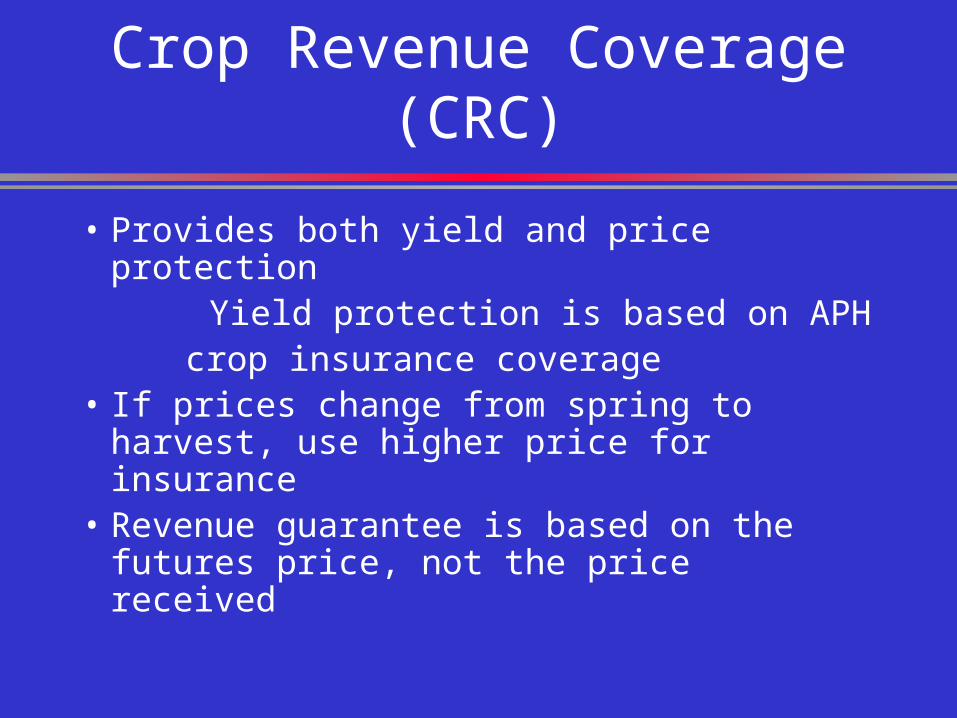

Crop Revenue Coverage (CRC)

• Provides both yield and price protection Yield protection is based on APH crop insurance coverage• If prices change from spring to harvest,

use higher price for insurance• Revenue guarantee is based on the

futures price, not the price received

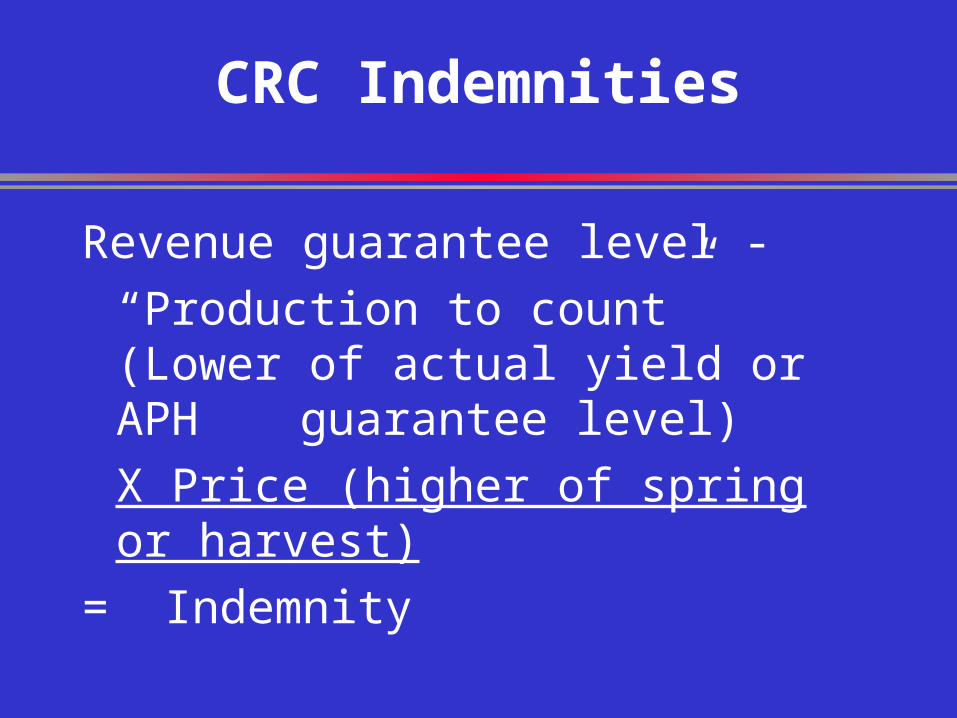

CRC Indemnities

Revenue guarantee level -

“Production to count” (Lower of actual yield or APH guarantee level)

X Price (higher of spring or harvest)

= Indemnity

Crop Revenue Coverage

Indemnities are triggered by shortfalls in revenue due to:

1. Low yields 2. Low prices 3. Combination of low prices and

yields• Premiums (both yield and price) are

subsidized

Revenue Assurance (RA)

• Generally similar to CRCNo harvest price option - uses spring priceHarvest price option - uses higher price

like CRC• Some differences in units from CRC

Generally larger units or combinations of enterprises

Check with insurance agent

Income Protection Plan (IPP)

• Similar to CRC - income coverage• If income falls below insured level, pays

an indemnity • Low yield/high price may result in no

indemnity if income level is above insured level

• Builds on the “natural hedge”Low yields generally have higher prices

• Premiums generally lower than APH

Group Risk Plan (GRP)

• Coverage is based on expected county yields and actual county yields

• Individual’s yield is not relevant• “Trigger level” - based on % of expected

county yieldRanges from 70 to 90% of exp. yieldCan insure up to 150% of county yield

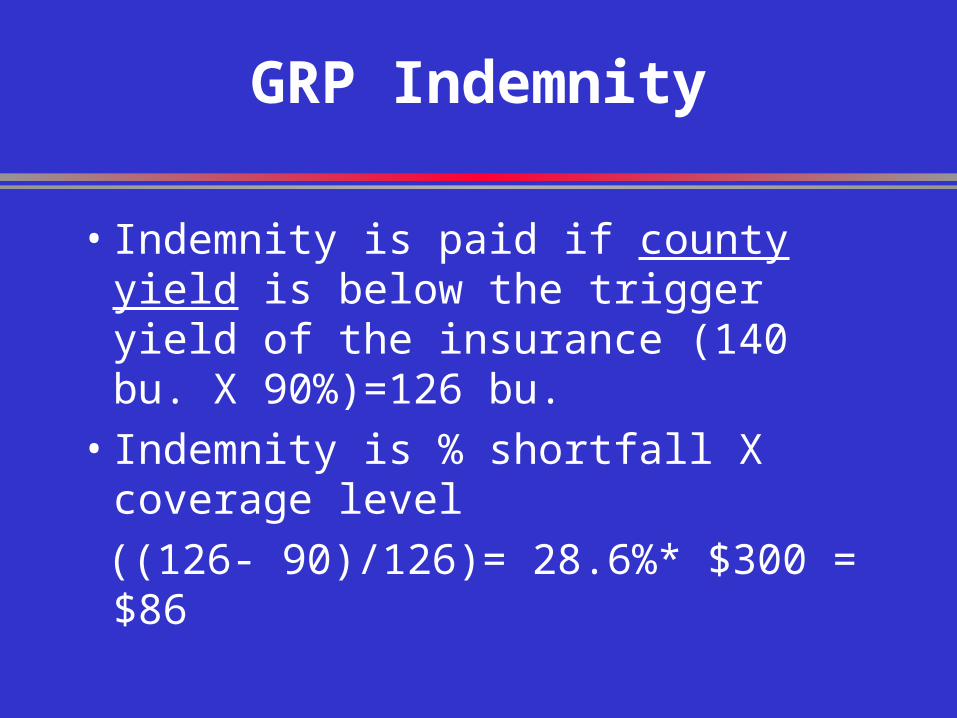

GRP Indemnity

• Indemnity is paid if county yield is below the trigger yield of the insurance (140 bu. X 90%)=126 bu.

• Indemnity is % shortfall X coverage level

((126- 90)/126)= 28.6%* $300 = $86

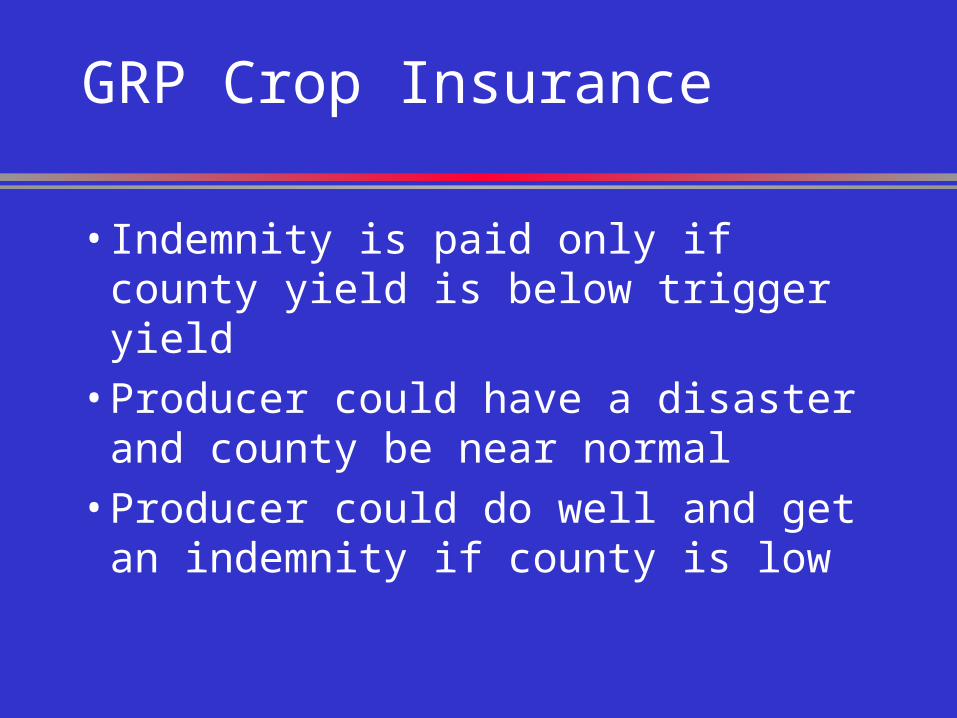

GRP Crop Insurance

• Indemnity is paid only if county yield is below trigger yield

• Producer could have a disaster and county be near normal

• Producer could do well and get an indemnity if county is low

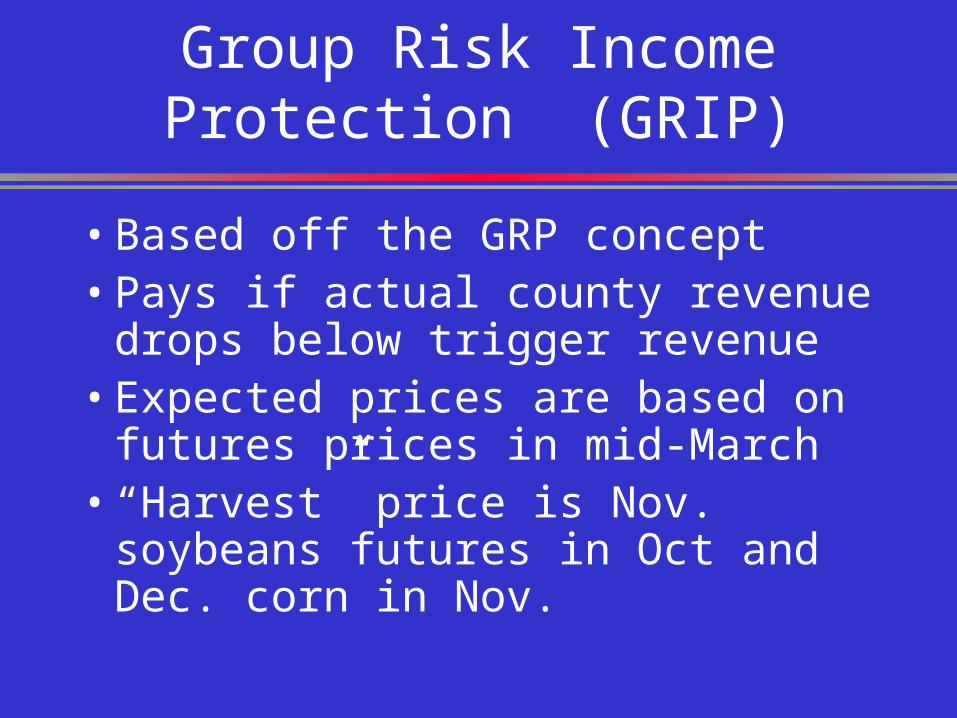

Group Risk Income Protection (GRIP)

• Based off the GRP concept• Pays if actual county revenue drops

below trigger revenue• Expected prices are based on

futures prices in mid-March• “Harvest” price is Nov. soybeans

futures in Oct and Dec. corn in Nov.

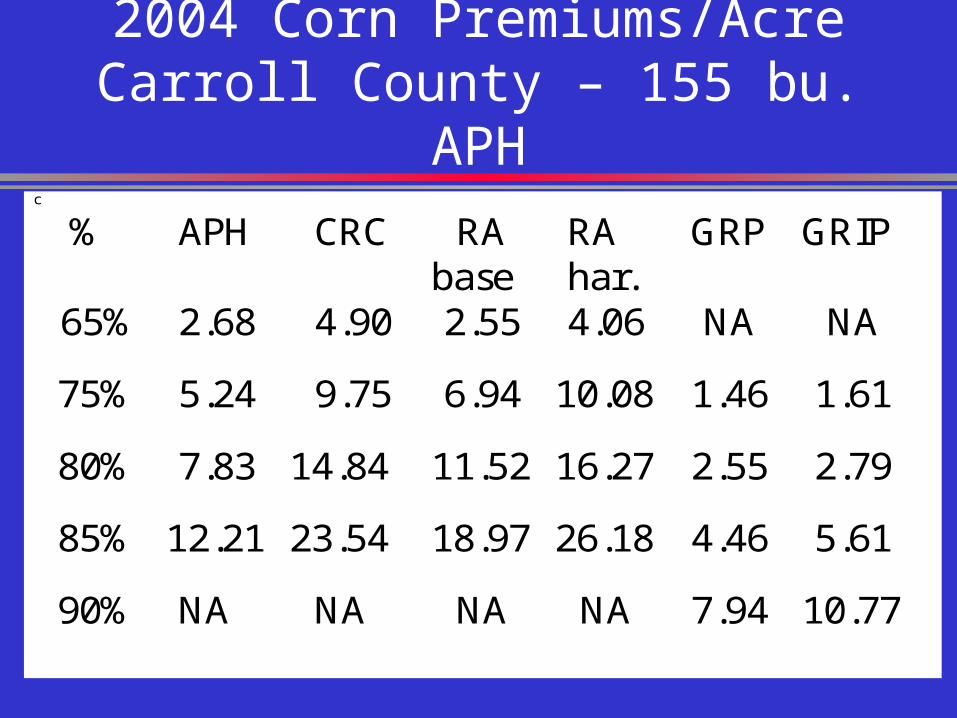

2004 Corn Premiums/AcreCarroll County – 155 bu. APH

c

% APH CRC RA base

RA har.

GRP GRIP

65% 2.68 4.90 2.55 4.06 NA NA

75% 5.24 9.75 6.94 10.08 1.46 1.61

80% 7.83 14.84 11.52 16.27 2.55 2.79

85% 12.21 23.54 18.97 26.18 4.46 5.61

90% NA NA NA NA 7.94 10.77

2004 Soybean Premiums/AcreCarroll County 51 bu. APH

c

% APH CRC RA base

RA har.

GRP GRIP

65% 1.99 3.49 2.12 2.94 NA NA

75% 3.87 6.89 5.80 7.62 1.15 1.29

80% 6.07 10.84 9.58 12.42 1.48 2.10

85% 9.68 17.48 15.72 20.13 2.46 3.47

90% NA NA NA NA 4.50 6.85

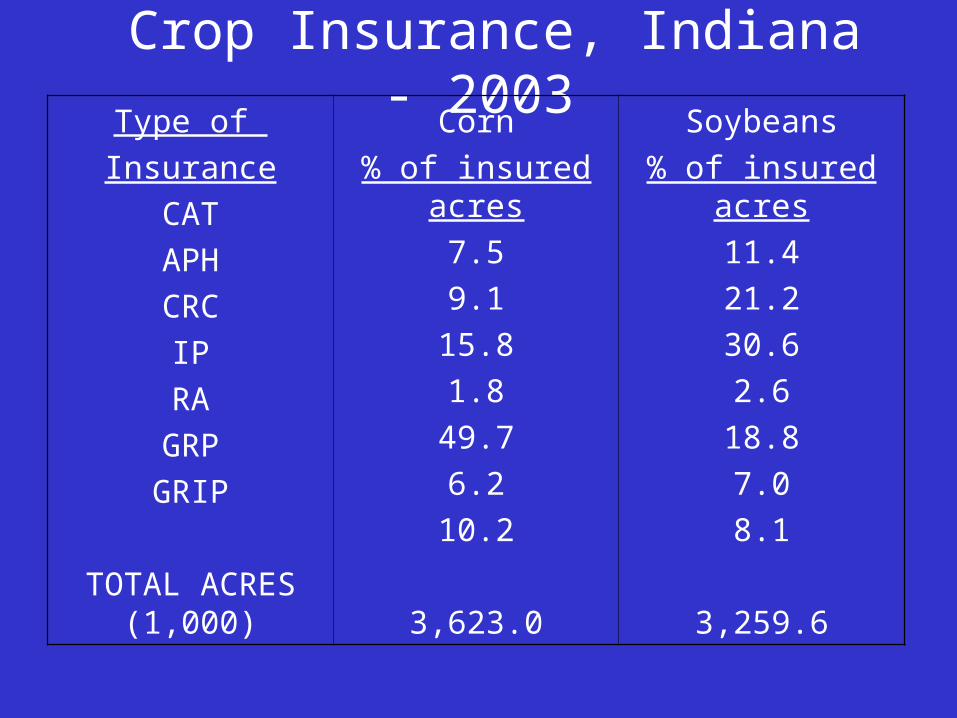

Crop Insurance, Indiana - 2003Type of

Insurance

CAT

APH

CRC

IP

RA

GRP

GRIP

TOTAL ACRES (1,000)

Corn

% of insured acres

7.5

9.1

15.8

1.8

49.7

6.2

10.2

3,623.0

Soybeans

% of insured acres

11.4

21.2

30.6

2.6

18.8

7.0

8.1

3,259.6

General Crop Insurance Information

Purdue Ag. Econ. Report

Sept. 2001 “Crop and Revenue Insurance Alternatives”

www.agecon.purdue.edu/

extension/pubs/paer/archives.asp

County Specific Information

www.farmdoc.uiuc.edu/cropins/1. Premium Calculator Specify county, crop and yield2. Insurance Evaluator

Specify county and crop Analyzes performance

Research Results

Carroll County farm 1986-2000

Excludes ’89,’92,’94 and ’96

- years following “short” crop have different price patterns

Benchmark - Cash sale at harvest with no insurance

Average returns after risk management costs

are subtracted

Value at Risk (VaR) Concept

5% VaR “Value at Risk” concept

• Measure of downside risk

95% of the time revenue will be greater than this amount (worst year in 20)

• Strategy with higher VaR is preferred if average revenue is the same

Figure 1. Average and 5% VAR Revenues of Top 10 Marketing Strategies as % of Cash Sale at Harvest

70

75

80

85

90

95

100

105

Puts100%

Mar 15

Puts 66%

Mar 15

Puts33%

Mar 15

Fut.100%

Mar 15

Fut.66%

Mar 15

For.Cont100%

Mar 15

For.Cont66%

Mar 15

Fut.33%

Mar 15

For.Cont33%

Mar 15

Fut.66%

Jun 15

Sal

e at

Har

vest

= 1

00

Average Revenue 5% VAR Revenue

Marketing Strategies

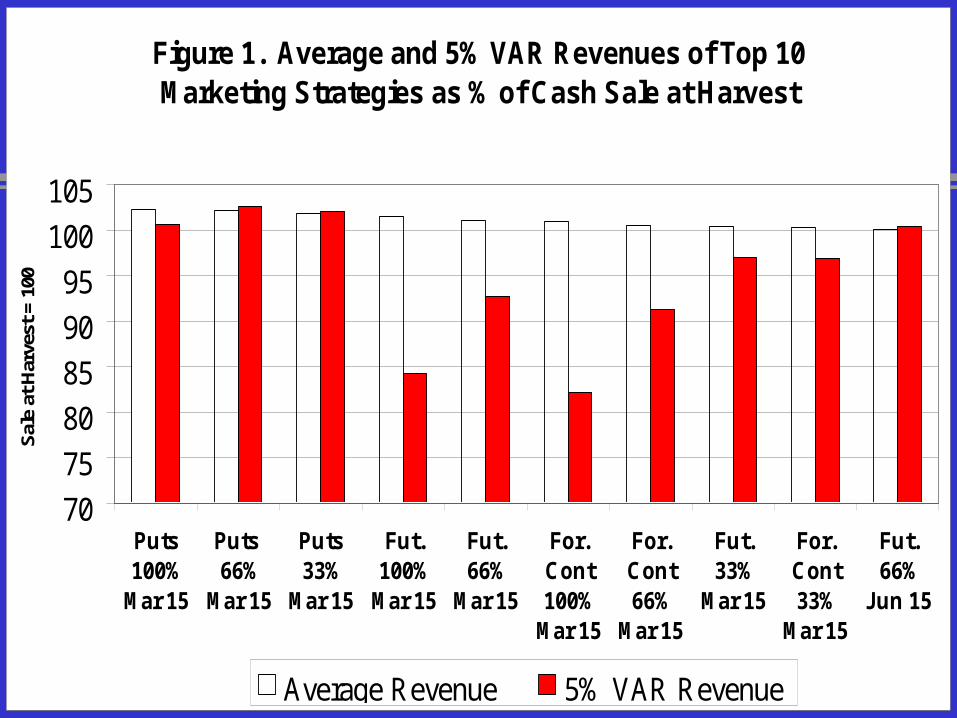

Using marketing strategies will keep average revenue high, but involves more downside risk than cash sale at harvest.

Marketing earlier in year generates a higher average revenue than later sales, but presents more downside risk. Does not work well in drought years.

Figure 2. Average and 5% VAR Revenues of Top 10 Insurance Strategies as % of Cash Sale at Harvest

85

90

95

100

105

110

115

120

125

APH 85% CRC85%

RA-BP75%

CRC75%

RA-HP85%

RA-BP85%

RA-HP75%

RA-HP65%

IP 75% CRC65%

Sal

e at

Har

vest

= 1

00

Average Revenue 5% VAR Revenue

Insurance Strategies

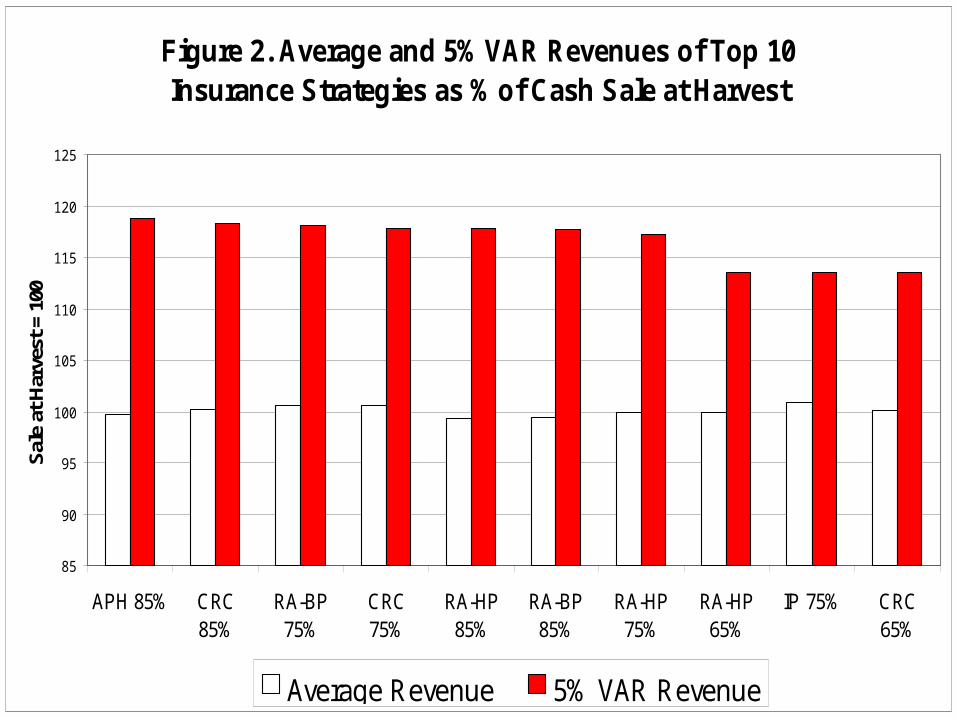

Insurance can reduce downside risk , but generally has a lower average return due to insurance premium

Individual insurances (i.e., APH and CRC) has greater downside protection than group plans but reduce avg. returns

Higher coverage levels -greater downside protection but reduce avg. returns

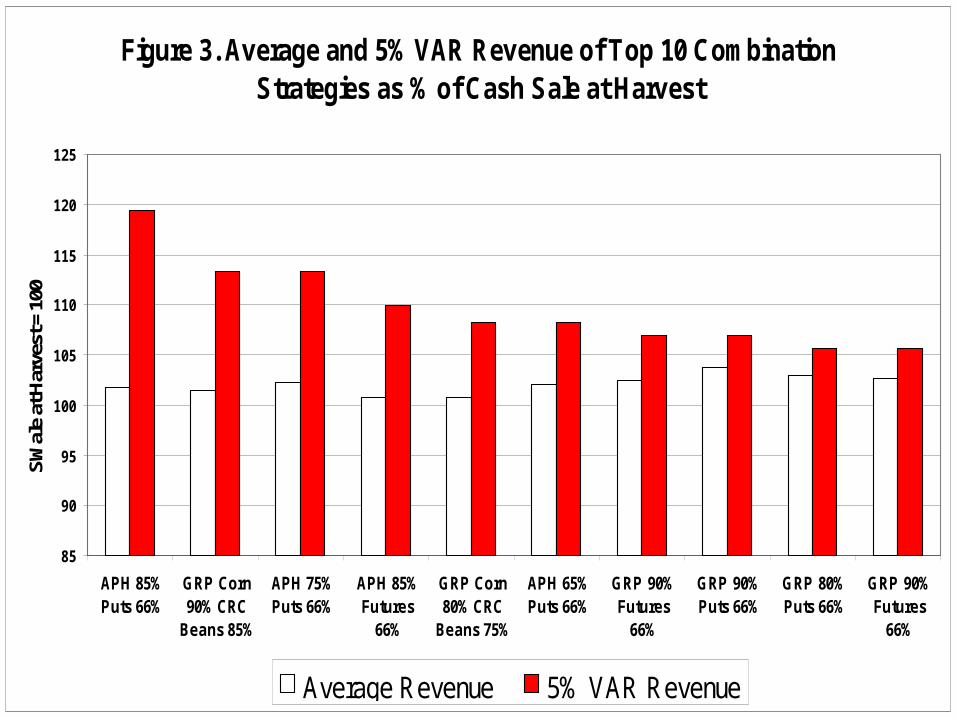

Figure 3. Average and 5% VAR Revenue of Top 10 Combination Strategies as % of Cash Sale at Harvest

85

90

95

100

105

110

115

120

125

APH 85%Puts 66%

GRP Corn90% CRC

Beans 85%

APH 75%Puts 66%

APH 85%Futures

66%

GRP Corn80% CRC

Beans 75%

APH 65%Puts 66%

GRP 90%Futures

66%

GRP 90%Puts 66%

GRP 80%Puts 66%

GRP 90%Futures

66%

SW

ale

at H

arve

st =

100

Average Revenue 5% VAR Revenue

Combination Strategies

Combination strategies, especially yield insurance and marketing tools, (synthetic revenue insurance) tend to have high revenue and 5% VaR

Synthetic revenue insurance requires more management than revenue insurance

Concluding Remarks

Trade-offs exist among all of risk management alternatives

BUT producers can increase average revenue and reduce downside risk relative to cash sales at harvest

Differences are relatively small

No ONE “best” strategy for all producers

Reference Material

“Protecting Farm Revenues with Pre-Harvest Pricing and Insurance”

Purdue Ag. Econ. Report

Dec. 2001 p. 5-12

www.agecon.purdue.edu/

extension/pubs/paer/archives.asp

Crop Insurance for Hogs

Livestock Risk Protection (LPR)

• Price protection only

• Can insure 70% to 95% of expected cash price over a 13 to 27 week production period

Crop Insurance for Hogs

• Very similar to an option – provides downside protection and does not limit upside potential

• 1 hog to 32,000 hogs annually

Advantages of LRP Coverage

1. More flexible than options or futures (quantity)

2. No margin calls

3. Premiums are subsidized

4. Simple to understand

5. Provides some basis protection

Disadvantages of LRP

1. Offers only price protection

2. Some basis risk

3. Specified settlement date whether hogs are ready

4. Use of futures/options restricted

5. Based on price outlook