Embed Size (px)

Citation preview

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 1/32

CHAPTER – I

INTRODUCTION

1.1 Evolution of the Bank

Banks are among the most important financial institution in the economy andessential for business in thousands of local towns and cities.A Bank is anorganization whose primary functions are concerned with accumulation of idlemoney from general public and advancing loans to individuals, traders, industriesand business houses for expenditure.Generally, the bank collect money fromgeneral public for which it should pay interest regularly.The money thusaccumulated can be invested in different sectors such as business, foreigntrades,agriculture, industry and social works for which it charges certainpercentages of interest which is higher than interest paid by the bank to

accumulate fund.uch charges on advancing loan in the ma!or revenue source of the bank by which it can bear administration expenses incurring in the process of operating its activities.Thus, the bank is a good mediator between depositors andloan takers."

According to #ent $A bank is an organization whose principle operations areconcerned with the accumulation of the temporarily idle money of the generalpublic for the purpose of advancing to other for expenditure.%

&ence, the bank may be summarized as an institution which excepts depositsfrom the public and advance loans by creating money.There is no unanimity

amoung the economists about the origin of the word $Banking'.The term bankwas derived from the (atin word bancus,which refers to the bench on which thebankers would keep its money and records.&istory tells us that it was themerchant bankers who first involved the system of banking by trading incommodities than money. The next stage in the growth of banking was theGoldsmith.)inally,money lenders in the early age also contributed in the growthof banking in a large extent.Thus, it is believed that the ancestors of modernbanking system were merchants, Goldsmith and money lenders.The bank calledthe $Bank of *enice% was established in *enice, +taly in - was regarded as thefirst modern bank.ubse/uently, following its establishments various banks suchas the Bank of Barcelona 0123, Bank of Geneva 0123, Bank of Amsterdam

04253, Bank of &industan 023 were established.

6abil Bank (imited was established in 724 B.. 6abil bank was the first !ointventure with 8ubai bank (imited of 9nited Arab :mirates.The second !ointventure bank was 6epal +ndosuez Bank.+t was established in falgun 724; under the collaboration with +ndosuez Bank of <aris. +n =agh 4 ,724;, 6epal GrindleysBank was establised under the collaboration with the Grindleys Bank of (ondon.As the country follower liberalization, there was massive entrance of

(i/uidity <osition of 6abil Bank 1

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 2/32

foreign banks as a !oint *enture with &abib bank (imited, <akistan, 6epal B+bank as the !oint venture with the state bank of +ndia, 6epal Bangladesh Bank asthe !oint venture with +nternational finance investment and commercial bank of 8haka, 6epal bank of >eylon as the !oint venture with the bank of >eylon of rilanka are the example of expansion of banking industry in 6epal.

1.1.1 Concept of Bankin

Banking is a business much like any other business. The commercial bank isrelatively business concern. A bank provides certain services for its customer 08epositors and Borrowers3 and in return, receives payment in one form or other.+t tries to earn profit for its stock owners.

?.. ayers defined the bank as, $@rdinary banking business consists of changing cash for bank deposits and bank deposits for cash transferring bankdeposits from one person or corporation to anothergiving bank deposits in

exchange, government bonds, the secured or unsecured promises of business torepay etc.

According to 6epal commercial Bank Act 72, $A commercial Bank refers tosuch type of bank which deals in money exchange, accepting deposit, advancingloans and other commercial transactions other than one special functionsperformed by specified banks. uch as coCoperatives, agriculture and industrialbanks.%

Thus, from above definition, we can say that if any institution fulfills the followingconditions, it will satisfy the definition of banking company D

. Accepting of deposits from the public or other source, reCpayable ondemand or otherwise.

7. The deposit must be withdrawn by che/ues, draft and order or otherwise.. :ven money accepted as deposit must be for the purpose of lending or

investing, making advance and investment of fund are e/ually importantfunctions.

1. >ommercial bank also provides miscellaneous services like letter credit,travelerEs che/ue.

1.1.! Develop"ent of #inancial In$titution in Nepal

+n respect of formation of financial institutions in the 6epal, simple lending andborrowing functions existed during the regime period. +n 1 th century, kingFayasthiti =alla divided the people in 41 casts on the basis of their professions.@ne on them was named $Tankadari% who used to perform simple lending andborrowing functions.

(i/uidity <osition of 6abil Bank 2

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 3/32

8uring the period of ?ana prime =inister ?anodeep,%Ta!arath Adda% wasestablished to provide loan facility to government staffs and general public under the collateral of gold and silver in the term of - percent interest 05 B.517B..3

There were moneylenders known as =arwari merchant,Faminder, Goldsmiths,ahu and <awan Brokers etc.They still exist in some remote part of nation.+ndiancurrency was accumulated in Terai Area. &undi functions had been done throughmerchants.

$ainik 8ravya #osh% was established in 55 B.. specially established for thefuture welfare of government staff and sainiks only.ince 725 B.. #armacharianchaya #osh has been performing more functions than ainik 8ravya #osh togive facility not only to the staff of government but also to the staff of corporation.

+n 6epal, the introduction of modern banking activities had been traced back to

551 B.. 05A.8.3 when the 6epal Bank Act 72 was first <romulgatedduring the period of <rime =inister Fuddha hamsher. Before that the creditneeds or people for commercial and other purpose were mostly fulfilled by theunorganized market of private money lenders.

+n 722 B.., there was great political change.6epal ?astra Bank, central bank of 6epal was established in 72; B.. with authorized capital of 6?s.2222222.imilarly, ?astriya Bani!iya Bank as the second commercial bankof 6epal was established in 7277 B.. An +ndustrial Bank nearly 6epal +ndustrial8evelopment Bank 06+8>3 was established in 7221 B.., Agriculture8evelopment Bank 0A8B3 of 6epal established.

6abil Bank (imited was established in 721 B.. 6abil bank was the first !ointventure with 8ubai Bank (td. of 9nited Arab :mirates. The second !oint ventureband was 6epal +ndosuez Bank. +t was established in )algun 7217 under thecollaboration with +ndosuez bank <aris.+n =agh 4, 721, 6epal Grindleys Bankwas established under the collaboration with Grindleys Bank of (ondon.As thecountry followed economic liberalization, there was massive entrance of foreignbank in 6epla.The establishment o &imalayan Bank as a !oint venture with &abibBank (td. <akistan,6epal B+ Bank (td. as a !oint venture with +.).+.>. Bank (td.of Bangladesh, Bank of #athmandu as a !oint venture with Thailand Bank,:verest Bank as a !oint venture with <un!ab 6ational Bank, +ndia, 6epal Bank of >eylon as a !oint venture with Bank of >eylon of rilanka, are the example of expansion of Banking industry in 6epal.

1.1.% Bankin Develop"ent of Nepal

The history of banking in 6epal may be described as a component of the gradualand orderly evolution in the financial and economic spare of the 6epaleselife.:ven, now the finance system is still in the evolutionary phase.The existence

(i/uidity <osition of 6abil Bank 3

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 4/32

of unorganized money market consisting of (andlord, shahukars0richmerchants3,shopkeepers and other indigenous individual moneylenders hasacted as barrier to institutionalized credit.

imple lending and borrowing functions existed from Gunakamadev in the

(ichhavi period,;2 B..And in th

century, in king Fayasthiti =allasHs period$Tenkadhari% used to perform simple lending and borrowing functions.

8uring the ?ana prime =inister ship of ?anodip ingh $Te!arath Adda% wasestablished to provide loan facilities for government staffs and to general publicunder the collateral of gold and silver in the term of -I interest rate 055B..3There were money lenders known as =arawaris, Famindar, Goldsmith,Broker etc.They still exist in some remote part of the 6ation.

$ainik 8ravya #osh% was established in 5 B.. specially established for thefuture welfare of government staff and sainiks only.ince 725 B.. #armachari

anchaya #osh has been performing more functions than ainik 8ravya #osh togive facility not only to the staffs of government but also to the staffs of corporations.

+n 6epal, banking in the true sense of term started with the inspection of nepalBank (imited on 2th kartik,551 B..?ight for the inspection,it carried outfunction of commercial bank.6epal bank act 5 was st <romulgated during theprime ministership of Fuddha hamsher F.B.?. Before that the credit need for commercial and other propose were mostly be unrecognized market of theprivate money lenders.

6epal bank (td. had a &erculear responsibility of attracting people towardsbanking sector from preCdominant ahu maha!anHs transactions and of introducing other banking services as well. Being a commercial bank, it was butnatural that 6epal Bank (td. paid more attention to profit generating business.Butit is the one of government to look into neglected sectors too.%=uluki #hanna%which had banking perform some banking functions has issued notes of differentdomination such as ,7,2 and 22 rupees.

+n 722 B..,there was great political change.6epal ?astra Bank% as a centralbank of 6epal was established in 727 B.. with one crore of authorizedcapital.imilarly,?astriya Bani!iya Bank was established in 7277 B.. +n 724B.. with the view to develop the industrial sector.6epal +ndustrial developmentcorporation was established in 721 B..,Agriculture development bank bankwas established.ince the year 721 B..05;1 A.8.3 &=G of 6epal hasestablished five rural development banks.6epal commercial bank act 72B..05-A.8.3 has been amended several times in accordance with need.

+n order to establish and develop other !oint venture commercial banks and other financial institution came into existence.6epal adopted free economic policy,

(i/uidity <osition of 6abil Bank 4

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 5/32

&=G permitted the establishments of different !oint venture banks with foreigncollaborations. +n addition to those commercial banks other regional commercialbanks were also established.

6epal is one of the least developed country under the rank of poverty

line.Agriculture plays a crucial role in the 6epalese economy.The development of the bank in 6epal is in infant stage.+n this way the bank plays a primitive role for the economic development of 6epal.

1.! Int&o'uction of Na(il Bank )i"ite'

Before the introduction of 6abil Bank (td. in 5;1, the financial sectors of 6epalwas sluggish despite all the efforts of the government.The inception of 6epal

Arab Bank in 5;1 as a first !oint venture bank proved to be a milestone gave anew ray of hope to the sluggish financial year.

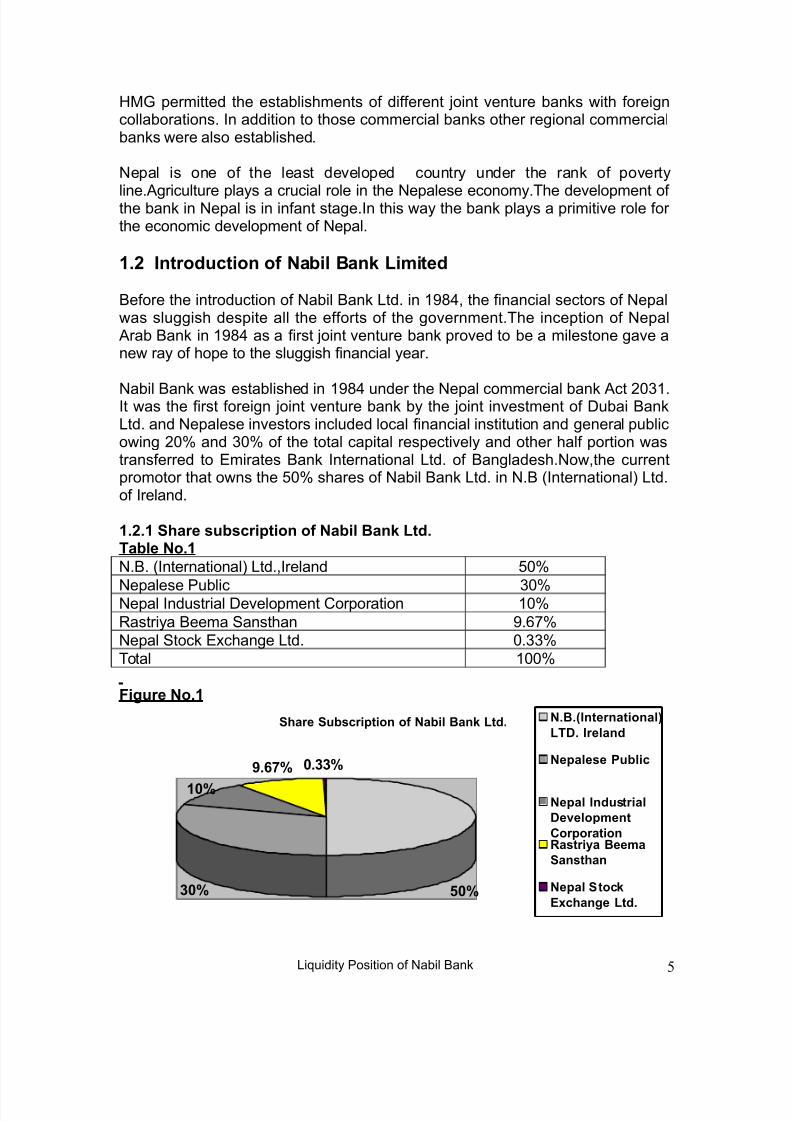

6abil Bank was established in 5;1 under the 6epal commercial bank Act 72.+t was the first foreign !oint venture bank by the !oint investment of 8ubai Bank(td. and 6epalese investors included local financial institution and general publicowing 72I and 2I of the total capital respectively and other half portion wastransferred to :mirates Bank +nternational (td. of Bangladesh.6ow,the currentpromotor that owns the -2I shares of 6abil Bank (td. in 6.B 0+nternational3 (td.of +reland.

1.!.1 *ha&e $u($c&iption of Na(il Bank )t'.Ta(le No.1

6.B. 0+nternational3 (td.,+reland -2I

6epalese <ublic 2I6epal +ndustrial 8evelopment >orporation 2I?astriya Beema ansthan 5.4I6epal tock :xchange (td. 2.ITotal 22I #iu&e No.1

*ha&e *u($c&iption of Na(il Bank )t'.

+.%%,-./,

0+,%+,

1+,

N.B.Inte&national2

)TD. I&elan'

Nepale$e Pu(lic

Nepal In'u$t&ial

Develop"ent

Co&po&ationRa$t&i3a Bee"a

*an$than

Nepal *tock

E4chane )t'.

(i/uidity <osition of 6abil Bank 5

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 6/32

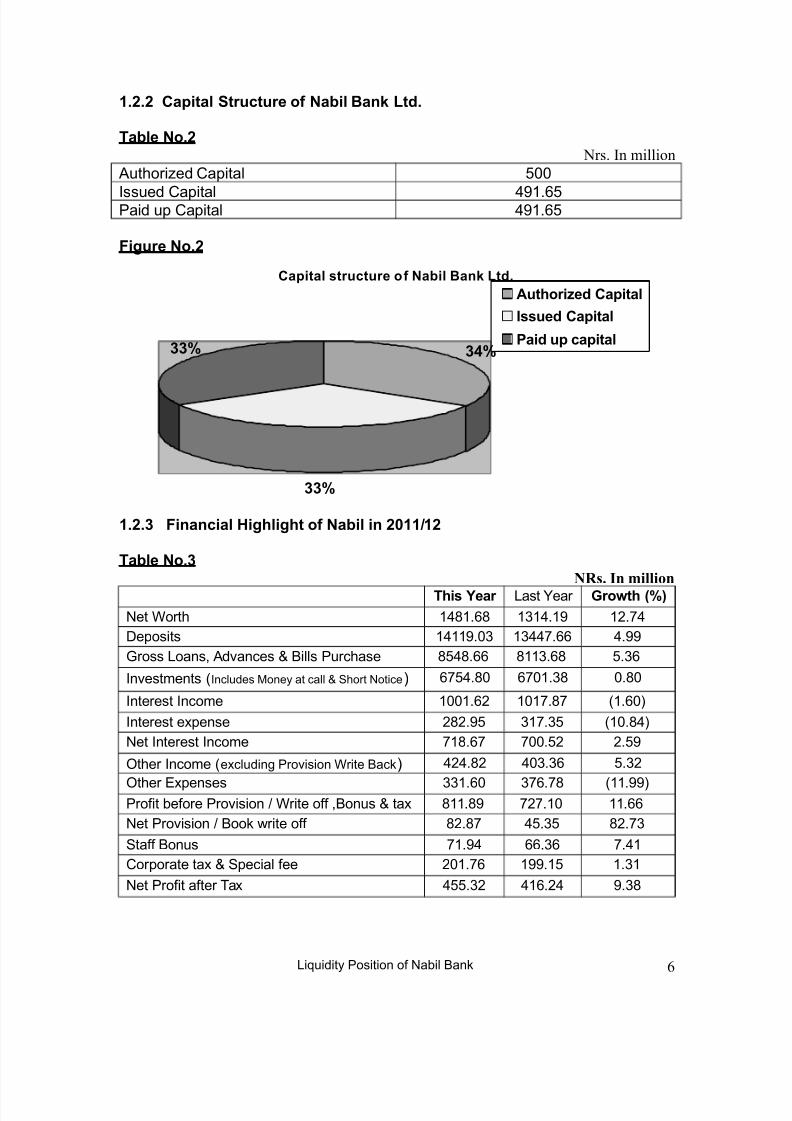

1.!.! Capital *t&uctu&e of Na(il Bank )t'. Ta(le No.!

Nrs. In million

Authorized >apital -22

+ssued >apital 15.4-<aid up >apital 15.4-

#iu&e No.!

Capital $t&uctu&e of Na(il Bank )t'.

%%,

%5,%%,

Autho&i6e' Capital

I$$ue' Capital

Pai' up capital

1.!.% #inancial Hihliht of Na(il in !+1171!

Ta(le No.%NRs. In million

Thi$ 8ea& (ast Jear 9&o:th ,2

6et Korth 1;.4; 1.5 7.18eposits 15.2 11.44 1.55Gross (oans, Advances L Bills <urchase ;-1;.44 ;.4; -.4

+nvestments 0+ncludes =oney at call L hort 6otice3 4-1.;2 42.; 2.;2

+nterest +ncome 22.47 2.; 0.423

+nterest expense 7;7.5- .- 02.;136et +nterest +ncome ;.4 22.-7 7.-5

@ther +ncome 0excluding <rovision Krite Back3 171.;7 12.4 -.7

@ther :xpenses .42 4.; 0.553<rofit before <rovision M Krite off ,Bonus L tax ;.;5 7.2 .446et <rovision M Book write off ;7.; 1-.- ;7.

taff Bonus .51 44.4 .1>orporate tax L pecial fee 72.4 55.- .

6et <rofit after Tax 1--.7 14.71 5.;

(i/uidity <osition of 6abil Bank 6

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 7/32

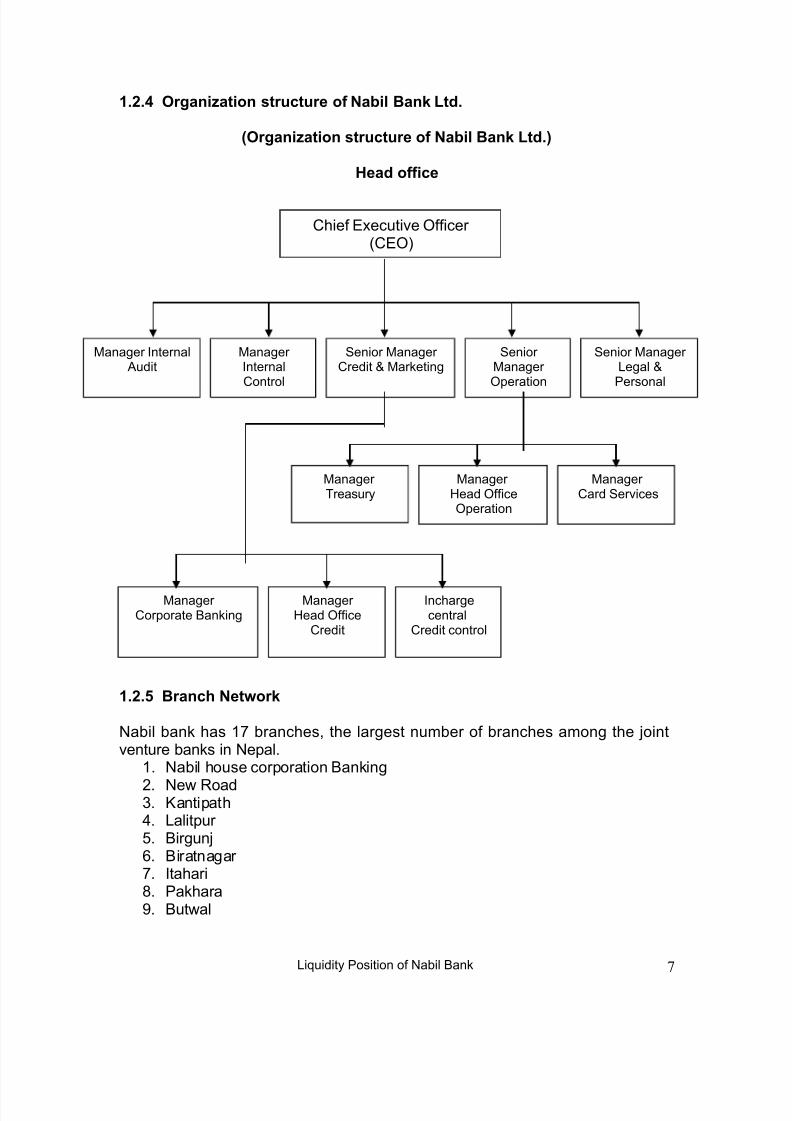

1.!.5 O&ani6ation $t&uctu&e of Na(il Bank )t'.

O&ani6ation $t&uctu&e of Na(il Bank )t'.2

Hea' office

1.!.0 B&anch Net:o&k

6abil bank has branches, the largest number of branches among the !ointventure banks in 6epal.

. 6abil house corporation Banking

7. 6ew ?oad. #antipath1. (alitpur -. Birgun!4. Biratnagar . +tahari;. <akhara5. Butwal

(i/uidity <osition of 6abil Bank 7

>hief :xecutive @fficer 0>:@3

=anager +nternal Audit

=anager +nternal>ontrol

enior =anager >redit L =arketing

enior =anager @peration

enior =anager (egal L<ersonal

=anagerTreasury

=anager&ead @ffice@peration

=anager >ard ervices

=anager >orporate Banking

=anager &ead @ffice

>redit

+nchargecentral

>redit control

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 8/32

2.<okhara (akeside. Bhairahawa7.Forpati.Bhalawadi1.6epalgun!

There are also two banking counters at 3 Airport and 73 Thamel.6abil wasplanning to open a branch office at #olkota but the capital re/uirement of reservebank of +ndia was high.Therefore,the proposal was dropped.The head office of 6abil Bank is situated at kamaladi,#athmandu.This head office coCordinate theactivities of 6abil Bank branches all over 6epal to provide better services to its*+< customer. @ne new branch is opened as corporate at round 2222depositors at 6abil bank and around 222 depositors at #amaladi branch.

1.!. P&o'uct an' $e&vice$ of Na(il Bank )t'.

6abil Bank is well known and famous for providing highly personalized servicesto customers. +t provides full range of commercial banking services through itsbranch network nation wide.To extend more efficient services to its customers,6abil Bank has been adopting innovation and latest banking technology.6abilBank provides the following services D

1.!..1 Depo$it;

)ollowing types of accounts can be opened at any 6abil branches uponcompletion of simple documentary re/uirement.All the accounts can be openedin various currencies 0against which rates are provided3 sub!ect to rule of openingand fulfilling the re/uired documents. aving >urrent )ixed >all

1.!..! 9ua&antee$;

6abil bank issues guarantees and Bonds on behalf of customers to thebeneficiaries in 6epal.9pon fulfillment of re/uirement, 6abil also arrangesinsurance of guarantees in the name of foreign beneficiaries through the reputed

+nternational banks.

1.!..% C&e'it Ca&'$D

6abil is the first bank in 6epal to issue ?upee 0valid in 6epal and +ndia3 and+nternational 0valid worldwide3 master card in 6epal, a global prestigious servicesto its esteemed clients.6abil is also expanding credit card facilities by issuingvisa credit cards very soon.

(i/uidity <osition of 6abil Bank 8

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 9/32

1.!..5 Tele (ankin;

Telephone bank is another product provided by 6abil bank to its customer, under this aggrement, customer can know the balance of hisMher account through

telephone without human assistance.1.!..0 <e$te&n Union =one3 T&an$fe&;

6abil bank has established uni/ue money remittance system with Kestern 9nionmoney remittance system where by money can be remitted anywhere in theworld within minutes. Through onCline computer system funds can be transferredinstantly to about --22 location in 4- countries of the world.

6epalese wage earners can send money to their near and dear ones in 6epalwithin a very short time.By using the above services, you can now send and

receive money within minutes in 4- countries in the world.1.!.. *:ift *ociet3 fo& :o&l':i'e Inte& Bank #inancial Teleco""unication2;

6abil has standard worldwide transfer of funds by this fast and efficient fundtransfer and messaging system. =essaging and funds transfer and carriedthrough K+)T with minimum time and cost.

1.!../ *afe Depo$it )ocke&;

6abil has provided safe deposit (ocker to keep value safety at a minimumcost.<resently, this facility available at kantipath offfice.

1.!..> Auto"ate' Telle& =achine AT=2;

6abil has launched the AT= to its account holders to enable fast withdrawal of funds.An account holder need not wait a long hours for withdrawing money andsign che/ues any more.A simple card with a uni/ue <+6 number known only tothe account holder will suffice.

1.!..- Othe& facilitie$;

The bank provide the facilities for the customers like deposit the service loansand advances,consumer finance, cash management remittance service etc.

1.!./ Int&o'uction to )i?ui'it3

(i/uidity <osition of 6abil Bank 9

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 10/32

(i/uidity is defined as banks capacity to exchange cash for deposits.+n other words,li/uidity is bank capacity to meet immediate maturing liabilities.<ublic puttheir money with a hope that bank repays it as demanded by them. This is thegreat trust of public to the bank.+f the bank fails to repay the money on demand,in such a situation bank may loose the public trust towards the bank and even

very strong banks may collapse.>onsidering this fact,bank should maintainenough li/uidity to meet the demands.A bank needs li/uidty for transactionmotive,precaution of security motive and speculative motive.

1.!.> I"po&tance of )i?ui'it3

The li/uidity management function of bank is regular one.:ach and every bankmust attach with great importance of li/uidity for maintaining confidence of customer and its survival.The importance of li/uidity management are as follows

1.!.>.1 To "eet the e4pen$e$ fo& the (ank$ 'ail3 a'"ini$t&ative :o&k;

A bank is a legal person.+t canHt run without cash book.The transaction of thebank is related to the money.many types of expenses go on taking place in thebank daily.Kith the lack of expenses, it is nearly impossible for the bank to do itstransaction.o the li/uidity is necessary for daily expenses that it is spent in theadministrative functions.The administrative expenditure canHt be fulfilled withoutli/uidity.&ence, li/uidity is important for the banks.

1.!.>.! To pa3 all $o&t$ if 'epo$it$; A bank opens the current, saving and fixed account for its customers and acceptthe deposit from the customers.According to the nature of deposit, the banksshould pay in the time when the customers asks.

1.!.>.% To cont&ol the econo"ic fluctuation an' to keep $afe f&o" the &i$k;+t canHt be said, there will be the same situation of transaction in the bank willalways remain in balanced conditions. There will be effect of internal and externalcircumstance in the nation.uch condition may have effect on economicsector.There is necessity of li/uidity to keep the bank free from such economicrise and fall or economic crisis.The bank should maintain some li/uidity of somecertain percent cash fund to keep sage from such situation.

1.!.>.5 To fulfill the 'e"an' of 'e(to&$; A bank provides loan to debtors.The bank earns income from it.=any kinds of people come to the banks with the purpose of loan.After the loan is granted,thebank is obliged to give the loan to the debtor.Therefore, there is necessity of li/uidity in bank to provide fresh loan to the debtors.

(i/uidity <osition of 6abil Bank 10

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 11/32

1.!.>.0 To ain t&u$t of faith; A bank has a great responsibility because of the financial institution that doesmonetary transaction.+t must gain trast of its banking transaction.)or this, a bankshould do many types of function.+t has to pay attention to the time and the will of

the customers to provide the banking services.)or the name and fame, a bankshould earn the trust from the public including other sectors.

1.!.- C&ite&ia fo& "ea$u&in (ank li?ui'it3

+t is very important to study criteria for measuring bank li/uidity.The bank li/uidityis the most important aspect of a bank.+f there is less bank li/uidity, the bankcannot be run.+f there is much li/uidity, the bank should bear great losseconomically.The bank should be able to keep the li/uidity in balance.There arecertain criteria forwarded by 6epal ?astra bank,the central bank of 6epal by

which li/uidity position of each and every commercial bank as a individualisticview as well as whole can be measured.&owever, the bank li/uidity can bemeasured by the following ratiosD

1.!.-.1 Depo$it Inve$t"ent Ratio;Ke can measure the li/uidity by the deposit investment ratio.The depositorydeposit the cash in current,saving and fixed accounts.The bank receives themost li/uid as deposits.The bank invests the capital collected by the depositors inthe various profitable and productive sector in the form of loan.By earning muchprofit from it, the bank can get a lot of amount from the amount of deposit.Thebank has the nature of paying low interest to the depositors and taking higher interest from the place it invested. And the bank canHt invest all the cash onloan.A part from the deposit invested, the bank also has other cash.Ke can findout the criteria of li/uidity from it,

1.!.-.! #iel' of Inve$t"ent ;The criteria of measuring li/uidity in a bank depends on the type of assets whichthe bank has made investment. The bank does not waste cash stock receivedfrom different sources of capital.The bank can invest the money, it posses indifferent types of assets.uch as house,land for the bank and other permanentshort of assets.+n such condition,the bank has low li/uidity because theinvestment made in such nature of assets needs much cash.And the bank gainincome very low for such nature of assets.But in contrast to it, if the bank hasinvested in the share of various companies, the investment in governmentsecurities and treasury bills and in the debentures of different businessinstitution, bank li/uidity is abundant.+n this way, the investment that the bankdeed can be used the criteria of measuring li/uidity.

(i/uidity <osition of 6abil Bank 11

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 12/32

1.!.-.% Ca$h Re$e&ve Ratio;The cash reserve ratio too can be taken as criteria of measuring bankli/uidity.The commercial bank should maintain the cash reserve ratio as fixed bythe central bank and also should maintain the statutory li/uidity ratio, in its own

treasury. +t change from time to time.Ke can measure the bank li/uidity from thistoo.

1.!.-.5 P&ofita(lit3;+t is the another criteria for measuring banks li/uidity position.+n case of higher profitability ratio, the li/uidity position will be higher whereas a lower profitabilityratio then the li/uidity will be lower.

1.!.-.0 Inve$t"ent in loan;The bank distributes loans in different sectors.The source of loan investment isimportant for the various source of income of the bank.+t is important to know

what sort of loan and how much loans the bank has distributed while the bankdistributes the loan.+f the bank is identified with the concept of gaining profit,thebank flows loan on a long term and mid term basis.+f it has paid its attention tothe safety it invest in short term loan.+f a great deal of amount is invested in theshort term loan,the bank retains high li/uidity.+f it has invested in long term, midterm, there is more li/uidity.Thus, loan investment too can be the criteria of measuring the li/uidity.

1.!.-. *t&uctu&e of (ank;The organizational structure of a bank i.e. subCdivision branches too givesspeculation of bank li/uidity.+f the structure of the bank is in single nature,there ishigher li/uidity in the bank.+ f the banks have many branches li/uidity is lower because the li/uidity remains scattered in different branches and sub branches.+nthis way, we can find out the bankHs li/uidity from the structure and theorganizational structure of a bank.

1.% P&o(le" I'entification

Though, many banks are being operated in different parts of 6epal.Thus existseveral problems,which are as followsDi3 +n 6epal , the largest banks namely 6B (td. and ?BB are unable to earn

more profit as compared to !oint venture banks.o, low profitability is theproblem.ii3 +n 6epal, corruption and reposition occur mainly in the public sector

banks.+n such banks loan are granted only if some benefits to theconcerned employees are granted.

iii3 The another problem is the existence of organized banks which includemoney lenders, merchants and goldsmiths who do the lending businessunder personal basis.

(i/uidity <osition of 6abil Bank 12

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 13/32

iv3 Another problem of banking in 6epal is traditional system.ome banksnamely 6epal bank (td. and ?astriya Bani!iya Bank still operate with oldlenders and in many branches.

v3 =any banks are still unable to maintain capital ade/uacy ratio inaccordance with the rule and regulation of 6?B as well as internal

standard.vi3 The problem of banking in 6epal includes less investment in productivesectors, repotism and favoritism over staffing concentration of banks incity area, high li/uidity.

vii3 >ut through competition between commercial banks creat a lot of problem.+n the other hand, it helps to increase the efficiency andeffectiveness of banks.But mostly it creates various problems if ever canlead the bank to li/uidation.

1.5 *inification of the $tu'3

This is of field report writing mainly deal with the student.Through this type of report writing fieldwork, students may enable to enchance their knowledge in thefield of problem, =arketing and public relation etc. And they able to deal withsuch type of activities.+he main significance of the study are i3 To get desired data with some aspect of li/uidity by performing various

finanacial analysis.ii3 To come to conclusion about the li/uidity position of 6abil Bank.iii3 To find out the position of 6abil Bank.iv3 To find out strength and weakness of 6abil Bank.v3 To find out the marketing style and public relation of the bank.

1.0 )i"itation of the $tu'3

i3 The study only covers seven years beginning from 55; to 7221.ii3 There are many factors that effect li/uidity and valuation of firm.&owever

only related factor are taken to consideration in the study.iii3 The study has been felt to be in ade/uate to some extent due to

availability of sufficient literature !ournals.iv3 (ack of industry average ratios for comparision.v3 @nly 6abil Bank (td.is taken.vi3 @nly seven years trend is taken.

1. Re$ea&ch =etho'olo3

?esearch methodology refers to the different techni/ues and tools under to makethe study significant and efficient.There are varieties of techni/ues and toolsavailable to accomplish the study.The financial analysis is ma!or tools.Thisanalysis is useful to reflect the li/uidity position of the concerned bank.

(i/uidity <osition of 6abil Bank 13

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 14/32

1..1 Re$ea&ch De$in;

?esearch design regers to the prospective method to accomplish the study tofulfill the ob!ective of the study.The students have only secondary datasavailable through the annual report published by the concerned bank.o, to get

desired result efficient, the interview and /uestions are most necessary processfor calculating, tabulating and interpretating.

1..! =etho' Anal3$i$;

*arious finanacial analysis tools have been used in this study.The analysis of data will be done according to the pattern of data available.The relationshipbetween different figures related to study topic will be drawn out using ratioanalysis.The various calculated results are tabulated in a choronology order under different heading which are later on compared with each other to interpretthe result.

1..% *ou&ce of Data;

The source of data means the place or materials from which the re/uired datahave been found.There are mainly secondary datas available for study i.e.themain source of data is balance sheet of the concerned bank i.e. 6abil Bank from55; to 7221 has been used.

1..%.1 P&i"a&3 'ata $ou&ce;The data which are originally collected by an investigator or an agent for the firsttime, for the purpose of statistical en/uiry are known as primary data.The primarydata are collected personally through the /uestionnaries, observation andinterviewing method.These data highlight the real and fact information of 6abilBank (td.+n this report structured interview and unstructured observation methodwere used.

1..%.! *econ'a&3 'ata;The source of secondary data are those which has been collected by other people.ome of the secondary data of 6abil BankHs annual report 0722-M24 to72M73 were used for making this report.

1..5 Population an' $a"ple+n our country also there is mainly !oint venture bank have been establishedwhen 6epal has also adopted the economic liberalize.Although there is many

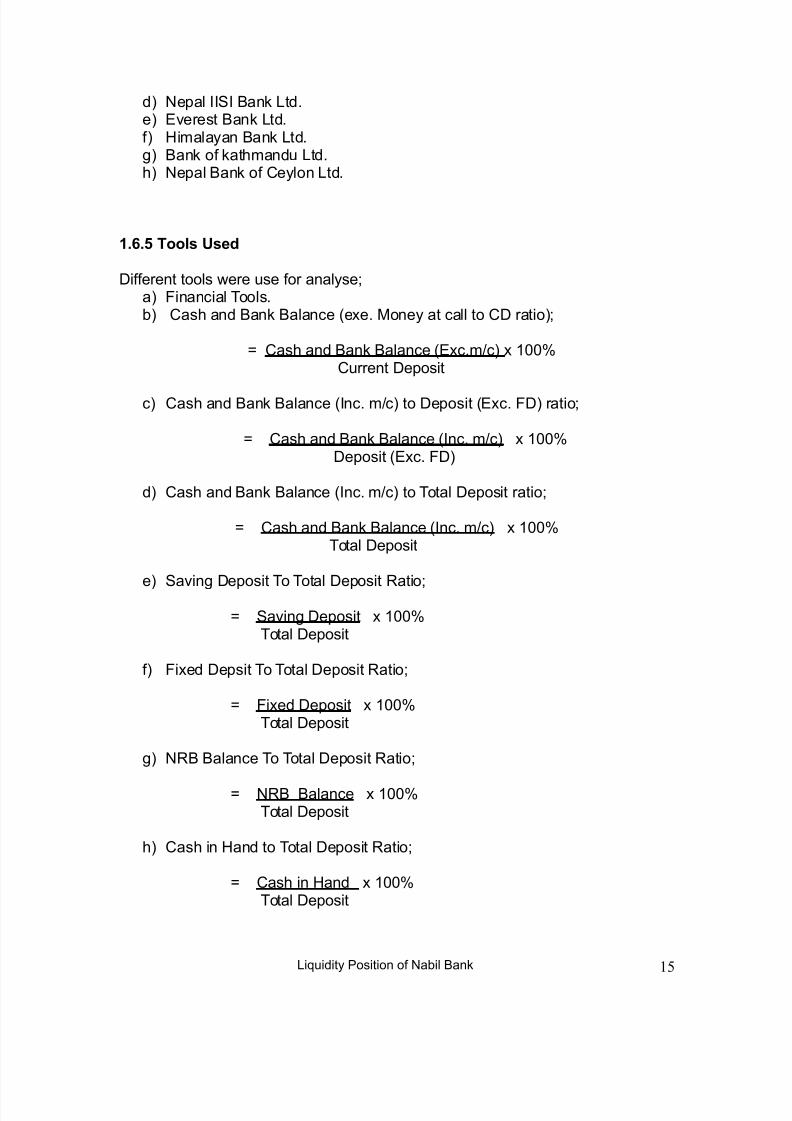

!oint venture banks participating in banking business, to study about these allbanks can not be possible so sampling is re/uired to select one.The populationof !oint venture banks are as followsD

a3 tandard >hartered Bank 6epal (td.b3 6abil Bank (td.c3 6epal +ndosuez Bank (td.

(i/uidity <osition of 6abil Bank 14

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 15/32

d3 6epal +++ Bank (td.e3 :verest Bank (td.f3 &imalayan Bank (td.g3 Bank of kathmandu (td.h3 6epal Bank of >eylon (td.

1..0 Tool$ U$e'

8ifferent tools were use for analysea3 )inancial Tools.b3 >ash and Bank Balance 0exe. =oney at call to >8 ratio3

N >ash and Bank Balance 0:xc.mMc3 x 22I >urrent 8eposit

c3 >ash and Bank Balance 0+nc. mMc3 to 8eposit 0:xc. )83 ratio

N >ash and Bank Balance 0+nc. mMc3 x 22I 8eposit 0:xc. )83

d3 >ash and Bank Balance 0+nc. mMc3 to Total 8eposit ratio

N >ash and Bank Balance 0+nc. mMc3 x 22I Total 8eposit

e3 aving 8eposit To Total 8eposit ?atio

N aving 8eposit x 22I Total 8eposit

f3 )ixed 8epsit To Total 8eposit ?atio

N )ixed 8eposit x 22I Total 8eposit

g3 6?B Balance To Total 8eposit ?atio

N 6?B Balance x 22I Total 8eposit

h3 >ash in &and to Total 8eposit ?atio

N >ash in &and x 22I Total 8eposit

(i/uidity <osition of 6abil Bank 15

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 16/32

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 17/32

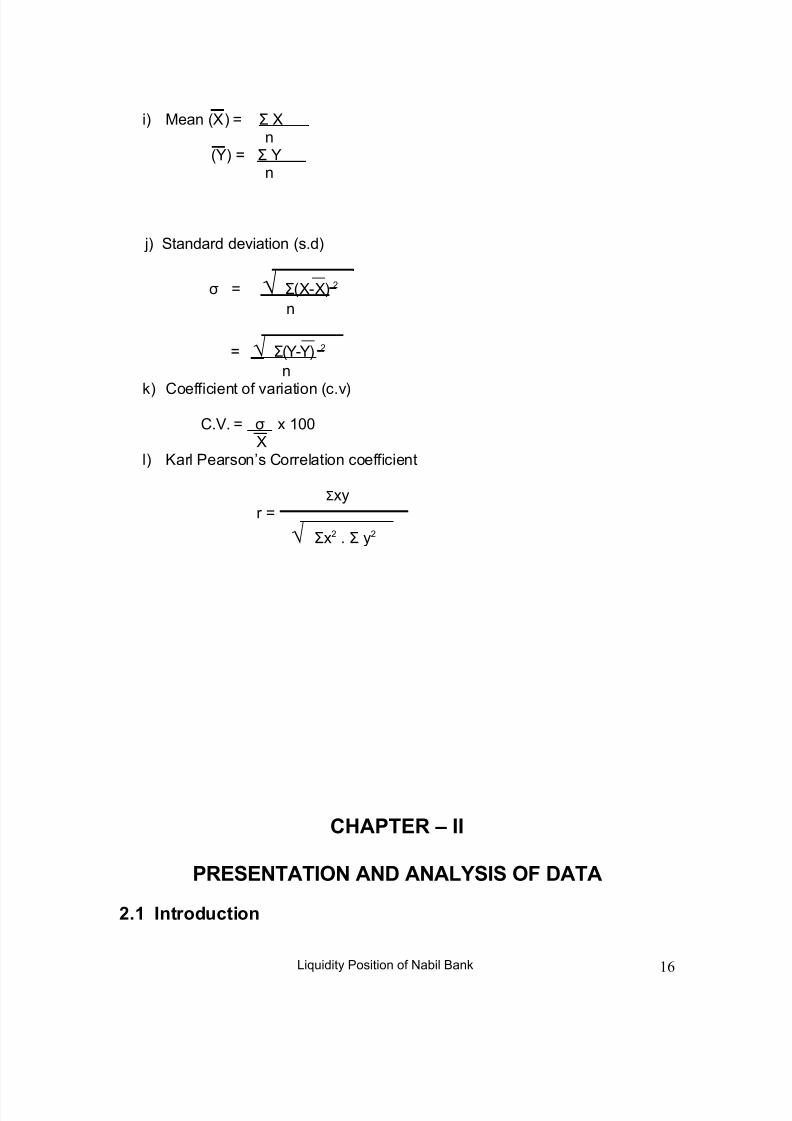

The discussion and analysis section is the heart of the report. This is the sectionin which data are presented and analyzed.The discussion of finding will normallybe the longest section of report to get desired ob!ectives described previouslyob!ectives of the study several analytical tools had been employed and used

research methodology and research design. This chapter is basically concernedwith presentation and analysis of datas.+n this chapter the effort had been madeto analyze the li/uidity position of the 6abil Bank.

:very presentation of the data follows its analysis so that can be drawn out andfuture prediction can be initiated.)or the propose of the analysis simple methodof financial tools, ratio analysis and statistically tools, mean, standard deviation,coefficient of variation are used.

!.! Ratio Anal3$i$

?atio analysis is widely used as a tool of financial analysis.+t is defined as asystematic use of ratioHs to interpreted the financial statement so that the strengthand weakness of a firm as well as its historical performance and current financialcondition can be defined.

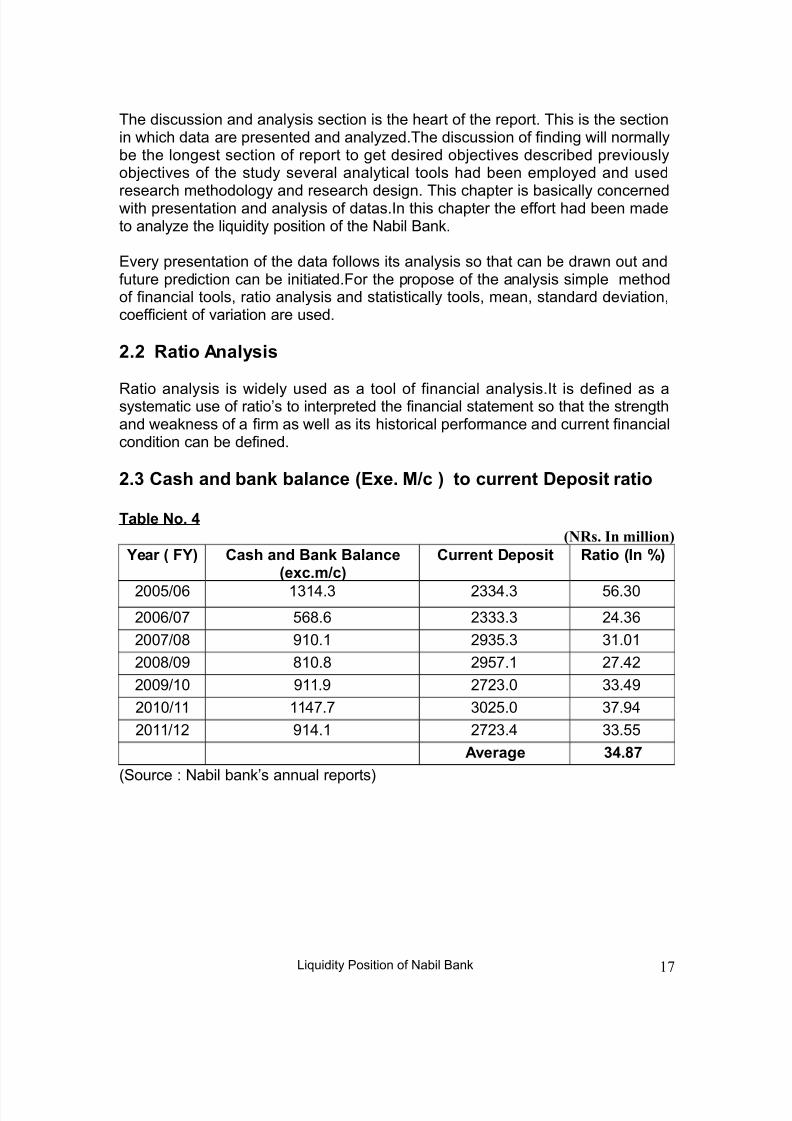

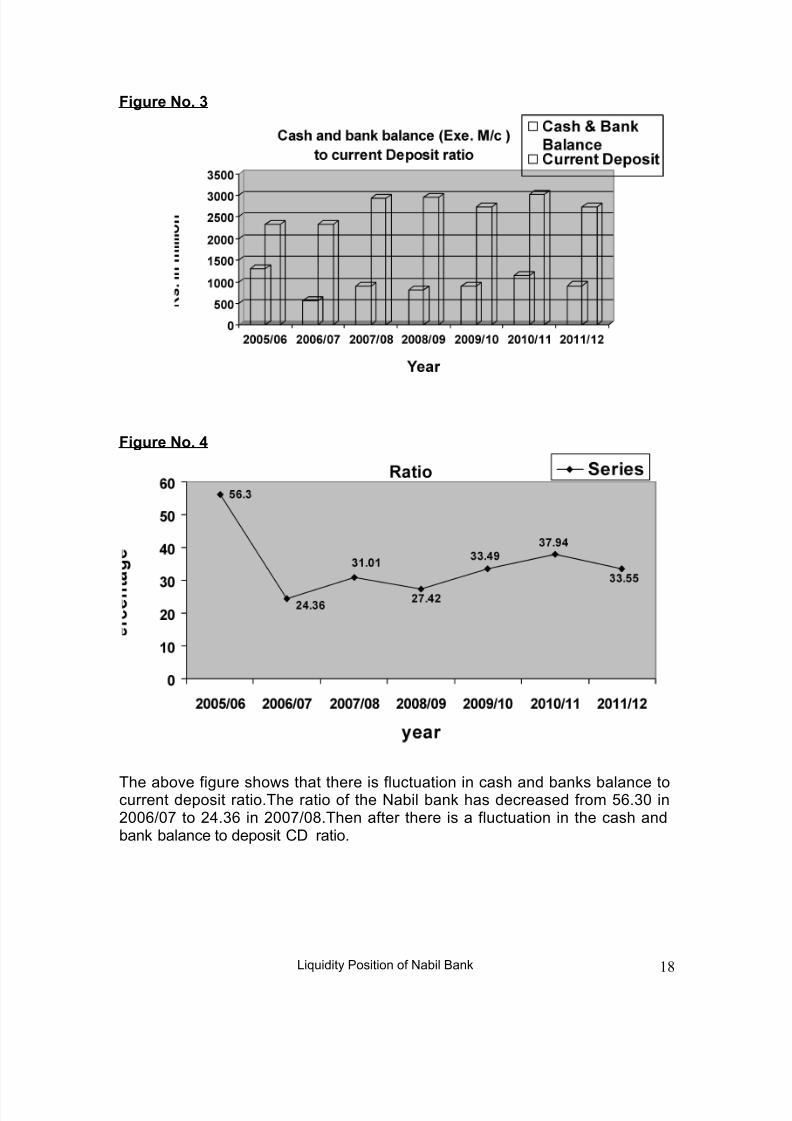

!.% Ca$h an' (ank (alance E4e. =7c 2 to cu&&ent Depo$it &atio

Ta(le No. 5(NRs. In million)

8ea& #82 Ca$h an' Bank Balancee4c."7c2

Cu&&ent Depo$it Ratio In ,2

722-M24 1. 71. -4.27224M2 -4;.4 7. 71.4

722M2; 52. 75-. .2

722;M25 ;2.; 75-. 7.17

7225M2 5.5 77.2 .15

722M 1. 27-.2 .51

72M7 51. 77.1 .--

Ave&ae %5.>/

0ource D 6abil bankHs annual reports3

(i/uidity <osition of 6abil Bank 17

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 18/32

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 19/32

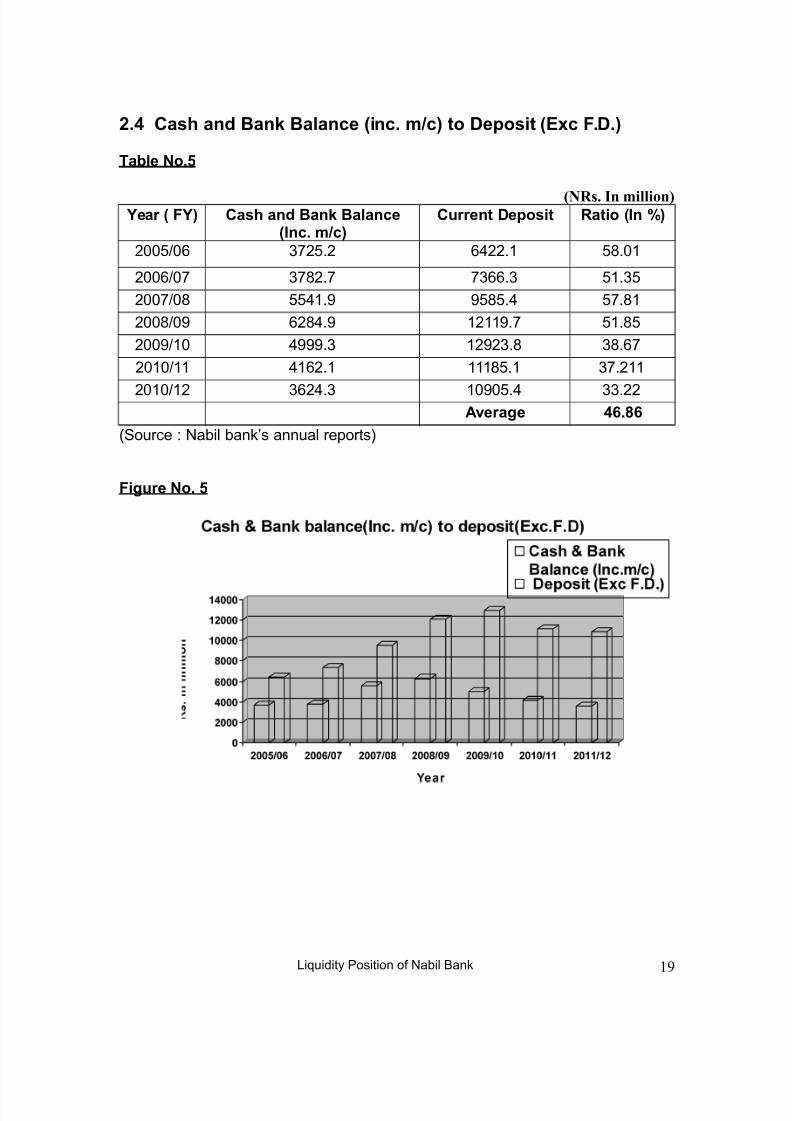

!.5 Ca$h an' Bank Balance inc. "7c2 to Depo$it E4c #.D.2

Ta(le No.0

(NRs. In million) 8ea& #82 Ca$h an' Bank Balance

Inc. "7c2Cu&&ent Depo$it Ratio In ,2

722-M24 7-.7 4177. -;.2

7224M2 ;7. 44. -.-

722M2; --1.5 5-;-.1 -.;

722;M25 47;1.5 75. -.;-

7225M2 1555. 757.; ;.4

722M 147. ;-. .7

722M7 471. 252-.1 .77Ave&ae 5.>

0ource D 6abil bankHs annual reports3

#iu&e No. 0

(i/uidity <osition of 6abil Bank 19

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 20/32

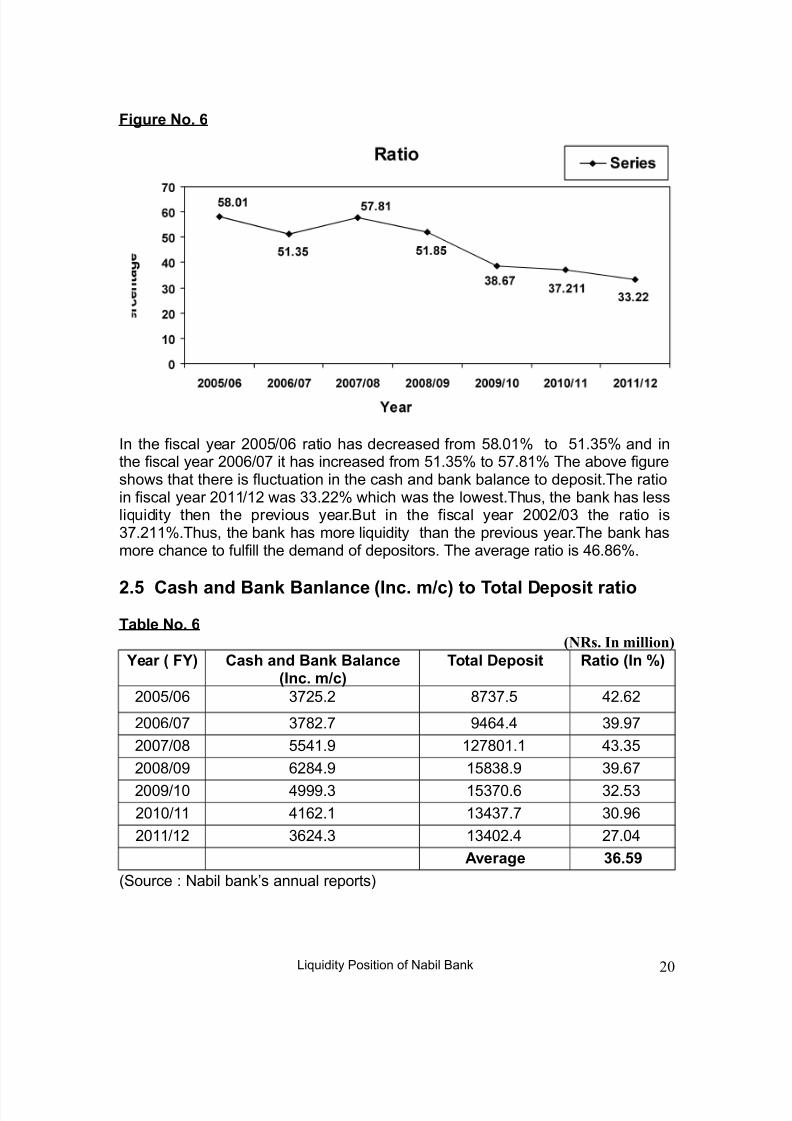

#iu&e No.

+n the fiscal year 722-M24 ratio has decreased from -;.2I to -.-I and inthe fiscal year 7224M2 it has increased from -.-I to -.;I The above figureshows that there is fluctuation in the cash and bank balance to deposit.The ratioin fiscal year 72M7 was .77I which was the lowest.Thus, the bank has lessli/uidity then the previous year.But in the fiscal year 7227M2 the ratio is.7I.Thus, the bank has more li/uidity than the previous year.The bank hasmore chance to fulfill the demand of depositors. The average ratio is 14.;4I.

!.0 Ca$h an' Bank Banlance Inc. "7c2 to Total Depo$it &atio

Ta(le No. (NRs. In million)

8ea& #82 Ca$h an' Bank BalanceInc. "7c2

Total Depo$it Ratio In ,2

722-M24 7-.7 ;.- 17.47

7224M2 ;7. 5141.1 5.5

722M2; --1.5 7;2. 1.-

722;M25 47;1.5 -;;.5 5.4

7225M2 1555. -2.4 7.-722M 147. 1. 2.54

72M7 471. 127.1 7.21

Ave&ae %.0-

0ource D 6abil bankHs annual reports3

(i/uidity <osition of 6abil Bank 20

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 21/32

#iu&e No. /

#iu&e No.>

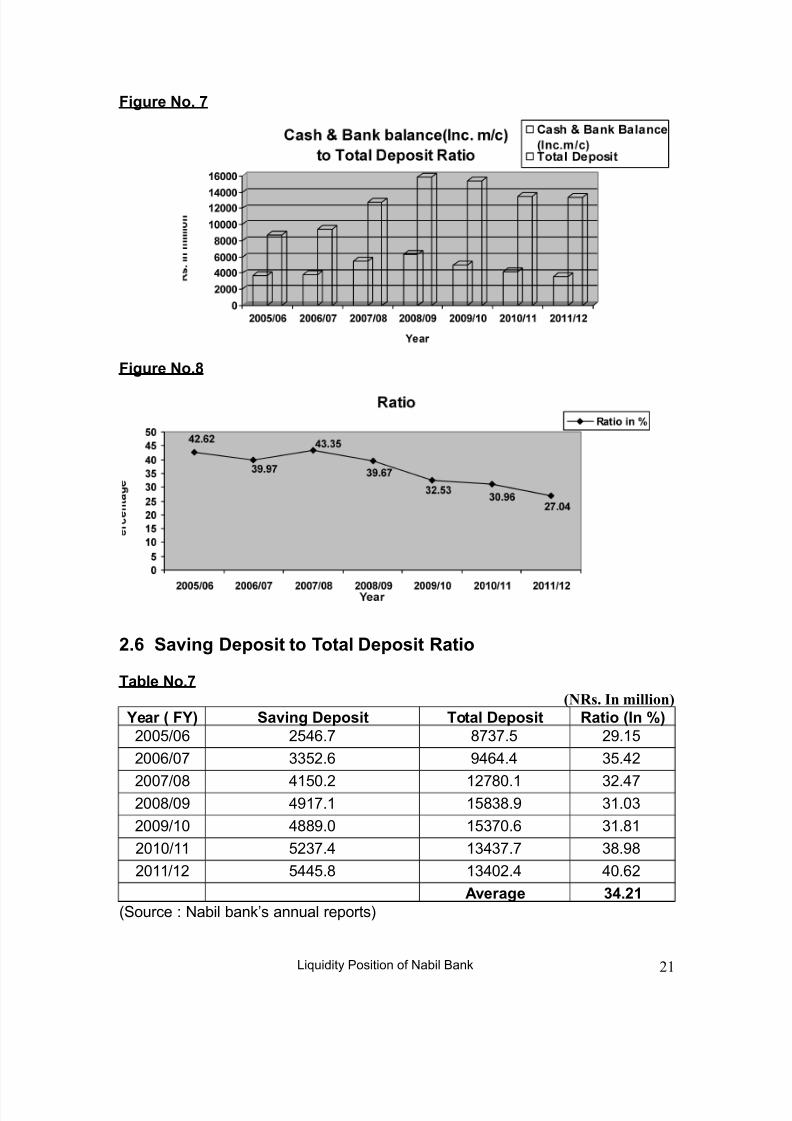

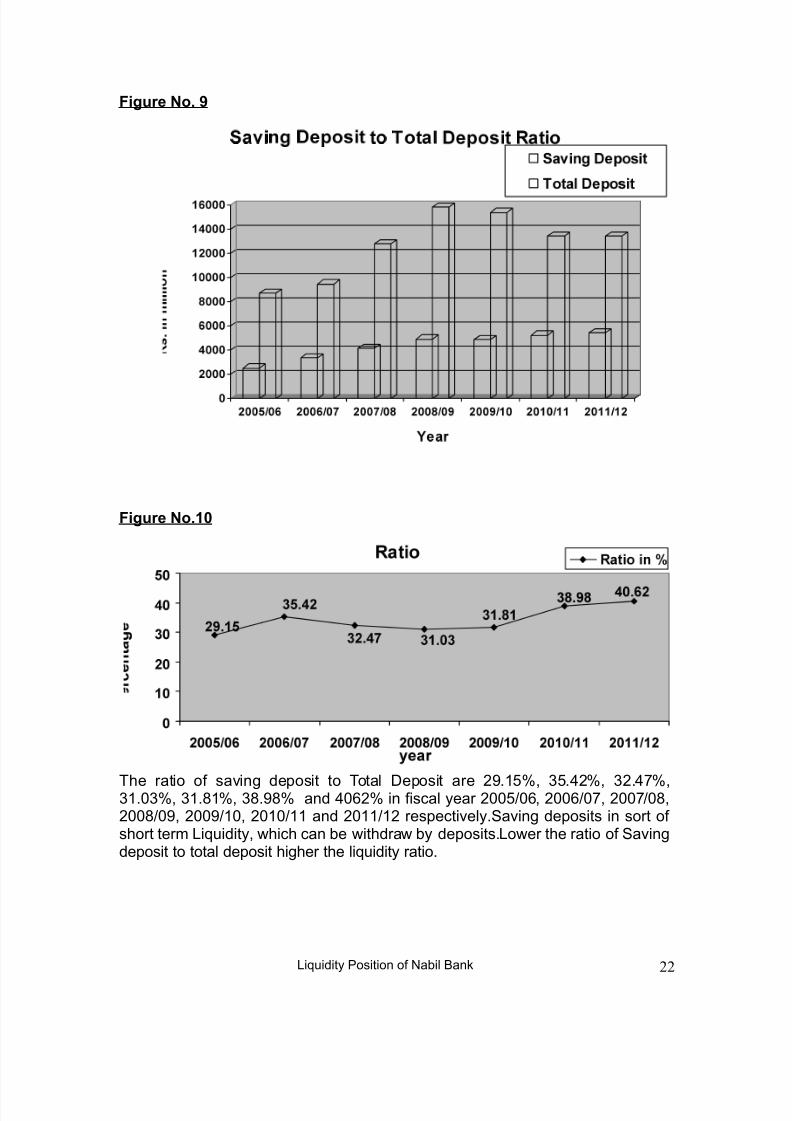

!. *avin Depo$it to Total Depo$it Ratio

Ta(le No./(NRs. In million)

8ea& #82 *avin Depo$it Total Depo$it Ratio In ,2

722-M24 7-14. ;.- 75.-

7224M2 -7.4 5141.1 -.17

722M2; 1-2.7 7;2. 7.1722;M25 15. -;;.5 .2

7225M2 1;;5.2 -2.4 .;

722M -7.1 1. ;.5;

72M7 -11-.; 127.1 12.47

Ave&ae %5.!1

0ource D 6abil bankHs annual reports3

(i/uidity <osition of 6abil Bank 21

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 22/32

#iu&e No. -

#iu&e No.1+

The ratio of saving deposit to Total 8eposit are 75.-I, -.17I, 7.1I,.2I, .;I, ;.5;I and 1247I in fiscal year 722-M24, 7224M2, 722M2;,722;M25, 7225M2, 722M and 72M7 respectively.aving deposits in sort of short term (i/uidity, which can be withdraw by deposits.(ower the ratio of avingdeposit to total deposit higher the li/uidity ratio.

(i/uidity <osition of 6abil Bank 22

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 23/32

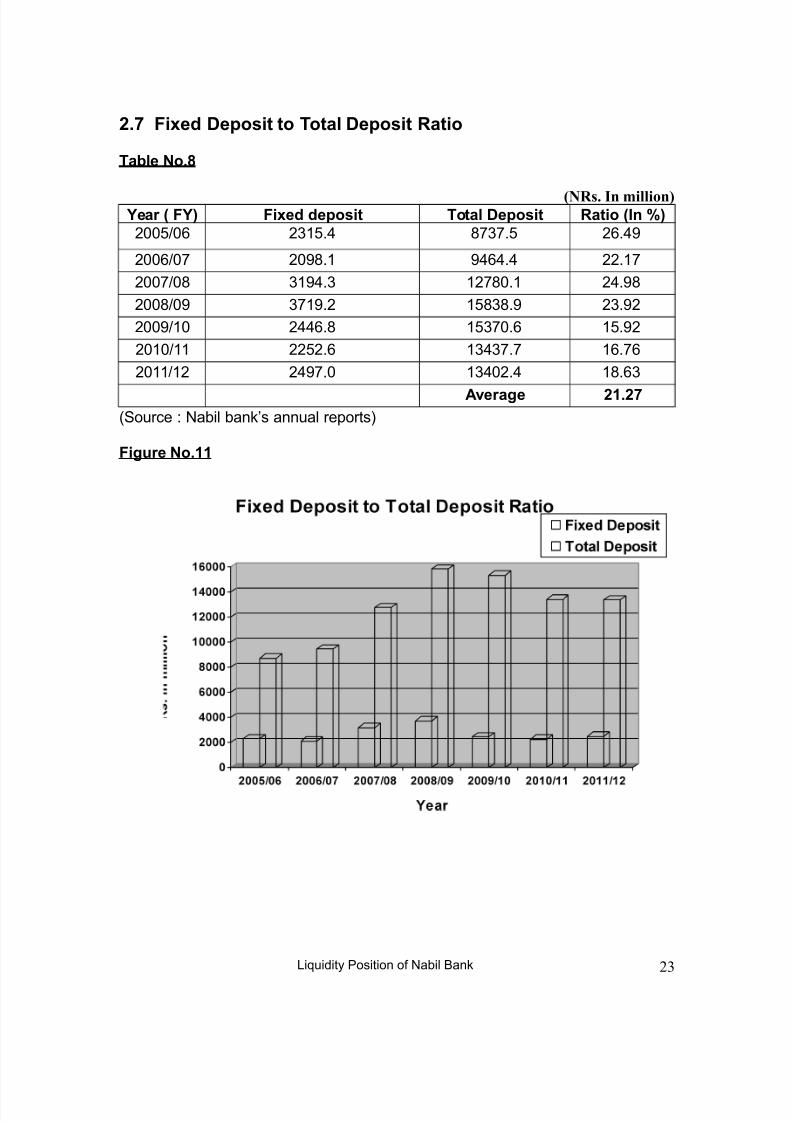

!./ #i4e' Depo$it to Total Depo$it Ratio

Ta(le No.>

(NRs. In million) 8ea& #82 #i4e' 'epo$it Total Depo$it Ratio In ,2

722-M24 7-.1 ;.- 74.15

7224M2 725;. 5141.1 77.

722M2; 51. 7;2. 71.5;

722;M25 5.7 -;;.5 7.57

7225M2 7114.; -2.4 -.57

722M 77-7.4 1. 4.4

72M7 715.2 127.1 ;.4

Ave&ae !1.!/

0ource D 6abil bankHs annual reports3

#iu&e No.11

(i/uidity <osition of 6abil Bank 23

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 24/32

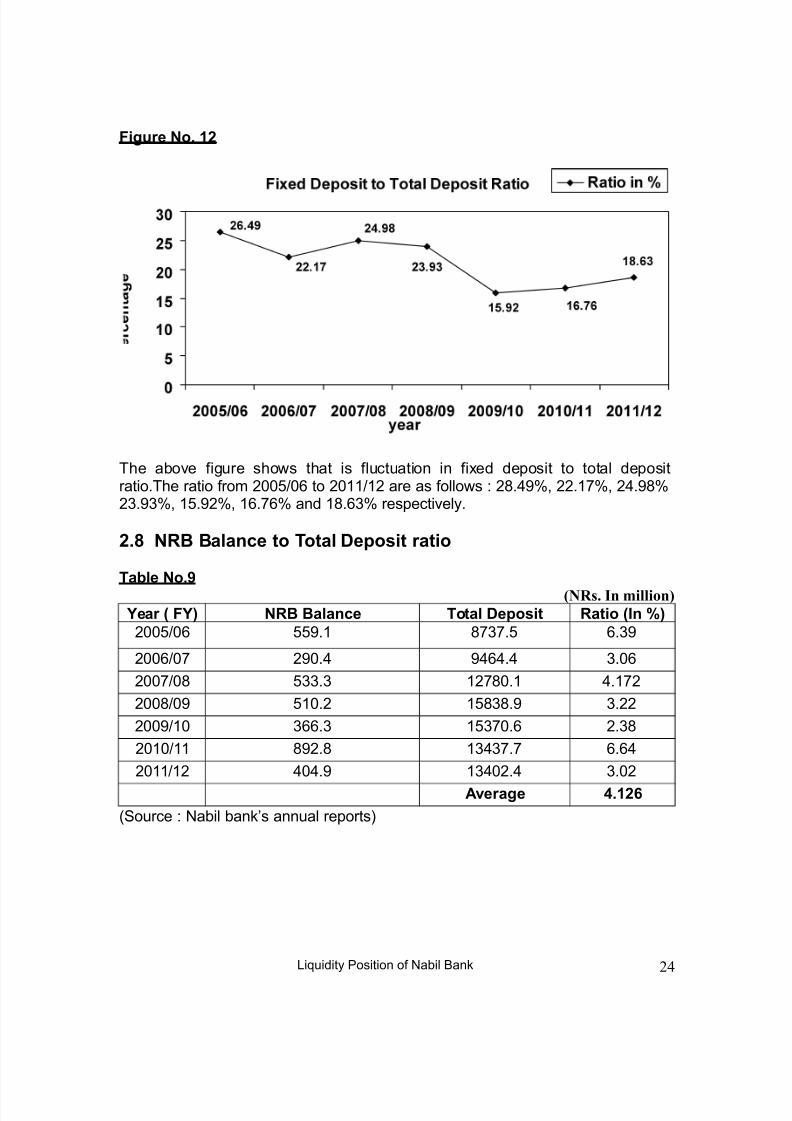

#iu&e No. 1!

The above figure shows that is fluctuation in fixed deposit to total depositratio.The ratio from 722-M24 to 72M7 are as follows D 7;.15I, 77.I, 71.5;I7.5I, -.57I, 4.4I and ;.4I respectively.

!.> NRB Balance to Total Depo$it &atio

Ta(le No.-(NRs. In million)

8ea& #82 NRB Balance Total Depo$it Ratio In ,2

722-M24 --5. ;.- 4.5

7224M2 752.1 5141.1 .24

722M2; -. 7;2. 1.7

722;M25 -2.7 -;;.5 .77

7225M2 44. -2.4 7.;

722M ;57.; 1. 4.41

72M7 121.5 127.1 .27

Ave&ae 5.1!

0ource D 6abil bankHs annual reports3

(i/uidity <osition of 6abil Bank 24

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 25/32

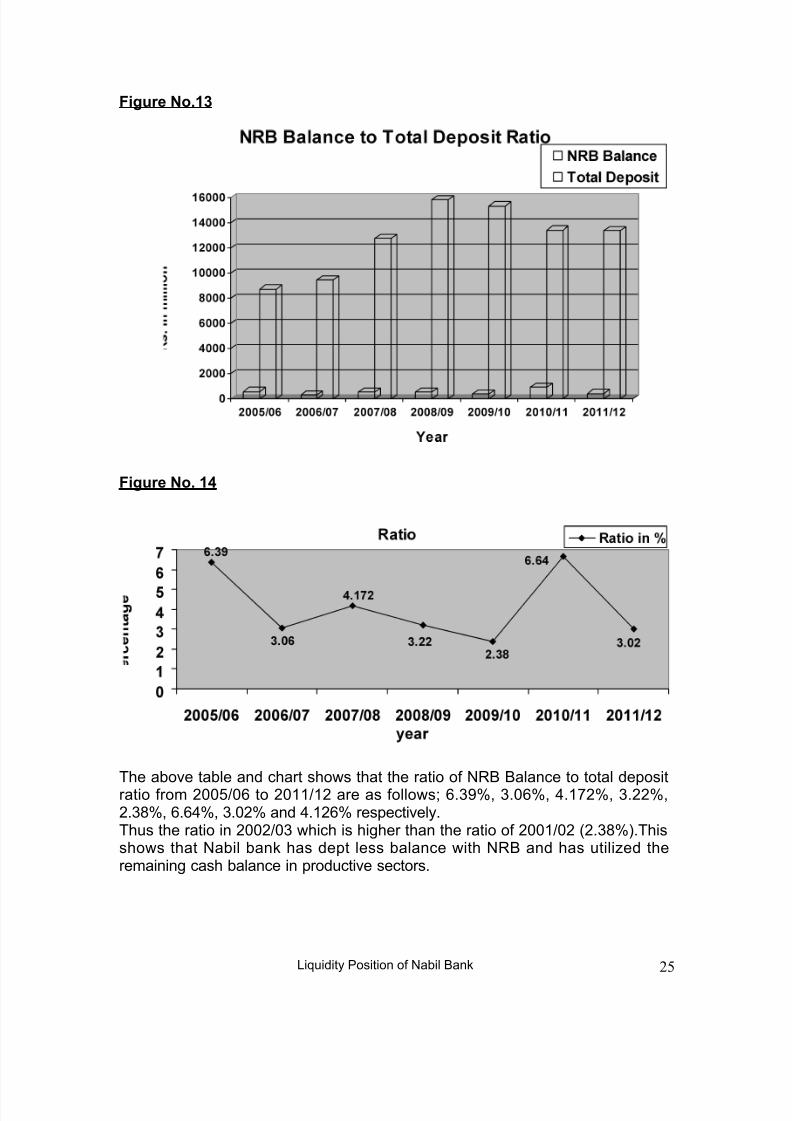

#iu&e No.1%

#iu&e No. 15

The above table and chart shows that the ratio of 6?B Balance to total depositratio from 722-M24 to 72M7 are as follows 4.5I, .24I, 1.7I, .77I,7.;I, 4.41I, .27I and 1.74I respectively.Thus the ratio in 7227M2 which is higher than the ratio of 722M27 07.;I3.Thisshows that 6abil bank has dept less balance with 6?B and has utilized theremaining cash balance in productive sectors.

(i/uidity <osition of 6abil Bank 25

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 26/32

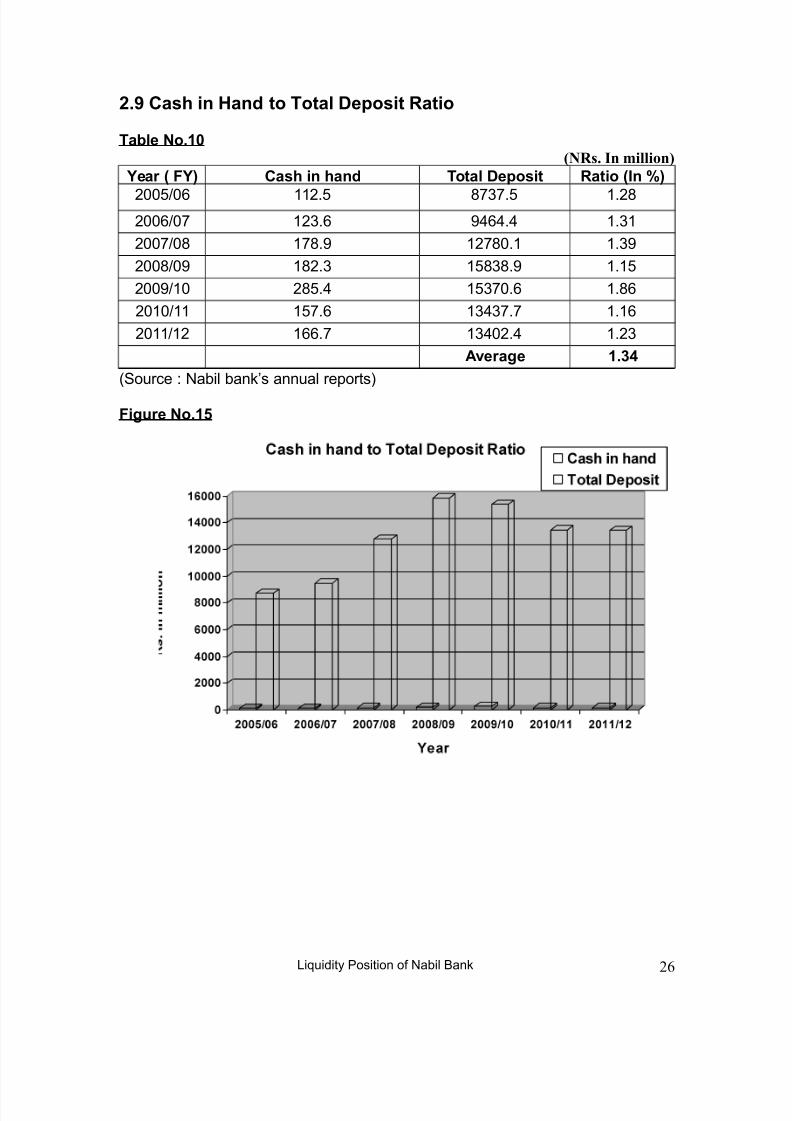

!.- Ca$h in Han' to Total Depo$it Ratio

Ta(le No.1+(NRs. In million)

8ea& #82 Ca$h in han' Total Depo$it Ratio In ,2

722-M24 7.- ;.- .7;7224M2 7.4 5141.1 .

722M2; ;.5 7;2. .5

722;M25 ;7. -;;.5 .-

7225M2 7;-.1 -2.4 .;4

722M -.4 1. .4

72M7 44. 127.1 .7

Ave&ae 1.%5

0ource D 6abil bankHs annual reports3

#iu&e No.10

(i/uidity <osition of 6abil Bank 26

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 27/32

#iu&e No. 1

The above table and chart shows that the ratio of cash in hand to total depositfrom 722-M24 to 72M7 are as follows .7;I, .I, .5I, .-I, .;4I,.4- and .7I.respectively.

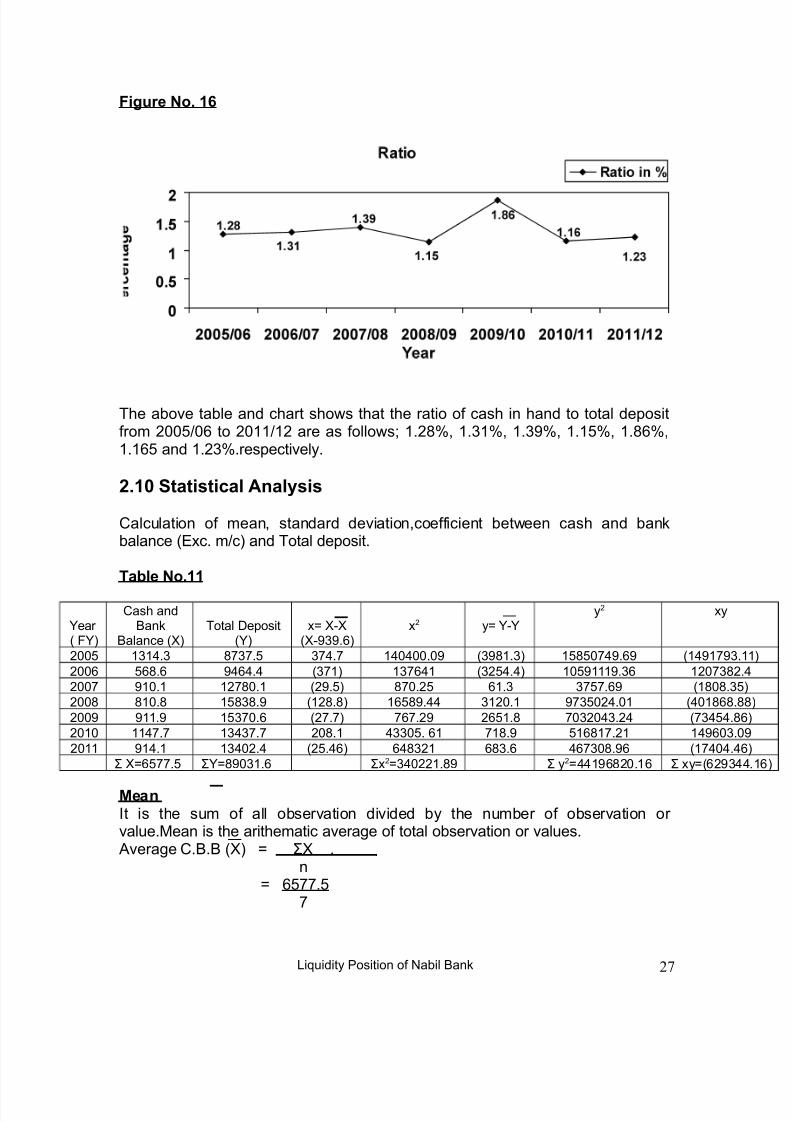

!.1+ *tati$tical Anal3$i$

>alculation of mean, standard deviation,coefficient between cash and bankbalance 0:xc. mMc3 and Total deposit.

Ta(le No.11

Jear0 )J3

>ash andBank

Balance 0O3Total 8eposit

0J3xN OCO

0OC55.43x7 yN JCJ

y7 xy

722- 1. ;.- 1. 12122.25 05;.3 -;-215.45 0155.7224 -4;.4 5141.1 03 41 07-1.13 2-55.4 72;7722 52. 7;2. 075.-3 ;2.7- 4. -.45 0;2;.-722; ;2.; -;;.5 07;.;3 4-;5.11 72. 5-271.2 012;4;.;7225 5.5 -2.4 07.3 4.75 74-.; 2721.71 01-1.;722 1. 1. 72;. 12-. 4 ;.5 -4;.7 1542.272 51. 127.1 07-.143 41;7 4;.4 142;.54 0121.1

P ON4-.- PJN;52.4 Px7N1277.;5 P y7N1154;72.4 P xyN04751

=ean+t is the sum of all observation divided by the number of observation or value.=ean is the arithematic average of total observation or values.

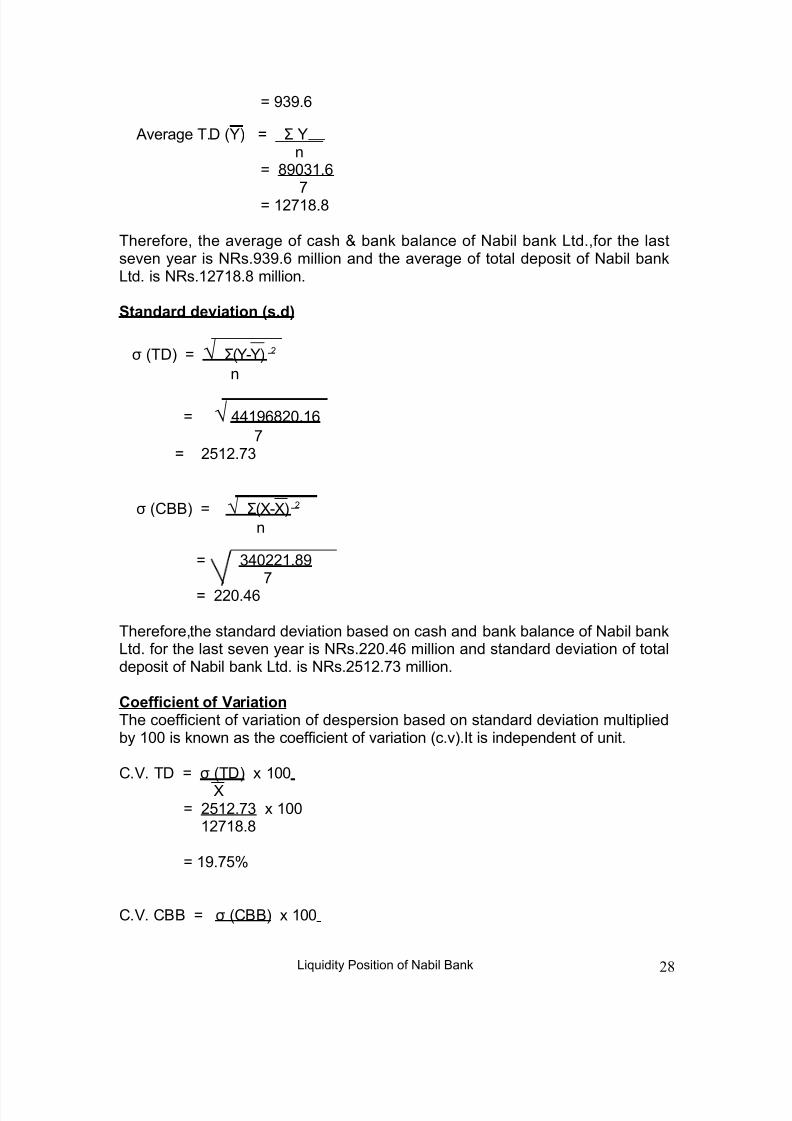

Average >.B.B 0O3 N PO .n

N 4-.-

(i/uidity <osition of 6abil Bank 27

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 28/32

N 55.4

Average T.8 0J3 N P Jn

N ;52.4 N 7;.;

Therefore, the average of cash L bank balance of 6abil bank (td.,for the lastseven year is 6?s.55.4 million and the average of total deposit of 6abil bank(td. is 6?s.7;.; million.

*tan'a&' 'eviation $.'2

Q 0T83 N R P0JCJ3 7

n

N R 1154;72.4 N 7-7.

Q 0>BB3 N R P0OCO3 7

n

N 1277.;5 N 772.14

Therefore,the standard deviation based on cash and bank balance of 6abil bank(td. for the last seven year is 6?s.772.14 million and standard deviation of totaldeposit of 6abil bank (td. is 6?s.7-7. million. Coefficient of @a&iationThe coefficient of variation of despersion based on standard deviation multipliedby 22 is known as the coefficient of variation 0c.v3.+t is independent of unit.

>.*. T8 N Q 0 T8 3 x 22O

N 7-7. x 22 7;.;

N 5.-I

>.*. >BB N Q 0 >BB 3 x 22

(i/uidity <osition of 6abil Bank 28

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 29/32

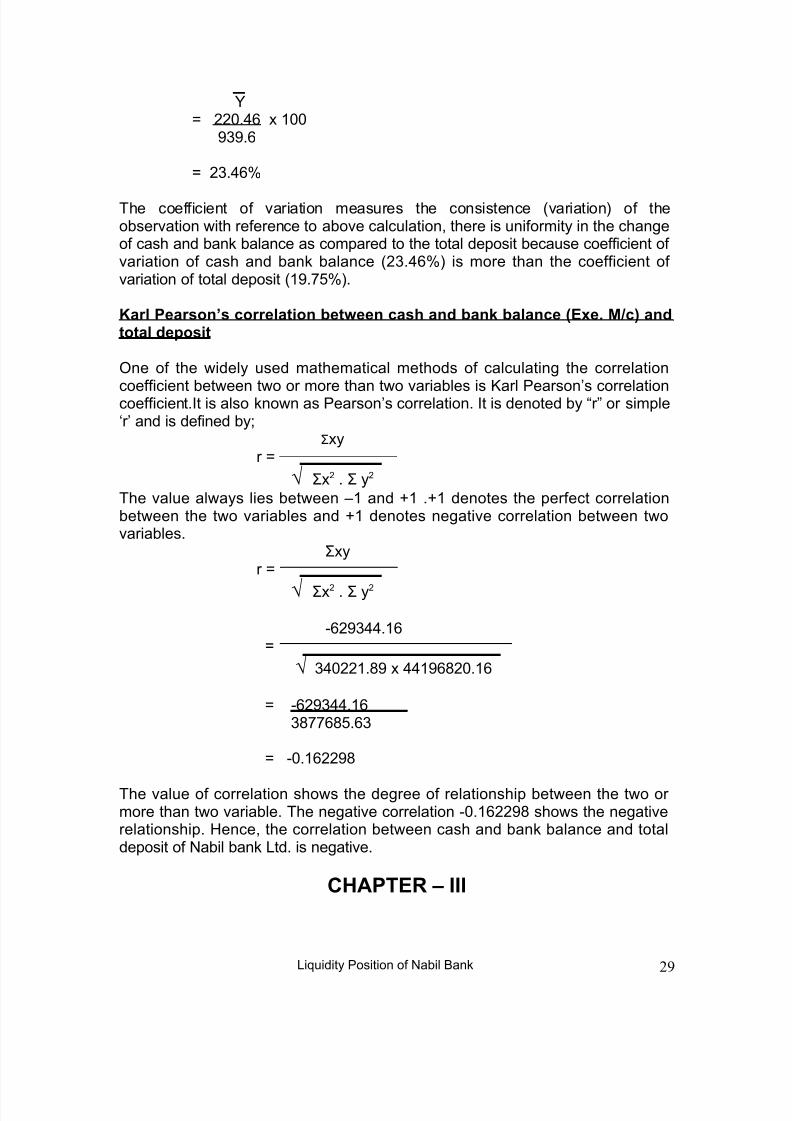

J N 772.14 x 22 55.4

N 7.14I

The coefficient of variation measures the consistence 0variation3 of theobservation with reference to above calculation, there is uniformity in the changeof cash and bank balance as compared to the total deposit because coefficient of variation of cash and bank balance 07.14I3 is more than the coefficient of variation of total deposit 05.-I3.

a&l Pea&$on$ co&&elation (et:een ca$h an' (ank (alance E4e. =7c2 an'total 'epo$it

@ne of the widely used mathematical methods of calculating the correlation

coefficient between two or more than two variables is #arl <earsonHs correlationcoefficient.+t is also known as <earsonHs correlation. +t is denoted by $r% or simpleSrH and is defined by

Pxyr N

R Px7 . P y7

The value always lies between and . denotes the perfect correlationbetween the two variables and denotes negative correlation between twovariables. Pxy

r N

R Px7 . P y7

C47511.4N

R 1277.;5 x 1154;72.4

N C47511.4;4;-.4

N C2.4775;

The value of correlation shows the degree of relationship between the two or more than two variable. The negative correlation C2.4775; shows the negativerelationship. &ence, the correlation between cash and bank balance and totaldeposit of 6abil bank (td. is negative.

CHAPTER – III

(i/uidity <osition of 6abil Bank 29

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 30/32

*U==AR8 AND CONC)U*ION

%.1 *u""a&3

6epal is one of the less developed countries of the world for most of the

developing process. +t is financial depend on the foreign countriesit iseconomically too week in 6epalese banking industries.

=odern commercial banks make the economy always alive and smart to run andmaintain day to day commercial economic and banking transactions.+n shortbanking transactions help a country to develop its economy swifty.+t there weresystematic and scientific programs for economic and scientific developmentscountries like 6epal would have developed if its economy as much as thosecountries which have development like might have been perhaps narroweddown.

At present commercial banks including !oint venture banks are operating in6epalese +ndustry.+t is remarkable fact that any country cannot have a developedeconomy in the absence of modern banking system.Because any developmentworks needs a sufficient capital and lack of sufficient capital is also one of themain reason as to why 6epal has been backward for developing its economy.

o it is very important to find out whether or not the banks are serving animportant contribution to developed different sector of the economy.(i/uidity isaid to be the general business of fund, which shows the banks ability to meetcash re/uirements.+n this record, this study has been based upon the ob!ective toevaluate the li/uidity position of 6abil bank (td.

%.! =ao& #in'in$

The ma!or findings of this study are as follows

The cash and bank balance to current deposit ratio is .--I in 722M21. The cash and bank balance 0+nc. mMc3 to deposit 0:xe. )ixed deposit3 is

.77 in 722M21. The cash and bank balance 0+nc.mMc3 to total deposit ratio is 7.21 in

722M21. The saving deposits to total deposit ratio is 12.47 in fiscal year 722M21. The fixed deposit to total deposit ratio is ;.4 in fiscal year 722M21. The 6?B balance to total deposit ratio is .27 in the financial year

722M21. The cash in hand to total deposit ratio is .7 in the financial year 722M21.

%.% Conclu$ion

(i/uidity <osition of 6abil Bank 30

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 31/32

Thus banks play vital role for the country.+t should utilize the resources of thecountry and its people in the proper way making all the policy properly.Generalactivities and management and commercial banks directly effect the economicdevelopment of 6epal.

By the study of a li/uidity position of the 6abil bank (td.,the current deposit of thefinancial year is less then the precious year and its ratio is decreased from .51to .--.The ratio of cash and bank balance 0+nc. mMc3 to deposit 0:xc. )83 isdecreased from .7I to .77,the cash and bank balance 0+nc. mMc3 to totaldeposit ratio is decreased from 2.54I to 7.21I, the saving deposit is more inprecious year than current year, 6?B balance to total deposit ratio is decreasedfrom frevious year and the ratio of cash in hand to total deposit is increased fromthe year 7227M2 0.4I3 to 722M21 0.7I3.

%.5 Reco""en'ation

ome suggestion and recommndation forwarded on the basis of the study are

:conomic condition of the country is deteriorating, there is danger inslacking of the business and industial activities.o, the bank should beinterested only in collecting huge amount of deposit by increasing theinterest rate.

@ther than shareholders annual report, the bank should publish anddistribute booklets containing detail information about its activities andpercormance as well

The bank should follow the discipline and adopt directions of 6epal ?astra

bank.This helps to maintain harmonious relationship between other !ointventure banks as well. >onsidering the present economic condition of the country, the banks

should play pivotal rales for the economic development of thecountry.They should promote balances regional development by finanacialfunds in remote areas and other priority sections.

&igh interest rate is tool to attract customer, which effent the collection of fund.The cash deposited by the customer are li/uid asset,which help tomaintain ade/uate li/uidity position of bank.

6abil bank should broaden its basic operational areas other than bankinglike agrifulture, industry, financial sectors etc.

Government, 6?B and commercial banks should take necessary steps toform and regulate banking habit of 6epalese people especially people of rural areas.

BIB)IO9RAPH8

(i/uidity <osition of 6abil Bank 31

8/12/2019 Liquidity Position of Nabil

http://slidepdf.com/reader/full/liquidity-position-of-nabil 32/32

1. <rof. G8 <ant, >haudhary A.#. “Business Statistics and Mathemetics.”

072-; B..3

2. “Annual Report of Nabil Bank” from fiscal year 722; to 727.

3. “Bankin ! financial statistics”. 6?B mid !uly 727

". “#ommercial Bank Act 2$31”% C6?B.

&. Bhandari 8illi ?a!, “'rinciples ! 'ractice of Bankin !

(nsurance” ,Fan.72 :dition.

). <radhan, ?adhe hyam% ”Manaement of *orkin #apital” , 6ew 8elhi

+. Gupta .<.,” Statistical Method”.

,. 6ational Book @rganization,5;4.

-. #hadka, her Fung%“Analsis of /inancial Ratio”% #athmandu +nstitute of

=anagement,T.9.

1$.<ant, <rem ?a!. /ield0ork Assinment And Report *ritin. 0st :dition 722-3