Embed Size (px)

Citation preview

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 1/22

1

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

The Journey Matters: Using Behavioral Finance in theManagement of Client Portfolios

Peter Brooks, Ph.D.

Behavioural Finance Specialist, Asia

May 2013

Securitizing a Cure for Cancer

Andrew W. LoCharles E. and Susan T. Harris Professor andDirector of the MIT Laboratory for Financial EngineeringMIT Sloan School of Management

17 October 2013

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 2/22

2

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Conundrum

Genuine Breakthroughs In Biopharma:• 2001: Gleevec, first of a new class of drugs based on molecular biology

(tyrosine kinase inhibitor)• 2004: Avastin, angiogenesis inhibitor (VEGF)• 2006: Sutent, approved for RCC and GIST simultaneously• 2008: First cancer genome (leukemia) sequenced by Wash U. Genome

Institute, Nature 456 (2008):66–72.• 2012: Dr. Lukas Wartman, Wash U. “cured” of acute lymphoblastic leukemiavia RNA analysis and Sutent

• 2012: David Aponte “cured” of same type of leukemia using immunotherapy (T-cells targeting CD19)

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 3/22

3

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Conundrum (2)

Weak Performance In Biopharma Investments

• January 2002 to January 2012, NYSE/ARCA Pharma Index return:1.2%

• 2001 to 2010 VentureXpert average biotech IRR: 1.0%

-10%

0%

10%

20%

30%

40%

-25%

5%

35%

65%

95%

125%

1 2 / 3 1 9 8 6

1 2 / 3 1 / 9 0

1 2 / 3 1 / 9 4

1 2 / 3 1 / 9 8

1 2 / 3 1 / 0 2

1 2 / 3 1 / 0 6

1 2 / 3 1 / 1 0

1 yr IRR (LHS) 10 yr trailing IRR (RHS)

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 4/224

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Conundrum (3)

Why??• Conjecture: biopharma business model may be broken• As we get smarter, business risk increases (why?)• Additional uncertainty due to recent economic events• VC, private equity, and public equity are not ideal Funding is declining despite/because of better science

Financial Engineering May Offer A Solution• Portfolio theory: multiple “shots on goal”• Securitization: long-term debt, tranches, guarantees,…

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 5/22

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 6/226

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

497613

1,1491,027

685

1,693

2,338

3,173

1,917

2,2302,110

2,204

1,404

2,041 1,976

1,660

2,056

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Lessons from the Financial Crisis? (2)U.S. Mortgage-Related Debt Issuance ($Billions)

Source: SIFMA

What could possiblygo wrong?

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 7/227

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

How Could This Have Happened?

Who Benefited From This Trend?:

Commercial banks Credit rating agencies (S&P, Moody’s, Fitch) Economists Government sponsored enterprises Homeowners Insurance companies (multiline, monoline) Investment banks and other issuers of MBSs, CDOs, and CDSs Investors (hedge funds, pension funds, mutual funds, others) Mortgage lenders, brokers, servicers, trustees Politicians Regulators (CFTC, Fed, FDIC, FHFA, OCC, OTS, SEC, etc.)

“ A Rising Tide Lifts All Boats”

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 8/228

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

How Could This Have Happened? (2)

Innovation Requires Financial Infrastructure!

• Private investment• Accounting, legal, regulatory structures• Systemic stability• Well-functioning capital markets

• Proper design of securities Incentives Are Needed To Motivate Action

Fear Works Faster; Greed Is More Sustainable

• Greed and altruism need not be incompatible

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 9/229

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

The Power of Global Capital Markets

0

100

200

300

400

500

600

700

800

900

1000

0

50

100

150

200

250

1880 1900 1920 1940 1960 1980 2000 2020

P o p u l a t i o n

i n M i l l i o n s

R e a l H o m

e P r i c e I n d e x

U.S. Real Home Price Index, 1890–2012

Source: Robert J. Shiller

Population

E = mc2

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 10/22

10

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Investment Problem

Consider The Following Investment Opportunity:

$200MM investment, 10-year horizon

Probability of positive payoff is 5%

If successful, annual profits of $2B for 10-year patent

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 11/22

11

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Investment Problem (2)

Consider The Following Investment Opportunity:

• $200MM investment, 10-year horizon• Probability of positive payoff is 5%

• If successful, annual profits of $2B for 10-year patent

$200MM

p = 5%

1 p = 95% –100.0%

+51.0%

E[R] = 11.9%

SD[R] = 423.5%

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 12/22

12

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

What If We Invest In 150 Programs Simultaneously?:

• Requires $30B of capital• Assume programs are IID (can be relaxed)

• Diversification changes the economics of the business:

• But can we raise $30B??

Investment Problem (3)

E[R] = 11.9%

SD[R] = 423.5% / √150 = 34.6% ____

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 13/22

13

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

What If We Invest In 150 Programs Simultaneously?:

• Given the reduction in risk, debt-financing is possible!

• $17B of high-quality 10-year debt can be issued

• With securitization (RBOs) and third-party guarantees (CDS), debt

capacity is even larger

Investment Problem (4)

Event Probability

Minimum

Year-10

NPV

Maximum Year-0

Proceeds at

3.75% (10-Yr Aa

as of 9/13/13)

Maximum Year-0

Proceeds at

4.06% (10-Yr A

as of 9/13/13)

At least 1 hit: 99.95% $12,289 $8,504 $8,254

At least 2 hits: 99.59% $24,578 $17,009 $16,509At least 3 hits: 98.18% $36,867 $25,513 $24,763

At least 4 hits: 94.52% $49,157 $34,017 $33,017

At least 5 hits: 87.44% $61,446 $42,522 $41,272

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 14/22

14

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Simulating A Cancer Megafund

• Fernandez, Stein, Lo (Nature Biotech, Oct 2012)• Tufts Medical School CSDD + Deloitte/RECAP cancer compounds database from1990–2011

• 2,000+ compounds 733 after cleaning data

• Cost and revenue assumptions from historical data and literature (e.g., Bloomberg,DiMasi et al. 2003, etc.)

• Estimate transition probability matrix and valuations

• Fagnan, Fernandez, Lo, Stein ( AER, May 2013)• Pricing and impact of third-party guarantees on debt capacity and investment

performance

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 15/22

15

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Simulating A Cancer Megafund (2)

Simulation Results: Matlab and R Software Available

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 16/22

16

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

• What About Personalized/Precision Medicine?

• Fagnan, Gromatzky, Fernandez, Stein, and Lo (2013)• Orphan Diseases: smaller population, urgent need, higher prices,

lower development costs, higher success rates (20%), faster timeto approval (3–7 years)

Simulating A Cancer Megafund (3)

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 17/22

17

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

What About Personalized/Precision Medicine?

Simulation results for funds of $135 million and $225 million areeven more attractive!

Simulating A Cancer Megafund (4)

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 18/22

18

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Is This Realistic?

Is There Capacity From Investors? In 2012:

• U.S. bond market: $38.1T• Mutual funds: $13.1T

• Money-market funds: $2.7T

• Norwegian sovereign wealth fund: $683B

• CalPERS: $237B (as of June 30, 2012)• Target return of 126 public funds (2012): 8%

In 2012, the Size of the Entire VC Industry Was:

$199B

7.5%

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 19/22

19

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

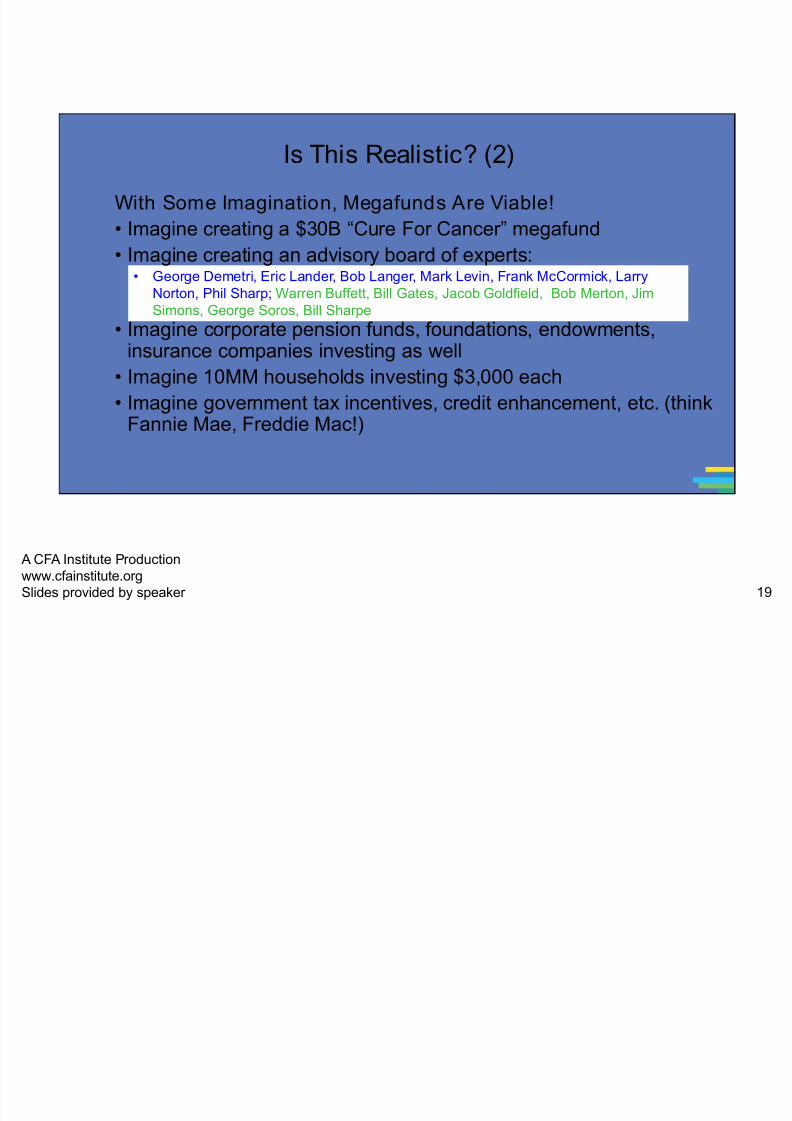

Is This Realistic? (2)

With Some Imagination, Megafunds Are Viable!

• Imagine creating a $30B “Cure For Cancer” megafund

• Imagine creating an advisory board of experts:

• Imagine corporate pension funds, foundations, endowments,insurance companies investing as well

• Imagine 10MM households investing $3,000 each

• Imagine government tax incentives, credit enhancement, etc. (think

Fannie Mae, Freddie Mac!)

• George Demetri, Eric Lander, Bob Langer, Mark Levin, Frank McCormick, LarryNorton, Phil Sharp; Warren Buffett, Bill Gates, Jacob Goldfield, Bob Merton, JimSimons, George Soros, Bill Sharpe

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 20/22

20

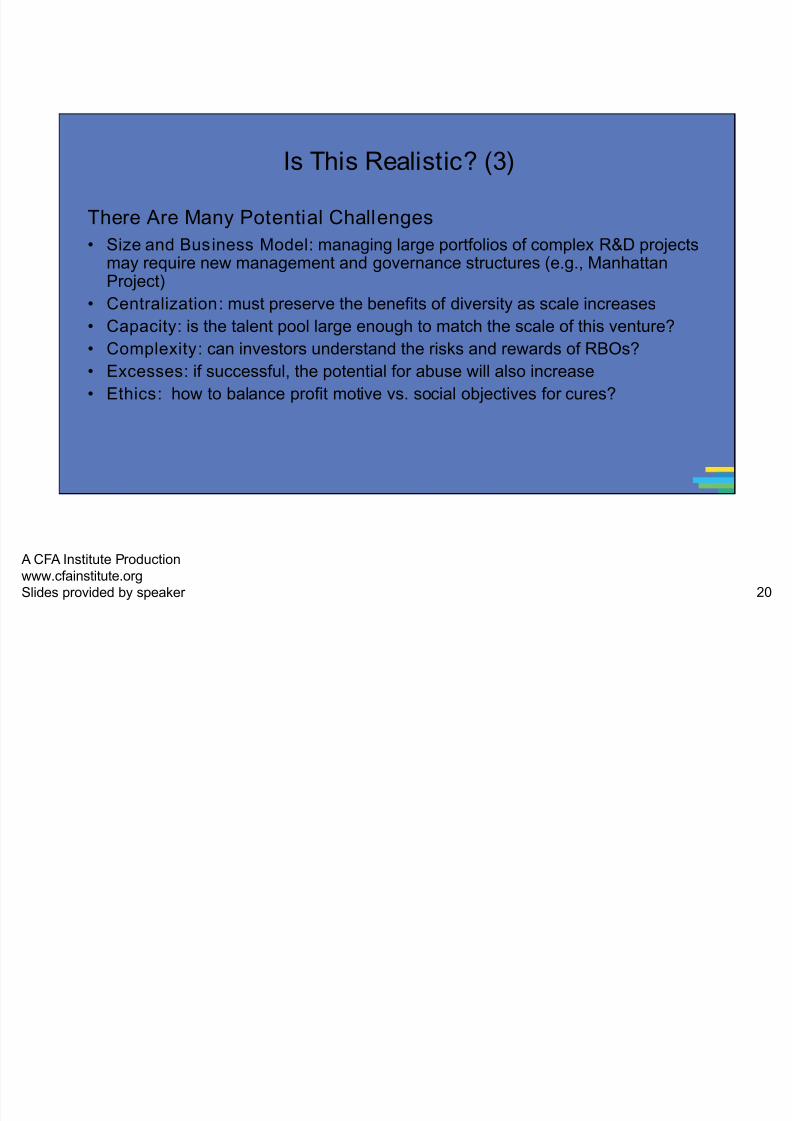

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

There Are Many Potential Challenges• Size and Business Model: managing large portfolios of complex R&D projects

may require new management and governance structures (e.g., ManhattanProject)

• Centralization: must preserve the benefits of diversity as scale increases

• Capacity: is the talent pool large enough to match the scale of this venture?• Complexity: can investors understand the risks and rewards of RBOs?

• Excesses: if successful, the potential for abuse will also increase

• Ethics: how to balance profit motive vs. social objectives for cures?

Is This Realistic? (3)

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 21/22

21

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Next Steps

• Expose each stakeholder group to the tools, challenges, andopportunities of other groups in the biomedical ecosystem

• Clinicians, researchers, biopharma professionals, VCs, insurancecompanies, regulators, investors, financial engineers, patients

• Identify major obstacles to private-sector funding of translationalmedical R&D

• Propose some potential solutions to these obstacles (seehttp://cancerx.mit.edu)

8/11/2019 Lo_1up

http://slidepdf.com/reader/full/lo1up 22/22

22

A CFA Institute Productionwww.cfainstitute.orgSlides provided by speaker

Conclusion

Don’t Declare War OnCancer…Put A Price Tag

On Its Head Instead!

With Sufficient Scale, We Can Do Well By Doing Good• Finance does not always have to be a zero-sum game