Embed Size (px)

DESCRIPTION

Long-term Liabilities. Bonds. Written promise to pay a specific sum of money on a speciific future date Purchaser is bondholder Receives Bond certificate. Classification of Bonds. Registered - issued in name of holder Secured - assets pledged as security - PowerPoint PPT Presentation

Citation preview

1© Copyrright Doug Hillman 2000

Long-termLiabilities

2© Copyrright Doug Hillman 2000

Bonds

Written promise to pay a specific sum of money on a speciific future date

Purchaser is bondholder Receives Bond certificate

3© Copyrright Doug Hillman 2000

Classification of Bonds

Registered - issued in name of holder Secured - assets pledged as security Debenture (unsecured) - based on

general credit Serial - mature in installments Callable - corporation has option of

retiring

4© Copyrright Doug Hillman 2000

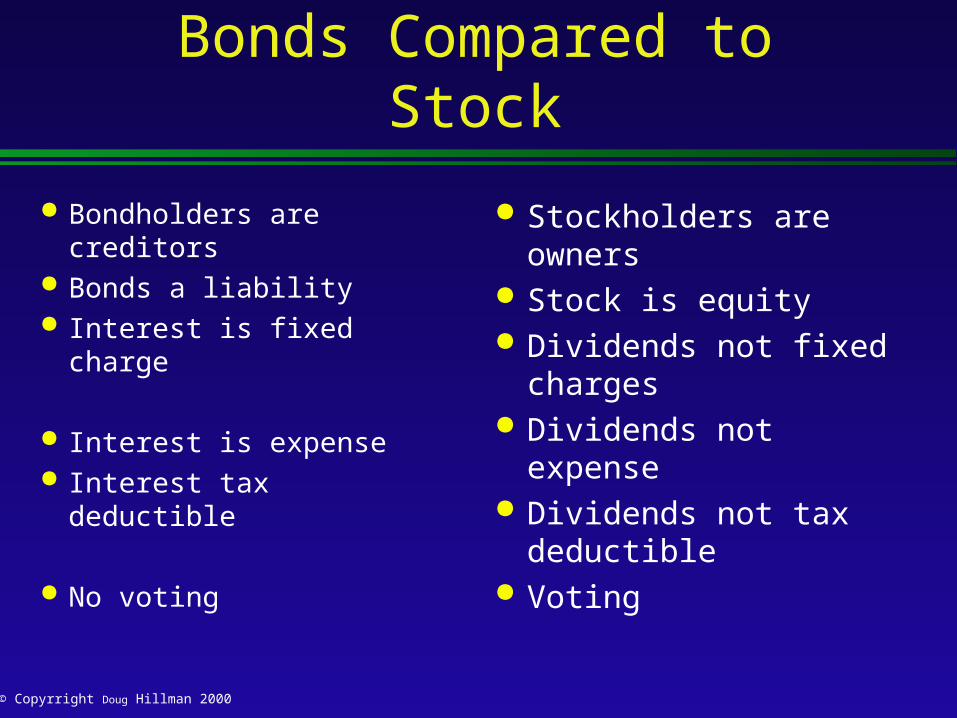

Bonds Compared to Stock

Bondholders are creditors

Bonds a liability Interest is fixed charge

Interest is expense Interest tax deductible

No voting

Stockholders are owners

Stock is equity Dividends not fixed

charges Dividends not expense Dividends not tax

deductible Voting

5© Copyrright Doug Hillman 2000

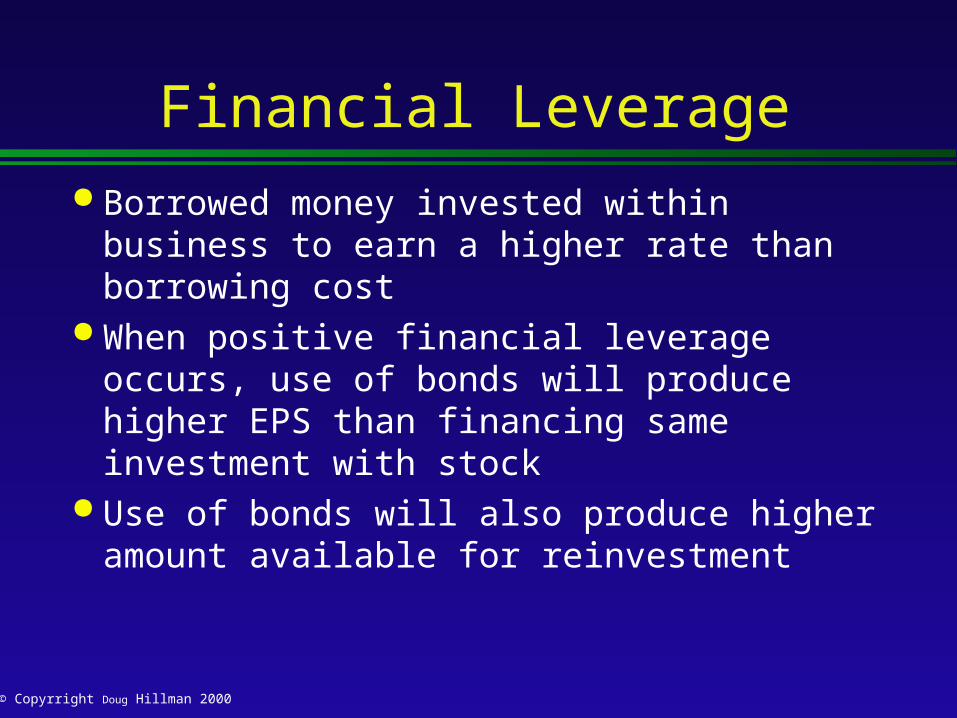

Financial Leverage Borrowed money invested within business

to earn a higher rate than borrowing cost When positive financial leverage occurs,

use of bonds will produce higher EPS than financing same investment with stock

Use of bonds will also produce higher amount available for reinvestment

6© Copyrright Doug Hillman 2000

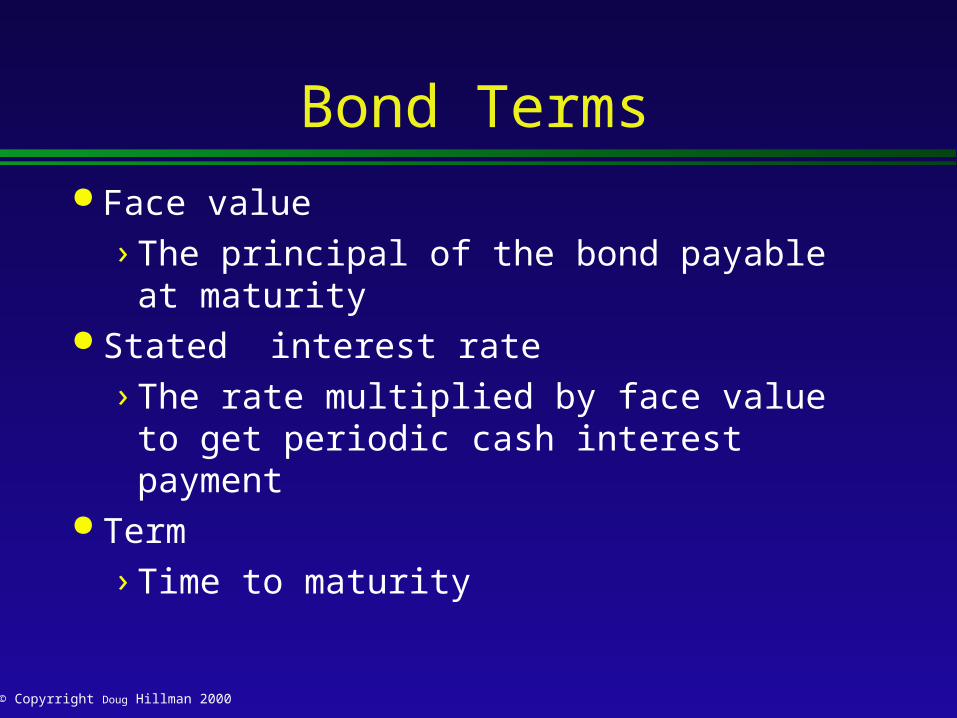

Bond Terms Face value

› The principal of the bond payable at maturity

Stated interest rate

› The rate multiplied by face value to get periodic cash interest payment

Term

› Time to maturity

7© Copyrright Doug Hillman 2000

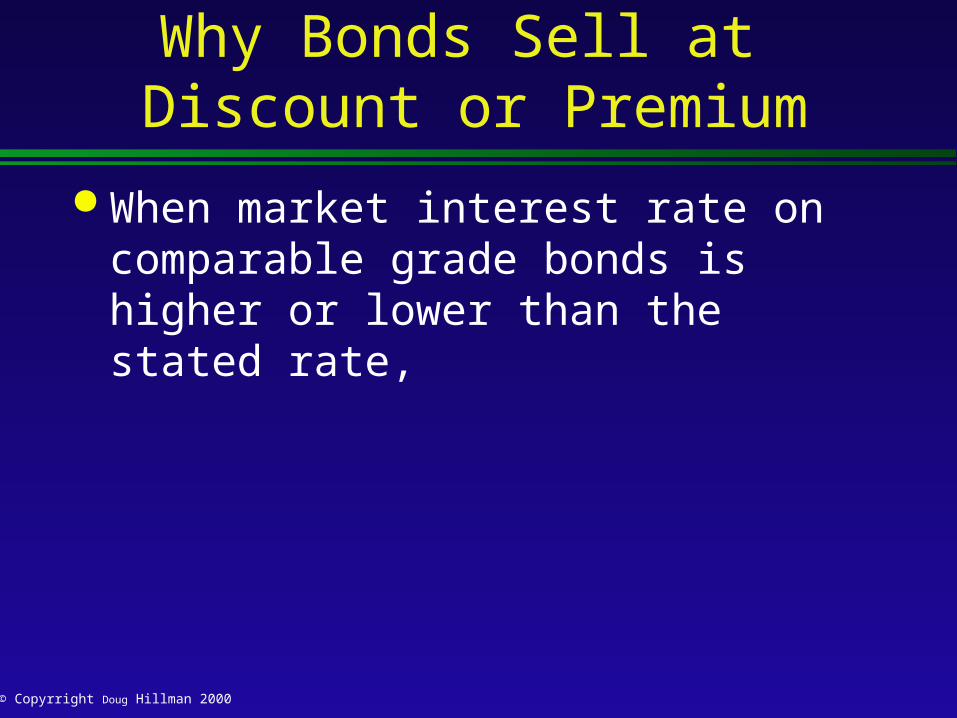

Why Bonds Sell at Discount or Premium

When market interest rate on comparable grade bonds is higher or lower than the stated rate,

8© Copyrright Doug Hillman 2000

Why Bonds Sell at Discount or Premium

When market interest rate on comparable grade bonds is higher or lower than the stated rate, investors will adjust the purchase price of the bond so that they earn the desired market interest rate

9© Copyrright Doug Hillman 2000

Why Bonds Sell at Discount or Premium

Why Bonds Sell at Discount or PremiumWhen market interest rate on comparable grade bonds is higher or lower than the stated rate, investors will adjust the purchase price of the bond so that they earn the desired market interest rate

Issuing price determines effective or yield rate

10© Copyrright Doug Hillman 2000

Why Bonds Sell at Discount or Premium

If the market rate is higher than stated rate, investors will offer less than face value

Difference between price paid and face value is discount

Effective interest rate is higher than stated interest rate

11© Copyrright Doug Hillman 2000

Why Bonds Sell at Discount or Premium

If market rate is lower than stated rate, investors will offer more than face value

Difference between price paid and face value is premium

Effective interest rate is lower than stated interest rate

12© Copyrright Doug Hillman 2000

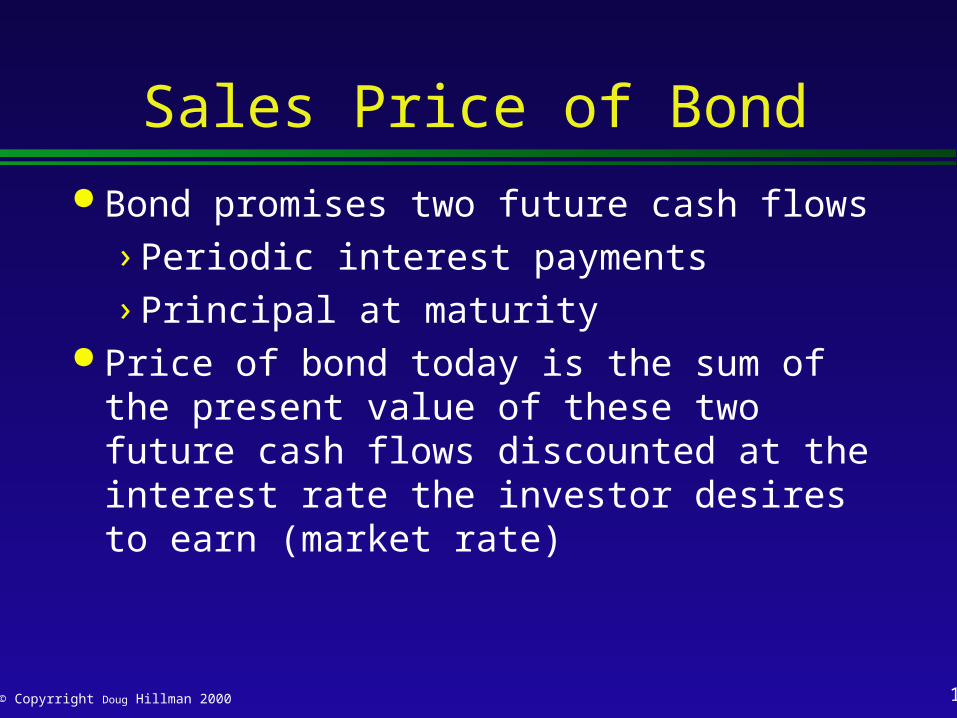

Sales Price of Bond

Bond promises two future cash flows

› Periodic interest payments

› Principal at maturity Price of bond today is the sum of the

present value of these two future cash flows discounted at the interest rate the investor desires to earn (market rate)

13© Copyrright Doug Hillman 2000

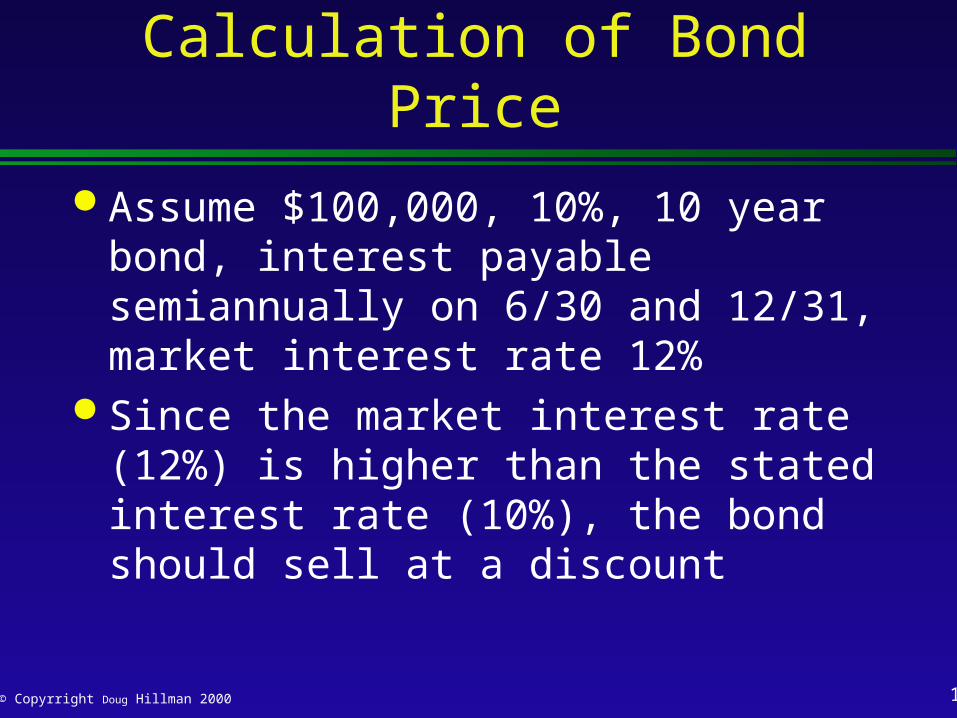

Calculation of Bond Price

Assume $100,000, 10%, 10 year bond, interest payable semiannually on 6/30 and 12/31, market interest rate 12%

Since the market interest rate (12%) is higher than the stated interest rate (10%), the bond should sell at a discount

14© Copyrright Doug Hillman 2000

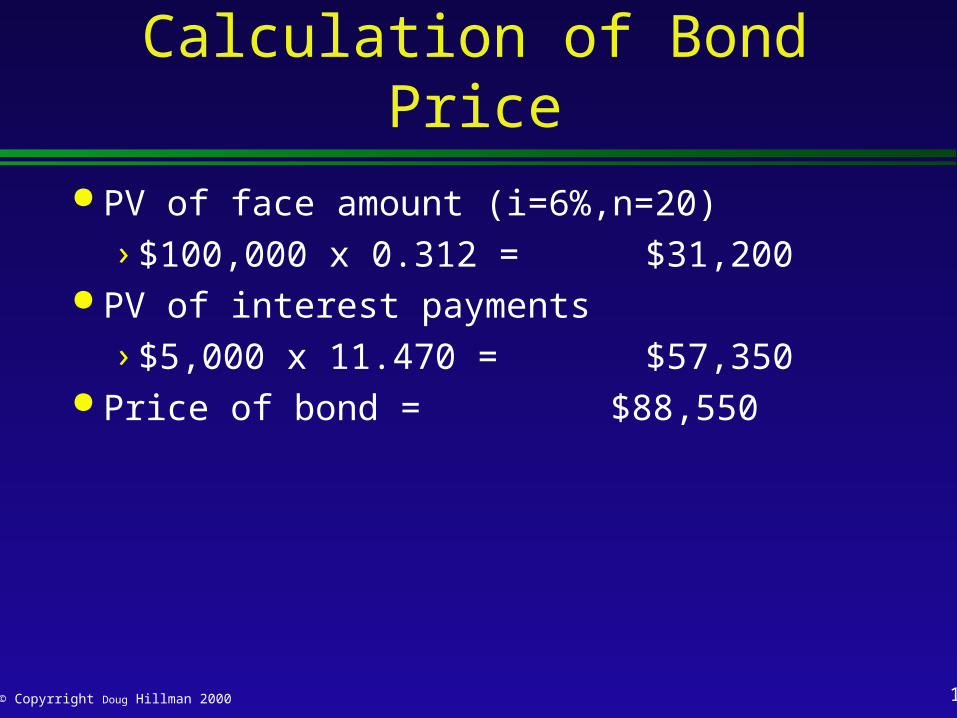

Calculation of Bond Price PV of face amount (i=6%,n=20)

› $100,000 x 0.312 = $31,200 PV of interest payments

› $5,000 x 11.470 = $57,350 Price of bond = $88,550

15© Copyrright Doug Hillman 2000

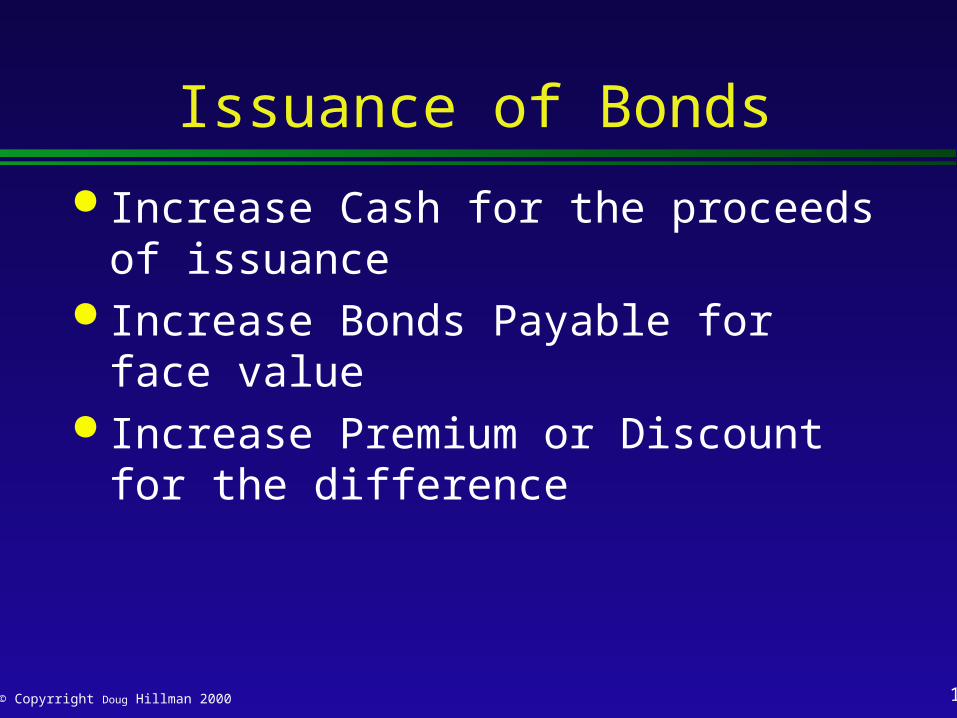

Issuance of Bonds

Increase Cash for the proceeds of issuance

Increase Bonds Payable for face value Increase Premium or Discount for the

difference

16© Copyrright Doug Hillman 2000

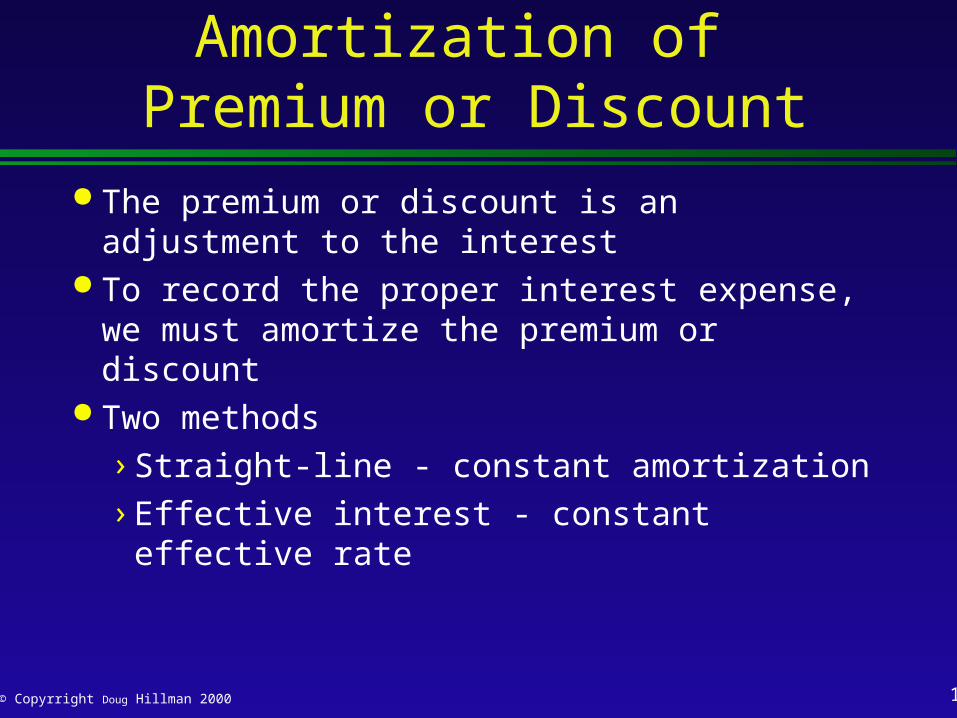

Amortization of Premium or Discount

The premium or discount is an adjustment to the interest

To record the proper interest expense, we must amortize the premium or discount

Two methods› Straight-line - constant amortization› Effective interest - constant effective rate

17© Copyrright Doug Hillman 2000

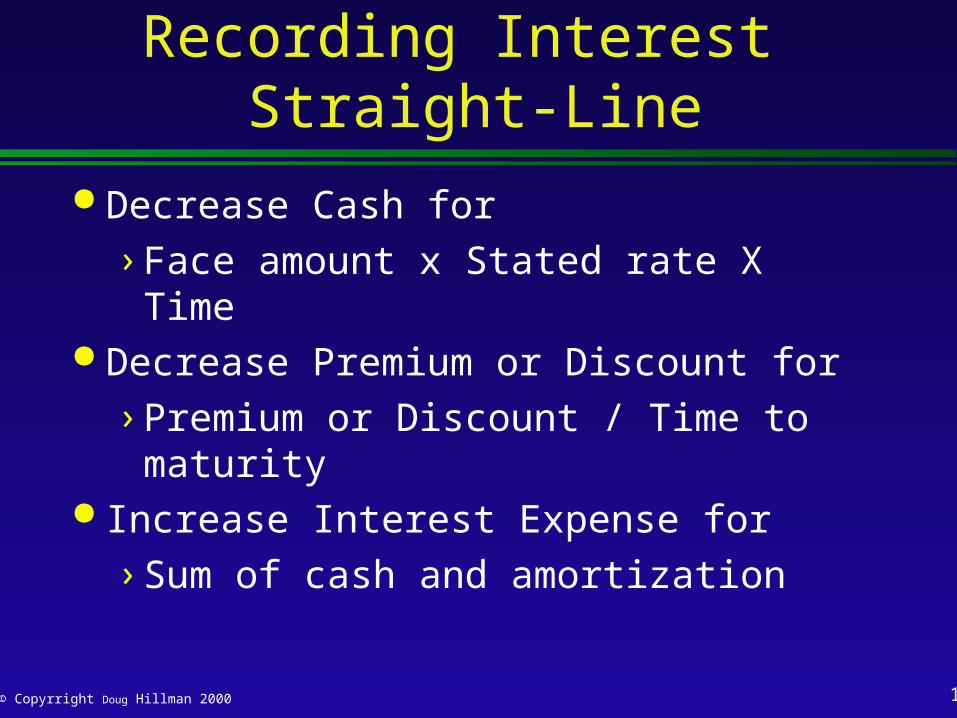

Recording Interest Straight-Line

Decrease Cash for

› Face amount x Stated rate X Time Decrease Premium or Discount for

› Premium or Discount / Time to maturity

Increase Interest Expense for

› Sum of cash and amortization

18© Copyrright Doug Hillman 2000

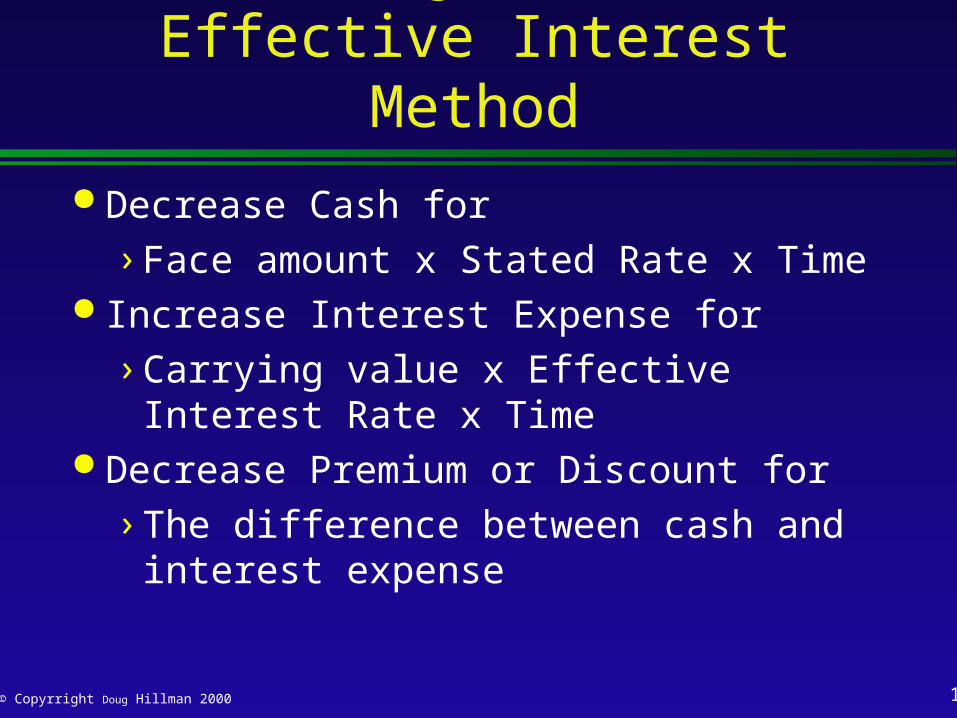

Recording Interest Effective Interest Method

Decrease Cash for

› Face amount x Stated Rate x Time Increase Interest Expense for

› Carrying value x Effective Interest Rate x Time

Decrease Premium or Discount for

› The difference between cash and interest expense

19© Copyrright Doug Hillman 2000

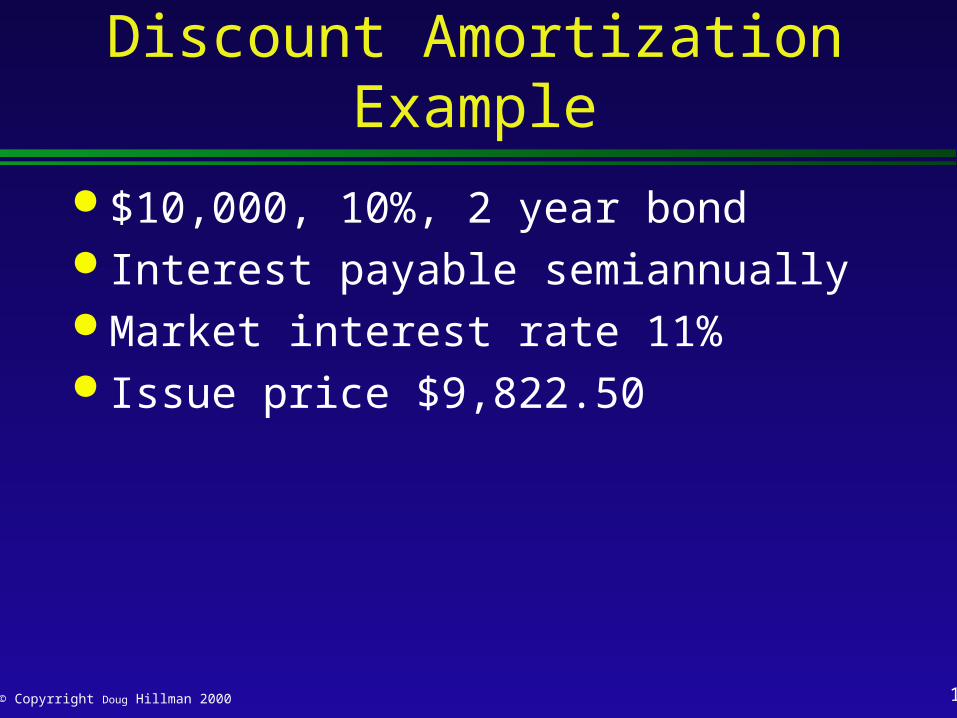

Discount Amortization Example

$10,000, 10%, 2 year bond Interest payable semiannually Market interest rate 11% Issue price $9,822.50

20© Copyrright Doug Hillman 2000

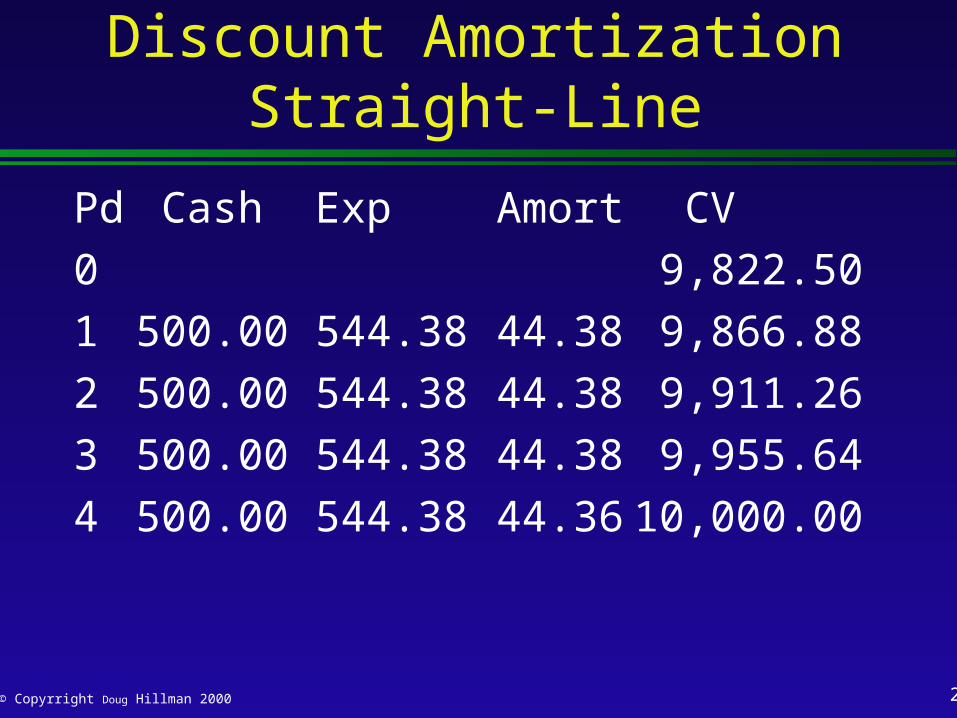

Discount Amortization Straight-Line

Pd Cash Exp Amort CV

0 9,822.50

1 500.00 544.38 44.38 9,866.88

2 500.00 544.38 44.38 9,911.26

3 500.00 544.38 44.38 9,955.64

4 500.00 544.38 44.36 10,000.00

21© Copyrright Doug Hillman 2000

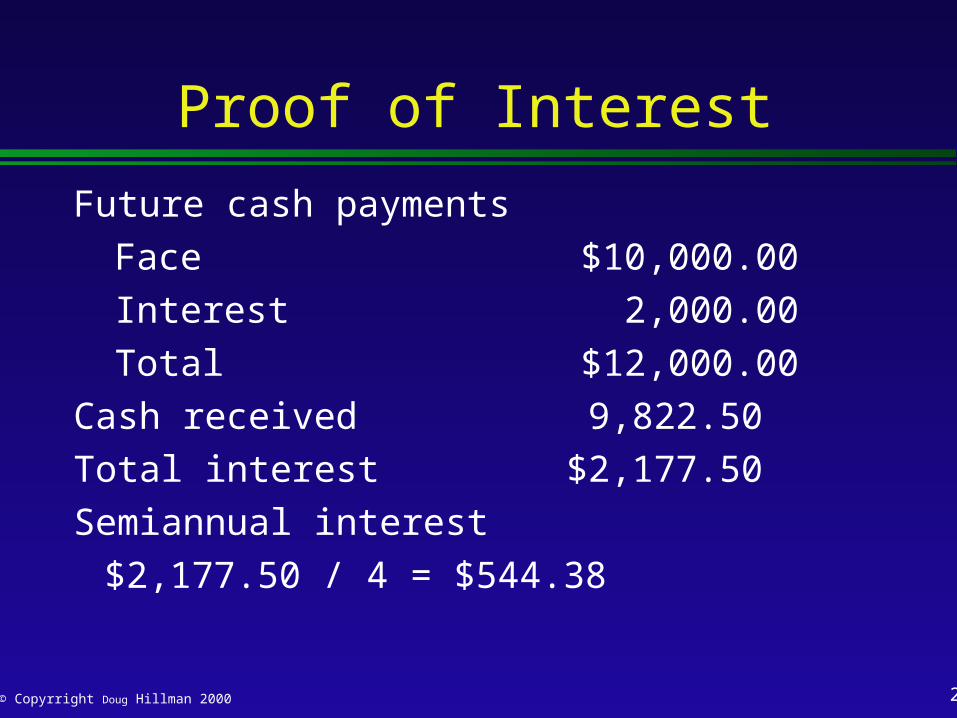

Proof of Interest

Future cash payments

Face $10,000.00

Interest 2,000.00

Total $12,000.00

Cash received 9,822.50

Total interest $2,177.50

Semiannual interest

$2,177.50 / 4 = $544.38

22© Copyrright Doug Hillman 2000

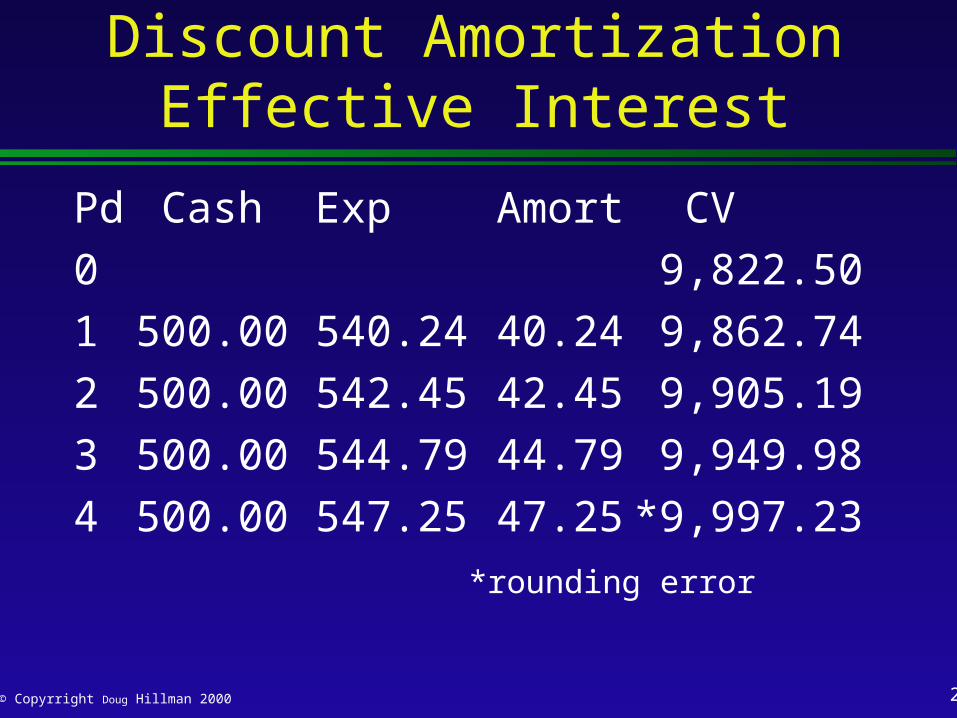

Discount Amortization Effective Interest

Pd Cash Exp Amort CV

0 9,822.50

1 500.00 540.24 40.24 9,862.74

2 500.00 542.45 42.45 9,905.19

3 500.00 544.79 44.79 9,949.98

4 500.00 547.25 47.25 *9,997.23

*rounding error

23© Copyrright Doug Hillman 2000

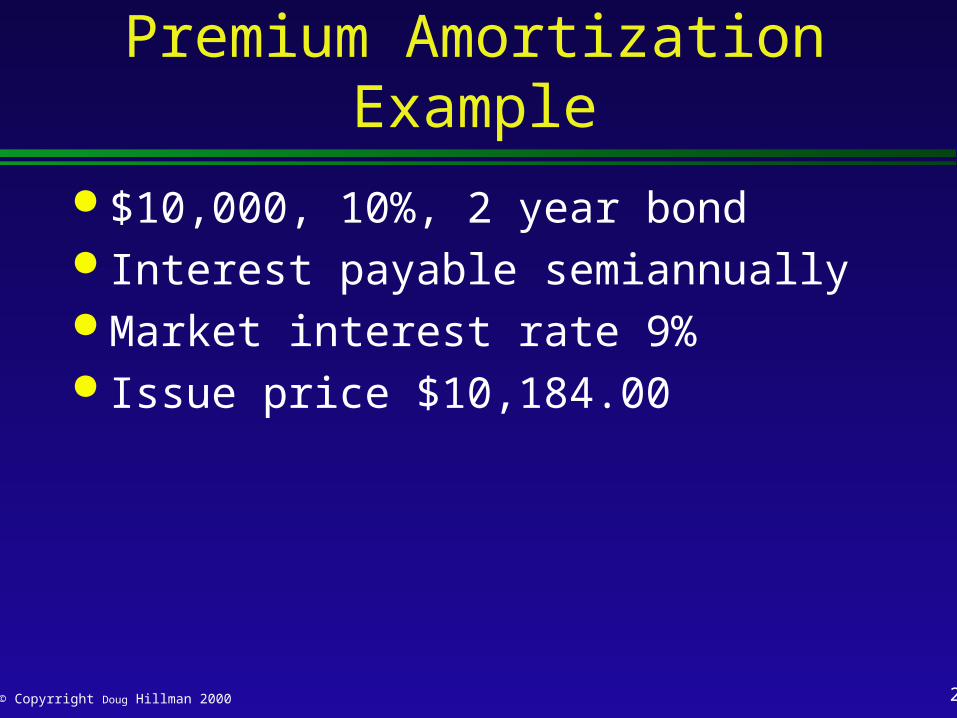

Premium Amortization Example

$10,000, 10%, 2 year bond Interest payable semiannually Market interest rate 9% Issue price $10,184.00

24© Copyrright Doug Hillman 2000

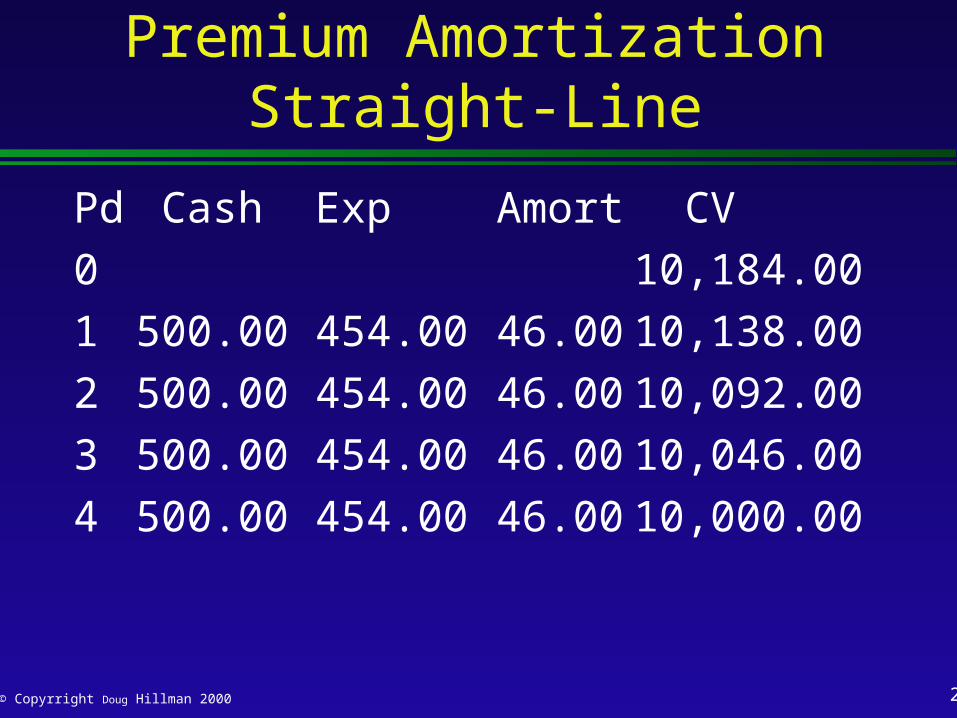

Premium Amortization Straight-Line

Pd Cash Exp Amort CV

0 10,184.00

1 500.00 454.00 46.00 10,138.00

2 500.00 454.00 46.00 10,092.00

3 500.00 454.00 46.00 10,046.00

4 500.00 454.00 46.00 10,000.00

25© Copyrright Doug Hillman 2000

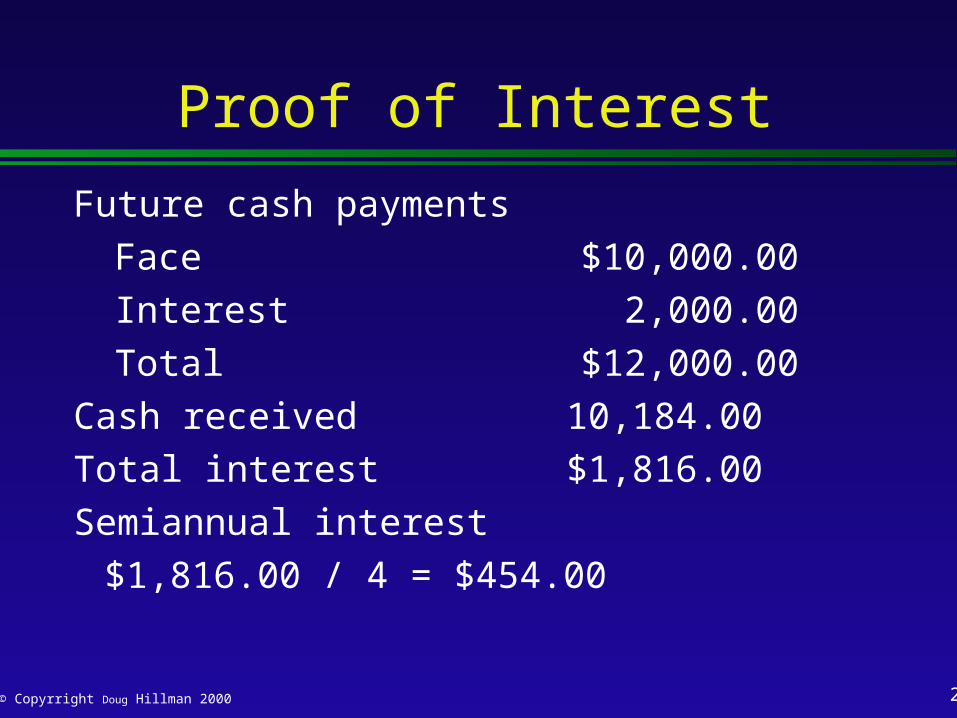

Proof of Interest

Future cash payments

Face $10,000.00

Interest 2,000.00

Total $12,000.00

Cash received 10,184.00

Total interest $1,816.00

Semiannual interest

$1,816.00 / 4 = $454.00

26© Copyrright Doug Hillman 2000

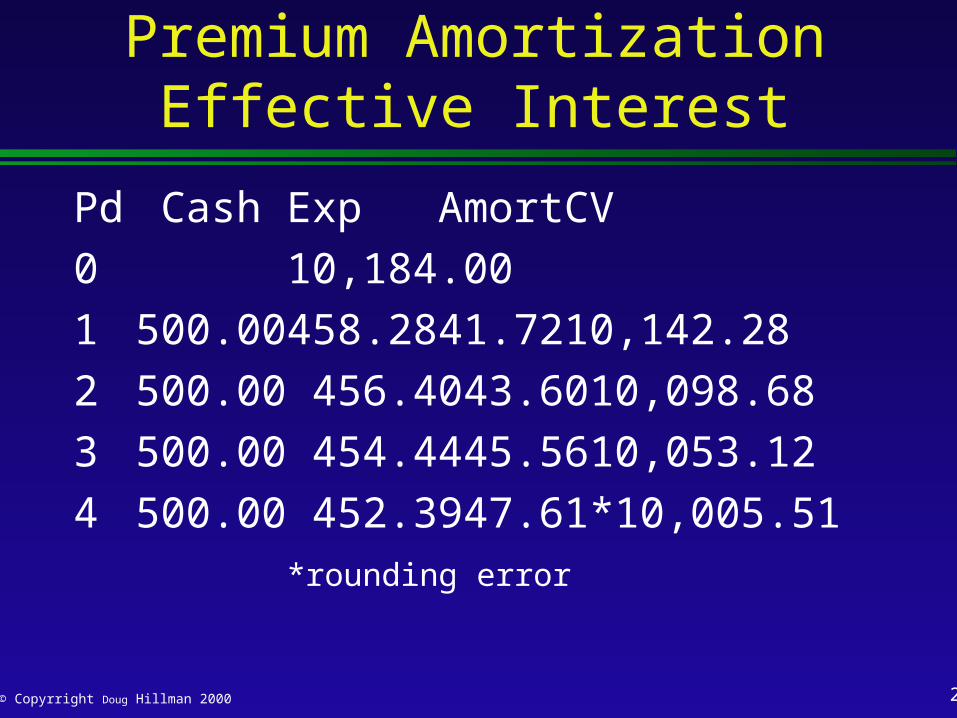

Premium Amortization Effective Interest

Pd Cash Exp Amort CV

0 10,184.00

1 500.00 458.28 41.72 10,142.28

2 500.00 456.40 43.60 10,098.68

3 500.00 454.44 45.56 10,053.12

4 500.00 452.39 47.61 *10,005.51*rounding error

27© Copyrright Doug Hillman 2000

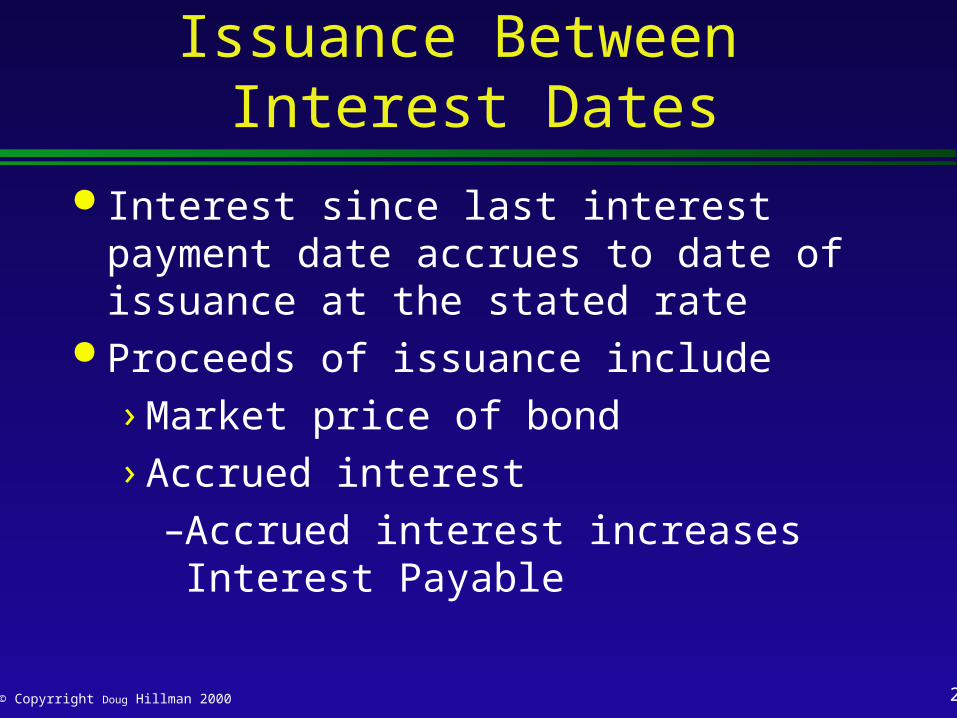

Issuance Between Interest Dates

Interest since last interest payment date accrues to date of issuance at the stated rate

Proceeds of issuance include

› Market price of bond

› Accrued interest

–Accrued interest increases Interest Payable

28© Copyrright Doug Hillman 2000

Issuance Between Interest Dates

Next interest payment is for full 6 months and pays off Interest Payabe

Resulting interest expense is only for period since issuance

29© Copyrright Doug Hillman 2000

Mortgage Notes Payable Long-term note with assignment of an

interest in property Mortgage paid in equal periodic installments Each payment includes

› Interest at specified rate on unpaid principal

› Reduction of principal for difference between payment and interest

30© Copyrright Doug Hillman 2000

Analyzing Information Is the level of total debt manageable? Does it seem likely interest and principal

payments can be met?

› Times Interest Earned ratio

› Debit ratio If firm needs additional financing, would

you recommend lending or investing in it?