Embed Size (px)

Citation preview

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 1/31

Real Estate and Portfolio Theory

Lecture Map – Review of Portfolio Management Theories

Asset allocation using the efficient frontier

Immunization and liability hedging

– Role of Real Estate in an Investment Portfolio

– Asset selection within the Real Estate Asset

Class What do institutions want from their real estate

investments?

Is there a „best way‟ to select real estate investments?

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 2/31

Real Estate Investing in the Context of

Portfolio Theory

Investing in real estate offers an ideal fit withportfolio theory

– Efficient Frontier → low correlation → diversification → fixed income and

appreciation attributes – Immunization → fixed income attributes

→ „alpha‟ enhancementopportunities

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 3/31

Portfolio Management Theories

Efficient Frontier Theory – Optimize combination of assets along the “efficient frontier”

to maximize returns relative to acceptable level of risk

– Diversify portfolio using mean variance theory to reducecorrelation of returns

Immunization Strategies

– Select base portfolio to cover projected stream of liabilities – Balance of the portfolio invested to enhance returns – i.e.,

increase “alpha”

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 4/31

The Efficient Frontier

In theory, investors should maximize returns at themargin for the amount of risk they are willing to bear

“Risk” in this case is measured by the volatility of

returns and the correlation - or lack thereof - of relative returns across asset classes

Assets are worth more in combination thanindividually if optimally combined based on thecovariance of their returns

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 5/31

Defining the Frontier

Frontier represents unique combinations of assets that optimizerisk adjusted returns

– i.e., optimal covariance between holdings in portfolio At each point along the Frontier, there are no “dominant”

portfolios – i.e., no portfolios that offer greater return given the risk level

Any other asset combinations either increase risk for same or lower returns, or decrease return for at least the same level of risk

Adding imperfectly correlated assets to a portfolio extends theefficient frontier to the NW, providing better reward to riskpayoffs – The lower the correlation, the greater the benefit of diversification

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 6/31

Portfolio Selection Using Mean

Variance Analysis

Start with the expected returns and the

covariance between the different assetclasses.

Find the mean-variance efficient portfolio of the different asset classes.

– If the expected returns of the different assetclasses change over time, asset allocationschange

– Investment managers in practice are continually

“re-balancing” their portfolios against the target

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 7/31

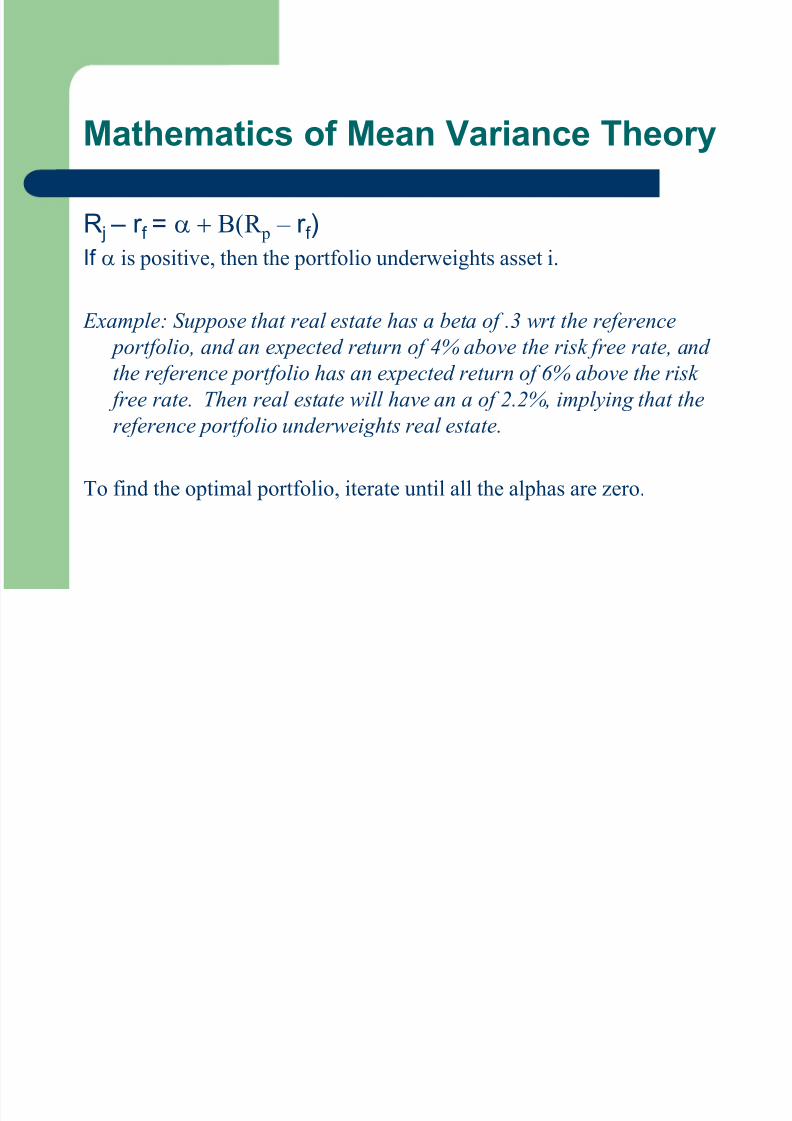

Mathematics of Mean Variance Theory

R j – r f = a + B(R p – r f )If a is positive, then the portfolio underweights asset i.

Example: Suppose that real estate has a beta of .3 wrt the reference

portfolio, and an expected return of 4% above the risk free rate, and

the reference portfolio has an expected return of 6% above the risk

free rate. Then real estate will have an a of 2.2%, implying that the

reference portfolio underweights real estate.

To find the optimal portfolio, iterate until all the alphas are zero.

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 8/31

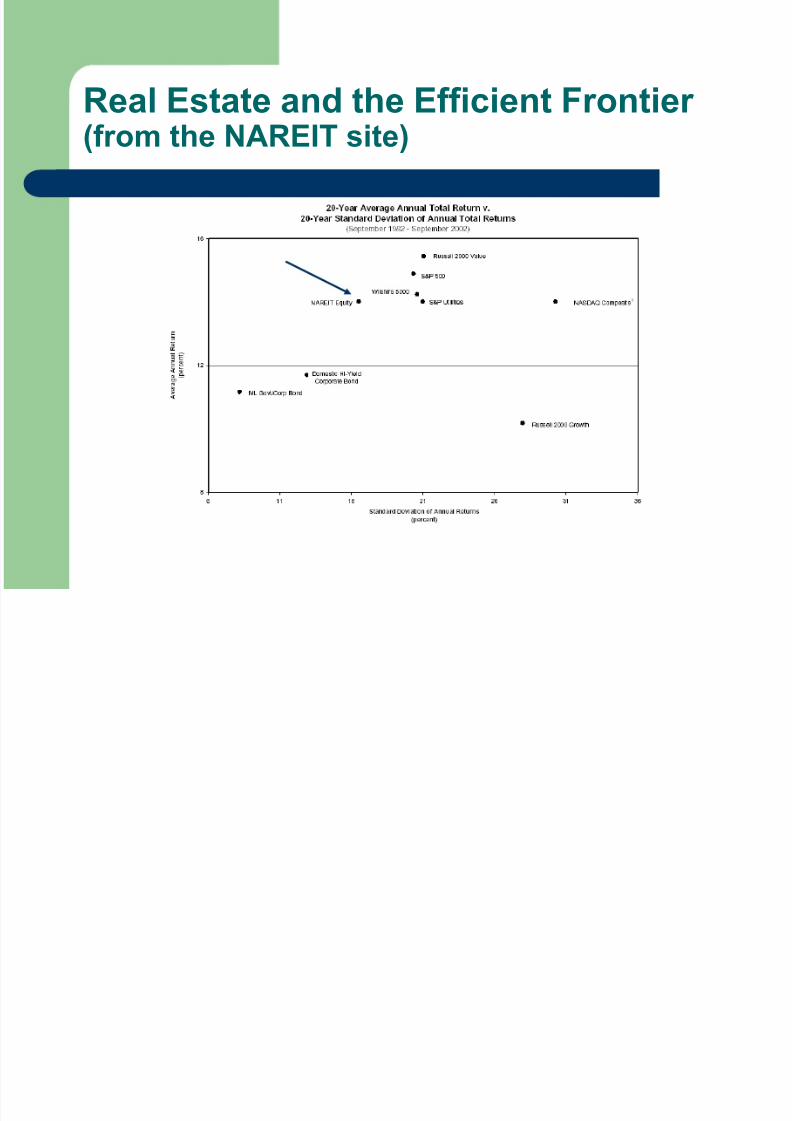

Real Estate and the Efficient Frontier

(from the NAREIT site)

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 9/31

CAPM and The Efficient Frontier

CAPM takes the risk adjusted return theory down to the assetlevel

If markets converge around risk/return expectations – themarket clearing price for assets – then only the relative risk of one asset versus others matters at the margin – Diversification should eliminate asset specific risk

– “Beta” management

Implies that all investors at any given risk level or return targetshould have basically the same assets in their portfolios at eachpoint along the curve

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 10/31

CAPM and Asset Allocation

Choosing the asset mix of your portfolio – Growth stocks – Value stocks – Fixed Income – Real Estate

Direct Commingled Funds REITs

Should the asset mix change over time? – Timing – Style Rotation

Does the CAPM really help with asset selection? – Especially with selecting real estate investments?

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 11/31

Special Challenges for Real Estate in

the Efficient Frontier Model

The mean variance asset allocation model suggests thatpension funds have been historically underweighting real estateand value stocks.

One theory is that these models ignore reinvestment risk.

– Suppose that expected rates of return on risky investmentsdecline.

– This causes asset prices to increase (which is good) butimplies that new investments will realize a lower rate of return (which is bad).

– Growth stocks tend to realize the highest returns in thesesituations, and thus provide the best hedge against areduction in reinvestment risk. Hence, growth stocksdeserve a higher allocation than implied by the mean

variance model.

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 12/31

Special Challenges for Real Estate with

the Efficient Frontier Model (cont.)

In practice, it is very difficult to measure covariances for realestate – A number of studies assume unrealistically low covariances for

real estate which result in very high allocations Versus the mean variance theory which traditionally has

underweighted real estate Historical data is not as robust as it is for stocks, bonds, making

measurement even more difficult

Private real estate markets are also fragmented, inefficient,illiquid – Some properties correlate well with bonds – single credit net lease

deals, multi-family – Others exhibit high volatility – hotels, suburban office – Performance can vary significantly between properties, markets

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 13/31

Another Challenge of the Mean

Variance Model

The mean variance model also ignores

pension liabilities. – Plan sponsors would like to generate income that

matches their liabilities.

– Liabilities are likely to increase with income

levels. – One might expect real estate returns to roughly

increase with increases in income, which wouldmake real estate more attractive than thepredictions of the mean variance model.

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 14/31

Real Estate, Re-Balancing the Portfolio

and the Efficient Frontier

Lack of liquidity in private real estate poses achallenge in re-balancing – Institutions favor direct deals that offer some

relative control over exit timing

Benchmarking against target returns andindexes is also problematic for real estate – Most targets are annual

– Most indexes are benchmarked quarterly

– Real estate is a long term asset!

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 15/31

REITS and the Efficient Frontier Model

Where do REITs fit in: are they really a differentasset class than real estate? – Need to also ask whether REITs are different than other

value stocks. The high allocation to REITs in some studiesignore the substitution between REITs and other valuestocks.

At least REITs offer the ability to build a long termdata base with the mark - to – market characteristicsof stock and bond indices – Should improve the analysis of REIT covariances over time

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 16/31

Portfolio Immunization

Investment strategy based on meeting planned and/or projected liabilities versus a target rate of return

Methodology splits the portfolio into two pieces: – Core investments indexed to liability streams

Generates income to match size, timing of liabilities Ties well with fixed income investments

– Balance of the portfolio invested to enhance total return Alternative assets, equities, etc. “Alpha” management

Works best with fully and/or overfunded pension plans – Underfunded plans are by definition behind the total return curve in

meeting even known liabilities – May need to take more risk to meet obligations

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 17/31

Portfolio Immunization (cont.)

Immunization is getting lots of attention in the

portfolio management world today: – “Post bubble” phenomenon

Institutional portfolios severely hurt by tech boom/bust

Portfolio discipline was missing in over-allocation totech, private equity and venture capital

Concern over looming obligations to retiring babyboomers

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 18/31

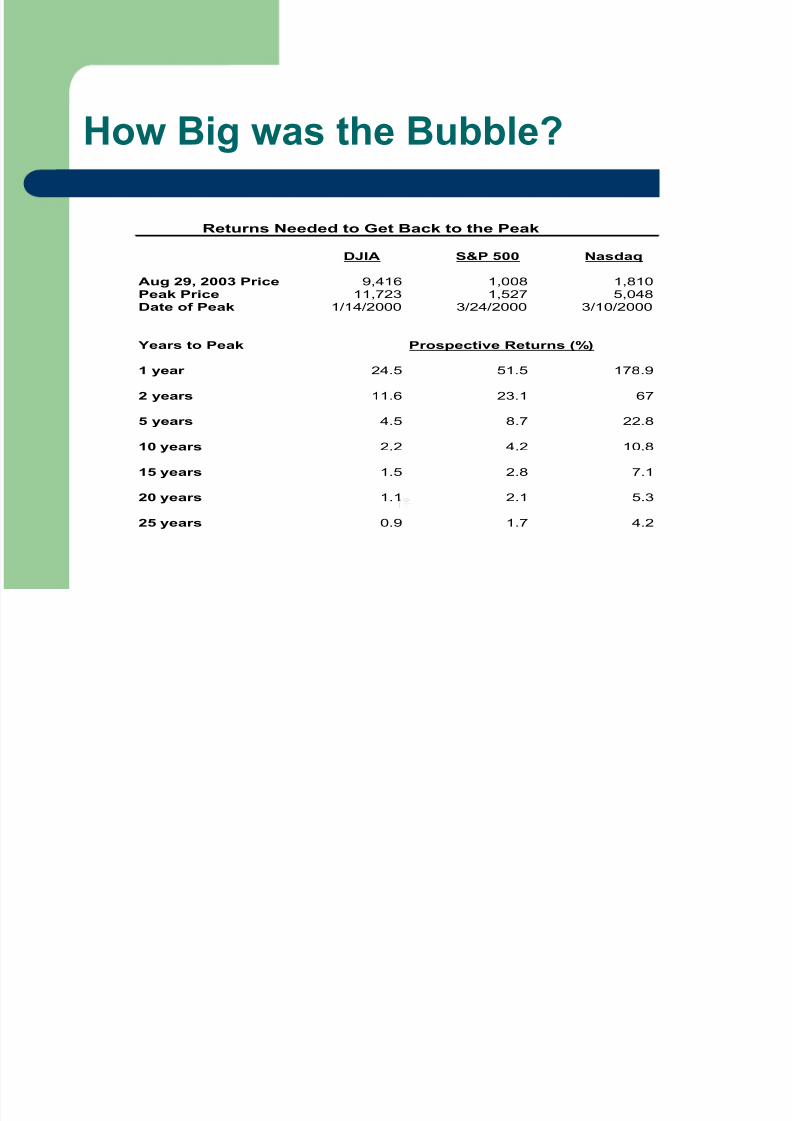

How Big was the Bubble?

D J I A S & P 5 0 0 N a s d a q

A ug 29, 2003 Price 9 , 4 1 6 1 , 0 0 8 1 , 8 1 0

Peak Price 1 1 , 7 2 3 1 , 5 2 7 5 , 0 4 8D ateofPeak 1/ 14/ 2000 3/24/ 2000 3/10/ 2000

Yearsto Peak Prospect i veR eturns (%)

1year 2 4 . 5 5 1 .5 1 7 8 .9

2years 1 1 . 6 2 3 .1 67 5years 4 . 5 8 .7 2 2 .8

10years 2 . 2 4 .2 1 0 .8

15years 1 . 5 2 .8 7.1

20years 1 . 1 2 .1 5.3

25years 0 . 9 1 .7 4.2

Returns Needed to Get Back to the Peak

DJIA S&P 500 Nasdaq

Aug 29, 2003 Price 9,416 1,008 1,810Peak Price 11,723 1,527 5,048

Date of Peak 1/14/2000 3/24/2000 3/10/2000

Years to Peak Prospective Returns (%)

1 year 24.5 51.5 178.9

2 years 11.6 23.1 67

5 years 4.5 8.7 22.8

10 years 2.2 4.2 10.8

15 years 1.5 2.8 7.1

20 years 1.1 2.1 5.3

25 years 0.9 1.7 4.2

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 19/31

Other Attractions of Immunization

Stop the proliferation of „asset classes‟ – Immunization would classify assets by their role in the

portfolio as opposed to role in diversification “what is the job” of each asset? Inflation hedge; current income; long term growth

– Addresses concern that covariance analysis may be lessrelative as the global economy gets more interdependent

– Will whole markets and asset classes become more

vulnerable to each other? How efficient is asset allocation today anyway?

– Look at real estate fundamentals vs. pricing – Are we creating another bubble of a different type?

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 20/31

Why Real Estate Looks So Good in the

Immunization World

Real estate combines return features of both bondsand stocks with low correlations to those asset

classes – Current income and total return – Same argument used by the efficient frontier model, but for

immunizers, the current income provides a hedge againstliabilities; growth component offers “alpha”

Real estate also offers multiple investment strategies

within the asset class to enhance alpha – Opportunistic plays – Property type and sector plays – Market selection

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 21/31

Does Immunization Work?(or, Does it Really Make Any Difference

Which Approach You Use?)

Does this strategy makes sense for portfolios that wereseverely damaged in the bust? –

Significant number of pension funds today are underfunded – Evidenced by stress on Pension Benefit Guarantee Corp.

Is the eventual portfolio outcome going to be that much differentunder this theory than under efficient frontier theory? – Both call for diversification

– Both require a minimum return target

– Both look to increase alpha on a relative basis, or against selectedbenchmarks

Can real estate be effectively used as an immunization tool?

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 22/31

Role of Real Estate in An Investment

Portfolio

Regardless of theory, widely agreed today that realestate should be a part of every investor‟s portfolio

Also generally agreed that investors are on averagesignificantly underweighted in real estate – Institutional universe has approximate 2% of assets in real

estate This small allocation still represents $80 billion in privates, $12

billion in REITS and REOC‟s

– Only the largest pension funds invest in real estate 25 largest funds control 74% of all pension fund investments in

real estate – Control 82% of all pension investments in REITs

– The rest of universe hasn‟t shown up for the party!

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 23/31

Institutional Real Estate Strategies

Involves Selection of Investment Vehicles andManagers

Primary Investment Vehicles: – Private Equity Real Estate Funds

Core

Value-Add

Opportunistic

– REITs Market proxies

Regional, property type plays

– Direct Deals

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 24/31

Institutional Real Estate Strategies

(cont.)

Implementation of any strategy is critically

dependent upon manager selection – Expertise and track record Deal experience

History of producing targeted returns

–

Transparency How good, frequent, honest is the reporting?

– Alignment of Interests Incentive-based reward structure

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 25/31

Institutional Real Estate Strategies

(cont.)

Institutions invest disproportionately inprivate, direct deals today – Public REIT markets, universe of private equity

funds too small to accommodate available capital

– Selection of, relationship with manager is key Real and/or perceived ability to influence operations and

outcome of the investment – Facilitates periodic rebalancing if needed

Less liquidity than a REIT, but more than a fund with agreater degree of control over the asset, exit timing

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 26/31

Real Estate Investment Strategies –

Moving Beyond the Vehicle

Real Estate provides multiple opportunities toenhance returns at the margin – “alpha” – in all

investment vehicles – Stage and/or strategy selection – Property type allocation – Regional allocation – Market Selection – Property Selection

What are the selection issues? – Correlation between strategies – Long term economic and demographic shifts

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 27/31

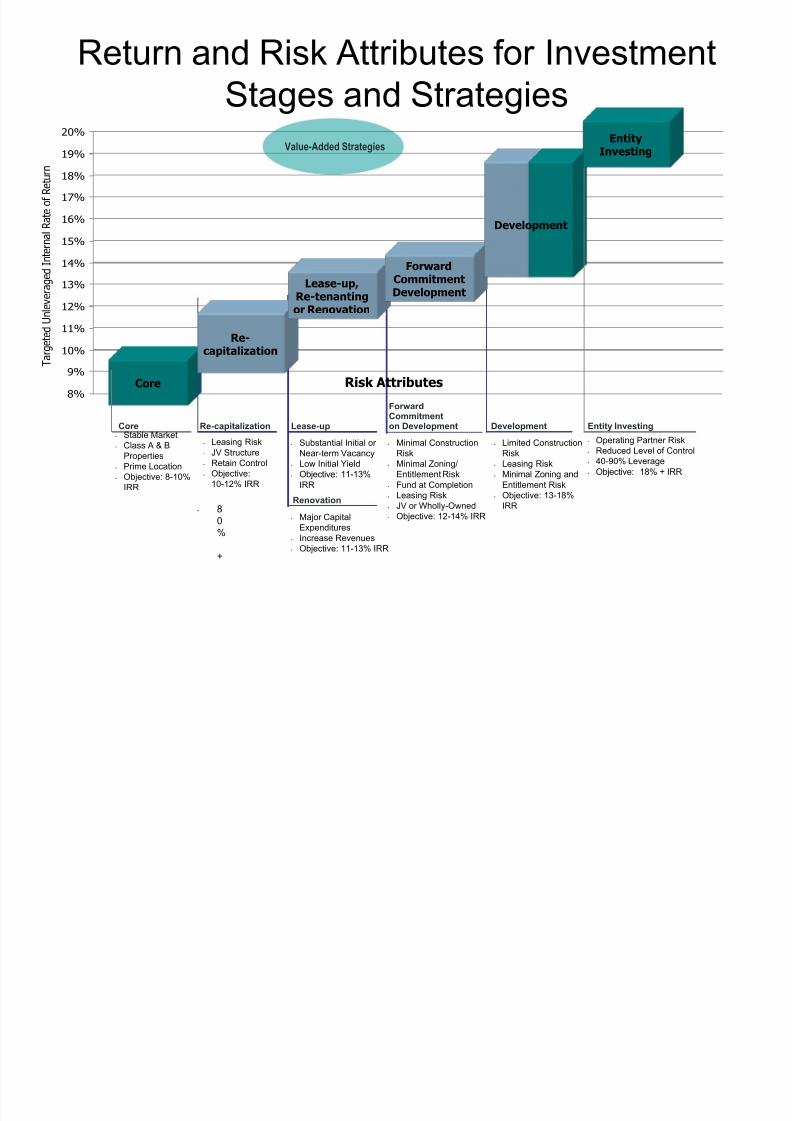

Return and Risk Attributes for InvestmentStages and Strategies

8%

9%

10%

11%

12%

13%

14%

15%

16%

17%

18%

19%

20%

T a r g e t e d

U n l e v e r a g e d

I n t e r n a l R a t e

o f R e t u r n

Core

Re-capitalization

Lease-up,Re-tenantingor Renovation

Forward

CommitmentDevelopment

Core Re-capitalization

Renovation

Lease-up

Forward

Commitmenton Development Development

• Stable Market• Class A & B

Properties• Prime Location• Objective: 8-10%

IRR

• 80%

+

• Leasing Risk• JV Structure• Retain Control• Objective:

10-12% IRR

• Substantial Initial or Near-term Vacancy

• Low Initial Yield• Objective: 11-13%

IRR

• Major CapitalExpenditures

• Increase Revenues• Objective: 11-13% IRR

• Minimal ConstructionRisk

• Minimal Zoning/Entitlement Risk

• Fund at Completion• Leasing Risk• JV or Wholly-Owned• Objective: 12-14% IRR

• Limited ConstructionRisk

• Leasing Risk• Minimal Zoning and

Entitlement Risk• Objective: 13-18%

IRR

Development

EntityInvesting

Entity Investing

• Operating Partner Risk• Reduced Level of Control• 40-90% Leverage• Objective: 18% + IRR

Risk Attributes

Value-Added Strategies

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 28/31

Property Type Allocation

Office and Industrial properties are most cyclical,most closely reflect economic cycles

– Office → either the best or the worst performer. A laggingindicator. Time the cycles, underweight suburban“commodity” deals in general

– Industrial → generally outperforms office, more stablereturns than office. More of a leading indicator.

Retail and Multifamily are considered more stable – Retail → negative correlation with office, good absolutereturns. Reflects consumer-driven economy – Multifamily → considered defensive, counter-cyclical.

Influenced by demographic trends as well as job growth

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 29/31

Regional Allocation

Property type selection within regions is important – Gets back to economic base analysis! – What industries, activities drive the local economy and will be reflected in

real estate needs? East and West

– Higher returns, higher risk – More heavily concentrated in office product because of the financial focus

of coastal economies

Midwest – Correlated with the East coast, although more heavily industrial in nature

South – Low correlations with West, higher risk adjusted returns on average than

either coast – Long term demographic shifts favor the south

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 30/31

Market Selection

Drivers of Market Selection: – Employment growth and comparative economic strength – Ease of adding new supply

– Historical absorption track record – Property preferences → which do better in given market?

International vs. National Markets: – Direct comparisons are difficult to make

U.S. market is a “traded” market; foreign markets are not Long term holds might favor stability of yield in W. Europe

– Does the recommended diversification model apply here? – Prologis strategy: provide U.S.-style service to customers in foreign

markets – Goldman approach: move opportunistically in and out of international

markets

7/28/2019 LS.real Estate and Portfolio Theory

http://slidepdf.com/reader/full/lsreal-estate-and-portfolio-theory 31/31

Property Selection

Pick your size – Smaller assets has historically outperformed larger assets

Wider audience offers greater liquidity

If your holding period is short, evaluated exit opportunity Pick within asset classes

– Suburban vs. CBD office CBD considered more stable

– Regional mall vs. power center vs. neighborhood center Neighborhood center in favor

– Flex R&D vs. distribution

Flex R&D is more cyclical – Garden-style multifamily vs. high rise, urban condominium

Garden-style considered more generic and defensive

– Full service, limited service, resort hotels Luxury full service most defensive, resort most cyclical