Embed Size (px)

Citation preview

Rob Reider

Do you want tooperate at theleast costs,

improve operationalefficiencies, andimplement best prac-tices at your firm? Doyou want to effectivelyincrease positiveresults and improve real profits?An operational review can helpyou do all these things.

The objective of this articleis to help you understand thebasic principles involved inplanning and conducting anoperational review, directedtoward the continual implemen-tation of best practices, in anorganized program of continuousimprovements. In addition, itwill provide the information andfundamentals you must know touse operational review conceptsto operate most economically,efficiently, and effectively. Thegoal is to maximize operatingresults at the least cost using themost efficient methods.

The materials presented inthis article can be used by topmanagement, supervisors, andother employees to performoperational reviews for theiroperational areas of responsibili-ty. In addition, the tools and

techniques presented can beused by othersÑsuch as internaland external consultants andauditorsÑto maintain operationsin the most economical, effi-cient, and effective manner.

WHY DO AN OPERATIONALREVIEW?

In todayÕs many-faceted andmultidisciplined economic envi-ronment, organizational manage-ment has placed an increasingemphasis on increasing resultswith fewer resources through theevaluation of the economy, effi-ciency, and effectiveness of theorganizationÕs operations. Theoperational review is the toolused to perform such an evalua-tionÑsingly or as part of anoth-er procedure, such as bench-marking, activity-based manage-ment, total quality management,reengineering, and so on. Thisarticle presents the basic princi-

ples of planning andconducting such anoperational review, aswell as the fundamen-tals needed for thereviewer to understandoperational reviewconcepts.

DO YOU HAVE HELPFUL SYSTEMS?

In many organizations today,top management is grasping forways to become competitive andmaintain market positionÑormerely to survive. Managershave sensed that many of theirorganizational systems are detri-mental to progress, and haveheld them back. These are thevery systems that are supposedto be helpful. For example:

1. Planning systems, long andshort term, that resulted indocumented plans but not inactual results.

2. Budget systems that becamecostly in terms of allocatingresources effectively andcontrolling costs in relationto results.

3. Organizational structuresthat created unwieldy hierar-chies, which produced sys-

Operational reviews can help your company oper-ate at the least costs, improve operational effi-ciencies, implement best practices, and boost realprofits. The author, an acknowledged expert in thearea, reveals how to do operational reviews thatreally pay off for your firm. © 2000 John Wiley & Sons, Inc.

Looking Beyond the Numbers: DoingOperational Reviews that Get Results

featu

reartic

le

25© 2000 John Wiley & Sons, Inc.

tems of unnecessary policingand control.

4. Cost accounting structuresthat obscured true productcosts and resulted in pricing that constrainedcompetitiveness.

5. Management systems thatproduced elaborate computersystems and reporting with-out enhancing the effective-ness of operations.

6. Sales functions and forecaststhat resulted in selling thoseproducts that maximizedsales commissions but maynot have been the productsmanagement desired to selland produce.

7. Operating practices thatperpetuated outmodedsystems (ÒweÕve alwaysdone it that wayÓ)rather than promotedbest practices.

Operational reviews,together with other tech-niques, are tools to makethese systems helpful asintended and direct the organiza-tion toward its goals.Theoretically, organizationsshould operate in an economic,efficient, and effective manner atall times. If such was the case,operational review techniqueswould be applied on an ongoingbasis. However, with the passageof time, good intentions and ini-tially helpful systems tend todeteriorate. Operational reviewsare then necessary to help getthe organization back on trackby pinpointing operational defi-ciencies, developing practicalrecommendations, and imple-menting positive changes.

SETTING MANAGEMENTRESPONSIBILITY

Managers at all levels shouldbe held accountable for using the

scarce resources entrusted to themto achieve maximum results at theleast possible costs. Althoughmanagement should embraceoperational review concepts andapply them as they proceed, thisis rarely the case. More typically,management needs to be sold onthe value of operational reviews.

In selling the benefits of con-ducting operational reviews, it isimportant to stress that, unlikeother techniques that cost timeand money for uncertain results,operational reviews pay for them-selves. In effect, the operationalreview environment becomes aprofit center instead of a cost cen-

ter. Although there are no guaran-tees, a successful operationalreview should result in at leastthree to four times its cost inannual savings. These are notone-time savings, but ongoingÑthat is, savings year after year.With the success of an operationalreview, management quickly real-izes that the more operationalreviews done, and the more rec-ommended economies and effi-ciencies implemented, the greaterthe savings and results. In addi-tion, the residual capability forperforming operational reviewsremains in the area under reviewso operations personnel can con-tinue to apply operational reviewconcepts on an ongoing basis.

Keep in mind that the intentof the operational review is notto be critical of present opera-tions but to review operations

and develop a program of bestpractices and continuous positiveoperational improvements byworking with management andstaff personnel. This can beaccomplished most effectivelyby working with operations per-sonnel in areas where they rec-ognize deficiencies and are will-ing to cooperate. The concept ofoperational reviews should besold as an internal program ofreview directed toward improvedeconomies and efficiencies thatwill produce increased opera-tional results.

WHO IS THE OPERATIONALREVIEWER?

An operational reviewcan be performed by any-one with the appropriateskills. However, internaland/or external consultants,because of their knowledgeof the operations and theiranalytical skills, are typical-ly requested to performsuch services. In some

organizations, a separate opera-tional review unit trained in oper-ational review concepts is estab-lished. The most effective way inwhich to implement such proce-dures is to assign overall respon-sibility for implementing organi-zationwide operational reviewprocedures, which would includethe performance of operationalreviews as well as training opera-tions personnel in implementingthese techniques in their areas.

The progress and ultimatesuccess in achieving the benefitsof operational reviews dependgreatly on the reviewersÕ skillsand what management and oth-ers think of them. Thoseassigned to an operationalreview engagement must possessthe ability to review and analyzefinancial, management, andoperational areas. The attributes

26 The Journal of Corporate Accounting & Finance

© 2000 John Wiley & Sons, Inc.

In selling the benefits of conductingoperational reviews, it is importantto stress that, unlike other tech-niques that cost time and money foruncertain results, operational reviewspay for themselves.

of an effective operationalreviewer include the following:

1. The ability to spot the troubleareasÑto look at a given situ-ation and quickly determinewhatÕs getting in the way.

2. The ability to identify thecritical problem areas, so asto avoid chasing mice whenone should be chasing ele-phants. The application of the80/20 rule states that opera-tional reviews require 80 per-cent common sense and 20percent technical expertise;and that 80 percent of thetrouble areas cause 20 percentof the problems, and that 20percent cause 80 percent ofthe problems.

3. The ability to place oneself inmanagementÕs position toanalyze the problemand ask questions frommanagementÕs perspec-tive. This is sometimesdifficult, as many timesthe reviewer has neverbeen in an operational-related managementposition. Even whenthis is not true, thereviewer may have difficultyunderstanding the constraintsunder which the managermust workÑin effect, whatthey can and canÕt do.

4. The skill to effectively com-municate operational reviewresults. The success of youroperational review is meas-ured by the degree withwhich your recommenda-tions are implementedÑandimplementation is a directby-product of effectivecommunication. A rule ofthumb in operationalreviews is that you havebeen successful if you canconvince management toadopt more than 50 percentof your recommendations.

Success as an effective opera-tional reviewer is based on whatis accomplishedÑthat is, recom-mendations made to managementthat are subsequently implement-ed. Operational reviews should befascinating and rewarding to thereviewer as well as operationspersonnel. The individualÕs statureas an operational reviewer, credi-bility of the entire review staff,managementÕs and othersÕ posi-tive regard of the review staffÑall will increase in proportion tothe degree of success attained inthe operational review.

Because of the number ofdifferent types and complexitiesof operational reviews and thevarying skills required, support-ing functional disciplines areoften necessary to supplementthe regular review staffÕs skills

and abilities. However, it is notalways practical to maintain per-sonnel with all of the requiredskills on the operational reviewstaff. Thus, one should considerthe skills that are necessary forthe successful conduct of eachoperational review, and eithermake sure that such skills areavailable on staff or contract forneeded outside expertise.

UNDERSTANDING OPERA-TIONAL REVIEW CONCEPTS

Organizations have been inexistence for thousands ofyearsÑsome successful and longlasting, others short lived.Through the years there havebeen no clear-cut criteria or for-

mulas for success. Many businessorganizations have been success-ful through such intangible attrib-utes as dumb luck, falling into aniche marketplace, being the first,consumer acceptance, and so on.Other companies using the bestavailable business acumen andmethods have failed miserably.Identifying, implementing, andmaintaining the secrets of successare elusive targets. Banking onwhat has worked in the past andyour own internal ouija board areineffective substitutes for objec-tive internal appraisal and exter-nal comparison and analysisÑwhat we call an operationalreview. Operational reviews arebecoming the tool of choice forgathering data related to programsof continuous improvement andto gain competitive advantage.

Operational review canbe defined as a process foranalyzing internal opera-tions and activities to iden-tify areas for positiveimprovement in a programof continuous improve-ment. The process beginswith an analysis of existingoperations and activities,

identifies areas for positiveimprovement, and then establish-es a performance standard uponwhich the activity can be meas-ured. The goal is to improve eachidentified activity so that it canbe the best possibleÑand staythat way. The best practice is notalways measured in terms ofleast costs, but may be morewhat stakeholders value, andexpected levels of performance.

Operational review processesare directed towards the continu-ous pursuit of positive improve-ments, excellence in all activities,and the effective use of best prac-tices. The focal point in achievingthese goals is the customerÑbothinternal and externalÑwho estab-lishes performance expectations

May/June 2000 27

© 2000 John Wiley & Sons, Inc.

Operational reviews are becomingthe tool of choice for gatheringdata related to programs of continu-ous improvement and to gain com-petitive advantage.

and is the ultimate judge ofresultant quality. A company cus-tomer is defined as anyone whohas a stake or interest in theongoing operations of the organi-zationÑanyone who is affectedby our results (type, quality, andtimeliness). Stakeholders includeall those who are dependent uponthe survival of the organization,such as:

¥ Suppliers/vendors: external;¥ Owners/shareholders: inter-

nal/external;¥ Management/supervision:

internal;¥ Employees/subcontractors:

internal/external; and¥ Customers/end-users:

external.

Operational reviewresults provide the compa-nyÑ owners, management,and employeesÑwith datanecessary for effectiveresource allocation and thestrategic focus for the organiza-tion. The operational reviewprocess provides for those objec-tive measures to determine thesuccess of the companyÕs internalgoals, objectives, and detail plansas well as external and competi-tive performance measures.Evaluating the companyÕs per-formance against stakeholderexpectations enables the companyto pursue its program of continu-ous improvement and the road toexcellence. Effective operationalreview procedures encompassesboth internal and external needs.

Managers or supervisors whoare responsible for an operationalarea have traditionally maintainedthe operation as they found it.That is, they primarily acceptedthe organization, personnel, andfunctions they inherited. Theywere not allowed or did notunderstand how to make theirassigned area of responsibility

more efficient. And many times,systems were in effect (such asovercontrolling bosses) that pre-vented such positive changes.

The purpose of the opera-tional review is to assist managersand operations personnel to lookat their areas of responsibilityfrom an operational viewpoint.What do we mean when we sayÒfrom an operational viewpointÓ?We mean that operations areviewed with an eye as to whetheroperations can be improved so asto be performed more efficiently,effectively, or economically.

Given todayÕs increasinglyvaried and competitive economicenvironment, management placesmore and more emphasis on the

evaluation of the economy, effi-ciency, and effectiveness of theorganizationÕs operations. Manytimes, the managers and employ-ees of an operational area are tooclose to operations, too resistantto change, too enmeshed in dailyoperations, and so on, to objec-tively review their own opera-tions. Since both internal andexternal consultants have the fact-finding and diagnostic skills need-ed to perform such operationalreviews, they are frequently askedto do so. In some organizations, aseparate unit is formed strictly toperform operational reviews.

Operational reviewing got itsstart when management stoppedbeing concerned solely withreviewing the reporting of infor-mation and started wonderingwhy a transaction was made inthe first place and if there was abetter way to do it. Operationalreview is the process whereby

the reviewer determines whethermanagement is using theresources entrusted to them inthe most economical and effi-cient manner to achieve the mosteffective results of operations.

What are some of the rea-sons an operational reviewshould be performed? The focusand scope of operations in boththe public and private sectorshave changed in recent years.Management has increaseddemands for more relevant infor-mation on the conduct of itsoperations and related resultsthan can be found in strictlyfinancial data. Both business andgovernment management seekmore information with which to

judge the quality of opera-tions and make operationalimprovements. That is whyoperational review tech-niques are needed to evalu-ate the effectiveness andefficiency of operations.

ECONOMY, EFFICIENCY, ANDEFFECTIVENESS

Operational review proce-dures embrace the concept ofconducting operations for econo-my, efficiency, and effectiveness.The following is a brief descrip-tion of each of the Òthree Es ofoperational reviewsÓ:

1. Economy (or the cost of oper-ations). Is the organizationcarrying out its responsibili-ties in the most economicalmannerÑthat is, through dueconservation of its resources?In appraising the economy ofoperations, and related alloca-tion and use of resources, thereviewer may considerwhether the organization is:

¥ Following sound purchasingpractices;

¥ Overstaffed as related to per-forming necessary functions;

28 The Journal of Corporate Accounting & Finance

© 2000 John Wiley & Sons, Inc.

Operational review proceduresembrace the concept of conductingoperations for economy, efficiency,and effectiveness.

¥ Allowing excess materials tobe on hand;

¥ Using equipment that is moreexpensive than necessary; or

¥ Avoiding the waste ofresources.

2. Efficiency (or methods ofoperations). Is the organiza-tion carrying out its respon-sibilities with the minimumexpenditure of effort?Examples of operationalinefficiencies that youshould be aware of include:

¥ Improper use of manual andcomputerized procedures;

¥ Inefficient paperwork flow;¥ Inefficient operating systems

and procedures;¥ Cumbersome organizational

hierarchy and/or communica-tion patterns;

¥ Duplication of effort; or¥ Unnecessary work steps.

Note that economy andefficiency are both relativeterms, and it is not possibleto determine whether thearea under review hasreached the maximum prac-ticable level of either.However, the reviewer and opera-tions personnel are continuallylooking for best practices in aprogram of continuous improve-ments. Economy and efficiencyare continually being appraisedand improved uponÑthey are notput in place based on the opera-tional review and then ignored.

Economy and efficiency areconcerned with achieving theoptimum balance between costsand results. In performing thispart of the review, the reviewerevaluates cost minimization,emphasizing reduction of costs,but not to the point where resultsare not accomplished. In addition,productivity maximization maybe analyzed, but not to the pointwhere the costs become exces-sive. In evaluating economy and

efficiency, the reviewer analyzesthe use of resources: people, facil-ities, equipment, supplies, andmoney. For example, the reviewermight analyze the following:

¥ Allocation of responsibilitiesand authority within theorganization structure;

¥ Physical deployment of dis-tribution of resources;

¥ Scheduling of resourcesÑwhen people work, whenfacilities are used;

¥ Segmentation of tasks intological groupings;

¥ Match between skill level,capacity, performance capa-bility, etc., and the way aresource is used;

¥ Prices paid;¥ Charges levied;¥ Rate at which tasks are per-

formed; and¥ Number of tasks completed.

Within the economy andefficiency concept, the reviewerdoes not ask whether the func-tion is worthwhile in terms ofwhat is accomplished. Thereviewer accepts that the func-tion exists and asks whether thisis the most economical and effi-cient way to get it done. Resultsare considered as part of thereview of effectiveness.

3. Effectiveness (or results ofoperations). Is the organiza-tion achieving results orbenefits based on statedgoals and objectives or someother measurable criteria?The review of the results ofoperations includes:

¥ Appraisal of the organiza-tional planning system as to

its development of realisticgoals, objectives, and detailplans;

¥ Assessment of the adequacyof managementÕs system formeasuring effectiveness;

¥ Determination of the extentto which results areachieved; and

¥ Identification of factorsinhibiting satisfactory per-formance of results.

Although it is managementÕscontinuing responsibility to assessthe results of operations, its objec-tives and measurement criteria arenot always clearly defined.Without such clarification, thereviewer cannot meaningfullyevaluate the results of operations.If management has not done soprior to starting the operationalreview, the reviewer should workwith management to (1) state the

objectives, (2) establishmeasurement criteria, and(3) establish methods foraccumulating the data nec-essary to measure achieve-ment of operational results.Effectiveness is concerned

with results and accomplishmentsachieved and benefits provided.In evaluating the effectiveness ofoperations, the reviewer askswhether the activity is achievingits ultimate intended purpose.Analysis is qualitative rather thanquantitative.

The relationship of economyand efficiency and their impacton results can be seen as a see-saw. That is, there is an attemptto balance them to achieve justthe right amount of each. In aperfectly balanced situation, thecost of operations would bemaintained at the lowest possiblelevel without sacrificing effi-ciency (or the methods of opera-tions) and effectiveness (or theresults of operations), thuseffecting economy. At the same

May/June 2000 29

© 2000 John Wiley & Sons, Inc.

Economy and efficiency are concernedwith achieving the optimum balancebetween costs and results.

time, the methods of operationswould be performed at the leastpossible cost without sacrificingresults, thus producing efficien-cy. Can you see, then, why econ-omy and efficiency are normallyreviewed together as part of theoperational review procedure?

FINANCIAL AUDITS VERSUSOPERATIONAL REVIEWS

To illustrate the differencesbetween financial audits and oper-ational reviews using operationalreview concepts, consider this:The reviewer is less concernedwith determining whether pur-chase requisitions and orders andsuppliersÕ invoices reflect properapprovals, as in a financial audit,but is more concerned with opera-tional aspects, such as whether:

1. The materials were reallyneeded;

2. Quantities used or purchasedwere reasonable;

3. There was avoidable wasteand exposure to damage orloss; and

4. Requisitioners exercisedundue influence over pur-chasing by designatingsources of purchase.

For example, a typical finan-cial audit step could be to deter-mine whether vendor purchaserequisitions and invoices havebeen properly approved.However, when looking at theoperational aspects of vendor pur-chases, the reviewer might ask:

1. Were materials really need-ed? For example, were mate-rials mistakenly ordered thatcould not be used owing tochanges in production speci-fications because the productspecifications unit failed tocommunicate with the pur-chasing department?

2. Were quantities used or pur-chased reasonable? For exam-ple, assuming the materialswere usable, were goodsbought for inventory abovecalculated safety stock levelsbecause of the fear of incur-ring a stock-out?

3. Was there avoidable wasteand exposure to damage orloss? For example, weresteel components and partsthat were susceptible to rustbought and stored in an out-side yard owing to an over-crowded inside storeroom?

4. Did the requisitioner exerciseundue influence by statingspecific sources or brands?For example, did the requisi-tioner specify an IBM micro-computer or a Xerox copierwhen a less-expensive brandwould do just as well?

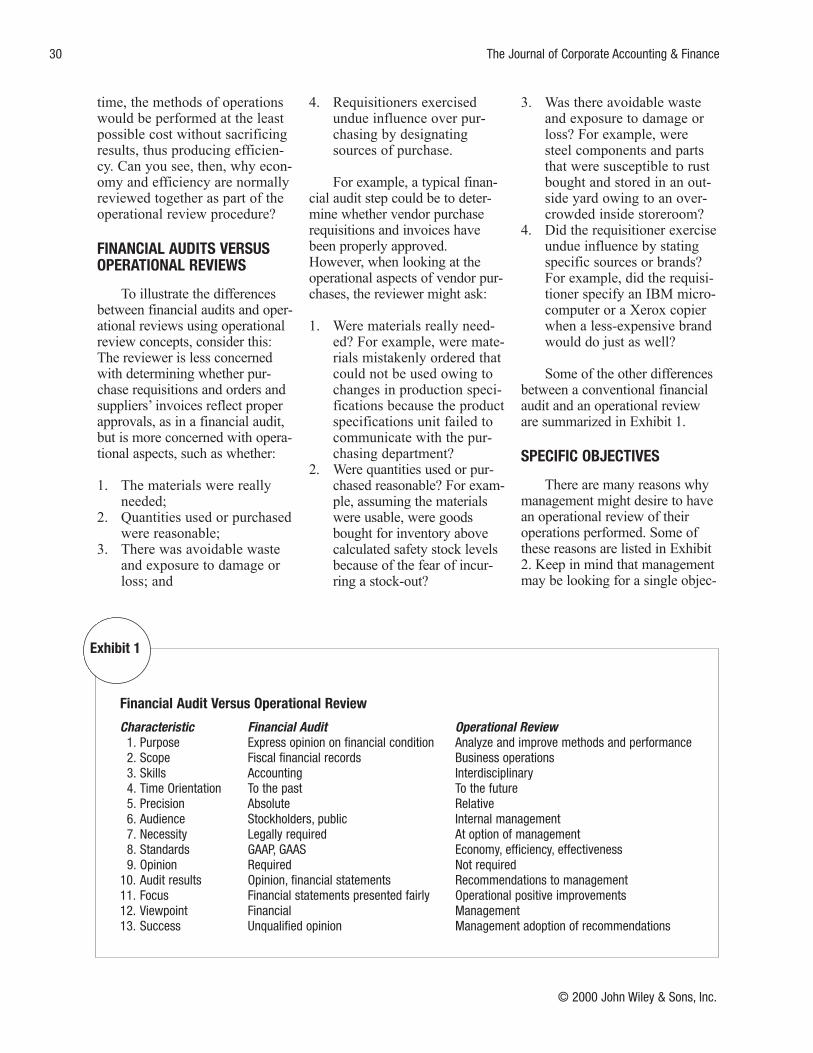

Some of the other differencesbetween a conventional financialaudit and an operational revieware summarized in Exhibit 1.

SPECIFIC OBJECTIVES

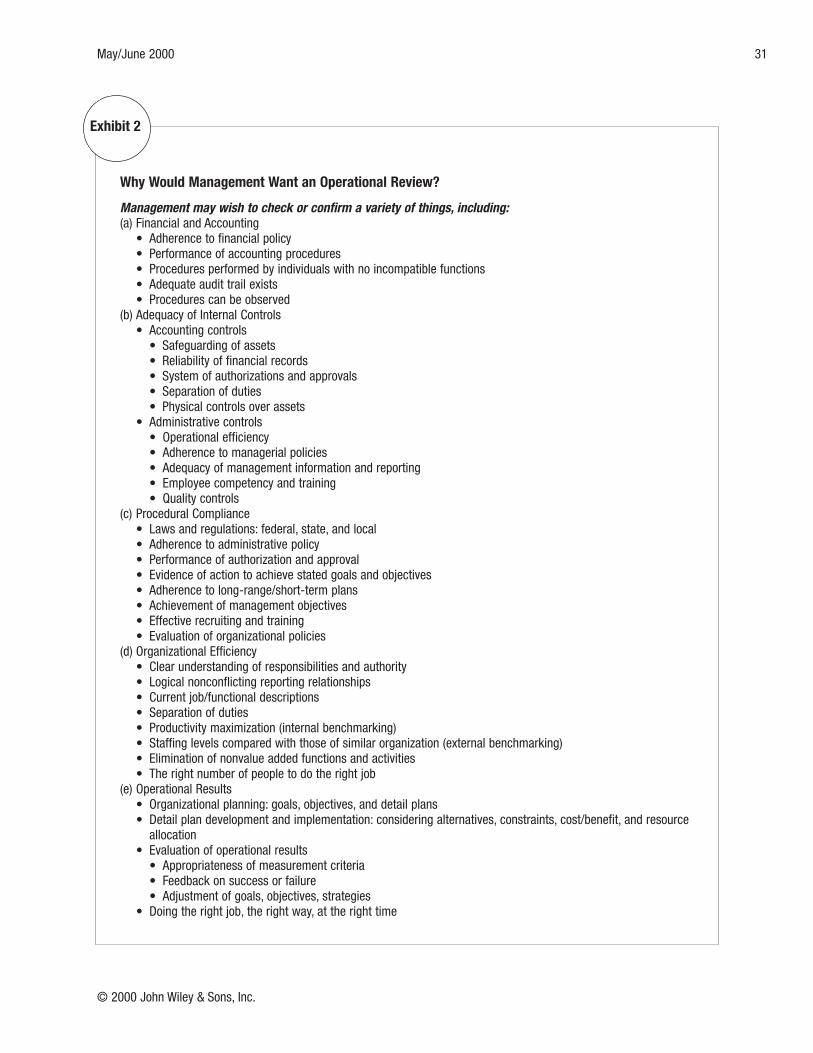

There are many reasons whymanagement might desire to havean operational review of theiroperations performed. Some ofthese reasons are listed in Exhibit2. Keep in mind that managementmay be looking for a single objec-

30 The Journal of Corporate Accounting & Finance

© 2000 John Wiley & Sons, Inc.

Financial Audit Versus Operational Review

Characteristic Financial Audit Operational Review1. Purpose Express opinion on financial condition Analyze and improve methods and performance2. Scope Fiscal financial records Business operations3. Skills Accounting Interdisciplinary4. Time Orientation To the past To the future 5. Precision Absolute Relative6. Audience Stockholders, public Internal management7. Necessity Legally required At option of management 8. Standards GAAP, GAAS Economy, efficiency, effectiveness9. Opinion Required Not required

10. Audit results Opinion, financial statements Recommendations to management11. Focus Financial statements presented fairly Operational positive improvements12. Viewpoint Financial Management13. Success Unqualified opinion Management adoption of recommendations

Exhibit 1

May/June 2000 31

© 2000 John Wiley & Sons, Inc.

Why Would Management Want an Operational Review?

Management may wish to check or confirm a variety of things, including:(a) Financial and Accounting

• Adherence to financial policy• Performance of accounting procedures • Procedures performed by individuals with no incompatible functions • Adequate audit trail exists• Procedures can be observed

(b) Adequacy of Internal Controls• Accounting controls

• Safeguarding of assets • Reliability of financial records• System of authorizations and approvals • Separation of duties • Physical controls over assets

• Administrative controls• Operational efficiency• Adherence to managerial policies• Adequacy of management information and reporting• Employee competency and training• Quality controls

(c) Procedural Compliance• Laws and regulations: federal, state, and local• Adherence to administrative policy• Performance of authorization and approval• Evidence of action to achieve stated goals and objectives• Adherence to long-range/short-term plans• Achievement of management objectives• Effective recruiting and training• Evaluation of organizational policies

(d) Organizational Efficiency • Clear understanding of responsibilities and authority• Logical nonconflicting reporting relationships• Current job/functional descriptions• Separation of duties • Productivity maximization (internal benchmarking) • Staffing levels compared with those of similar organization (external benchmarking) • Elimination of nonvalue added functions and activities • The right number of people to do the right job

(e) Operational Results• Organizational planning: goals, objectives, and detail plans • Detail plan development and implementation: considering alternatives, constraints, cost/benefit, and resource

allocation• Evaluation of operational results

• Appropriateness of measurement criteria • Feedback on success or failure • Adjustment of goals, objectives, strategies

• Doing the right job, the right way, at the right time

Exhibit 2

tive (e.g., operational efficiency),a combination of objectives (e.g.,least cost but most efficient sys-temsÑbest practices), or theirown specific agenda (e.g.,achievement of results on thebasis of cost versus benefits).

OPERATIONAL REVIEW PHASES

Operational reviews consistbasically of gathering informa-tion, making evaluations, anddeveloping recommendationswhere appropriate. An operationalreview is essentially the evalua-tion of an activity for potentialimprovement. Management hasthe primary responsibility forproper planning, conduct, andcontrol of activities. Thus,review and evaluation of theway management itselfplans, conducts, and con-trols the activities become amajor consideration andfocal point in the conduct ofthe review. In addition, thereview includes analyzing resultsand being alert to problems.These also provide insights intothe effectiveness of managementand the potential for improve-ments.

The phases through which anoperational review progresses are:

1 Planning;2. Work programs;3. Fieldwork;4. Development of findings

and recommendations; and5. Reporting.

The operational reviewer mayperform two types of reviews:preliminary and in-depth, eachhaving all five phases. The differ-ence between the two is thedegree of emphasis, the specifictechniques chosen, and the objec-tives of a particular phase. In apreliminary review, fieldworkmight consist of limited transac-

tion testing and interviewing, andthe report may be a briefing tomanagement. In an in-depthreview, fieldwork might consist ofdetailed examination using tech-niques such as work measure-ment, workload analysis, cost-benefit analysis, and so onÑandthe report may be formally writ-ten, with wider distribution. Theoperational review phases can bedescribed as follows:

(a) PlanningThe reviewer obtains general

information about the kinds ofactivities performed, the generalnature of those activities and theirrelative importance, and other

general information to help planthe early portions of the review. (b) Work Programs

The reviewer prepares theoperational review work pro-gram for the preliminary reviewof those activities selected forreview in the planning phase.Well constructed work programsare essential for conductingoperational reviews in an effi-cient and effective manner. Suchprograms must be individualizedfor each situation, and eachwork step must state clearly thework to be done and why.(c) Fieldwork

The reviewer analyzes opera-tions to determine the effective-ness of management and relatedcontrols. Such functions and con-trols are tested in actual operation,with particular emphasis on areasdifficult to control and havinghigh potential for weakness. Thepurpose of this phase is to deter-

mine whether a situation needsimprovement, is significant, andwhat should be done about it.(d) Development of Findingsand Recommendations

Based on the significantareas identified during the field-work phase, specific findings aredeveloped according to the fol-lowing attributes:¥ Condition: What did you

find?¥ Criteria: What should it be?¥ Effect: What is the impact

on operations?¥ Cause: Why did it happen?¥ Recommendation: What

needs to be done to correctthe situation? (based onpresent best practices, andalways subject to change)(e) Reporting

The reviewer preparesthe report relative to theresults of the review. Thepurpose of the report is tobring these results to theattention of those having an

interest in or responsibility forthe findings. In reality, the major-ity of findings, if not all, shouldhave been reported to manage-ment with remedial actionalready being taken or completedprior to the formal report. Thereport becomes a summary of theresults of the review.

WHAT FUNCTIONS SHOULDYOU REVIEW?

The most critical question toanswer for an organization iswhat function or functions toinclude in the operational review.Where shall we review? Do weperform the operational reviewfor all functions of the organiza-tion or only for selected areas? Agood starting point is to list theorganizationÕs major functions, tocheck off those where operationalreview would be most helpful,and then to prioritize each func-

32 The Journal of Corporate Accounting & Finance

© 2000 John Wiley & Sons, Inc.

An operational review is essentiallythe evaluation of an activity forpotential improvement.

tion as to its criticalness and/orthe desired order of review.

One way to decide whichfunctions to review is to deter-mine how critical each functionis to the overall organizationaloperation. For instance, for amanufacturing business, the mostcritical area might be the inven-tory or production control func-tions. For a service-oriented con-cern, where personnel costsapproximate 70 percent of totalexpenditures, the personnel func-tion would be more critical.Normally, reviewers work with alimited budget in terms of hoursallocated to the operationalreview, so they are greatly con-cerned with spending these hourson functional areas that offer thegreatest potential for operationalimprovements in return for theireffort. Criteria for determining acompanyÕs critical areas includethe following:

1. Areas with large numbers inrelationship to other func-tions, such as revenues,costs, percentage of totalassets, number of sales, unitsof production, and personnel.

2. Areas where controls areweak, for example, a lack ofan effective manufacturingcontrol system, managementreporting system, or organi-zational planning and con-trol system.

3. Areas subject to abuse orlaxity, for example, theremay be inventory and pro-duction controls that allowtransactions to go unreportedand undetected, uncontrol-lable time and cost report-ing, and ineffective person-nel evaluation procedures.

4. Areas that are difficult tocontrol; for example, theremay be ineffective store-room, shipping, or timerecording procedures.

5. Areas where functions are notperformed efficiently or eco-nomically; for example, theremaybe ineffective proce-dures, duplication of efforts,unnecessary work steps; orinefficient use of resources,such as data processingequipment, overstaffing, andexcess purchases.

6. Areas indicated by ratio,change, or trend analysis,such as characterized bywide up or down whencompared over a number ofperiods. Examples includesales changes by productline, costs by major catego-ry, number of personnel,inventory levels, and soforth.

7. Areas where managementhas identified specific weak-nesses or needs for, such aspersonnel functions, manu-facturing procedures, data

processing operations, andmanagement reporting.

Another factor to considerwhen choosing the critical oper-ational area to review is the will-ingness of the personnel in thearea to cooperate in the perform-ance of the review. First, thosein operational managementshould want to have their opera-tions reviewed and be willing towork with the reviewers in theimprovement of their operations.Without such top managementcommitment, the operationalreview is not likely to succeed.Second, staff and operating per-sonnel must be willing to workwith the reviewers, both in per-forming the operational reviewand in the subsequent implemen-tation of operational improve-ments. Cooperation at all levelsof the organization is essential toa successful operational review.

The reviewer must enlist thecooperation of all personnel:members of management toensure top commitment to thereview, and operations personnelto help in identifying areas toreview and proposed improve-ments. Normally, in most opera-tions, the staff or operating per-sonnel know precisely what isgoing on day by day and withfirsthand knowledge of opera-tions, can help you to identifythe most critical areas to review.

May/June 2000 33

© 2000 John Wiley & Sons, Inc.

Rob Reider, Ph.D., CPA, MBA, is the president of Reider Associates, a management and organizational con-sulting firm located in Santa Fe, New Mexico, which he founded in 1976. Prior to starting Reider Associates,Dr. Reider was a manager in the Management Consulting Department of Peat, Marwick in Philadelphia. Hisarea of expertise encompasses planning and budget systems, managerial and administrative systems, dataprocessing, financial and accounting procedures, organizational theory, management advisory services, largeand small business consulting, management information and control techniques, and management trainingand staff development. Dr. Reider has been a consultant to numerous large, medium and small businessesin these areas. In addition, he has conducted many varied operational reviews, and has trained both internalstaff and external consultants in operational review techniques and reporting procedures. He is the author ofThe Complete Guide to Operational Auditing (John Wiley & Sons, 1993), among other books.