Embed Size (px)

Citation preview

Long term global economic trends and implications for Nigeria

pwc.co.uk/economics-policy

June 2015

John HawksworthChief Economist, PwC

PwCJune 2015

Agenda

Long term global economic trends and implications for Nigeria •

World in 2050 study – motivation and methodology

Key findings from World in 2050

The importance of institutions

Implications for Nigeria: challenges and opportunities for growth

Discussion

PwCJune 2015

World in 2050: motivation and methodology

1

1Long term global economic trends and implications for Nigeria •

PwCJune 2015

What is the motivation for our World in 2050 study?Some key questions the analysis helps to answer

2Long term global economic trends and implications for Nigeria •

Section 1 – World in 2050: motivation and methodology

How fast will global economic power shift to Asia and other emerging markets such as Nigeria?

How much will an ageing population slow down GDP growth?

How important are institutions in enabling long term growth?

How will technological change, investment and education affect economic growth?

PwCJune 2015

World in 2050Country coverage

Our original ‘World in 2050’ study in 2006 made long-term GDP projections for the 17 largest economies in the world based on GDP at purchasing power parities (PPPs):

•G7 plus Spain, Australia and South Korea

•E7 emerging economies:

BRICs (Brazil, Russia, India and China); and

Indonesia, Mexico and Turkey.

Current study: Expanded to cover 32 leading economies including Nigeria, South Africa and Egypt within Africa, covering around 84% of global GDP in 2014.

3Long term global economic trends and implications for Nigeria •

Section 1 – World in 2050: motivation and methodology

PwCJune 2015

Methodology

How can we make GDP projections so far into the future?

• We ignore short-term cyclical variations (very hard to predict) and focus on long-term supply side fundamentals (slightly easier)

• Assume no major global catastrophes or political shifts that cut economies off from the flow of new technologies and ideas that drive long-term growth

Growth in the World in 2050 model is driven by four main supply side factors (using a Cobb-Douglas production function):

4Long term global economic trends and implications for Nigeria •

Section 1 – World in 2050: motivation and methodology

Working-age population

growth

Investment in physical capital

Investment in human capital

Catch-up with US total factor

productivity levels

Focus on GDP at PPPs, but include market exchange rate projections

PwCJune 2015

Key findings from World in 2050

5

2Long term global economic trends and implications for Nigeria •

PwCJune 2015

NGAVNMBGD IND PHL IDN PAK ZAF EGY MYS COL MEX THA CHN TUR SAU BRA ARG AUS POL IRN USA GBR KOR CAN RUS FRA ESP NLD ITA DEU JPN(1%)

0%

1%

2%

3%

4%

5%

6%

Average Pop Growth p.a % Average Real Growth per capita p.a % Average GDP growth p.a. (in domestic currency)

9ef92bd9d6a54b2fbc899ce8d1e1389c

b8593a17f74d4771ba0c68b210a20f5b

Column Stacked

Breakdown of average real GDP growth (in domestic currency/PPPs)Nigeria projected to have highest average annual growth rate (5.3% p.a.) during the period to 2050. Chinese growth slows sharply in long run (3.4% average).

6Long term global economic trends and implications for Nigeria •

Section 2 – Key findings from World in 2050

Nigeria (but depends on high rate of population growth)

ChinaIndia

US Euro areaand Japan

PwCJune 2015

GDP growth profile of major economies - reversion to the meanGrowth in China will moderate sharply after 2020 – could grow at only 2.5-3% p.a. by the 2040s. Indian growth will also slow after 2020, but much less sharply.

7Long term global economic trends and implications for Nigeria •

Section 2 – Key findings from World in 2050

Brazil Russia India China US UK EU World

0%

1%

2%

3%

4%

5%

6%

7%

Growth profile of BRICs, US, EU and the World

2014 - 2020 2021 - 2030 2031 - 2040 2041 - 2050

Av

era

ge

an

nu

al

% c

ha

ng

e i

n G

DP

, P

PP

Col-umn Regular

c73ec2a58c7047d7ab11f4e82b912ffb

Nigeria also expected to see somedeceleration in growth from 6-7%in medium term to 5-6% in long run

PwCJune 2015

CHN IND USA IDN BRA MEX JPN RUS NGA DEU GBR SAU FRA TUR PAK EGY KOR ITA CAN PHL THA VNM BGD MYS IRN ESP ZAF AUS COL ARG POL NLD

0%

20%

40%

60%

80%

100%

120%

140%

160%

GDP rankings, 2050 (USA = 100%)

Col-umn Regular

0db1bc3627df46408df1cf150347595d

GDP rankings (at PPPs and MERs) in 2050 (USA = 100)By 2050, our model suggests that China, the US and India are likely to be by far the three largest economies in the world

8Long term global economic trends and implications for Nigeria •

Section 2 – Key findings from World in 2050

Large gap between Big 3 and

rest by 2050.

Source: PwC projections (first bar shows GDP at PPPs, second bar GDP at MERs)

Nigeria – could move into top 10 by 2050 (15-18% of US GDP)

PwCJune 2015

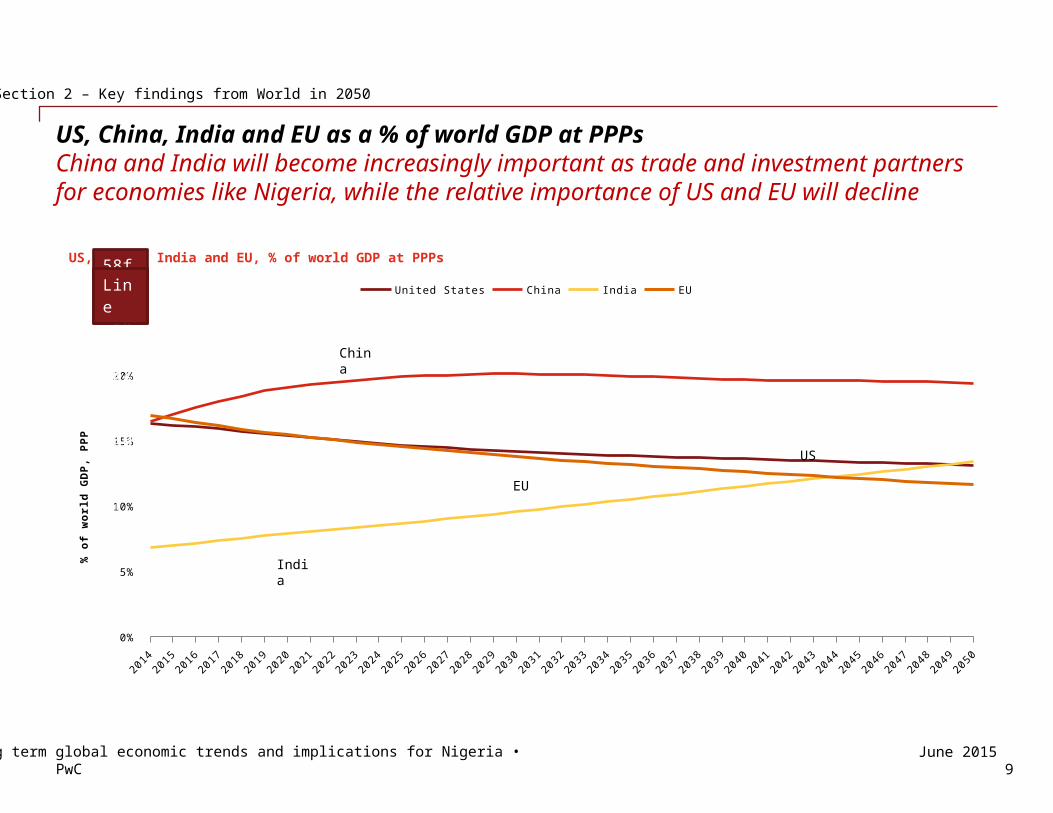

US, China, India and EU as a % of world GDP at PPPsChina and India will become increasingly important as trade and investment partners for economies like Nigeria, while the relative importance of US and EU will decline

9Long term global economic trends and implications for Nigeria •

Section 2 – Key findings from World in 2050

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

0%

5%

10%

15%

20%

25%

US, China, India and EU, % of world GDP at PPPs

United States China India EU

% o

f w

orl

d G

DP

, P

PP

32974fe197e441208967eda957b6-cabf

58f95ea816054c5fb2fcf4128662458b

Line

China

India

EU

US

PwCJune 2015

Population projections for major economies China and India will account for about 3 billion of the world’s total population by 2050

10Long term global economic trends and implications for Nigeria •

Section 2 – Key findings from World in 2050

IND CHN USA NGA IDN JPN EU7

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2014 2020 2030 2040 2050

Col-umn Regular

aa1b58966c6b44f78188fd2aa6ea98c8

Nigeria has fastest growing population(440m by 2050 – 3rd largest in world)

Source: UN projections

PwCJune 2015

GDP per capita of key economies in 2050Average income levels of advanced economies in 2050 will still be much higher than emerging economies – Nigeria still lagging well behind at 17% of US level in 2050

Long term global economic trends and implications for Nigeria

2 Key findings from World in 2050

United States

United Kingdom

Turkey Mexico South Africa China Brazil Indonesia India Nigeria -

10

20

30

40

50

60

70

80

90

100

GDP per capita, PPP (USA = 100)

Col-umn Regular

4d968135c0194b0883d28af9577ef-fce

11

Nigeria

PwCJune 2015

The importance of institutions

12

3Long term global economic trends and implications for Nigeria •

PwCJune 2015

PwC ESCAPE Index - Methodology

ESCAPE Index

Economic1. GDP per capita, PPP2. GDP per capita (previous 10 year CAGR

%)3. Annual inflation 4. General government gross debt5. Adjusted trade openness6. Total investment7. Unemployment rate8. Current account balance (% of GDP)

Social 1. Life expectancy at birth2. Average years of total

schooling3. GINI Index4. Most people can be trusted

(%)

Environmental1. Access to an improved

water source2. CO2 emissions

Political1. Political stability 2. Control of corruption3. Rule of law4. Ease of doing business

index

Communications1. Internet users2. Mobile cellular suscriptions

40%

10% 20%

20% 10%

20 variables

5% weight each

Normalised

42 countries

13Long term global economic trends and implications for Nigeria •

Section 3 – The importance of institutions

PwCJune 2015

PwC ESCAPE Index – emerging economies still lag behind in quality of political and economic institutions

Long term global economic trends and implications for Nigeria

3 The importance of institutions

Sweden

Singa

pore

Indo

nesia

Mex

ico

Turke

y

Brazil

Indi

a

South

Africa

Niger

ia0

10

20

30

40

50

60

70

80

Index f

or

2013

(glo

bal

avera

ge =

50)

14

Nigeria

PwCJune 2015

The importance of institutionsRelative weaknesses of largest emerging markets based on PwC ESCAPE Index components – Nigeria has several key institutional weaknesses to addressCountry Economic growth and stability Political and social institutions

China Credit bubble might pose future problems Ease of doing business, political stability, rule of law, income inequality

India Inflation, current account deficit Political stability, corruption, rule of law, income inequality, ease of doing business

Brazil Inflation, investment to GDP ratio, current account deficit, government debt

Low trust levels

Russia Low investment to GDP ratio Corruption, income inequality

Indonesia Inflation, current account deficit Corruption, income inequality

Mexico GDP per capita growth, low investment to GDP ratio Corruption, rule of law, trust, ease of doing business

Nigeria Low investment to GDP ratio Political stability, income inequality, corruption, rule of law, ease of doing business

15Long term global economic trends and implications for Nigeria •

Section 3 – The importance of institutions

PwCJune 2015

Implications for Nigeria: challenges and opportunities for growth

16

4Long term global economic trends and implications for Nigeria •

PwCJune 2015

Challenges for Nigeria

1.Political stability, corruption and the rule of law – requires great political will and consensus for change to underpin long-term reform (c.f. UK in 19th century, US in early 20th century, SE Asia since 1960s/70s)

2.Infrastructure investment – energy (particularly power supply to reduce dependence on diesel), transport, communications, water, sanitation

3.Education – aiming for Asian levels of achievement in maths and science

4.Poverty and income inequality – broader and more progressive tax system with increased compliance; increased investment in healthcare, education and better public services (which people will expect if taxes rise)

5.Jobs – critical to avoid the demographic dividend becoming a curse, which also requires more investment in education and skills

6.Diversification – to reduce reliance on oil for exports and government revenues, reducing exposure to global shocks and rent-seeking behaviour – the fall in oil prices since mid-2014 provides an incentive to move faster on this.

17Long term global economic trends and implications for Nigeria •

Section 4 – Implications for Nigeria

PwCJune 2015

Opportunities for growth in Nigerian output and jobs

•Retail and consumer: rapidly expanding middle class should drive growth (but need to reduce reliance on imports of consumer goods and address issues on land availability for large modern stores and road quality for logistics)

•Agriculture: need to raise yields through mechanisation, greater use of fertilisers, shift to higher value crops and greater economies of scale

•Manufacturing: under-developed (c.7% of GDP) but could grow rapidly in areas like food processing, automotive and textiles if supported by investment in power supply, better transport links and a more skilled labour force

•Construction: could be a boom area with continued urbanisation and increased infrastructure investment

•Financial and professional services: after the post-crisis reforms, financial sector is more stable and professional services could grow on the back of this expansion as Lagos becomes a key finance hub in Africa

•Strategies need to be tailored to strengths of individual States

18Long term global economic trends and implications for Nigeria •

Section 4 – Implications for Nigeria

PwCJune 2015

Discussion

19

5Long term global economic trends and implications for Nigeria •

Contacts and website

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

The full report and other supporting material are available at:http://www.pwc.com/world2050

This forms part of our wider Megatrends research programme:http://www.pwc.co.uk/issues/megatrends/

John HawksworthChief Economist, PwC UKT: +44 (0) 20 7213 1650 E: [email protected]