Embed Size (px)

Citation preview

Live the life you want

CARE Super Pty Ltd (Trustee) ABN 91 006 670 060 AFSL 235226 | CARE Super (Fund) ABN 98 172 275 725

Your guide to planning for life after work

2 | caresuper.com.au

Life after work can be great to imagine. But it can also be intimidating, especially if you’re not feeling 100% prepared.

The good news? It’s never too late to put yourself in a better financial position.

The information provided in this document is general advice only and has been prepared without taking into account your particular financial needs, circumstances or objectives. You should consider your own investment objectives, financial situation and needs and read the appropriate product disclosure statement prior to making an investment decision. You may also wish to consult a licensed financial adviser.Some products and services mentioned in this Guide are provided by third parties. The Trustee is not responsible for the products or services, views or actions of these third parties. Terms and conditions may apply which should be obtained from third parties direct. The Trustee does not accept liability if loss or damage is incurred from the acquisition of third party products or services.The information in this document is current at the date of issue and may change due to legislative or other changes. The superannuation planning calculators mentioned in this Guide are provided by Industry Fund Services Limited (IFS) under its Australian financial services licence, ABN 54 007 016 195, AFSL 232514. Projections are based on information that you provide in addition to certain required assumptions which generate the projections. The projections are not guaranteed to be accurate or complete and CARE Super Pty Ltd takes no responsibility for errors or omissions.

Congratulations! You’ve worked hard to build up your super. Now it’s time to think about the future.

At CareSuper, we help our members answer these questions every day – and we can help you too.

• How much money will I need after work?

• How much will I be able to spend?

• Could I outlive my money?

• How can I save more?

• What tools and resources are available?

• Who can help me come up with a plan?

This guide is for you if you’ve been wondering:

CareSuper 1300 664 781 | 3 | 3

Four steps to living well after work

Start planning

What sort of future are you prepared to commit to? See how much better off you could be.

Tools and resources

Access tools, seminars and financial planning advice over the phone – all at no extra cost.

Income for living

Learn about when you can access your super, your retirement income choices and ways to make your money last.

Page 23

Page 4 Page 12

Page 30

Time for you

Life after work is a time for new beginnings and choice. Learn about how much you’ll need to pay for your new life.

1 2

43

CareSuper 1300 664 781 | 5 | 5

Retirement is changing. With most of us staying healthier longer and life expectancies continuing to rise, our later-in-life years are starting to look quite different. Life in our late 50s, 60s and 70s can be a time for new beginnings and more choice.

So, imagine how you’d like to live life in your later years. Ask yourself:

• What will my routine look like?

• Do I see myself travelling, volunteering or taking up a new hobby?

• How much time would I like to spend with friends and family?

• Would I prefer to stop paid work completely – or wind down gradually?

• Do I want to change jobs – try something new that fits my interests and lifestyle?

Don’t just think about it. Talk to your friends. Write it down. Create a storyboard or a Pinterest board. Be imaginative.

These days it’s not unusual for people to retire from their ‘career’ of a lifetime and then find work on a part-time, casual or occasional basis that’s more aligned with their interests and lifestyle. It could be using skills they’ve built up that can be carried across industries, or it might involve changing tack completely.

For example, the chemist that retires and then decides to help out at the local micro brewery on a seasonal contract basis, because they’re bored. The office manager who picks up a part-time mowing franchise because they’ve always loved gardening. Sometimes retirement from your ‘career’ can open up working in a whole new way, add a new dimension to life – and help stretch your super savings.

Imagine living the life you want

it’s not unusual for people to retire from their ‘career’ and then find work on a more casual basis Ti

me

for

you

6 | caresuper.com.au

Another way to find new interests outside work could be through volunteering.Here are some ideas to get you started.

• Follow your passion. Support something you believe in and it will shine through everything you do.

• Look at your transferrable skills. You might be an accountant, but what if you’re also a whiz at organising and promoting events?

• Develop new skills and career pathways. Volunteer organisations understand people come to them to flex new skills in lieu of payment.

• Don’t be afraid to ask for paid work. Once you’re in an organisation, it’s easier to spot job opportunities and connect with the right people.

• Stay connected. Even if you stop volunteering, keep up the relationships. It could be a great way to build friendships for the future.

Learn more at Volunteering Australia at www.volunteeringaustralia.org GoVolunteer at govolunteer.com.au, and Probono Australia at probonoaustralia.com.au/volunteer. Even SEEK has a volunteering section at www.volunteer.com.au

CareSuper 1300 664 781 | 7 | 7

Tim

e fo

r yo

u

How much income will you need? Once you’ve thought about what you’d like to do, let’s look at how much you might spend.

The Association of Superannuation Funds of Australia (ASFA) has analysed the spending patterns of a large number of Australians and used the findings to estimate how much most of us need to live on. Here’s what it found.

Modest lifestyle Comfortable lifestyle

Single Couple Single Couple

Total per year $27,368 $39,353 $42,764 $60,264

Figures from ASFA as at March 2018 quarter and are based on the budgets and living standards of someone aged around 65. The figures in each case assume that the retiree(s) own their own home and relate to expenditure by the household. This can be greater than household income after income tax where there is a drawdown on capital over the period of retirement. Single calculations are based on female figures. Visit superannuation.asn.au for more information.

Modest vs comfortable lifestyle

In ASFA’s terms, a ‘modest’ lifestyle allows you to cover life’s basics, like groceries, bills and transport. A ‘comfortable’ lifestyle lets you do things like pursue your hobbies, take out private health insurance, buy a reasonable car and travel.

This research shows that the Age Pension alone is often not enough to fund even a modest lifestyle in retirement. Add to that the fact that we’re living longer means super will be vital to providing income for our retirement years.

the fact that we’re living longer means super will be vital to providing income for our retirement years

8 | caresuper.com.au

The good news is that Australians are living longer. Australians aged 85+ increased by over 130% in the past two decades. The only downside – you could outlive your savings.

Outliving your savings is also known as ‘longevity risk’. If you do, you’ll be forced to rely solely on the Age Pension, which is currently a maximum of $907.60 per fortnight

‘Magical’ retirement income numberEveryone’s income needs are different, and they’ll change over time as you move through the various life stages after you stop working, including:

• Active stage – for many the ‘doing’ years when you have a go at all the things you said you’d get around to ‘some day’. May include part-time work, travel, volunteering.

• Sedentary stage – more about consolidation and staying closer to home, a time to choose fun things, develop old skills, explore fresh talents and grow new friendships.

• Reflection stage – health and finances may limit choice, a time to accept help graciously, reflect on precious memories and keep up with hobbies, old friends and loved ones.

Each of these stages comes with different spending patterns. Your ability to realise your active stage dreams and fund your later-in-life needs will depend largely on how much super and other income sources you have when you stop working.

Could you outlive your savings?for a single, or $1368.20 per fortnight combined for a couple (at March 2018).

At CareSuper, we offer a Guaranteed Income product designed to last a lifetime or fixed period which, used in combination with other retirement income products, could help to reduce longevity risk. Find out more on page 17.

CareSuper 1300 664 781 | 9 | 9

Tim

e fo

r yo

u

Percentage of Australians aged 65 or over

By 2056 1 in 4 people will be aged over 65.

If you’re 65 now, there’s a 50% chance

you’ll live to 90. If you live as a couple,

there’s a 50% chance one of you may live to 93.

Australians aged 85+ increased

132.9% over past 2 decades.

Australian Population Projections, Australian Bureau of Statistics, 2008, Updated 2013 Life Expectancy, The Australian Institute of Health and Welfare, 2015 2015 Intergenerational Report Australia in 2055, The Commonwealth of Australia Deaths, The Australian Institute of Health and Welfare, 2015

What is the life expectancy of Australians?

83Men

aged 55 now 86Women

aged 55 now

An ageing population

4%

13.5%

23%

1901 2010 2041

Life expectancy, the big picture

will be aged over 85.

Between 1.7 and 3.1 million

Did you know?

1 in 2 people will be diagnosed with cancer by age 85, but the survival rate has improved

by 24%.

10 | caresuper.com.au

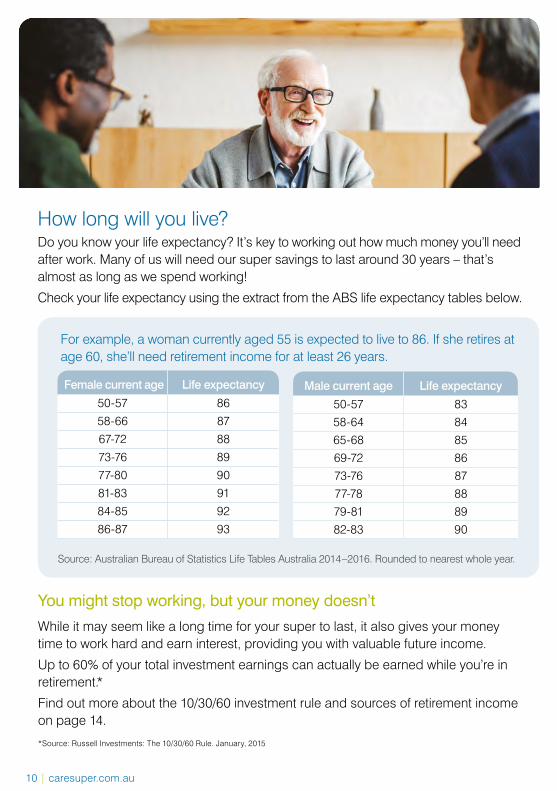

Source: Australian Bureau of Statistics Life Tables Australia 2014–2016. Rounded to nearest whole year.

How long will you live? Do you know your life expectancy? It’s key to working out how much money you’ll need after work. Many of us will need our super savings to last around 30 years – that’s almost as long as we spend working!

Check your life expectancy using the extract from the ABS life expectancy tables below.

You might stop working, but your money doesn’t

While it may seem like a long time for your super to last, it also gives your money time to work hard and earn interest, providing you with valuable future income.

Up to 60% of your total investment earnings can actually be earned while you’re in retirement.*

Find out more about the 10/30/60 investment rule and sources of retirement income on page 14.

*Source: Russell Investments: The 10/30/60 Rule. January, 2015

Female current age Life expectancy

50-57 86

58-66 87

67-72 88

73-76 89

77-80 90

81-83 91

84-85 92

86-87 93

Male current age Life expectancy

50-57 8358-64 8465-68 8569-72 8673-76 8777-78 8879-81 8982-83 90

For example, a woman currently aged 55 is expected to live to 86. If she retires at age 60, she’ll need retirement income for at least 26 years.

CareSuper 1300 664 781 | 11 | 11

Tim

e fo

r yo

u

Live your future life today

You can check how much income your current super will give you when you stop now with our Income stream calculator at caresuper.com.au/incomestream.

Compare it with your personal household budget to see how well that income covers your current lifestyle costs and what small adjustments, such as working longer or making extra super contributions, could mean for your future income.

Road test your future incomeOnce you have an idea of your estimated weekly income, why not road test your future life by spending just that much for a week? See how it feels.

Some extra helpCareSuper has a range of calculators to help with budgeting and spending. Visit caresuper.com.au/supercalculators

your life expectancy is key to working out how much money you’ll need after work

What to do next

CareSuper 1300 664 781 | 13 | 13

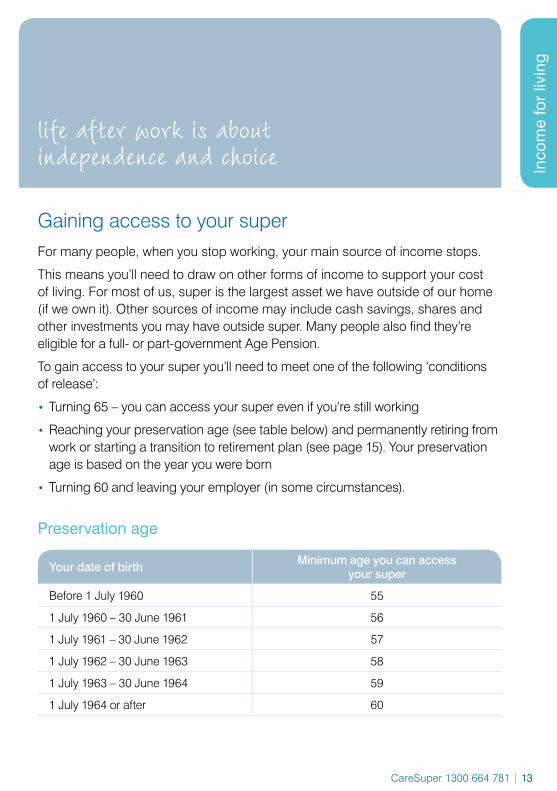

Income for living

Gaining access to your superFor many people, when you stop working, your main source of income stops.

This means you’ll need to draw on other forms of income to support your cost of living. For most of us, super is the largest asset we have outside of our home (if we own it). Other sources of income may include cash savings, shares and other investments you may have outside super. Many people also find they’re eligible for a full- or part-government Age Pension.

To gain access to your super you’ll need to meet one of the following ‘conditions of release’:

• Turning 65 – you can access your super even if you’re still working

• Reaching your preservation age (see table below) and permanently retiring from work or starting a transition to retirement plan (see page 15). Your preservation age is based on the year you were born

• Turning 60 and leaving your employer (in some circumstances).

Inco

me

for

livin

g

life after work is about independence and choice

Preservation age

Your date of birth Minimum age you can access your super

Before 1 July 1960 55

1 July 1960 – 30 June 1961 56

1 July 1961 – 30 June 1962 57

1 July 1962 – 30 June 1963 58

1 July 1963 – 30 June 1964 59

1 July 1964 or after 60

14 | caresuper.com.au

Savings while working Investment returns while working Investment returns after work

10%

30%60%

Sources of retirement income

10/30/60 investment ruleThere’s a commonly-held investment rule* that says your retirement income will come from the following sources:

• 10% from your super contributions

• 30% from the investment returns before you stop work and

• 60% from the investment returns on your retirement capital after you stop work.

That’s right… 60% of your retirement income will likely come from investment returns after you stop work.

This means you are still investing at least some of your super for the long term. Think about the day you expect to withdraw your last dollar from super – how far in the future is that? If you are in your 60s now, that might be 15 or 20 years away. This becomes your long-term time horizon for investing. Being a long-term investor for at least part of your super means you can afford to take more risk for that portion, in the expectation of generating higher returns.

60% of your retirement income will likely come from investment returns after you stop work

Generally, investment in high risk assets will produce higher returns over the long term, with a greater chance of a negative return over the short term. Be aware that there are risks in investing too conservatively. The main risk is that your money will grow too slowly, leaving you short. A financial planner can help you decide how much risk is appropriate and help you make informed investment decisions. Find out more on page 31.

* The 10/30/60 rule assumes someone joins super at age 25 and contributes $1000 a month, with this amount rising 4.75% every year after that until retirement. The person begins receiving a retirement income at age 65 and this rises 3% each year until death at age 90, when their account balance is nil. The investment return is assumed to be 7.8% each year. The 10/30/60 Rule, Russell Investments, January 2008, Revised July 2012

CareSuper 1300 664 781 | 15 | 15

Inco

me

for

livin

g

Turning super into incomeThe good news is you can start accessing your super even while you are still working, under transition to retirement rules.

Transition to retirement A transition to retirement (TTR) plan allows you to withdraw funds from your super while continuing to build your savings. It is designed to provide both financial freedom and free time while you’re still working. Once you reach your preservation age (see page 13), you can open an account.

Less work, same payWith a CareSuper transition to retirement plan you can cut back your working hours and maintain your cash flow with regular payments from your pension account. You could even decrease the amount of tax you pay on your income by making salary sacrifice contributions into super.

Find out more at caresuper.com.au/TTR

• You need a minimum of $10,000 to open an account

• Minimum annual pension payment amounts apply, based on your age

• Maximum annual payment of 10% of your account balance each year

• Earnings from your pension account are taxed up to 15%

• Payments are tax free after you turn 60

Facts & figures

16 | caresuper.com.au

Stay investedWith CareSuper, you have a wide range of investment options, so your money can keep working hard. Eligible members can even invest in our Direct Investment option, for more choice over where their money goes.

Tax-free earningsWith a CareSuper Pension you pay no tax on investment earnings.

Find out more at caresuper.com.au/pension

CareSuper Pension When you leave your job permanently or turn 65, you can convert your super lump sum into regular payments with a CareSuper Pension, just like a regular pay cheque.

You can choose to be paid twice monthly, monthly, quarterly, half yearly or yearly. The money goes straight into your bank account, just like when you were working. And you can change the frequency any time.

Want to spoil the grandkids? Or need to do some home repairs? You can take a lump sum from your pension account if you need to. Lump sum withdrawals can be done easily using PensionOnline.

Facts & figures• Payments are tax free once you turn 60• Minimum pension drawdowns based on your age• Maximum initial investment and transfer balance cap of $1.6 million applies

• Earnings are tax free• You can open an account when you:

– Reach your preservation age (see page 13) and permanently retire – Reach age 60 and leave your job, or – Reach age 65.

you can take a lump sum from your pension account if you want to spoil the grandkids or need some home repairs

CareSuper 1300 664 781 | 17 | 17

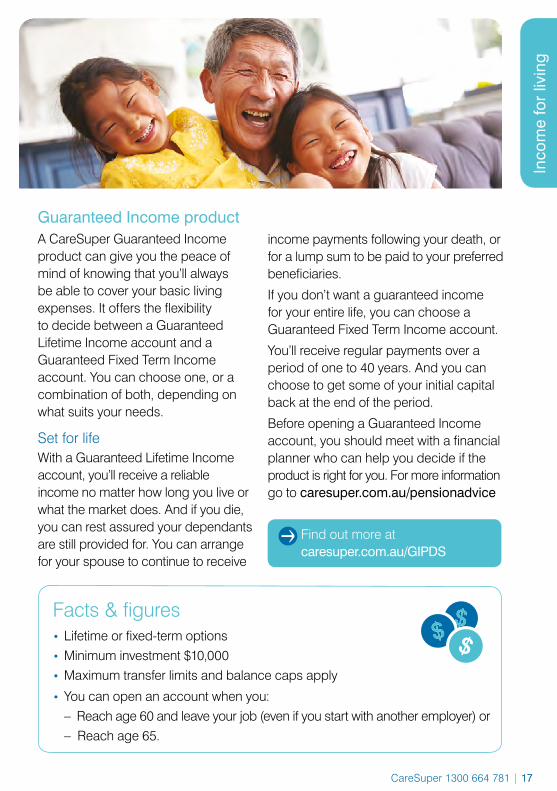

Guaranteed Income product

Inco

me

for

livin

g

A CareSuper Guaranteed Income product can give you the peace of mind of knowing that you’ll always be able to cover your basic living expenses. It offers the flexibility to decide between a Guaranteed Lifetime Income account and a Guaranteed Fixed Term Income account. You can choose one, or a combination of both, depending on what suits your needs.

Set for lifeWith a Guaranteed Lifetime Income account, you’ll receive a reliable income no matter how long you live or what the market does. And if you die, you can rest assured your dependants are still provided for. You can arrange for your spouse to continue to receive

income payments following your death, or for a lump sum to be paid to your preferred beneficiaries.

If you don’t want a guaranteed income for your entire life, you can choose a Guaranteed Fixed Term Income account.

You’ll receive regular payments over a period of one to 40 years. And you can choose to get some of your initial capital back at the end of the period.

Before opening a Guaranteed Income account, you should meet with a financial planner who can help you decide if the product is right for you. For more information go to caresuper.com.au/pensionadvice

Facts & figures• Lifetime or fixed-term options• Minimum investment $10,000• Maximum transfer limits and balance caps apply

• You can open an account when you: – Reach age 60 and leave your job (even if you start with another employer) or – Reach age 65.

Find out more at caresuper.com.au/GIPDS

18 | caresuper.com.au

Age Pension and other assistance

Government Age PensionIf you’re an eligible Australian resident, have reached pension age (between 65 and 67) and satisfy both an income and assets test, you can access the Age Pension. It works as a regular fortnightly income, designed to help pay for basic living expenses.

Payment rates

Per fortnight Single Couple each

Couple combined

Couple apart due to ill health

Maximum basic rate $826.20 $622.80 $1245.60 $826.20

Maximum Pension Supplement $67.30 $50.70 $101.40 $67.30

Energy Supplement $14.10 $10.60 $21.20 $14.10

Total $907.60 $684.10 $1368.20 $907.60

Source: Australian Department of Human Services, 20 March 2018

Other government assistanceEven if you don’t qualify for the Age Pension, you may still be eligible for other types of support, including a Commonwealth Seniors Health Card, Low Income Health Care Card and/or Pensioner Concession Card. These can be quite valuable giving you access to reduced prescription medicines under the Pharmaceutical Benefits Scheme and other medical services funded by the Australian Government, along with concessions offered by state, territory and local governments.

For further information visit humanservices.gov.au

other types of government assistance can be quite valuable

CareSuper 1300 664 781 | 19 | 19

Income layeringWhile we are fortunate to have the safety net of the Age Pension, the payment is modest, at best. For most, it will not be enough to live on.

It’s common for people to retire and start off receiving a part pension, which gets used for their basic costs, with super topping up the cost of essentials and covering the ‘nice-to-haves’.

Income layering works on the principle that cash to cover your basic cost of living and spending money can come from different sources. And this is a good thing, as it allows you to spread your super into different income products, each with its own, but complementary, benefits, risks and features.

For example, fixed income annuities, like CareSuper’s Guaranteed Income product, can provide a layer of guaranteed income to cover your

essential expenses. A Guaranteed Income account could be layered with an account-based pension, like a CareSuper Pension, which gives you access to market-linked income to cover variable or discretionary spending.

Can I afford to spend more at the beginning?

When you’re in the first active stage of retirement, you may want to spend more on hobbies, travel or renovations. By using income layering, you can make the most of your market-linked pension to fund this active stage. Then, as you get older, you’ll have the comfort of knowing the Guaranteed Income account and the Age Pension should cover your essential living costs.

No matter what your investment choice, it is important to understand risk and return and how they relate to achieving your income goals.

Inco

me

for

livin

g

20 | caresuper.com.au

CASE STUDY – Have your cake and eat it too

So, how does income layering work? Let’s look at Jean Bernard and Deirdre as an example.

Jean Bernard and Deirdre are both 65 years old and own their home. They’ve met with a financial planner to develop a plan to support them now that they’re ready to stop work. Here’s a snapshot of their financial position:

Assets and income Jean Bernard Deirdre

Super $500,000 $200,000

Employment income (p.a.) Nil Nil

Combined

Personal assets $10,000

Investment property $0

Other assets $15,000

Term deposit/cash $10,000

An important consideration for their financial planner is how long Jean Bernard and Deirdre are expected to live. Using the ABS Life Tables, here’s their life expectancy, given their current ages:

75% chance 50% chance 25% chance

Jean Bernard 16 years 23 years 28 years

Deirdre 19 years 25 years 30 years

As a couple (at least one person alive)

24 years 28 years 31 years

a financial planner can help you plan for retirement

Deirdre’s family is also known for living long lives, with both her parents reaching their 90s.

CareSuper 1300 664 781 | 21 | 21

As Jean Bernard and Deirdre have a 50% chance of one of them still being alive in 28 years, it makes sense to plan for a guaranteed secure income to help fund their essential needs as well as having growth assets and a flexible income to cover their ‘nice-to-have’ spending. They expect they will need $40,000 to cover essential costs and $12,000 for discretionary spending.

Their financial planner recommends the following combination of income products to meet Jean Bernard and Deirdre’s income needs over 12 months:

This example is provided for illustrative purposes only. It is general information only and not financial product advice and has been prepared without taking into account any person’s objectives, financial situation or needs. We strongly encourage you to seek professional advice, as well as taxation and social security advice, in relation to your individual financial circumstances before making any decisions.

Wants• Holidays• Meals out• Health insurance

Needs• Food• Clothing• Utilities• Car expenses

Inco

me

for

livin

g

CareSuper income $33,285

Guaranteed income $11,146

Age Pension $7,168

Other $400

22 | caresuper.com.au

What to do nextBudgeting tipsGood, old-fashioned money management is vital once you stop working, as your sources of income may be fixed and life, as we know, is full of surprises. Follow these simple steps for budgeting success:

• Separate your essential and discretionary costs. This will be important if income layering is an approach you think could work for you.

• Make it a priority to pay off non-deductible debts, like personal loans or credit cards first, then consider paying more off your mortgage or adding to super.

• Compare your current spending with your expected income. If you look like you’re going to fall short, consider adding to your savings now. Learn about ways to boost your super on page 25.

Some extra helpCareSuper has a range of calculators to help with budgeting and spending, as well as setting savings goals and managing debts. Visit caresuper.com.au/supercalculators

good, old-fashioned money management is vital once you stop working

CareSuper 1300 664 781 | 23 | 23

Start planning3

24 | caresuper.com.au

One of the questions we get asked a lot is ‘how can I save more?’

Our answer is surprisingly simple. Ask yourself two questions:

1 Can I increase my income?

2 Can I reduce my expenses?

Let’s just say that by increasing your income or reducing your expenses, you could save an extra $250 per month. What do you do with it?

Well, you’ve got choices. Some factors to consider are:

• Return on your investment• Tax treatment• Flexibility.

While there are lots of ways to invest your money, super was specifically designed to help us save for life after work. It’s tax-friendly when you put money in, and when it earns investment returns, and can still be one of the best ways to get the most out of your savings, while you have time to save. CareSuper has a team of experts to look after your investments while you’re working and when you retire.

Ways to save more

See what type of contribution could give your super the biggest boost with CareSuper’s Spare change calculator at caresuper.com.au/sparechange

super was specifically designed to help us save for life after work

CareSuper 1300 664 781 | 25 | 25

Sta

rt p

lann

ing

Pay for something in your future by boosting your super today You can add to your super before-tax (known as concessional contributions) or after-tax (known as non-concessional contributions), as well as add to your spouse’s super.

1. Type Before-tax*Make contributions before you pay income tax (salary sacrifice). Includes employer contributions.You can also split contributions with your spouse before-tax (if their fund accepts split contributions).Also known as ‘concessional contributions’.

After-tax#

Make contributions after you pay income tax.Spouse contributions could provide you a tax offset up to $540. If eligible, you could receive a boost from the Government, known as a co-contribution.Also known as ‘non-concessional contributions’.

2. Dollar Limits

$25,000 p.a.Taxed at 15%

$100,000 p.a.̂or $300,000 over 3 years (if you’re under 65 and contributing more than $100,000 in one year).

3. Age Limit 75 75

4. How Talk to your employer to set up a salary sacrifice arrangement.

You can make after-tax contributions to CareSuper using BPAY or direct debit. You may also choose to claim a tax deduction on these contributions (subject to certain restrictions), and these will be treated as concessional contributions.

* Before-tax contributions may have tax benefits, as the contributions tax you pay will generally be less than your marginal tax rate. If your taxable income is less than $250,000 p.a., your super contributions are taxed at 15%. If you earn more than $250,000 p.a., you’ll pay 30% tax on super contributions.

# If your total super balance (all your accounts) is $1.6 million or more, you cannot make after-tax contributions.

^ Transitional rules apply for after-tax contributions made between now and the 2018–19 financial year.

Information is current at the time of publication and is subject to change. For latest information visit ato.gov.au

26 | caresuper.com.au

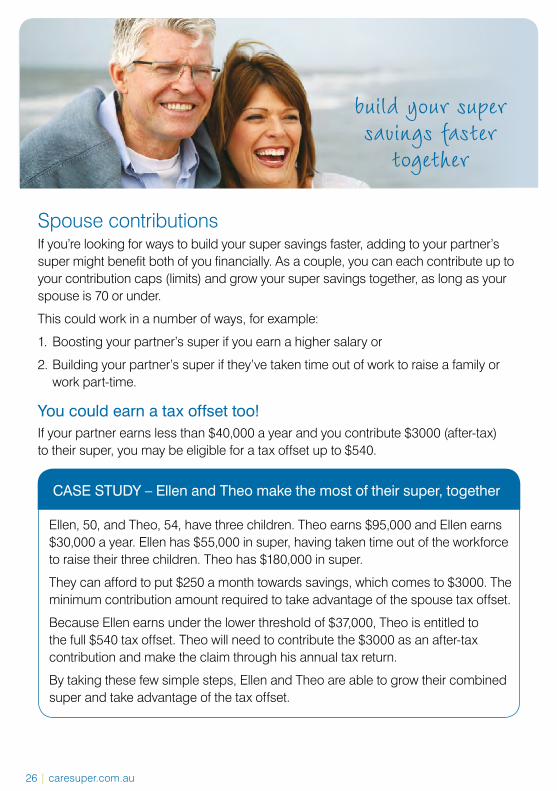

CASE STUDY – Ellen and Theo make the most of their super, together

Spouse contributionsIf you’re looking for ways to build your super savings faster, adding to your partner’s super might benefit both of you financially. As a couple, you can each contribute up to your contribution caps (limits) and grow your super savings together, as long as your spouse is 70 or under.

This could work in a number of ways, for example:

1. Boosting your partner’s super if you earn a higher salary or

2. Building your partner’s super if they’ve taken time out of work to raise a family or work part-time.

You could earn a tax offset too!If your partner earns less than $40,000 a year and you contribute $3000 (after-tax) to their super, you may be eligible for a tax offset up to $540.

Ellen, 50, and Theo, 54, have three children. Theo earns $95,000 and Ellen earns $30,000 a year. Ellen has $55,000 in super, having taken time out of the workforce to raise their three children. Theo has $180,000 in super.

They can afford to put $250 a month towards savings, which comes to $3000. The minimum contribution amount required to take advantage of the spouse tax offset.

Because Ellen earns under the lower threshold of $37,000, Theo is entitled to the full $540 tax offset. Theo will need to contribute the $3000 as an after-tax contribution and make the claim through his annual tax return.

By taking these few simple steps, Ellen and Theo are able to grow their combined super and take advantage of the tax offset.

build your super savings faster

together

CareSuper 1300 664 781 | 27 | 27

Sta

rt p

lann

ing

Know what’s aheadThere are aspects to life after work you’ll need to consider down the track. Downsizing, aged care and estate planning are big life decisions most of us will face as we get older. So why not be prepared?

Downsizing – cracking open another nest egg

downsizing, aged care and estate planning are big life decisions most of us will face, so why not be prepared?

Downsizing from a family home in an area where real estate prices are high to a less expensive and maybe smaller place may be a good way to release valuable equity for your future income needs. A bit like cracking open another financial nest egg!

Moving to a smaller home or apartment could have other benefits too. Like, less time spent on gardening and maintenance. Lower utility bills. Or an opportunity to help your children with expenses, a home deposit, or even an early inheritance.

A key consideration is the impact from a cash flow perspective. There are often costs involved with downsizing like preparing the property for sale and real estate selling costs.

Downsizing out of the family home opens up all sorts of lifestyle options. For some it’s about finding a smaller place in their familiar neighbourhood, and staying connected to your favourite doctor, green grocer, gym and pharmacist. For others it’s about a complete change of scene – a ‘tree change’ or ‘sea change’ – with the appeal of clean air, fresh water and the ability to go sailing, fishing, bushwalking or golfing.

28 | caresuper.com.au

How much better off could you be by adding to your super? ASIC’s MoneySmart Super contributions optimiser can help you understand which type of contribution might give your super the biggest boost, as well as which is the most tax-effective.

Once you have an idea of how much to add, why not check out our Income stream calculator at caresuper.com.au/incomestream to see what a difference it could make to your retirement income?

Some extra helpASIC’s MoneySmart website has a range of super and retirement calculators to help you make the most of your retirement income. Visit moneysmart.gov.au

Aged careThanks to our longer life expectancies and better health care, there is a shift in the way we age.

By 2056, an estimated one in four Australians will be aged over 65 and between 1.7 and 3.1 million people will be older than 85.* And, there is a growing trend for us to want to age in our own homes, rather than moving to residential care.

Recent government reforms to the aged care sector mean that from February 2017 in-home care packages are delivered on a consumer-directed care basis.

Essentially, what most people want is the ability to choose. You may not know now what’s going to suit you best – ageing at home or moving into an aged care facility – but it’s good to plan your finances to be able to afford either.

What to do next

* Australian Population Projections, Australian Bureau of Statistics, 2008, Updated 2013

CareSuper 1300 664 781 | 29 | 29

Can’t afford extra contributions? Here are some tips that won’t cost you a cent!

• Combine your super accounts If you have more than one super account you may be paying duplicate fees. By combining all your super into one fund, it’ll also be easier to keep track of how much super you have. (Before combining your super you should consider if you’ll be charged any exit or other fees. You should also consider the impact on any insurance (such as loss of insurance) or other benefits you may have with your other super funds.)

• Could you have lost super? Visit caresuper.com.au/supermatch and we’ll search for you. You just need your member number. If we

Log in to MemberOnline to check in on your super, investments and insurance any time at caresuper.com.au/login

find other or lost super and you’d like to combine it into your CareSuper account, we can help with that too.

• Review your insurance You may find your needs have changed and adjusting your cover may mean more money going towards your retirement.

• Check your investment choice Does it still fit with your goals and timeframes? It’s a good idea to check in on your investments at least once a year to ensure you’re comfortable with where your super is invested and the expected risk and return for your investment choice.

Super boosting tips

if you have more than one fundyou may be paying multiple fees

Sta

rt p

lann

ing

CareSuper 1300 664 781 | 31 | 31

Financial planningResearch shows six out of 10 Australian seniors are turning to financial advisers for information about retirement finances.̂

As a member, you can get advice at no extra cost over the phone on general matters regarding super, through CareSuper’s relationship with IFS.* We can help you with advice on your investment choice, ways to boost your super and insurance inside super.

For more comprehensive advice, you can make an appointment to create a more personalised plan.

IFS planners can take the worry out of planning for retirement and give you the confidence you’re making the best possible choices, because they’re the experts. Helping people make the most of their retirement finances is what they do every day.

They can offer advice on topics like:

• Maximising the Age Pension and other investments (including super)

• Estate planning and powers of attorney

• Setting up a Guaranteed Income account or a combination of CareSuper income accounts

• Budgeting and strategies to maximise your retirement income.

The first consultation for CareSuper members is complimentary and is a chance for the planner to decide what advice you need and provide an obligation-free quote. No personal advice is provided at this meeting. Fees for advice are transparent, competitive and commission-free. You can also deduct a portion of the fee from your super account for super-related advice.

What about your partner?If you have a partner and they’re with a different super fund, that’s ok, we can still help. Your financial planner will create a plan that covers both of you, no matter which super fund your partner is with.

six out of 10 australian seniors are turning to financial advisers about retirement finances To

ols

and

reso

urce

s

* Financial advice is offered through CareSuper’s relationship with Industry Fund Services Limited (IFS), and is provided by an authorisation under the Australian financial services licence of IFS, ABN 54 007 016 195, AFSL 232514

^ Seniors more savvy about retirement income, National Seniors Australia and Challenger, October 2017

32 | caresuper.com.au

Kali is 61, earns $85,000 p.a. and is divorced. Kali has a passion for wildlife and loves to volunteer at elephant sanctuaries. She owns her own home, but it’s really too big for her now.

With $280,000 in super and $50,000 in a short-term deposit, Kali decides to meet with a CareSuper IFS planner to discuss her dreams and how to set up her finances for when she leaves work permanently at age 65.

After reviewing her financial situation, Kali’s financial planner recommends a three-step approach to winding down work:

1. Start a transition to retirement but keep working full-time for the next four years and boost her super through salary sacrifice.

2. Investigate options to sell her home and downsize into a smaller apartment with shared facilities.

This would free up some profit from the sale that could boost her super and help fund her passion for volunteering.

3. At age 65, Kali sets up an income layering strategy with a CareSuper Guaranteed Income account and a CareSuper Pension, which is invested to give her super a chance to work hard over the next 22 years (Kali’s life expectancy).

This example is provided for illustrative purposes only. It is general information only and not financial product advice and has been prepared without taking into account any person’s objectives, financial situation or needs. We strongly encourage you to seek professional advice, as well as taxation and social security advice, in relation to your individual financial circumstances before making any decisions.

CASE STUDY – Kali makes the most of her savings and her dreams!

CareSuper 1300 664 781 | 33 | 33

Tool

s an

d re

sour

ces

Time to get startedLife after work by its very nature shouldn’t be hard. It’s a time to smell the roses. (Or the rosé.) Not a time to ponder unnecessary paperwork. At CareSuper, we make setting up your new life easy.

We’ll help you plan your finances for when you stop work, so you’re confident you’ve got that sorted. And we’ll help you make the most of your choices and investments after you retire.

After you’ve stopped work, it pays to review your finances at least annually – say in the lead up to 30 June or when you receive your CareSuper statement – so your financial plan takes into account the latest rules relating to tax, super and Centrelink. If you need to adjust your income payments or other arrangements, our financial planners can help you take advantage of new opportunities to maximise your income.

We make it easier for you to live the life you want.

Keep an eye out for upcoming events and free seminars at caresuper.com.au

it’s a time to smell the roses and make setting up your new life easy

34 | caresuper.com.au

What to do nextCongratulations! Now you’ve finished this guide, it’s time to take the next steps.

At CareSuper, we can help you get started with tools, seminars and financial advice you can get at no extra cost.

Ready to start? If you’re ready to get started, so are we. Call us on 1300 664 781 to take the next step.

CareSuper’s website, caresuper.com.au/retirement has lots of helpful information, including:

• Short online modules on retirement, goal-setting and estate planning

• Online calculators to get an estimate of your retirement income based on your situation (subject to certain assumptions)

• Upcoming events and free seminars including the CareSuper transition to retirement seminars

• CareSuper’s pension investment returns and awards

• Access to financial planning about your super at no extra cost over the phone*

• Forms to help you transfer your super and the CareSuper Pension Guide Product Disclosure Statement which outlines the important features and benefits of our income products in greater detail.

* Financial planning is offered through CareSuper’s relationship with Industry Fund Services Limited, and is provided by an authorisation under the Australian financial services licence of IFS, ABN 54 007 016 195, AFSL 232514.

CareSuper 1300 664 781 | 35 | 35

everyone’s journey is different and often the best outcome is a combination of strategies and product solutions

CR/RETIRE/GDE 941.0 05/18 ISS5

CareSuperLine 1300 664 781 caresuper.com.au

we make it easy for you

Issue date May 2018

ecoStar is an environmentally responsible paper made Carbon Neutral. The greenhouse gas emissions of the manufacturing process including transportation of the finished product to BJ Ball Papers Warehouses has been measured by the Edinburgh Centre for Carbon Management (ECCM) and offset by the Carbon Neutral Company and the fibre source has been independently certified by the Forest Stewardship Council (FSC). ecoStar is manufactured from 100% Post Consumer Recycled paper in a Process Chlorine Free environment under the ISO 14001 environmental management system.