Embed Size (px)

Citation preview

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

LNG in Russia: A Catalyst for

Change?

James Henderson

OX

FO

RD

IN

ST

ITU

TE

FO

R E

NE

RG

Y S

TU

DIE

S N

atu

ral G

as

Re

se

arc

h P

rog

ram

me

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

• Eight LNG projects have been proposed in Russia, with a total potential

capacity of over 100mtpa

• However, only one is producing while one is under construction

• The outlook for the remainder is uncertain at best

Russia’s LNG Projects – A Varied Set of Outcomes

Baltic LNG

- Gazprom

Pechora LNG –

Rosneft / Alltech

Yamal LNG

- Novatek

Gydan LNG

- Novatek

Far East LNG –

Rosneft / ExxonMobil

Sakhalin 2

- Gazprom

Vladivostok LNG

- Gazprom

Shtokman –

Gazprom & partners

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

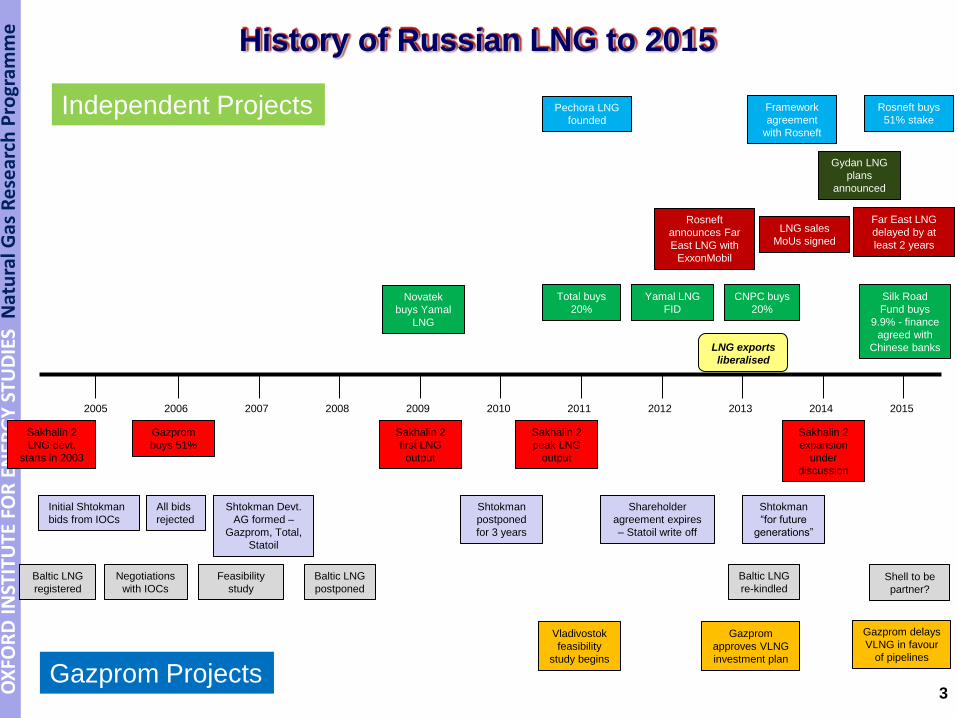

History of Russian LNG to 2015

3

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Initial Shtokman

bids from IOCs

All bids

rejected

Shtokman Devt.

AG formed –

Gazprom, Total,

Statoil

Shareholder

agreement expires

– Statoil write off

Shtokman

postponed

for 3 years

Shtokman

“for future

generations”

Baltic LNG

registered

Negotiations

with IOCs

Feasibility

study

Baltic LNG

postponed Shell to be

partner?

Baltic LNG

re-kindled

Vladivostok

feasibility

study begins

Gazprom

approves VLNG

investment plan

Gazprom delays

VLNG in favour

of pipelines

Gazprom

buys 51%

Sakhalin 2

first LNG

output

Sakhalin 2

peak LNG

output

Sakhalin 2

expansion

under

discussion

Novatek

buys Yamal

LNG

Total buys

20%

Yamal LNG

FID

CNPC buys

20%

Silk Road

Fund buys

9.9% - finance

agreed with

Chinese banks

Sakhalin 2

LNG devt.

starts in 2003

Gazprom Projects

Rosneft

announces Far

East LNG with

ExxonMobil

Far East LNG

delayed by at

least 2 years

LNG sales

MoUs signed

LNG exports

liberalised

Independent Projects

Gydan LNG

plans

announced

Pechora LNG

founded

Framework

agreement

with Rosneft

Rosneft buys

51% stake

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

The future for Russian LNG

4

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Baltic LNG

scheduled

for start-up

Sakhalin 2

expansion

launched?

Project

finance

completed

Gazprom Projects

Far East LNG

onstream?

Independent Projects

Gydan LNG

FID planned

Pechora LNG awaits inclusion on

LNG export list

Train 1

first LNG

Sakhalin 2

expansion

FID planned

Train 2

first LNG Train 3

first LNG

Construction

starts?

First LNG

output?

Debate over pipeline

access on Sakhalin

Assess impact

of sanctions on

South

Kirinskoye

Discussions

with Shell on

Baltic

partnership

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

• Plans for Russian to export LNG have also been delayed due to sanctions

and financing problems

• Gazprom has essentially deferred all its LNG projects in the East and re-

focussed on its pipeline plans

• Baltic LNG remains a “live” project in the west, although the 2020 planned

start-up seems unrealistic

• Competition has emerged from Novatek and Rosneft, but the latter has now

deferred its Far East LNG scheme well into the 2020s

Russia’s LNG plans look much less positive than even 12

months ago

0

10

20

30

40

50

60

70

80

2015 2020 2025 2030

mtp

a

Sakhalin 2 Yamal LNG Baltic LNG

Sakhalin 2 Expansion Vladivostok LNG Far East LNG

Arctic LNG Pechora LNG Shtokman

Estimate of Russian LNG output

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

Key Themes in Russian LNG Debate

6

Gazprom

Novatek Rosneft

Russian LNG

Business

Competitive

Position

Strategic

Priorities

Sanctions

Risk

Gas Supply

Customer

Support

Foreign

Partners

Project

Economics

Government

Support

Financing

Capability

Operational

Capability

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

Vladivostok LNG a casualty of China negotiations

7

Gazprom attempted to replicate Rosneft’s ESPO strategy

Liquefaction at Vladivostok was always a high cost alternative

Little interest from buyers or partners who were unclear about

source of gas or long term economics

Could it re-emerge as a plan in late 2020s in Sakhalin 3

development occurs?

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

Can a rational solution be found on Sakhalin?

Could sanctions on South Kirinskoye and Rosneft’s financial difficulties

provide a catalyst for resolution of Sakhalin issues?

Expansion of Sakhalin 2 is clearly Russia’s most logical LNG development

Map of Sakhalin oil and gas fields and infrastructure

8

Sakhalin 1

Sakhalin 1

Sakhalin 2

Sakhalin 2 Kirinsky fields

(Sakhalin 3)

Possible

locations for Far

East LNG plant

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

• Low gas price in NW Russia can boost economics of Baltic LNG

• However, key will be project cost – current total cost estimate of $18

billion would lead to a very high tolling fee

• A reasonable liquefaction cost could allow Baltic LNG to compete with US

LNG on a full cost basis

• Foreign partner needed to bring liquefaction expertise?

• Is there a big enough market for a full 10mt project?

Gazprom’s Baltic LNG scheme could be competitive if

costs can be controlled

Possible cost of supply from Baltic LNG

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Baltic (Low) Baltic (High) US LNG

US$

/mm

btu

Gas Input Liquefaction Transport Re-gas

Liquefaction Fee

$4-6/mmbtu

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

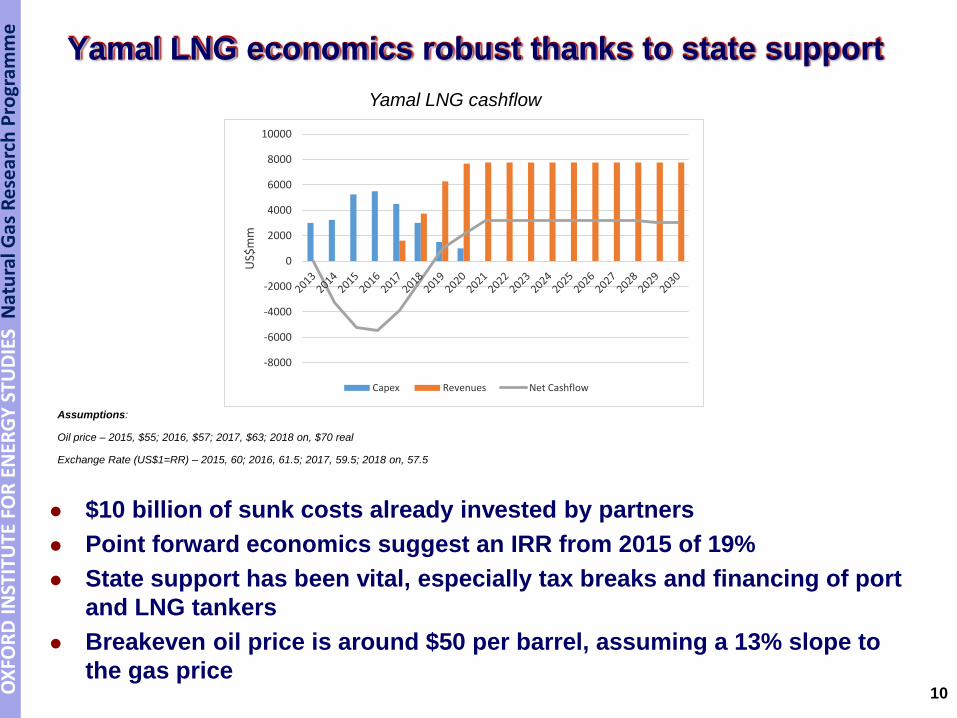

Yamal LNG economics robust thanks to state support

$10 billion of sunk costs already invested by partners

Point forward economics suggest an IRR from 2015 of 19%

State support has been vital, especially tax breaks and financing of port

and LNG tankers

Breakeven oil price is around $50 per barrel, assuming a 13% slope to

the gas price

Yamal LNG cashflow

10

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

US$

mm

Capex Revenues Net Cashflow

Oil price – 2015, $55; 2016, $57; 2017, $63; 2018 on, $70 real

Exchange Rate (US$1=RR) – 2015, 60; 2016, 61.5; 2017, 59.5; 2018 on, 57.5

Assumptions:

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

A new project (e.g. Gydan LNG) would not work at

current prices

Assumes same costs and production as Yamal LNG

Capex assumed to start in 2018, production in 2022

Implied IRR from 2015 is 8%, so does not recover cost of capital

Breakeven long-term oil price is $75-80 per barrel

Will Novatek take FID in 2016? A delay would seem likely.

Gydan LNG cashflow

11

Oil price – 2015, $55; 2016, $57; 2017, $63; 2018 on, $70 real

Exchange Rate (US$1=RR) – 2015, 60; 2016, 61.5; 2017, 59.5; 2018 on, 57.5

Assumptions:

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

US$

mm

Capex Revenues Net Cashflow

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

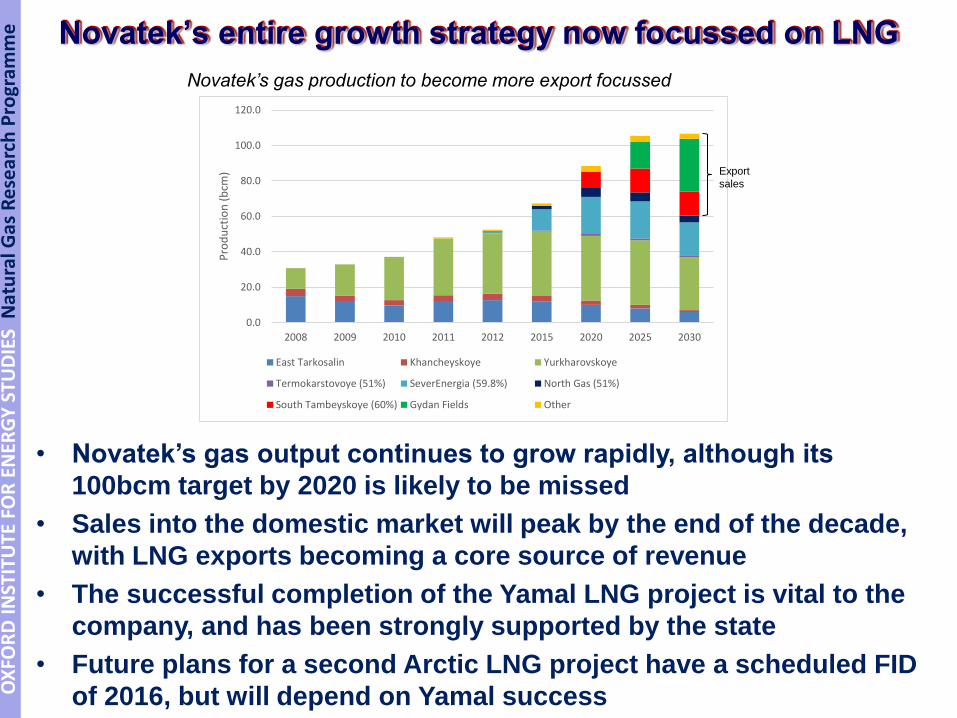

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2008 2009 2010 2011 2012 2015 2020 2025 2030

Pro

du

ctio

n (

bcm

)

East Tarkosalin Khancheyskoye Yurkharovskoye

Termokarstovoye (51%) SeverEnergia (59.8%) North Gas (51%)

South Tambeyskoye (60%) Gydan Fields Other

• Novatek’s gas output continues to grow rapidly, although its

100bcm target by 2020 is likely to be missed

• Sales into the domestic market will peak by the end of the decade,

with LNG exports becoming a core source of revenue

• The successful completion of the Yamal LNG project is vital to the

company, and has been strongly supported by the state

• Future plans for a second Arctic LNG project have a scheduled FID

of 2016, but will depend on Yamal success

Novatek’s entire growth strategy now focussed on LNG

Novatek’s gas production to become more export focussed

Export

sales

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

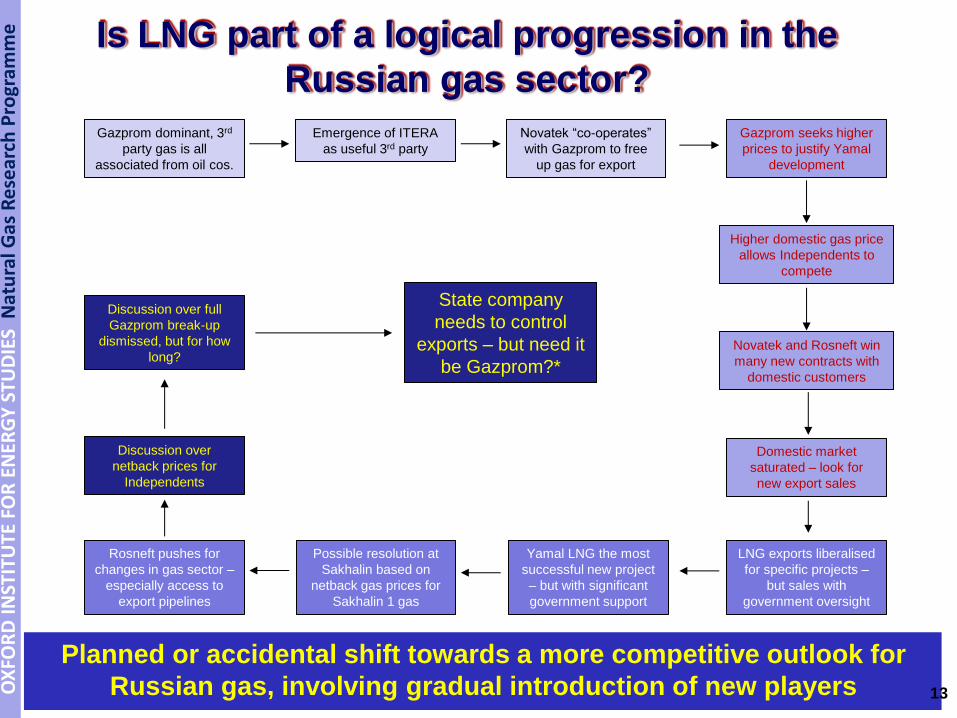

Is LNG part of a logical progression in the

Russian gas sector?

Planned or accidental shift towards a more competitive outlook for

Russian gas, involving gradual introduction of new players 13

Gazprom dominant, 3rd

party gas is all

associated from oil cos.

Emergence of ITERA

as useful 3rd party

Novatek and Rosneft win

many new contracts with

domestic customers

Possible resolution at

Sakhalin based on

netback gas prices for

Sakhalin 1 gas

Higher domestic gas price

allows Independents to

compete

Novatek “co-operates”

with Gazprom to free

up gas for export

Gazprom seeks higher

prices to justify Yamal

development

Rosneft pushes for

changes in gas sector –

especially access to

export pipelines

Yamal LNG the most

successful new project

– but with significant

government support

LNG exports liberalised

for specific projects –

but sales with

government oversight

Domestic market

saturated – look for

new export sales

Discussion over full

Gazprom break-up

dismissed, but for how

long?

Discussion over

netback prices for

Independents

State company

needs to control

exports – but need it

be Gazprom?*

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

Appendix

14

OX

FOR

D I

NST

ITU

TE F

OR

EN

ERG

Y S

TUD

IES

Nat

ura

l Gas

Re

sear

ch P

rogr

amm

e

Russian LNG Projects – Detail and Status

Gazprom dominates in terms of potential projects but has a poor record for

implementation

Shell is a key partner, but will sanctions interfere with progress?

Rosneft has the involvement of Exxon, but its project is hardly a priority

Only Novatek has the key involvement of China, the core market for gas in

the East 15

Russian

Operator

Partners Volume

(mtpa)

Status

Sakhalin 2 Existing Gazprom Shell, Mitsubishi,

Mitsui

10 Producing since 2009

Yamal LNG Novatek Total, CNPC, Silk

Road Fund

16.5 Under construction; first output

planned 2017/18

Baltic LNG Gazprom Shell ? 5-10 Start-up planned for 2020, but still in

planning stages

Sakhalin 2 Expansion Gazprom Shell, Mitsubishi,

Mitsui

5 FID planned for 2017, but now

uncertain due to Sakhalin 3 sanctions

Far East LNG (Sakhalin 1) Rosneft Exxon, Sodeco,

ONGC

5-10 Initially planned for 2019, but now

postponed to early 2020s

Vladivostok LNG Gazprom 10-15 Postponed until beyond 2020

Arctic LNG Novatek 16.5 New LNG concept based on Gydan

peninsula fields. Possible start-up in

mid-2020s

Pechora LNG Rosneft Alltech 4 Concept outlined, but no firm plans

yet

Schtokman (Phase 1) Gazprom Previously Total &

Statoil

15 Postponed indefinitely