Embed Size (px)

Citation preview

LondonHouston

WashingtonNew YorkPortlandCalgary

SantiagoBogota

Rio de JaneiroSingapore

BeijingTokyo

SydneyDubai

MoscowAstana

KievPorto

JohannesburgRiga

Market Reporting

Consulting

Events

Challenges and opportunities for the inland waterwaysInland Ports and Terminals Annual Conference, Shreveport, Louisiana

Todd Tranausky, North American Transportation Editor30 April 2015

illuminating the markets

• World’s largest independently held energy markets PRA – 600 staff, 23 countries

• Publish > 8,000 daily commodity price assessments + energy market intelligence

• Recent acquisitions◦ DeWitt, JJ&A (Petrochemicals)◦ FMB (Fertilizers)◦ Wax Data◦ Metal-Pages◦ MetalPrices.com

• Coverage expansions◦ US Natural Gas◦ Base Oils

• Services◦ Price reporting and indexation◦ Consulting◦ Conferences

• Indexation examples◦ Global crude oil and condensate◦ US refined products (incl. VGO)◦ Global base oils

Argus Media: global, market-focused, independent

Copyright © 2015 Argus Media Ltd. All rights reserved.

Copyright © 2015 Argus Media Ltd. All rights reserved.

Argus Publications

• Argus covers all aspects of commodity movement

• Argus Petroleum Transportation focuses on the pricing of petroleum product movements

• Argus Coal Transportation focuses on coal moving across all modes

Market Reporting

Consulting

Events

Issues and opportunity on the inland waterways

Copyright © 2015 Argus Media Ltd. All rights reserved.

State of the inland waterway system

Potential opportunities in changing traffic mix

Weather and lock and dam issues

Necessary investments in infrastructure

Where the industry can focus its attention

• Significant delays to movements

◦ High water

◦ Lock closures

• Extra equipment needed to cope with conditions, volumes

• Demand increasing

◦ Dry bulk and liquids

• Uncertainty about the future

Copyright © 2015 Argus Media Ltd. All rights reserved.

Conditions facing shippers and operators

Copyright © 2015 Argus Media Ltd. All rights reserved.

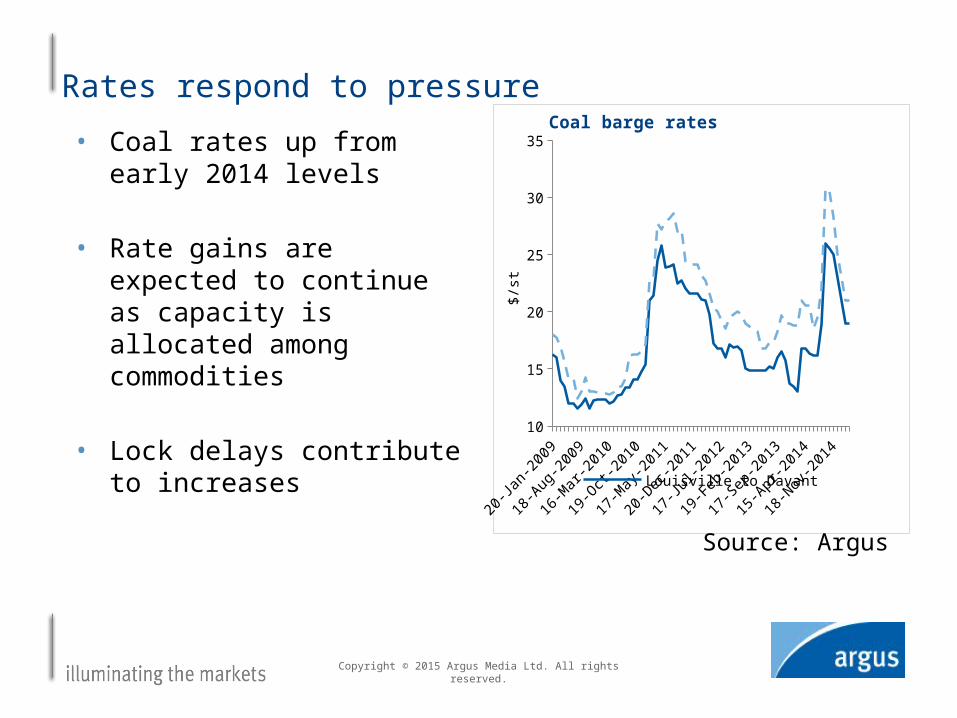

Rates respond to pressure

Jan 0910

15

20

25

30

35Coal barge rates

Louisville to Davant$

/st

• Coal rates up from early 2014 levels

• Rate gains are expected to continue as capacity is allocated among commodities

• Lock delays contribute to increases

Source: Argus

Copyright © 2015 Argus Media Ltd. All rights reserved.

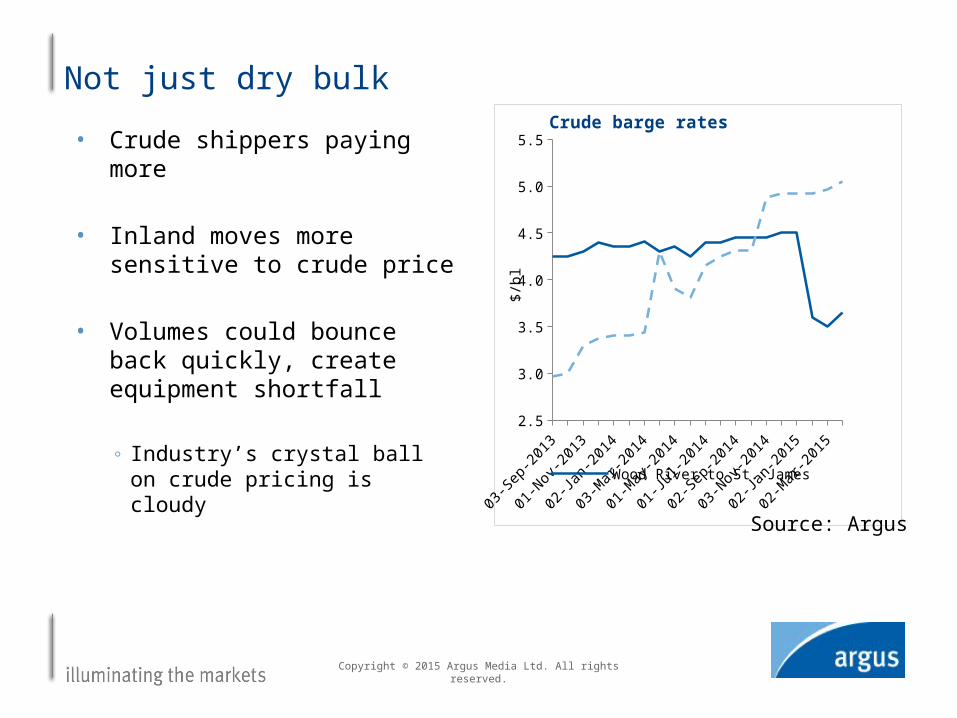

• Crude shippers paying more

• Inland moves more sensitive to crude price

• Volumes could bounce back quickly, create equipment shortfall

◦ Industry’s crystal ball on crude pricing is cloudy

Not just dry bulk

Sep 13 Dec 13 Apr 14 Aug 14 Dec 14 Apr 152.5

3.0

3.5

4.0

4.5

5.0

5.5Crude barge rates

Wood River to St. JamesCorpus Christi to St. James

$/b

l

Source: Argus

Market Reporting

Consulting

Events

Future traffic mix changes

Copyright © 2015 Argus Media Ltd. All rights reserved.

• Demand outpaced supply in 2013, early 2014

◦ Created a need for shippers to find rail alternative

• Potential reduced dramatically by drilling slowdown

◦ Barge is the swing mode for this traffic

• Will give railroads ability to catch up, create potential oversupply

◦ Eliminating the sense of crisis shippers felt last year

Sand’s growth potential

Copyright © 2015 Argus Media Ltd. All rights reserved.

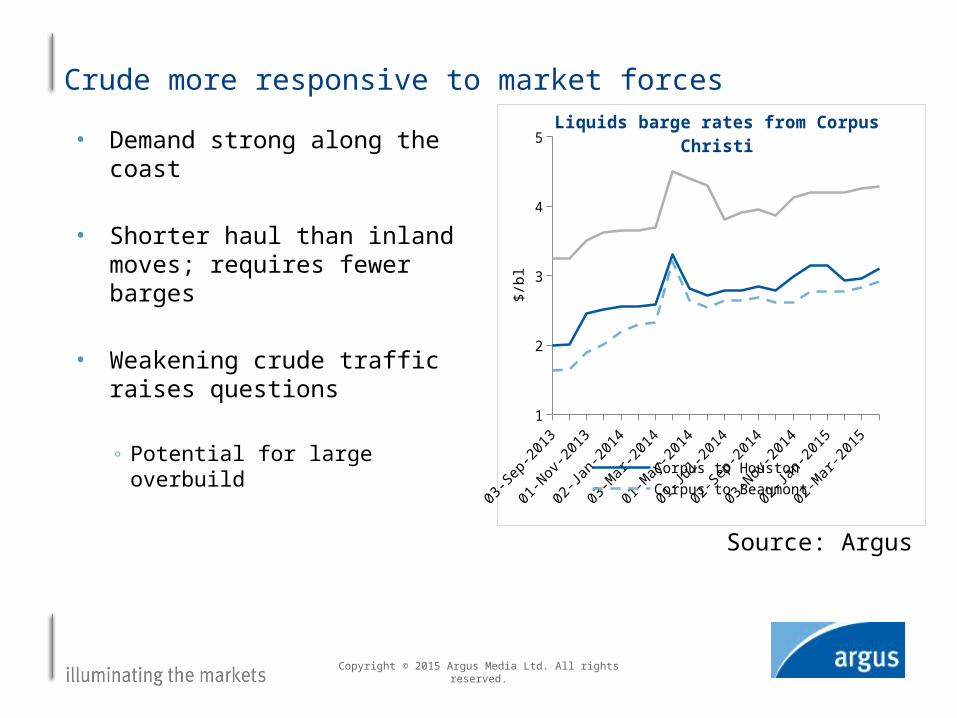

• Demand strong along the coast

• Shorter haul than inland moves; requires fewer barges

• Weakening crude traffic raises questions

◦ Potential for large overbuild

Crude more responsive to market forces

Sep 13 Dec 13 Apr 14 Aug 14 Dec 14 Apr 151

2

3

4

5Liquids barge rates from Corpus

Christi

Corpus to HoustonCorpus to Beaumont

$/b

l

Source: Argus

Copyright © 2015 Argus Media Ltd. All rights reserved.

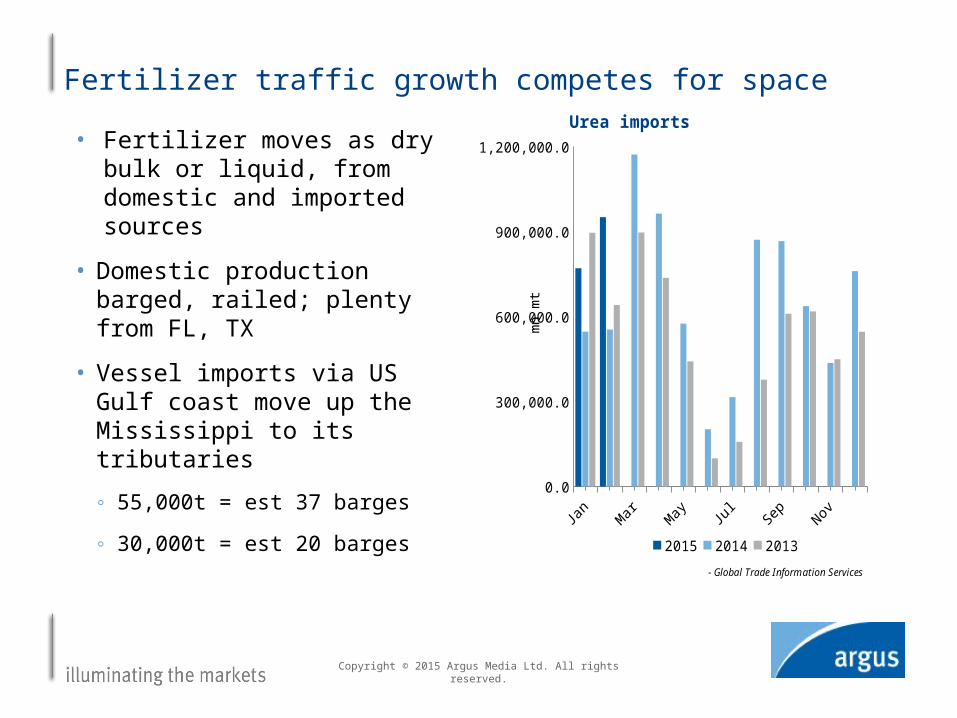

• Fertilizer moves as dry bulk or liquid, from domestic and imported sources

• Domestic production barged, railed; plenty from FL, TX

• Vessel imports via US Gulf coast move up the Mississippi to its tributaries

◦ 55,000t = est 37 barges

◦ 30,000t = est 20 barges

Fertilizer traffic growth competes for space

Jan Apr Jul Oct0.0

300,000.0

600,000.0

900,000.0

1,200,000.0

Urea imports

2015 2014 2013

- Global Trade Information Services

mn

mt

Market Reporting

Consulting

Events

Conditions set stage for growth, challenges

Copyright © 2015 Argus Media Ltd. All rights reserved.

• Increasing amounts of salt, fertilizer on barges

• Grain seeks barge backup for rail, but volumes could decline

◦ Currency issues dent exports

◦ More domestic traffic handled by trucks, rail

• Barge operators are likely to hold capacity for committed contract shippers

Dry bulk commodities increase waterway reliance

Copyright © 2015 Argus Media Ltd. All rights reserved.

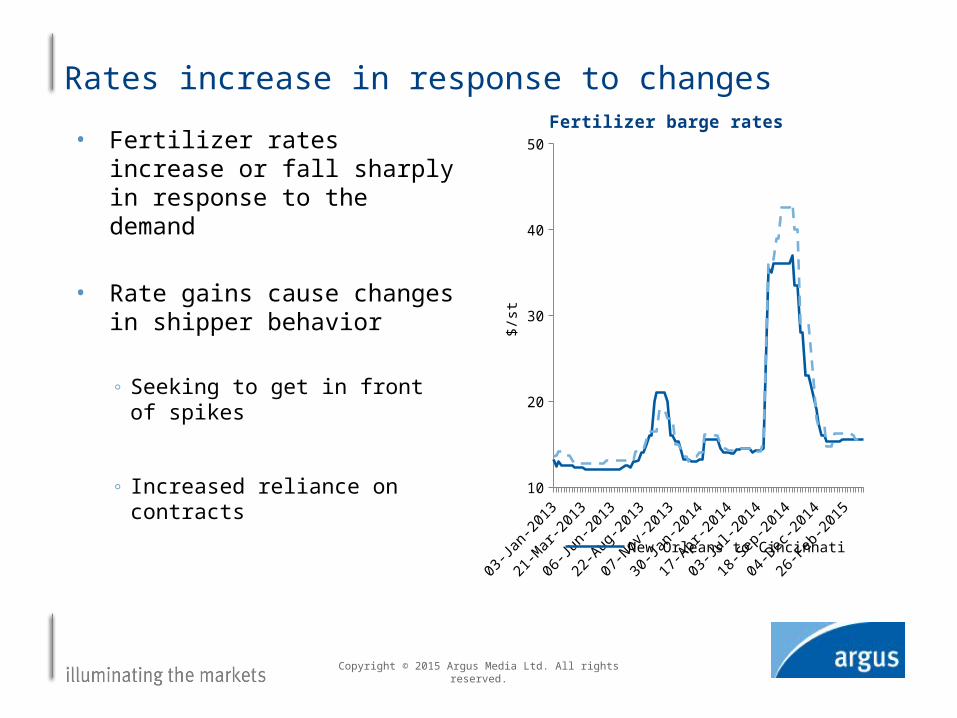

• Fertilizer rates increase or fall sharply in response to the demand

• Rate gains cause changes in shipper behavior

◦ Seeking to get in front of spikes

◦ Increased reliance on contracts

Rates increase in response to changes

Jan 13 Jun 13 Dec 13 May 14 Nov 14 Apr 1510

20

30

40

50

Fertilizer barge rates

New Orleans to Cincinnati

$/s

t

Copyright © 2015 Argus Media Ltd. All rights reserved.

• Ice and high water slowed or stalled barges

◦ Loading delayed by flooding at docks

◦ High waters slow transits, lower tonnages

• Adverse conditions forced at least one barge company to halt shipments on the Big Sandy river this month

• Additional tug requirements and slower transits create reliability issues

Weather complicates shipments in 2015

Copyright © 2015 Argus Media Ltd. All rights reserved.

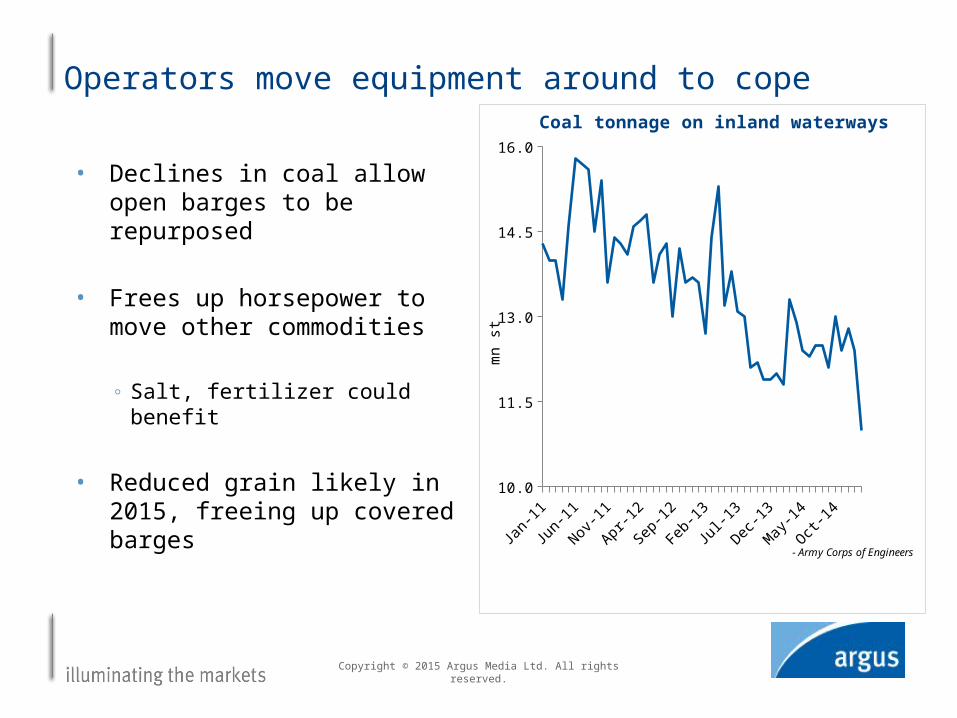

• Declines in coal allow open barges to be repurposed

• Frees up horsepower to move other commodities

◦ Salt, fertilizer could benefit

• Reduced grain likely in 2015, freeing up covered barges

Operators move equipment around to cope

Jan 11 Oct 11 Aug 12 Jun 13 Apr 14 Feb 1510.0

11.5

13.0

14.5

16.0

Coal tonnage on inland waterways

- Army Corps of Engineers

mn

st

Copyright © 2015 Argus Media Ltd. All rights reserved.

• Lock work planned across the river system later this year

◦ Ohio River Lock and dam 52 and 53 could cause delays

• Inola/Catoosa could be completely shut off by lock closures later this year

◦ But high water levels could allow lock to be bypassed

• High water is postponing some work, making the summer and early fall even more prone to delays

Maintenance will present further disruptions

Copyright © 2015 Argus Media Ltd. All rights reserved.

• Advocating for Congress to fund improvements

• Not appearing to customers that the system is failure prone and that shipments might face delays

• Reliability underpins pricing power of operators, creating a balancing act

Industry faces conundrum over disruptions

Market Reporting

Consulting

Events

Financing upgrades

Copyright © 2015 Argus Media Ltd. All rights reserved.

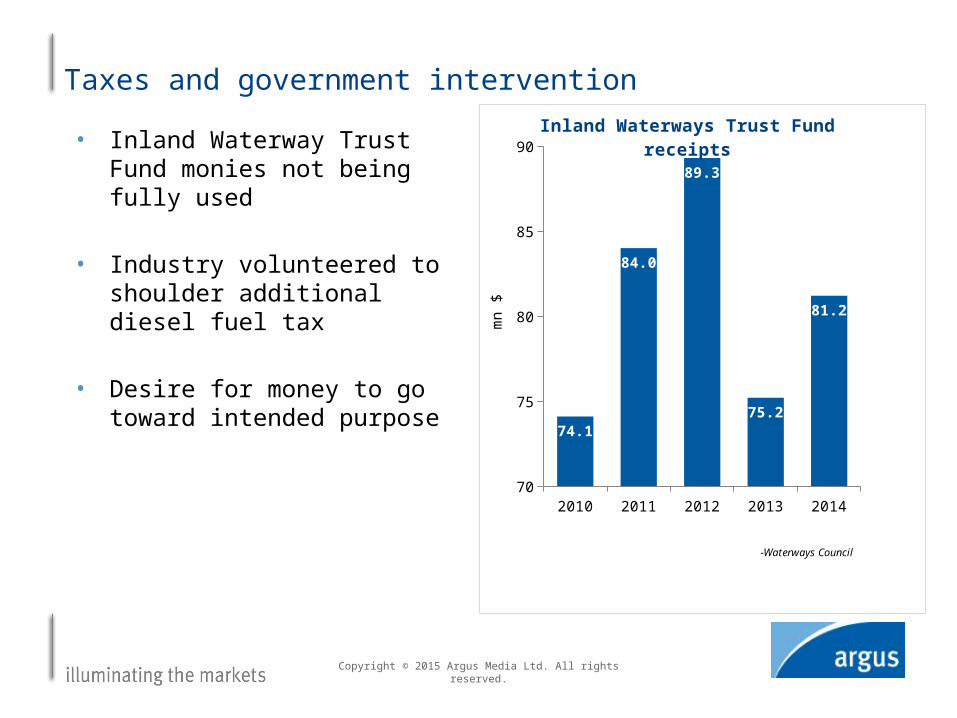

• Inland Waterway Trust Fund monies not being fully used

• Industry volunteered to shoulder additional diesel fuel tax

• Desire for money to go toward intended purpose

Taxes and government intervention

2010 2011 2012 2013 201470

75

80

85

90

74.1

84.0

89.3

75.2

81.2

Inland Waterways Trust Fund receipts

-Waterways Council

mn

$

Copyright © 2015 Argus Media Ltd. All rights reserved.

• Industry waiting on Corps and Congress to set direction, funding levels

• New bill allows $100mn/yr for waterways projects

• Proposed FY 2016 budget down 13pc, “not adequate” for dredging and maintaining existing network

Congress, Army Corps hold the cards

Copyright © 2015 Argus Media Ltd. All rights reserved.

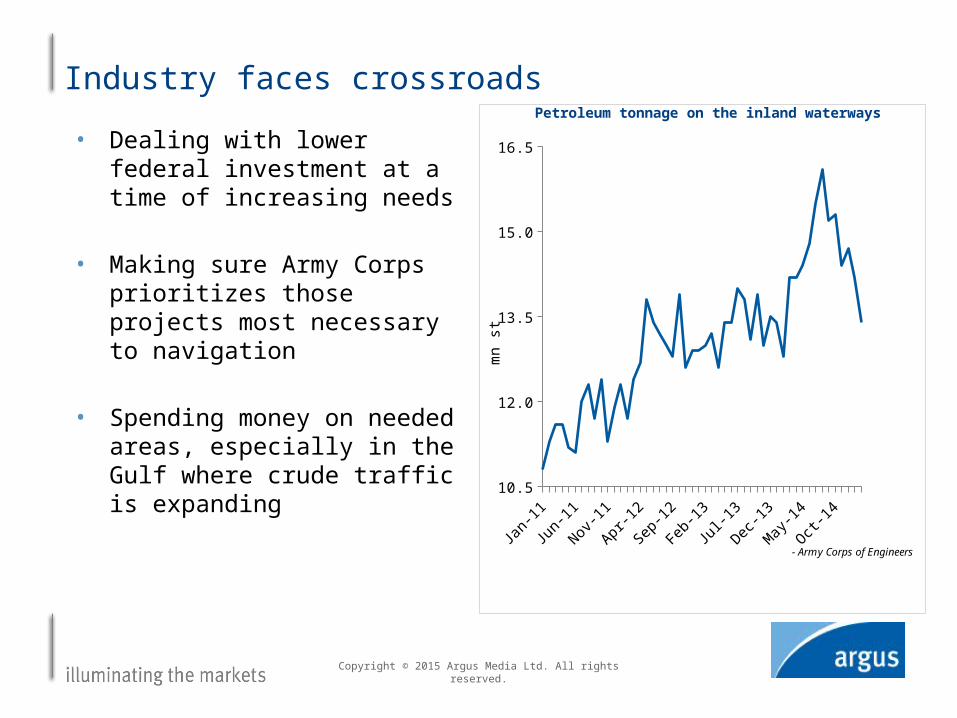

• Dealing with lower federal investment at a time of increasing needs

• Making sure Army Corps prioritizes those projects most necessary to navigation

• Spending money on needed areas, especially in the Gulf where crude traffic is expanding

Industry faces crossroads

Jan 11 Oct 11 Aug 12 Jun 13 Apr 14 Feb 1510.5

12.0

13.5

15.0

16.5

- Army Corps of Engineers

mn

st

Petroleum tonnage on the inland waterways

Market Reporting

Consulting

Events

Final thoughts

Copyright © 2015 Argus Media Ltd. All rights reserved.

Rates are likely to rise as capacity tightens

Delays have the potential to get worse

Lock and dam infrastructure is cause for concern

Industry needs to take lead to ensure financing is adequate

Key takeaways for operators, shippers

Copyright notice Copyright © 2015 Argus Media Ltd. All rights reserved. All intellectual property rights in this presentation and the information herein are the exclusive property of Argus and and/or its licensors and may only be used under licence from Argus. Without limiting the foregoing, by reading this presentation you agree that you will not copy or reproduce any part of its contents (including, but not limited to, single prices or any other individual items of data) in any form or for any purpose whatsoever without the prior written consent of Argus. Trademark notice ARGUS, the ARGUS logo, ARGUS MEDIA, ARGUS DIRECT, ARGUS OPEN MARKETS, AOM, FMB, DEWITT, JIM JORDAN & ASSOCIATES, JJ&A, FUNDALYTICS, METAL-PAGES, METALPRICES.COM, Argus publication titles and Argus index names are trademarks of Argus Media Limited.

Disclaimer All data and other information presented (the “Data”) are provided on an “as is” basis. Argus makes no warranties, express or implied, as to the accuracy, adequacy, timeliness, or completeness of the Data or fitness for any particular purpose. Argus shall not be liable for any loss or damage arising from any party’s reliance on the Data and disclaims any and all liability related to or arising out of use of the Data to the full extent permissible by law.

Todd TranauskyNorth American Transportation Editor

[email protected]+1 713-400-7835Houstonwww.argusmedia.com