Embed Size (px)

Citation preview

Air Cargo Day Switzerland

Zurich, June 2014

Logistics of

tomorrow –

Challenges and

opportunities in the

air cargo industry

2 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

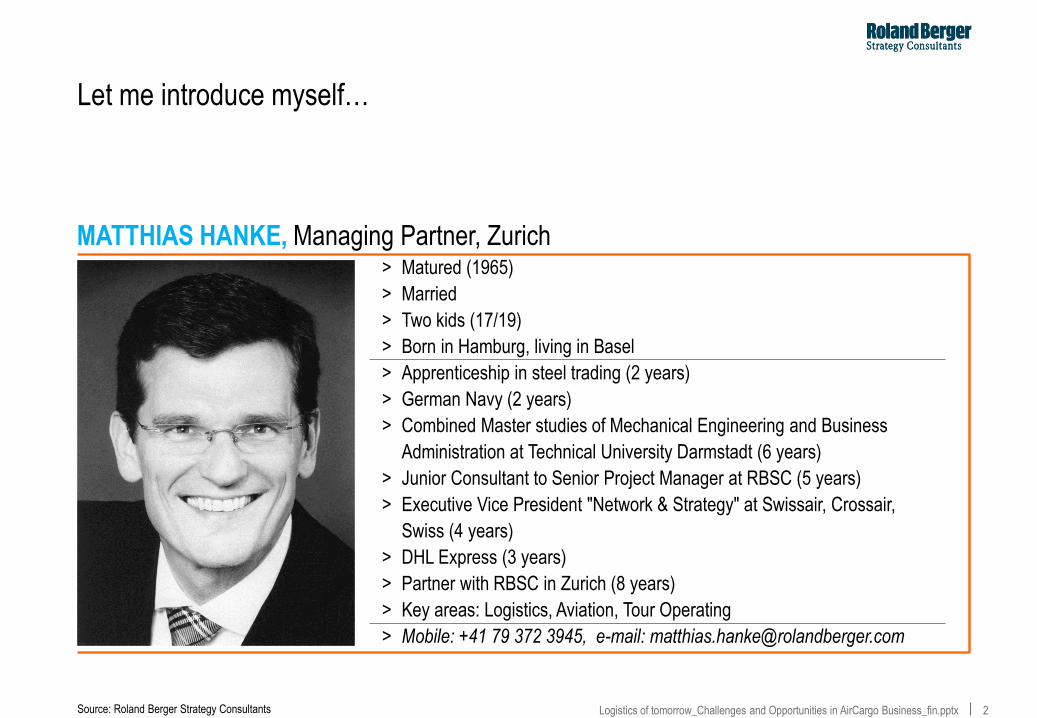

Let me introduce myself…

MATTHIAS HANKE, Managing Partner, Zurich > Matured (1965)

> Married

> Two kids (17/19)

> Born in Hamburg, living in Basel

> Apprenticeship in steel trading (2 years)

> German Navy (2 years)

> Combined Master studies of Mechanical Engineering and Business

Administration at Technical University Darmstadt (6 years)

> Junior Consultant to Senior Project Manager at RBSC (5 years)

> Executive Vice President "Network & Strategy" at Swissair, Crossair,

Swiss (4 years)

> DHL Express (3 years)

> Partner with RBSC in Zurich (8 years)

> Key areas: Logistics, Aviation, Tour Operating

> Mobile: +41 79 372 3945, e-mail: [email protected]

Source: Roland Berger Strategy Consultants

3 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

…and let me introduce our company

Founded in 1967 in Germany by Roland Berger

51 offices in 36 countries, with 2.500 employees

About 200 RB Partners currently serving

~1.000 international clients

Our scope and global reach

Source: Roland Berger Strategy Consultants

4 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

This document shall be treated as confidential. It has been compiled for the exclusive, internal use by our client and is not complete without the underlying detail analyses and the oral presentation. It may

not be passed on and/or may not be made available to third parties without prior written consent from Roland Berger Strategy Consultants. RBSC does not assume any responsibility for the completeness

and accuracy of the statements made in this document.

© Roland Berger Strategy Consultants

Contents Page

This document shall be treated as confidential. It has been compiled for the exclusive, internal use by our client and is not complete without the underlying detail analyses and the oral presentation. It may

not be passed on and/or may not be made available to third parties without prior written consent from Roland Berger Strategy Consultants. RBSC does not assume any responsibility for the completeness

and accuracy of the statements made in this document.

© Roland Berger Strategy Consultants

A. The European air cargo market is dealing currently with demand stagnation and

growing overcapacity 5

B. Air cargo carriers find themselves in a "commodity trap" 16

C. Potential escape-ways from the commodity-trap have to be actively paved by top

management 23

5 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

A. The European air-cargo

market is currently

dealing with demand

stagnation and growing

overcapacity

6 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

Competition in the airfreight market is becoming fiercer – Business model under

pressure

Summary

GENERAL TRENDS IN WORLD TRADE

> Trade-lanes to/from Europe are rather stagnating – fastest growing trade-lanes in Intra-Asia

> Historically low seafreight rates paired with low interest rates drive shippers to rethink their transportation strategy

> Overcapacities in sea- and airfreight are contributing to high volatility of rates and overall price pressure

> Overcapacity in airfreight especially fuelled by growing belly-space to/from the MEAST with impact on South-East Asia business

> Traditional "airfreight industries" enforcing a modal shift from air to sea in the past years

> Legacy market barriers within the airfreight segment are loosing their relevance

> Airfreight rates are seasonally volatile – overall so far stable … but for how long?

> Air-cargo carriers find themselves in a commodity trap – the current business model is under pressure

IMPLICATIONS FOR THE AIR-CARGO INDUSTRY

Source: Roland Berger Strategy Consultants

7 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

7

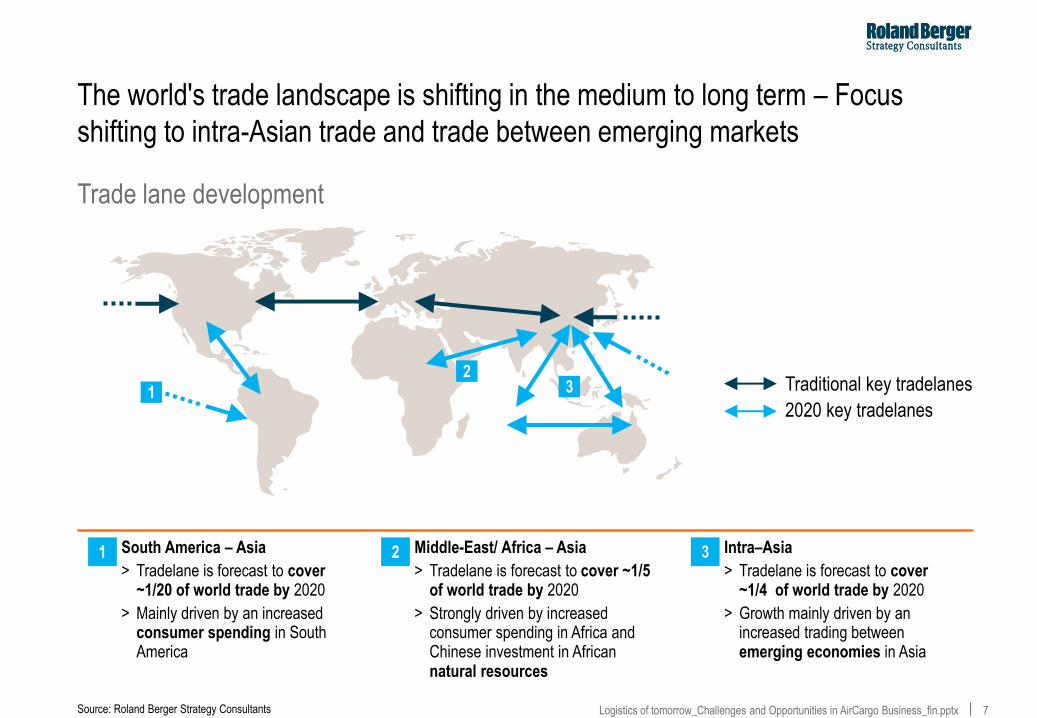

The world's trade landscape is shifting in the medium to long term – Focus

shifting to intra-Asian trade and trade between emerging markets

Traditional key tradelanes

2020 key tradelanes 1

2 3

1 South America – Asia

> Tradelane is forecast to cover ~1/20 of world trade by 2020

> Mainly driven by an increased consumer spending in South America

2 Middle-East/ Africa – Asia

> Tradelane is forecast to cover ~1/5 of world trade by 2020

> Strongly driven by increased consumer spending in Africa and Chinese investment in African natural resources

3 Intra–Asia

> Tradelane is forecast to cover ~1/4 of world trade by 2020

> Growth mainly driven by an increased trading between emerging economies in Asia

Trade lane development

Source: Roland Berger Strategy Consultants

8 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

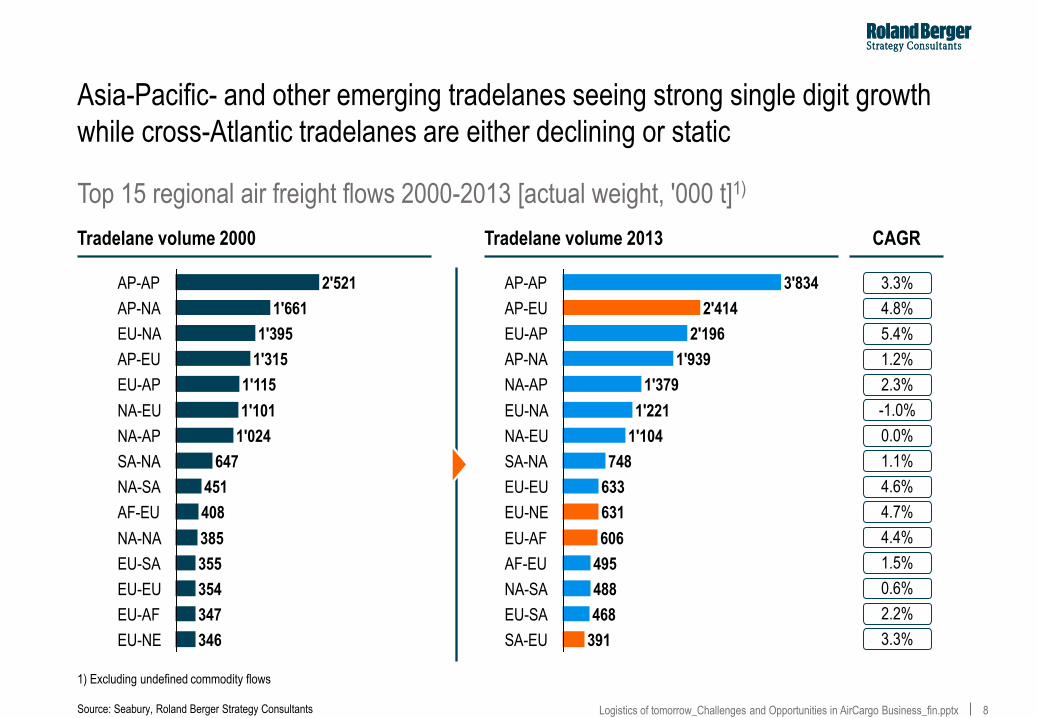

Asia-Pacific- and other emerging tradelanes seeing strong single digit growth

while cross-Atlantic tradelanes are either declining or static

Top 15 regional air freight flows 2000-2013 [actual weight, '000 t]1)

Source: Seabury, Roland Berger Strategy Consultants

1) Excluding undefined commodity flows

EU-NA

AP-AP

AP-NA 1′661

2′521

1′395

AP-EU

EU-AP

NA-EU

647

451

408

NA-NA

EU-AF

EU-EU

EU-NE

EU-SA

NA-AP

SA-NA

NA-SA

AF-EU

1′315

1′115

1′101

1′024

385

355

354

347

346

1′104

633

1′379 NA-AP

631

EU-NA

748

EU-NE

SA-NA

EU-EU

NA-EU

1′221

AP-NA 1′939

EU-AP 2′196

AP-EU 2′414

AP-AP 3′834

AF-EU

EU-SA

EU-AF

NA-SA

606

SA-EU

495

488

468

391

3.3%

3.3%

4.8%

5.4%

1.2%

2.3%

-1.0%

0.0%

1.1%

4.6%

4.7%

4.4%

1.5%

0.6%

2.2%

Tradelane volume 2000 Tradelane volume 2013 CAGR

9 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

During the next ~20 years China will take over USA's role as the dominant

trading nation

9

Status Origin Destination Value

1 China USA 594,741

2 China Japan 336,183

3 China Korea 281,140

4 China India 263,063

5 China Germany 201,382

6 Japan USA 189,785

7 China Singapore 178,291

8 NEW China Indonesia 169,356

9 Germany USA 167,467

10 NEW China Malaysia 162,376

11 NEW China Nigeria 151,570

12 Germany UK 144,131

13 UK USA 143,725

14 NEW China Thailand 141,201

15 NEW China Saudi Arabia 140,320

16 NEW China Brazil 136,295

17 NEW USA India 125,826

18 NEW China UK 121,603

19 NEW China UAE 120,318

20 China Australia 117,340

IMPACT

> New tradelanes are growing in importance for the air cargo industry

> China expected to become a new driver – origin or destination for 15 of the top 20 tradelanes

> Tradelanes from developing economies will be bilateral, instead of mainly focusing on export to developed countries

> Development changes the focus of the industry and creates challenges to build up a presence in new markets

Source: Roland Berger Strategy Consultants

Top 20 tradelanes 2030 [value of goods, sea and air]

10 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

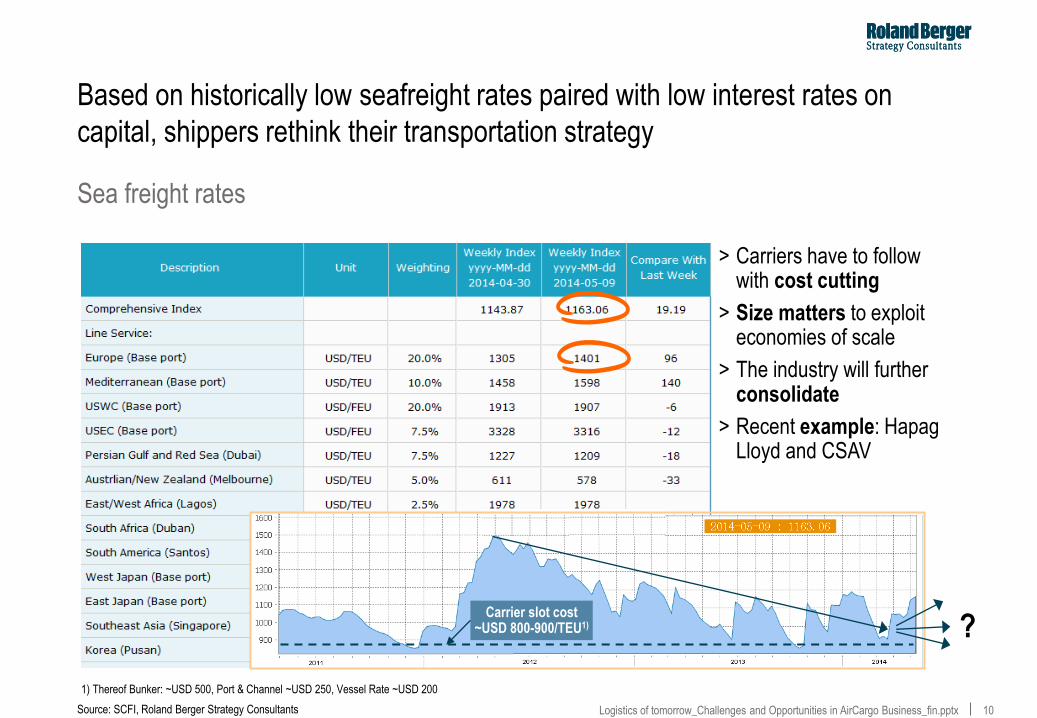

Based on historically low seafreight rates paired with low interest rates on

capital, shippers rethink their transportation strategy

Sea freight rates

Carrier slot cost ~USD 800-900/TEU1) ?

> Carriers have to follow with cost cutting

> Size matters to exploit economies of scale

> The industry will further consolidate

> Recent example: Hapag Lloyd and CSAV

Source: SCFI, Roland Berger Strategy Consultants

1) Thereof Bunker: ~USD 500, Port & Channel ~USD 250, Vessel Rate ~USD 200

11 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

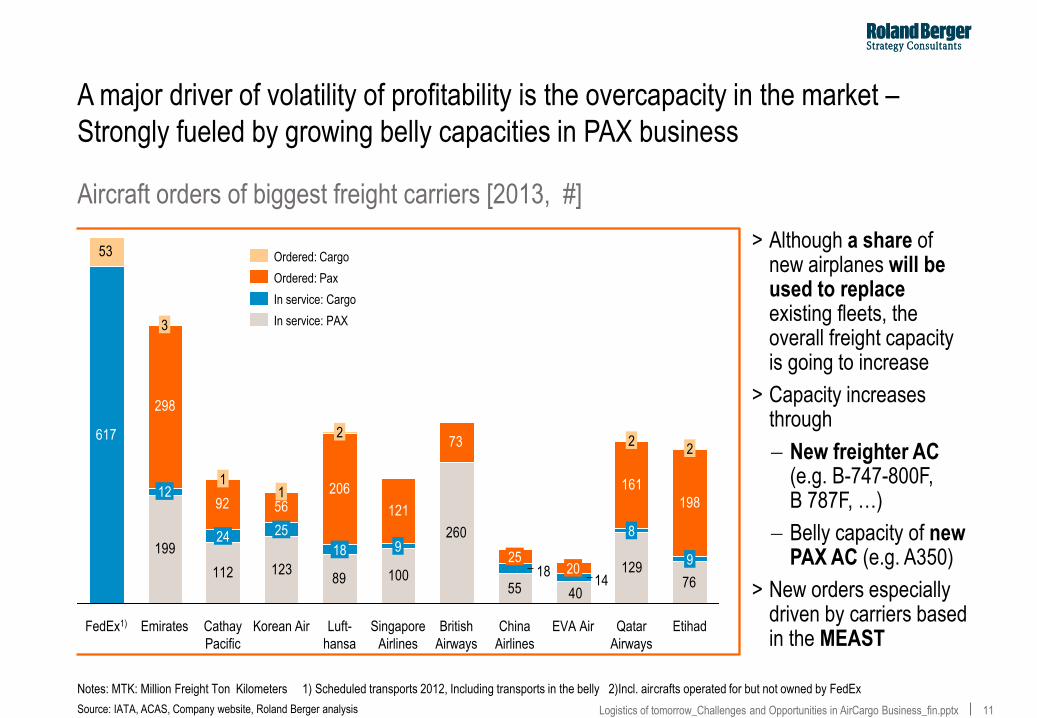

A major driver of volatility of profitability is the overcapacity in the market –

Strongly fueled by growing belly capacities in PAX business

> Although a share of new airplanes will be used to replace existing fleets, the overall freight capacity is going to increase

> Capacity increases through

New freighter AC (e.g. B-747-800F, B 787F, …)

Belly capacity of new PAX AC (e.g. A350)

> New orders especially driven by carriers based in the MEAST

Source: IATA, ACAS, Company website, Roland Berger analysis

Notes: MTK: Million Freight Ton Kilometers 1) Scheduled transports 2012, Including transports in the belly 2)Incl. aircrafts operated for but not owned by FedEx

Aircraft orders of biggest freight carriers [2013, #]

199

112 12389 100

260

55

12976

298

92 56

206

121

73

161

198

4014

18

617

53

FedEx1)

3

1 1

Etihad

9

Qatar

Airways

8

EVA Air

20

China

Airlines

25

British

Airways

25

Cathay

Pacific

24

Emirates

12

Singapore

Airlines

9

Luft-

hansa

18

Korean Air

2 2

2

Ordered: Cargo

In service: PAX

In service: Cargo

Ordered: Pax

12 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

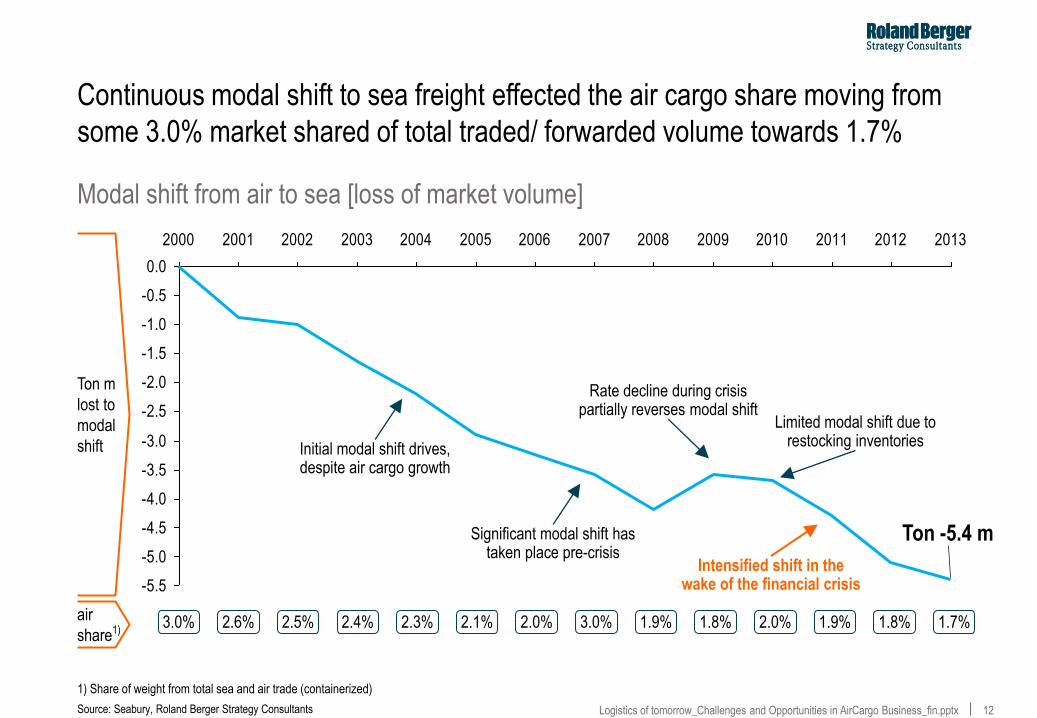

Continuous modal shift to sea freight effected the air cargo share moving from

some 3.0% market shared of total traded/ forwarded volume towards 1.7%

Source: Seabury, Roland Berger Strategy Consultants

Modal shift from air to sea [loss of market volume]

1) Share of weight from total sea and air trade (containerized)

-5.5

-5.0

-4.5

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ton -5.4 m

3.0% 1.7% 2.6% 2.5% 2.4% 2.3% 2.1% 2.0% 3.0% 1.9% 1.8% 2.0% 1.9% 1.8%

Ton m

lost to

modal

shift

air

share1)

Initial modal shift drives, despite air cargo growth

Rate decline during crisis partially reverses modal shift

Limited modal shift due to restocking inventories

Intensified shift in the wake of the financial crisis

Significant modal shift has taken place pre-crisis

13 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

13

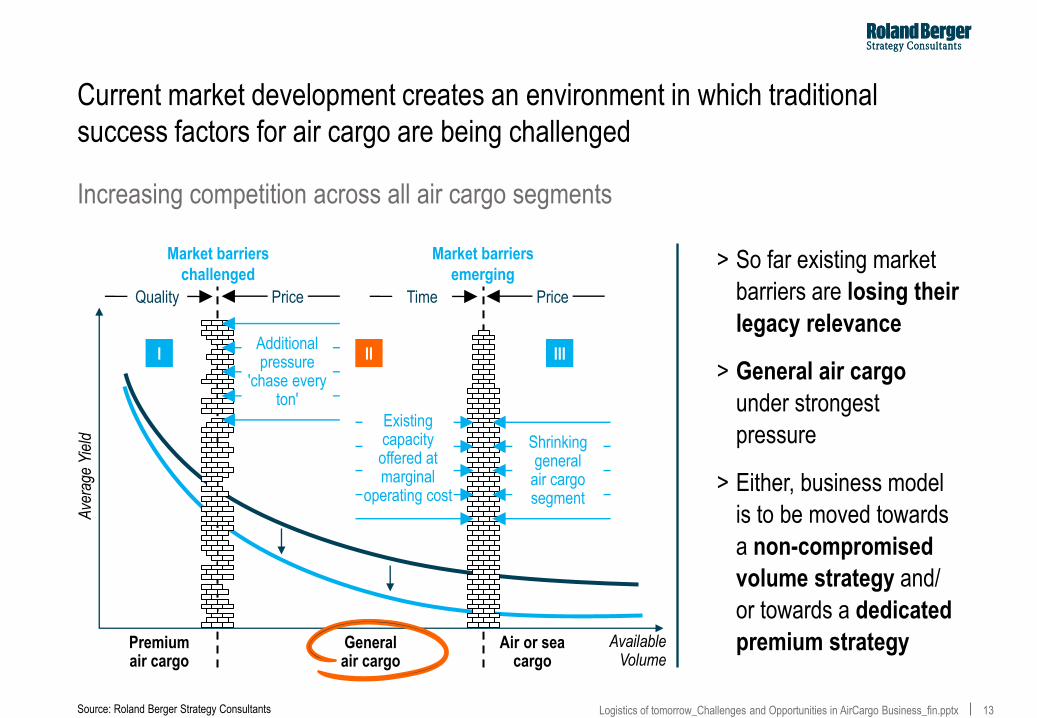

Current market development creates an environment in which traditional

success factors for air cargo are being challenged

> So far existing market

barriers are losing their

legacy relevance

> General air cargo

under strongest

pressure

> Either, business model

is to be moved towards

a non-compromised

volume strategy and/

or towards a dedicated

premium strategy

Source: Roland Berger

Available Volume

Premium air cargo

General air cargo

Air or sea cargo

III

Market barriers

challenged

Market barriers

emerging

Quality Price Time Price

Ave

rage

Yie

ld

II I Additional pressure

'chase every ton'

Shrinking general

air cargo segment

Existing capacity offered at marginal

operating cost

Increasing competition across all air cargo segments

Source: Roland Berger Strategy Consultants

14 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

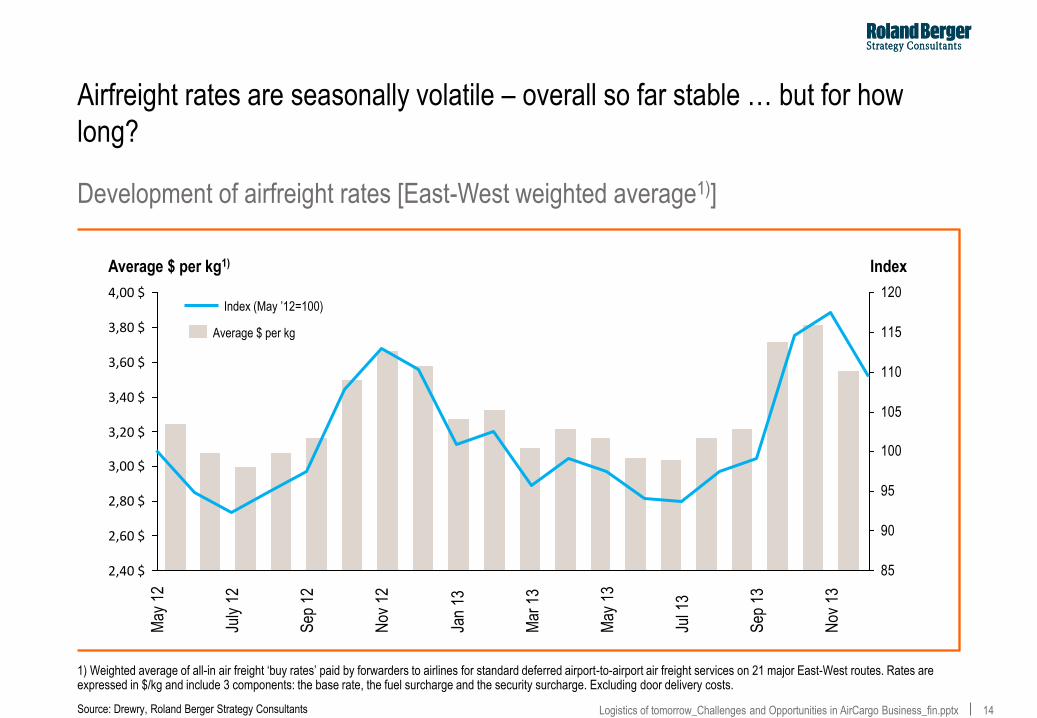

Airfreight rates are seasonally volatile – overall so far stable … but for how

long?

Development of airfreight rates [East-West weighted average1)]

Average $ per kg1)

Source: Drewry, Roland Berger Strategy Consultants

3,00 $

4,00 $

3,80 $

2,40 $

3,60 $

3,40 $

2,60 $

3,20 $

2,80 $

85

90

95

100

105

110

115

120S

ep 1

2

July

12

Jan

13

May

13

Jul 1

3

May

12

Nov

12

Sep

13

Mar

13

Nov

13

Average $ per kg

Index (May ’12=100)

1) Weighted average of all-in air freight ‘buy rates’ paid by forwarders to airlines for standard deferred airport-to-airport air freight services on 21 major East-West routes. Rates are expressed in $/kg and include 3 components: the base rate, the fuel surcharge and the security surcharge. Excluding door delivery costs.

Index

15 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

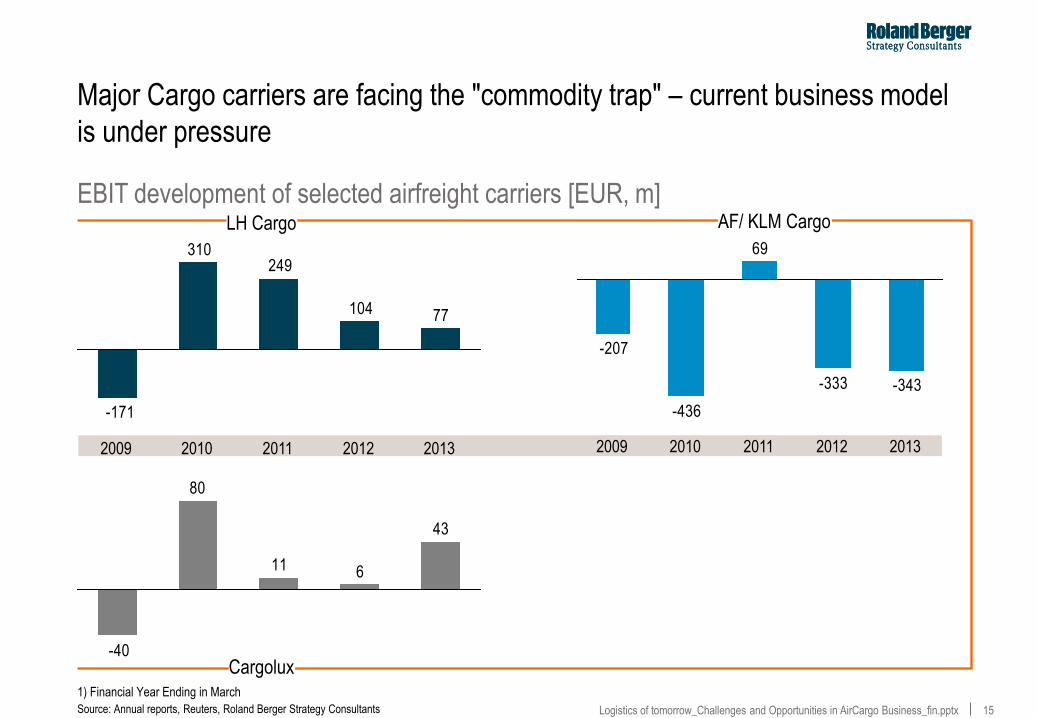

Major Cargo carriers are facing the "commodity trap" – current business model

is under pressure

EBIT development of selected airfreight carriers [EUR, m]

-343-333

69

-436

-207

2009 2012 2013 2011 2010

Source: Annual reports, Reuters, Roland Berger Strategy Consultants

1) Financial Year Ending in March

104

249310

-171

77

2013 2012 2011 2010 2009

43

611

80

-40

LH Cargo AF/ KLM Cargo

Cargolux

16 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

B. Air Cargo carriers find

themselves in a

"commodity trap"

17 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

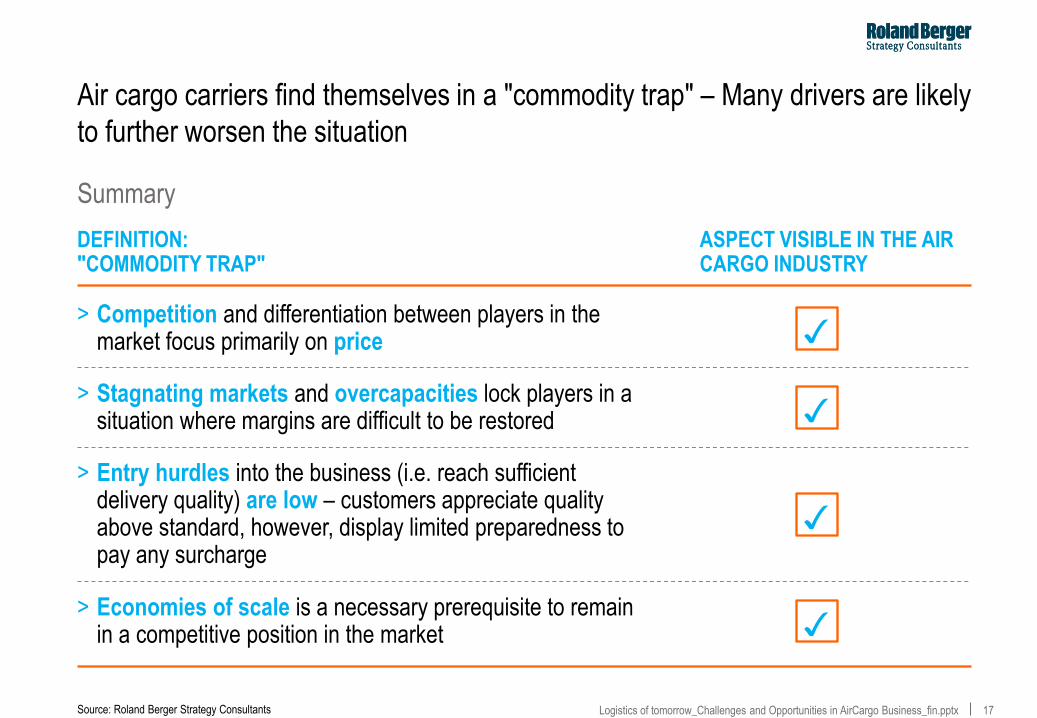

Air cargo carriers find themselves in a "commodity trap" – Many drivers are likely

to further worsen the situation

DEFINITION: "COMMODITY TRAP"

> Competition and differentiation between players in the market focus primarily on price

ASPECT VISIBLE IN THE AIR CARGO INDUSTRY

Source: Roland Berger Strategy Consultants

Summary

> Stagnating markets and overcapacities lock players in a situation where margins are difficult to be restored

> Entry hurdles into the business (i.e. reach sufficient delivery quality) are low – customers appreciate quality above standard, however, display limited preparedness to pay any surcharge

> Economies of scale is a necessary prerequisite to remain in a competitive position in the market

✓

✓

✓

✓

18 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

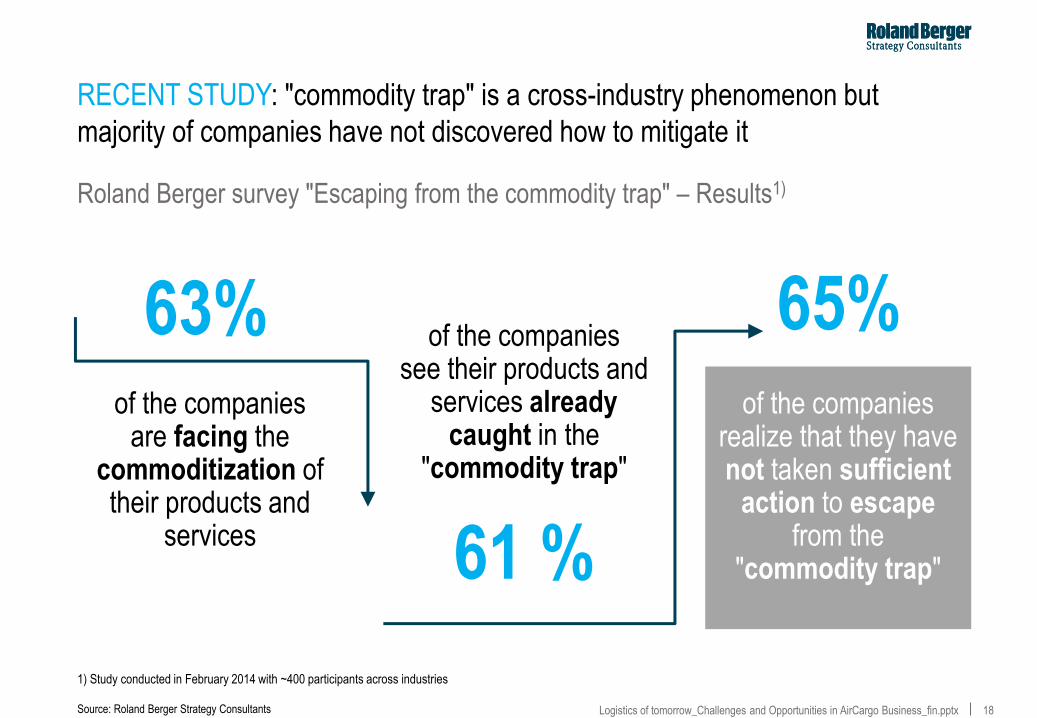

RECENT STUDY: "commodity trap" is a cross-industry phenomenon but

majority of companies have not discovered how to mitigate it

Roland Berger survey "Escaping from the commodity trap" – Results1)

1) Study conducted in February 2014 with ~400 participants across industries

61 %

63% 65% of the companies

are facing the commoditization of their products and

services

of the companies see their products and

services already caught in the

"commodity trap"

of the companies realize that they have not taken sufficient

action to escape from the

"commodity trap"

Source: Roland Berger Strategy Consultants

19 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

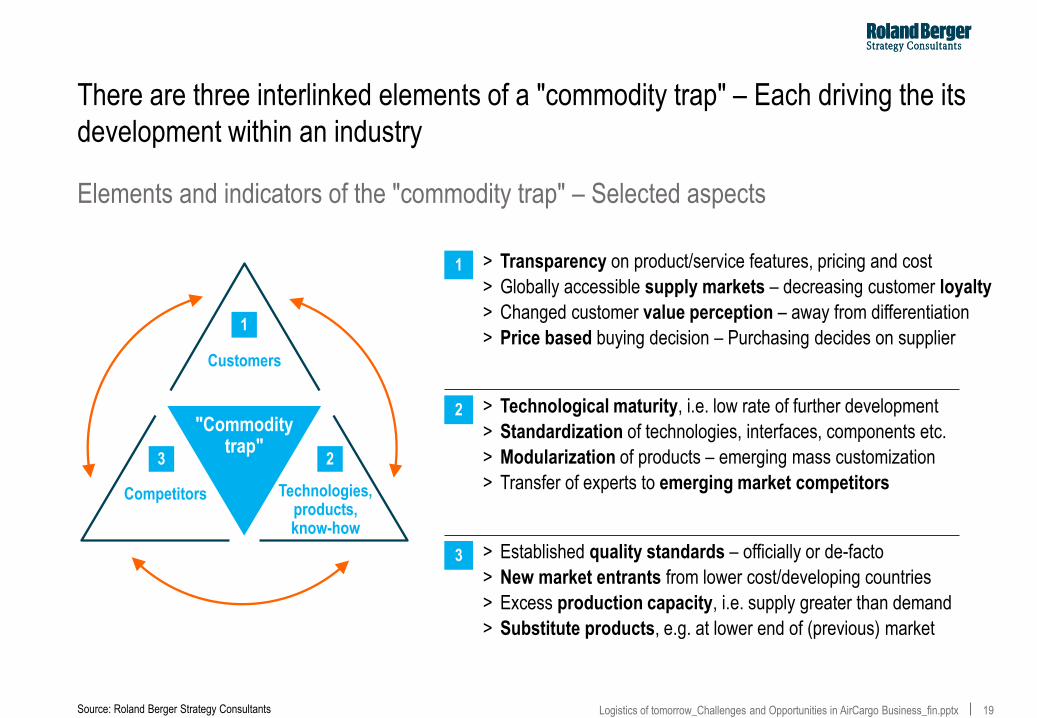

There are three interlinked elements of a "commodity trap" – Each driving the its

development within an industry

Elements and indicators of the "commodity trap" – Selected aspects

Technologies, products, know-how

Competitors

Customers

1

2 3

"Commodity trap"

1 > Transparency on product/service features, pricing and cost

> Globally accessible supply markets – decreasing customer loyalty

> Changed customer value perception – away from differentiation

> Price based buying decision – Purchasing decides on supplier

Source: Roland Berger Strategy Consultants

2 > Technological maturity, i.e. low rate of further development

> Standardization of technologies, interfaces, components etc.

> Modularization of products – emerging mass customization

> Transfer of experts to emerging market competitors

3 > Established quality standards – officially or de-facto

> New market entrants from lower cost/developing countries

> Excess production capacity, i.e. supply greater than demand

> Substitute products, e.g. at lower end of (previous) market

20 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

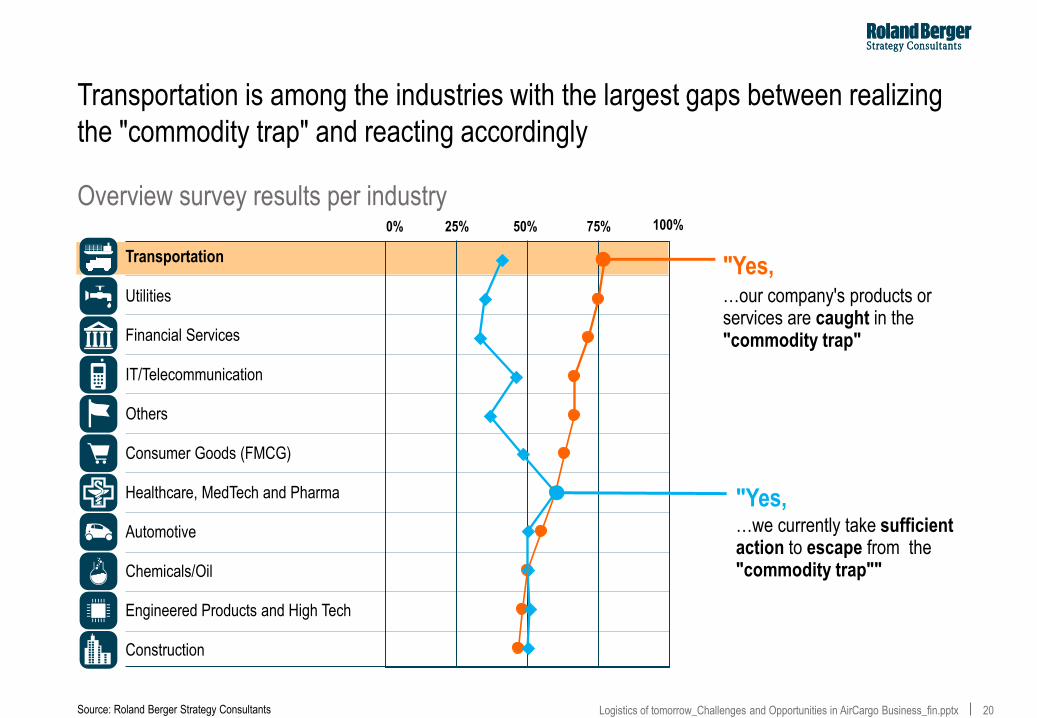

Transportation is among the industries with the largest gaps between realizing

the "commodity trap" and reacting accordingly

Automotive

Chemicals/Oil

Transportation

Consumer Goods (FMCG)

Healthcare, MedTech and Pharma

Construction

IT/Telecommunication

Utilities

Others

Financial Services

Engineered Products and High Tech

Overview survey results per industry 0% 100% 25% 50% 75%

"Yes,

"Yes,

…our company's products or services are caught in the "commodity trap"

…we currently take sufficient action to escape from the "commodity trap""

Source: Roland Berger Strategy Consultants

21 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

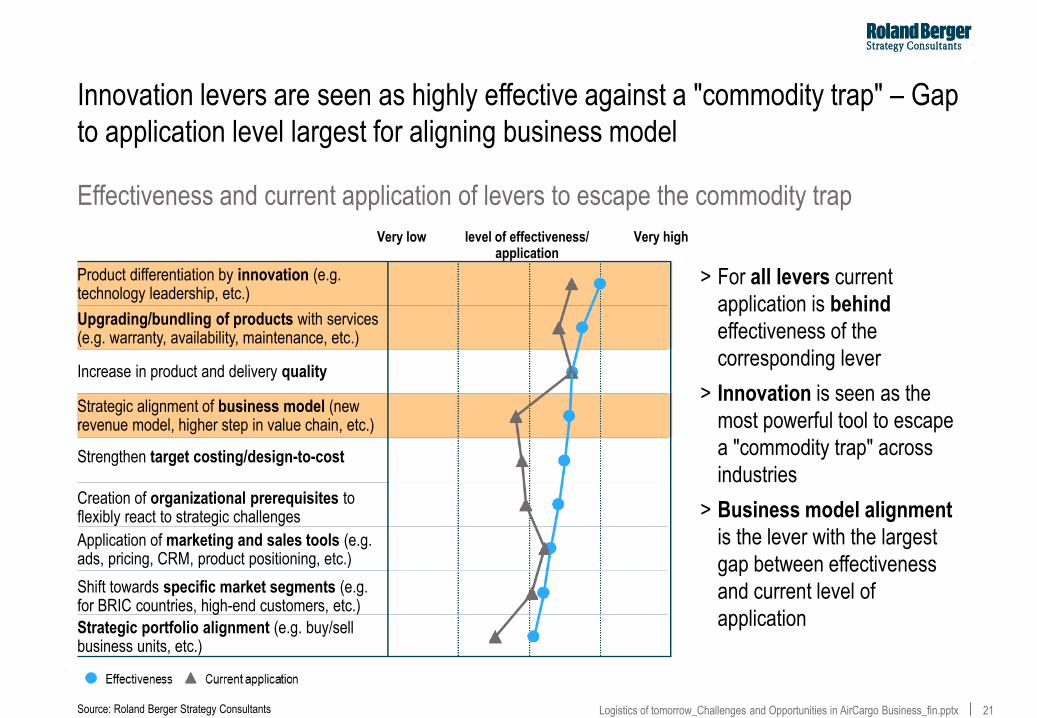

Innovation levers are seen as highly effective against a "commodity trap" – Gap

to application level largest for aligning business model

Very low

Application of marketing and sales tools (e.g. ads, pricing, CRM, product positioning, etc.)

Upgrading/bundling of products with services (e.g. warranty, availability, maintenance, etc.)

Shift towards specific market segments (e.g. for BRIC countries, high-end customers, etc.)

Product differentiation by innovation (e.g. technology leadership, etc.)

Increase in product and delivery quality

Strategic portfolio alignment (e.g. buy/sell business units, etc.)

Strategic alignment of business model (new revenue model, higher step in value chain, etc.)

Creation of organizational prerequisites to flexibly react to strategic challenges

Strengthen target costing/design-to-cost

Effectiveness and current application of levers to escape the commodity trap

> For all levers current

application is behind

effectiveness of the

corresponding lever

> Innovation is seen as the

most powerful tool to escape

a "commodity trap" across

industries

> Business model alignment

is the lever with the largest

gap between effectiveness

and current level of

application

Very high level of effectiveness/ application

Source: Roland Berger Strategy Consultants

22 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

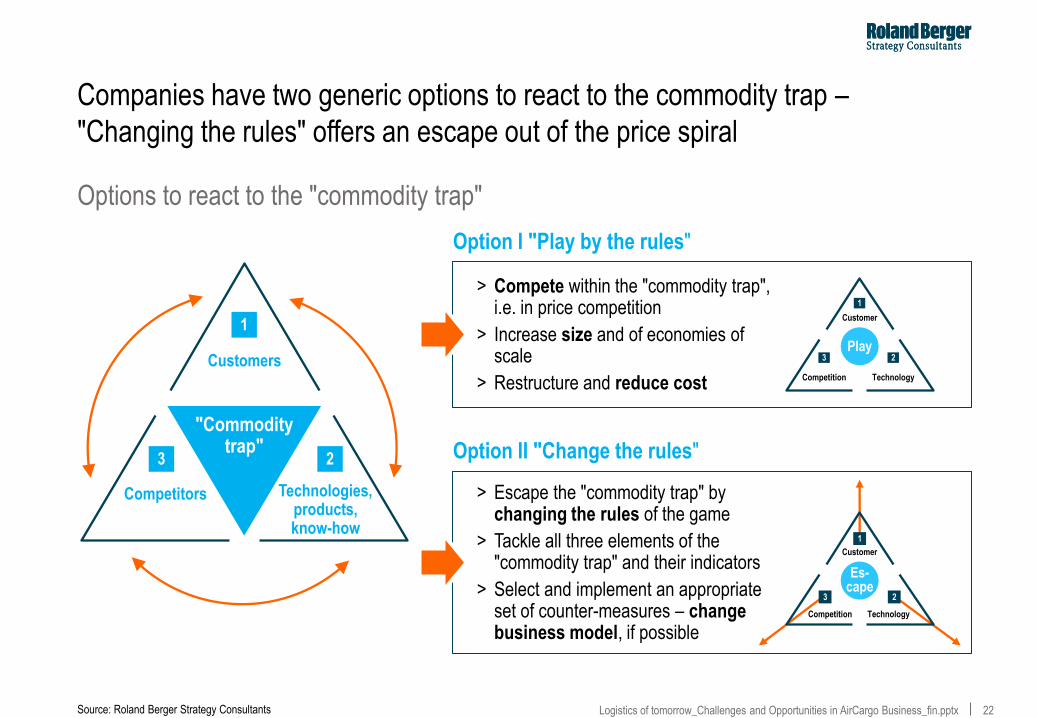

Companies have two generic options to react to the commodity trap –

"Changing the rules" offers an escape out of the price spiral

> Compete within the "commodity trap", i.e. in price competition

> Increase size and of economies of scale

> Restructure and reduce cost

Option I "Play by the rules"

Option II "Change the rules"

> Escape the "commodity trap" by changing the rules of the game

> Tackle all three elements of the "commodity trap" and their indicators

> Select and implement an appropriate set of counter-measures – change business model, if possible

Technology Competition

Customer

1

2 3 Play

Technology Competition

Customer

1

2 3

Es- cape

Source: Roland Berger Strategy Consultants

Options to react to the "commodity trap"

Technologies, products, know-how

Competitors

Customers

1

2 3

"Commodity trap"

23 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

C. Escape-ways from the

commodity-trap have to

be actively paved by top

management

24 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

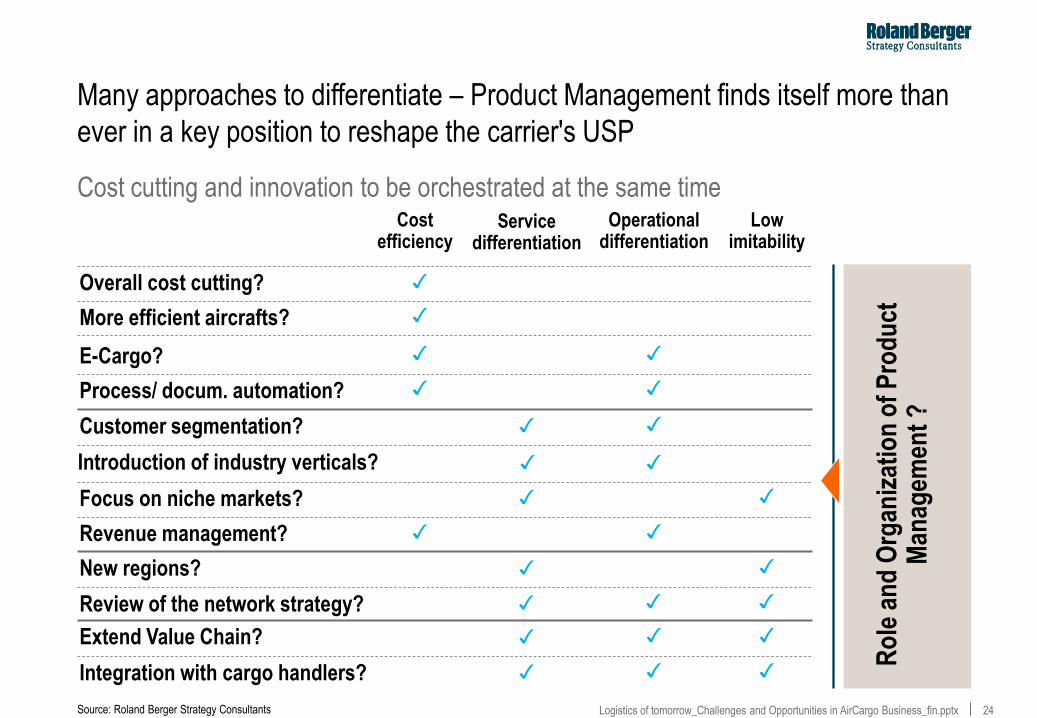

Many approaches to differentiate – Product Management finds itself more than

ever in a key position to reshape the carrier's USP

Cost cutting and innovation to be orchestrated at the same time

Ro

le a

nd

Org

aniz

atio

n o

f P

rod

uct

M

anag

emen

t ?

Cost efficiency

Service differentiation

Operational differentiation

Low imitability

Source: Roland Berger Strategy Consultants

Process/ docum. automation? ✓ ✓

Focus on niche markets? ✓ ✓

More efficient aircrafts? ✓

Integration with cargo handlers? ✓ ✓ ✓

Customer segmentation? ✓ ✓

Revenue management? ✓ ✓

New regions? ✓ ✓

Review of the network strategy?

Extend Value Chain? ✓ ✓ ✓

✓ Overall cost cutting?

Introduction of industry verticals? ✓ ✓

E-Cargo? ✓ ✓

✓ ✓ ✓

25 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

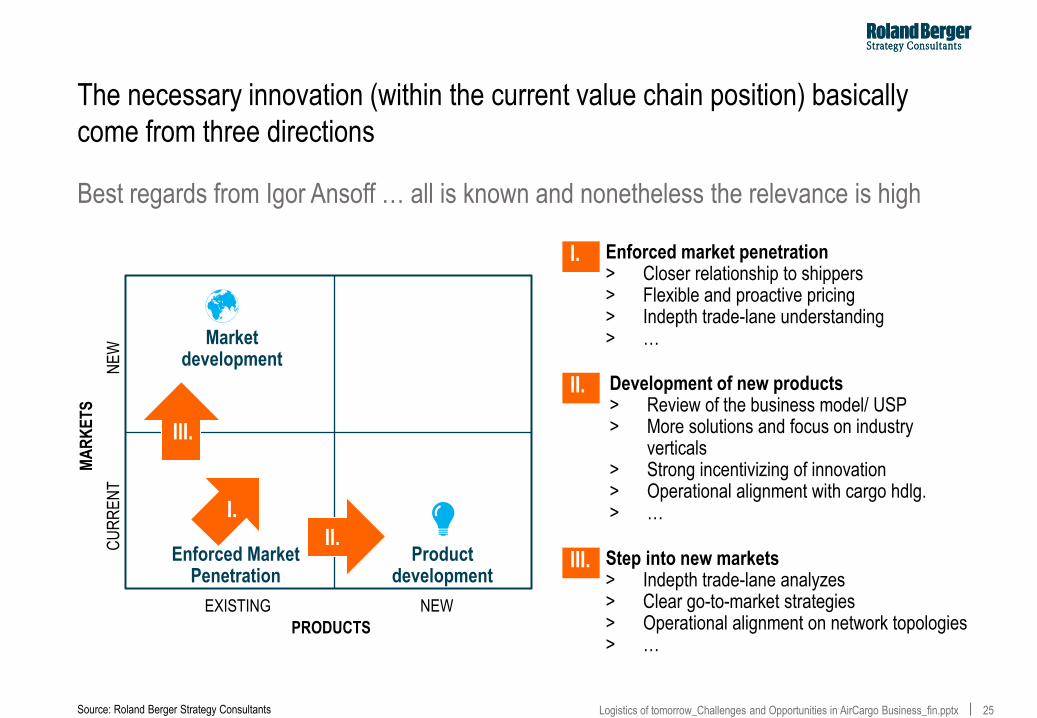

The necessary innovation (within the current value chain position) basically

come from three directions

Best regards from Igor Ansoff … all is known and nonetheless the relevance is high

Source: Roland Berger Strategy Consultants

MA

RK

ET

S

PRODUCTS

NE

W

CU

RR

EN

T

EXISTING NEW

Market development

Enforced Market Penetration

Product development

I.

III.

II.

> Enforced market penetration > Closer relationship to shippers > Flexible and proactive pricing > Indepth trade-lane understanding > …

I.

> Development of new products > Review of the business model/ USP > More solutions and focus on industry

verticals > Strong incentivizing of innovation > Operational alignment with cargo hdlg. > …

II.

> Step into new markets > Indepth trade-lane analyzes > Clear go-to-market strategies > Operational alignment on network topologies > …

III.

26 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

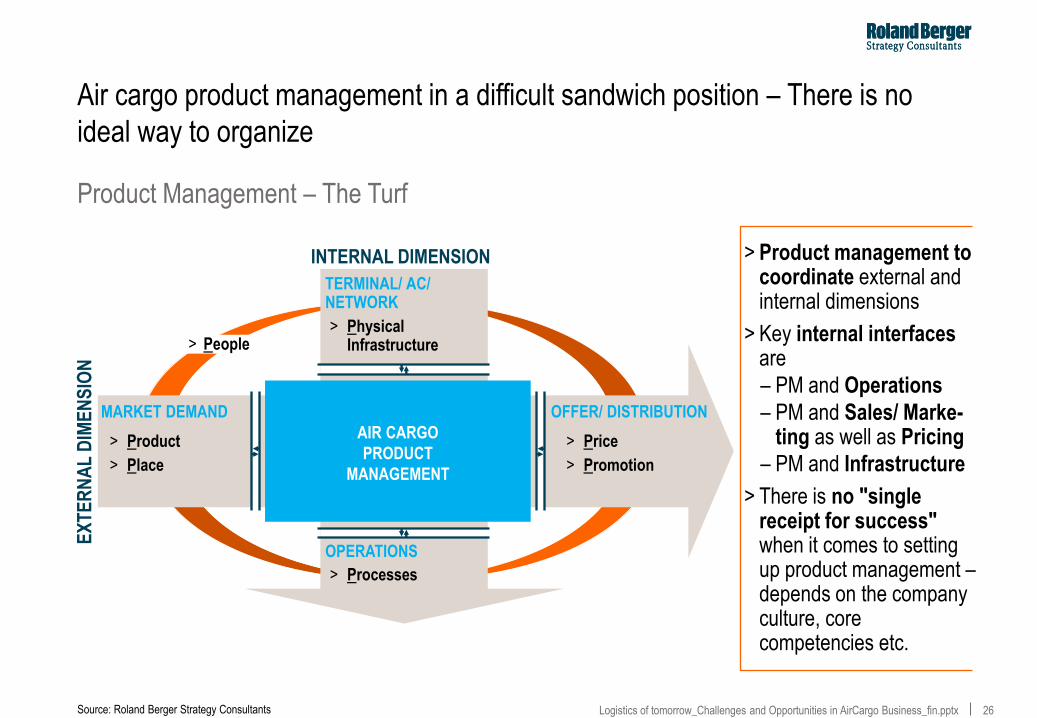

Air cargo product management in a difficult sandwich position – There is no

ideal way to organize

Product Management – The Turf

INTERNAL DIMENSION

EX

TE

RN

AL

DIM

EN

SIO

N

TERMINAL/ AC/ NETWORK

> Physical Infrastructure

OPERATIONS

> Processes

MARKET DEMAND

> Product

> Place

OFFER/ DISTRIBUTION

> Price

> Promotion

AIR CARGO

PRODUCT

MANAGEMENT

> People

> Product management to coordinate external and internal dimensions

> Key internal interfaces are

– PM and Operations

– PM and Sales/ Marke-ting as well as Pricing

– PM and Infrastructure

> There is no "single receipt for success" when it comes to setting up product management – depends on the company culture, core competencies etc.

Source: Roland Berger Strategy Consultants

27 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

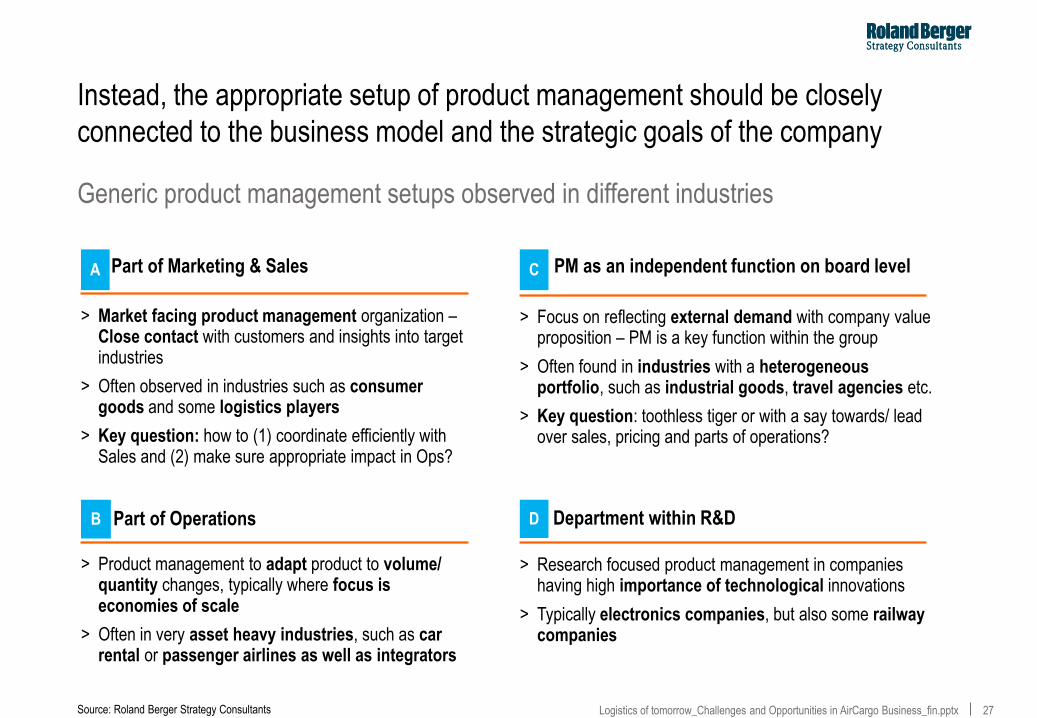

Instead, the appropriate setup of product management should be closely

connected to the business model and the strategic goals of the company

Generic product management setups observed in different industries

Source: Roland Berger Strategy Consultants

Part of Marketing & Sales

> Market facing product management organization – Close contact with customers and insights into target industries

> Often observed in industries such as consumer goods and some logistics players

> Key question: how to (1) coordinate efficiently with Sales and (2) make sure appropriate impact in Ops?

A

Part of Operations

> Product management to adapt product to volume/ quantity changes, typically where focus is economies of scale

> Often in very asset heavy industries, such as car rental or passenger airlines as well as integrators

B Department within R&D

> Research focused product management in companies having high importance of technological innovations

> Typically electronics companies, but also some railway companies

D

PM as an independent function on board level

> Focus on reflecting external demand with company value proposition – PM is a key function within the group

> Often found in industries with a heterogeneous portfolio, such as industrial goods, travel agencies etc.

> Key question: toothless tiger or with a say towards/ lead over sales, pricing and parts of operations?

C

28 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

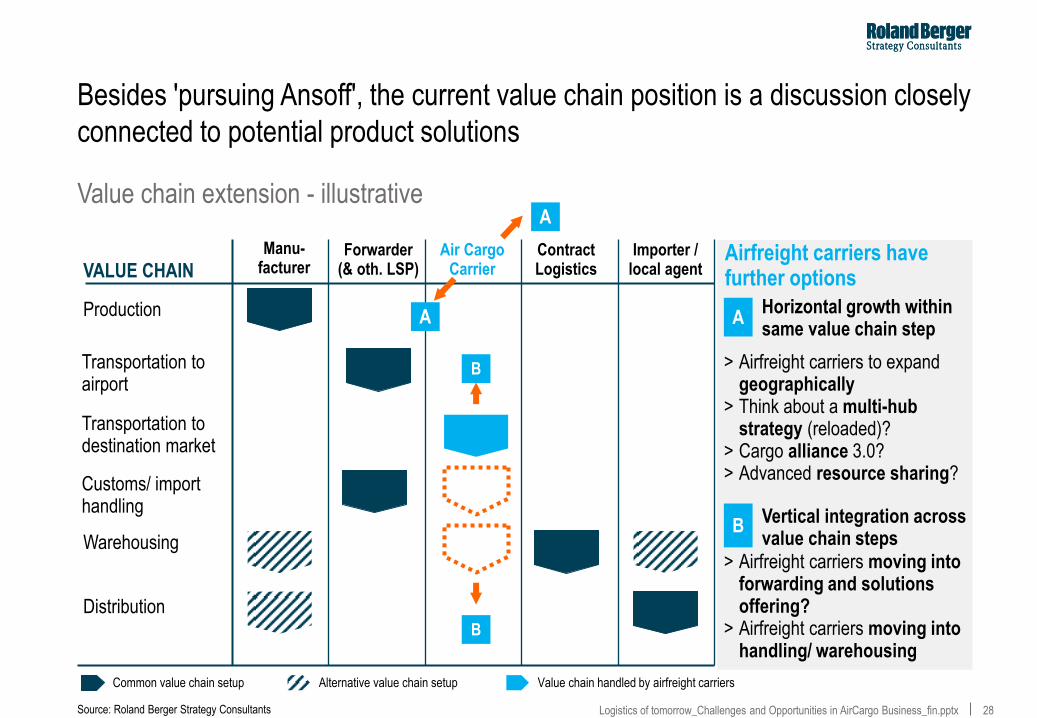

Besides 'pursuing Ansoff', the current value chain position is a discussion closely

connected to potential product solutions

Value chain extension - illustrative

Source: Roland Berger Strategy Consultants

Airfreight carriers have further options

Manu- facturer

Forwarder (& oth. LSP)

Importer / local agent

Contract Logistics VALUE CHAIN

Production

Common value chain setup Alternative value chain setup Value chain handled by airfreight carriers

Distribution B

A

B

> Airfreight carriers to expand geographically

> Think about a multi-hub strategy (reloaded)?

> Cargo alliance 3.0? > Advanced resource sharing?

Horizontal growth within same value chain step

> Airfreight carriers moving into forwarding and solutions offering?

> Airfreight carriers moving into handling/ warehousing

Vertical integration across value chain steps

Transportation to airport

Customs/ import handling

Warehousing

Transportation to destination market

Air Cargo Carrier

B

A

A

29 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

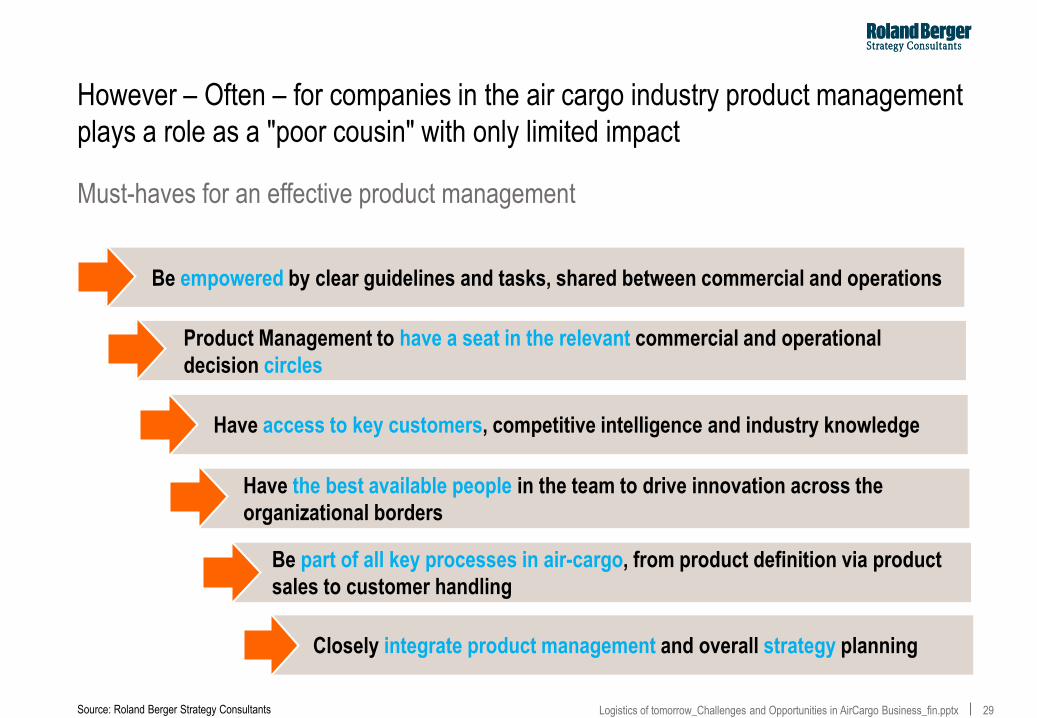

However – Often – for companies in the air cargo industry product management

plays a role as a "poor cousin" with only limited impact

Must-haves for an effective product management

Source: Roland Berger Strategy Consultants

Be empowered by clear guidelines and tasks, shared between commercial and operations

Product Management to have a seat in the relevant commercial and operational

decision circles

Have access to key customers, competitive intelligence and industry knowledge

Have the best available people in the team to drive innovation across the

organizational borders

Be part of all key processes in air-cargo, from product definition via product

sales to customer handling

Closely integrate product management and overall strategy planning

30 Logistics of tomorrow_Challenges and Opportunities in AirCargo Business_fin.pptx

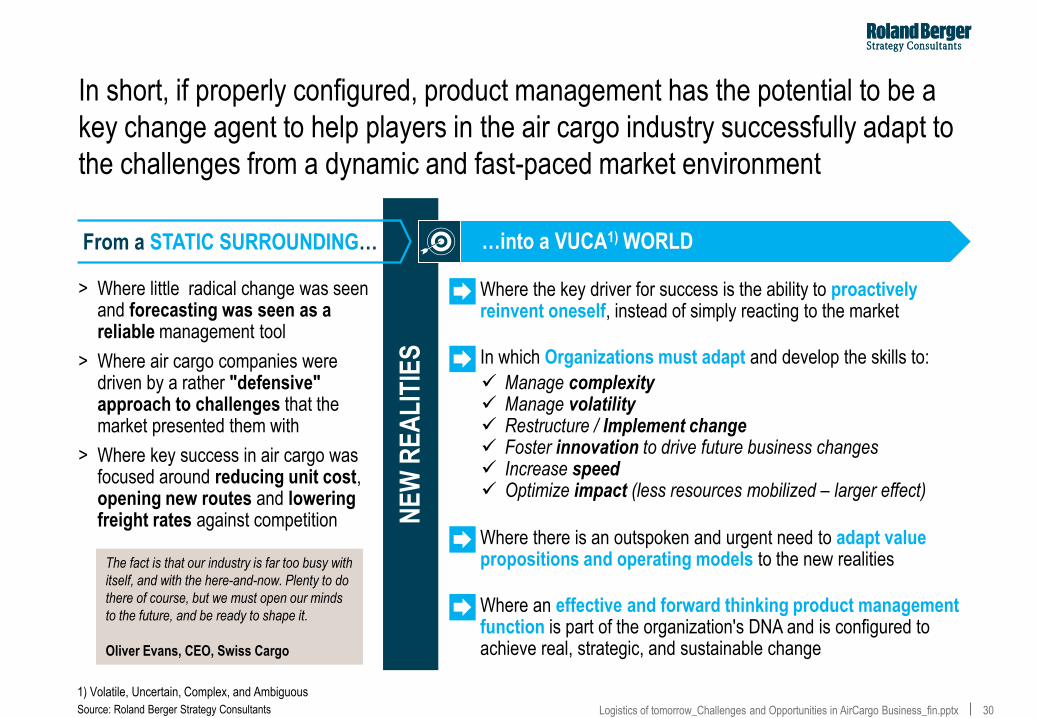

In short, if properly configured, product management has the potential to be a

key change agent to help players in the air cargo industry successfully adapt to

the challenges from a dynamic and fast-paced market environment

From a STATIC SURROUNDING…

The fact is that our industry is far too busy with

itself, and with the here-and-now. Plenty to do

there of course, but we must open our minds

to the future, and be ready to shape it.

Oliver Evans, CEO, Swiss Cargo

1) Volatile, Uncertain, Complex, and Ambiguous

NE

W R

EA

LIT

IES

…into a VUCA1) WORLD

> Where little radical change was seen and forecasting was seen as a reliable management tool

> Where air cargo companies were driven by a rather "defensive" approach to challenges that the market presented them with

> Where key success in air cargo was focused around reducing unit cost, opening new routes and lowering freight rates against competition

– Where the key driver for success is the ability to proactively reinvent oneself, instead of simply reacting to the market

Source: Roland Berger Strategy Consultants

– In which Organizations must adapt and develop the skills to:

Manage complexity Manage volatility Restructure / Implement change Foster innovation to drive future business changes Increase speed Optimize impact (less resources mobilized – larger effect)

– Where there is an outspoken and urgent need to adapt value propositions and operating models to the new realities

– Where an effective and forward thinking product management function is part of the organization's DNA and is configured to achieve real, strategic, and sustainable change

THANK YOU FOR YOUR

ATTENTION

![› fileadmin › produkte › prozesssicherheit › IG-KUB-PTU › Product... PRE-TORQUE MULTIFLANGE RUPTURE DISC HOLDER IG-KUB …Technical data NPS [in] DN [mm] Pressure class ANSI](https://img.pdfslide.us/doc/110x75/5e5c81b2e284b369207b1909/a-fileadmin-a-produkte-a-prozesssicherheit-a-ig-kub-ptu-a-product-pre-torque.jpg)