Embed Size (px)

Citation preview

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 1

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Liquor LiabilityExposures and Coverages

Presented by:

Allen Messer, CIC, CPCU

December 12, 2013

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 1

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

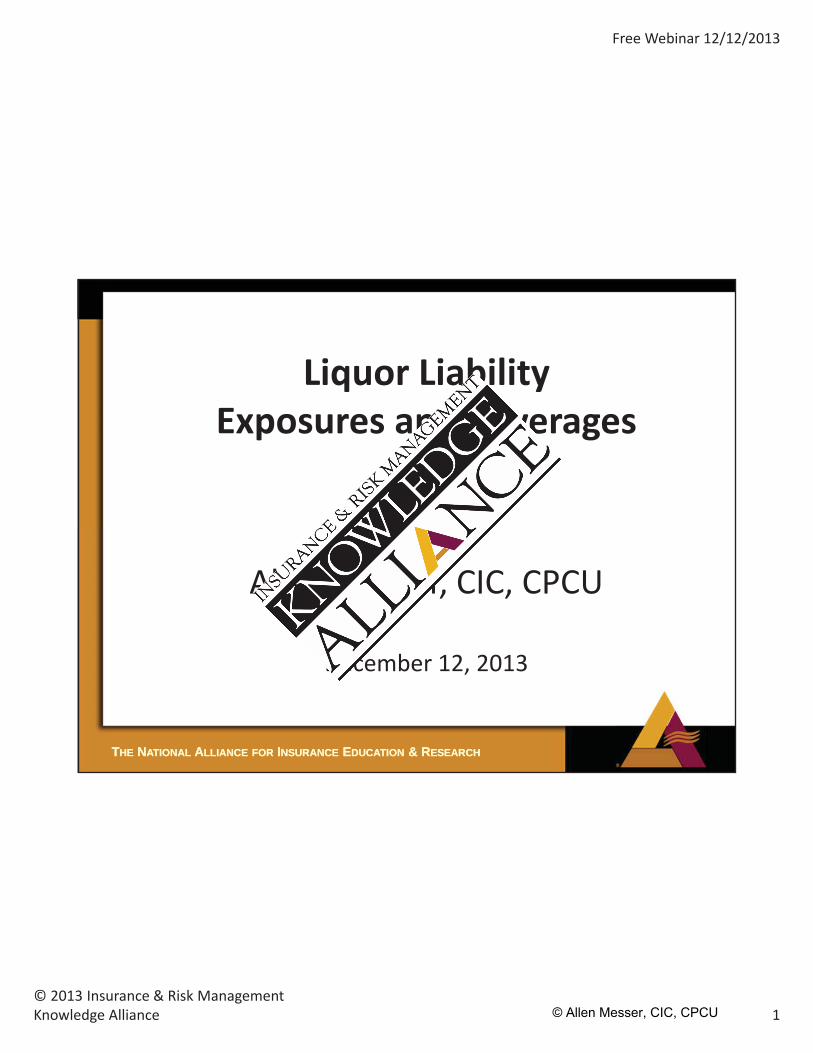

Common Law Liability TODAY• Purpose – good public policy

–But at first no liability for seller – consumption to bethe only responsible party

• Nature – “new common law”– “Seller” (defendant) created a foreseeable andunreasonable risk of injury to plaintiff

–May apply to:• On premises/off premises vendors• Social hosts/others

–Based on:• Gross Negligence• Negligence Per Se• Negligence

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Dram Shop Statutes TODAY

• Purposes–Protect innocent victim–Give seller incentive for compliance– Impose restrictions on consumption

• Nature–Plaintiff’s burden may differ from negligence – maycreate strict liability

–Common elements among jurisdictions• Sale/gift to AIP (allegedly intoxicated person)• Alleged Intoxication (either cause or contribute to)• Wrongful Act by AIP (intoxication is contributing factor)

–May be the exclusive remedy (jurisdictional)

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 2

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

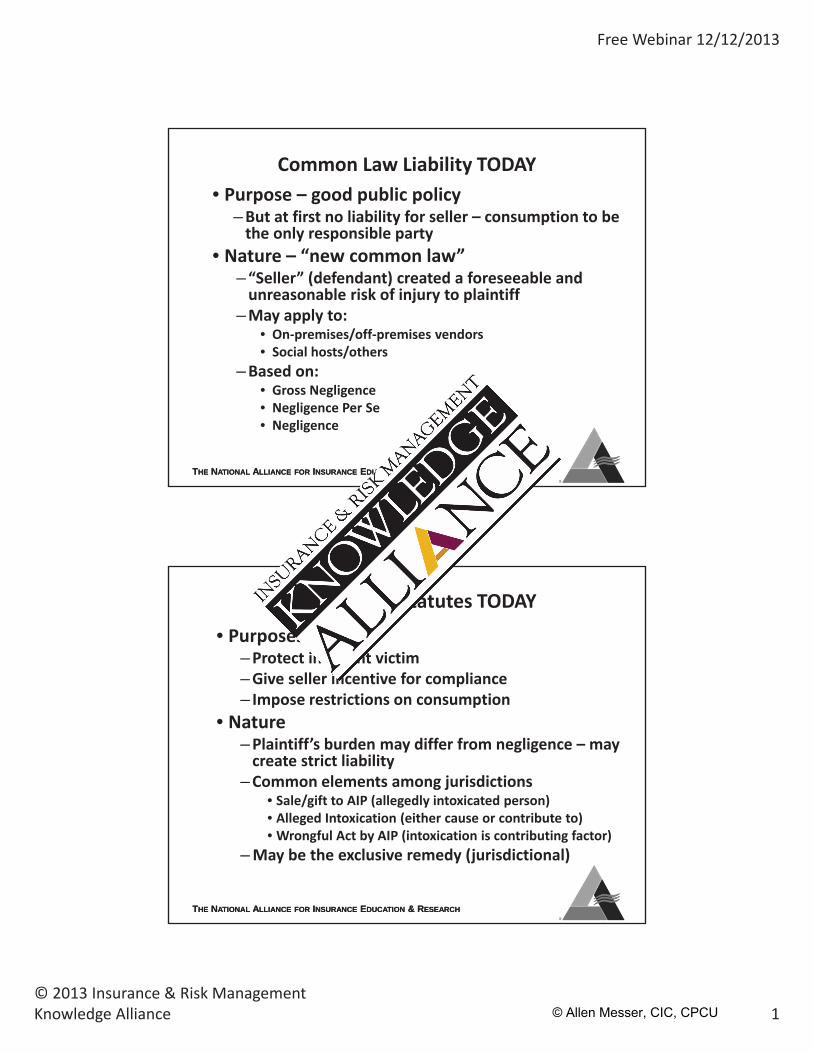

Usual Causes of LiabilityUnder Dram Shop Statute

• Sale/gift to someone who is “visibly”intoxicated– @.15 .29 BAL individual is more likely to display signs of visible intoxication

• Sale/gift to a minor (here we are talking about under the legal drinking age of 21)

• Sale to a habitual drunkard

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Liquor Liability Is Jurisdictional• Today 43 states and the District of Columbia recognize

some form of liability for purveyors of alcoholicbeverages based either on a dram shop statute (37states) and/or on common law principles (6 states) –NOT Delaware, Kansas, Maryland, Nebraska, Nevada,South Dakota or Virginia – and some statutes createa “limitation of liability” (e.g., Louisiana)

• Social hosts as well as “sellers” may have potentialliability (e.g., Indiana)

• You may have clients that operate in or travel in/tomultiple jurisdictions that may be more “liberal” thanthe jurisdiction where the business is located

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 3

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

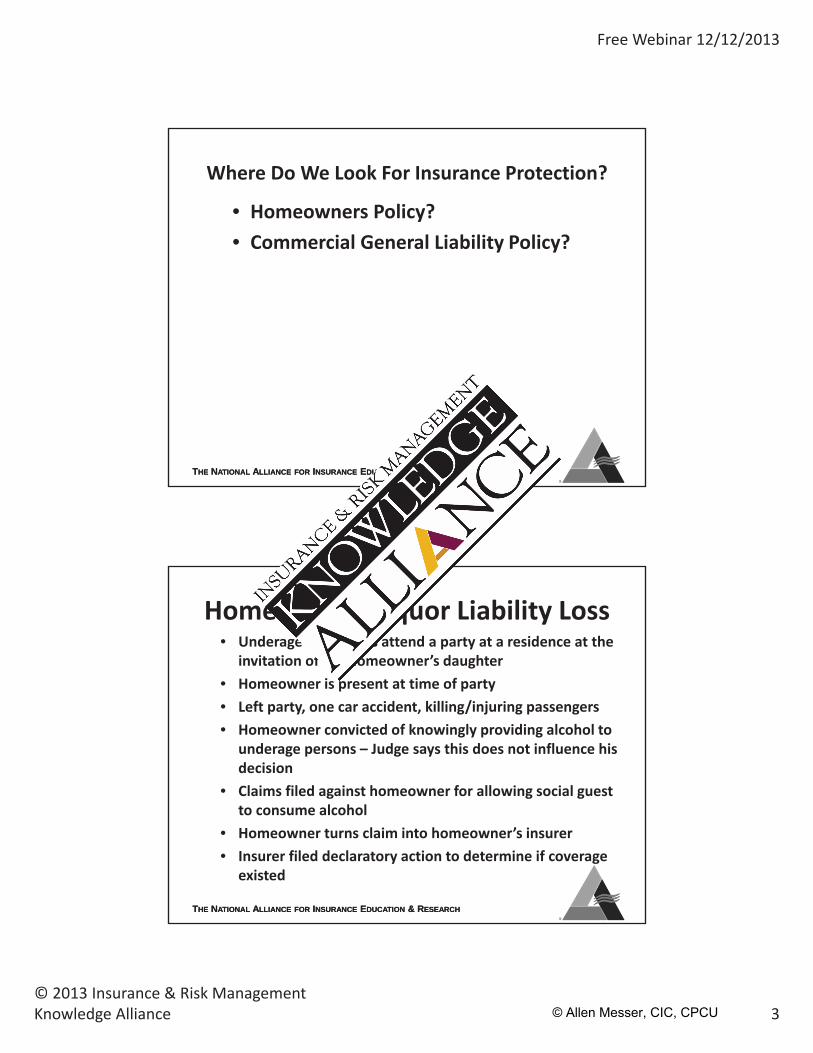

Where Do We Look For Insurance Protection?

• Homeowners Policy?• Commercial General Liability Policy?

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Homeowners Liquor Liability Loss• Underage individuals attend a party at a residence at the

invitation of the homeowner’s daughter• Homeowner is present at time of party• Left party, one car accident, killing/injuring passengers• Homeowner convicted of knowingly providing alcohol to

underage persons – Judge says this does not influence hisdecision

• Claims filed against homeowner for allowing social guestto consume alcohol

• Homeowner turns claim into homeowner’s insurer• Insurer filed declaratory action to determine if coverage

existed

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 4

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

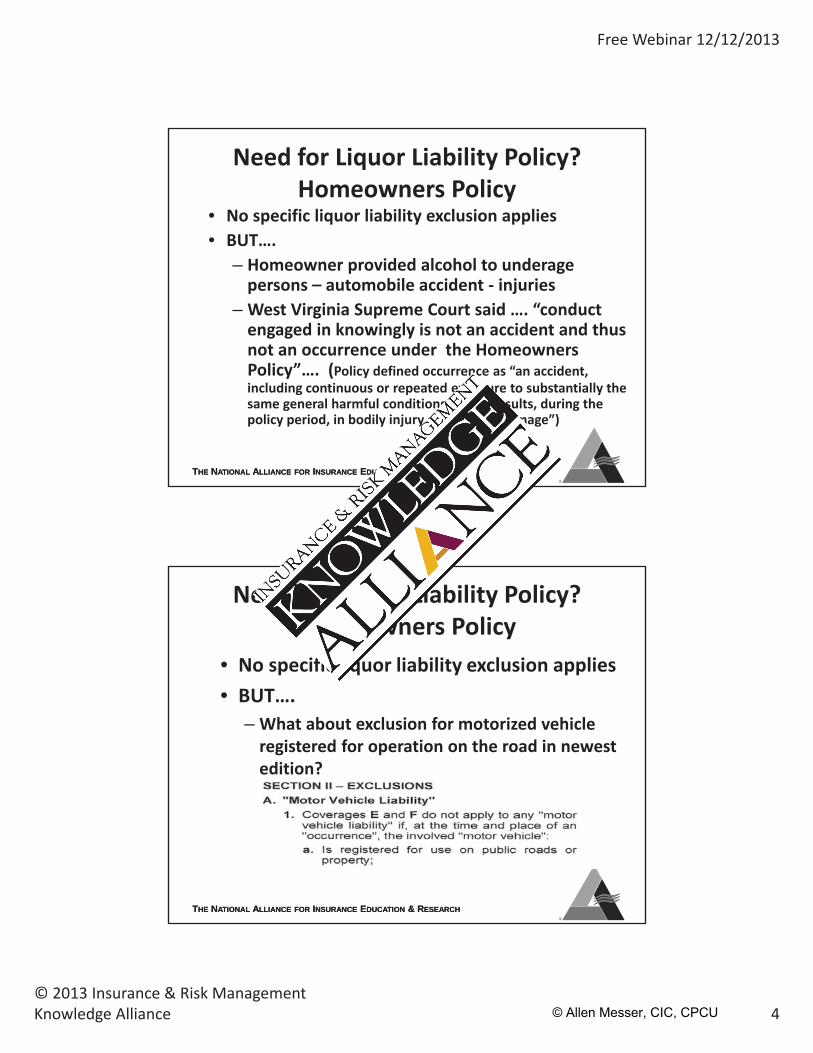

Need for Liquor Liability Policy?Homeowners Policy

• No specific liquor liability exclusion applies• BUT….

– Homeowner provided alcohol to underagepersons – automobile accident injuries

– West Virginia Supreme Court said …. “conductengaged in knowingly is not an accident and thusnot an occurrence under the HomeownersPolicy”…. (Policy defined occurrence as “an accident,including continuous or repeated exposure to substantially thesame general harmful conditions, which results, during thepolicy period, in bodily injury or property damage”)

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Need for Liquor Liability Policy?Homeowners Policy

• No specific liquor liability exclusion applies• BUT….

– What about exclusion for motorized vehicleregistered for operation on the road in newestedition?

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 5

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

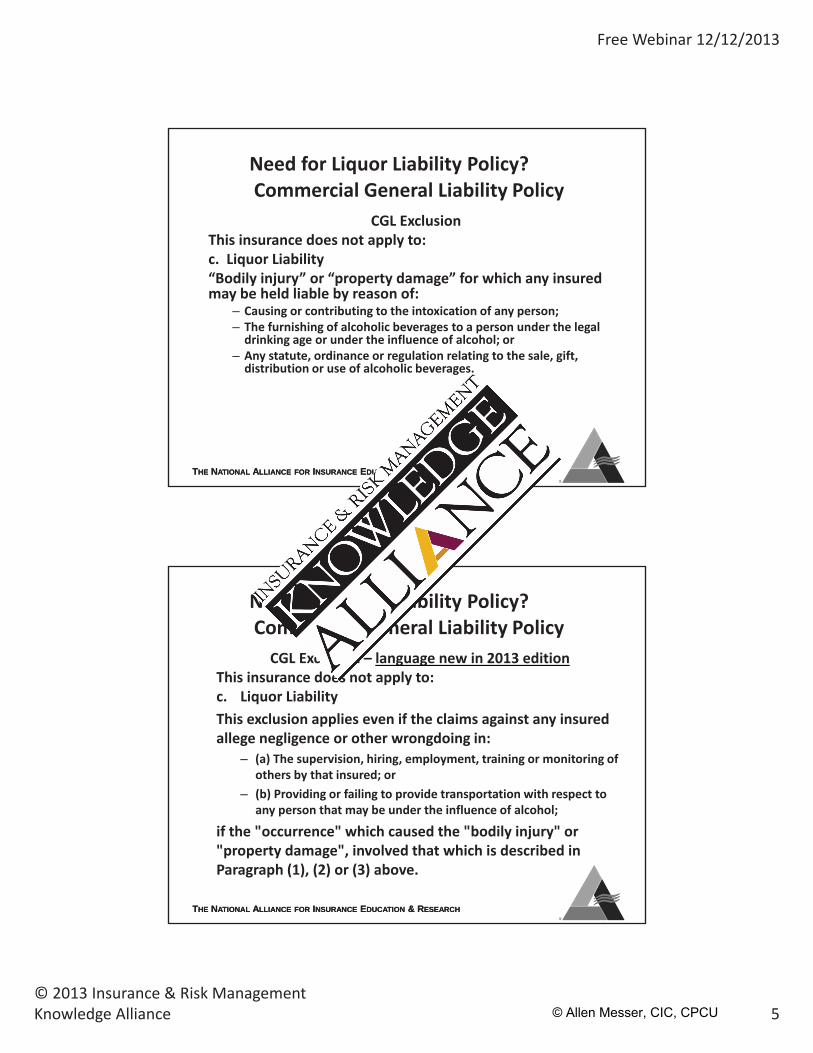

Need for Liquor Liability Policy?Commercial General Liability Policy

CGL ExclusionThis insurance does not apply to:c. Liquor Liability“Bodily injury” or “property damage” for which any insuredmay be held liable by reason of:

– Causing or contributing to the intoxication of any person;– The furnishing of alcoholic beverages to a person under the legaldrinking age or under the influence of alcohol; or

– Any statute, ordinance or regulation relating to the sale, gift,distribution or use of alcoholic beverages.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Need for Liquor Liability Policy?Commercial General Liability PolicyCGL Exclusion – language new in 2013 edition

This insurance does not apply to:c. Liquor LiabilityThis exclusion applies even if the claims against any insuredallege negligence or other wrongdoing in:

– (a) The supervision, hiring, employment, training or monitoring ofothers by that insured; or

– (b) Providing or failing to provide transportation with respect toany person that may be under the influence of alcohol;

if the "occurrence" which caused the "bodily injury" or"property damage", involved that which is described inParagraph (1), (2) or (3) above.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 6

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Need for Liquor Liability Policy?Commercial General Liability Policy

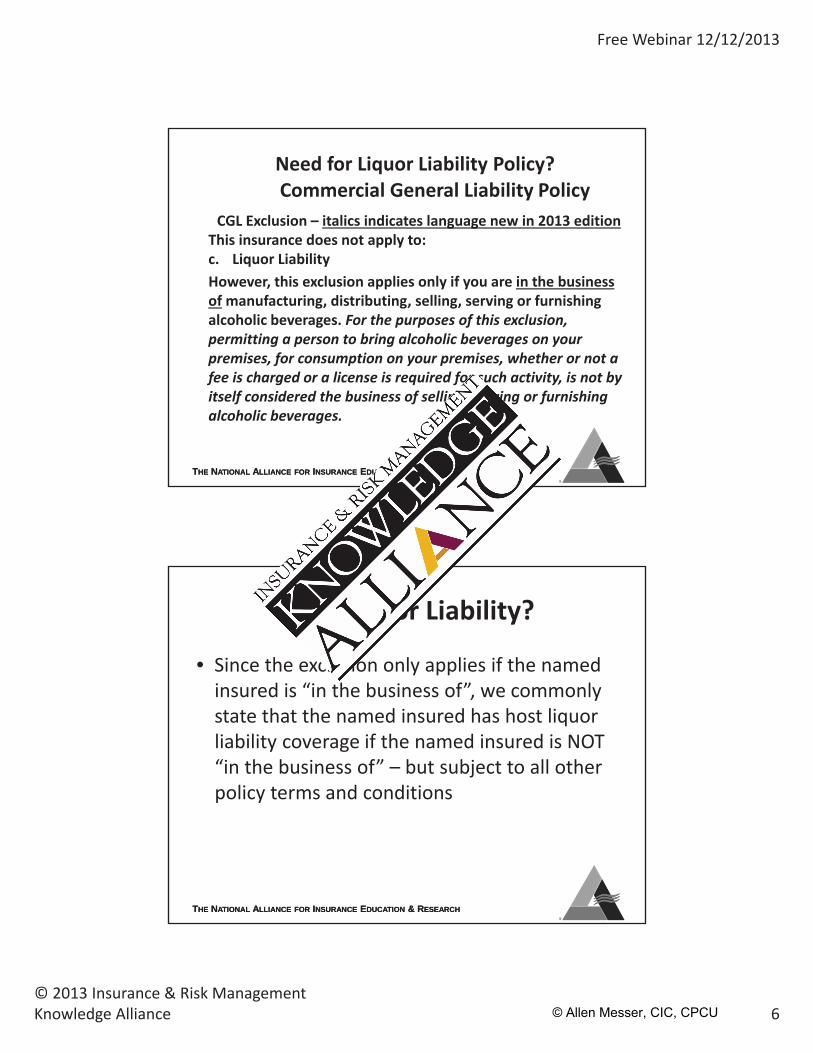

CGL Exclusion – italics indicates language new in 2013 editionThis insurance does not apply to:c. Liquor LiabilityHowever, this exclusion applies only if you are in the businessof manufacturing, distributing, selling, serving or furnishingalcoholic beverages. For the purposes of this exclusion,permitting a person to bring alcoholic beverages on yourpremises, for consumption on your premises, whether or not afee is charged or a license is required for such activity, is not byitself considered the business of selling, serving or furnishingalcoholic beverages.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Host Liquor Liability?

• Since the exclusion only applies if the namedinsured is “in the business of”, we commonlystate that the named insured has host liquorliability coverage if the named insured is NOT“in the business of” – but subject to all otherpolicy terms and conditions

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 7

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

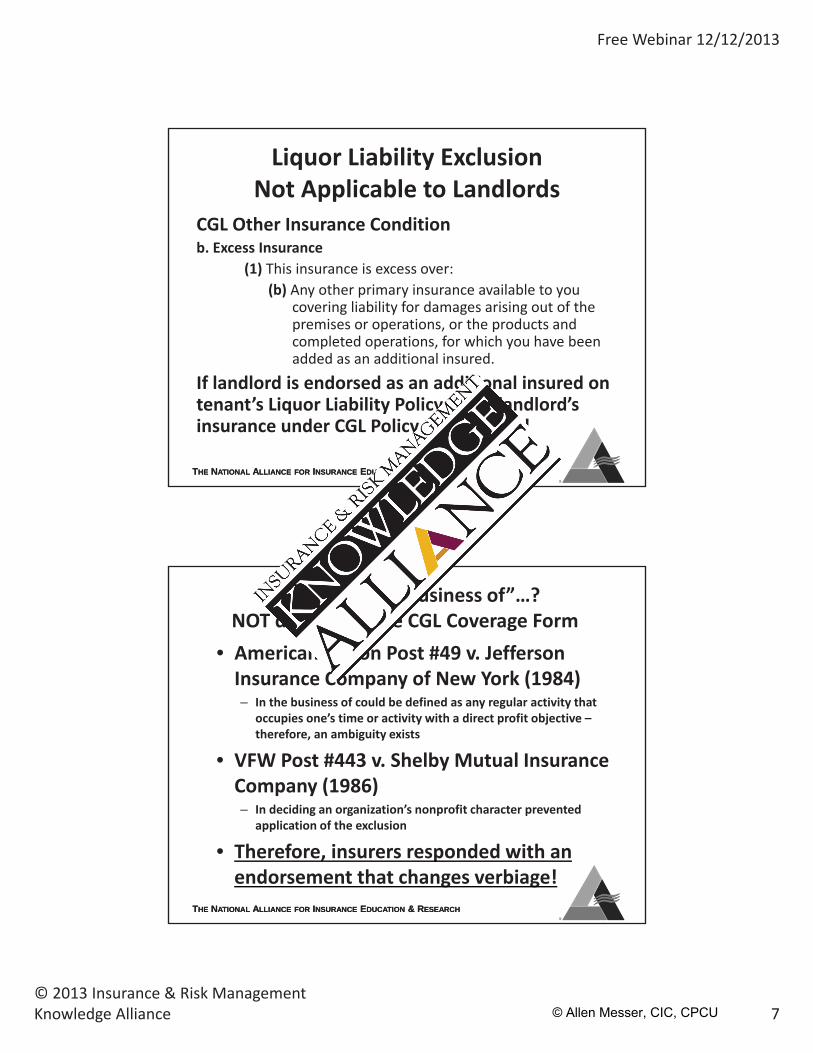

Liquor Liability ExclusionNot Applicable to Landlords

CGL Other Insurance Conditionb. Excess Insurance

(1) This insurance is excess over:(b) Any other primary insurance available to you

covering liability for damages arising out of thepremises or operations, or the products andcompleted operations, for which you have beenadded as an additional insured.

If landlord is endorsed as an additional insured ontenant’s Liquor Liability Policy, want landlord’sinsurance under CGL Policy to be excess!

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

What is “in the business of”…?NOT defined by the CGL Coverage Form

• American Legion Post #49 v. JeffersonInsurance Company of New York (1984)– In the business of could be defined as any regular activity that

occupies one’s time or activity with a direct profit objective –therefore, an ambiguity exists

• VFW Post #443 v. Shelby Mutual InsuranceCompany (1986)– In deciding an organization’s nonprofit character prevented

application of the exclusion

• Therefore, insurers responded with anendorsement that changes verbiage!

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 8

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Commercial General Liability EndorsementCG 21 50 Amendment of Liquor Liability Exclusion

Not applicable in all jurisdictions (MA/NJ/TX/WA)!Exclusion c. of COVERAGE A (Section I) is replaced by the following:

c. “Bodily injury” or “property damage” for which any insured may be held liable by reason of– Causing or contributing to the intoxication of any person;– The furnishing of alcoholic beverages to a person under the legal drinking age or under the influence

of alcohol; or– Any statute, ordinance or regulation relating to the sale, gift, distribution or use of alcoholic beverages.This exclusion applies even if the claims against any insured allege negligence or otherwrongdoing in:• The supervision, hiring, employment, training or monitoring of others by that insured; or• Providing or failing to provide transportation with respect to any person that may be

under the influence of alcohol; if the "occurrence" which caused the "bodily injury" or"property damage", involved that which is described in Paragraph (1), (2) or (3) above.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Commercial General Liability EndorsementCG 21 50 Amendment of Liquor Liability Exclusion

Exclusion c. of COVERAGE A (Section I) is replaced by the following:

This exclusion applies only if you:–Manufacture, sell or distribute alcoholic beverages;– Serve or furnish alcohol beverages for a chargewhether or not such activity:

• Requires a license;• Is for the purpose of financial gain or livelihood,or

– Serve or furnish alcoholic beverages without acharge, if a license is required for such activity.

– Permit any person to bring any alcoholic beverageson your premises for consumption on yourpremises.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 9

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

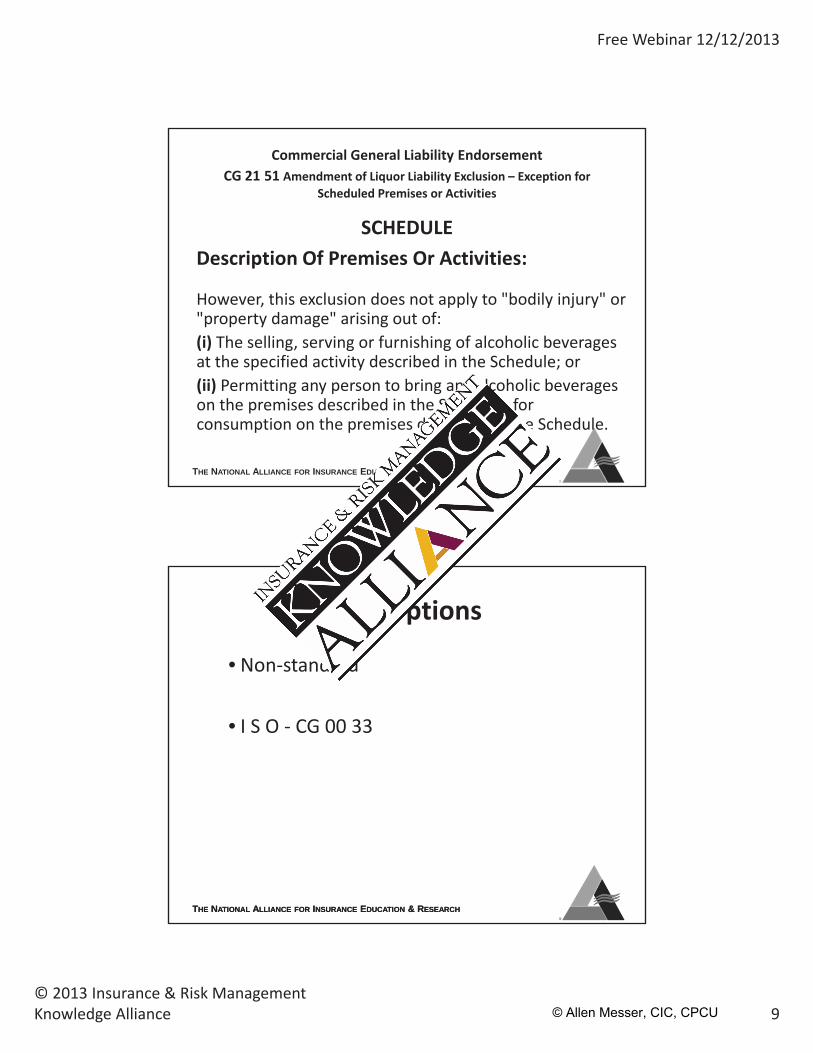

Commercial General Liability EndorsementCG 21 51 Amendment of Liquor Liability Exclusion – Exception for

Scheduled Premises or Activities

SCHEDULEDescription Of Premises Or Activities:

However, this exclusion does not apply to "bodily injury" or"property damage" arising out of:(i) The selling, serving or furnishing of alcoholic beveragesat the specified activity described in the Schedule; or(ii) Permitting any person to bring any alcoholic beverageson the premises described in the Schedule, forconsumption on the premises described in the Schedule.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Policy Options

• Non standard

• I S O CG 00 33

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 10

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

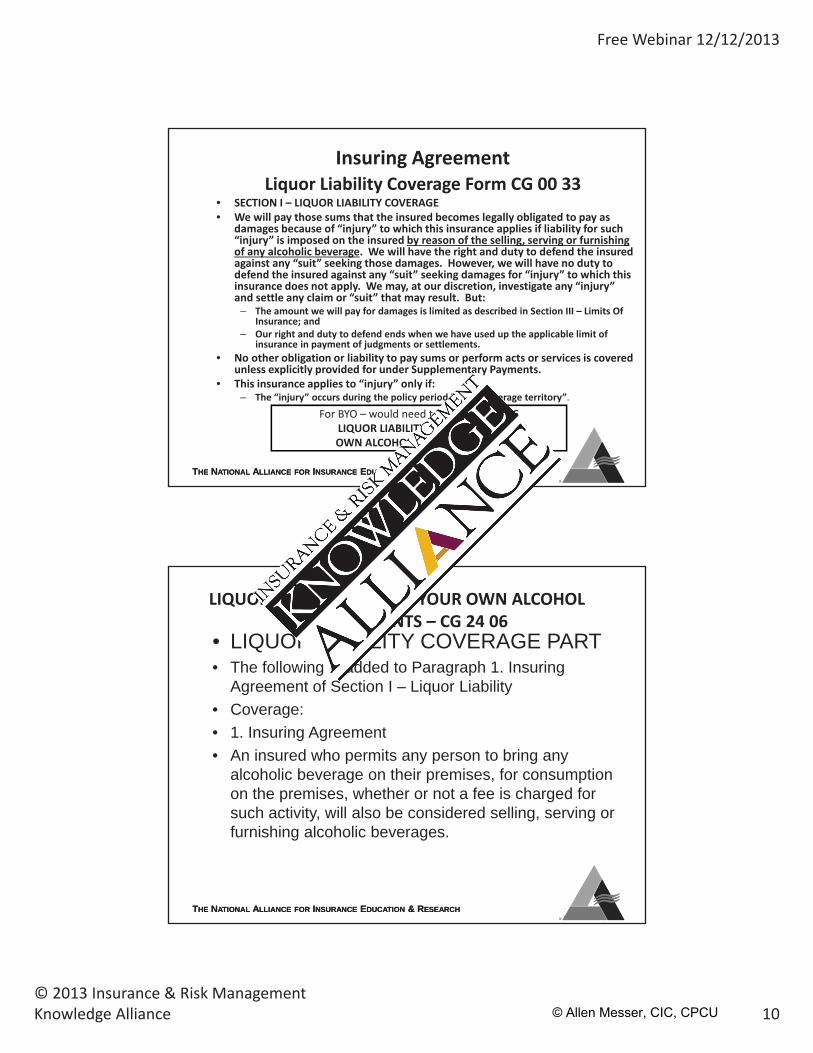

Insuring AgreementLiquor Liability Coverage Form CG 00 33

• SECTION I – LIQUOR LIABILITY COVERAGE• We will pay those sums that the insured becomes legally obligated to pay as

damages because of “injury” to which this insurance applies if liability for such“injury” is imposed on the insured by reason of the selling, serving or furnishingof any alcoholic beverage. We will have the right and duty to defend the insuredagainst any “suit” seeking those damages. However, we will have no duty todefend the insured against any “suit” seeking damages for “injury” to which thisinsurance does not apply. We may, at our discretion, investigate any “injury”and settle any claim or “suit” that may result. But:

– The amount we will pay for damages is limited as described in Section III – Limits OfInsurance; and

– Our right and duty to defend ends when we have used up the applicable limit ofinsurance in payment of judgments or settlements.

• No other obligation or liability to pay sums or perform acts or services is coveredunless explicitly provided for under Supplementary Payments.

• This insurance applies to “injury” only if:– The “injury” occurs during the policy period in the “coverage territory”.

For BYO – would need to attach CG 24 06LIQUOR LIABILITY – BRING YOUROWN ALCOHOL ESTABLISHMENTS

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

LIQUOR LIABILITY – BRING YOUR OWN ALCOHOLESTABLISHMENTS – CG 24 06

• LIQUOR LIABILITY COVERAGE PART• The following is added to Paragraph 1. Insuring

Agreement of Section I – Liquor Liability• Coverage:• 1. Insuring Agreement• An insured who permits any person to bring any

alcoholic beverage on their premises, for consumption on the premises, whether or not a fee is charged for such activity, will also be considered selling, serving or furnishing alcoholic beverages.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 11

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

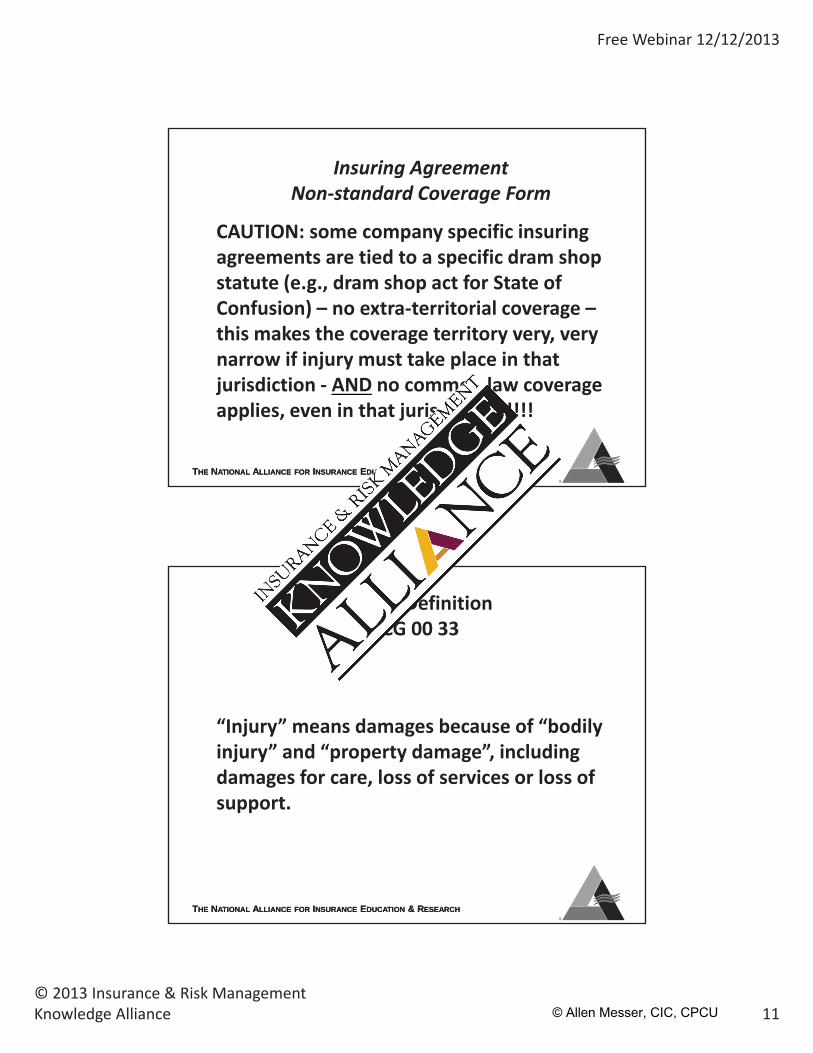

Insuring AgreementNon standard Coverage Form

CAUTION: some company specific insuringagreements are tied to a specific dram shopstatute (e.g., dram shop act for State ofConfusion) – no extra territorial coverage –this makes the coverage territory very, verynarrow if injury must take place in thatjurisdiction AND no common law coverageapplies, even in that jurisdiction!!!!!

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Injury DefinitionCG 00 33

“Injury” means damages because of “bodilyinjury” and “property damage”, includingdamages for care, loss of services or loss ofsupport.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 12

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

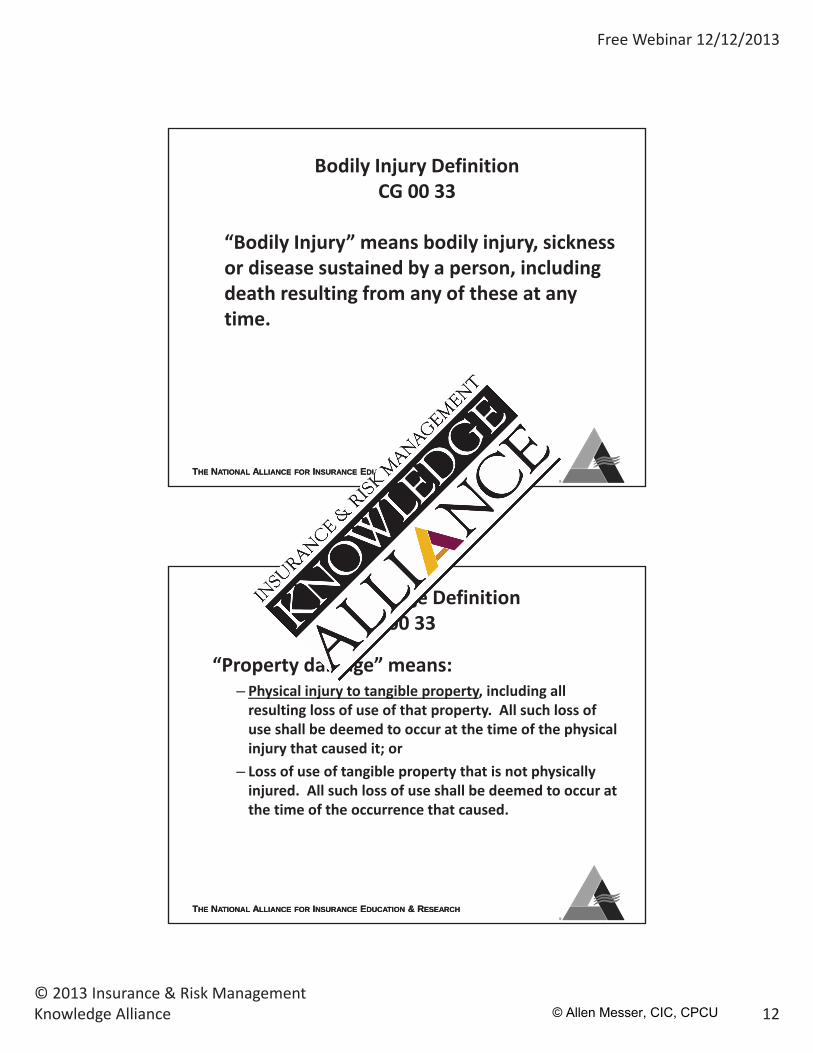

Bodily Injury DefinitionCG 00 33

“Bodily Injury” means bodily injury, sicknessor disease sustained by a person, includingdeath resulting from any of these at anytime.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Property Damage DefinitionCG 00 33

“Property damage” means:– Physical injury to tangible property, including allresulting loss of use of that property. All such loss ofuse shall be deemed to occur at the time of the physicalinjury that caused it; or

– Loss of use of tangible property that is not physicallyinjured. All such loss of use shall be deemed to occur atthe time of the occurrence that caused.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 13

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

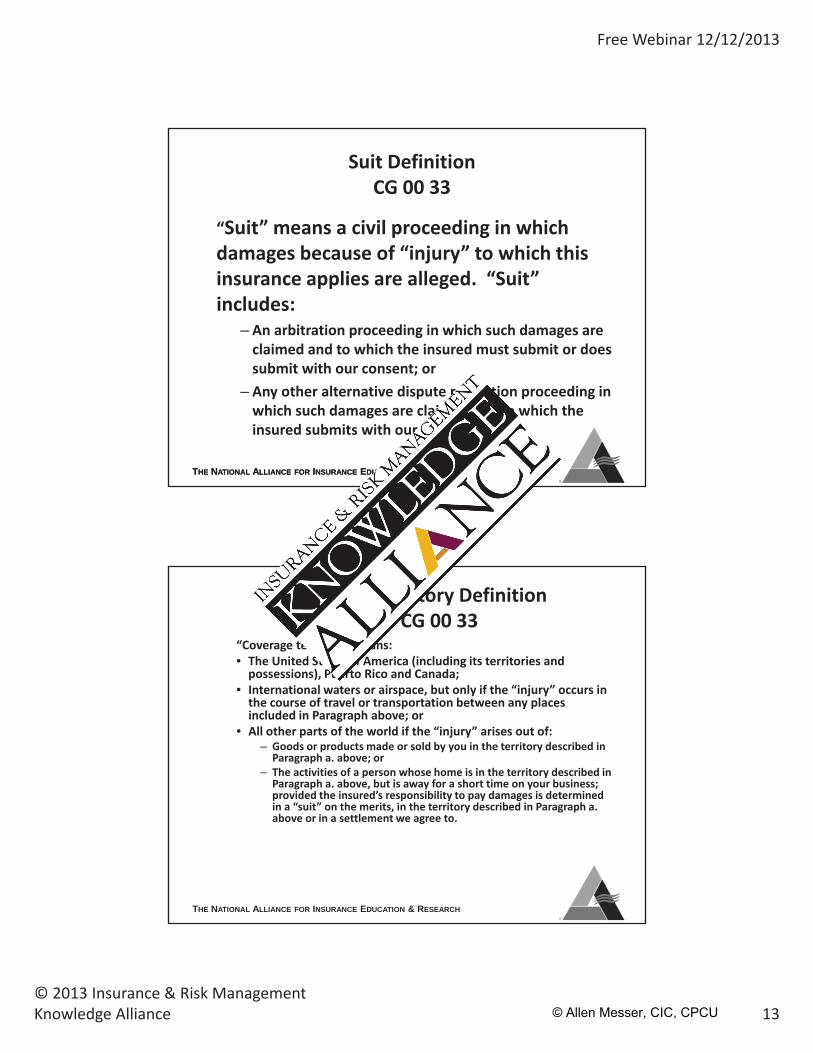

Suit DefinitionCG 00 33

“Suit” means a civil proceeding in whichdamages because of “injury” to which thisinsurance applies are alleged. “Suit”includes:

– An arbitration proceeding in which such damages areclaimed and to which the insured must submit or doessubmit with our consent; or

– Any other alternative dispute resolution proceeding inwhich such damages are claimed and to which theinsured submits with our consent.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Coverage Territory DefinitionCG 00 33

“Coverage territory” means:• The United States of America (including its territories andpossessions), Puerto Rico and Canada;

• International waters or airspace, but only if the “injury” occurs inthe course of travel or transportation between any placesincluded in Paragraph above; or

• All other parts of the world if the “injury” arises out of:– Goods or products made or sold by you in the territory described inParagraph a. above; or

– The activities of a person whose home is in the territory described inParagraph a. above, but is away for a short time on your business;provided the insured’s responsibility to pay damages is determinedin a “suit” on the merits, in the territory described in Paragraph a.above or in a settlement we agree to.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 14

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

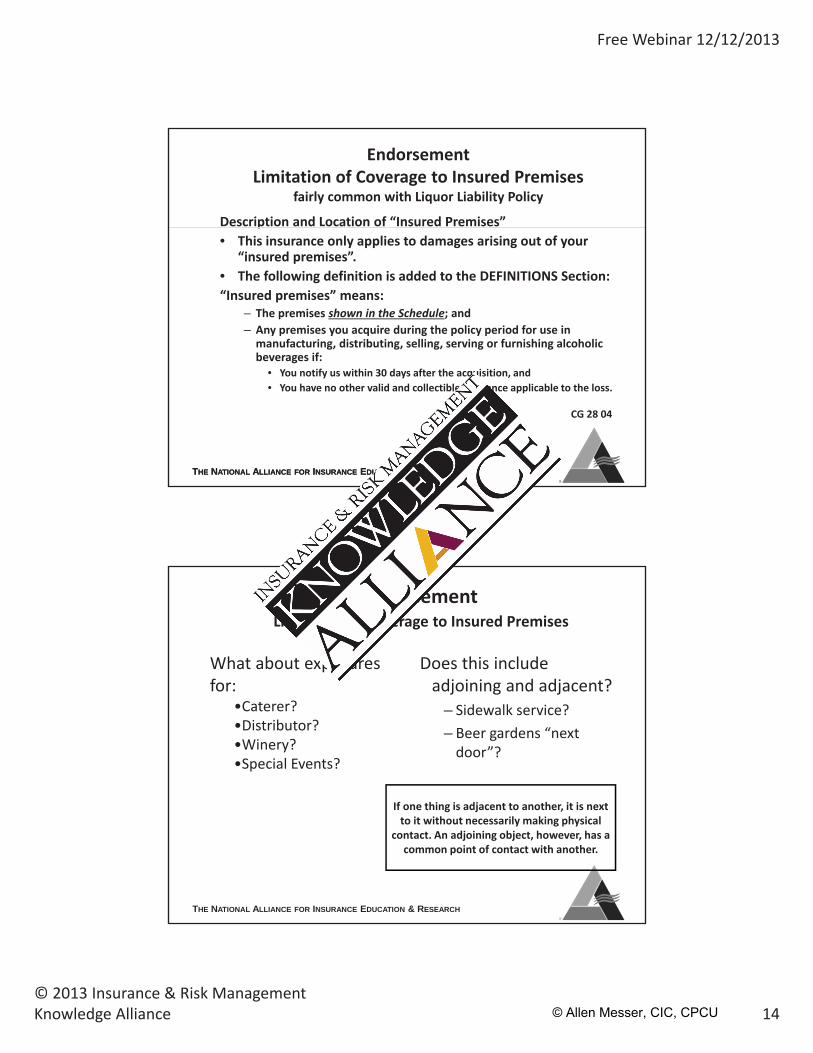

EndorsementLimitation of Coverage to Insured Premises

fairly common with Liquor Liability Policy

Description and Location of “Insured Premises”• This insurance only applies to damages arising out of your

“insured premises”.• The following definition is added to the DEFINITIONS Section:“Insured premises” means:

– The premises shown in the Schedule; and– Any premises you acquire during the policy period for use inmanufacturing, distributing, selling, serving or furnishing alcoholicbeverages if:

• You notify us within 30 days after the acquisition, and• You have no other valid and collectible insurance applicable to the loss.

CG 28 04

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

EndorsementLimitation of Coverage to Insured Premises

Does this includeadjoining and adjacent?

– Sidewalk service?– Beer gardens “nextdoor”?

What about exposuresfor:

•Caterer?•Distributor?•Winery?•Special Events?

If one thing is adjacent to another, it is nextto it without necessarily making physical

contact. An adjoining object, however, has acommon point of contact with another.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 15

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

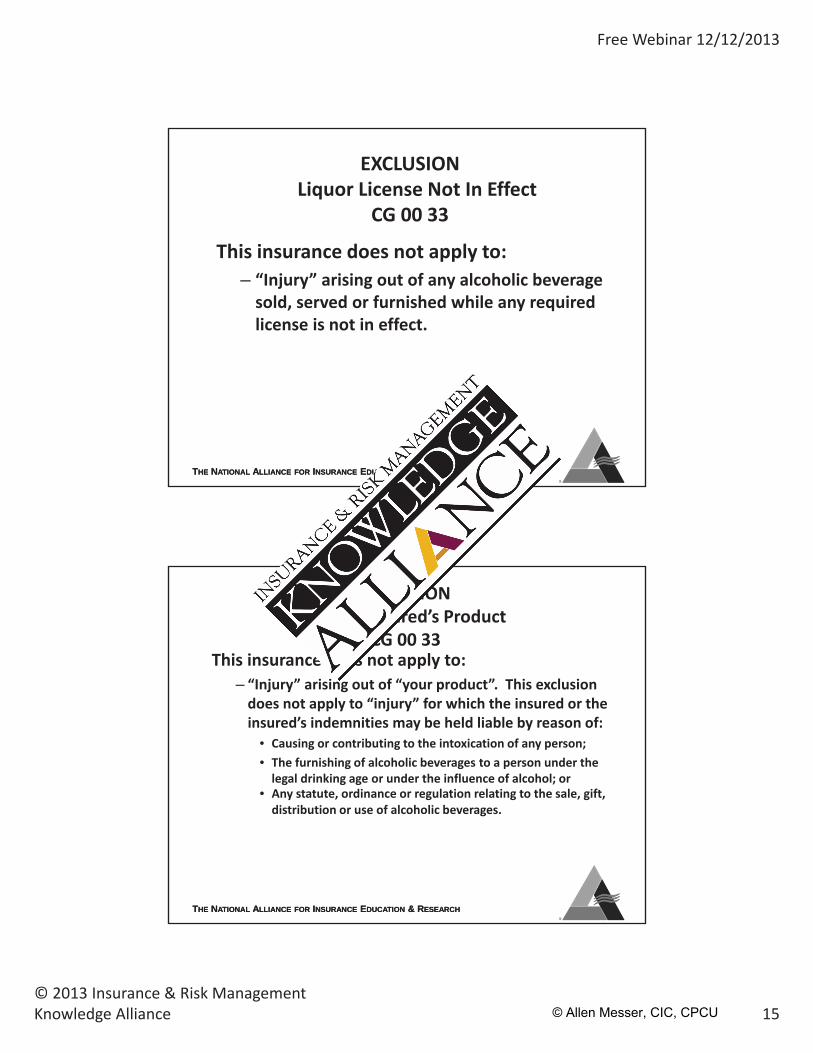

EXCLUSIONLiquor License Not In Effect

CG 00 33

This insurance does not apply to:– “Injury” arising out of any alcoholic beveragesold, served or furnished while any requiredlicense is not in effect.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

EXCLUSIONNamed Insured’s Product

CG 00 33This insurance does not apply to:

– “Injury” arising out of “your product”. This exclusiondoes not apply to “injury” for which the insured or theinsured’s indemnities may be held liable by reason of:

• Causing or contributing to the intoxication of any person;• The furnishing of alcoholic beverages to a person under thelegal drinking age or under the influence of alcohol; or

• Any statute, ordinance or regulation relating to the sale, gift,distribution or use of alcoholic beverages.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 16

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

EXCLUSIONOther Acts

This insurance does not apply to:–“Injury” caused directly or indirectly by any actof an “insured,” and “employee” of an“insured,” or anyone acting on behalf of an“insured” other than the selling, serving, orfurnishing of any alcoholic beverage.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

EXCLUSIONAssault and/or Battery

This insurance does not apply to:– “Injury” arising from or resulting from assault and battery orphysical altercations that occur in, on, near or away from theinsured’s premises as a result of the selling, serving or furnishing ofalcoholic beverages:

• Whether or not caused by, at the instigation of or with the direct orindirect involvement of the insured, the insured’s employees, patrons orother persons in, on, near or away from insured’s premises, or

• Whether or not caused by or arising out of the insured’s failure toproperly supervise or keep the insured’s premises in a safe condition, or

• Whether or not caused by or arising out of any insured’s act or omissionin connection with the prevention or suppression of the assault andbattery or physical altercation, including, but not limited to, negligenthiring, training and/or supervision.

• Whether or not caused by or arising out of negligent, reckless, or wantonconduct by the insured, the insured’s employees, patrons or otherpersons.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 17

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

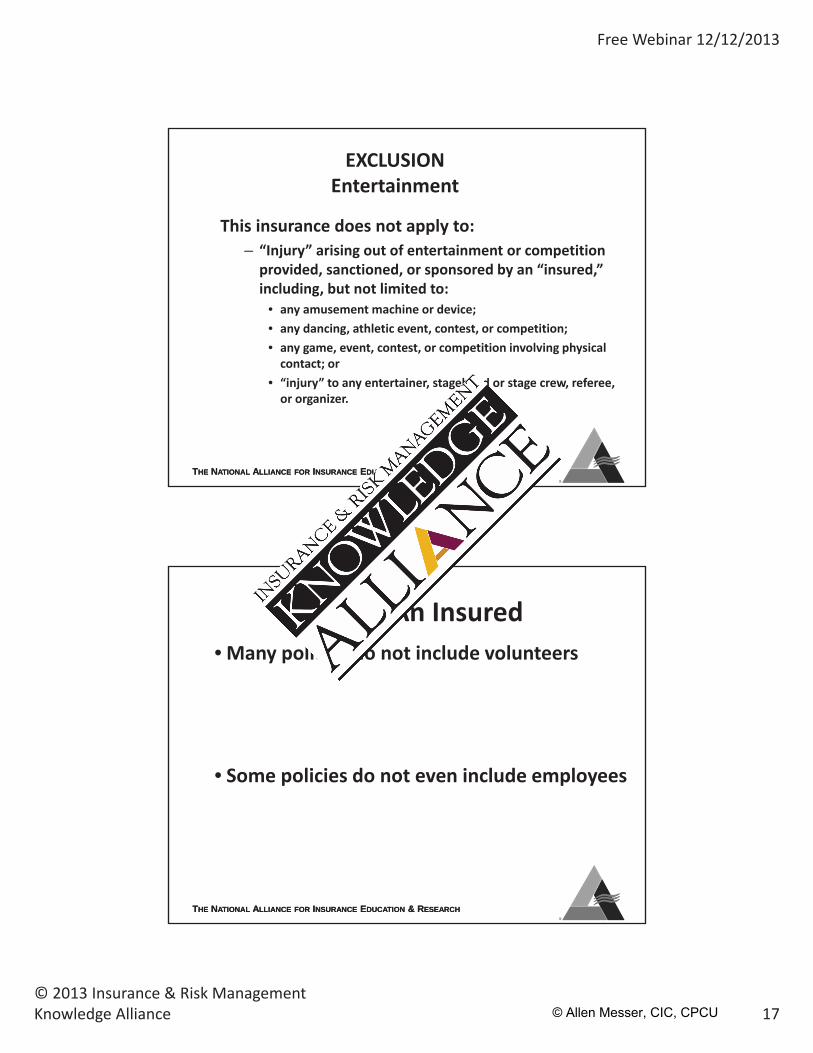

EXCLUSIONEntertainment

This insurance does not apply to:– “Injury” arising out of entertainment or competitionprovided, sanctioned, or sponsored by an “insured,”including, but not limited to:

• any amusement machine or device;• any dancing, athletic event, contest, or competition;• any game, event, contest, or competition involving physicalcontact; or

• “injury” to any entertainer, stagehand or stage crew, referee,or organizer.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Who Is An Insured• Many policies do not include volunteers

• Some policies do not even include employees

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 18

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

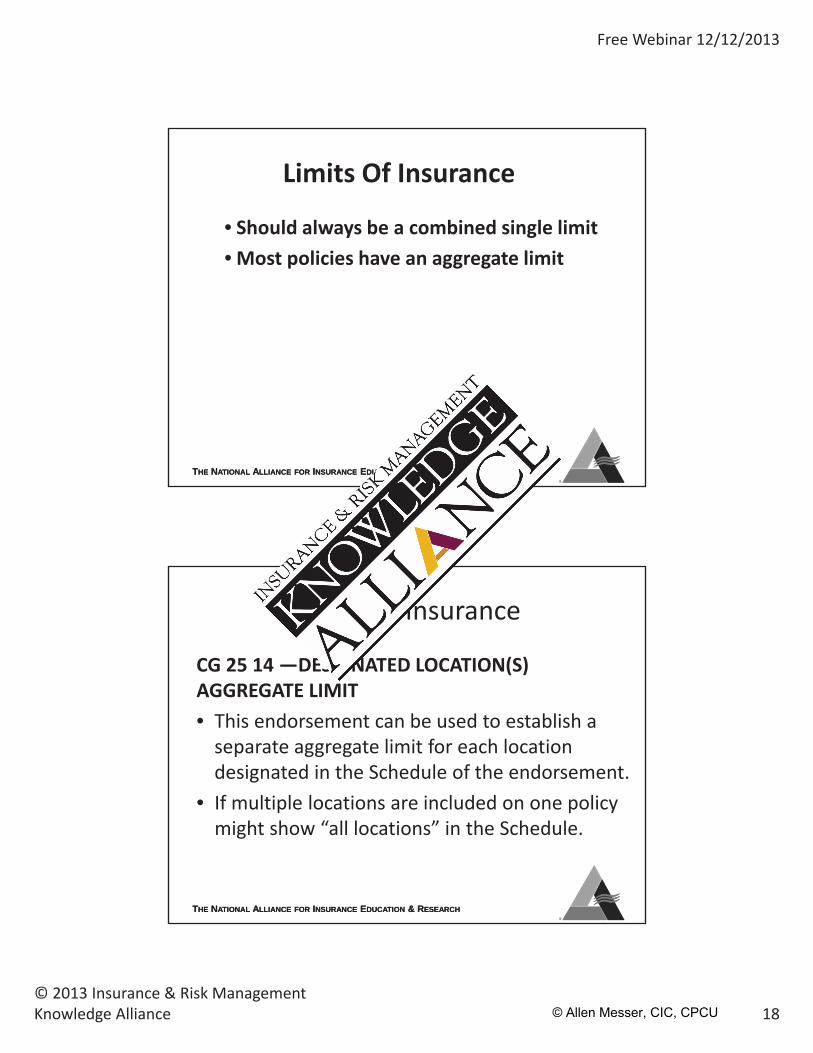

Limits Of Insurance

• Should always be a combined single limit• Most policies have an aggregate limit

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Limits Of Insurance

CG 25 14 —DESIGNATED LOCATION(S)AGGREGATE LIMIT• This endorsement can be used to establish aseparate aggregate limit for each locationdesignated in the Schedule of the endorsement.

• If multiple locations are included on one policymight show “all locations” in the Schedule.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 19

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

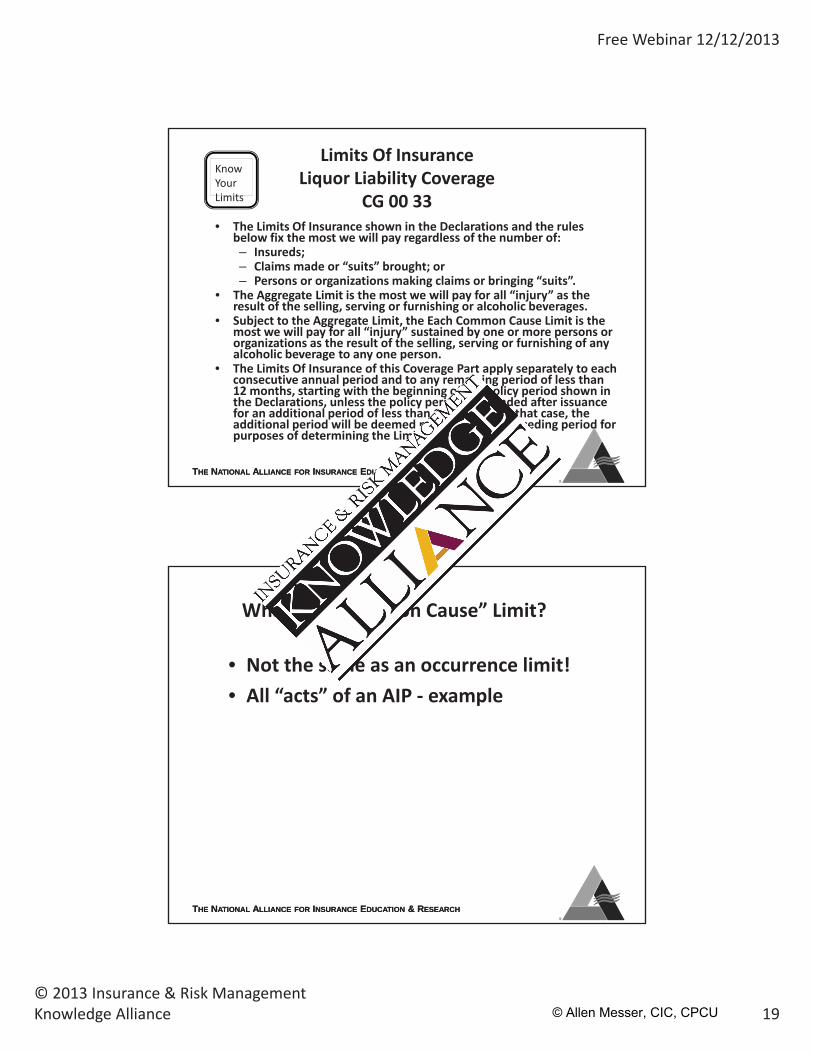

Limits Of InsuranceLiquor Liability Coverage

CG 00 33• The Limits Of Insurance shown in the Declarations and the rules

below fix the most we will pay regardless of the number of:– Insureds;– Claims made or “suits” brought; or– Persons or organizations making claims or bringing “suits”.

• The Aggregate Limit is the most we will pay for all “injury” as theresult of the selling, serving or furnishing or alcoholic beverages.

• Subject to the Aggregate Limit, the Each Common Cause Limit is themost we will pay for all “injury” sustained by one or more persons ororganizations as the result of the selling, serving or furnishing of anyalcoholic beverage to any one person.

• The Limits Of Insurance of this Coverage Part apply separately to eachconsecutive annual period and to any remaining period of less than12 months, starting with the beginning of the policy period shown inthe Declarations, unless the policy period is extended after issuancefor an additional period of less than 12 months. In that case, theadditional period will be deemed part of the last preceding period forpurposes of determining the Limits Of Insurance.

KnowYourLimits

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

What Is A “Common Cause” Limit?

• Not the same as an occurrence limit!• All “acts” of an AIP example

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 20

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

CONDITIONSLoss DutiesCG 00 33

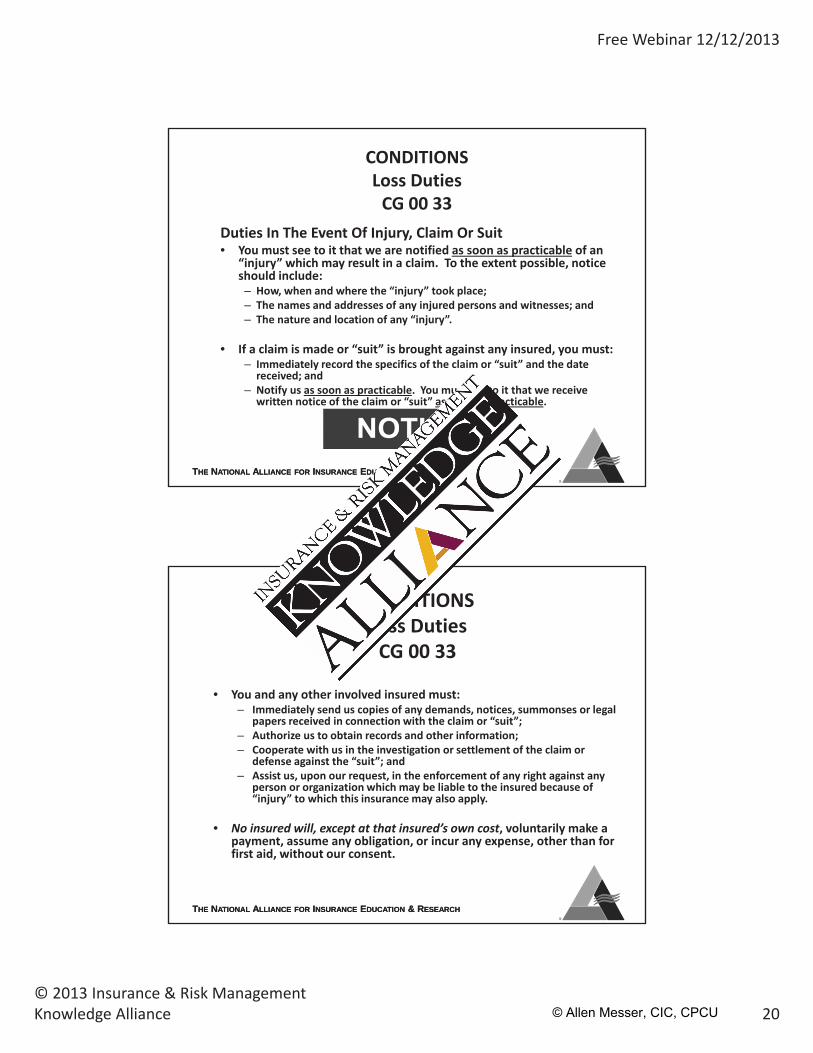

Duties In The Event Of Injury, Claim Or Suit• You must see to it that we are notified as soon as practicable of an

“injury” which may result in a claim. To the extent possible, noticeshould include:– How, when and where the “injury” took place;– The names and addresses of any injured persons and witnesses; and– The nature and location of any “injury”.

• If a claim is made or “suit” is brought against any insured, you must:– Immediately record the specifics of the claim or “suit” and the datereceived; and

– Notify us as soon as practicable. You must see to it that we receivewritten notice of the claim or “suit” as soon as practicable.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

CONDITIONSLoss DutiesCG 00 33

• You and any other involved insured must:– Immediately send us copies of any demands, notices, summonses or legal

papers received in connection with the claim or “suit”;– Authorize us to obtain records and other information;– Cooperate with us in the investigation or settlement of the claim or

defense against the “suit”; and– Assist us, upon our request, in the enforcement of any right against any

person or organization which may be liable to the insured because of“injury” to which this insurance may also apply.

• No insured will, except at that insured’s own cost, voluntarily make apayment, assume any obligation, or incur any expense, other than forfirst aid, without our consent.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 21

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

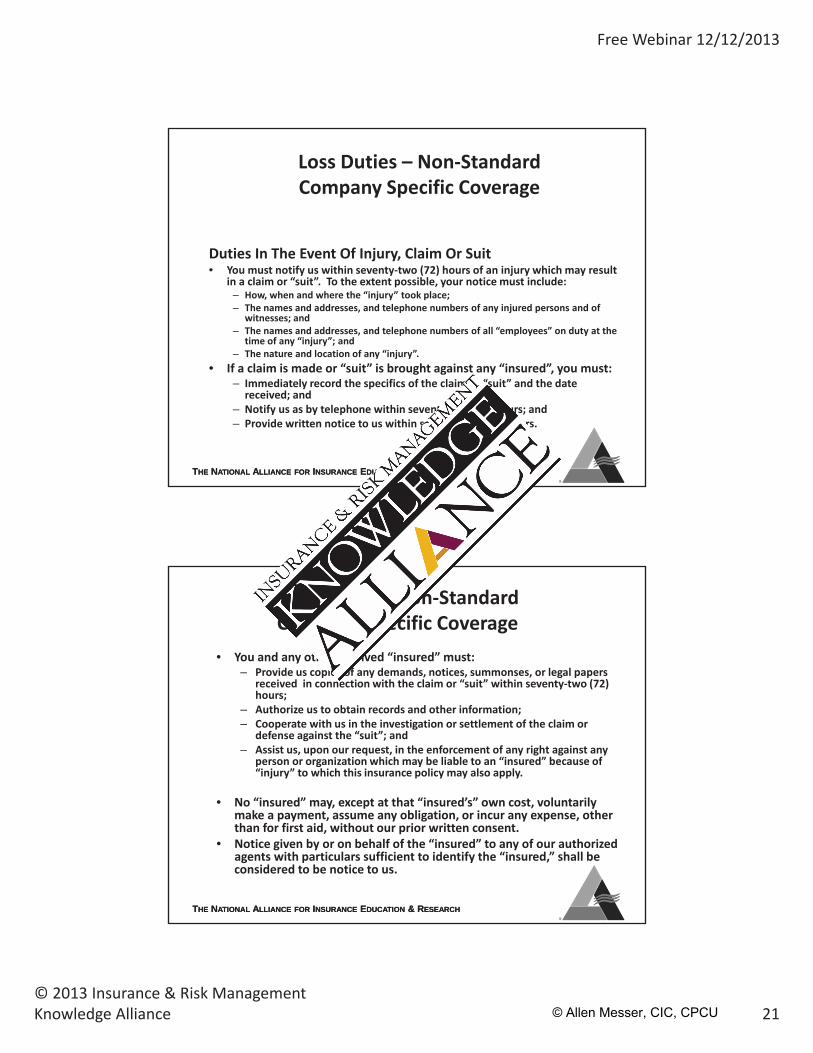

Loss Duties – Non StandardCompany Specific Coverage

Duties In The Event Of Injury, Claim Or Suit• You must notify us within seventy two (72) hours of an injury which may result

in a claim or “suit”. To the extent possible, your notice must include:– How, when and where the “injury” took place;– The names and addresses, and telephone numbers of any injured persons and of

witnesses; and– The names and addresses, and telephone numbers of all “employees” on duty at the

time of any “injury”; and– The nature and location of any “injury”.

• If a claim is made or “suit” is brought against any “insured”, you must:– Immediately record the specifics of the claim or “suit” and the datereceived; and

– Notify us as by telephone within seventy two (72) hours; and– Provide written notice to us within seventy two (72) hours.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Loss Duties – Non StandardCompany Specific Coverage

• You and any other involved “insured” must:– Provide us copies of any demands, notices, summonses, or legal papers

received in connection with the claim or “suit” within seventy two (72)hours;

– Authorize us to obtain records and other information;– Cooperate with us in the investigation or settlement of the claim or

defense against the “suit”; and– Assist us, upon our request, in the enforcement of any right against any

person or organization which may be liable to an “insured” because of“injury” to which this insurance policy may also apply.

• No “insured” may, except at that “insured’s” own cost, voluntarilymake a payment, assume any obligation, or incur any expense, otherthan for first aid, without our prior written consent.

• Notice given by or on behalf of the “insured” to any of our authorizedagents with particulars sufficient to identify the “insured,” shall beconsidered to be notice to us.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 22

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

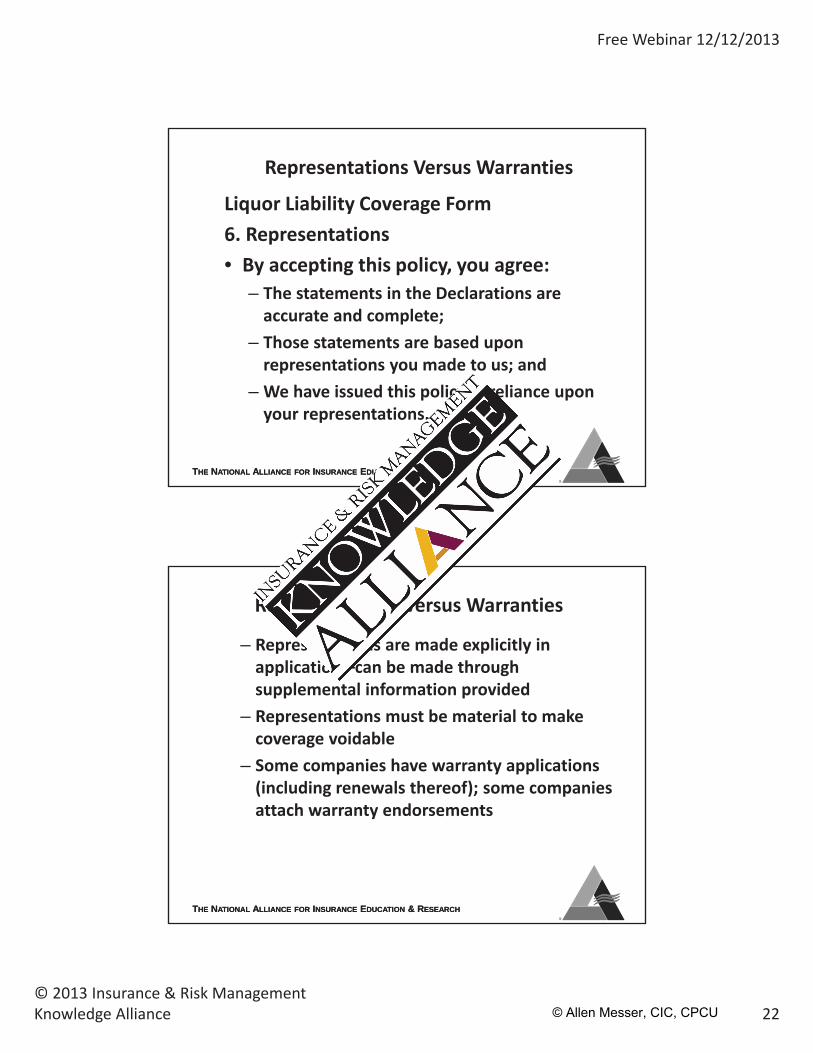

Representations Versus Warranties

Liquor Liability Coverage Form6. Representations• By accepting this policy, you agree:

– The statements in the Declarations areaccurate and complete;

– Those statements are based uponrepresentations you made to us; and

– We have issued this policy in reliance uponyour representations.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Representations Versus Warranties

– Representations are made explicitly inapplication –can be made throughsupplemental information provided

– Representations must be material to makecoverage voidable

– Some companies have warranty applications(including renewals thereof); some companiesattach warranty endorsements

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 23

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

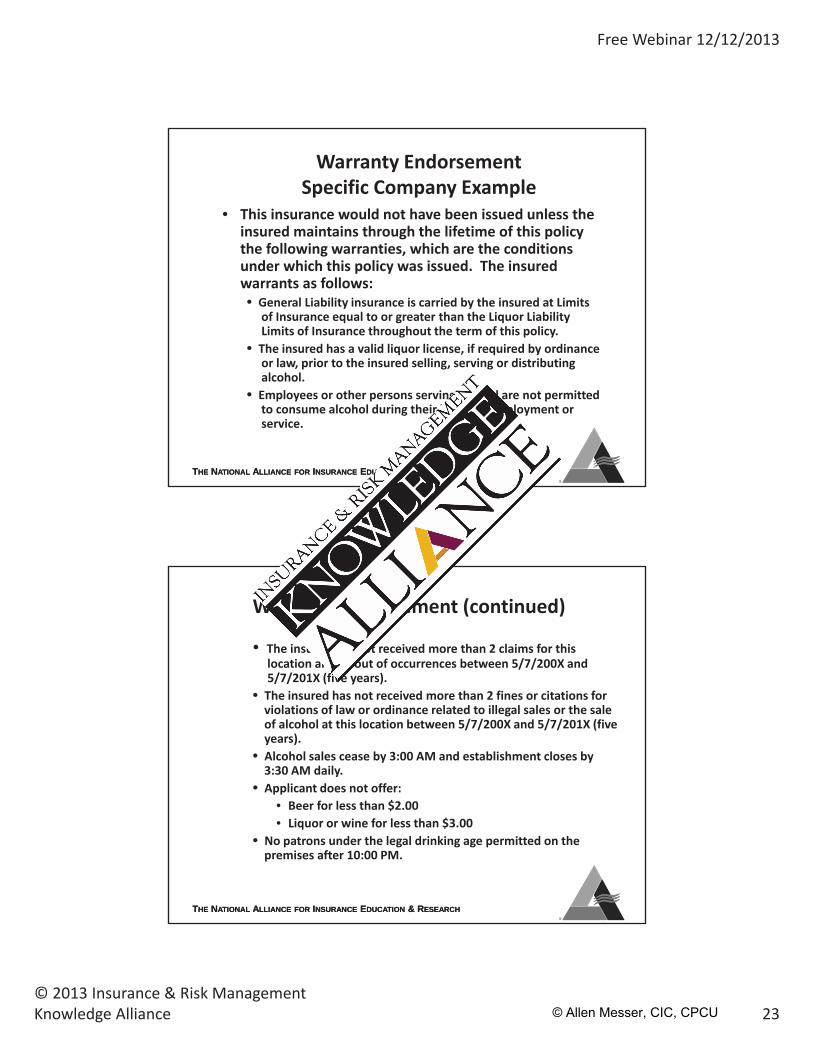

Warranty EndorsementSpecific Company Example

• This insurance would not have been issued unless theinsured maintains through the lifetime of this policythe following warranties, which are the conditionsunder which this policy was issued. The insuredwarrants as follows:

General Liability insurance is carried by the insured at Limitsof Insurance equal to or greater than the Liquor LiabilityLimits of Insurance throughout the term of this policy.The insured has a valid liquor license, if required by ordinanceor law, prior to the insured selling, serving or distributingalcohol.Employees or other persons serving alcohol are not permittedto consume alcohol during their hours of employment orservice.

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

Warranty Endorsement (continued)

The insured has not received more than 2 claims for thislocation arising out of occurrences between 5/7/200X and5/7/201X (five years).The insured has not received more than 2 fines or citations forviolations of law or ordinance related to illegal sales or the saleof alcohol at this location between 5/7/200X and 5/7/201X (fiveyears).Alcohol sales cease by 3:00 AM and establishment closes by3:30 AM daily.Applicant does not offer:

• Beer for less than $2.00• Liquor or wine for less than $3.00

No patrons under the legal drinking age permitted on thepremises after 10:00 PM.

© Allen Messer, CIC, CPCU

Free Webinar 12/12/2013

© 2013 Insurance & Risk ManagementKnowledge Alliance 24

THE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCHTHE NATIONAL ALLIANCE FOR INSURANCE EDUCATION & RESEARCH

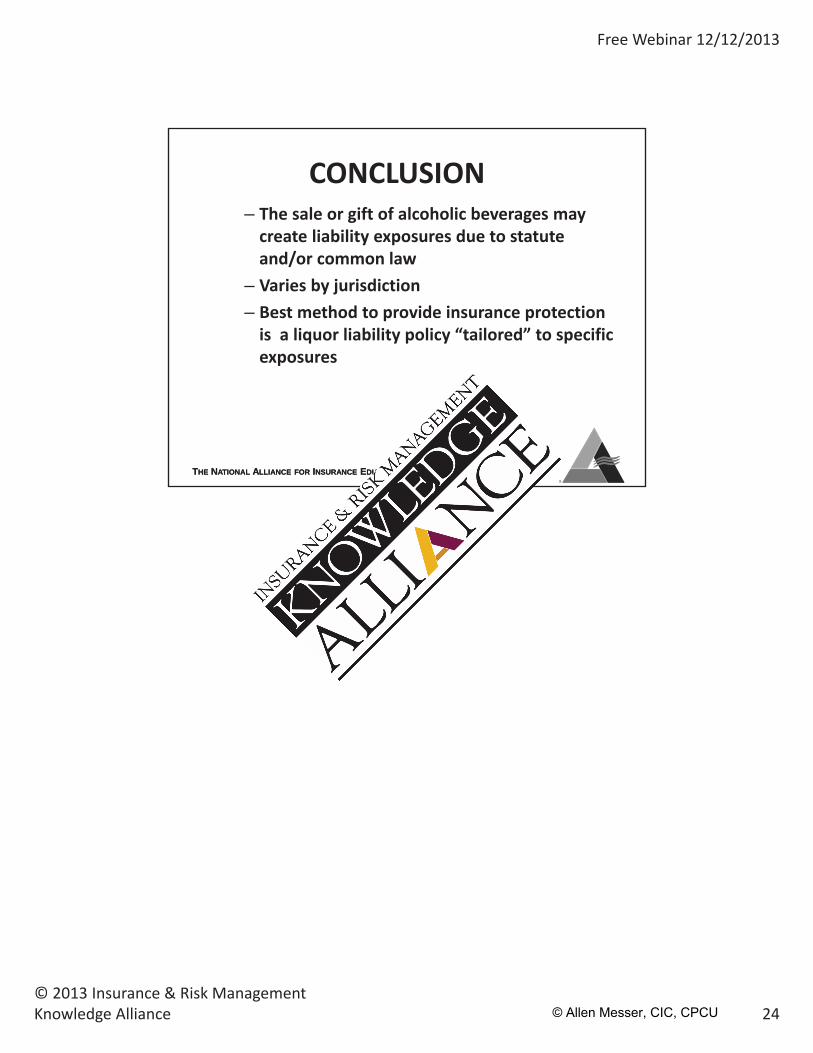

CONCLUSION– The sale or gift of alcoholic beverages maycreate liability exposures due to statuteand/or common law

– Varies by jurisdiction– Best method to provide insurance protectionis a liquor liability policy “tailored” to specificexposures

© Allen Messer, CIC, CPCU