Embed Size (px)

Citation preview

The 2012 guide toSe

ptem

ber 2

012

Published in conjunction with:J.P. MorganRBSSEBStandard Chartered Bank

Liquidity Management

OFC_2012.indd 1 06/09/2012 15:03

J.P. Morgan - Euromoney - Advert.pdf 1 06/09/2012 14:05

Looking to the long term 2Faced with an unusually broad and persistent range of challenges, treasurers are looking for sustainable solutions

Moving to the next level in liquidity 4managementSEB

Liquidity Management Survey 2012 6

Liquidity management: Managing the risks 8Standard Chartered Bank

Is your treasury ready for the new 12global rules?J.P. Morgan

Contents

This guide is for the use of professionals only. It states the position of the market as at the time of going to press and is not a substitute for detailed local knowledge.

Euromoney Trading LimitedNestor HousePlayhouse YardLondon EC4V 5EXTelephone: +44 20 7779 8888Facsimile: +44 20 7779 8739 / 8345

Directors: Padraic Fallon (chairman and editor-in-chief ), Sir Patrick Sergeant, The Viscount Rothermere, Richard Ensor (managing director), Neil Osborn, Dan Cohen, John Botts, Colin Jones, Diane Alfano, Christopher Fordham, Jaime Gonzalez, Jane Wilkinson, Martin Morgan, David Pritchard, Bashar Al-Rehany

Editor: Philip AyresDirector of research guides: Soledad Contreras Journalist: Laurence NevilleCover illustration: Daniel PalmerPrinted in the United Kingdom by Wyndeham Group

© Euromoney Trading Limited 2012Euromoney is registered as a trademark in the United States and the United Kingdom.

210x286Contents.indd 1 05/09/2012 15:47

Liquidity Management Survey 2012: looking to the long termFaced with an unusually broad and persistent range of challenges, treasurers are looking for sustainable solutions. By Laurence Neville

Liquidity management has never been more important. Four years on from the onset of the financial crisis, treasurers continue to intensify their efforts to improve the flow of liquidity across their corporate structures. Meanwhile, the ongoing and seemingly intractable debt crisis in the eurozone – and the threat to the euro itself – has added to treasurers’ headaches in managing counterparty risk.

Working capital, funding requirements and the ability to react to eco-nomic and political developments – and continue to function in spite of them – are companies’ main concerns. As Lisa Rossi, global head of liquid-ity management at Deutsche Bank, notes, this has widened the breadth of treasurers’ once chiefly functional roles and forced them not only to think more strategically, but also to find solutions that enable them to do more with less across their organizations.

As further constraints are placed on resources, the management of time, costs, budgets and human capital is requiring the use of technology to enhance and promote operational efficiencies. “Fortunately, technology has become generally cheaper and more readily available, as well as being easier to apply,” notes Willem Dokkum, global head of sales payments and cash management at ING. Indeed, advances in technology are ac-celerating, according to most bankers interviewed for this article, and are delivering practical benefits in the forms of increased transparency and control over working capital and liquidity. “It means organizations are able to better manage risk and maximize internal funding across time zones, currencies and numerous banking relationships,” adds Rossi.

Practical stepsThe economic and financial environment has necessarily prompted treasurers to make changes to how their departments operate. However, Yera Hagopian, liquidity solutions executive, treasury services EMEA, at JP Morgan, says the broad range of challenges facing treasurers – an even deeper and more sustained period of low interest rates and a number of economic tremors ranging from sovereign downgrades to the threat of eurozone member exits – has prompted treasurers to take a longer-term view. “Corporates are looking for sustainable approaches to address their liquidity management challenges rather than a series of knee-jerk reac-tions,” she notes.

In practical terms, corporates are aiming to achieve broadly the same goals they have pursued for the past few decades – only more effectively. “Cli-ents are increasingly looking to manage their liquidity risks more tightly, and take control of unproductive surplus cash within the organization as

they seek more efficient means to channel the funding of their working capital needs,” explains Martijn Stocker, global head, liquidity manage-ment, transaction banking, at Standard Chartered. “Therefore, there has been a greater demand for more diverse capabilities in liquidity manage-ment products as clients’ needs grow.”

However, as trade flows evolve – with emerging markets becoming relatively more important to the global economy – the range of challenges that liquidity management must address is also changing. “One of the key trends in the market today is the increasing demand and complexity of liquidity management as companies expand beyond their home or current operating sphere,” says Elyse Weiner, global head, liquidity and investments, at Citi.

Even companies formerly considered best in class are revisiting their processes to take advantage of new technologies and, in some situations, deregulation, according to Weiner. “In the midst of a succession of financial crises, now primarily centred on the eurozone, risk management is top of mind with treasurers as they consider ways to mitigate both funding and supply chain risk through rationalization of bank relationships and accounts and re-engineering of operational processes, and trade finance options. There is a laser-like focus on de-risking the business and contin-gency planning.”

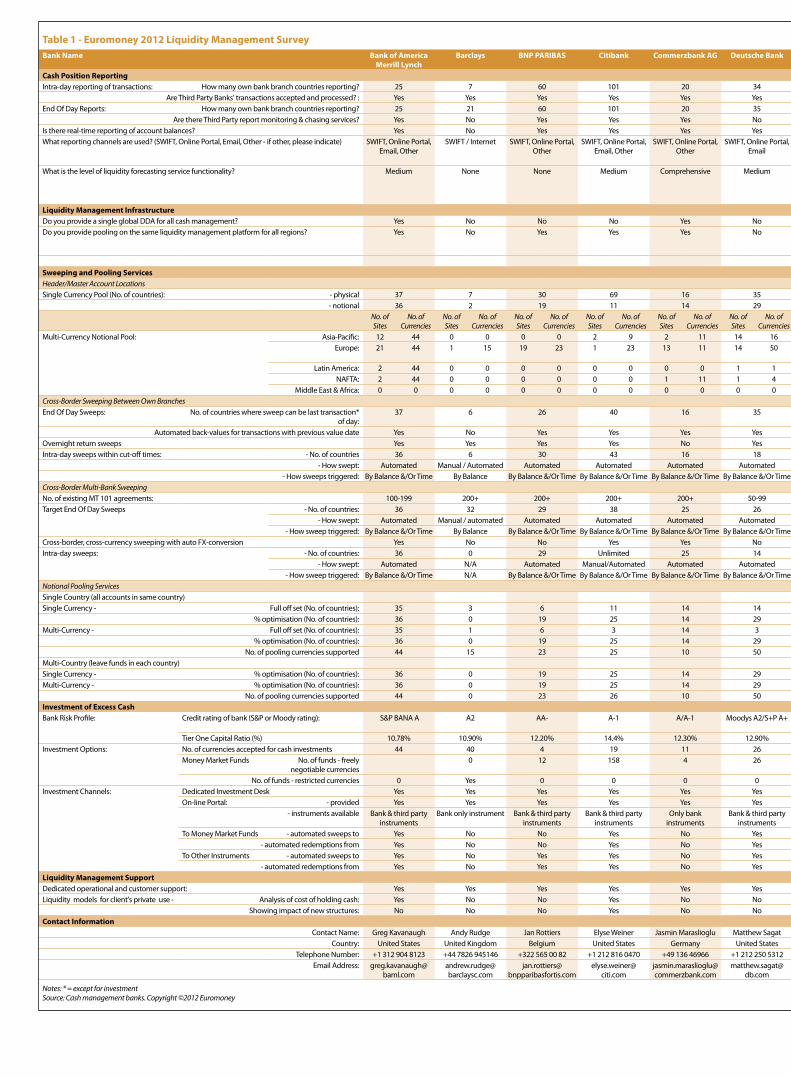

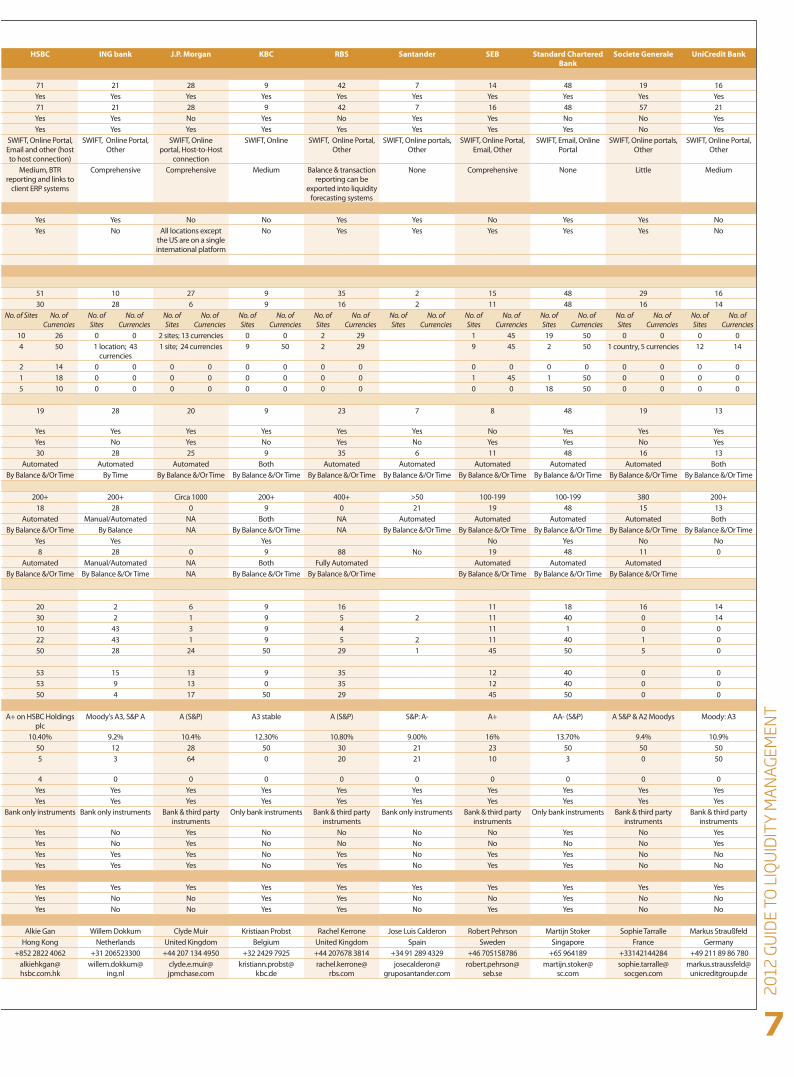

The 2012 Liquidity Management SurveyA total of 16 banks participated in Euromoney’s 2012 survey, the seven global network banks plus nine leading cash management banks: Bank of America Merrill Lynch, Barclays, BNP Paribas, Citi, Commerzbank, Deutsche Bank, HSBC, ING, JP Morgan, KBC, RBS, Santander, SEB, Société Générale, Standard Chartered and UniCredit. Each bank completed a questionnaire covering its cash position reporting services, liquidity management infra-structure, sweeping and cash pooling services, investment services and liquidity management support (see table 1).

Cash position reportingThe strained financial environment continues to highlight the importance of using existing cash from the business more effectively. The growing corporate use of Swift reflects this trend: it had around 900 corporate users at the end of 2011 and has an ambitious goal of 5,000 corporate users by 2015.

As a result of difficult financial conditions, cash position reporting has as-sumed greater importance and forecasting has become a paramount con-

Laurence_V3.indd 2 05/09/2012 15:50

LIQU

IDIT

Y M

ANAG

EMEN

T SU

RVEY

201

2 •

Look

ing

to th

e lo

ng te

rm

3

cern for treasurers: unless they know where cash is, they cannot deploy it effectively. “There is a growing emphasis on accurate cash forecasting and in-depth reporting to enable treasurers to do their job even more effectively than before,” says Dokkum at ING.

Weiner at Citi agrees: “The ability to visualize, mobilize and optimize cash throughout the organization is a prerequisite to improved funding efficiency, full utilization of internal cash assets and improved invest-ment returns,” she says. “In addition, transparency is key to governance of corporate policy, ensuring operating subsidiaries are compliant and oper-ating in a risk-aware manner. As companies expand globally, maintaining control is becoming more challenging. [Equally], newly acquired compa-nies may be operating on disparate platforms for some time before they can be fully integrated.”

At many banks, improving visibility of cash for clients has been a priority for transaction banking investment. “We have continued to invest in prod-ucts and solutions [to facilitate] ever increasing visibility of cash,” explains Jan Rottiers, head of liquidity management products at BNP Paribas. “We are delivering enhanced visibility and forecasting functionality within the liquidity management module of our electronic channels.”

All the banks participating in the survey now provide end-of-day reports from their own branches. As in previous surveys, Citi has the largest number of own bank branch countries reporting (101) with HSBC second at 71 – both have added a single country since last year. Ten of the banks – compared to eight last year – provide services to monitor and chase missing reports. All of the banks provide some intra-day reporting of transactions.

Liquidity management infrastructureOnly half of the participating banks offer a single account for all cash management and only 10 provide pooling on the same liquidity manage-ment platform for all regions – although JP Morgan does now have all locations except the US on a single international platform.

Opinions on the benefits of a single global platform are divided. “In-creasingly, clients are moving to managing a global liquidity position,” explains Thomas Schickler, global head of liquidity, global payments and cash management at HSBC. “This makes it important for them to have a consistency of service across the markets in which they operate but, most importantly, it ensures robust connectivity between the developed and developing markets.”

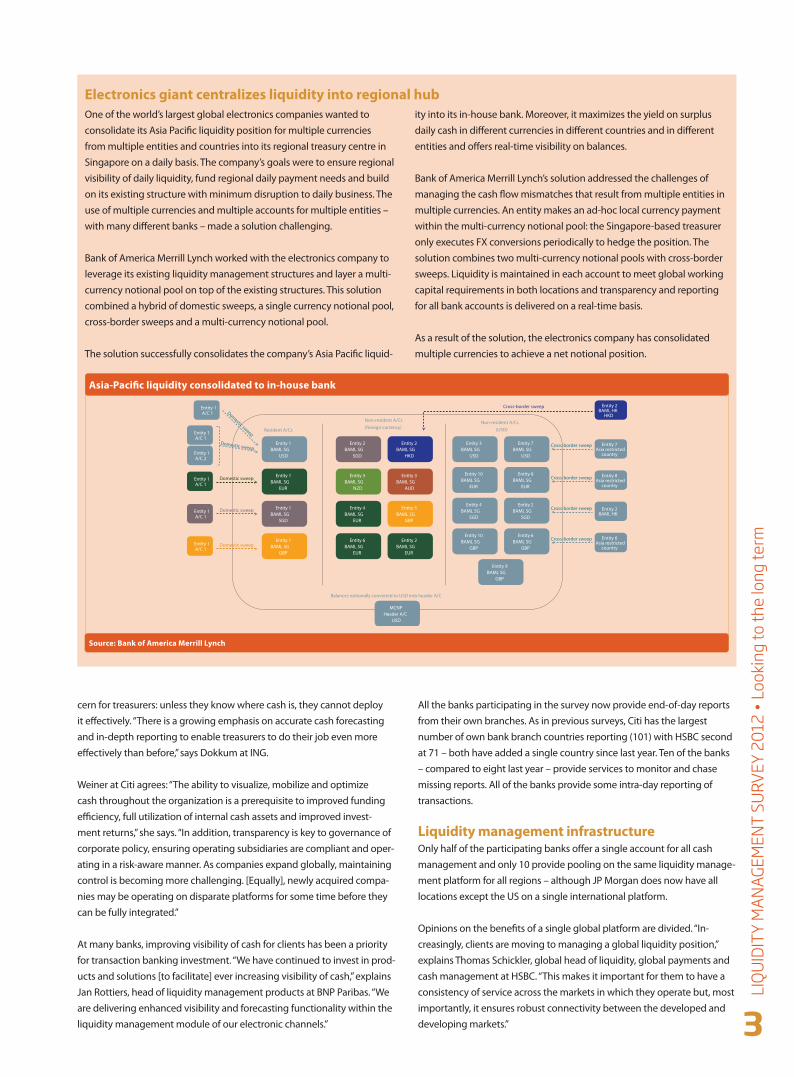

Electronics giant centralizes liquidity into regional hubOne of the world’s largest global electronics companies wanted to consolidate its Asia Pacific liquidity position for multiple currencies from multiple entities and countries into its regional treasury centre in Singapore on a daily basis. The company’s goals were to ensure regional visibility of daily liquidity, fund regional daily payment needs and build on its existing structure with minimum disruption to daily business. The use of multiple currencies and multiple accounts for multiple entities – with many different banks – made a solution challenging.

Bank of America Merrill Lynch worked with the electronics company to leverage its existing liquidity management structures and layer a multi-currency notional pool on top of the existing structures. This solution combined a hybrid of domestic sweeps, a single currency notional pool, cross-border sweeps and a multi-currency notional pool.

The solution successfully consolidates the company’s Asia Pacific liquid-

ity into its in-house bank. Moreover, it maximizes the yield on surplus daily cash in different currencies in different countries and in different entities and offers real-time visibility on balances.

Bank of America Merrill Lynch’s solution addressed the challenges of managing the cash flow mismatches that result from multiple entities in multiple currencies. An entity makes an ad-hoc local currency payment within the multi-currency notional pool: the Singapore-based treasurer only executes FX conversions periodically to hedge the position. The solution combines two multi-currency notional pools with cross-border sweeps. Liquidity is maintained in each account to meet global working capital requirements in both locations and transparency and reporting for all bank accounts is delivered on a real-time basis.

As a result of the solution, the electronics company has consolidated multiple currencies to achieve a net notional position.

Entity 1 BAML SG

USD

Entity 1 BAML SG

EUR

Entity 1 BAML SG

SGD

Entity 1 BAML SG

GBP

Resident A/Cs

Non-resident A/Cs (foreign currency)

Entity 2 BAML SG

SGD

Entity 3 BAML SG

NZD

Entity 4 BAML SG

EUR

Entity 6 BAML SG

EUR

Entity 2 BAML SG

HKD

Entity 3 BAML SG

AUD

Entity 5 BAML SG

GBP

Entity 2 BAML SG

EUR

Non-resident A/Cs (USD)

Entity 3 BAML SG

USD

Entity 10 BAML SG

EUR

Entity 4 BAML SG

SGD

Entity 10 BAML SG

GBP

Entity 7 BAML SG

USD

Entity 8 BAML SG

EUR

Entity 2 BAML SG

SGD

Entity 6 BAML SG

GBP

Entity 9 BAML SG

GBP

Balances notionally converted to USD into header A/C

MCNP Header A/C

USD

Entity 2 BAML HK

HKD

Cross-border sweep

Entity 1 A/C 1

Entity 1 A/C 2

Entity 1 A/C 1 Domestic sweep

Domestic sweep

Entity 1 A/C 1

Domestic sweep

Entity 1 A/C 1

Domestic sweep

Entity 1 A/C 1

Domestic sweep

Entity 7 Asia restricted

country

Entity 8 Asia restricted

country

Entity 2 BAML HK

Entity 6 Asia restricted

country

Cross-border sweep

Cross-border sweep

Cross-border sweep

Cross-border sweep

Asia-Pacific liquidity consolidated to in-house bank

Source: Bank of America Merrill Lynch

Laurence_V3.indd 3 05/09/2012 15:50

Moving to the next level in liquidity managementHaving centralized liquidity, the next priority for treasurers is to quantify how much liquidity the company actually needs, and how to minimize the costs and risks associated with managing it. By Robert Pehrson, global head of product management (corporate segment), and Patrik Bergström, financial strategy, client relationship management, SEB Merchant Banking

Over the past couple of years, treasurers and finance managers have proved very successful in leveraging cash concentration and notional pooling structures to optimize access to liquidity both regionally and globally. In most cases, large multinationals now have solutions in place to enable the efficient concentration of liquidity, cost-effective internal financing and the best use of cash resources. Having centralized liquidity, the next priority for treasurers is to quantify how much liquidity the com-pany actually needs, and how to minimize the costs and risks associated with managing it.

Prioritizing liquidityThere are a variety of reasons why liquidity has become such a significant area of focus, both operationally, making sure that cash is available for use across the business and, strategically, in terms of managing balance sheet and counterparty risk. The first factor is the scarcity of liquidity in the market, particularly for lower-rated companies. This situation has existed since 2008 and with ongoing volatility, a lack of market confidence and tightening regulations, the availability of liquidity is unlikely to increase. Interest spreads have increased, while interest rates are very low, and even negative in some currencies, such as DKK and CHF. In addition, certain types of corporate deposits are less attractive for banks compared with retail deposits, further depressing returns available to corporate investors.

While these factors are all significant in elevating the importance of liquid-ity management, perhaps the most important issue of all is liquidity risk, which was rarely mentioned five years ago. Volatile markets, such as in the Eurozone, combined with uncertainty over banks’ interpretation of Basel III, mean that treasurers can no longer be complacent about where their funding will come from in the future. This is resulting in corporates seek-ing alternative forms of funding, such as accessing the markets directly through corporate bond and commercial paper issuance, as opposed to relying on bank funding. In addition, they are increasingly leveraging their financial assets both to fund working capital requirements and manage liquidity risk, such as receivables financing and supply chain financing.

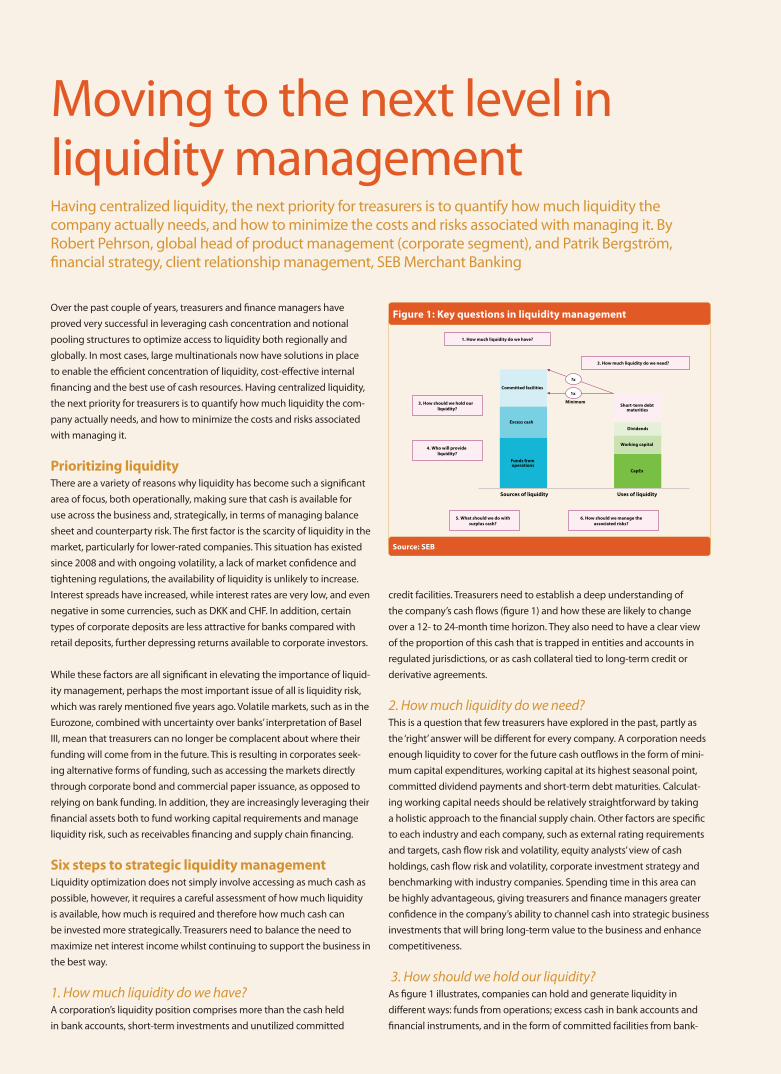

Six steps to strategic liquidity managementLiquidity optimization does not simply involve accessing as much cash as possible, however, it requires a careful assessment of how much liquidity is available, how much is required and therefore how much cash can be invested more strategically. Treasurers need to balance the need to maximize net interest income whilst continuing to support the business in the best way.

1. How much liquidity do we have? A corporation’s liquidity position comprises more than the cash held in bank accounts, short-term investments and unutilized committed

credit facilities. Treasurers need to establish a deep understanding of the company’s cash flows (figure 1) and how these are likely to change over a 12- to 24-month time horizon. They also need to have a clear view of the proportion of this cash that is trapped in entities and accounts in regulated jurisdictions, or as cash collateral tied to long-term credit or derivative agreements.

2. How much liquidity do we need? This is a question that few treasurers have explored in the past, partly as the ‘right’ answer will be different for every company. A corporation needs enough liquidity to cover for the future cash outflows in the form of mini-mum capital expenditures, working capital at its highest seasonal point, committed dividend payments and short-term debt maturities. Calculat-ing working capital needs should be relatively straightforward by taking a holistic approach to the financial supply chain. Other factors are specific to each industry and each company, such as external rating requirements and targets, cash flow risk and volatility, equity analysts’ view of cash holdings, cash flow risk and volatility, corporate investment strategy and benchmarking with industry companies. Spending time in this area can be highly advantageous, giving treasurers and finance managers greater confidence in the company’s ability to channel cash into strategic business investments that will bring long-term value to the business and enhance competitiveness.

3. How should we hold our liquidity? As figure 1 illustrates, companies can hold and generate liquidity in different ways: funds from operations; excess cash in bank accounts and financial instruments, and in the form of committed facilities from bank-

Funds from operations

Excess cash

Committed facilities

CapEx

Working capital

Dividends

Short-term debt maturities

1x

Minimum

?x

5. What should we do with surplus cash?

4. Who will provide liquidity?

3. How should we hold our liquidity?

2. How much liquidity do we need?

1. How much liquidity do we have?

6. How should we manage the associated risks?

Sources of liquidity Uses of liquidity

Figure 1: Key questions in liquidity management

Source: SEB

SEB_Liquidity_to print.indd 4 05/09/2012 15:52

5

JPM

orga

n •

Is yo

ur tr

easu

ry re

ady

for t

he n

ew g

loba

l rul

es?

ing partners. Again, there is no ‘right’ way to hold cash as it will differ by industry and individual company. In making the decision treasurers should balance costs and benefits for holding liquidity. Key areas in this respect include: cash flow dynamics; future potential investment opportunities; li-quidity risk (eg, reliability of long-term bank financing); the cost of facilities and interest rates obtainable in the market. Ongoing market volatility also means that this is a question treasurers should revisit regularly.

4. Who will provide liquidity? Related to the previous question, treasurers should identify the most reli-able sources of liquidity, which could be internal funding, banks, financial markets, suppliers and/or customers. As we have established previously, liquidity risk can come in a variety of forms, requiring a multi-faceted risk management approach. For example, we have noted the trend for corporate bond issuance, but also alternative sources of financing such as receivables financing and supply chain financing, leveraging companies’ own financial assets as sources of liquidity. Again, as the business evolves, and the shape of the financial supply chain shifts, the liquidity solutions that are optimal for a particular company are likely to change over time.

5. What should we do with surplus cash? Working through the previous questions will give treasurers a clear view about short-, medium- and long-term cash requirements, and the liquidity buffer that is required to mitigate risk. Treasurers can therefore divide their cash between operating cash that is required in the short term, and cash that can be invested for a longer period. During the early months of the global financial crisis, we saw a flight to liquidity, with companies placing large amounts of cash in short-term instruments. Low interest rates and enhanced counterparty risk management techniques are now motivat-ing treasurers to invest their cash more strategically to enhance yield. This issue has become further accentuated with the introduction of Basel III, as banks value some types of deposit more than others. Treasurers who have undertaken detailed calculations and scenario analysis to understand their liquidity needs will have more confidence in seeking the most favourable deposit terms and counterparties.

6. How should we manage the associated risks? We have mentioned liquidity risk, which is a key factor in deciding on the tenor of investments, but other forms of risk, such as counterparty and sovereign risk, are also key decision criteria. One way of managing these risks is to diversify investments across counterparties, tenors, instrument types and locations, and leverage inherently diversified instruments such as money market funds. In addition, risks related to the supply chain need to be managed.

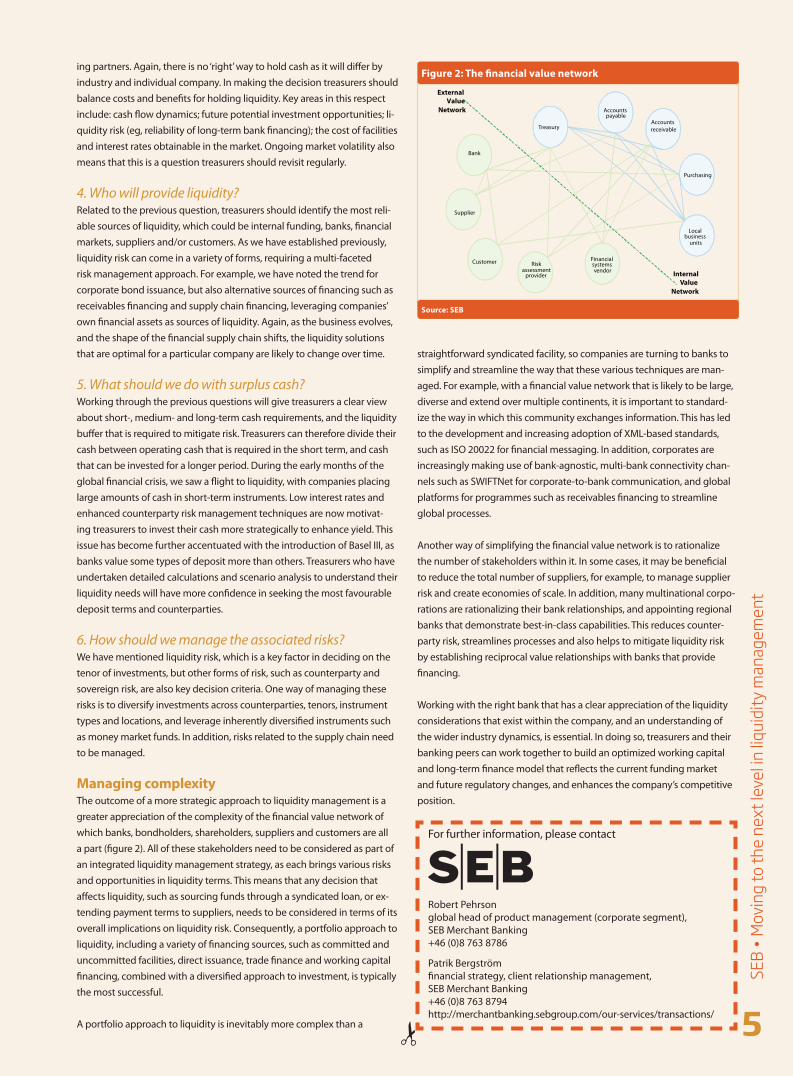

Managing complexityThe outcome of a more strategic approach to liquidity management is a greater appreciation of the complexity of the financial value network of which banks, bondholders, shareholders, suppliers and customers are all a part (figure 2). All of these stakeholders need to be considered as part of an integrated liquidity management strategy, as each brings various risks and opportunities in liquidity terms. This means that any decision that affects liquidity, such as sourcing funds through a syndicated loan, or ex-tending payment terms to suppliers, needs to be considered in terms of its overall implications on liquidity risk. Consequently, a portfolio approach to liquidity, including a variety of financing sources, such as committed and uncommitted facilities, direct issuance, trade finance and working capital financing, combined with a diversified approach to investment, is typically the most successful.

A portfolio approach to liquidity is inevitably more complex than a

straightforward syndicated facility, so companies are turning to banks to simplify and streamline the way that these various techniques are man-aged. For example, with a financial value network that is likely to be large, diverse and extend over multiple continents, it is important to standard-ize the way in which this community exchanges information. This has led to the development and increasing adoption of XML-based standards, such as ISO 20022 for financial messaging. In addition, corporates are increasingly making use of bank-agnostic, multi-bank connectivity chan-nels such as SWIFTNet for corporate-to-bank communication, and global platforms for programmes such as receivables financing to streamline global processes.

Another way of simplifying the financial value network is to rationalize the number of stakeholders within it. In some cases, it may be beneficial to reduce the total number of suppliers, for example, to manage supplier risk and create economies of scale. In addition, many multinational corpo-rations are rationalizing their bank relationships, and appointing regional banks that demonstrate best-in-class capabilities. This reduces counter-party risk, streamlines processes and also helps to mitigate liquidity risk by establishing reciprocal value relationships with banks that provide financing.

Working with the right bank that has a clear appreciation of the liquidity considerations that exist within the company, and an understanding of the wider industry dynamics, is essential. In doing so, treasurers and their banking peers can work together to build an optimized working capital and long-term finance model that reflects the current funding market and future regulatory changes, and enhances the company’s competitive position.

5

For further information, please contact

Robert Pehrson global head of product management (corporate segment), SEB Merchant Banking +46 (0)8 763 8786

Patrik Bergström financial strategy, client relationship management, SEB Merchant Banking+46 (0)8 763 8794http://merchantbanking.sebgroup.com/our-services/transactions/

SEB

• M

ovin

g to

the

next

leve

l in liq

uidi

ty m

anag

emen

t

1

Treasury

Purchasing

Accounts payable

Accounts receivable

Local business

units

Bank

Supplier

Customer Financial

systems vendor

External

Value

Network

Internal

Value

Network

Risk assessment provider

Figure 2: The financial value network

Source: SEB

SEB_Liquidity_to print.indd 5 07/09/2012 14:40

Bank Name Bank of America Merrill Lynch

Barclays BNP PARIBAS Citibank Commerzbank AG Deutsche Bank HSBC ING bank J.P. Morgan KBC RBS Santander SEB Standard Chartered Bank

Societe Generale UniCredit Bank

Cash Position ReportingIntra-day reporting of transactions: How many own bank branch countries reporting? 25 7 60 101 20 34 71 21 28 9 42 7 14 48 19 16

Are Third Party Banks' transactions accepted and processed? : Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes YesEnd Of Day Reports: How many own bank branch countries reporting? 25 21 60 101 20 35 71 21 28 9 42 7 16 48 57 21

Are there Third Party report monitoring & chasing services? Yes No Yes Yes Yes No Yes Yes No Yes No Yes Yes No No YesIs there real-time reporting of account balances? Yes No Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes No YesWhat reporting channels are used? (SWIFT, Online Portal, Email, Other - if other, please indicate) SWIFT, Online Portal,

Email, OtherSWIFT / Internet SWIFT, Online Portal,

OtherSWIFT, Online Portal,

Email, OtherSWIFT, Online Portal,

OtherSWIFT, Online Portal,

EmailSWIFT, Online Portal, Email and other (host to host connection)

SWIFT, Online Portal, Other

SWIFT, Online portal, Host-to-Host

connection

SWIFT, Online SWIFT, Online Portal, Other

SWIFT, Online portals, Other

SWIFT, Online Portal, Email, Other

SWIFT, Email, Online Portal

SWIFT, Online portals, Other

SWIFT, Online Portal, Other

What is the level of liquidity forecasting service functionality? Medium None None Medium Comprehensive Medium Medium, BTR reporting and links to

client ERP systems

Comprehensive Comprehensive Medium Balance & transaction reporting can be

exported into liquidity forecasting systems

None Comprehensive None Little Medium

Liquidity Management InfrastructureDo you provide a single global DDA for all cash management? Yes No No No Yes No Yes Yes No No Yes Yes No Yes Yes NoDo you provide pooling on the same liquidity management platform for all regions? Yes No Yes Yes Yes No Yes No All locations except

the US are on a single international platform

No Yes Yes Yes Yes Yes No

Sweeping and Pooling ServicesHeader/Master Account LocationsSingle Currency Pool (No. of countries): - physical 37 7 30 69 16 35 51 10 27 9 35 2 15 48 29 16

- notional 36 2 19 11 14 29 30 28 6 9 16 2 11 48 16 14No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

Multi-Currency Notional Pool: Asia-Pacific: 12 44 0 0 0 0 2 9 2 11 14 16 10 26 0 0 2 sites; 13 currencies 0 0 2 29 1 45 19 50 0 0 0 0Europe: 21 44 1 15 19 23 1 23 13 11 14 50 4 50 1 location; 43

currencies1 site; 24 currencies 9 50 2 29 9 45 2 50 1 country, 5 currencies 12 14

Latin America: 2 44 0 0 0 0 0 0 0 0 1 1 2 14 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0NAFTA: 2 44 0 0 0 0 0 0 1 11 1 4 1 18 0 0 0 0 0 0 0 0 1 45 1 50 0 0 0 0

Middle East & Africa: 0 0 0 0 0 0 0 0 0 0 0 0 5 10 0 0 0 0 0 0 0 0 0 0 18 50 0 0 0 0Cross-Border Sweeping Between Own BranchesEnd Of Day Sweeps: No. of countries where sweep can be last transaction*

of day: 37 6 26 40 16 35 19 28 20 9 23 7 8 48 19 13

Automated back-values for transactions with previous value date Yes No Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes No Yes Yes YesOvernight return sweeps Yes Yes Yes Yes No Yes Yes No Yes No Yes No Yes Yes No YesIntra-day sweeps within cut-off times: - No. of countries 36 6 30 43 16 18 30 28 25 9 35 6 11 48 16 13

- How swept: Automated Manual / Automated Automated Automated Automated Automated Automated Automated Automated Both Automated Automated Automated Automated Automated Both - How sweeps triggered: By Balance &/Or Time By Balance By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time

Cross-Border Multi-Bank SweepingNo. of existing MT 101 agreements: 100-199 200+ 200+ 200+ 200+ 50-99 200+ 200+ Circa 1000 200+ 400+ >50 100-199 100-199 380 200+Target End Of Day Sweeps - No. of countries: 36 32 29 38 25 26 18 28 0 9 0 21 19 48 15 13

- How swept: Automated Manual / automated Automated Automated Automated Automated Automated Manual/Automated NA Both NA Automated Automated Automated Automated Both - How sweep triggered: By Balance &/Or Time By Balance By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance NA By Balance &/Or Time NA By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time

Cross-border, cross-currency sweeping with auto FX-conversion Yes No No Yes Yes No Yes Yes Yes No Yes No NoIntra-day sweeps: - No. of countries: 36 0 29 Unlimited 25 14 8 28 0 9 88 No 19 48 11 0

- How swept: Automated N/A Automated Manual/Automated Automated Automated Automated Manual/Automated NA Both Fully Automated Automated Automated Automated - How sweep triggered: By Balance &/Or Time N/A By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time NA By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time

Notional Pooling ServicesSingle Country (all accounts in same country)Single Currency - Full off set (No. of countries): 35 3 6 11 14 14 20 2 6 9 16 11 18 16 14

% optimisation (No. of countries): 36 0 19 25 14 29 30 2 1 9 5 2 11 40 0 14Multi-Currency - Full off set (No. of countries): 35 1 6 3 14 3 10 43 3 9 4 11 1 0 0

% optimisation (No. of countries): 36 0 19 25 14 29 22 43 1 9 5 2 11 40 1 0No. of pooling currencies supported 44 15 23 25 10 50 50 28 24 50 29 1 45 50 5 0

Multi-Country (leave funds in each country)Single Currency - % optimisation (No. of countries): 36 0 19 25 14 29 53 15 13 9 35 12 40 0 0Multi-Currency - % optimisation (No. of countries): 36 0 19 25 14 29 53 9 13 0 35 12 40 0 0

No. of pooling currencies supported 44 0 23 26 10 50 50 4 17 50 29 45 50 0 0Investment of Excess CashBank Risk Profile: Credit rating of bank (S&P or Moody rating): S&P BANA A A2 AA- A-1 A/A-1 Moodys A2/S+P A+ A+ on HSBC Holdings

plcMoody's A3, S&P A A (S&P) A3 stable A (S&P) S&P: A- A+ AA- (S&P) A S&P & A2 Moodys Moody: A3

Tier One Capital Ratio (%) 10.78% 10.90% 12.20% 14.4% 12.30% 12.90% 10.40% 9.2% 10.4% 12.30% 10.80% 9.00% 16% 13.70% 9.4% 10.9%Investment Options: No. of currencies accepted for cash investments 44 40 4 19 11 26 50 12 28 50 30 21 23 50 50 50

Money Market Funds No. of funds - freely negotiable currencies

0 12 158 4 26 5 3 64 0 20 21 10 3 0 50

No. of funds - restricted currencies 0 Yes 0 0 0 0 4 0 0 0 0 0 0 0 0 0Investment Channels: Dedicated Investment Desk Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes

On-line Portal: - provided Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes - instruments available Bank & third party

instrumentsBank only instrument Bank & third party

instrumentsBank & third party

instrumentsOnly bank

instrumentsBank & third party

instrumentsBank only instruments Bank only instruments Bank & third party

instrumentsOnly bank instruments Bank & third party

instrumentsBank only instruments Bank & third party

instrumentsOnly bank instruments Bank & third party

instrumentsBank & third party

instrumentsTo Money Market Funds - automated sweeps to Yes No No Yes No Yes Yes No Yes No No No No Yes No Yes

- automated redemptions from Yes No No Yes No Yes Yes No Yes No No No No No No YesTo Other Instruments - automated sweeps to Yes No Yes Yes No Yes Yes Yes Yes No Yes No Yes Yes No No

- automated redemptions from Yes No Yes Yes No Yes Yes Yes Yes No Yes No Yes Yes No NoLiquidity Management SupportDedicated operational and customer support: Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes YesLiquidity models for client's private use - Analysis of cost of holding cash: Yes No No Yes No No Yes No No Yes Yes No No Yes No No

Showing impact of new structures: No No No Yes No No Yes No No Yes Yes No Yes Yes No NoContact Information

Contact Name: Greg Kavanaugh Andy Rudge Jan Rottiers Elyse Weiner Jasmin Maraslioglu Matthew Sagat Alkie Gan Willem Dokkum Clyde Muir Kristiaan Probst Rachel Kerrone Jose Luis Calderon Robert Pehrson Martijn Stoker Sophie Tarralle Markus StraußfeldCountry: United States United Kingdom Belgium United States Germany United States Hong Kong Netherlands United Kingdom Belgium United Kingdom Spain Sweden Singapore France Germany

Telephone Number: +1 312 904 8123 +44 7826 945146 +322 565 00 82 +1 212 816 0470 +49 136 46966 +1 212 250 5312 +852 2822 4062 +31 206523300 +44 207 134 4950 +32 2429 7925 +44 207678 3814 +34 91 289 4329 +46 705158786 +65 964189 +33142144284 +49 211 89 86 780Email Address: greg.kavanaugh@

elyse.weiner@ citi.com

alkiehkgan@ hsbc.com.hk

willem.dokkum@ ing.nl

rachel.kerrone@ rbs.com

robert.pehrson@ seb.se

martijn.stoker@ sc.com

Notes: * = except for investment Source: Cash management banks. Copyright ©2012 Euromoney

Table 1 - Euromoney 2012 Liquidity Management Survey

Bank Name Bank of America Merrill Lynch

Barclays BNP PARIBAS Citibank Commerzbank AG Deutsche Bank HSBC ING bank J.P. Morgan KBC RBS Santander SEB Standard Chartered Bank

Societe Generale UniCredit Bank

Cash Position ReportingIntra-day reporting of transactions: How many own bank branch countries reporting? 25 7 60 101 20 34 71 21 28 9 42 7 14 48 19 16

Are Third Party Banks' transactions accepted and processed? : Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes YesEnd Of Day Reports: How many own bank branch countries reporting? 25 21 60 101 20 35 71 21 28 9 42 7 16 48 57 21

Are there Third Party report monitoring & chasing services? Yes No Yes Yes Yes No Yes Yes No Yes No Yes Yes No No YesIs there real-time reporting of account balances? Yes No Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes No YesWhat reporting channels are used? (SWIFT, Online Portal, Email, Other - if other, please indicate) SWIFT, Online Portal,

Email, OtherSWIFT / Internet SWIFT, Online Portal,

OtherSWIFT, Email SWIFT, Online Portal,

OtherSWIFT, Online Portal,

EmailSWIFT, Online Portal, Email and other (host to host connection)

SWIFT, Online Portal, Other

SWIFT, Online portal, Host-to-Host

connection

SWIFT, Online SWIFT, Online Portal, Other

SWIFT, Online portals, Other

SWIFT, Online Portal, Email, Other

SWIFT, Email, Online Portal

SWIFT, Online portals, Other

SWIFT, Online Portal, Other

What is the level of liquidity forecasting service functionality? Medium None None Medium Comprehensive Medium Medium, BTR reporting and links to

client ERP systems

Comprehensive Comprehensive Medium Balance & transaction reporting can be

exported into liquidity forecasting systems

None Comprehensive None Little Medium

Liquidity Management InfrastructureDo you provide a single global DDA for all cash management? Yes No No No Yes No Yes Yes No No Yes Yes No Yes Yes NoDo you provide pooling on the same liquidity management platform for all regions? Yes No Yes Yes Yes No Yes No All locations except

the US are on a single international platform

No Yes Yes Yes Yes Yes No

Sweeping and Pooling ServicesHeader/Master Account LocationsSingle Currency Pool (No. of countries): - physical 37 7 30 69 16 35 51 10 27 9 35 2 15 48 29 16

- notional 36 2 19 11 14 29 30 28 6 9 16 2 11 48 16 14No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

No. of Sites

No. of Currencies

Multi-Currency Notional Pool: Asia-Pacific: 12 44 0 0 0 0 2 9 2 11 14 16 10 26 0 0 2 sites; 13 currencies 0 0 2 29 1 45 19 50 0 0 0 0Europe: 21 44 1 15 19 23 1 23 13 11 14 50 4 50 1 location; 43

currencies1 site; 24 currencies 9 50 2 29 9 45 2 50 1 country, 5 currencies 12 14

Latin America: 2 44 0 0 0 0 0 0 0 0 1 1 2 14 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0NAFTA: 2 44 0 0 0 0 0 0 1 11 1 4 1 18 0 0 0 0 0 0 0 0 1 45 1 50 0 0 0 0

Middle East & Africa: 0 0 0 0 0 0 0 0 0 0 0 0 5 10 0 0 0 0 0 0 0 0 0 0 18 50 0 0 0 0Cross-Border Sweeping Between Own BranchesEnd Of Day Sweeps: No. of countries where sweep can be last transaction*

of day: 37 6 26 40 16 35 19 28 20 9 23 7 8 48 19 13

Automated back-values for transactions with previous value date Yes No Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes No Yes Yes YesOvernight return sweeps Yes Yes Yes Yes No Yes Yes No Yes No Yes No Yes Yes No YesIntra-day sweeps within cut-off times: - No. of countries 36 6 30 43 16 18 30 28 25 9 35 6 11 48 16 13

- How swept: Automated Manual / Automated Automated Automated Automated Automated Automated Automated Automated Both Automated Automated Automated Automated Automated Both - How sweeps triggered: By Balance &/Or Time By Balance By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time

Cross-Border Multi-Bank SweepingNo. of existing MT 101 agreements: 100-199 200+ 200+ 200+ 200+ 50-99 200+ 200+ Circa 1000 200+ 400+ >50 100-199 100-199 380 200+Target End Of Day Sweeps - No. of countries: 36 32 29 38 25 26 18 28 0 9 0 21 19 48 15 13

- How swept: Automated Manual / automated Automated Automated Automated Automated Automated Manual/Automated NA Both NA Automated Automated Automated Automated Both - How sweep triggered: By Balance &/Or Time By Balance By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance NA By Balance &/Or Time NA By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time

Cross-border, cross-currency sweeping with auto FX-conversion Yes No No Yes Yes No Yes Yes Yes No Yes No NoIntra-day sweeps: - No. of countries: 36 0 29 Unlimited 25 14 8 28 0 9 88 No 19 48 11 0

- How swept: Automated N/A Automated Manual/Automated Automated Automated Automated Manual/Automated NA Both Fully Automated Automated Automated Automated - How sweep triggered: By Balance &/Or Time N/A By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time NA By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time By Balance &/Or Time

Notional Pooling ServicesSingle Country (all accounts in same country)Single Currency - Full off set (No. of countries): 35 3 6 11 14 14 20 2 6 9 16 11 18 16 14

% optimisation (No. of countries): 36 0 19 25 14 29 30 2 1 9 5 2 11 40 0 14Multi-Currency - Full off set (No. of countries): 35 1 6 3 14 3 10 43 3 9 4 11 1 0 0

% optimisation (No. of countries): 36 0 19 25 14 29 22 43 1 9 5 2 11 40 1 0No. of pooling currencies supported 44 15 23 25 10 50 50 28 24 50 29 1 45 50 5 0

Multi-Country (leave funds in each country)Single Currency - % optimisation (No. of countries): 36 0 19 25 14 29 53 15 13 9 35 12 40 0 0Multi-Currency - % optimisation (No. of countries): 36 0 19 25 14 29 53 9 13 0 35 12 40 0 0

No. of pooling currencies supported 44 0 23 26 10 50 50 4 17 50 29 45 50 0 0Investment of Excess CashBank Risk Profile: Credit rating of bank (S&P or Moody rating): S&P BANA A A2 AA- A-1 A/A-1 Moodys A2/S+P A+ A+ on HSBC Holdings

plcMoody's A3, S&P A A (S&P) A3 stable A (S&P) S&P: A- A+ AA- (S&P) A S&P & A2 Moodys Moody: A3

Tier One Capital Ratio (%) 10.78% 10.90% 12.20% ? 12.30% 12.90% 10.40% 9.2% 10.4% 12.30% 10.80% 9.00% 16% 13.70% 9.4% 10.9%Investment Options: No. of currencies accepted for cash investments 44 40 4 19 11 26 50 12 28 50 30 21 23 50 50 50

Money Market Funds No. of funds - freely negotiable currencies

0 12 158 4 26 5 3 64 0 20 21 10 3 0 50

No. of funds - restricted currencies 0 Yes 0 0 0 0 4 0 0 0 0 0 0 0 0 0Investment Channels: Dedicated Investment Desk Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes

On-line Portal: - provided Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes - instruments available Bank & third party

instrumentsBank only instrument Bank & third party

instrumentsBank & third party

instrumentsOnly bank

instrumentsBank & third party

instrumentsBank only instruments Bank only instruments Bank & third party

instrumentsOnly bank instruments Bank & third party

instrumentsBank only instruments Bank & third party

instrumentsOnly bank instruments Bank & third party

instrumentsBank & third party

instrumentsTo Money Market Funds - automated sweeps to Yes No No Yes No Yes Yes No Yes No No No No Yes No Yes

- automated redemptions from Yes No No Yes No Yes Yes No Yes No No No No No No YesTo Other Instruments - automated sweeps to Yes No Yes Yes No Yes Yes Yes Yes No Yes No Yes Yes No No

- automated redemptions from Yes No Yes Yes No Yes Yes Yes Yes No Yes No Yes Yes No NoLiquidity Management SupportDedicated operational and customer support: Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes YesLiquidity models for client's private use - Analysis of cost of holding cash: Yes No No Yes No No Yes No No Yes Yes No No Yes No No

Showing impact of new structures: No No No Yes No No Yes No No Yes Yes No Yes Yes No NoContact Information

Contact Name: Greg Kavanaugh Andy Rudge Jan Rottiers Elyse Weiner Jasmin Maraslioglu Matthew Sagat Alkie Gan Willem Dokkum Clyde Muir Kristiaan Probst Rachel Kerrone Jose Luis Calderon Robert Pehrson Martijn Stoker Sophie Tarralle Markus StraußfeldCountry: United States United Kingdom Belgium United States Germany United States Hong Kong Netherlands United Kingdom Belgium United Kingdom Spain Sweden Singapore France Germany

Telephone Number: +1 312 904 8123 +44 7826 945146 +322 565 00 82 +1 212 816 0470 +49 136 46966 +1 212 250 5312 +852 2822 4062 +31 206523300 +44 207 134 4950 +32 2429 7925 +44 207678 3814 +34 91 289 4329 +46 705158786 +65 964189 +33142144284 +49 211 89 86 780Email Address: greg.kavanaugh@

elyse.weiner@ citi.com

alkiehkgan@ hsbc.com.hk

willem.dokkum@ ing.nl

rachel.kerrone@ rbs.com

robert.pehrson@ seb.se

martijn.stoker@ sc.com

Notes: * = except for investment Source: Cash management banks. Copyright ©2012 Euromoney 20

12 G

UIDE

TO

LIQU

IDIT

Y M

ANAG

EMEN

T

7

Table Daniel 280812.indd 7 05/09/2012 15:54

Liquidity management: Managing the risksCorporate treasurers and their bank counterparts are starting to employ similar strategies in dealing with liquidity risk. Both have learned valuable lessons over the past few years, and now it’s time to put them to good use. by Martijn Stoker, Director, Global Head Liquidity Management, Transaction Banking, at Standard Chartered Bank

Liquidity risk management can be seen as two sides of the same coin. Increasingly, the needs of both banks and corporates are converging as liquidity is the life blood for the survival of both. Developing an effective risk governance structure involves measuring your organization’s risk appetite, defining strategies to limit these risks and testing the efficacy of your oversight measures. All of this will need to be supported by the right systems and procedures.

Corporate treasury is rapidly evolving from a task-based department into the financial ‘nerve’ centre of the organization. At the same time, treasurers at corporates and banks are becoming more and more aligned in terms of risk management practices, as both need to be fully aware of the impact of liquidity risks on their business activities.

Invisible riskThe collapses of Northern Rock and Bear Stearns prove that profitability and capital are no defence against liquidity risk. Both made profits in the quarter before they defaulted and both were well-capitalized businesses. And yet, as a result of their failure to deal with their liquidity risk issues, they vanished. The fact is, no one talked much about liquidity risk and as a result, liquidity was largely an invisible risk for many firms.

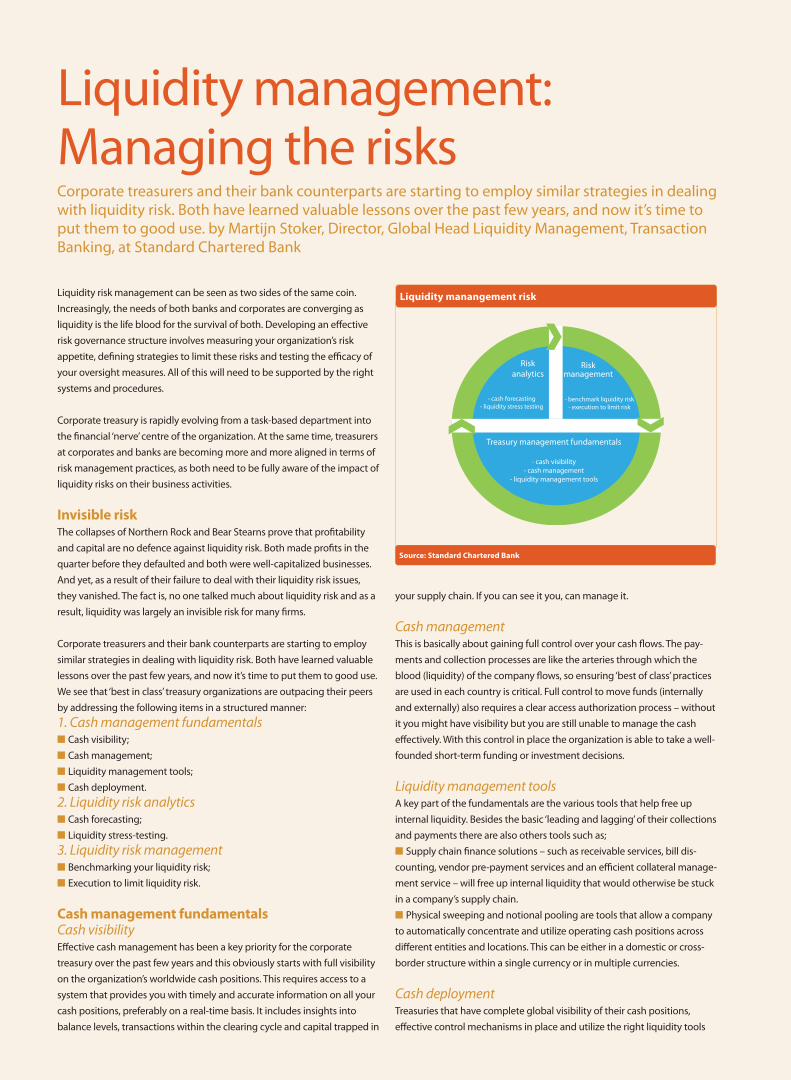

Corporate treasurers and their bank counterparts are starting to employ similar strategies in dealing with liquidity risk. Both have learned valuable lessons over the past few years, and now it’s time to put them to good use. We see that ‘best in class’ treasury organizations are outpacing their peers by addressing the following items in a structured manner: 1. Cash management fundamentals n Cash visibility; n Cash management; n Liquidity management tools; n Cash deployment. 2. Liquidity risk analytics n Cash forecasting; n Liquidity stress-testing. 3. Liquidity risk management n Benchmarking your liquidity risk; n Execution to limit liquidity risk.

Cash management fundamentalsCash visibilityEffective cash management has been a key priority for the corporate treasury over the past few years and this obviously starts with full visibility on the organization’s worldwide cash positions. This requires access to a system that provides you with timely and accurate information on all your cash positions, preferably on a real-time basis. It includes insights into balance levels, transactions within the clearing cycle and capital trapped in

your supply chain. If you can see it you, can manage it.

Cash managementThis is basically about gaining full control over your cash flows. The pay-ments and collection processes are like the arteries through which the blood (liquidity) of the company flows, so ensuring ‘best of class’ practices are used in each country is critical. Full control to move funds (internally and externally) also requires a clear access authorization process – without it you might have visibility but you are still unable to manage the cash effectively. With this control in place the organization is able to take a well-founded short-term funding or investment decisions.

Liquidity management toolsA key part of the fundamentals are the various tools that help free up internal liquidity. Besides the basic ‘leading and lagging’ of their collections and payments there are also others tools such as; n Supply chain finance solutions – such as receivable services, bill dis-counting, vendor pre-payment services and an efficient collateral manage-ment service – will free up internal liquidity that would otherwise be stuck in a company’s supply chain. n Physical sweeping and notional pooling are tools that allow a company to automatically concentrate and utilize operating cash positions across different entities and locations. This can be either in a domestic or cross-border structure within a single currency or in multiple currencies.

Cash deploymentTreasuries that have complete global visibility of their cash positions, effective control mechanisms in place and utilize the right liquidity tools

Riskanalytics

Riskmanagement

Treasury management fundamentals

- cash visibility- cash management

- liquidity management tools

- cash forecasting- liquidity stress testing

- benchmark liquidity risk- execution to limit risk

Liquidity manangement risk

Source: Standard Chartered Bank

StanChart_Liquidity_V4.indd 8 06/09/2012 15:00

9

Stan

dard

Cha

rter

ed B

ank •

Liq

uidi

ty m

anag

emen

t: M

anag

ing

the

risks

are in a better position to deploy their cash where and when it’s needed. Intercompany lending provided to operating companies, either directly or indirectly via multi-entity physical sweeping structures, limits the need for external funding.

Based on the lessons learned in the financial crisis, cash will be even more valuable in the future. These changes also bring opportunities for corporate treasurers. With upcoming regulatory changes around Basel III, balances linked to operating business may provide a valuable alternative to other short-term investments as banks will start to provide more incen-tives in order to hold on to operating account balances.

Liquidity risk analyticsOver the past year many banks have been reviewing their liquidity policy statements and contingency funding plans and are challenging the as-sumptions made that underpin their behavioural modelling and funding mismatch guidelines. These items should also be a vital part of any corpo-rate liquidity risk analytics toolkit and could be linked to the company’s cash flow forecasting and liquidity stress testing.

Cash forecastingIndustry-leading treasuries have all the cash management fundamentals in place and are currently focusing on improving their cash forecasting methodologies and systems. The quality rather than quantity of data is the critical factor. Industry leaders tend to use the following framework: n Senior management support – top management needs to acknowl-edge the strategic importance of cash flow forecasting and give incen-tives to encourage the right behaviour. n Decide what data will be used – it is critical that an organization identi-fies the most relevant data that will provide the needed information. The data is usually captured from multiple sources. n Automatically link the above data sources to the forecasting tool – most organizations spend more time on bringing all the information together than they spend on validating, analyzing and acting on the information. n Performance testing – understand how accurate your forecast is and find out what the critical drivers are. You need to understand the differ-ence between the forecast and the actual results. Optimizing the model could take up 80% of your time spent on cash flow forecasting and this is usually underestimated. This is where most corporate treasuries stop, but taking the next step is just as important. To be able to understand the impact of changes in the underlying drivers you need to perform a scenario analysis or stress test.

Liquidity scenario-testingAll treasurers are struggling to better understand and monitor the inter-relationships between market, credit and liquidity risk. A practical way of dealing with scenario testing is to follow a three-step approach: n Identify liquidity risk drivers such as: Decreasing sales margins and increased costs of goods; Evaporating funding; Decline in value of liquid assets. n Design scenarios and assign probabilities: External scenarios such as a market shock in your line of business, market risk (rates, FX or commodi-ties); Internal scenarios such as operational risks resulting in claims, rating downgrade impacting your loan covenants; Ad-hoc scenarios covering industry or country specific events. n Model the scenarios: Step 1: Quantify the liquidity outflows in all scenarios for each of the defined risk drivers; Step 2: Identify the potential cash inflows to mitigate the liquidity shortfalls identified; Step 3: Deter-mine what your net liquidity position is under each scenario.

Liquidity risk managementEven with having the cash management fundamentals in place and being able to forecast your cash positions, plus what the impact of different scenarios on those positions will be, you are only half way there. The next step is to determine what the acceptable risk levels are and, more importantly, what is not an acceptable risk level any more. This requires benchmarks that are clearly communicated within the organization.

Benchmarking your liquidity riskThe benchmark for liquidity management tools should be the most ef-ficient method of freeing up internal cash. Depending on the company’s operating model, solutions such as supply chain financing and physical sweeping and notional pooling structures should be optimized.

In the current environment companies should consider a careful review of their investment objectives, portfolio characteristics, risk tolerance, invest-ment credit quality, limits and performance.

Clear investment guidelines and benchmarks will provide a common basis for understanding the investment practices within your company.

Execution to limit liquidity riskLiquidity risk management is entering a new and much more demand-ing era whereby speed of execution is of the utmost importance. This requires the support of a bank that understands your business model and the specific markets you are in, and that is able to provide you the latest technology and advice to grow your business.

Too often the systems capturing information on operational/business risks, counterparty/credit risks and market risks are separated. It’s time to combine these, remove the silos created by banks and corporates alike and have a more holistic view on how to manage liquidity risks.

ConclusionIn the end it’s all about an effective risk governance structure – what is your risk appetite, what are your limits, what are your strategies to limit these risks and how effective is your oversight?

Due to the changed market circumstances some corporates and most banks are changing their risk policies. They are all changing the way they work today. Most companies have a management committee made up of the top senior managers and the treasurer, and their main responsibility is the formulation of risk management policies for the company. Treasur-ers are mostly charged with the implementation of such policies, with the committee having oversight responsibility. Besides efficient systems and processes there is a need to weave this new risk awareness attitude into the social fibre of the organization, to create a real liquidity risk management culture.

9

For further information, please contact

Martijn StokerTel: +65 6596 4189http://wholesalebanking.standardchartered.com

Stan

dard

Cha

rter

ed B

ank •

Liq

uidi

ty m

anag

emen

t: M

anag

ing

the

risks

StanChart_Liquidity_V4.indd 9 06/09/2012 15:00

Deutsche Bank does not provide pooling on the same liquidity manage-ment platform for all regions. Despite this, Rossi says that the bank does manage concentration and pooling services on a global basis but chooses to o� er them based on strategic regional � nancial hubs to sup-port and address local market regulatory and legal requirements. “Many of our clients prefer to combine the two by having a locally managed regional structure that works in conjunction with a centrally managed global overlay,” she says. “The chief advantage of this is that transaction-related information and reporting can be viewed centrally or regionally, depending on our clients’ individual requirements.”

Sweeping and pooling servicesIf visibility of cash is essential to be able to deploy cash e� ectively, then it is sweeping and notional pooling that provide the control that treasurers increasingly require (see boxes on electronics and retailer case studies). “Our clients are operating in an environment of multiple currencies, jurisdictions and legal entities,” says Greg Kavanaugh, head of global liquidity at Bank of America Merrill Lynch, which has re-launched its single-currency and multi-currency notional pooling o� ering recently. “By o� ering both notional and physical cash concentration options, we can help them improve the value they receive from their liquidity balances around the globe.”

All the participating banks o� er both single-currency physical and notional cash pools. Citi has the largest number of locations for physical pools (69) and Standard Chartered the largest number for notional pools (48). Europe continues to o� er the largest number of locations for banks o� ering multi-currency notional pools: within the region Bank of America Merrill Lynch o� ers the greatest number of sites (21) while Deutsche Bank, KBC and Standard Chartered tie to o� er the greatest number of currencies (50).

In Asia, Standard Chartered has the most multi-currency notional pooling

locations with 19 (up from 14 last year). “Enhancements – to deliver fully integrated liquidity management solutions globally – are being made to cross-currency cash concentration, integrated multi-bank sweeping capabilities and multi-currency notional pooling solutions,” says Stocker. Interestingly, Standard Chartered also o� ers online ‘simulation pooling’ capabilities for clients that want to analyse various pooling options.

Weiner at Citi says that expanding and enhancing the bank’s cross-border cash concentration services to provide clients with the highest level of coverage across their operating networks has been the most important liquidity management development at Citi in the past 12 months. “Over the last year, we have extended the application of our concentration engine to over 44 countries, with even more imminently available,” she says. “Along with that expansion comes a host of features that allow our clients to customize liquidity structures in respect of regulations and tax considerations as well as unique operational requirements.”

SweepingAll of the banks in the survey can now ensure that a sweep is the last transaction of the day (last year one bank could not): Standard Chartered continues to o� er the largest number of countries where this service is available. Two banks do not provide automated back values for transac-tions with previous value dates. All but � ve of the banks o� er overnight return sweeps, most triggered by balance or time. All the banks o� er automated intra-day sweeps within cut-o� times, most triggered by bal-ance or time.

All the participating banks have multiple MT101 partner bank drawdown agreements, 11 banks with 200 partners or more compared to last year’s nine. “This increase may re� ect an increasing emphasis by corporates of the need to improve visibility and control while managing counterparty risk,” says Steve Everett, global head of cash management and head of transaction services products EMEA at RBS. “The idea that e� ciency can

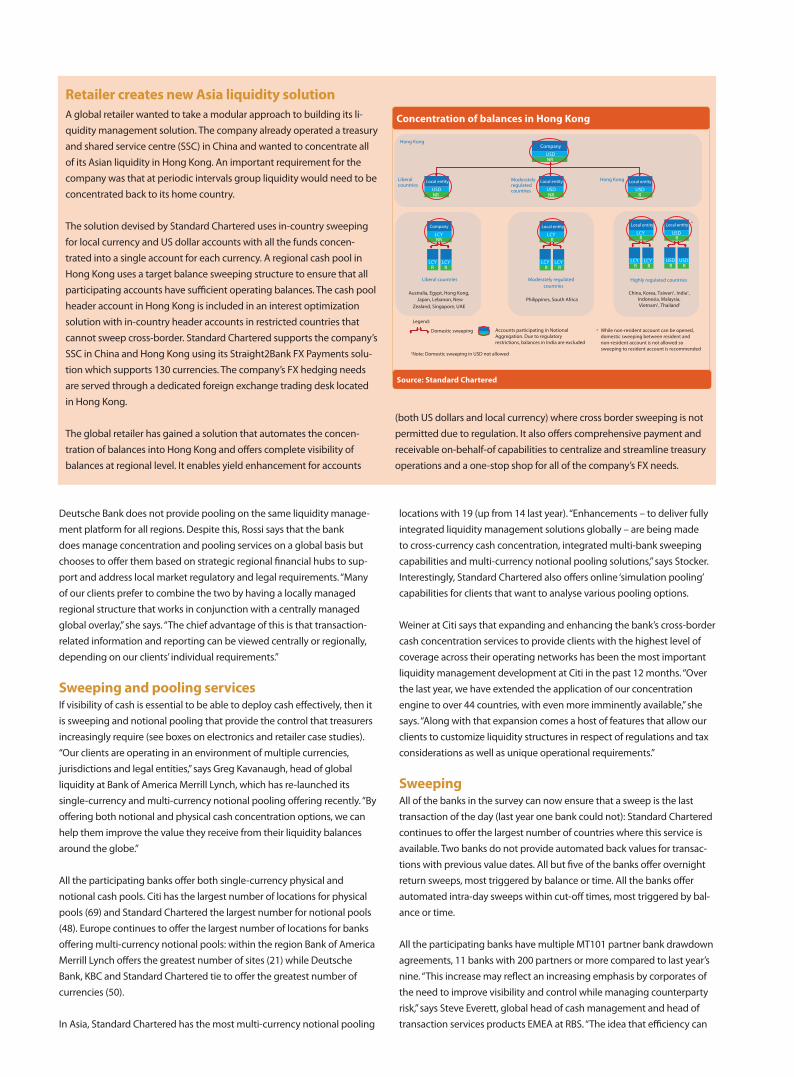

Retailer creates new Asia liquidity solutionA global retailer wanted to take a modular approach to building its li-quidity management solution. The company already operated a treasury and shared service centre (SSC) in China and wanted to concentrate all of its Asian liquidity in Hong Kong. An important requirement for the company was that at periodic intervals group liquidity would need to be concentrated back to its home country.

The solution devised by Standard Chartered uses in-country sweeping for local currency and US dollar accounts with all the funds concen-trated into a single account for each currency. A regional cash pool in Hong Kong uses a target balance sweeping structure to ensure that all participating accounts have su� cient operating balances. The cash pool header account in Hong Kong is included in an interest optimization solution with in-country header accounts in restricted countries that cannot sweep cross-border. Standard Chartered supports the company’s SSC in China and Hong Kong using its Straight2Bank FX Payments solu-tion which supports 130 currencies. The company’s FX hedging needs are served through a dedicated foreign exchange trading desk located in Hong Kong.

The global retailer has gained a solution that automates the concen-tration of balances into Hong Kong and o� ers complete visibility of balances at regional level. It enables yield enhancement for accounts

(both US dollars and local currency) where cross border sweeping is not permitted due to regulation. It also o� ers comprehensive payment and receivable on-behalf-of capabilities to centralize and streamline treasury operations and a one-stop shop for all of the company’s FX needs.

USD NR

Company

LCY NR

Company

LCY R

LCY R

Liberal countries

Australia, Egypt, Hong Kong, Japan, Lebanon, New

Zealand, Singapore, UAE

LCY R

Local entity

LCY R

LCY R

Moderately regulated countries

Philippines, South Africa

USD R

USD R

Highly regulated countries

China, Korea, Taiwan1, India1, Indonesia, Malaysia, Vietnam1, Thailand1

Hong Kong

LCY R

Local entity

LCY R

LCY R

USD R

Local entity * *

USD NR

Local entity Liberal countries

USD NR

Local entity Moderately regulated countries

Accounts participating in Notional Aggregation. Due to regulatory restrictions, balances in India are excluded

Legend:

Domestic sweeping * While non-resident account can be opened, domestic sweeping between resident and non-resident account is not allowed so sweeping to resident account is recommended

1Note: Domestic sweeping in USD not allowed

USD R

Local entity Hong Kong

Concentration of balances in Hong Kong

Source: Standard Chartered

Laurence_V3.indd 10 05/09/2012 15:51

11

LIQU

IDIT

Y M

ANAG

EMEN

T SU

RVEY

201

2 •

Look

ing

to th

e lo

ng te

rm

only be delivered by working with one bank is no longer widely held.”

JP Morgan has one of the largest numbers of MT101 agreements (over 1,000) in place for multi-bank sweeping. The bank’s Hagopian says that bilateral agreements are important for the bank’s capabilities. “Multi-bank sweeping leverages these bilateral agreements by issuing MT101 drawdown messages to automatically concentrate funds from a client’s global relationship banks into a single position with an overlay bank, thus enabling more efficient use of the consolidated global position,” she explains. JP Morgan can also concentrate funds in countries where Swift is not the standard method of bank-to-bank communication.

The importance of multi-bank sweeping is increasingly reflected in the design of other products. Among the services launched in the past year by Société Générale’s newly created Global Transaction Banking business line is a re-designed cross-border cross-currency notional pooling solu-tion, which allows clients to notionally manage their global cash position in a unique reference currency, without any need for FX transactions or swaps. Crucially, it “can adapt to any multi-bank cash concentration

structure already in place and include the countries of the clients’ choice,” notes Sophie Tarralle, head of cash pooling products, global transaction banking, at the bank. Additional enhancements in the coming months will include an integrated reporting service to facilitate intercompany loans management in a multi-bank environment.

More generally, sweeping has come to the fore in the past year with a number of leading companies announcing – presumably for the benefit of investors – that they are taking precautions against the threat of an exit by a eurozone member or even a break-up of the currency union: Voda-fone says it sweeps funds daily; GSK that it keeps nothing in the eurozone overnight and WPP says that it not only keeps nothing in the eurozone overnight, but swaps it all to dollars every night (see box on Diageo case study). “For global companies with the ability to sweep and hold cash in different countries, the quest for security means that cash balances are frequently being swept out of continental European countries and into UK bank accounts on a nightly basis by many of the world’s largest companies,” says David Manson, global head of liquidity management at Barclays.

InvestmentThis year’s liquidity management survey shows that all but one of the banks accept a range of 10 currencies or more for cash investments. A handful of banks – HSBC, KBC, Société Générale, Standard Chartered and UniCredit accept 50 currencies. “Our cash investment capabilities complement our cash management services,” explains HSBC’s Schickler. “As we offer deep local payable and receivables solutions in nearly every market in which we operate, it is necessary to offer local currency services that correlate accordingly. As most developed market interest rates remain low if not close to zero, some companies are choosing to accept heightened FX exposure in order to generate increased returns on their cash portfolio.”

In line with the 2011 survey, this year’s survey shows that all the banks provide both an investment desk and an investment portal, with just over half providing investment instruments from other financial institutions as well as their own bank.

For corporates, the turbulent macro-economic and financial environment has created a conundrum in relation to investment. According to Tarralle at Société Générale, they have been unwilling to invest in the business

Diageo plans for any eurozone eventualityWith storm clouds darkening over the eurozone, the extreme volatility of market and economic conditions has been a concern for corporate treasury teams worldwide, especially for those that operate in Europe. Specifically, fears have mounted regarding the potential for assets to be effectively frozen should problems in a country in the eurozone deepen. Diageo’s treasury team wanted to plan to reduce the impact of such a scenario. Its treasury function operates as an in-house corporate bank and all cash is concentrated in London. To minimise its exposure, the company wanted to find a reliable and risk-managed solution to enable consolidation of cash flows, while establishing centralised control in London.

Diageo’s solution was to partner with Bank of America Merrill Lynch to work through the impact of different scenarios on its cash manage-ment structures to enable it to put in place the right contingency planning to make sure it could minimise potential disruption.

The solution allows Diageo to configure parameters according to its exact requirements to provide unprecedented control over its in-country cash positions. Specifically, it enables the company to refine existing sweeping functionality to incorporate real time benefits and to automatically calculate and pull balances from third-party bank accounts in specific countries for repatriation to the UK, where regula-tions are supportive. It also allows Diageo to instantly restrict any outgoing payments in the event of a sudden change in the market conditions, in line with its cash management policy.

Implementation of the solution has ensured that Diageo could retain its local bank accounts in the countries with both Bank of America Merrill Lynch and its various third-party banks, for its daily payables/receivables management. The seamless flow of funds in and out of the centralised liquidity structure enables it to effectively manage its risk and limit exposure. However, the structure significantly reduces the risk of losing any cash associated with the intra-day movement of funds. In these unprecedented economic times, Diageo’s foresight provides treasury teams with a smart solution to protect their cash in the event of a crisis incident.

Martijn Stocker, global head, liquidity management, transaction banking, Standard Chartered

Laurence_V3.indd 11 05/09/2012 15:51

Is your treasury ready for the new global rules?For most of the past decade, treasurers have coped with challenges to their corporations’ liquidity management – from financial markets melting down to a global recession, potential national defaults and regional debt imbalances. In response to these increased stresses and a sustained low interest rate environment, these finance executives have accumulated historically unprecedented levels of cash

The objective of the cash accumulation has been to maintain a cushion against future challenges to their organizations’ access to capital and pro-vide flexibility to fund strategic opportunities. A recent Treasury Strategies study placed corporate cash holdings by US companies at $2.23 trillion, €1.9 billion for companies in the eurozone and £785 billion for those in the UK (as of 31 December 2011). And, in the US, corporations hold almost 75% of total liquidity in overnight investments, money funds and bank deposits, according to the treasury consulting firm’s study.

Although a survey last year by the Association for Financial Professionals (AFP) indicates that the drive to build cash has abated somewhat as eco-nomic conditions have improved, most corporations still find themselves awash with short-term funds. Now, however, they face more limited options for cash placement, thanks to a host of shifting market conditions and impending rule changes.

Rather than another global challenge, finance executives are about to

confront a raft of new global and US regulations instituted in the wake of the economic collapse and designed to strengthen the overall stability of the markets. Ostensibly aimed at financial institutions to prevent some future unknown threat from spilling over into the broader economy, these new rules are also likely to drive treasurers to rethink investment choices for short-term cash in terms of risk profile, liquidity and return.

A quick look at the regulationsIn the US, the Dodd-Frank Wall Street Reform and Consumer Protection Act mandates, among other things, unlimited Federal Deposit Insur-ance Corporation (FDIC) protection for balances in non-interest bearing transaction accounts. However, that protection may expire at the end of this year. The end of this insurance coverage may add a degree of risk to an otherwise conservative cash strategy.

The Basel III Accord will take effect over the next several years. It will establish new global standards on bank capital adequacy and market risk. Banks will be required to maintain strong liquidity buffers of high-quality assets – mainly government-backed – against a portion

of any deposit that does not have a term of greater than 30 days. In cases where deposits are not considered operating funds this new requirement may significantly limit the value and desirability of short-term funds for banks.

Finally, there is also the potential for new regulations affecting money market funds. The changes under consideration include capital require-ments, holdback provisions and variable fund net asset values.

Preparing your treasury While the full impact of the rule changes has yet to play out, their aim is to require a higher degree of precision in liquidity and investment management.

Here is a checklist of questions treasurers may want to consider, not only to protect short-term funds and invest them wisely, but also to maximize their value in this changing environment. The list is simply an attempt to

raise awareness about some initial issues facing treasuries, and help to begin a dialogue within your companies and with your bankers about the impact of change.

Operating cash at banksFirst, take a look at operating cash being held at banks. This is cash that can provide a tremendous source of value in times of crisis. Key elements to consider are the complexity of managing cash flows across your operating relationships, particularly in times of market stress, and the importance placed on having the right partnership with your primary operating bank. n Have you adequately assessed the resilience of your operating banks? Have you examined their capital strength? n Have you explored how the expected removal of unlimited FDIC insurance at the end of 2012 for non-interest bearing balances will impact your management of counterparty limits? n Should full FDIC coverage expire, will you require additional counterparties? If yes, have you calculated the risks and costs of managing a larger number of counterparties? n Have you identified the implied term extension of your operating cash?

"While the full impact of the rule changes has yet to play out, their aim is to require a higher degree of precision in liquidity and investment management.”

JPM_Liquidity_V8.indd 16 06/09/2012 14:11

17

JPM

orga

n •

Is yo

ur tr

easu

ry re

ady

for t

he n

ew g

loba

l rul

es?

n Where possible, have you explored how cash concentration structures – within a currency and cross-currency – can help provide visibility into counterparty exposures and mobilize cash quickly? n Are you regularly reviewing your investment policy to ensure that there is enough flexibility to make changes quickly? n When looking at counterparty limits vis-à-vis investment duration, have you analyzed your level of liquid versus term cash in determining limits? n Have you maximized the return on your bank operating balances through earnings credit rate (ECR) programmes? n Have you explored extending your ECR programmes globally to get more value for operating cash? Have you talked to your bank about extending ECR value to non-traditional operating product classes?

Non-operating short-term deposits at banksUnder Basel III, financial institutions will have to maintain liquidity buffers of high-quality assets against a portion of any deposit that does not have a term of greater than 30 days. In many cases, this may significantly limit the value of these funds to both banks and corporations. n Have you discussed with your counterparties the disposition of non-operating balances post-Basel III? n Have you asked if pro-forma reporting by banks in 2012 through 2014 could accelerate the impact of Basel III regulations prior to full industry adoption in 2015? n Have you examined your balances and sources of cash to determine which funds might qualify as operating balances? n Are there other options for these funds, such as laddered contractual terms or other means of extending contractual term while retaining liquidity?

Money market fund placements Money market mutual funds are still among the most popular investments for corporate cash, providing an excellent source of liquidity and

diversification. However, the new rules being considered, especially for funds operating in FINRA jurisdictions, may ultimately affect their overall utility and raise questions about how and when to appropriately use them. n Have you considered expanding your money market fund programme to include additional currencies? n For non-operating short-term cash, how do you balance diversification while effectively monitoring counterparty investment limits? n Are you considering changes in response to the new regulations? For example, will you alter the amount of money you will put into money market funds given new liquidity requirements? n Have you considered the implications for your investment guidelines of floating net asset values or holdback provisions? What Enterprise Risk Management (ERM) or other systems (eg, tax) updates would you require? n Have you looked at the potential impact on operating accounts if funds are swept to a floating Net Asset Value (NAV) programme? On reconciliation systems?

Secured investment alternativesThe regulatory changes and market dynamics, including the proposed expiration of unlimited FDIC insurance, may also drive financial managers to consider alternative, high-quality secured investments. n Are you appropriately positioned in terms of credit and concentration risk? Will your positioning change if unlimited FDIC insurance expires for transaction balances? n Are you prepared as short-term market rates trend negative in a growing number of currencies? n Have you explored secured short-term investments, such as non-traditional repo or collateralized commercial paper, as part of a diversified cash management strategy in light of expiring unlimited FDIC coverage?

The time seems ripe to assess how best to prepare for the impending changes and begin to review the innovative ways available to meet these new challenges. J.P. Morgan stands ready to assist. If you would like to discuss these issues further, contact your local relationship manager or e-mail: [email protected].

13

For further information, please contact

e-mail: [email protected]

JPM

orga

n •

Is yo

ur tr

easu

ry re

ady

for t

he n

ew g

loba

l rul

es?

Phillip Lindow, Head of J.P. Morgan treasury & securities services liquidity solutions

JPM_Liquidity_V8.indd 17 06/09/2012 14:11