Embed Size (px)

Citation preview

1

LocalGovernment

BudgetManagementPerformance:A Survey of 41 Local Governments in

Indones ia

2

Acknowledgements This Report on Local Government Budget Management Performance in 2008 is theresultofcooperationbetweenSeknasFITRAandTheAsiaFoundation.TheSeknasFITRAteamwas coordinatedby Yuna Farhan,with Yenni Sucipto,MuhammadMaulana andHadi Prayitno as themembers; TheAsia Foundation’s teamwas coordinated by JohnBrownlee andhad as itsmembersR.AlamSuryaPutra,Hana Satriyo, ErmanRahmanandHariKusdaryanto.This report was written based on the results of field research performed by localresearchers from around 30 civil society organizations: Afrizal, Baihaqi and Nasrudin(Gerak Aceh), Diba Suraya (FITRA Sumut), Aryadie Adnan and Wibawadi Murdwiono(PKSBE West Sumatra), Fahriza (FITRA Riau), Novi Ramadhona and Rozidateno PutriHanida (Maarif Institute), Agus Sugandhi (PINUS Garut), Yenti Nurhidayat (SanggarBandung),Hirzuddin,MuhammadEfril,MuhitEffendi,SyaifulMustai’n (PPLakpesdamNU), Alif Basuki, Andwi JokoMulyanto, Aminuddin Aziz, Arifin, Dini Inayati, Ermy SriArdhiyanti,NurHidayat, ZazadDjuaini (Pattiro),Dahkelan (FITRATuban),Heri FerdianandJimmyWilopo(Inisiatif),DwiEndah(PWAisyiyahEast Java),Akhdiansyah(Lensa),Dwi Arisanto (Legitimed), Jumarim (YPKM), Suhaimi (LSBH), Andi Nilawati Ridha,Sudirman,Wildayanti(YLP2EM),St.Hasmah(LPPBone),Rosniaty(Yasmib),NhasirDjalil(KPPA),ArtenH.Mobonggi,M.GandhiTapu(LP2G),Ngusmanto(Fakta)andMuttaqien(LabdaJogjakarta).FielddatawereverifiedbyateamofverifierscomprisingHendriadi(Somasi), Rosniaty (Yasmib), Ermy Sri Ardhiyanti (Pattiro), Devi (Maarif Institute) andDahkelan (FITRA Tuban). The process of analysis and writing of the report wasperformed jointlybyMuhammadMulana (SeknasFITRA)andR.AlamSuryaPutraandHanaSatriyo(TheAsiaFoundation).AssistanceindataprocessingwasprovidedbythelateDr.RizalHikmat(UniversityofIndonesia).ThisactivitywascarriedoutwithfundingsupportfromtheDepartmentforInternationalDevelopment(DfID)oftheUnitedKingdomgovernment.However,allopinions,findings,interpretationsandconclusions in this reportare theviewsof the civil societygroupsandnotthoseofTheAsiaFoundationandDfID.

3

List of Terms and Abbreviations

APBD : AnggaranPendapatandanBelanjaDaerah,LocalGovernmentRevenueandExpenditureBudget

APBDP : AnggaranPendapatandanBelanjaDaerahPerubahan,RevisedLocalGovernmentRevenueandExpenditureBudget

APBN : AnggaranPendapatandanBelanjaNegara,StateRevenueandExpenditureBudget

Bappeda : BadanPerencanaanPembangunanDaerah,LocalDevelopmentPlanningAgency

Bappenas : BadanPerencanaanPembangunanNasional,NationalDevelopmentPlanningAgency

BPK : BadanPemeriksaKeuangan,StateAuditAgency

DAK : DanaAlokasiKhusus,SpecialAllocationFund

DAU : DanaAlokasiUmum,GeneralAllocationFund

DPA : DokumenPelaksanaanAnggaran,BudgetImplementationDocument

DPRD : DewanPerwakilanRakyatDaerah,RegionalPeople’sRepresentativeAssembly

ILPPD : InformasiLaporanPertanggungjawabanPemerintahanDaerah,LocalGovernmentAccountabilityReportInformation

KUA‐PPAS : KebijakanUmumAnggaran–PrioritasdanPlatfomAnggaranSementara,GeneralBudgetPolicy–ProvisionalBudgetPrioritiesandCeiling

LKPD : LaporanKeuanganPemerintahDaerah,LocalGovernmentFinancialStatements

Musrenbang : MusyawarahPerencanaanPembangunan,DevelopmentPlanningConference

MusrenbangCam : MusyawarahPerencanaanPembangunanKecamatan,DistrictDevelopmentPlanningConference

MusrenbangKab/Kot : MusyawarahPerencanaanPembangunanKabupaten/Kota,District/MunicipalityDevelopmentPlanningConference

Perkada : PeraturanKepalaDaerah,RegulationoftheHeadoftheRegion

4

Permendagri : PeraturanMenteriDalamNegeri,MinisteroftheInteriorRegulation

Perda : PeraturanDaerah,LocalRegulation

Pokja : KelompokKerja,WorkGroup

PP : PeraturanPemerintah,GovernmentRegulation

PUG : PengarusUtamaanGender,GenderMainstreaming

RAPBD : RancanganAnggaranPendapatandanBelanjaDaerah,DraftLocalGovernmentRevenueandExpenditureBudget

Renja : RencanaKerja,WorkPlan

Renstra : RencanaStrategis,StrategicPlan

RKA : RencanaKerjadanAnggaran,WorkPlanandBudget

RKPD : RencanaKerjaPemerintahDaerah,LocalGovernmentWorkPlan

RPJMD : RencanaPembangunanJangkaMenengahDaerah,LocalMedium‐TermDevelopmentPlan

SKPD : SatuanKerjaPemerintahDaerah,LocalGovernmentWorkUnit

5

Executive Summary

Budgets(boththeStateBudget(APBN)andlocalgovernmentbudgets(APBD))areanimportantinstrumentforgovernmentstocarryouttheirprograms,whicharetosomeextent influenced by how the budget is managed. The government budget is areflectionofpoliticaldecisionsbetweentheexecutiveandthelegislature,whichreflectwhatthegovernmentdoeseachyear.Thesepoliticaldecisionshaveabroadimpactonthepublic’sstandardofliving,particularlyintheefforttoprovidebetterbasicservicesto residents, especially women and the poor. It is assumed that how the budget ismanaged – from planning through accountability – will influence how effectively thebudgetcanstimulateeconomicgrowthandprovidebetterbasicservices.

This report presents the results of research performed to assess Local GovernmentBudget Management Performance (Kinerja Pengelolaan Anggaran Daerah, KiPAD)basedonfouraspectsofgoodgovernance.Thebudgetmanagementprocessassessedby KiPAD covers the stages of planning, budget deliberation, implementation, andaccountability.Budgetmanagementperformanceinthesefourstagesisassessedbasedon four aspects of good governance: transparency, participation, accountability, andgender equality. The scores for each local government in these four aspects of goodgovernanceareaggregated intheformofaKiPADIndextoeasecomparisonbetweendistricts/municipalities.

Researchwasconductedin41districts/municipalitiesin16provinces,anditishopedthat the results can be used as a reference to improve KiPAD in the respectivedistricts/municipalities. Researchwasdoneonlocalgovernmentdataanddocumentsfortheyears2007(fortheaccountabilitystage)and2008(fortheplanning,discussion,andbudgetimplementationstages),andontheapplicabledocumentsforyear2008(forthemedium‐termplanningdocuments).Itishopedthatthisassessmentwillspurlocalgovernments to continuously improve their performance in applying the principles ofgoodgovernance. It isalsohopedthattheassessmentwillenhancerelationsbetweengovernmentsandtheircommunities.Forthecentralandprovincialgovernments,whichplayaroleinsupervisingdistrict/municipalitygovernments,thisassessmentcanhelpinprioritizingtheattentionandsupportthatcanbegiven.

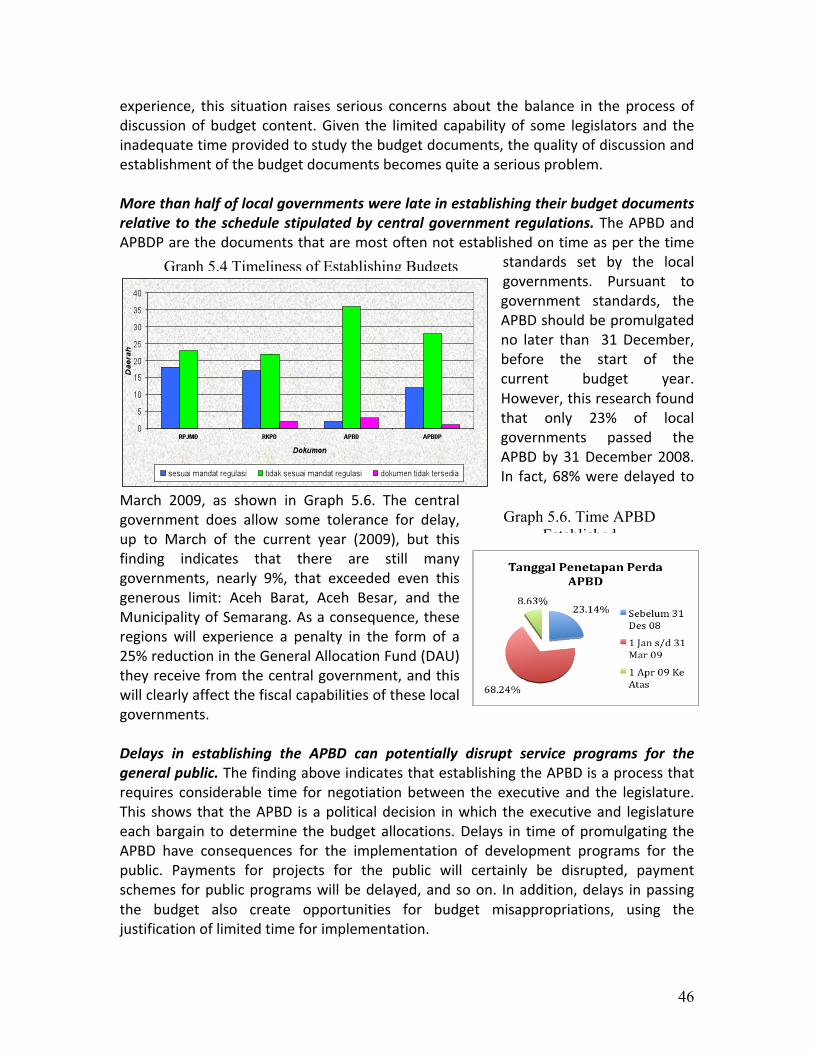

The level of transparency is relatively high in the first three stages of budgetmanagement,butrelativelylowintheaccountabilitystage.TheexistenceofLawNo.14of2008onOpennessofPublicInformationseemstohavehadareasonablypositiveimpact in the relatively high public access to budget‐related documents. However,aroundathirdofthelocalgovernmentsstudiedhavenotproducedLocalGovernmentAccountabilityReportInformation(InformasiLaporanPertanggungjawabanPemerintahDaerah,ILPPD),andaroundathirdofthosethathavepreparedILPPDdonotgrantthegeneral public access to it. One major challenge for local governments is managingpublicdocumentsthroughanadequatearchivingsystem.Notonelocalgovernmenthas

6

suchasystem,soevenwhen inprinciple the informationcanbeaccessed,most localgovernmentsstillrequirebureaucraticproceduresandinformalrelationshipswithlocalgovernmentofficialstoobtainit.

The participation performance of the local governments studied is relatively low,particularlyinthebudgetdiscussionandaccountabilitystages.Inthebudgetplanningstage, most local governments provide vehicles for participation, although these arerelatively low for sectoral planning, such as in the formulation of the Strategic Plans(Rencana Strategis, Renstra) and Work Plans (Rencana Kerja, Renja) of LocalGovernment Work Units (Satuan Kerja Pemerintah Daerah, SKPD). In the budgetdiscussionstage–draftingof theGeneralBudgetPolicy/ProvisionalBudgetPrioritiesand Ceiling (Kebijakan Umum Anggaran ‐ Prioritas dan Plafon Anggaran Sementara,KUA‐PPAS)andtheDraftLocalGovernmentBudget (RancanganAnggaranPemerintahDaerah, RAPBD), in the executive and the legislature – around 60% of the localgovernmentsstudieddonotconductanypublicconsultationinthedraftingprocess.Intheimplementationstage,fewerthan50%ofthelocalgovernmentsstudiedprovideameans to accommodate citizen complaints. The situation is even worse in theaccountability stage; only one region provides a vehicle for participation beforepromulgating the Local Government Financial Statements (Laporan KeuanganPemerintahDaerah,LKPD).

Intheaspectofaccountability,theperformanceofthe41localgovernmentsstudiedisrelatively high, though there is still room for improvement. Amajority of the localgovernments already have price standards, which are updated each year, forprocurementofgoodsandservicesintheirregions,thoughveryfewlocalgovernmentsare undertaking reform in this sector. With regard to time for discussion andestablishment of the budget, most of the local governments studied do not provideenoughtimeforthelegislaturetodeliberatetheKUA‐PPAS,RAPBDandRevisedRAPBD,which leads todelays inpassing theAPBDandRevisedAPBD.Thisclearly reduces theopportunity for local governments to make investments and provide public services.Meanwhile,basedontheresultsofauditsbyBPK(BadanKeuanganNegara,theStateAudit Agency), most of the local governments studied received Qualified Opinions,sevenreceivedAdverseOpinions,andfourreceivedDisclaimersofOpinion.

Effortstoimproveequalityforwomeninbudgetmanagementgenerallyremainlow,especially in the implementation and accountability stages. Very few localgovernments provide vehicles for participation bywomen, such as special discussionsfor women at the community level or representation for women in the planningprocess.Furthermore,onlyaroundhalfofthelocalgovernmentsstudiedhaveformedgendermainstreamingworkgroups(PokjaPUG),andmorethanhalfofthesehavenotbeen officially established. Only five districts/municipalities have established gendermainstreamingfocalpoints ineachSKPD.WithregardtouseofdisaggregateddataaspartoftheWorkPlanandBudget(RencanaKerjadanAnggaran,RKA)planningprocess,again only five regions use disaggregated data, and even then it is not yet used indraftingtheRKA.Specialvehiclestomonitorbudgetimplementationandaccountabilityarealsoveryseldomprovidedbylocalgovernments.

7

Overall,SumedangDistrict,PadangPanjangMunicipalityandSlemanDistricthavethehighestKiPAD index ratings. Regionswith relatively limited fiscal capability hold thetopKiPADratings,whileregionswithsubstantialfiscalcapabilityareinthelowerranks.Meanwhile, no significant difference was found between municipality and districtgovernments in the KiPAD rankings, or between local governments in Java and thoseoutsideJava.However,secondarymunicipalitiesseemtohavebetterKiPADratingsthanlarge(metropolitan)municipalities.

8

Chapter I

Introduction: Assessing the Local Government Budget Management Process

A. Background

This report present the results of researchperformed to assess the execution of thebudgetmanagement process in certain regions. The budgetmanagement process isdefinedastheactivitiesperformedbyalocalgovernmentinplanningactivityprogramsand drafting the budget (the planning stage), deliberating and deciding on activityprograms and budgets (the discussion stage), implementing the budgeted activityprograms (the implementation stage) and providing accountability for theimplementationoftheactivityprogramsandbudgets(theaccountabilitystage).

Budgetmanagement should ideally be done by internalizing the principles of goodgovernancesothatthebudgetpolicyandimplementationproducedaccommodatetheinterestsofthestakeholders.Thepowersheldbythegovernmentconstituteamandatethatderives fromthevoiceof thepeople.Thegovernment isentrusted to implementtheoperationsofthepoliticalorganizationofthestateinordertobringprosperitytoallthepeople–thosewhograntedthemandate.Thus,thecitizensarethetrueholdersofpowerandauthority.Thegovernmentcannotactarbitrarilyinmakingpublicpolicies.Itis important to apply the principles of good governancebecause the citizens and thegovernmentoften have different perceptions and interests as stakeholders in budgetplanning,whichmaybedetrimentaltoonesideortheother.

Government budgets (both APBN and APBD) are an important instrument for thegovernment to set development program priorities at both the national and locallevels. We could even say that the government budget is a reflection of politicaldecisionsbetweentheexecutiveandthelegislature.Thesepoliticaldecisionsobviouslyhaveatremendousimpactonthelivingstandardsofthepublic,dependingonhowwellthedevelopmentbudgetallocationspromoteeffortstoprovidebetterbasicservicestoresidents,especiallywomenandthepoor.Therefore,thebudgetisalsoameasurementtooltoevaluatethegovernment’ssupportforitscitizens.

FindingsbySeknasFITRAin2007and2008indicatethatlocalgovernmentbudgetsstilldonotreflectpoliciesthatcreatepublicprosperity.Theresultsofanalysisin2007in30localitiesshowedthatthedirectexpendituresforeducationandhealth,afterdeductingDAK(SpecialAllocationFunds),wereonaveragestillverylow.Intheeducationsector,the local governments’ direct expenditure allocations were only around 8.3% of the

9

total APBD expenditure. And on average, only 4.6% of total APBD expenditure wasallocated for thehealthcaresector. In2008, theaveragedirectexpenditureallocatedforeducation in29localitieswasonly15.3%ofthetotaleducationexpenditure,whiletheindirectexpenditureallocatedforeducationwasmuchhigher,at76%.Inthehealthsector,theaveragedirectexpenditureallocatedwas39.5%,whileindirectexpenditurewas44.9%oftotalhealthexpenditure1.

Several studies2 have also described the serious problems faced by the public inbecominginvolvedinlocalgovernmentbudgetplanning.First,limitedpublicspaceforinvolvement in determining budget allocations. The existing development planning isnot significantly correlated with the budgeting process. As a consequence, often theresults of community planning are not used as a reference or basis in drafting thebudget. Second, although some localities have developed policies that ensuretransparencyofpublicdocuments,thepublicstillhasdifficultygainingaccesstobudgetdocuments. Thismeans that budget documents such as theWork Plans and Budgets(Rencana Kerja Anggaran, RKA) and Budget Implementation Documents (DokumenPelaksanaanAnggaran, DPA) of local government agencies and offices, and the LocalGovernment Revenue and Expenditure Budget (Anggaran Pendapatan dan BelanjaDaerah, APBD) documents, are still hard for the public to access. Third, some localgovernmentsstilldonotcomplywiththeadministrationoftheplanningandbudgetingprocessesasstipulatedinlawsandregulations;forexample,budgetsarenotpassedontime, and the content of thebudget documents is inadequate. This situationdisruptstheimplementationofdevelopmentprograms,whichmeansthatservicestothepublicaredisruptedaswell.

This research is one way for civil society groups to be involved in monitoring andevaluation of the conduct of local government, specifically in the planning andbudgetingprocesses.Thecentralandprovincialgovernmentshaveanimportantroleinmonitoringandevaluatingthelocalgovernmentsbelowthem,asmandatedinLawNo.32 of 2004. However, the involvement of civil society groups needs to be developedthroughvariousactivities,suchasthisresearch.

1 Refleksi Penganggaran 2008: Selusin Dosa Besar Pengelolaan Anggaran 2008 (Reflections on Budgeting 2008: A Dozen Major Sins in Budget Management in 2008), Seknas FITRA, 2009. 2 Inovasi Demokratisasi Penganggaran Daerah: Refleksi Gerakan Advokasi Anggaran Mewujudkan Kedaulatan Rakyat atas Anggaran (Innovations in Democratization of Local Budgeting: Reflections of the Budget Advocacy Movement Realizing People’s Sovereignty over the Budget), Seknas FITRA, The Asia Foundation and Yayasan TIFA, 2007, containing a collection of research results by budget advocacy activists.

10

B. Research Aims

Thisresearchisaimedatseeingtowhatextentthepracticesofbudgetmanagementin the regions are conducted applying the principles of good governance:transparency, participation, accountability and gender equality. Specifically, thisresearch is intended to provide input to local governments to improve theirperformanceinplanningandbudgetingprocessesthatbetteremphasizetheprinciplesofparticipation,transparency,accountability,andgenderequality.

Inaddition,itisalsohopedthatthisresearchcanbeusedbythecentralgovernmentasareferenceforevaluatingandimprovingpoliciesonthelocalbudgetmanagementprocess.Thisresearchwillalsobeusefultoaddtothefindingsofpreviousresearchandto serve as basic data for improving the performance of local governments inconducting planning and budgeting processes that pay more attention to the publicinterest.

C. Methodology

Thisresearchwasperformedbytracingdocumentsonthelocalbudgetmanagementcycle in four stages: documents on the planning, discussion, implementation, andaccountability stages. These documents were then assessed by observing to whatextentthebudgetmanagementprocessappliedtheprinciplesofgoodgovernance.

Four principles of good governance are used as the bases for the analysis in thisresearch: transparency, participation, accountability, and gender equality3. Each oftheseprinciplesisusedasatooltoanalyzetheentirebudgetmanagementcycle,fromplanning,throughdiscussionandimplementation,toaccountability.Eachindicatorhasalimiteddefinition,basedonthefollowingconditions:

- Transparency is formulatedasasystematiceffortbygovernmentforopennessinproviding,andgrantingaccessto,informationinallstagesofbudgetplanning.Theindicatorsusedforpresenceorabsenceoftransparencyareavailabilityandpublic accessibility of budget documents, and completeness of the content ofbudgetdocuments.

- Participationisformulatedasthelevelofcitizeninvolvementindecisionmakingateachstageofbudgetplanning.Themattersnotedinthisindicatoraremeansforparticipationprovidedbythegovernment,theparticipantswhoareinvolved,regulatoryguarantees,anddecisionmakingauthorityinparticipatoryprocesses.

3 These indicators are adapted from the principles of good governance.

11

- Accountabilityisformulatedasaneffortbythelocalgovernmentadministrationtoopenlyaccounttothelegislatureandthepublicforthebudgetthathasbeenmanaged. The indicators include themeans used for conveying accountability,timelinessincompletingbudgetdocuments,andtheBPK’sopinionontheresultsofitsauditoflocalfinances.

- Genderequality isformulatedasaneffortbythegovernmenttoprovidespacefor participation by the poor and women in the budget planning cycle. Themattersseenfromthisindicatorarevehiclesprovidedbythegovernmentforthepoorandwomen,consideringtheirconditionsandpositioninsociety,toenablethem to takepart andbe considered inplanningandbudgeting; availabilityofmanagementinstitutions;andregulatoryguarantees.

Forthesereasons,thisresearchobtainsacross‐cuttingviewofthebudgetmanagementcycleandtheprinciplesofgoodgovernance.Seventy‐fivequestionswereasked,whichweredistributedasshowninthefollowingtable.

Table1.1.DistributionofResearchQuestionsbyCycleand

PrinciplesofGoodGovernance

Cycle

Principle

Planning Discussion Implementation AccountabilityNumberofquestions

Transparency 10 9 12 5 36Participation 10 4 1 3 18Accountability 2 3 4 4 13Equality 3 3 1 1 8

Totalquestions 25 19 18 13 75

Belowistheprocessflowofputtingintooperationtheconceptoftheprinciplesofgoodgovernanceinthebudgetmanagementcycle:

12

Chart1.FlowChartofOperationalizationofResearchConcepts

Nevertheless,furtherconfirmationwassoughtfromlocalgovernmentadministrations,thepublic,andlocallegislatures(DPRD)regardingtheresearchers’preliminaryfindingsinordertoobtainthebestpossibleanswers.Twotypesofdocumentswereexamined:planning documents and budgeting documents. In all, a total of 20 documents weretraced.Belowisachartofthedocumentsthatweretracedinthisresearch.

The standards used to measure the above four dimensions refer to internationalstandardsforbudgetmanagementandthenationallegalframeworkonplanningandbudgetingintheregions.AmongtheinternationalstandardsusedasreferencesaretheCodeofGoodPracticesonFiscalTransparencyreleasedbytheInternationalMonetaryFund (IMF) and the Open Budget Index (OBI) published by the International BudgetPartnership (IBP). Meanwhile, the national legal framework refers to the statutoryregulations relating to planning and budgeting processes in the regions, which arediscussedfurtherinChapter2.

Twenty budget management cycle documents were examined. Each stage in thebudgetmanagementcycleproducesquiteafewdocuments.Itisestimatedthatover30documentsneedtobeproducedduringtheentirebudgetmanagementcycle.However,

To know levels of transparency, participation, accountability, and gender equality in local government planning and budgeting processes

TRANSPARENCY PARTICIPATION ACCOUNTABILITY EQUALITY

• Availability of budget documents

• Accessibility of budget documents

• Adequacy of information

Vehicles and participants

Decision making authority

Regulatory guarantees

• Timeliness • Level of budget

misallocation • Audit results

• Vehicles and participants

• Institutions • Regulatory guarantees

Government openness in systematically providing and

opening access to information in all stages of planning and

budgeting

Level of citizen involvement in decision making at each stage

of budget planning

Emphasis on extent to which budget managed by Local

government can be accounted for

Examines extent to which local government provides vehicles for participation and involves the poor and women in the budget planning process

Research Objective Penalties

GG Principle Selected

Operational Definition

Operationalization of concept

Budget Management Cycle

Planning

Discussion

Implementation

Accountability

13

this research traced only 20 documents out of the entire budgetmanagement cycle,distributedasillustratedinthefollowingchart.

Chart2:Documentstracedintheresearch

Nearly all documents examined used data for year 2008. In the planning stage, alldocumentsexamineduseddatafor2008,excepttheLocalMedium‐TermDevelopmentPlan(RPJMD),whichwasbasedontheyearinwhichthemostrecentlyelectedheadofthe region was sworn in by the central government. All the documents for thediscussion and implementation stages used data for 2008. However, in theaccountabilitystage,thereweresomedocumentsthatdidnotusedatafor2008:LocalGovernment Financial Statements (LKPD) and Local Regulations on Accountability forLocalGovernmentFinances,whichstillused2007data.Thisisbecausethesetwotypesofdocumentsarepromulgatedafterthebudgetyearends,asstipulatedinGovernmentRegulation No. 8 of 2008 on Procedures for Planning and Evaluation of LocalDevelopment.

This research employs the expert judgment method4 in which the researchers, asexperts, have the authority to give scores for the key questions based on specifiedverificationtools.Thescoresgivenbytheresearchersserveasthebasisfortheprocessof ranking the performance of local governments in their budget managementprocesses. Generally, the researchers, who come from civil society organizations, are

4 This method is adopted from research performed by the International Budget Partnership (IBP) when it determines the budgeting indices of countries, Open Budget Index (OBI), years 2006 – 2008, adapted to the local context.

14

experts in the research topicandactively involved in similaractivities.Around30civilsocietyorganizationswereinvolvedinthisresearch.ThelistofcivilsocietyorganizationsinvolvedcanbeseeninAppendix1.

The ranking scores for localgovernmentperformanceareobtainedbyaddingupallthe scores obtained for the four indicators selected, i.e. the four principles of goodgovernance.Allresearchindicatorshavethesamescoreorweight.Thisapproachwasusedbasedon theconsideration thateach indicatorhas thesame levelofurgencyasthe others, and they all complement one another. For local governments, publicparticipationisjustasurgentastheaspectsoftransparency,accountabilityandequalityofwomen.Thesameappliesfortheotherindicators,whichhaveimportanceforotherindicatorsforthelocalgovernment.Theregionswiththehighesttotalscoresarejudgedto be the best local governments in terms of their performance in management ofregionalfinances.

D. Limitations of the Research Thisresearchisthefirstisaseriesofannualresearchstudiesthataretobeconducted.As the first in the series, this researchobviously has several limitations, including thefollowing:

TimeoftheresearchwaslimitedtotheperiodMarch–August2009.Therefore,matters relating to events occurring after that period are not portrayed, forexampleifalocalgovernmentissuedapolicyaftertheperiodoftheresearch.

The sampleof localities in this research representsonlya fewof theexistinglocal governments. This research takes as its sample only 41districts/municipalitiesin16provinces.

This research does not portray in detail the entire budget planning process,such as village and district level Musrenbang (Development PlanningConferences)asstipulatedintheregulationsonregionalfinances.

E. Research Locations

This researchwas conducted in 41districts/municipalities located in 16provinces ofIndonesia. Fifteenmunicipalities were studied; the other 26 local governments weredistricts.Thetablebelowshowsthedistributionoftheresearchlocalities,byprovince.

15

Table1.1.DistributionofResearchLocalities

No Province Districtsstudied Municipalitiesstudied

1 NangroeAcehDarussalam

AcehBarat,AcehUtara,AcehBesar

‐

2 NorthSumatra SerdangBedagai

3 WestSumatra ‐ Padang,PadangPanjang

4 Riau Dumai

5 Lampung BandarLampung

6 WestJava Garut,Sumedang Banjar

7 CentralJava Pekalongan,Kendal,Boyolali,Cilacap,Semarang

Pekalongan,Semarang,Surakarta

8 YogyakartaSpecialRegion(DIY)

Sleman

9 EastJava Situbondo,Bondowoso,Pasuruan,Malang,Bojonegoro

Blitar,Surabaya

10 WestNusaTenggara LombokBarat,LombokTimur,SumbawaBarat,Dompu

11 SouthSulawesi Wajo,Sidrap,Bone Parepare

12 WestSulawesi Polman

13 CentralSulawesi Palu

14 Gorontalo GorontaloUtara Gorontalo

15 CentralKalimantan Palangkaraya

16 WestKalimantan Pontianak

Thegeographicdistributionoftheresearchlocationscanalsobeseeninthefollowingmap:

16

The selection of the research locationswas based on the distribution of the humandevelopmentindex(HDI)andgenderdevelopmentindex(GDI)oftheregions.Inotherwords,thisresearchtriestoexaminebudgetmanagementperformanceinregionswithhigh,medium,and lowHDIandGDIscores.Ontheotherhand,because this researchuses localexperts, theavailabilityof institutionswithanactivity focuson localbudgetadvocacywasalsoaneedthathadtobeconsidered.Thus,thisresearchalsoconsideredtheavailabilityoflocalresources.

17

Chapter II

The Regulatory Framework for Local Government Budget Management

A. Policy Framework for Local Government Planning and Budgeting

The policy framework for local government planning and budgeting in Indonesia isregulatedintwodifferentspheres.PlanningpolicyisregulatedinaseparateLaw,whichplaces the National Development Planning Agency (Bappenas) as the authorizedinstitution. Meanwhile, financial management policy is regulated through a differentLaw,withtheauthorityheldbytheMinistryofFinance.LocalgovernmentdevelopmentplanningisregulatedbytheLawonLocalGovernance,whichsignaledthestartoftheeraofdecentralizationinIndonesia:LawNo.22of1999,amended by Law No. 32 of 2004. However, before amending the Law on LocalGovernance, the Indonesian Government also issued Law No. 25 of 2004 on theNational Development Planning System. As implementation of that Law, thegovernment issued Government Regulation (PP) No. 8 of 2008 on Procedures forRegional Development, which serves as the basic reference for the Minister of theInteriorandtheNationalDevelopmentPlanningAgency(Bappenas) in formulatingtheJointCircular (SEB) that regulates themechanism for implementationofDevelopmentPlanningConferences(Musrenbang)fromthevillagelevel,throughdistrict,district,andprovincial levels,uptothenational level.ThisCircular is issuedbythesetwoagencieseachyear.Meanwhile, local financialmanagementpolicy is regulatedby LawNo. 17of 2003onStateFinances.ThisLawwasthenreinforcedthroughLawNo.33of2004onFinancialBalancebetweentheCentralandLocalGovernments.Further,thetechnicalapplicationofthesetwoLawsisstipulatedthroughGovernmentRegulation(PP)No.58of2005onManagement of Local Government Finances and Minister of the Interior Regulation(Permendagri) No. 13 of 2006 on Management of Local Government Finances, asrevisedthroughPermendagriNo.59of2007.Alloftheseregulationsstipulateindetailtheproceduresforconductoflocalgovernmentbudgeting,fromtheformulationoftheGeneral Budget Policy (Kebijakan Umum Anggaran, KUA) to the placement of eachaccountcodeintheAPBD.

18

Table2.1.RegulatoryFrameworkBasedonStagesofLocalGovernmentBudgetManagement

No Stage RegulatoryFramework1 Planning ‐ LawNo.25/2004onNationalDevelopmentPlanning

System(SPPN)‐ LawNo.32/2004onLocalGovernment‐ PPNo.8/2008onProceduresforPlanningandEvaluation

ofRegionalDevelopment‐ JointCircularonMusrenbang

2 Drafting/Discussion ‐ Law17/2003onStateFinances‐ Law32/2004onLocalGovernment‐ Law33/2004onFinancialBalancebetweenCentraland

LocalGovernments‐ PP58/2005onGuidelinesforManagementofLocal

GovernmentFinances‐ Permendagri13/2006andPermendagri59/2007on

GuidelinesforManagementofLocalGovernmentFinances

‐ PermendagrionGeneralGuidelinesforDraftingAPBD(issuedeachyear)

3 BudgetImplementation(revisedbudget)

‐ Law17/2003onStateFinances‐ Law1/2004ontheStateTreasury‐ Law32/2004onLocalGovernment‐ Law33/2004onFinancialBalancebetweenCentraland

LocalGovernments‐ PP58/2005onGuidelinesforLocalGovernmentFinances‐ PP65of2005onMinimumServiceStandards‐ Permendagri13/2006andPermendagri59/2007on

GuidelinesforManagementofLocalGovernmentFinances

‐ Keppres80of2004anditsrevisionsonProcurementofPublicGoodsandServices

4 BudgetAccountability

‐ Law17/2003onStateFinances‐ Law15/2004onAccountabilityforStateFinances‐ Law32/2004onLocalGovernment‐ Law33/2004onFinancialBalancebetweenCentraland

LocalGovernments‐ PP58/2005onGuidelinesforLocalGovernmentFinances‐ Permendagri13/2006andPermendagri59/2007on

GuidelinesforManagementofLocalGovernmentFinances

‐ PP3of2007onReportsontheConductofLocalGovernment

19

TheemergenceofLawNo.14of2008onOpennessofPublic Information,whichwillcome into force in 2010, providesanew spirit for transparency in local governmentbudgetmanagement.Inthecontextofopennessofpublicinformationasabasicright,citizens’ access to public information, including budget planning information, ismandated in the Constitution and the various statutory regulations that specificallyregulatebudgetplanning.TheemergenceofLawNo.14of2008onOpennessofPublicInformation provides a foundation for the public to gain access to budget planninginformation.Inbudgettransparency,thepublichastherighttoobtaininformation,forexample in the form of documents on the process for implementation of budgetplanning activities, including the Provisional Budget Ceiling and Priorities (Plafon danPrioritas Anggaran Sementara, PPAS), General Budget Policy (Kebijakan UmumAnggaran,KUA),RKA‐SKPD,RAPBD,andsoon.Meanwhile,thegovernmentisobligedtodiscloseandpublishbudgetplanningdocumentsandactivitiestothepublic.

Diagram2.1.StagesofGovernmentBudgetManagement

B. Procedures for Local Government Budget Management NationalandLocalDevelopmentPlanningincludeslong‐term,20‐yearplanning,referredto as the (Local) Long Term Development Plan (Rencana Pembangunan JangkaPanjang/Daerah,RPJP/D);medium‐term,five‐yearplanning, referredtoasthe (Local)Medium TermDevelopment Plan (Rencana Pembangunan JangkaMenengah/Daerah,

20

RPJM/D); the Strategic Plans (Rencana Strategis, Renstra) of Ministries/ Institutions/Local Government Work Units; and annual plans, referred to as (Local) GovernmentWorkPlans (RencanaKerjaPemerintah/Daerah, RKP/D) and theWorkPlans (RencanaKerja,Renja)ofMinistries/Institutions/LocalGovernmentWorkUnits.TheLocalMedium‐TermDevelopmentPlan(RPJMD)isformulatedbasedonthevisionandmissionoftheelectedHeadoftheRegionthroughtheMusrenbangmechanismandpromulgatedno later than sixmonthsafter theHeadof theRegion is inaugurated. Intermsoftheregulatoryarrangements,therearesomeissuesthatcreateconfusionforlocalgovernments.InLawNo.25/2004,theRPJMDisstipulatedthroughaRegulationoftheHeadoftheRegion,whileLawNo.32/2004mandatesthattheRPJMDisestablishedthrough a Local Regulation. Apart from the RPJMD, Law No. 25/2004 and PP No.08/2008 also mandate sectoral medium‐term documents or Strategic Plans of LocalGovernmentWorkUnits(RenstraSKPD).TheseRenstraSKPDaretheelaborationoftheRPJMD,whichservesas thereference in theirdrafting.TheRPJMDandRenstraSKPD,accordingtoPPNo.8/2008,providemeansforcommunityparticipationinthedraftingprocessthroughtheMusrenbangmechanismorpublicconsultations.Withregardtoannualplanning,therearetwodocumentsthatserveasthereferenceindrafting the budget: the RKPD (Local Government/Development Work Plan) and theRenjaSKPD(WorkPlansofLocalGovernmentWorkUnits)5.TheRKPDandRenjaSKPDconstitute the output of the planning process in the Local Development PlanningConferences(Musrenbang).The policy framework already accommodates representation and involvement ofwomen in the planning process. The annual planning, for which the Musrenbangmechanism is designed in the Joint Circular (SEB), is procedurally quite an openmechanism and provides the opportunity for participation by all elements of thecommunity. In fact, the Musrenbang mechanism provides special communicationchannels forwomenandother vulnerable groups to ensure that their participation isequal to that of other groups. Before conducting the Village Musrenbang, theMusrenbang organizing committee is asked to facilitate a special pre‐Musrenbangforum for women and other vulnerable groups. At each level of the Musrenbang, aMusrenbangdelegationischosen,whichisrequiredtoincludeacertainyangquotaofwomen’srepresentatives.Localgovernmentdevelopmentplanningconferencesrunfromthevillageleveltothedistrict/municipalitylevel.LocaldevelopmentplanningstartsatthevillagelevelwithaVillage Musrenbang involving elements of the village administration and the villagecommunity,andproducesproposalsforactivityprogramstobefinancedbytheVillageRevenue and Expenditure Budget (APBDes,Anggaran Pendapatan Belanja Desa), and

5 In Law No 25 2004, RKPD is the abbreviation for Rencana Kerja Pemerintah Daerah (Local Government Work Plan), while in Law 32 2004 and PP 8/2008, it stands for Rencana Kerja Pembangunan Daerah (Local Develpment Work Plan).

21

thefirstandsecondlevelAPBD.Atthedistrict‐levelMusrenbang,delegationsfromtheVillageMusrenbanganddistrictadministrationofficialsattend,aswellasmembersoftheDPRD(local legislature)fromtherelevantconstituenciesasresourcepersons. TheDistrict Musrenbang discusses village priorities to be designated as district priorities.Ideally, thedistrict‐levelMusrenbangshouldprovide informationon indicativeceilingsfor localities and sectors, to assist the forum in setting the priorities of planningproposals.Next,theresultsoftheDistrictMusrenbangaresynchronizedwiththeprioritiesoftheSKPD (LocalGovernmentWorkUnits) in the SKPDForums,whichproduceDraft SKPDWork Plans. The results of the District Musrenbang and SKPD Forums, which alsoinclude participation by the DistrictMusrenbang delegations, are synchronized in theDistrict/MunicipalityMusrenbang,andthenestablishedastheLocalGovernmentWorkPlan(RKPD)document.TheRKPDdocumentthenservesastheguidelinefordraftingtheAPBD. The RKPD document must be established no later than the May before thecomingbudgetyear.Belowistheflowoflocalgovernmentplanningandbudgeting.

Diagram2.2.FlowofLocalGovernmentPlanningandBudgeting

Source:ModuleonBudgetAdvocacyforIslamicMassOrganizations;SeknasFITRA‐TAF(2007)

LawNo.17of2003statesthatdeliberationofthebudgetbeginswiththesubmissionoftheGeneralPolicyontheAPBD,whichisinlinewiththeRKPD,totheDPRDinmidJune.After it isapproved, theAPBDGeneralPolicyservesas thereference forsettingthe provisional budget priorities and ceiling, to serve as the reference for the SKPD.

22

Then, theHeadsof theSKPDdraft theRKASKPDandsubmit themtotheDPRDtobedeliberatedintheinitialdiscussionontheDraftLocalGovernmentBudget(RAPBD).Theresults of the RKA discussions are forwarded to the Local Government FinancialManagementofficerasmaterialfordraftingtheDraftLocalRegulation(Raperda)ontheAPBD, together with supporting documents, no later than the first week of October.TheDPRDmustmakeitsdecisionnolaterthanonemonthbeforethenewbudgetyearbegins.Inaddition,pursuanttoLawNo.32of2004,oncetheRAPBDisapprovedbytheDPRD, District/Municipality RAPBD shall be submitted to the Provincial Government,andProvincialRAPBDshallbesubmittedtotheMinisteroftheInterior,tobeevaluatedontheparameterthattheydonotconflictwiththepublicinterestortheLaws.Theregulatory frameworkguarantees that thepublichas theright toprovide input,orally or inwriting, in the deliberation of laws and regulations, including the LocalRegulation on the APBD. Permendagri No. 13/2006 also signals the need fordisseminatinginformationontheRaperdaAPBDanditsattachments.Similarly,LawNo.32 of 2004 states that the public has the right to provide input, in writing or orally,regardingDraftLocalRegulations(Raperda).SincetheRAPBDisproposedintheformofa Raperda, the local administration and/or DPRD should conduct public consultationsduringthebudgetdeliberationprocess.Implementationof the LocalGovernmentBudget ismarkedby the establishment oftheAPBD.TheAPBDisestablishedthroughaPerdaandthenelaboratedinaRegulationof theHeadof theRegion (Perkada)which is a compilationof theDPASKPD (BudgetDeclaration Documents of Local Government Work Units). The period ofimplementationofthelocalgovernmentbudget,pursuanttoLawNo.17/2003andLawNo. 1/2004, is one budget year, running from1 January through 31December. SincemanyAPBDarenotestablishedontime,thebudgetimplementationperiodisreduced.Typically,localitiesthathavenotestablishedtheAPBDbythespecifieddeadlineusethepreviousyear’sAPBDasareference.Changes in macroeconomic conditions and shifts of expenditures between activityprograms and units create the opportunity for the local government to revise theAPBD. The Law limits the time for establishing revision of the APBD to no later thanthreemonthsbeforetheendofthebudgetyearconcerned.TheprocessfordeliberationoftherevisedAPBDisthesameasthatfortheinitialAPBD.ThemechanismforrevisionoftheAPBDisperformedbysubmittingaRevisedKUAPPASwhichexplainsthereasonsfortheneedtorevisethebudget.Implementationof the localgovernmentbudget,particularly fordirectexpenditure, isdone through direct provision of public services (such as Community Health Centers,licensing,etc.)orprocurementofgoodsandservicesthroughopentenderforamountsoverRp50million.PresidentialDecreeNo.80of2003anditsrevisionsstatetheneedfor an institution forprocurementofpublic goodsand services that is integrated in asingleunittopromoteefficiencyinthetenderprocess.

23

Withregardtopublicservices, littleregulatoryreformhastakenplace.AlthoughthecentralgovernmenthasissuedPPNo.65/2005onMinimumServiceStandards(SPM),intheimplementationfewsectorshaveasyetformulatedtheirSPM.OnlytheHealthandEducationsectorshaveSPM.Furthermore,fewlocalgovernmentshavemechanismsforcitizenstosubmitcomplaintsaboutpoorlocalgovernmentservices.Budget accountability is the final process in the budget cycle, after the one‐yearbudget implementation period has ended. Three months after the budgetimplementationends,thelocalgovernmentmustsubmititsLocalGovernmentFinancialStatements (LKPD) to the BPK (State Audit Agency) to be audited. Later, the BPKpresents the results of its audit to the DPRD. The BPK audit resultmay state any ofseveral categories of opinions on the LKPD, from the best, Unqualified Opinion, toQualifiedOpinion,AdverseOpinion,andfinallyDisclaimerofOpinion.

Separatefromthefinancialstatements,pursuanttothemandateofPPNo.03/2007,thelocal government is obliged to prepare a Local Government Accountability Report(LPPD)asaformofbothverticalandhorizontalaccountability.TheLPPDissubmittedtothecentralgovernment(MinistryoftheInterior),theDPRD,andthepublic.Infact,theLPPD Information that is conveyed to thepublic requiresprovisionof space for thosewho wish to submit comments. Although such a mechanism is stipulated, few localgovernments actually apply LPPD in a timely way or provide means for citizenparticipation to provide comments on the Local Government Accountability ReportInformation(ILPPD).

24

Chapter III

Performance in Transparency of Local Government Budget Management

A. Introduction The existence of LawNo. 14 of 2008onOpenness of Public Information creates theopportunity for the public to obtain clear, full information on public services frompublicagencies,includinglocalgovernments.TheLawstatesthatallpublicdocumentsmaybeaccessedby thepublic– includinggovernmentworkplandocuments (central,provincialandlocal)andgovernmentbudgetdocuments–withoutexception.ThisLawwillcomeintoforcein2010.Forthisreason,governmentsneedtoimmediatelyprepareinformationserviceapparatus,proceduresandinstitutionstoensureeasier,moreopenaccesstoinformation.Transparency performance, in this research, refers to two indicators: availability oflocalgovernmentplanningandbudgetingdocuments,andaccessibilityofdocuments.These indicators aim to discover the degree of transparency of local governments insystematicallyprovidingandopeningupaccesstoinformationateachstageofbudgetplanning.Twenty budget planning documents were tested for budget transparencyperformance. There are actually over 30 local government planning and budgetingdocuments, but this research focuses only on the 20 documents that are consideredimportant to observe local governments’ performance in opening access to budgetdocuments. The selected documents were then categorized based on the localgovernment budgeting cycle: planning, discussion, implementation and accountabilitystages.ThetypesofdocumentsselectedcanbeseeninChapter1,specificallyinChart1.

B. Findings Localgovernments’effortstoprovideandopenaccesstolocalgovernmentplanningandbudgetdocuments show fairlygoodprogress.This is indicatedby the increasingnumberofpublicdocumentsthatarenowavailableandcanbeaccessedbythepublicintheplanning,discussionand implementationstages.Thisresearch indicatesthatthesethree stages of local government budget management have an adequate level oftransparency. The progress of local governments in promoting the process oftransparencydeservesappreciation,particularlyinthediscussionstage.Inthisstage,wefound several governments that are providing and opening up access to budgetingdocuments,specifically RKASKPDandRAPBD.Meanwhile, intheplanningstage, localgovernmentsgenerallyprovideandgrantaccesstoplanningdocumentsbecausethesedocumentsareusuallyintheformofpolicydirectionandactivityprograms,withoutany

25

budgetinformationprovided.Likewise,intheimplementationstage,governmentshaveahighleveloftransparencybecausethe budget documents available,such as the APBD, are products ofpolicies that have been establishedas Perda (local regulations) thatmustbepublished.Local governments face quiteserious challenges with regard tothe transparency of localgovernment budget managementdocuments in the accountabilitystage. In the accountability stage,local governments show a lowerlevel of transparency than in theother stages (see graph 3.1). Fromthe availability and accessibility testing, it was found that documents in theaccountabilitystagetendtobe lessavailableand lessaccessible.Thisfinding indicatesthat the efforts of local governments to open public access to documents on theoutcomesofimplementationofannualprogramsremainlow.Governmentsstilltendtoconcealinformationrelatingtotheaccountabilityreportfromthepublic.Publicspacetobecomeinvolvedintheprocessofevaluatingdevelopmentimplementationisrestrictedbythelackofaccessandavailabilityofthesebudgetdocuments.Withregardtoavailabilityofdocuments,localgovernmentshavegenerallyproducedtheexistingdocuments,apartfromILPPD.TheILPPD(LocalGovernmentAccountabilityReportInformation)isthedocumentmostoftennotprovidedbylocalgovernments.Wefound that 34.1% of local governments did not produce ILPPD documents. Thisdocument differs from the LKPD, which is a report on the local government’saccountability to themembers of the legislature as representatives of the people. Incontrast, the ILPPD is a document that the government must produce to provideinformation to the public on its accountability report on the execution of itsdevelopmentprogramsovertheyear.ThisisinlinewiththemandateofPPNo.3/2007onReportsontheConductofLocalGovernments,whichrequireslocalgovernmentstoproduce and publish ILPPD to the public. There are two reasons for thisscarmunicipality: First, governments have not paid enough attention to buildingmechanisms for public accountability and transparency through the ILPPD document;andsecond,severalofthelocalgovernmentssurveyedsaidthattheywerenotawareoftheexistenceoftheregulation,andthereforedidnotproduceILPPD.

Graph 3.1 Levels of Budget Transparency in Stages of Local Government Budget

Management

26

Graph3.2TypesofBudgetManagementDocumentsthatareNotProduced,Inaccessible,Accessible,andPublishedbyLocalGovernments

Of the20 typesof localgovernmentbudgetmanagementdocumentsexamined, 17(41.5%) of local governments did not produce one or two of the budget planningdocuments. These 17 localities were distributed throughout nearly all the provincesstudied. Only in the province of Central Java did all local governments produce allbudgetplanningdocuments.ApartfromtheILLPD,otherdocumentsnotproducedweretheRenjaSKPDforEducationinLombokBaratandMalangdistricts,theKUA‐PPASintheMunicipality of Blitar, the Semester I APBD Realization Report and Perda on APBDAccountabilityinPasuruanDistrict,andthePerdaonRevisedAPBDandthePerkadaonElucidationofAPBDPinAcehBesar.Withregardtoaccessibility,localgovernmentshaveopenedaccesstoobtainplanningand budgeting information documents, upon request through either formal orinformal mechanisms, at each stage of budget management. Over 75% of localgovernmentsconductsuchpractices.Oneformalchannelcommonlyused isarequestletter to the local government. Informal channels include the use of key informants,eithermembersofthelegislatureoradministrationofficials.Thisfindingindicatesthatthe governments’ efforts to open access to planning and budgeting documents andinformationaremovinginapositivedirectioninresponsetotheenactmentofLawNo.14of2008onOpennessofPublicInformation.Althoughmostdocumentscanbeobtainedthroughrequest letters, thebureaucraticchannels still create difficulty in accessing planning and budgeting documents.As aresult, not all budget planning documents studied were accessible. In only 11 local

27

Box 3.1: Budget Documents Kept at Home

A researcher in Bojonegoro District conducted a focus group discussion (FGD) with local government officials to test the availability and accessibility of documents. During the FGD, the researcher gave a presentation on his preliminary assessment based on the data testing and then asked the participants to comment. In his findings, the researcher noted that one SKPD had not produced its Renstra SKPD document. But a government official from the SKPD concerned disagreed with this assessment, saying the documents were in fact available. When asked where the documents were, the official explained that he kept the documents at home because it was often difficult to find the planning and budgeting documents when they were kept at the office.

governments (26.8%) were all the documents accessible. Most of the other localgovernments(30governments,or73.2%)didnotprovideaccesstouptoninetypesofplanning and budgeting documents, even using formal request letters and theapplicableprocedures.Therewasevenonelocalgovernmentwhere18ofthe20budgetdocuments studiedwere inaccessible. This research also found that ease in obtainingdocuments depended onwho the request letter was addressed to. Several Heads ofServicesandBappedaintheresearchregionsobjectedtorequestlettersbeingdirectedtothemasthepartiesthatcouldgrantaccesstoinformation/documents.TheyfeltthatsuchrequestsshouldbeaddresseddirectlytotheRegentorRegionalSecretary,astheydid not have the authority to grant the researchers access to the documents.Meanwhile, in several regions, we had to request a research permit beforehand toobtain access to documents. Not one region had a clear mechanism for obtainingdocuments. This indicates that openness of access to planning and budgetingdocumentsandinformationhasnotbeenconstructedsystematicallyfortheinterestsofthegeneralpublic.Notonelocalgovernmenthadanadequatefilingsystemforplanningandbudgetingdocuments.Planning and budgeting documentswere stored inadequately in all LocalGovernmentWorkUnits (SKPD). Even the SKPDdidnothaveplaces for filing all theirown planning and budgeting documents. Generally, the heads of SKPD and bureau

headsbelow themmaintainedthe documents personally. Inseveral local governments, itwasfoundthatthedocumentswere taken by individuals andkept at their homes.Furthermore, the Bappeda, animportant agency thatcoordinates the planning andbudgeting processes, also didnot have filing systems forbudget documents. Theresearchers were oftenreferred to other agencies orthe respective SKPD whenseeking the documents they

needed. This situation indicates that local governments do not have a one‐roofdocumentrequestmechanismthatwouldenablethepublictoeasilyaccessdocuments.Local governments aremore open with budget planning documents that deal withgeneralpolicybuttendtobemoresecretivewiththosedealingwithsectoralpolicies.TheRPJMDandRKPDarethedocumentsmostoftenpublishedbylocalgovernments.Incontrast, sectoral budget planning documents (Education, Health, and Public Works)such asWork Plans, RKA, andDPA SKPD are the documents that aremost often notpublishedornotevenaccessibletothepublic.Thissituationwasfoundinaround30%

28

to 40% of the local governments studied. In fact, these more detailed sectoraldocumentsprovideclearerinformationontheactivitiesandbudgetsoftheSKPD.TheEducationRKASKPDwasnotaccessibleattenlocalgovernments,theHealthRKASKPDcouldnotbeaccessedat12 localgovernments,andthePublicWorksRKASKPDcouldnotbeaccessedat13localgovernments.However,theRAPBDwasstillaccessibleat12localgovernments.AmongthethreesectoralSKPDstudied,PublicWorkswastheSKPDthatmostoftenshutoffaccesstoplanningandbudgetingdocuments.ThedocumentsinPublicWorksSKPDthatweredifficulttoaccessincludedtheWorkPlandocuments(RenjaSKPD)at16localgovernments,thePublicWorksRKAat13localgovernments,andthePublicWorksDPA at 15 local governments. Generally, the Public Works SKPD receives a largerproportion of the budget thanother SKPD, but they tended to be less transparent inopenness of information and documents. In fact, this SKPD is the spearhead forproviding infrastructure in the regions. The budget documents that are generallydifficulttoaccessarethosethathaveamajorinfluenceonlocalgovernmentbudgetingand officials, those that indicate the details of the budget ceilings, and those thatdescribebudgetrealization.Intheareaofpublicationofbudgetdocuments,thisresearchshowsthatmunicipalitygovernments tend to be more open than district governments. The locality thatpublishesthemostbudgetplanningdocuments,boththroughitswebsiteandthroughothermedia,istheMunicipalityofParepare.Thismunicipalitypublishedeight(40%)ofthe 20 budget planning documents studied. Among these eight documents were theRAPBD and Perkada on Revised APBD (in other local governments, these documentscouldonlybeaccesseduponspecialrequest).ThenextlocalitythatpublishedmanyofitsbudgetdocumentswastheMunicipalityofSurabaya(sevenbudgetdocuments).Ontheotherhand, localgovernmentsthatpublishedonlyonetypeofbudgetdocumentswereBoneDistrict,PolmanDistrict,theMunicipalityofSurakarta,BoyolaliDistrict,andMalangDistrict.The localitywhere itwasmostdifficult toaccess thebudgetdocumentswasCilacapDistrict.There,18 (90%)of the20documentscouldnotbeaccessed, followedby theMunicipalityofBanjarwith12documents(60%)andtheMunicipalityofBlitarwithten(50%) documents. There were 27 other localities where an average of five to sevenbudget documents could not be accessed. The following graph shows localgovernments’opennessingrantingaccesstotheirplanningandbudgetingdocuments.

29

Graph3.3.AccessibilityofBudgetDocumentsinResearchRegions

C. Budget Transparency Performance of Local Governments Municipality governments dominate the top rankings in budget managementtransparency performance of local governments.One factor that seems to influencethis is the availability of adequate infrastructure to support the provision of moretransparentinformationservices,aswellasthephysicalsizeoftheregions,whichtendtobesmallerformunicipalitiesthanfordistricts.Furthermore,thisresearchalsofound

30

that most of the lowest rankings in transparency performance were dominated bydistrictgovernments.Using an assessment of the availability and accessibility of budget managementdocuments, this researchplaces theMunicipalityofParepareas the regionwith thebestbudget transparencyperformanceamong the41 regions studied. Thenext topfour regions were, in order, the Municipality of Padang Panjang, Sleman District,MunicipalityofPontianakandMunicipalityofPekalongan.Incontrast,theMunicipalityofBanjarandfourdistricts–Malang,Cilacap,PasuruanandBondowoso–hadthefivelowest rankings. The following graph shows the budget transparency performance oflocalgovernments.

31

Graph3.4.BudgetManagementTransparencyPerformanceofLocalGovernments

TheMunicipalityofParepareisinthefirstrankingamongthetopfivebecauseithasthe most complete and most easily accessible budget management documents,althoughmostof thePlanningandDiscussiondocumentshad tobeobtained throughrequest, suchasRPJMD,RKPD,Renja SKPD,RKASKPD,andPPAS.Another interestingthing about this region is the extensive publication of several of the budgetimplementation andaccountability documents, including thePerdaonAPBD,PerkadaonElucidationofAPBD,PerdaonRevisedAPBD,PerkadaonRevisedAPBD,SemesterIAPBD Realization Report, Perda on Accountability for Implementation of APBD, andLPPDInformation.

32

In theMunicipality of Padang Panjang, which holds the second ranking, most of theplanning and budgeting documents were accessed through request; only the PerdaAPBDdocumentwaspublished,throughposters,andonedocumentwasnotaccessible– theRenjaSKPDonHealth.SlemanDistrictwas in thirdpositionbecausemanyof itsplanning and budgeting documents are published on its website and thereforeaccessibletothepublic.ThedocumentspublishedonthewebsiteincludeRPJMD,RKPD,PerdaonAccountabilityfor ImplementationofAPBD,andLPPDInformation,whiletheother documents are available upon request. However, compared with the two topregions(MunicipalityofParepareandMunicipalityofPadangPanjang),therearemoredocuments that are not accessible in Sleman District, including DPA SKPD for PublicWorks,DPASKPDforEducation,andRKASKPDforHealth.Incontrast,many localgovernments inEastJavaheldthe lowestrankings inbudgetmanagementtransparencyperformance.Obviously, this findingshouldserveas inputfortheEastJavaProvincialGovernmenttoprovidesupervisionandtechnicalassistancetoencouragegreatertransparencyinbudgetmanagement.

33

Chapter IV

Participation Performance in Local Government Budget Management

A. Introduction

Oneimportantindicatorfortheconductofgoodgovernanceinademocraticstateisincreasedactivityofpublicparticipationinvarioussectorsofcommunitylife.Effortstopromote the concepts and practices of participation in development planning andimplementationemergedininternationaldiscourseinthe1970s.Theconceptofcitizenparticipation then shifted from mere concern for the beneficiaries of charity or thedisadvantaged to a concern for the various forms of citizen participation in theformulationofpoliciesandmakingofdecisionsthatstronglyaffecttheirlives6.Indonesia’sgovernmentalregulatoryframeworkguaranteespublicinvolvementintheformulation and setting of public policy. Law No. 25 of 2004 on the DevelopmentPlanning System and Law No. 32 of 2004 on Local Governance stipulate citizeninvolvement inthedevelopmentplanningprocess.Citizenshavetherightasmembersoftheircommunitiestoprotectpublicspace,aggregateissues,planthepublicagenda,and continuously monitor the performance of the people’s representatives and thegovernmenttoensurethattheyworkinaccordancewiththemandatetheyhavebeengiven.This isparticularly importantwhensuchpoliticaldecisionshaveadirect impactonthepublicwelfare,specificallyplanningandbudgetingpolicies.Budget participation performance in this research refers to the degree of citizeninvolvement in decision making at each stage of budget planning. The indicatorsobserved are means or media for participation provided by the local government,guarantees of regulations produced by the local government, and representation ofparticipants and citizen authority for or influence in decision making. Means forparticipationaredefinedasavailabilityandformsofvehiclesforparticipationprovidedineachstageofplanningandbudgeting.

Although many studies state that participation has increased in the Musrenbangprocess, this research does not specifically look at the Musrenbang process at thevillage/subdistrict,district,anddistrictlevels.

6 Pelembagaan dan Penganggaran - Monev Partisipatif: Mewujudkan Pro Poor Budget (Institutions and Budgeting – Participatory Monitoring and Evaluation: Realizing a Pro Poor Budget), Pattiro Surakarta – The Asia Foundation, 2007, pp. 27-28.

34

B. Findings Budget participation performance of local governments is very low in all stages oflocal government budget management. Nearly all scores for budget participationperformancearebelow50.Budgetparticipationperformanceintheplanningstagehasaslightlyhigherscorethantheotherthreestagesintheplanningandbudgetingcycle.The planning stage is the stage in which the public is provided with a means forparticipation through the Development Planning Conferences (Musrenbang) at thevillage/subdistrict level. Representative mechanisms are provided at the district anddistrictlevelsandintheSKPDForums.Theaccountabilityanddiscussionstagesarethestages with the lowest levels of participation performance. As with the findings in

transparency performance, theprocess of public involvement inthe accountability stage is veryclosed, because this stage isgenerallyassumedtobethearenafor the executive’s accountabilityto the legislature, and so there isvirtuallynopublic space.Theonlypublic space in this stage isprovided through the mechanismfor drafting the ILPPD.Unfortunately, many localgovernments do not produce thisdocument. Furthermore, there isalmost no initiative from localgovernments to develop anaccountability mechanism byinvolving the public directlywithout going through their

representatives in the DPRD, since the head of the region is elected directly by thevoters. In the discussion stage, public participation is low because many localgovernments do not involve the public in the process of establishing the APBD. Thisprocess isstillconsideredtheexclusivespaceof theexecutiveandthe legislature;rhepublicwillbe involvedonce theAPBD ispromulgated, throughactivities to“socialize”theAPBD.Unfortunately,notevenoneregionhasdevelopedpublicconsultationontheRAPBDdocumentbefore it ispromulgatedas theAPBD. In fact, thisactivity isastagewherethepubliccouldprovideinputbeforetheAPBDisformallyestablished.Local governments tend to open up access for participation only in the planningprocess but not in the budgeting process. The findings of this research indicate thatmeans forpublicparticipationaregenerallyprovidedby localgovernmentsduringthedraftingofdevelopmentplanningdocumentssuchasRPJMD,RKPD,RenstraSKPDandRenjaSKPD.However,duringtheformulationofbudgetdocuments,vehiclesforpublic

Graph 4.1 Levels of Participation in Stages of Budget Management

35

involvementtendnottobeprovided,forexampleinthedraftingofKUAPPAS,RAPBDandRaperdaonAccountability.Graph4.2.AvailabilityofMeansforCitizenParticipationinDraftingofLocalGovernment

BudgetManagementDocuments

With regard to provision of means for participation, local governments often draftSKPDplanningdocumentswithoutannouncing it tothepublic.Thismeansthatevenwhen local governments have provided vehicles for the public to participate, in theactualimplementationthepublicisoftennotinvitedtotheseactivitiesbecausetheyarenotpubliclyannounced.ThedraftingofSKPDRenjaandRenstraaretheactivitiesthatare often not announced to the general public. The participants that are involved intheseactivitiesaregenerallyonlytheexecutive,thelegislatureandafewpeoplefromuniversities. In fact, to bring together the public interests in Education, Health, andInfrastructureservices,thereneedstobepublicconsultationbetweenthesectoralSKPDconcernedandthepublic.Incontrast,thedraftingofRPJMDandRKPDaretheactivitiesthat are most often announced to the public, though still to rather limited circles.Representativesofsectoralcommunitygroups,NGOs,themassmediaanduniversitiesare often invited to the drafting of these documents. It seems that local governmentprovidemeans for participation in the drafting of these two documents because it isexplicitlymandatedbyLawNo.25/2004ontheNationalDevelopmentPlanningSystemtoconductMusrenbangintheirformulation.

Graph4.3InformationMechanismsonDraftingofLocalGovernmentBudgetManagementDocuments

36

TheSurabayaMunicipalitygovernmentistheregionthatprovidesthemostmeansforparticipation involving the general public, though this only applies for the drafting ofRKPD,RPJMDandPublicWorksRenstraSKPDdocuments.Theregionthatprovidesnomeans of public participation at all in the formulation of planning documents isSitubondoDistrict.Only one local government providesmeans for the community toprovidecomments on the LKPD, establishedthrougharegulation.This is thecaseinBojonegoroDistrict. In contrast,17ofthelocalitiessurveyeddidnothavemeans for public participation toprovideinputontheILPPD.Andin15other localities, no such means isprovided because the localgovernment never produces theILPPD.Thissituationindicatesthatthecommitment of local governments todeveloptheirregionsonthebasisofthepublicinterestremainslow.Local governments’ commitment to ensuring public involvement in budget planningcould be much better. Local government regulations that provide a basis for citizeninvolvement in the planning and budgeting processes are almost non‐existent.Generally, in implementing community involvement, local governments use nationalstandardsas theunderlyingbasis, especially theMinisterof the Interior JointCircular(SEB) to regulate the mechanism for implementation of Musrenbang in the regions.Even so, this research shows that eleven regionshaveprovidedguarantees forpublicparticipation through local regulations (Perda),while four other regions regulate thisthrough regulations of the heads of the regions (Perkada). On the other hand, 20regions have no regulations to guarantee public involvement in budget planning. Thetablebelowprovidesalistofsomeoftheregulatoryguaranteesissuedbycertainlocalgovernments.

Box 4.1. Friday Forums as a Medium for Government/ Public Dialogue

The Bojonegoro District Government routinely conducts dialogues with citizens on Fridays after weekly prayers. This activity, called the “Friday Forum,” gives the residents of Bojonegoro an opportunity to provide input on all local development activities, including when the local government is preparing the Bojonegoro District Government’s Financial Statements (LKPD). The Friday Forums were established through Decree of the Regent of Bojonegoro No. 188/305/KEP/412.12/2008 on Public Dialogue between the Bojonegoro District Government and the People of Bojonegoro District.

Graph 4.4 Availability of Means of Participation in LKPD

37

Table4.1RegulationsGuaranteeingPublicParticipation

No Locality Description1 BoneDistrict PerdaNo.8of2008onMusrenbang2 GarutDistrict LocationRegulationNo.17of2008on

TransparencyandParticipation3 Municipalityof

BandarLampungBandarLampungMunicipalityRegulationNumber:13of2002onPublicparticipationinPreparationoftheBandarLampungMunicipalityRevenueandExpenditureBudget(APBD)

4 MunicipalityofGorontalo

• PerdaNumber2of2002onCommunity‐BasedDevelopmentPlanning

• PerdaNumber3of2002onTransparencyandPerdaNumber4of2002onOversightoftheConductofGovernance

5 MunicipalityofPalu PerdaNumber5of2006onTransparentandParticipatoryConductofLocalGovernanceintheMunicipalityofPalu

6 MunicipalityofPontianak

PerdaNo2of2009onOpennessofPublicInformation;guaranteeofparticipationismentionedinArticle1paragraph(20);

7 MunicipalityofSemarang

PerdaNo.9of2007onProcedureforFormulationofRegionalDevelopmentPlan

8 MunicipalityofParepare

PerdaNo.17of2004onConductofCommunity‐BasedDevelopment

9 SumbawaBaratDistrict

LocalRegulationNumber27of2008onNeighborhoodAssociation‐BasedDevelopment

10 SumedangDistrict PerdaNo1of2007onProceduresforLocalGovernmentPlanningandBudgetinginSumedangDistrict

10 WajoDistrict PerdaNo11of2004onParticipatoryDevelopmentinWajoDistrict

12 KendalDistrict LocalRegulationNo.6of2006onProceduresforFormulationofLocalDevelopmentPlanningandImplementationofLocalDevelopmentPlanningConferencesinKendalDistrict

13 MunicipalityofBlitar DecreeoftheMayorofBlitarNo.67of2004onParticipatoryDevelopmentManagementSystem

14 MunicipalityofSurakarta

MayoralRegulationNo17of2008onPreparationforImplementationofMusrenbang

15 MunicipalityofPadangPanjang

DecreeoftheMayorofPadangPanjangNo.31of2003onProceduresforParticipatoryPlanningintheMunicipalityofPadangPanjang

38

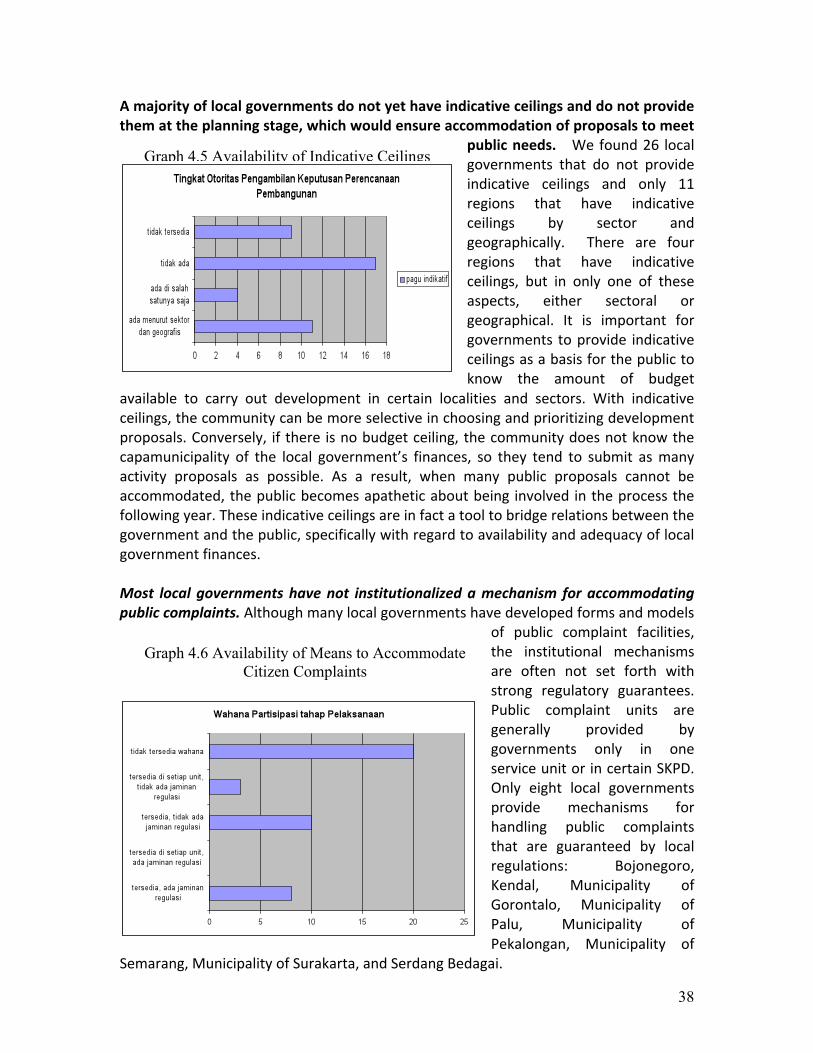

Amajorityoflocalgovernmentsdonotyethaveindicativeceilingsanddonotprovidethemattheplanningstage,whichwouldensureaccommodationofproposalstomeet

publicneeds. Wefound26 localgovernments that do not provideindicative ceilings and only 11regions that have indicativeceilings by sector andgeographically. There are fourregions that have indicativeceilings, but in only one of theseaspects, either sectoral orgeographical. It is important forgovernments toprovide indicativeceilingsasabasisforthepublictoknow the amount of budget

available to carry out development in certain localities and sectors. With indicativeceilings,thecommunitycanbemoreselectiveinchoosingandprioritizingdevelopmentproposals.Conversely, ifthere isnobudgetceiling,thecommunitydoesnotknowthecapamunicipality of the local government’s finances, so they tend to submit asmanyactivity proposals as possible. As a result, when many public proposals cannot beaccommodated,thepublicbecomesapatheticaboutbeing involved intheprocessthefollowingyear.Theseindicativeceilingsareinfactatooltobridgerelationsbetweenthegovernmentandthepublic,specificallywithregardtoavailabilityandadequacyoflocalgovernmentfinances.

Most localgovernmentshavenot institutionalizedamechanism foraccommodatingpubliccomplaints.Althoughmanylocalgovernmentshavedevelopedformsandmodels

of public complaint facilities,the institutional mechanismsare often not set forth withstrong regulatory guarantees.Public complaint units aregenerally provided bygovernments only in oneserviceunitorincertainSKPD.Only eight local governmentsprovide mechanisms forhandling public complaintsthat are guaranteed by localregulations: Bojonegoro,Kendal, Municipality ofGorontalo, Municipality ofPalu, Municipality ofPekalongan, Municipality of

Semarang,MunicipalityofSurakarta,andSerdangBedagai.

Graph 4.5 Availability of Indicative Ceilings

Graph 4.6 Availability of Means to Accommodate Citizen Complaints

39

Executivesandlegislaturesstilltendnottoconductpublicconsultationsinthebudgetmanagementprocess.Specifically inthediscussionofKUAPPASandRAPBD, innearlyhalf the research localities these two institutions do not conduct public consultationbefore these documents are promulgated. Furthermore, nearly 30% of localgovernments conduct public consultations with only limited invitations, withoutannouncementoraninvitationtothegeneralpublic.

Graph4.7.AvailabilityofPublicConsultationinDiscussionofKUAPPASandRAPBD

C. Participation Performance of Local Government Budget Management

As with transparency performance, municipality governments dominate the toprankingsinparticipationperformanceoflocalgovernmentbudgetmanagement,anddistrict governments dominate the lowest rankings. One important factor thatpromotesadequateparticipation is thephysical sizeof the region.Thesmaller sizeof

Box 4.2. Various Means for Accommodating Public Complaints

The commitment of the Pekalongan Municipality government to accommodate citizen complaints is implemented every Wednesday from 9 to 10 am through the Mayor’s talk show program on Radio Kota Batik, which provides a means for the public to present their complaints and have them answered by the Mayor. Meanwhile, in the Municipality of Blitar, the government has provided a means to accommodate public complaints by establishing a public complaint and information service unit, with a website, www.ulpim.net.

40

municipalities seems to have a significant influence in promoting better publicparticipation.The Municipality of Padang Panjang is the region with the best participationperformanceinlocalgovernmentplanningandbudgetingprocesses.Thismunicipalityprovidesmanymeans for communityparticipation through theguaranteesof existingregulations, though still in the form of a Mayoral Decree. The Padang PanjangMunicipality Government has an institutionalized means for accommodating publiccomplaints,thoughithasnotbeenestablishedthrougharegulation.

Graph4.8.ParticipationPerformanceinLocalGovernmentBudgetManagement

Sumedang District is the only district among the top five in terms of participationperformance in budget management. Most of the top five positions are held bymunicipalitygovernmentsratherthandistrictgovernments.ApartfromtheMunicipalityofPadangPanjang,theothermunicipalitiesthathadperformanceinthetopfivewere

41

Bandar Lampung, Surabaya andPekalongan. SumedangDistrict’s success in coming infourthinparticipationperformancewasduetotheexistenceofaLocalRegulationthatensurescitizenparticipationinthedevelopmentplanningprocess,PerdaNo1of2007onLocalGovernmentPlanningandBudgetingProcedures,asalegalfoundationforthebudget planning process in Sumedang District. Sumedang District is one of the 11regionsthathavebothsectoralandgeographicalindicativeceilings,andithasextensivemeans for participation in drafting of the RKPD and RPJMD, guaranteed through aPerda.

Bondowoso District is the region with the worst performance in ensuring publicparticipationinplanningandbudgetingprocesses.Ineverystage,thisdistricthasmuchlower scores than all other districts/municipalities. This means that in all stages –planning, discussion, implementation and accountability – this district fails to providemeans for community participation. Regulatory guarantees for participation are alsoinadequate. The four other regions with the lowest performance rankings were thedistrictsofSitubondo,AcehBarat,LombokBaratandPasuruan.

42

Chapter V

Accountability Performance in Local Government Budget Management

A. Introduction Publicaccountabilityisacriticalelementandconstitutesthemainchallengefacedbylocal governments. Public accountability is a principle which guarantees that thegovernmentelementsconcernedcanopenlyaccountforallactivitiesintheconductofgovernancetothepartiesaffectedbytheapplicationofpolicies.Thus,accountabilityisthe capamunicipality of a given government agency to account periodically for itssuccessesand failures incarryingout itsmissiontoachievetheobjectivesandtargetsthat have been set. In this definition, each government agency has an obligation toaccount for itsorganization’sachievements inmanagingtheresourcesentrustedto it,fromtheplanningstage,throughimplementation,tomonitoringandevaluation.7Theassessmentofaccountabilityusedinthisinstrumentfocusesmostlyontheextentof efforts by local governments to account for their budget management. Threeaspects are assessed: means provided by the government to convey accountability,timelinessinpreparationandpromulgationofplanningandbudgetingdocuments,andthe BPK’s opinion on the result of its audit of local government finances. Themeansprovided relate to the mechanism and system for management of procurement ofgoodsand services, theprocess forpresentationof financial statements to theDPRD,andsettingofpricestandards.Timelinessinpreparationandpromulgationofplanningandbudgetingdocumentshasbeenchosenaspartoftheassessmentofaccountabilitybecause delays in the promulgation of these documents will lead to delays in theimplementationofgovernmentprogramsforthepublic,andthiswilldirectlyaffecttheavailability of government public services to the community. For example, delay inpassingtheAPBDwillleadtoshortagesofmedicinesforthepoor,delayedpaymentofsalaries,agriculturalprogramsoutofsynchwiththeplantingseason,andsoon.In assessing timeliness in establishment and delivery of planning and discussiondocuments, this research uses the reference of the existing statutory regulations.Basedontheprevailingregulations,theprocessofestablishingplanningandbudgetingdocuments has been stipulated by the central government as shown in the followingtable:

7 Max. H. Pohan, Mewujudkan Tata Pemerintahan Lokal yang Baik (Good Governance) dalam Era Otonomi Daerah (Realizing Local Good Governance in the Era of Regional Autonomy), paper presented at the Third Musi Banyuasin Major Development Conference, Sekayu, 29 September – 1 October 2000.

43

Table5.1.RegulatoryFrameworkofTimesforEstablishingBudgetDocuments

Document TimeforEstablishment LegalBasisRPJMD Sixmonthsafterheadof

regionisinauguratedPPNo.8/2008,Article15paragraph(2)

RKPD EndofMay PPNo.58/2005,Article33paragraph(2)Permendagri13/2006,Article82paragraph(2)

APBD EarlyDecemberbeforestartofbudgetyear

PPNo.58/2005,Article45paragraph(1)PermendagriNo.13/2006,Article104paragraph(2)

APBDP Threemonthsbeforeendofcurrentbudgetyear

PermendagriNo.13/2006,Article172paragraph(5)

The time limits for discussion of planning and budgeting documents are stipulatedthroughthefollowingregulations:

Table5.2.RegulatoryFrameworkofDeadlinesforDiscussionofBudgetDocuments

Document SubmissionTime LegalBasisKUA‐PPAS EarlyJune PermendagriNo.13/2006RAPBD FirstweekofOctober PermendagriNo.13/2006RAPBDP Secondweekof

SeptemberArticle172paragraph(2),PermendagriNo.13/2006

C. Findings Localgovernments’effortstopromoteperformance in public accountabilitydeserveappreciation.Inthecontextofthisresearch,theaccountabilityoflocalgovernments shows relatively goodresults in all stages of budgetmanagement, particularly in theplanning, implementation andaccountability stages. The planningstage has a very high level ofaccountability performance becausethe planning documents are generally

Graph 5.1 Level of Accountability in Stages of Budget Management

44

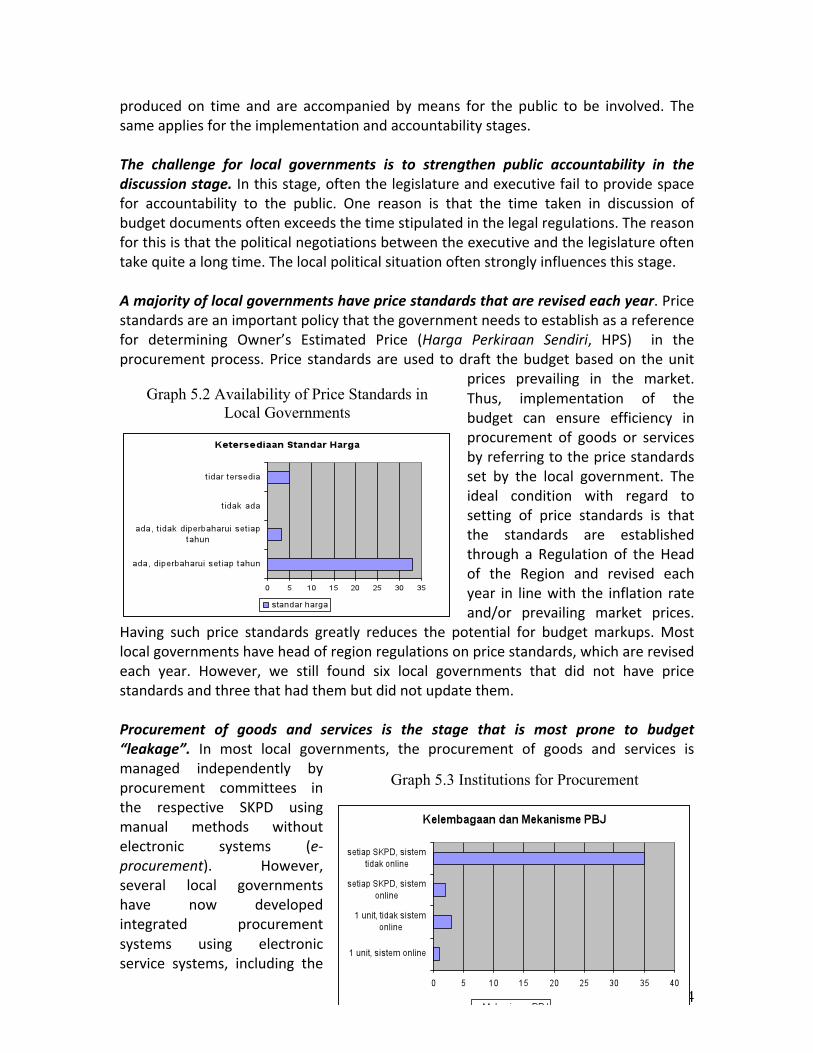

produced on time and are accompanied bymeans for the public to be involved. Thesameappliesfortheimplementationandaccountabilitystages.The challenge for local governments is to strengthen public accountability in thediscussionstage.Inthisstage,oftenthelegislatureandexecutivefailtoprovidespacefor accountability to the public. One reason is that the time taken in discussion ofbudgetdocumentsoftenexceedsthetimestipulatedinthelegalregulations.Thereasonforthisisthatthepoliticalnegotiationsbetweentheexecutiveandthelegislatureoftentakequitealongtime.Thelocalpoliticalsituationoftenstronglyinfluencesthisstage.Amajorityoflocalgovernmentshavepricestandardsthatarerevisedeachyear.Pricestandardsareanimportantpolicythatthegovernmentneedstoestablishasareferencefor determining Owner’s Estimated Price (Harga Perkiraan Sendiri, HPS) in theprocurementprocess.Price standardsareused todraft thebudgetbasedon theunit

prices prevailing in the market.Thus, implementation of thebudget can ensure efficiency inprocurement of goods or servicesbyreferringtothepricestandardsset by the local government. Theideal condition with regard tosetting of price standards is thatthe standards are establishedthrough a Regulation of theHeadof the Region and revised eachyear in linewith the inflation rateand/or prevailing market prices.

Having such price standards greatly reduces the potential for budgetmarkups.Mostlocalgovernmentshaveheadofregionregulationsonpricestandards,whicharerevisedeach year. However, we still found six local governments that did not have pricestandardsandthreethathadthembutdidnotupdatethem.Procurement of goods and services is the stage that is most prone to budget“leakage”. In most local governments, the procurement of goods and services ismanaged independently byprocurement committees inthe respective SKPD usingmanual methods withoutelectronic systems (e‐procurement). However,several local governmentshave now developedintegrated procurementsystems using electronicservice systems, including the

Graph 5.2 Availability of Price Standards in Local Governments

Graph 5.3 Institutions for Procurement

45

Box : Procurement of Goods and Services in Surabaya

The Municipality of Surabaya has pioneered the development of e-procurement systems since 2004, and the system used in Surabaya has now been adopted by two national agencies and nine districts/municipalities. The Surabaya Municipality Procurement Service Unit (ULP), which has 12 work groups and 36 certified staff, was established in early 2008. This reform of the procurement system has been proven to increase budget efficiency. In 2009 alone, from 2,193 work packages, there were savings of Rp 384 billion (efficiency of 32% of the total amount budgeted). With the Law on ITE, the entire procurement process can now be conducted in a fully electronic way, so that even the bid documents are provided as soft copies.

Province of West Java, Municipality of Surabaya, and Municipality of Cimahi. It isbelievedthatintegratedprocurementofgoodsandservicesbyestablishingacollectiveunittoservetheprocurementneedsofallSKPD,performedelectronically,will reducethe occurrence of collusion and corruption during tender processes. In addition, theexistence of an integrated institution can promote budget efficiency, enhance thecredibilityofprocurementcommittees,andfacilitatetheoversightmechanisms.

Mostexecutivesareseenasprovidingverylittletimeforthelegislaturetostudythebudgeting documents that have been submitted. Certain planning and budgetingdocuments require the approval of both the executive and the legislature for theirestablishment. All these documents are produced or prepared by the executive andthen submitted to the legislature to be studied before being deliberated in a plenarysessionbytheexecutiveandlegislature.Obviously,inthiscontext,thelegislatureneeds