Embed Size (px)

Citation preview

LNG Shipping

October 2006

Hauke L. Kite-Powell

Outline

• LNG shipping in context• shipping demand and supply

– trade projections– fleet development– implications for fleet utilization

• trends and risks– charter terms– short term (“spot”) trades– structural changes

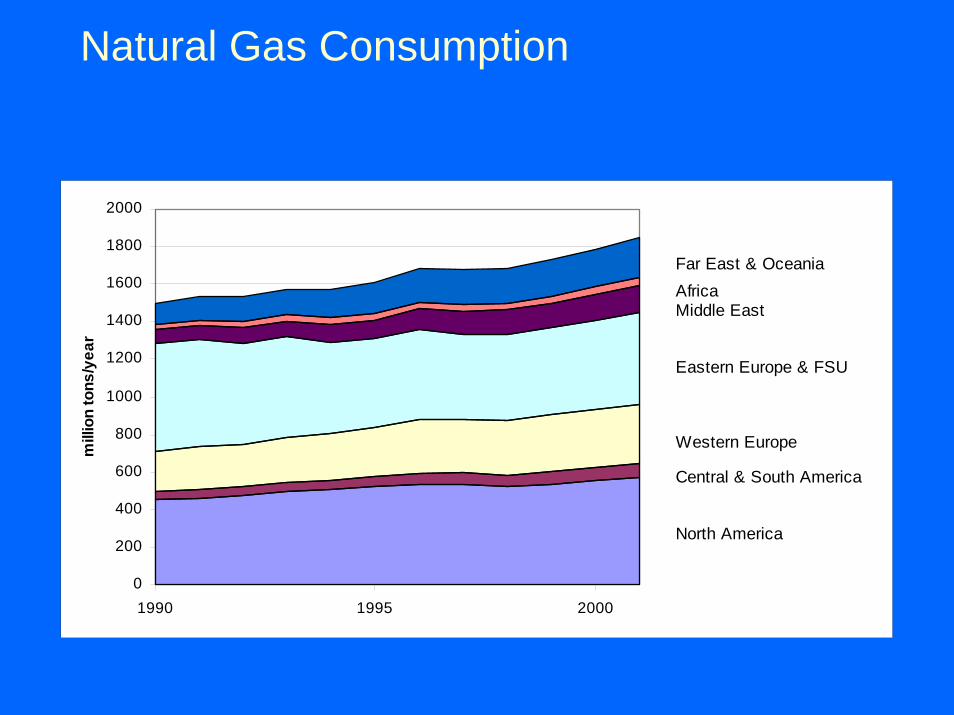

Natural Gas Consumption

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1990 1995 2000

mill

ion

tons

/yea

r

Far East & OceaniaAfricaMiddle East

Eastern Europe & FSU

Western Europe

Central & South America

North America

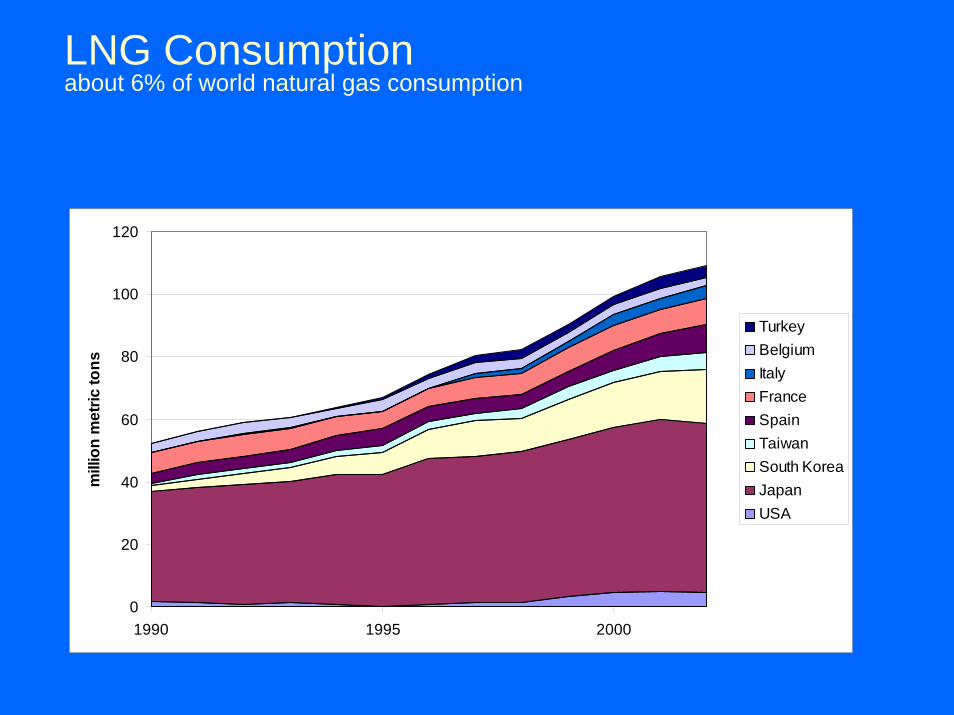

LNG Consumptionabout 6% of world natural gas consumption

0

20

40

60

80

100

120

1990 1995 2000

mill

ion

met

ric to

ns

TurkeyBelgiumItalyFranceSpainTaiwanSouth KoreaJapanUSA

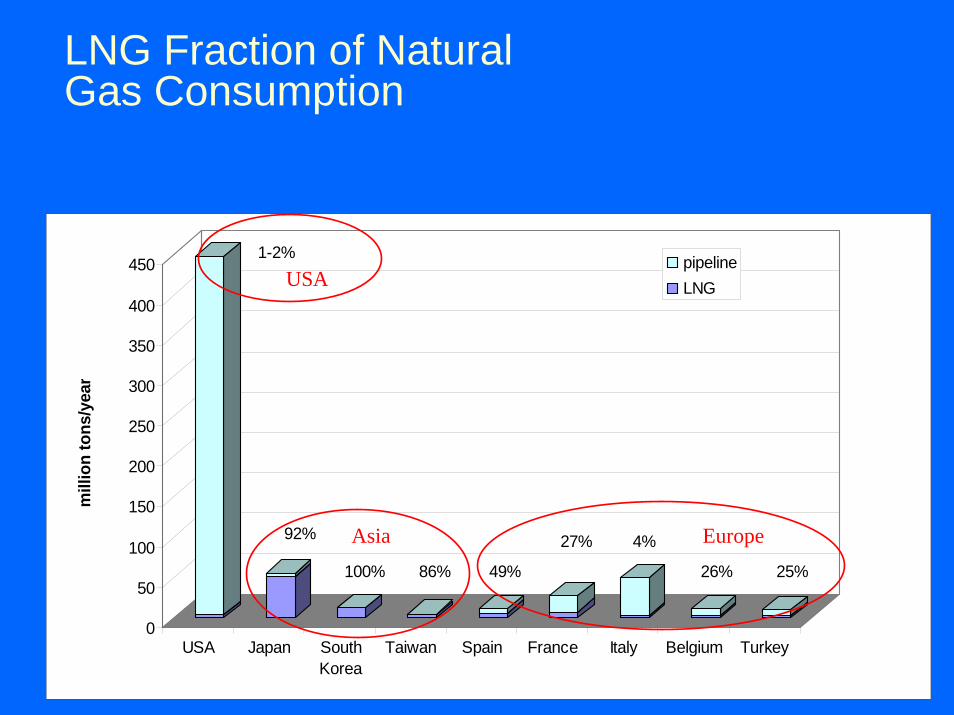

LNG Fraction of Natural Gas Consumption

0

50

100

150

200

250

300

350

400

450

USA Japan SouthKorea

Taiwan Spain France Italy Belgium Turkey

pipelineLNG

mill

ion

tons

/yea

r

1-2%

92%

100% 86% 49%

27% 4%

26% 25%

USA

Asia Europe

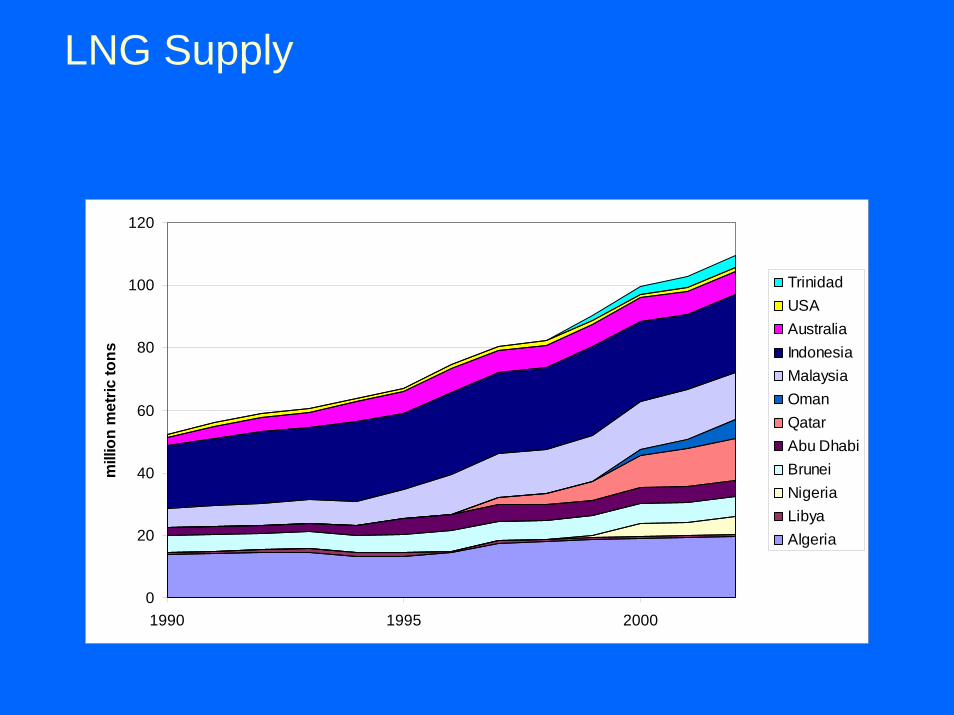

LNG Supply

0

20

40

60

80

100

120

1990 1995 2000

mill

ion

met

ric to

ns

TrinidadUSAAustraliaIndonesiaMalaysiaOmanQatarAbu DhabiBruneiNigeriaLibyaAlgeria

LNG Shipping Demand:Established Trade Routes

• Pacific basin:–Arabian Gulf → Japan, Korea, Taiwan (40%)–Malaysia → Japan, Korea, Taiwan–Indonesia → Japan, Korea, Taiwan (20%)–Australia → Japan (10%)–US (Alaska) → Japan

• Atlantic basin:–Algeria → Europe, US–Nigeria → Italy, Spain, France, Turkey (15%)–Libya → Spain–Trinidad → Spain, US

Map removed due to copyright restrictions.

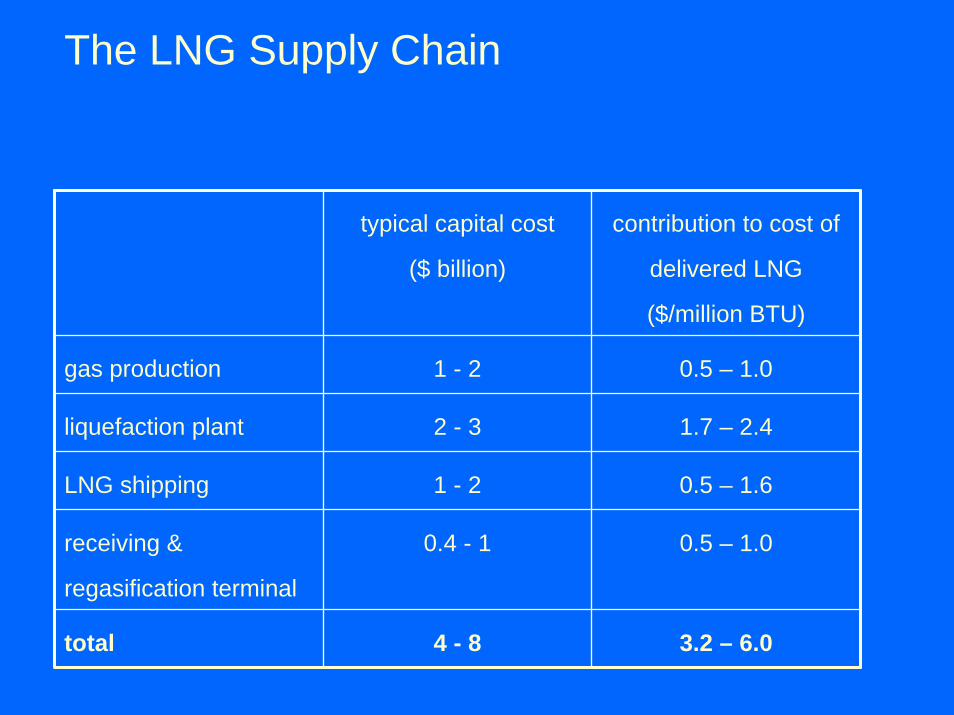

The LNG Supply Chain

typical capital cost

($ billion)

contribution to cost of

delivered LNG

($/million BTU)

gas production 1 - 2 0.5 – 1.0

liquefaction plant 2 - 3 1.7 – 2.4

LNG shipping 1 - 2 0.5 – 1.6

receiving &

regasification terminal

0.4 - 1 0.5 – 1.0

total 4 - 8 3.2 – 6.0

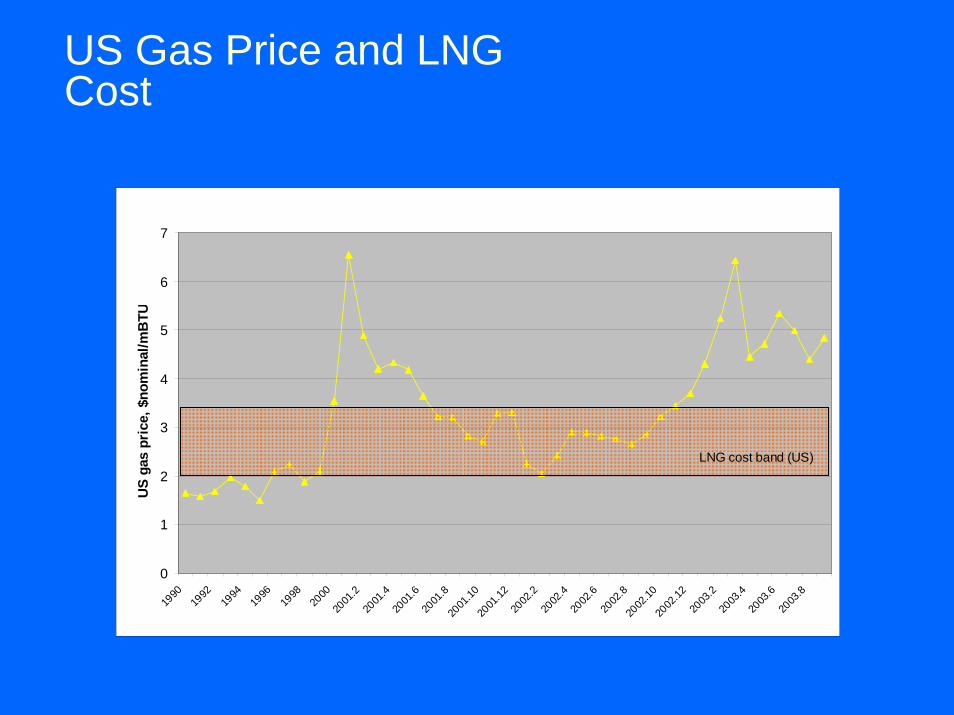

US Gas Price and LNG Cost

0

1

2

3

4

5

6

7

1990

1992

1994

1996

1998

2000

2001

.220

01.4

2001

.620

01.8

2001

.1020

01.12

2002

.220

02.4

2002

.620

02.8

2002

.1020

02.12

2003

.220

03.4

2003

.620

03.8

US

gas

pric

e, $

nom

inal

/mB

TU

LNG cost band (US)

Outline

• LNG shipping in context• shipping demand and supply

– trade projections• demand for LNG & import facilities• LNG supply (liquefaction trains)

– fleet development– implications for fleet utilization

• trends and risks– charter terms– short term (“spot”) trades– structural changes

LNG Demand Growth, 2010

• Asia: 7% annual growth– India and China – new importers; projections revised upward– Taiwan and South Korea– Japan – stated goal of increasing gas fraction– seasonal demand peaks

• United States: 30% annual growth?– gas consumption: 450 mt/year; LNG 6 mt (2003)– import capacity: 20 mt/year (all four facilities open)

• existing terminals plan to expand to 30 mt/year• proposals for 50 mt/y – only a few of these are likely to be built• Gulf Coast, Mexico terminals: strong progress

• Europe: 5% annual growth– import capacity 35 mt/y– may build to 80 mt/year by 2010– UK as import hub? progress on terminal plans

12

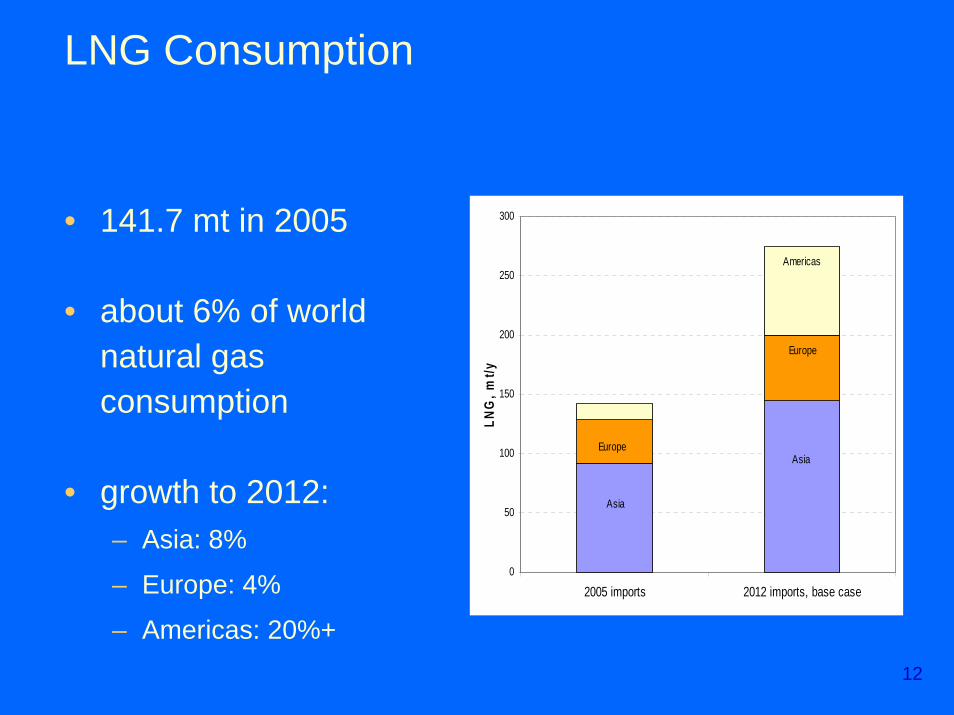

LNG Consumption

• 141.7 mt in 2005

• about 6% of world natural gas consumption

• growth to 2012:– Asia: 8%

– Europe: 4%

– Americas: 20%+

0

50

100

150

200

250

300

2005 imports 2012 imports, base case

LNG

, mt/y

Americas

Europe

Asia

Asia

Europe

13

North American Import Facility Projects – USA (1)

Cabrillo Port Oxnard, CA 6.0 mt/y BHP Billiton 2008

Calhoun LNG TX 6.5-7.5 mt/y Calhoun LNG FERC pending2009 startup

Compass Pass LLC

offshore LA 7.5 mt/y Conoco Phillips pending CG approval

Corpus Christi TX 19.5 mt/y Cheniere Energy Q4 2007constr. OK

Corpus Christi Bay

Corpus Christi, TX

7.5 mt/y Occidental FERC approval 2005

Crown Landing NJ 9.0 mt/y BP 2008EIS OK

Freeport TX 11.5 mt/y Freeport LNG under constr.

Northeast Gateway

Gloucester, MA 6.0 mt/y Excelerate shipboard regas, 2007

Gulf Gateway offshore LA 3.7 mt/y Excelerate shipb. regas, operating

Cameron LNG Hackberry, LA 11.0 mt/y Sempra Energy under constr.2007 startup

Broadwater Long Island Sound

7.5 mt/y TransCanada, Shell

14

North American Import Facility Projects – USA (2)

Main Pass offshore LA 18.7 mt/y Freeport McMoRan

pending approvals

Pearl Crossing offshore LA ? ExxonMobil on hold

Pelican Island Galveston, TX 9.0 mt/y BP no firm plans

Sempra Eng. Port Arthur,TX 11.0 mt/y Sempra EIS OK2009

Port Pelican offshore LA ? ChevronTex on hold

Sabine Pass LA 20-30 mt/y Cheniere Energy final approvals2008 startup

Golden Pass Sabine Pass, TX 15.0 mt/y ExxonMobil, Qatar Petro

2009

Terminal Island Long Beach, CA 7.5 mt/y Mitsubishi, ConocoPhillips

2008

Ventura offshore CA 7.5 mt/y Crystal Energy

Vista del Sol Corpus Christi, TX

7.5 mt/y ExxonMobil 2009

Gulf Landing W.Cameron, LA (offshore)

7.5 mt/y Shell 2008/09MarAd appr.

15

North American Import Facility Projects – non-US

Bear Head Point Tupper, Nova Scotia

7.5-11.0 mt/y Anadarko Petroleum

under constr.; delayed (07)

Canaport St. John, New Brunswick

3.7 mt/y Irving Oil, RepsolYPF

2008under constr.

Gros Cacouna Quebec 3.7 mt/y TransCanada, Petro-Canada

2008

Keltic LNG Goldboro, Nova Scotia

3.7-14.0 mt/y KelticPetrochemical

2007-09

Point Tupper Nova Scotia 3.7 mt/y Statia Terminals

Calypso & High Rock

Bahamas 6 mt/y El Paso, Florida P&L, Tractebel

2008

Altamira Tamaulipas, Gulf Coast

9.7 mt/y Shell, Total, Mitsui

nearing completion

Coronado Islands

Baja California 5.2-10.5 mt/y Chevron 2008approved

Costa Azul Baja California 7.5 mt/y Sempra Energy 2007approved

Manzanillo Colima, Mex 3.7 mt/y Mex. state power co.

2007

16

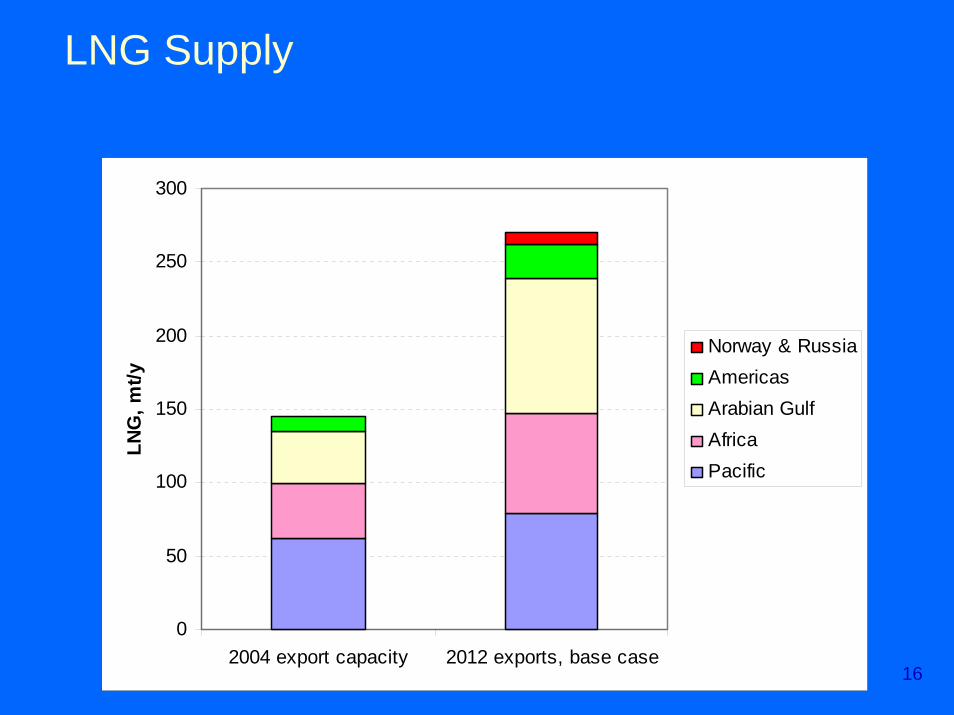

LNG Supply

0

50

100

150

200

250

300

2004 export capacity 2012 exports, base case

LNG

, mt/y

Norway & RussiaAmericasArabian GulfAfricaPacific

17

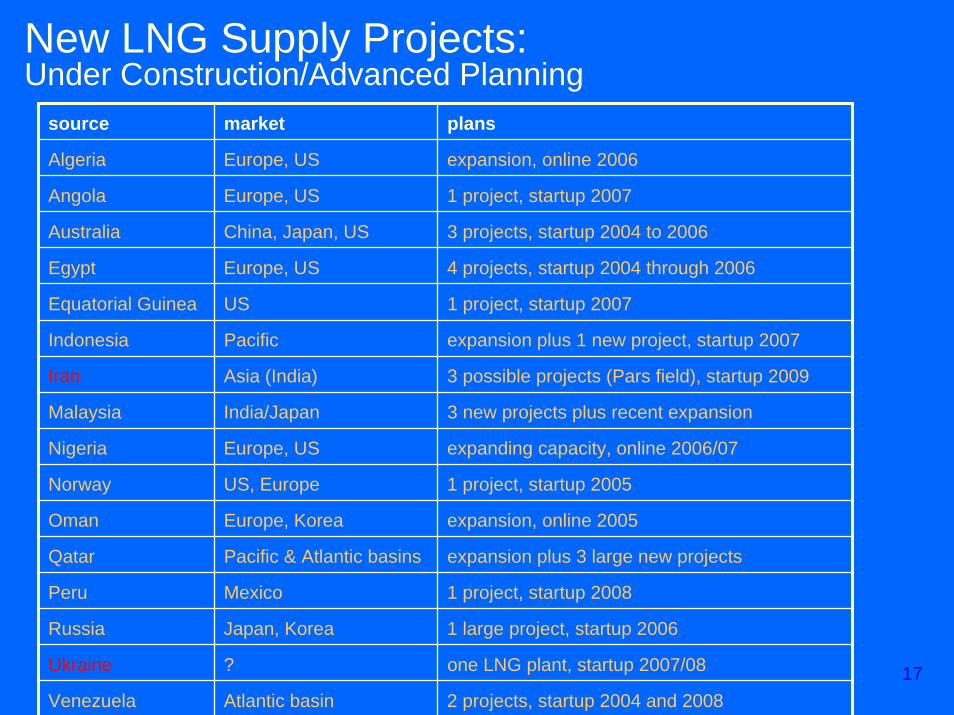

New LNG Supply Projects:Under Construction/Advanced Planning

source market plans

Algeria Europe, US expansion, online 2006

Iran Asia (India) 3 possible projects (Pars field), startup 2009

Angola Europe, US 1 project, startup 2007

Peru Mexico 1 project, startup 2008

Russia Japan, Korea 1 large project, startup 2006

Australia China, Japan, US 3 projects, startup 2004 to 2006

Egypt Europe, US 4 projects, startup 2004 through 2006

Equatorial Guinea US 1 project, startup 2007

Indonesia Pacific expansion plus 1 new project, startup 2007

Malaysia India/Japan 3 new projects plus recent expansion

Nigeria Europe, US expanding capacity, online 2006/07

Norway US, Europe 1 project, startup 2005

Oman Europe, Korea expansion, online 2005

Qatar Pacific & Atlantic basins expansion plus 3 large new projects

Ukraine ? one LNG plant, startup 2007/08

Venezuela Atlantic basin 2 projects, startup 2004 and 2008

18

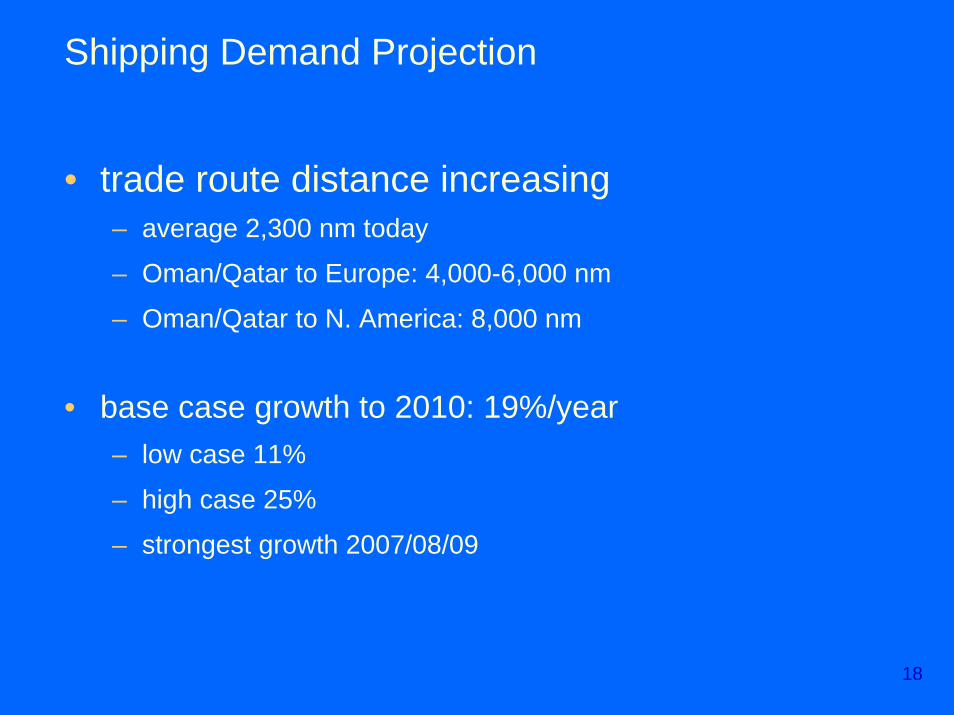

Shipping Demand Projection

• trade route distance increasing– average 2,300 nm today

– Oman/Qatar to Europe: 4,000-6,000 nm

– Oman/Qatar to N. America: 8,000 nm

• base case growth to 2010: 19%/year– low case 11%

– high case 25%

– strongest growth 2007/08/09

Outline

• LNG shipping in context• shipping demand and supply

– trade projections– fleet development– implications for fleet utilization

• trends and risks– charter terms– short term (“spot”) trades– structural changes

LNG Tank Designs:Spherical Tank (Moss)

Photo removed due to copyright restrictions.

LNG Tank Designs:Prismatic Membrane Tank

Photo removed due to copyright restrictions.

22

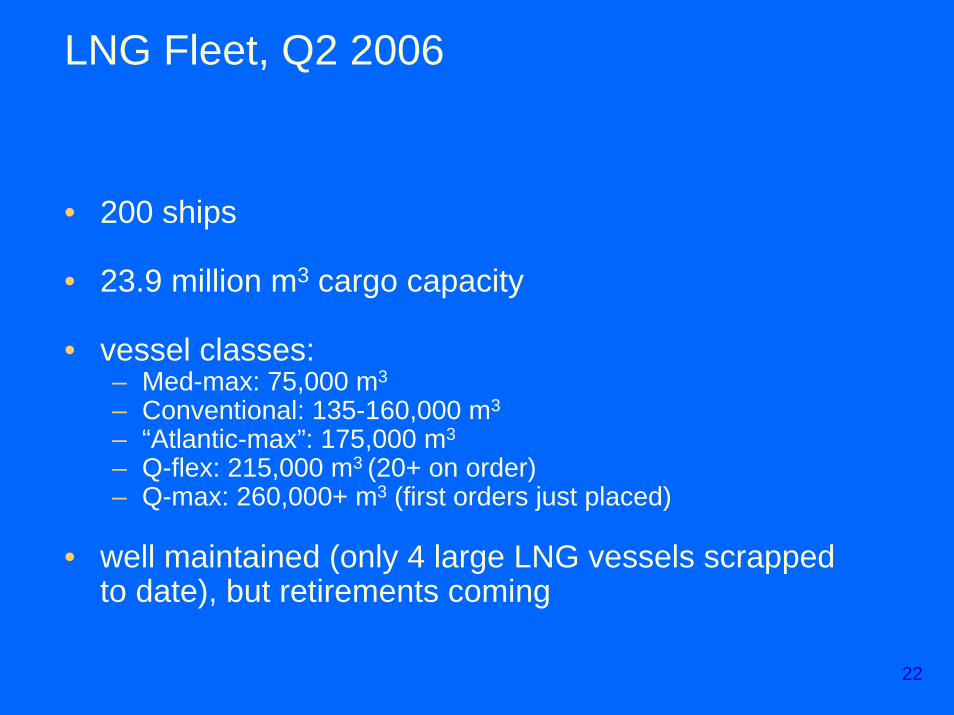

LNG Fleet, Q2 2006

• 200 ships

• 23.9 million m3 cargo capacity

• vessel classes: – Med-max: 75,000 m3

– Conventional: 135-160,000 m3

– “Atlantic-max”: 175,000 m3

– Q-flex: 215,000 m3 (20+ on order) – Q-max: 260,000+ m3 (first orders just placed)

• well maintained (only 4 large LNG vessels scrapped to date), but retirements coming

23

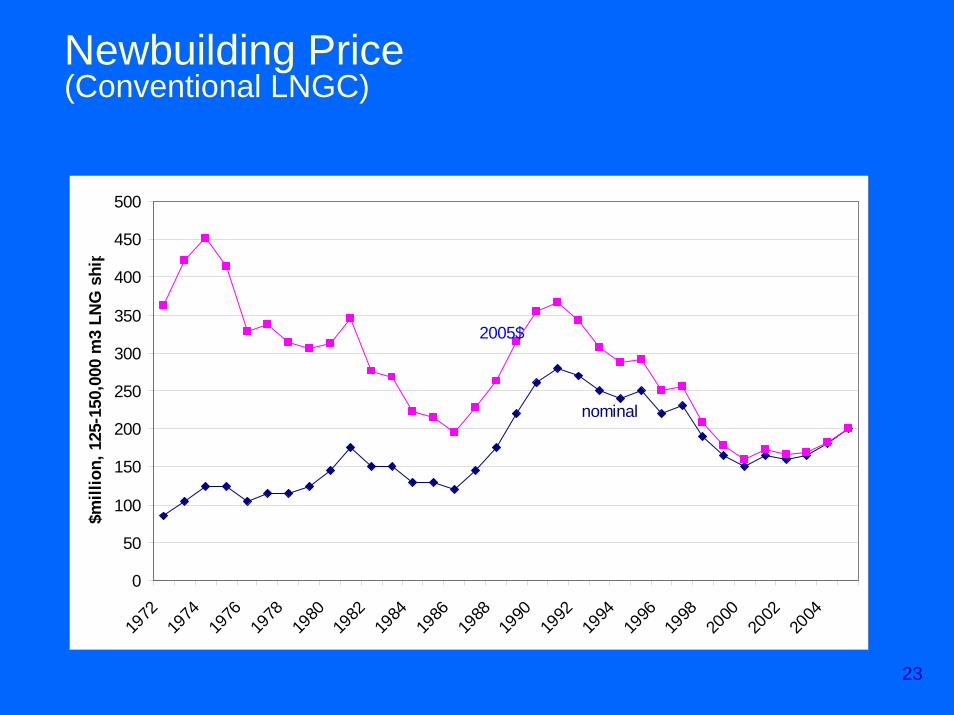

Newbuilding Price(Conventional LNGC)

0

50

100

150

200

250

300

350

400

450

500

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

$mill

ion,

125

-150

,000

m3

LNG

shi

p

nominal

2005$

24

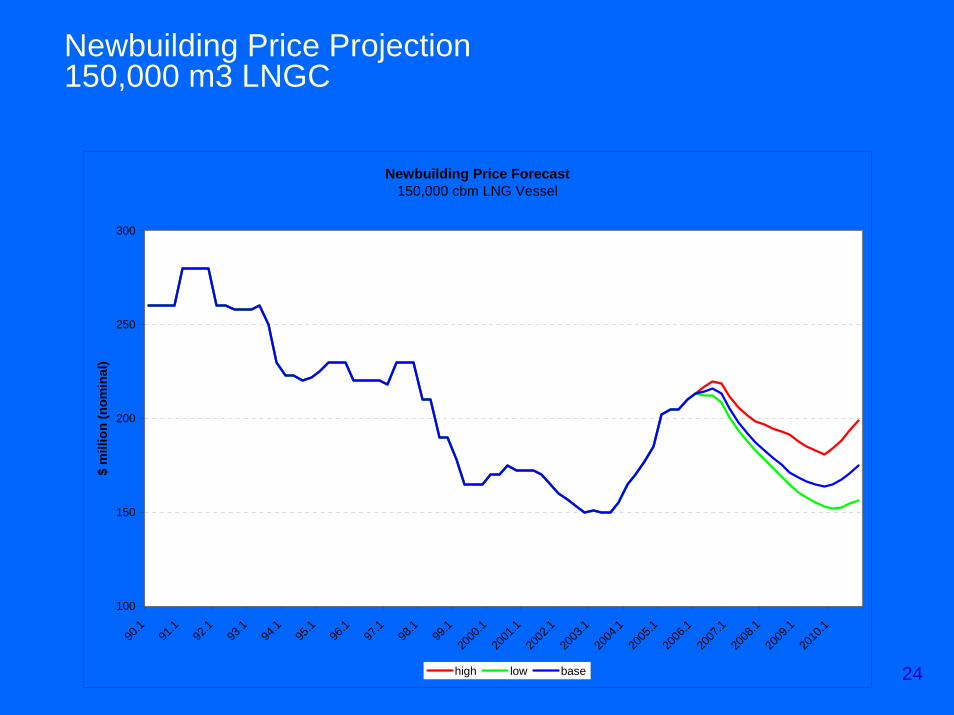

Newbuilding Price Projection150,000 m3 LNGC

Newbuilding Price Forecast 150,000 cbm LNG Vessel

100

150

200

250

300

90.1

91.1

92.1

93.1

94.1

95.1

96.1

97.1

98.1

99.1

2000

.120

01.1

2002

.120

03.1

2004

.120

05.1

2006

.120

07.1

2008

.120

09.1

2010

.1

$ m

illio

n (n

omin

al)

high low base

25

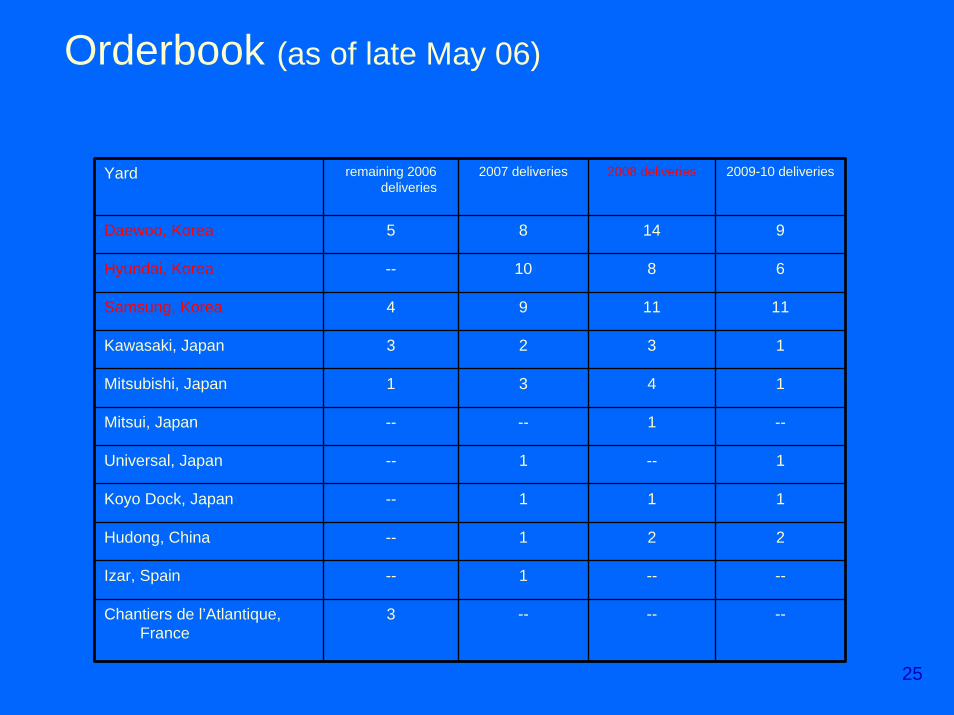

Orderbook (as of late May 06)

Yard remaining 2006 deliveries

2007 deliveries 2008 deliveries 2009-10 deliveries

Daewoo, Korea 5 8 14 9

Hyundai, Korea -- 10 8 6

Samsung, Korea 4 9 11 11

Kawasaki, Japan 3 2 3 1

Mitsubishi, Japan 1 3 4 1

Mitsui, Japan -- -- 1 --

Universal, Japan -- 1 -- 1

Koyo Dock, Japan -- 1 1 1

Hudong, China -- 1 2 2

Izar, Spain -- 1 -- --

Chantiers de l’Atlantique, France

3 -- -- --

26

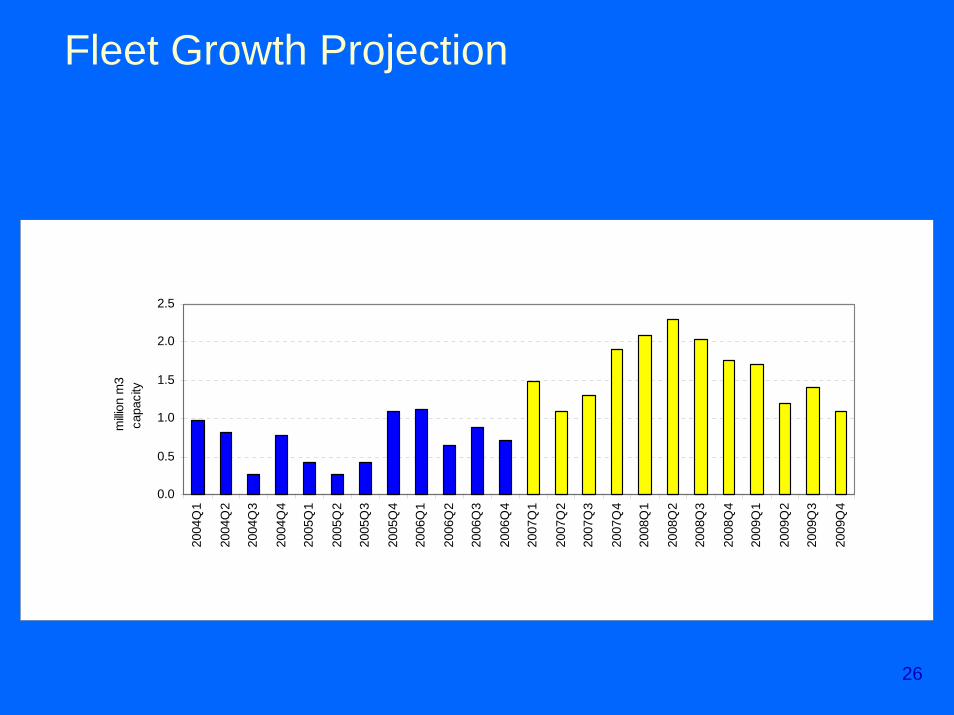

Fleet Growth Projection

0.0

0.5

1.0

1.5

2.0

2.5

2004

Q1

2004

Q2

2004

Q3

2004

Q4

2005

Q1

2005

Q2

2005

Q3

2005

Q4

2006

Q1

2006

Q2

2006

Q3

2006

Q4

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

milli

on m

3ca

paci

ty

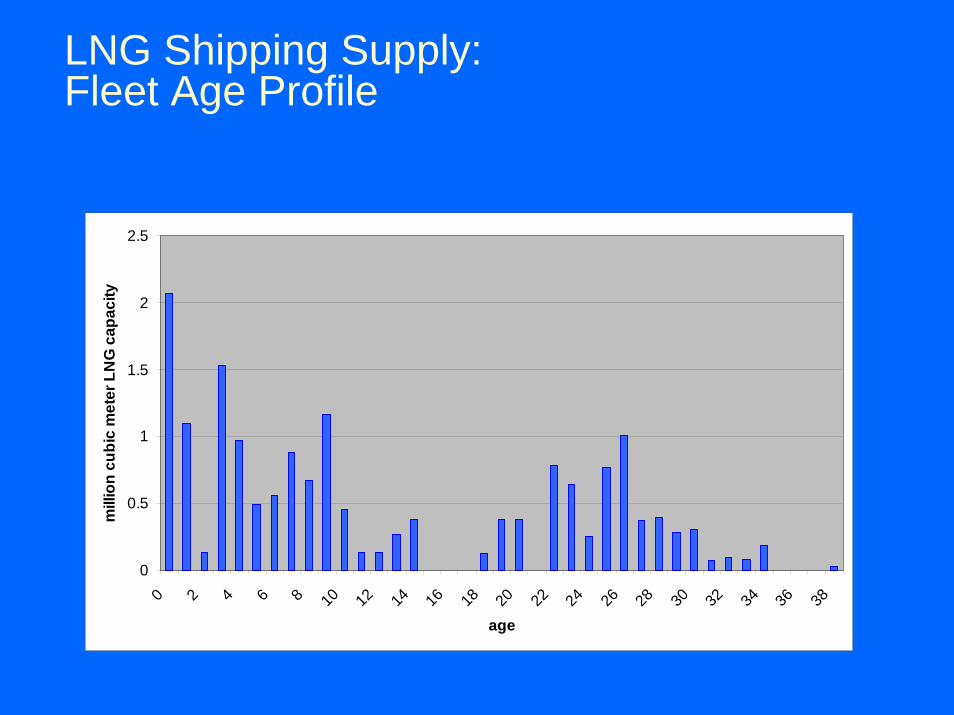

LNG Shipping Supply:Fleet Age Profile

0

0.5

1

1.5

2

2.5

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38

age

mill

ion

cubi

c m

eter

LN

G c

apac

ity

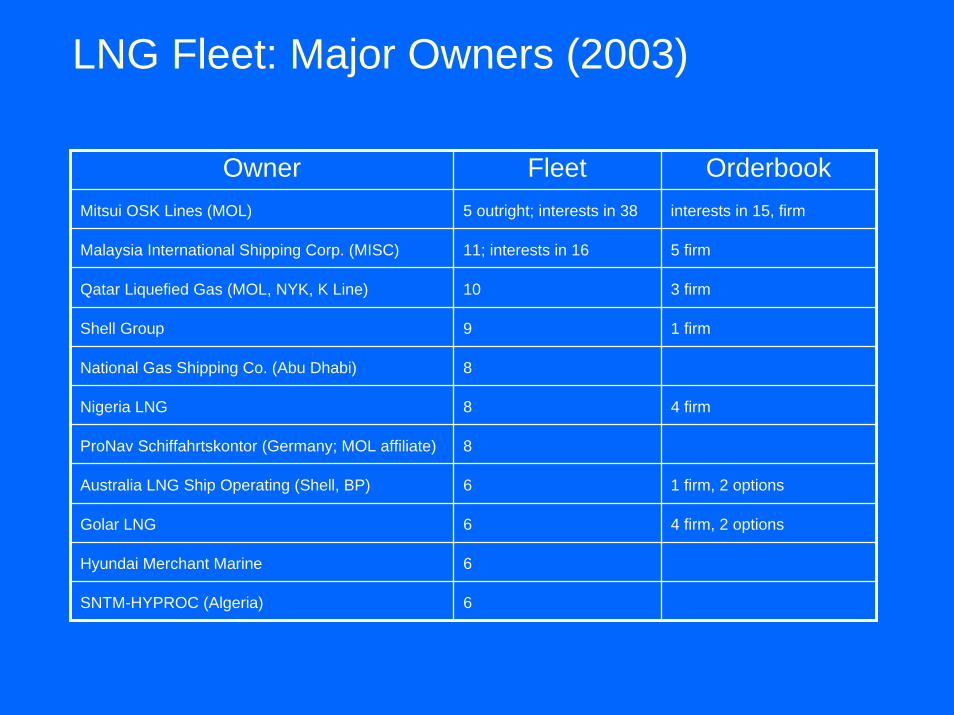

LNG Fleet: Major Owners (2003)

Owner Fleet OrderbookMitsui OSK Lines (MOL) 5 outright; interests in 38

11; interests in 16

10

9

8

8

8

6

6

6

SNTM-HYPROC (Algeria) 6

Malaysia International Shipping Corp. (MISC) 5 firm

interests in 15, firm

Qatar Liquefied Gas (MOL, NYK, K Line) 3 firm

Shell Group 1 firm

National Gas Shipping Co. (Abu Dhabi)

Nigeria LNG 4 firm

ProNav Schiffahrtskontor (Germany; MOL affiliate)

Australia LNG Ship Operating (Shell, BP) 1 firm, 2 options

Golar LNG 4 firm, 2 options

Hyundai Merchant Marine

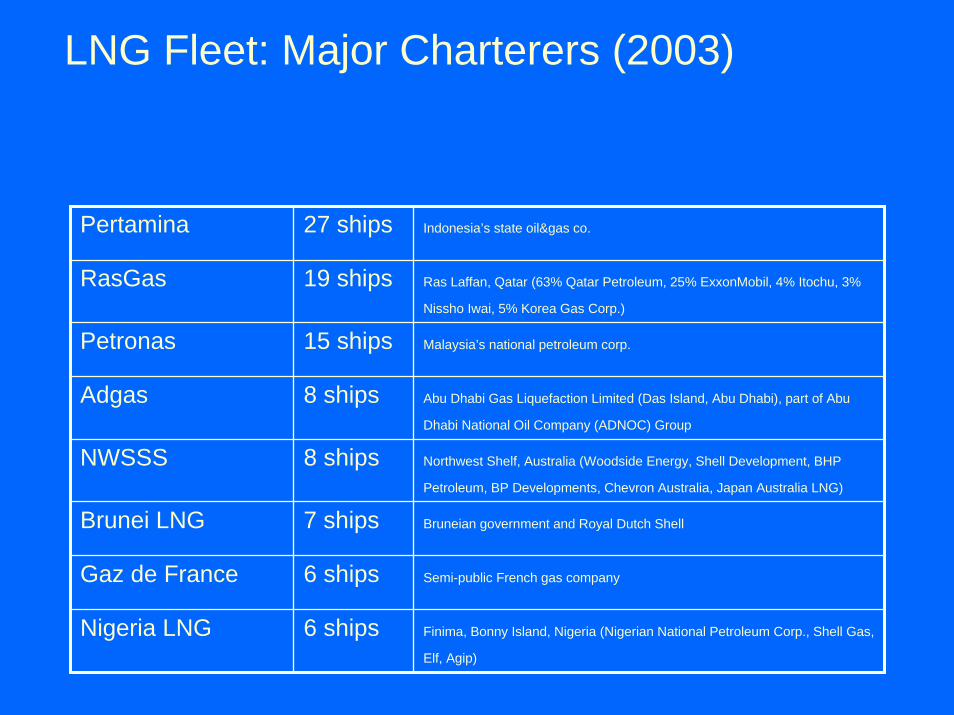

LNG Fleet: Major Charterers (2003)

Pertamina 27 ships Indonesia’s state oil&gas co.

RasGas 19 ships Ras Laffan, Qatar (63% Qatar Petroleum, 25% ExxonMobil, 4% Itochu, 3%

Nissho Iwai, 5% Korea Gas Corp.)

Petronas 15 ships Malaysia’s national petroleum corp.

Adgas 8 ships Abu Dhabi Gas Liquefaction Limited (Das Island, Abu Dhabi), part of Abu

Dhabi National Oil Company (ADNOC) Group

NWSSS 8 ships Northwest Shelf, Australia (Woodside Energy, Shell Development, BHP

Petroleum, BP Developments, Chevron Australia, Japan Australia LNG)

Brunei LNG 7 ships Bruneian government and Royal Dutch Shell

Gaz de France 6 ships Semi-public French gas company

Nigeria LNG 6 ships Finima, Bonny Island, Nigeria (Nigerian National Petroleum Corp., Shell Gas,

Elf, Agip)

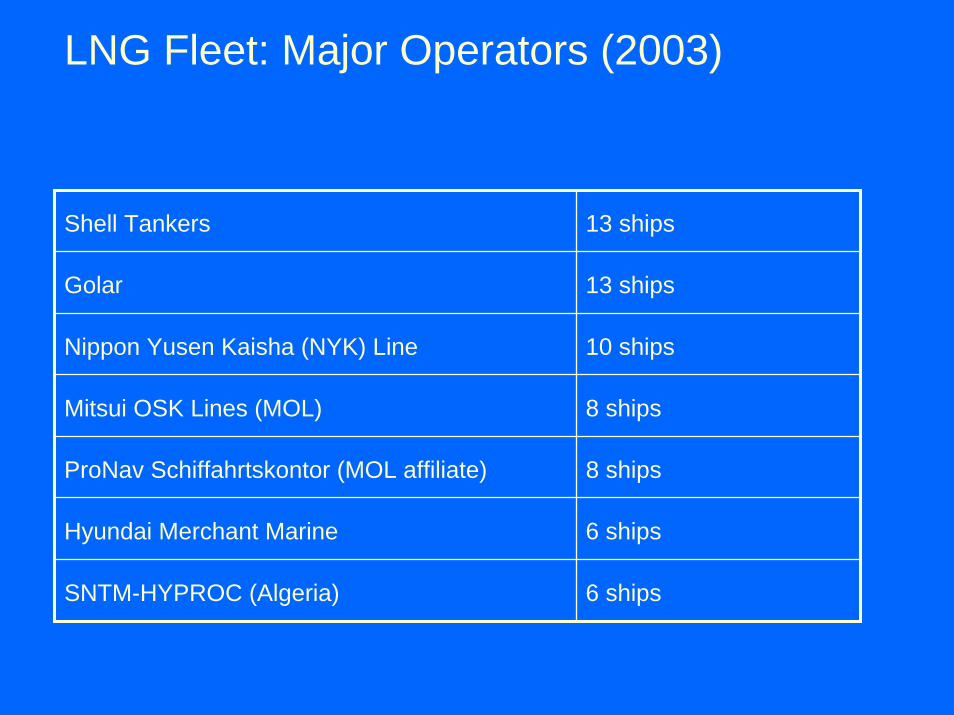

LNG Fleet: Major Operators (2003)

Shell Tankers 13 ships

Golar 13 ships

Nippon Yusen Kaisha (NYK) Line 10 ships

Mitsui OSK Lines (MOL) 8 ships

ProNav Schiffahrtskontor (MOL affiliate) 8 ships

Hyundai Merchant Marine 6 ships

SNTM-HYPROC (Algeria) 6 ships

Outline

• LNG shipping in context• shipping demand and supply

– trade projections– fleet development– implications for fleet utilization

• trends and risks– charter terms– short term (“spot”) trades– structural changes

32

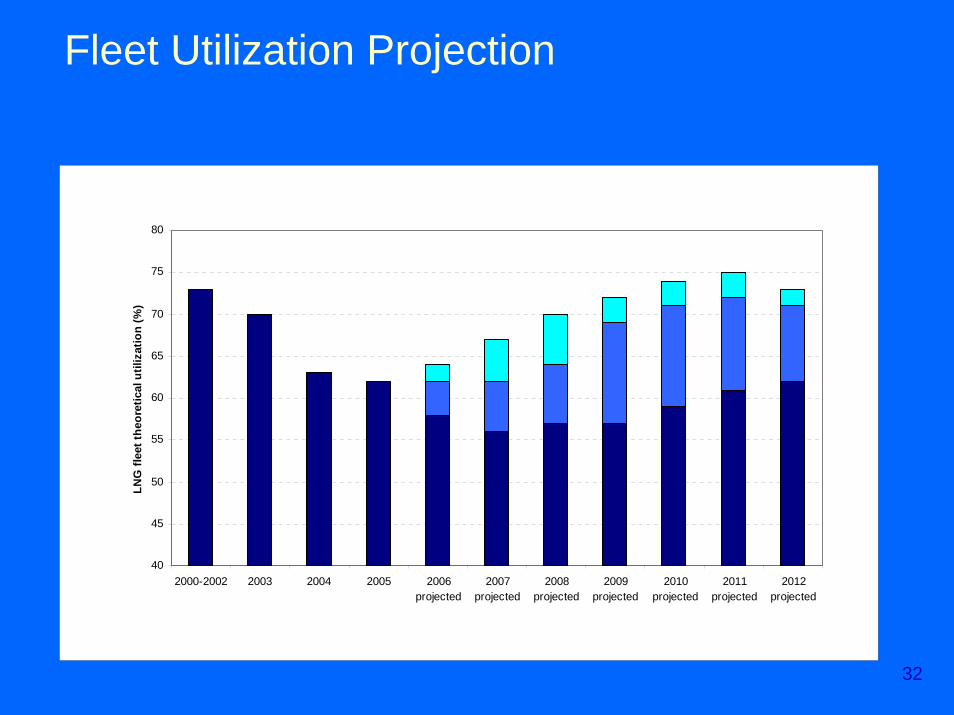

Fleet Utilization Projection

40

45

50

55

60

65

70

75

80

2000-2002 2003 2004 2005 2006projected

2007projected

2008projected

2009projected

2010projected

2011projected

2012projected

LNG

flee

t the

oret

ical

util

izat

ion

(%)

33

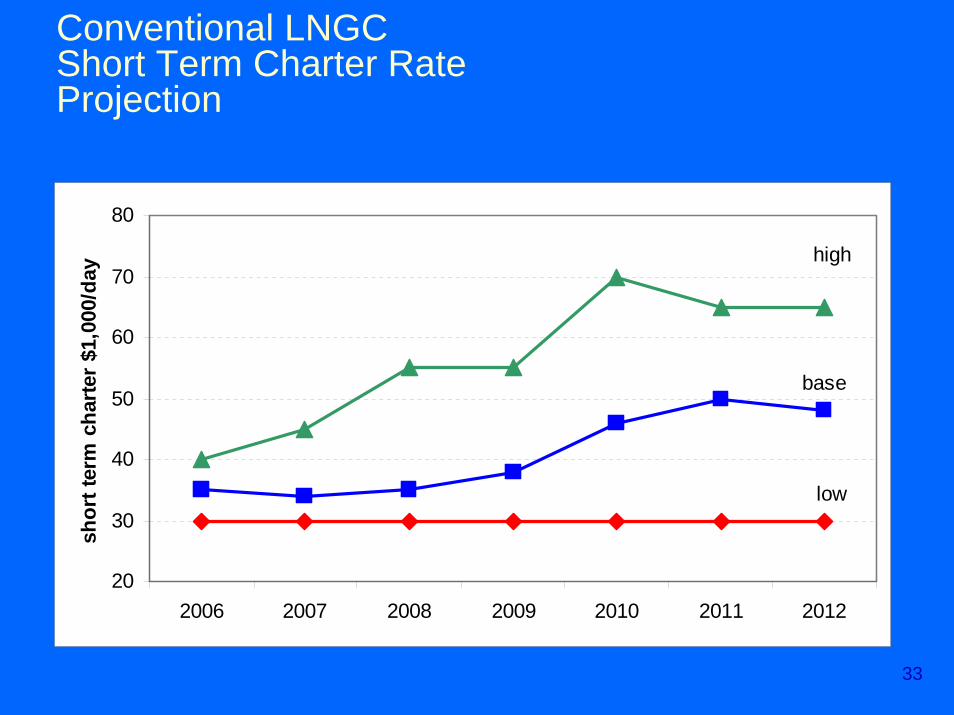

Conventional LNGC Short Term Charter Rate Projection

20

30

40

50

60

70

80

2006 2007 2008 2009 2010 2011 2012

shor

t ter

m c

harte

r $1

,000

/day

low

high

base

Outline

• LNG shipping in context• shipping demand and supply

– trade projections– fleet development– implications for fleet utilization

• trends and risks– charter terms– short term (“spot”) trades– structural changes

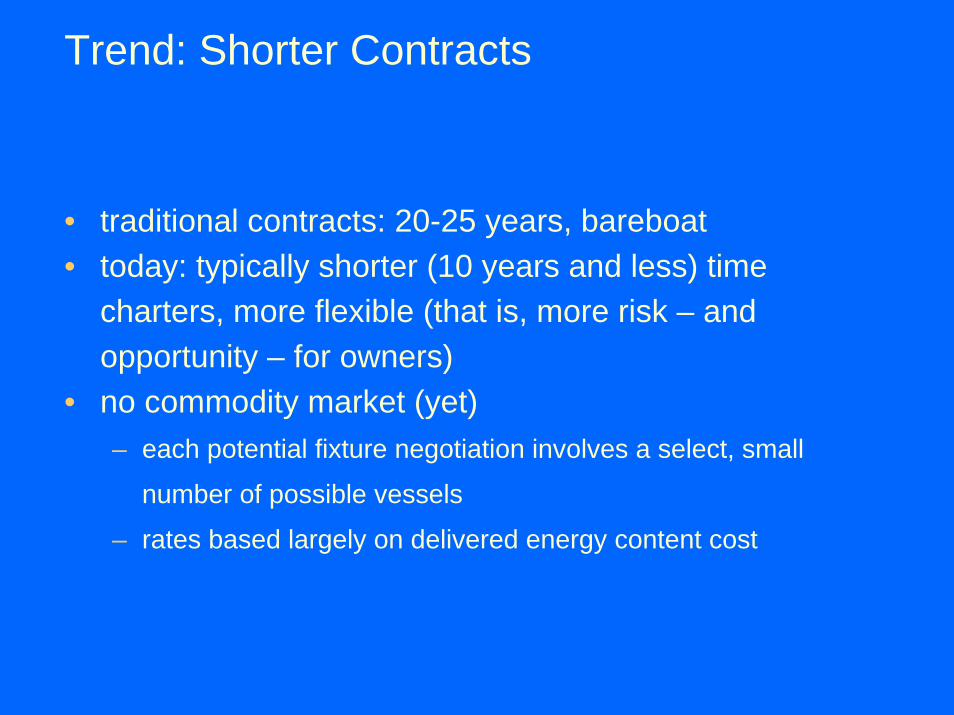

Trend: Shorter Contracts

• traditional contracts: 20-25 years, bareboat• today: typically shorter (10 years and less) time

charters, more flexible (that is, more risk – and opportunity – for owners)

• no commodity market (yet)– each potential fixture negotiation involves a select, small

number of possible vessels

– rates based largely on delivered energy content cost

Outline

• LNG shipping in context• shipping demand and supply

– trade projections– fleet development– implications for fleet utilization

• trends and risks– charter terms– short term (“spot”) trades– structural changes

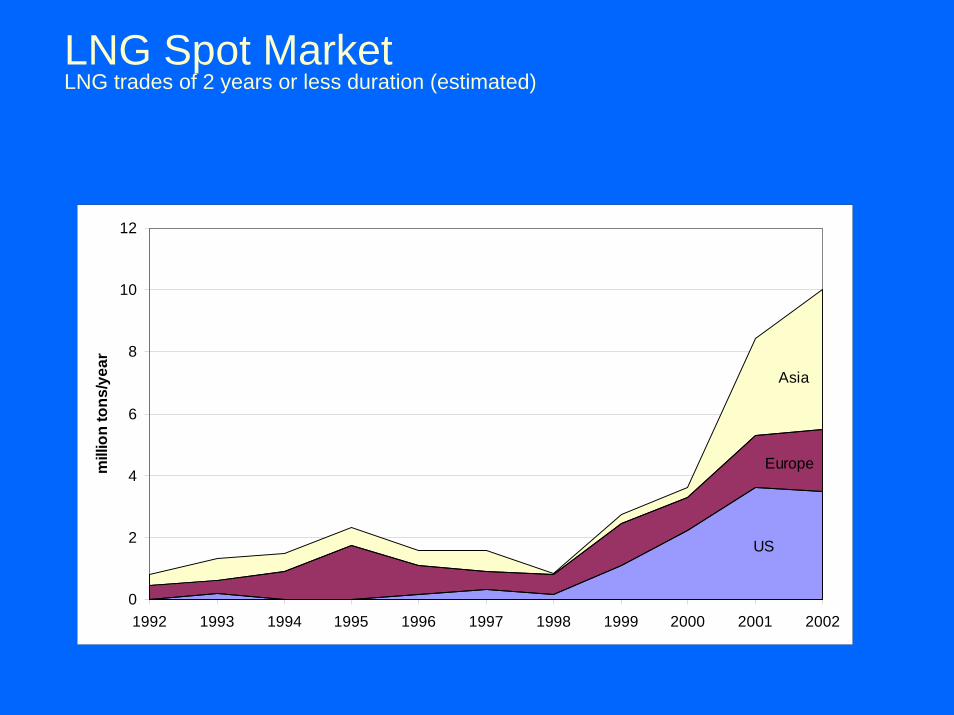

“Spot” Market Growing

• excess supply capacity • underutilized fleet• demand fluctuations and import terminal

capacity– Atlantic market (US)– Pacific market (Korea, Japan, India)

• “compartmentalized”

LNG Spot MarketLNG trades of 2 years or less duration (estimated)

0

2

4

6

8

10

12

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

mill

ion

tons

/yea

r

Asia

Europe

US

“Spot” Trade Participation

• 75% of short term fixtures have been vessels within their own contract trades (particularly on Pacific routes)

• most “spot” voyages to date on Atlantic routes, “Atlantic” owners– Africa, Arabia to Europe, US– Trinidad to US, Europe

• Asian routes & vessels becoming more engaged (MISC)

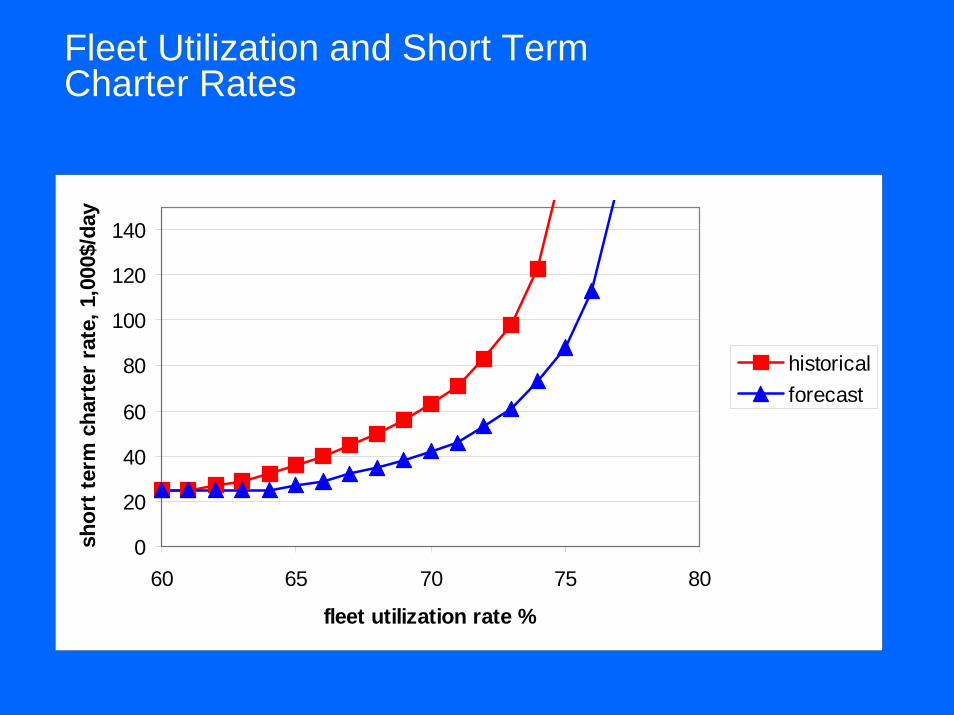

Fleet Utilization and Short Term Charter Rates

0

20

40

60

80

100

120

140

60 65 70 75 80

fleet utilization rate %

shor

t ter

m c

hart

er r

ate,

1,0

00$/

day

historicalforecast

Outline

• LNG shipping in context• shipping demand and supply

– trade projections– fleet development– implications for fleet utilization

• trends and risks– charter terms– short term (“spot”) trades– structural changes

Changing Shipping Field

• Traditional Asian players (Japan, Malaysia) positioning for Atlantic market, spot trade role

• Acquisitions– Teekay (Tapias)– Golar (stake in K Line)

• New players – Greek owners– Anangel– Tsakos Energy Navigation– Dynacom– others

LNG Shipping Trends

• More choices in power plants– Dual fuel diesel-electric

– Traditional slow-speed diesel w/reliquefaction

– Gas turbine?

• Greater range of vessel capacity and regas options

• More flexible/efficient fleet utilization

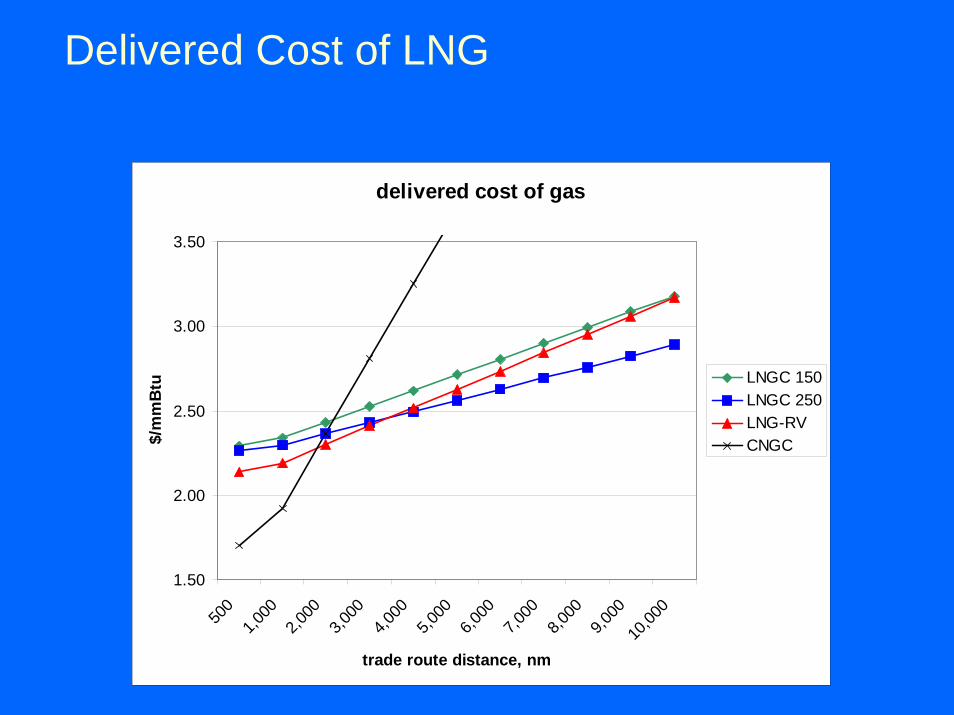

Delivered Cost of LNG

delivered cost of gas

1.50

2.00

2.50

3.00

3.50

500

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,00

0

trade route distance, nm

$/m

mB

tu LNGC 150LNGC 250LNG-RVCNGC

Summary:LNG Shipping Prospects

Opportunities:

• for the long run, trade is set to grow; ships are needed

• spot market growth – has been lucrative

• fleet utilization has been high

• newbuilding prices are low

Risks:

• catastrophic accident could derail (US) terminal plans

• project delays can slow trade growth

• strong fleet growth --utilization rates headed down short-term

• risk shifting to owners (contract patterns)

• technological change

Summary

• LNG trade volume to grow by 80-130% to 2010– import facilities?

• LNG “spot” market has softened; rebound not likely until 2006/07

• ordering is accelerating; 2008 slots filling fast; newbuild prices firming up

• new entrants: acquisitions, speculative ordering• shift in time charters and growing spot market are

pushing LNG toward the “standard” bulk shipping market model – within limits