Embed Size (px)

Citation preview

Grade: 7 Lesson # 9

Why should you start saving money early?

SS.8.FL.3.6 Identify the value of a person’s savings in the future as determined by the amount saved and the interest rate. Explain why the earlier people begin to save, the more savings they will be able to accumulate, all other things equal, as a result of the power of compound interest.

http://rjincometax.com/wp-content/uploads/2011/02/smart-money-savings.jpg

1

Correlated Literacy Standards:LAFS.7.RI.2.4 Determine the meaning of words and phrases as they are used in a text, including figurative, connotative, and technical meanings; analyze the impact of a specific word choice on meaning and tone.LAFS.7.W.3.8 Gather relevant information from multiple print and digital sources, using search terms effectively; assess the credibility and accuracy of each source; and quote or paraphrase the data and conclusions of others while avoiding plagiarism and following a standard format for citationLAFS.7.SL.1.2 Analyze the main ideas and supporting details presented in diverse media and formats

SS.8.FL.3.6 Identify the value of a person’s savings in the future as determined by the amount saved and the interest rate. Explain why the earlier people begin to save, the more savings they will be able to accumulate, all other things equal, as a result of the power of compound interest..

Start Saving Early

Lesson Number (1-15): 9

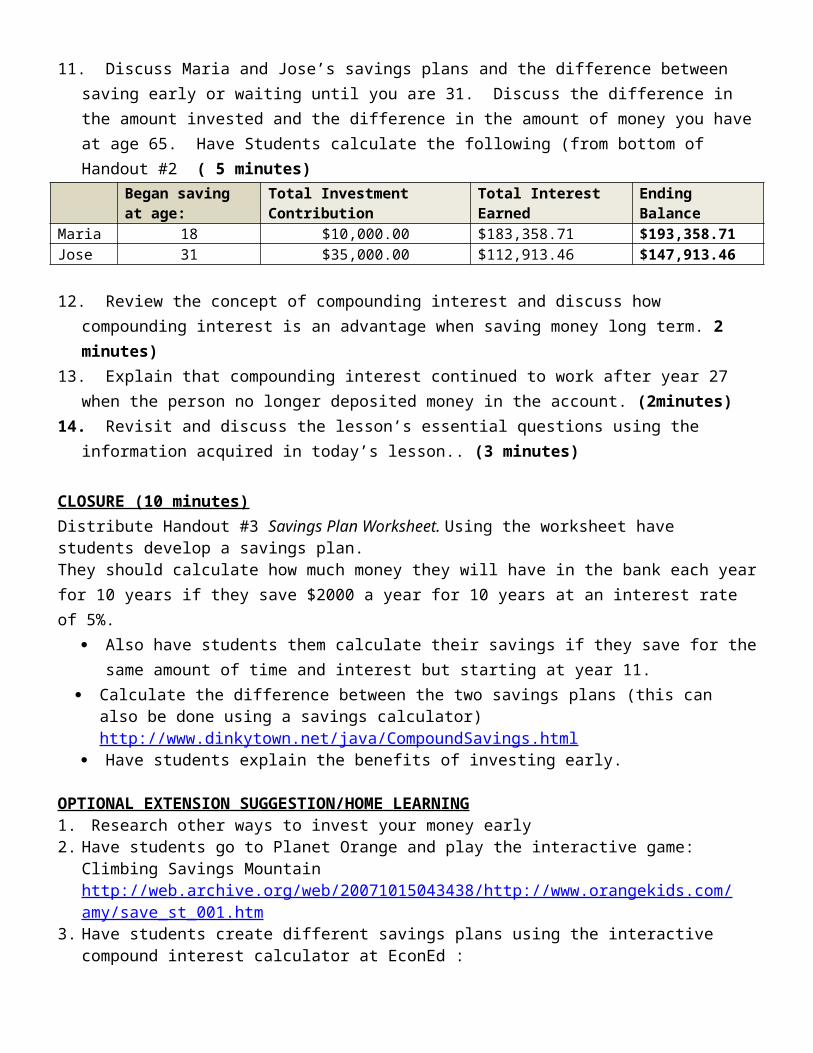

Correlated Florida Standards (See Full Text on Cover Page)LAFS.7.RI.2.4, LAFS.7.SL.1.2

Essential Question Why should you start saving money early?

Learning Goals/Objectives Understand Short term versus Long term savings Explain the benefits of beginning a savings plan early Describe how compound interest increases saving over time Identify the time value of money

OverviewIn this lesson, students will explore the time value of money and the benefits of starting to save money early. They will understand the advantages provided through compounding interest. By using video analysis and summative activities, students will be able to evaluate and explain the benefits of begging to save at an early age.

Materials Computer with internet connection Promethean or Smart Board Video: Need to Invest Early https://www.youtube.com/watch?v=5beqHhziyhs . (2:56) Handout #1: Thinking About the Video: Need to Invest Early (included) Handout #1: Thinking About the Video: Need to Invest Early Answer Key (included) Handout # 2 Advantages of Saving Early Worksheet Handout #3 Savings Plan Worksheet.

Time50 minutes

Activity SequenceINTRODUCTION/HOOK (2 minutes)

1. Ask the question: When should you start saving money?2. Discuss answers3. Ask students: Do you think there is a benefit to saving money early?4. Discuss answers5. Ask students: Why do you think it is important to start saving early?

6. Discuss answers

ACTIVITY( 38 minutes)1. Introduce the concept of short term goals and long term goals for saving money

Short Term Goals: takes a short length of time to achieve the money goal set such as a few weeks or a few months. You should use a short term savings goals when the item you want to purchase is not very expensive but you still do not have enough money to buy it.Examples: DVD, new shoes, latest fashion trend, movie ticketsLong term Goals: take a longer time to save the money needed. It can take several months or even years to save the amount of money needed to purchase the item. Long term savings is used for articles that are expensive.Example: bike, computer and spending money for a family trip. ( 5 minutes)

2. Introduce the concept of retirement as a long term goal (1 minute)3. Explain to the students that once you retire, you will have less income than when you are working.

Explain the importance of saving money while you are working to be able to afford to retire. (3 minutes)4. Introduce the time value of money concept and the importance of starting to save early.

From EconEd: If someone owes you money, should you require them to pay you back all at once, or in payments

divided over a period of time? According to a concept that economists call the time value of money: you would probably be better off getting your money right away, in one payment. You could invest this money and earn interest on it or you could use this money to pay off all or part of a loan. There are a million things you could do with this money. The time value of money refers to the fact that a dollar in hand today is worth more than a dollar promised at some future time.

But how can that be? A dollar is a dollar, isn't it? Yes, but a dollar in hand today can be invested in an interest-bearing account that would grow in value over time. This explains in part why the value of money is related to time. (3 minutes)

5. Reinforce concept by explaining to students that because of time value of money: Iit is important to start saving early because if you leave it for later you will need to save more money in order to make up for the time you did not save. (1 minute)

6. Explain to students that they will be watching a video that will demonstrate the benefits of beginning to save at an early age. One of the terms that will be used in the video is procrastinating. Ask if anyone knows the meaning of procrastinating? Discuss (to put off, delay, “drag your feet”) (1 minute)

7. Show video: Need to Invest Early https://www.youtube.com/watch?v=5beqHhziyhs . Have students take notes on the important points presented in the video. (3 minutes)

8. After viewing the video, distribute Handout # 1 Thinking About the Video: Need to Invest Early. Explain to students that they may use their notes to complete the handout. Provide time for students to complete. ( 5 minutes)

9. Review Handout with students. Discuss the advantages of early savings and the time value of money. (3 minutes)

10. Show students the advantage of starting early worksheet (1 minute)11. Discuss Maria and Jose’s savings plans and the difference between saving early or waiting until you are

31. Discuss the difference in the amount invested and the difference in the amount of money you have at age 65. Have Students calculate the following (from bottom of Handout #2 ( 5 minutes)

Began saving at age: Total Investment Contribution Total Interest Earned Ending BalanceMaria 18 $10,000.00 $183,358.71 $193,358.71Jose 31 $35,000.00 $112,913.46 $147,913.46

12. Review the concept of compounding interest and discuss how compounding interest is an advantage when saving money long term. 2 minutes)

13. Explain that compounding interest continued to work after year 27 when the person no longer deposited money in the account. (2minutes)

14. Revisit and discuss the lesson’s essential questions using the information acquired in today’s lesson.. (3 minutes)

CLOSURE (10 minutes)Distribute Handout #3 Savings Plan Worksheet. Using the worksheet have students develop a savings plan.They should calculate how much money they will have in the bank each year for 10 years if they save $2000 a year for 10 years at an interest rate of 5%.

Also have students them calculate their savings if they save for the same amount of time and interest but starting at year 11.

Calculate the difference between the two savings plans (this can also be done using a savings calculator) http://www.dinkytown.net/java/CompoundSavings.html

Have students explain the benefits of investing early.

OPTIONAL EXTENSION SUGGESTION/HOME LEARNING1. Research other ways to invest your money early2. Have students go to Planet Orange and play the interactive game: Climbing Savings Mountain

http://web.archive.org/web/20071015043438/http://www.orangekids.com/amy/save_st_001.htm3. Have students create different savings plans using the interactive compound interest calculator at EconEd

: http://www.econedlink.org/interactives/EconEdLink-interactive-tool-player.php?filename=interest.swf&lid=603

Sources/Bibliographic Information that contributed to this lesson:http://rjincometax.com/wp-content/uploads/2011/02/smart-money-savings.jpghttp://pbskids.org/itsmylife/money/managing/article3.htmlhttp://www.investopedia.com/terms/t/timevalueofmoney.asphttp://www.thesimpledollar.com/how-important-is-it-to-start-early/http://www.ncpublicschools.org/docs/curriculum/socialstudies/secondary/personalfinancialliteracy/section4.pdfhttp://education.howthemarketworks.com/teachers/personal-finance-lesson-plans/savings-lesson-plans/http://www.econedlink.org/teacher-lesson/603/Interactive Compound Interest Calculator http://www.econedlink.org/interactives/EconEdLink-interactive-tool-player.php?filename=interest.swf&lid=603

Handout #1 Name_______________________

Thinking About the Video: Need to Invest Early

1. Larry got off to an early start in saving money. At what age did Larry begin saving? ________

2. How much money did Larry save each year? ____________ What was his compound interest rate? _____

3. How many years did Larry Invest his $2000/per year?________ What was the total amount he put in savings? __________

4. Why did Larry stop investing? ___________________ ____________________________

5. Did he ever put more money into the account? _________________________

6. What happened to the money in Larry’s account? ___________________________________

7. Larry’s twin brother Barry is a procrastinator – he put off starting a savings plan until what age?_________

8. How much did Barry invest per year? ________________________________

9. How long did Barry invest his yearly $2,000.00? _____________________________

10. How much did Barry contribute to his savings? ______________________________

11.Fill in the chart below:Larry Barry

Age he began investing:

Total Amount of Contributions

Value at age 65

12.Based on the video and chart above, what conclusion can you make about the age one starts investing?_________________________________________________________

______________________________________________________________________13. Explain the time value of money in your own words:

Handout #1 Name_______________________________

Thinking About the Video: Need to Invest Early Answer Key

1. Larry got off to an early start in saving money. At what age did Larry begin saving? 19 years old

2. How much money did Larry save each year? $2000.00 per year What was his compound interest rate? __10%___

3. How many years did Larry Invest his $2000/per year?___8 years __ What was the total amount he put in savings? $16,000

4. Why did Larry stop investing? Had some bad times and couldn’t afford the $2000 per year any longer

5. Did he ever put more money into the account? No

6. What happened to the money in Larry’s account? IT continued to earn interest

7. Larry’s twin brother Barry is a procrastinator – he put off starting a savings plan until what age?___27

8. How much did Barry invest per year? _____$2,000.00

9. How long did Barry invest his yearly $2,000.00? until he was 65

10.How much did Barry contribute to his savings?__$78,000.00__

11.Fill in the chart below:

Larry Barry

Age he began investing: 19 27

Total Amount of Contributions

$16,000 $78,000

Value at age 65 $1,035,160.00 $883,185

12.Based on the video and chart above, what conclusion can you make about the age one starts investing? The earlier that you begin saving, the more time your money has to grow (earn interest). This equals more money earned.

13. Explain the time value of money in your own words:

Handout # 2 Advantages of Saving Early

Maria Age Balance Deposit Total 7 % Interest Ending Balance

18 $0.00 $1,000. $1,000.00 $70.00 $1,070.0019 $1,070.00 $1,000 $2,070.00 $144.90 $2,214.9020 $2,214.90 $1,000 $3,214.90 $225.04 $3,439.9421 $3,439.94 $1,000 $4,439.94 $310.80 $4,750.7422 $4,750.74 $1,000 $5,750.74 $402.55 $6,153.2923 $6,153.29 $1,000 $7,153.29 $500.73 $7,654.0224 $7,654.02 $1,000 $8,654.02 $605.78 $9,259.8025 $9,259.80 $1,000 $10,259.80 $718.19 $10,977.9926 $10,977.99 $1,000 $11,977.99 $838.46 $12,816.4527 $12,816.45 $1,000 $13,816.45 $967.15 $14,783.6028 $14,783.60 $0.00 $14,783.60 $1,034.85 $15,818.4529 $15,818.45 $0.00 $15,818.45 $1,107.29 $16,925.7430 $16,925.74 $0.00 $16,925.74 $1,184.80 $18,110.5431 $18,110.54 $0.00 $18,110.54 $1,267.74 $19,378.2832 $19,378.28 $0.00 $19,378.28 $1,356.48 $20,734.7633 $20,734.76 $0.00 $20,734.76 $1,451.43 $22,186.2034 $22,186.20 $0.00 $22,186.20 $1,553.03 $23,739.2335 $23,739.23 $0.00 $23,739.23 $1,661.75 $25,400.9836 $25,400.98 $0.00 $25,400.98 $1,778.07 $27,179.0437 $27,179.04 $0.00 $27,179.04 $1,902.53 $29,081.5838 $29,081.58 $0.00 $29,081.58 $2,035.71 $31,117.2939 $31,117.29 $0.00 $31,117.29 $2,178.21 $33,295.5040 $33,295.50 $0.00 $33,295.50 $2,330.68 $35,626.1841 $35,626.18 $0.00 $35,626.18 $2,493.83 $38,120.0242 $38,120.02 $0.00 $38,120.02 $2,668.40 $40,788.4243 $40,788.42 $0.00 $40,788.42 $2,855.19 $43,643.6144 $43,643.61 $0.00 $43,643.61 $3,055.05 $46,698.6645 $46,698.66 $0.00 $46,698.66 $3,268.91 $49,967.5646 $49,967.56 $0.00 $49,967.56 $3,497.73 $53,465.2947 $53,465.29 $0.00 $53,465.29 $3,742.57 $57,207.8648 $57,207.86 $0.00 $57,207.86 $4,004.55 $61,212.4249 $61,212.42 $0.00 $61,212.42 $4,284.87 $65,497.2850 $65,497.28 $0.00 $65,497.28 $4,584.81 $70,082.0951 $70,082.09 $0.00 $70,082.09 $4,905.75 $74,987.8452 $74,987.84 $0.00 $74,987.84 $5,249.15 $80,236.9953 $80,236.99 $0.00 $80,236.99 $5,616.59 $85,853.5854 $85,853.58 $0.00 $85,853.58 $6,009.75 $91,863.3355 $91,863.33 $0.00 $91,863.33 $6,430.43 $98,293.7656 $98,293.76 $0.00 $98,293.76 $6,880.56 $105,174.3357 $105,174.33 $0.00 $105,174.33 $7,362.20 $112,536.5358 $112,536.53 $0.00 $112,536.53 $7,877.56 $120,414.0959 $120,414.09 $0.00 $120,414.09 $8,428.99 $128,843.0760 $128,843.07 $0.00 $128,843.07 $9,019.02 $137,862.0961 $137,862.09 $0.00 $137,862.09 $9,650.35 $147,512.4362 $147,512.43 $0.00 $147,512.43 $10,325.87 $157,838.3063 $157,838.30 $0.00 $157,838.30 $11,048.68 $168,886.9864 $168,886.98 $0.00 $168,886.98 $11,822.09 $180,709.0765 $180,709.07 $0.00 $180,709.07 $12,649.64 $193,358.71

Jose

Age Balance Deposit Total 7 % Interest Ending Balance18 $0.0019 $0.0020 $0.0021 $0.0022 $0.0023 $0.0024 $0.0025 $0.0026 $0.0027 $0.0028 $0.0029 $0.0030 $0.0031 $0.00 $1,000.00 $1,000.00 $70.00 $1,070.0032 $1,070.00 $1,000.00 $2,070.00 $144.90 $2,214.9033 $2,214.90 $1,000.00 $3,214.90 $225.04 $3,439.9434 $3,439.94 $1,000.00 $4,439.94 $310.80 $4,750.7435 $4,750.74 $1,000.00 $5,750.74 $402.55 $6,153.2936 $6,153.29 $1,000.00 $7,153.29 $500.73 $7,654.0237 $7,654.02 $1,000.00 $8,654.02 $605.78 $9,259.8038 $9,259.80 $1,000.00 $10,259.80 $718.19 $10,977.9939 $10,977.99 $1,000.00 $11,977.99 $838.46 $12,816.4540 $12,816.45 $1,000.00 $13,816.45 $967.15 $14,783.6041 $14,783.60 $1,000.00 $15,783.60 $1,104.85 $16,888.4542 $16,888.45 $1,000.00 $17,888.45 $1,252.19 $19,140.6443 $19,140.64 $1,000.00 $20,140.64 $1,409.85 $21,550.4944 $21,550.49 $1,000.00 $22,550.49 $1,578.53 $24,129.0245 $24,129.02 $1,000.00 $25,129.02 $1,759.03 $26,888.0546 $26,888.05 $1,000.00 $27,888.05 $1,952.16 $29,840.2247 $29,840.22 $1,000.00 $30,840.22 $2,158.82 $32,999.0348 $32,999.03 $1,000.00 $33,999.03 $2,379.93 $36,378.9649 $36,378.96 $1,000.00 $37,378.96 $2,616.53 $39,995.4950 $39,995.49 $1,000.00 $40,995.49 $2,869.68 $43,865.1851 $43,865.18 $1,000.00 $44,865.18 $3,140.56 $48,005.7452 $48,005.74 $1,000.00 $49,005.74 $3,430.40 $52,436.1453 $52,436.14 $1,000.00 $53,436.14 $3,740.53 $57,176.6754 $57,176.67 $1,000.00 $58,176.67 $4,072.37 $62,249.0455 $62,249.04 $1,000.00 $63,249.04 $4,427.43 $67,676.4756 $67,676.47 $1,000.00 $68,676.47 $4,807.35 $73,483.8257 $73,483.82 $1,000.00 $74,483.82 $5,213.87 $79,697.6958 $79,697.69 $1,000.00 $80,697.69 $5,648.84 $86,346.5359 $86,346.53 $1,000.00 $87,346.53 $6,114.26 $93,460.7960 $93,460.79 $1,000.00 $94,460.79 $6,612.26 $101,073.0461 $101,073.04 $1,000.00 $102,073.04 $7,145.11 $109,218.1562 $109,218.15 $1,000.00 $110,218.15 $7,715.27 $117,933.4363 $117,933.43 $1,000.00 $118,933.43 $8,325.34 $127,258.7664 $127,258.76 $1,000.00 $128,258.76 $8,978.11 $137,236.8865 $137,236.88 $1,000.00 $138,236.88 $9,676.58 $147,913.46

Total Investment Contribution Total Interest Earned Ending BalanceMariaJose

Handout # 3

Savings Plan WorksheetYears Balance Deposits Total Interest Rate Interest Ending

Balance1 .052 .053 .054 .055 .056 .057 .058 .059 .0510 .0511 .0512 .0513 .0514 .0515 .0516 .0517 .0518 .0519 .0520 .05

Years Balance Deposits Total Interest Rate Interest Ending Balance

1234567891011 .0512 .0513 .0514 .0515 .0516 .0517 .0518 .0519 .0520 .05