Embed Size (px)

DESCRIPTION

Abridged version of my presentation at the IFSB Seminar held in Istanbul 1st October 2010. Discusses the key bottlenecks constraining liquidity and what can be done to ease the flow of liquidity.

Citation preview

LIQUIDITY & ISLAMIC CAPITAL MARKETSMARKETS SALES AND TRADING TREASURY

ISLAMIC FINANCE

SAYD FAROOK, GLOBAL HEAD ISLAMIC CAPITAL MARKETS 01 OCTOBER 2010

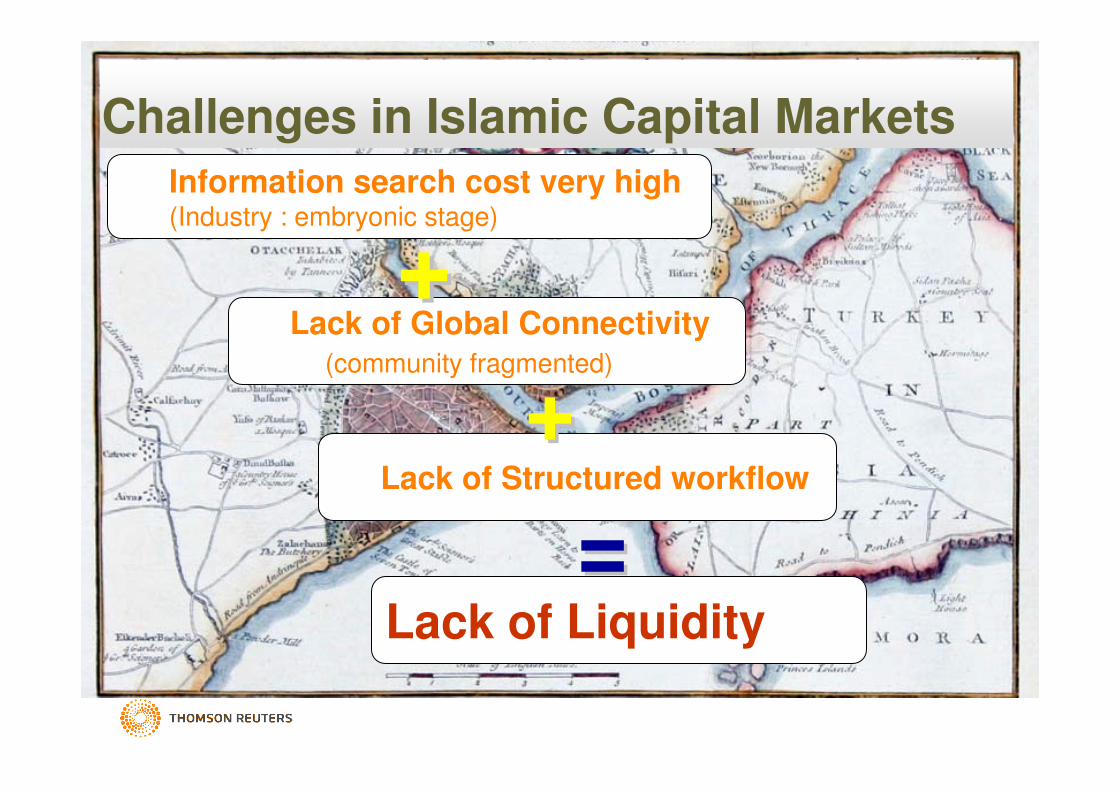

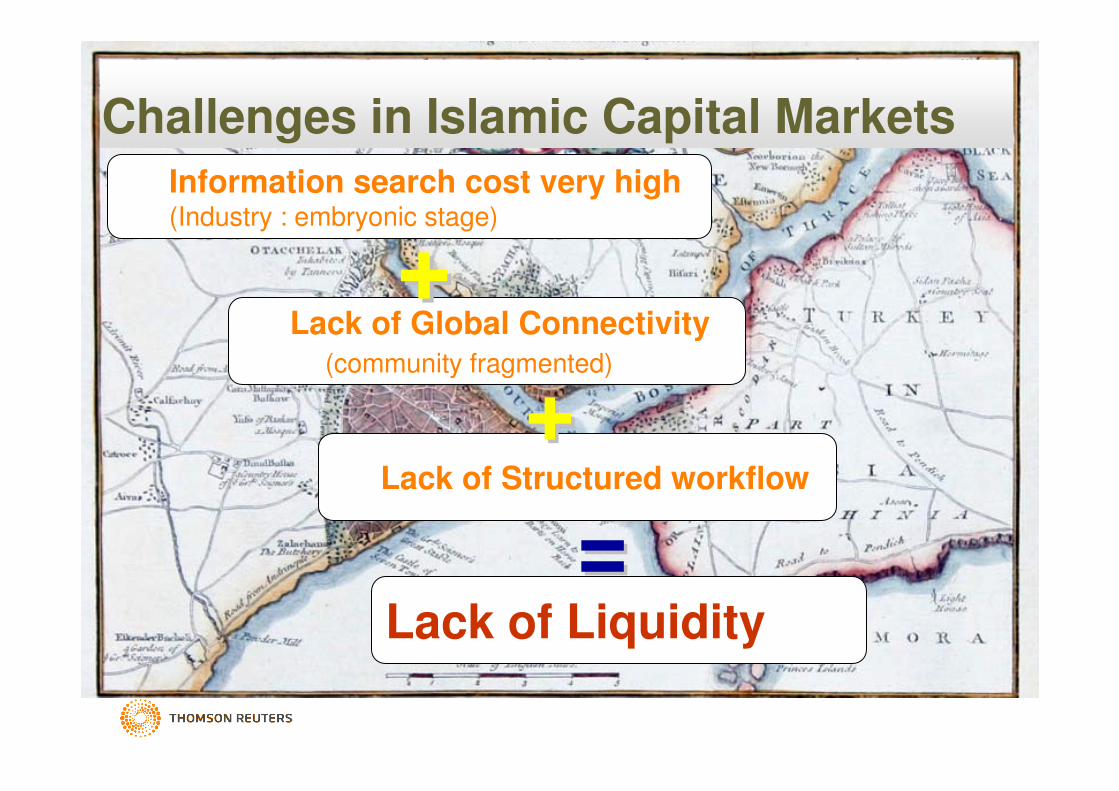

Challenges in Islamic Capital Markets

Information search cost very high(Industry : embryonic stage)

Lack of Global Connectivity(community fragmented)

Lack of Liquidity

++

==Lack of Structured workflow

++

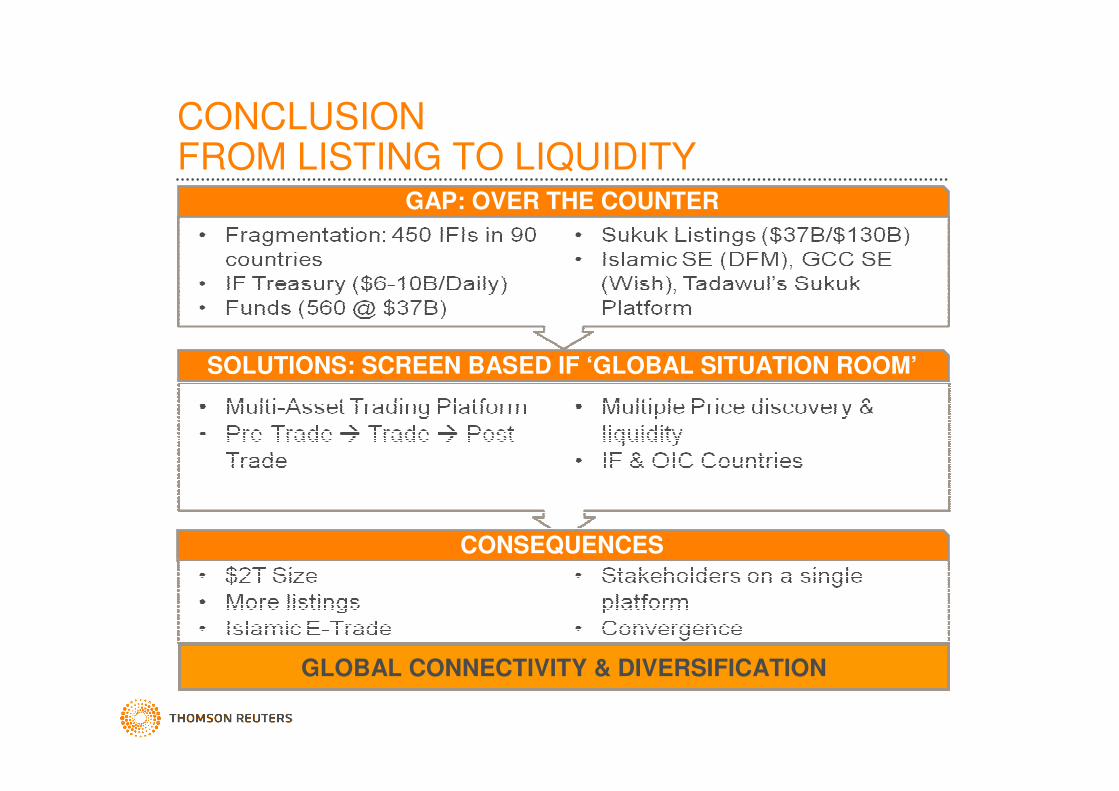

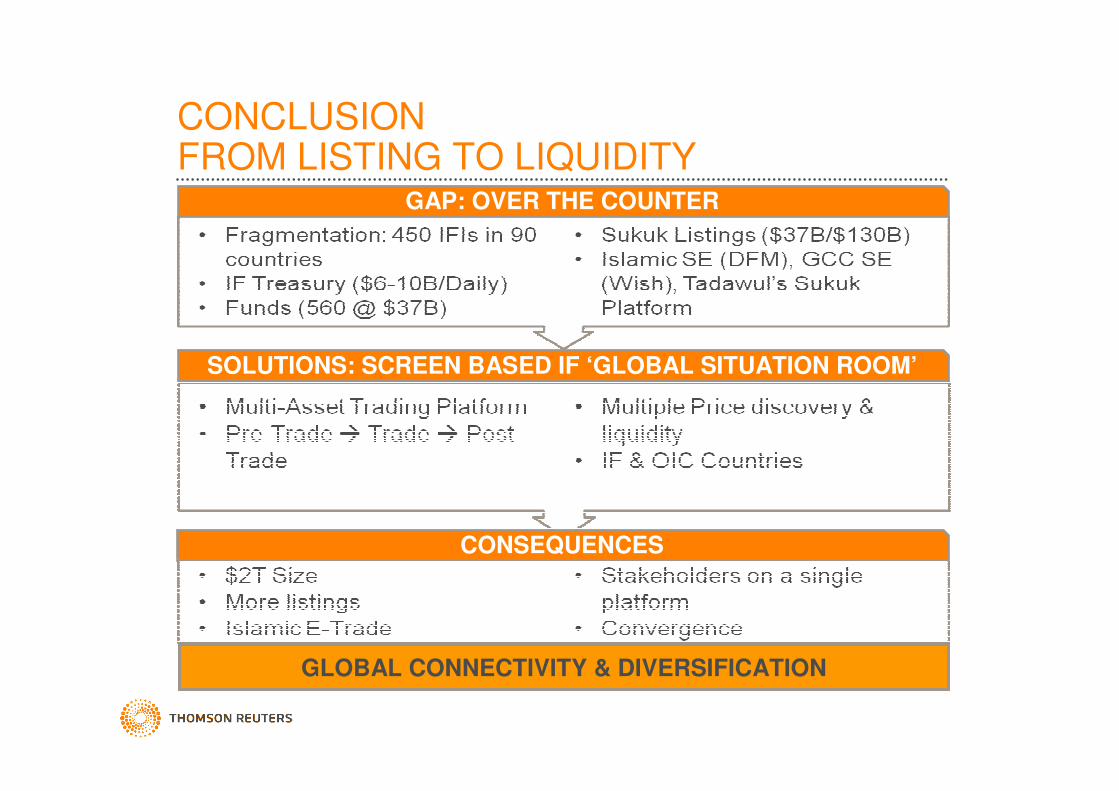

CONCLUSIONFROM LISTING TO LIQUIDITY

GAP: OVER THE COUNTER

SOLUTIONS: SCREEN BASED IF ‘GLOBAL SITUATION ROOM’

CONSEQUENCES

GLOBAL CONNECTIVITY & DIVERSIFICATION

AGENDA

• Islamic Treasury & Interbank Markets Focus

• Liquidity Status

• Unique Characteristics of Islamic Capital Markets

• Spurring Liquidity: Key factors and impediments

ISLAMIC TREASURY & INTERBANK MARKETS FOCUS

WHY TREASURY SHOULD BE THE FOCUS OF ISLAMIC CAPITAL MARKETS

DEVELOPMENT

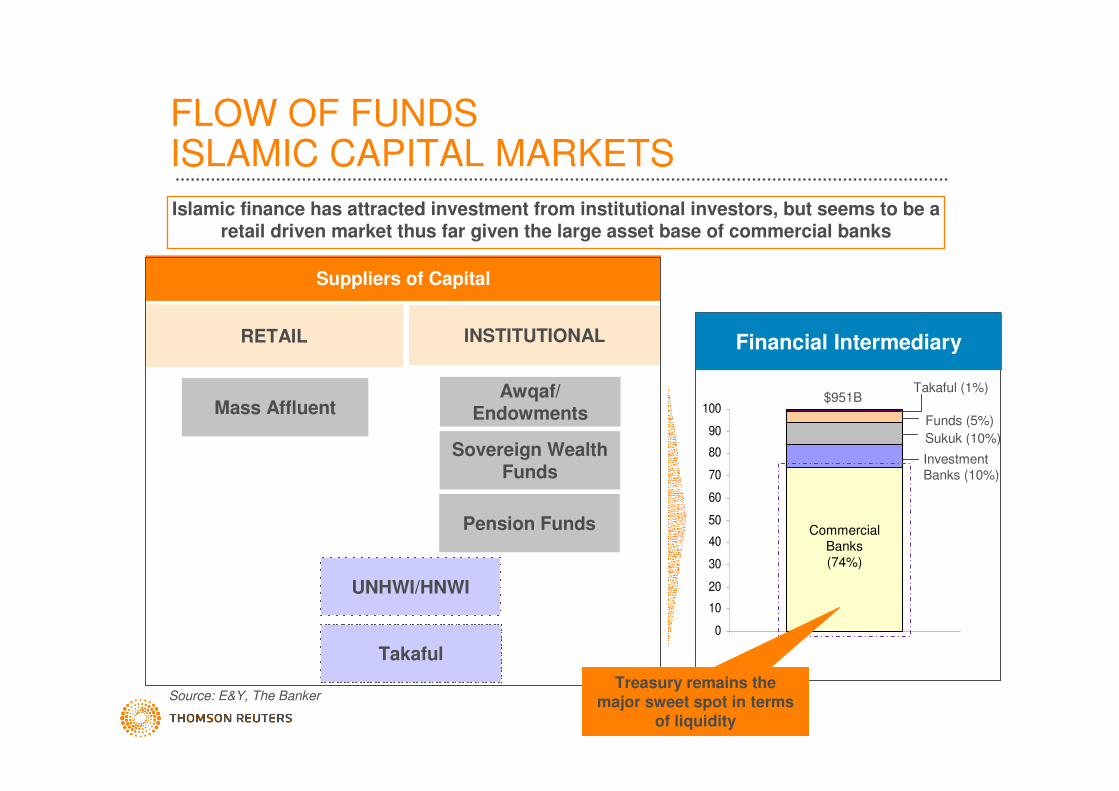

Source: E&Y, The Banker

Suppliers of Capital

RETAIL INSTITUTIONAL Financial Intermediary

Awqaf/Endowments

Pension Funds

Sovereign Wealth Funds

UNHWI/HNWI

Takaful

Mass Affluent

0

10

20

30

40

50

60

70

80

90

100

Sukuk (10%)

Funds (5%)

Takaful (1%)$951B

CommercialBanks (74%)

Investment Banks (10%)

FLOW OF FUNDSISLAMIC CAPITAL MARKETS

Islamic finance has attracted investment from institutional investors, but seems to be a retail driven market thus far given the large asset base of commercial banks

Treasury remains the major sweet spot in terms

of liquidity

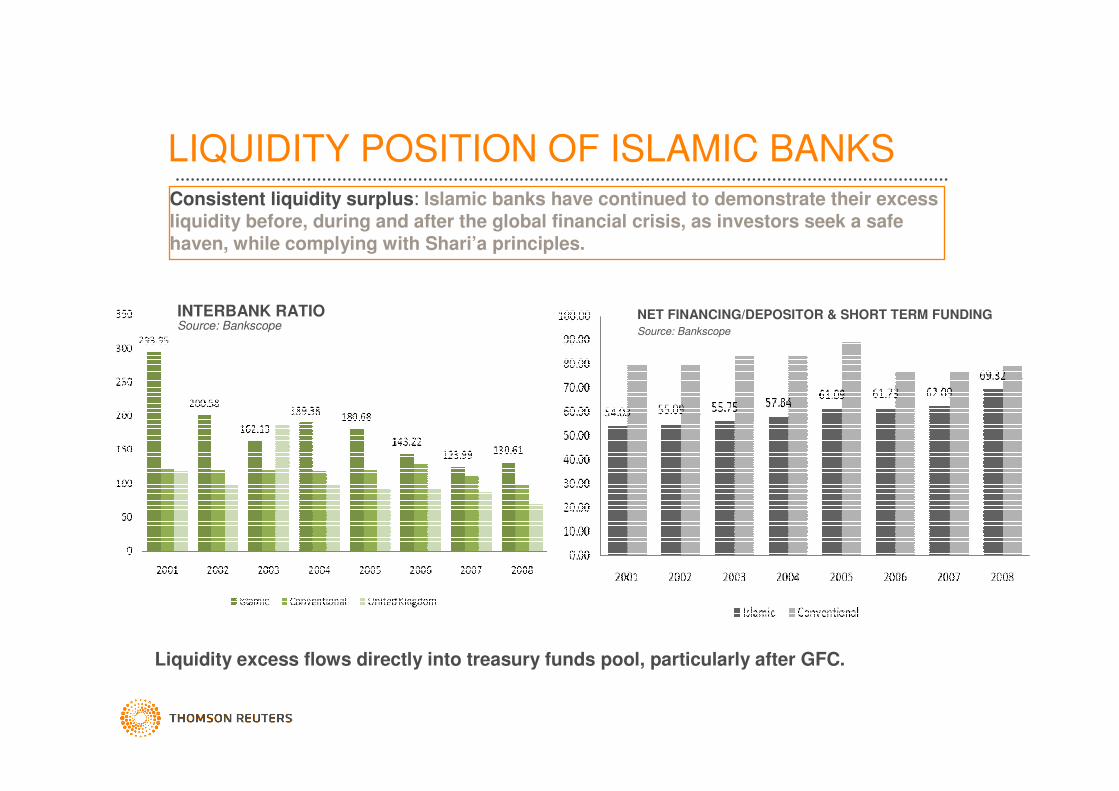

LIQUIDITY POSITION OF ISLAMIC BANKS

NET FINANCING/DEPOSITOR & SHORT TERM FUNDING Source: Bankscope

INTERBANK RATIOSource: Bankscope

Consistent liquidity surplus: Islamic banks have continued to demonstrate their excess liquidity before, during and after the global financial crisis, as investors seek a safe haven, while complying with Shari’a principles.

Liquidity excess flows directly into treasury funds pool, particularly after GFC.

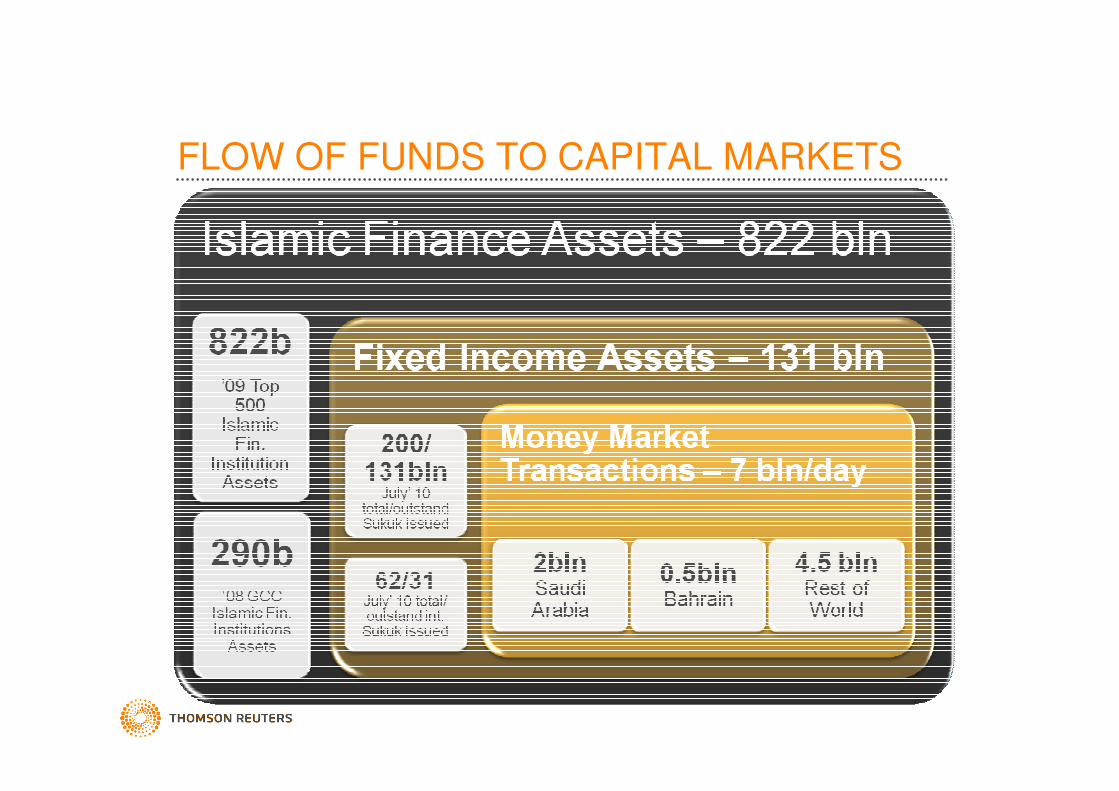

FLOW OF FUNDS TO CAPITAL MARKETS

LIQUIDITY STATUS

WHERE ARE WE RELATIVE TO WHERE WE SHOULD BE?

WHY IS LIQUIDITY DESIRABLE?

WITHOUT LIQUIDITY:

• Costs are higher

– Issuance & coupons – Higher costs for issuers

– Trading – Higher Brokerage Premiums & Wide Pricing

• Risks are higher

– Perceived Risk of holding instruments

– Mark to Market Calculations & VAR more accurate

• Market inefficient (even with solid primary markets)

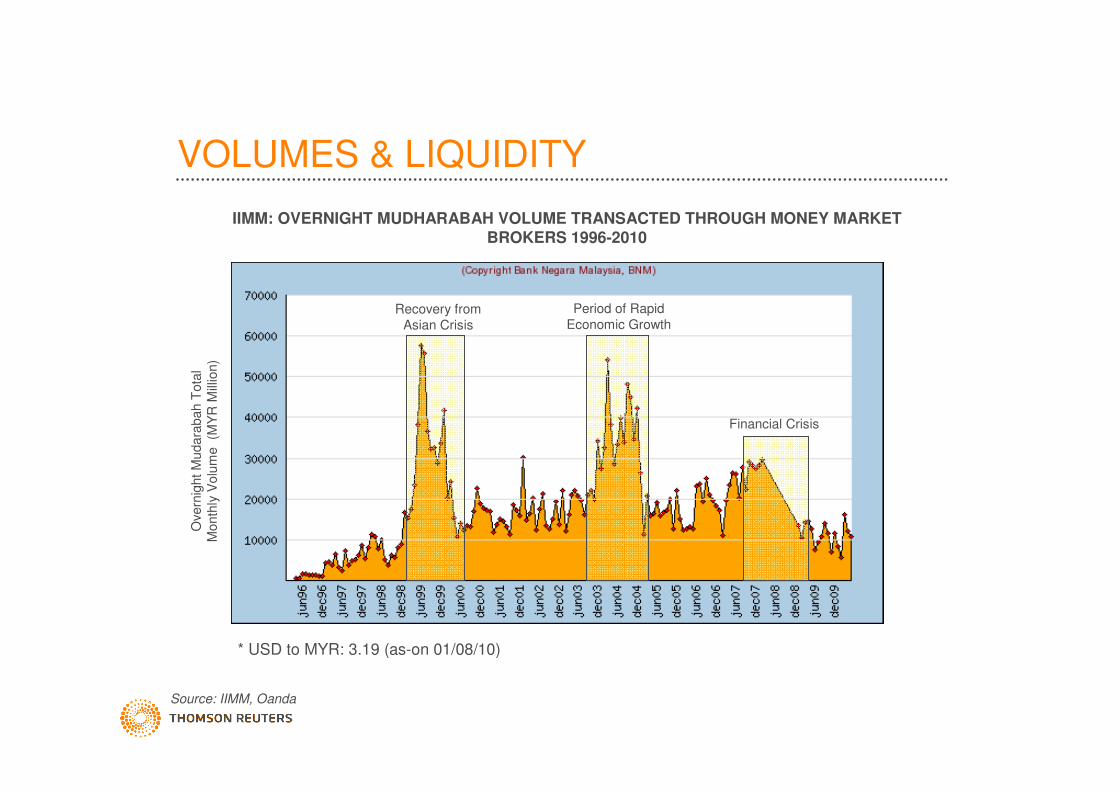

VOLUMES & LIQUIDITY

IIMM: OVERNIGHT MUDHARABAH VOLUME TRANSACTED THROUGH MONEY MARKET BROKERS 1996-2010

Source: IIMM, Oanda

Ove

rnig

ht M

udara

bah

Tota

l M

onth

ly V

olu

me (M

YR

Mill

ion)

Period of Rapid Economic Growth

Recovery from Asian Crisis

Financial Crisis

* USD to MYR: 3.19 (as-on 01/08/10)

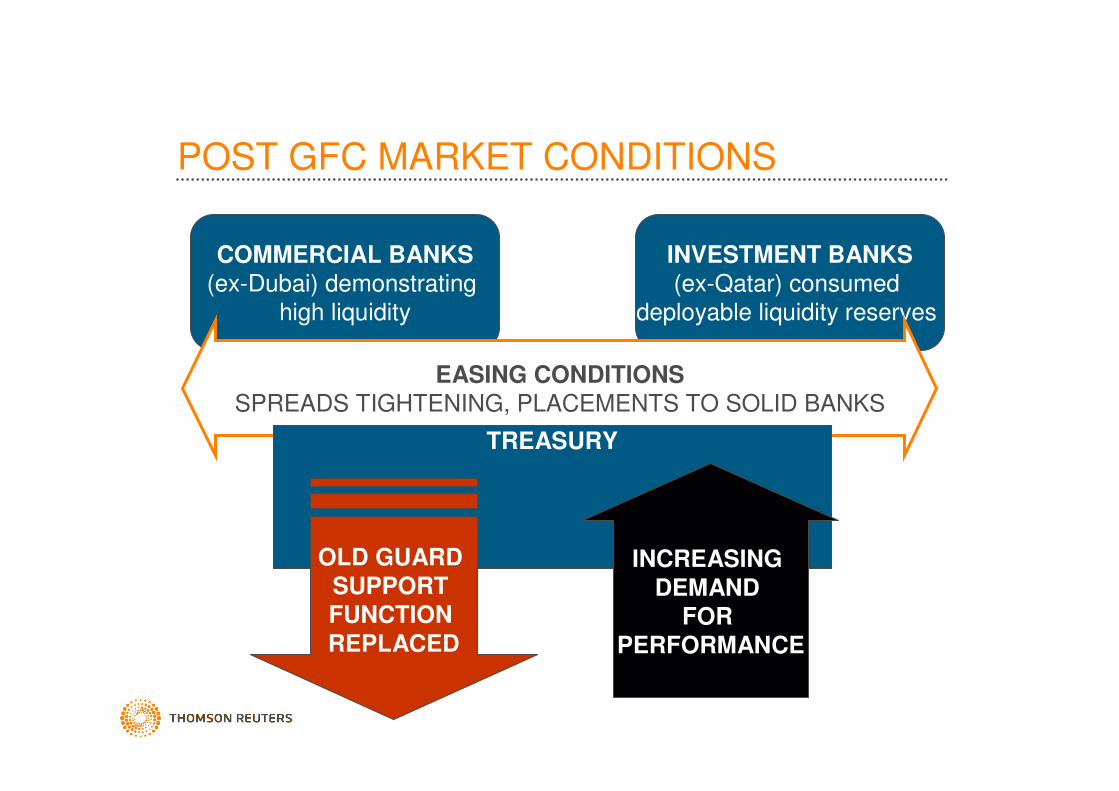

POST GFC MARKET CONDITIONS

COMMERCIAL BANKS(ex-Dubai) demonstrating

high liquidity

INVESTMENT BANKS(ex-Qatar) consumed

deployable liquidity reserves

EASING CONDITIONSSPREADS TIGHTENING, PLACEMENTS TO SOLID BANKS

TREASURY

OLD GUARD SUPPORT FUNCTION

REPLACED

INCREASING

DEMAND FOR

PERFORMANCE

0

10

20

30

40

50

60

70

80

2005 2006 2007 2008 2009

US

D B

lns

0

50

100

150

200

250

300

350

Total Issued Corporate

Quasi-Sovereign Change in Total Assets (Top 75 Islamic Banks)

Assets Top 75 Islamic Banks

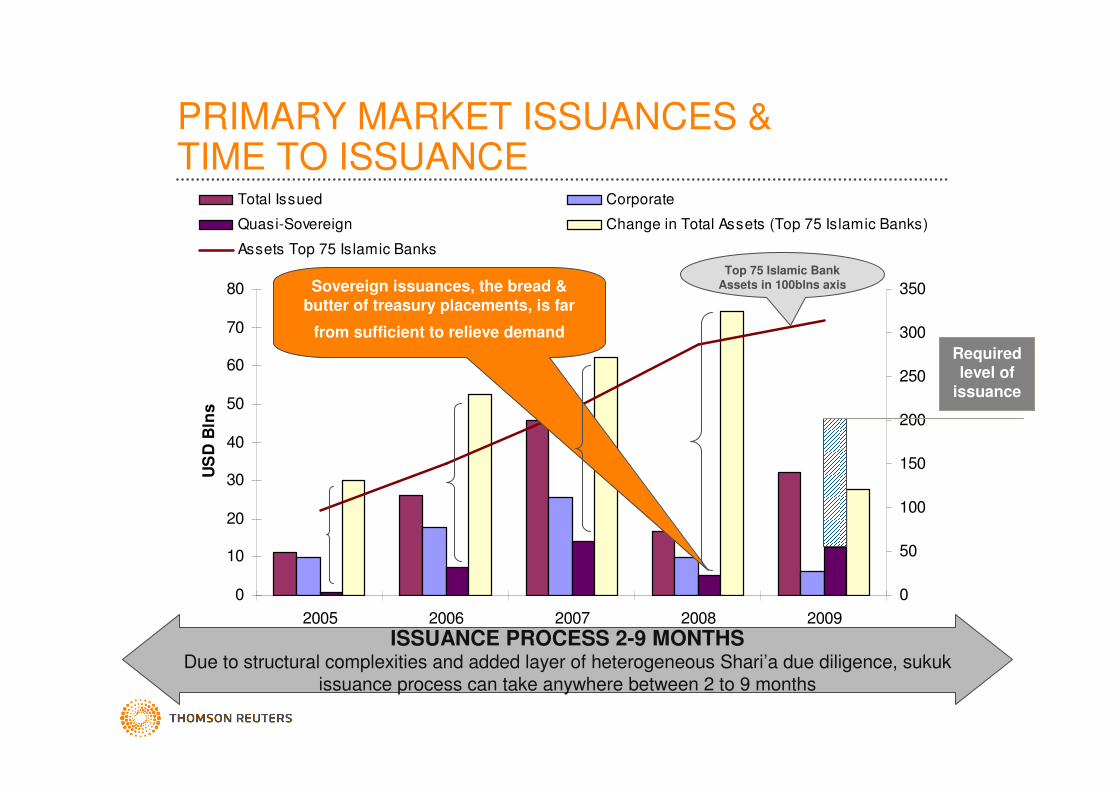

PRIMARY MARKET ISSUANCES & TIME TO ISSUANCE

ISSUANCE PROCESS 2-9 MONTHSDue to structural complexities and added layer of heterogeneous Shari’a due diligence, sukuk

issuance process can take anywhere between 2 to 9 months

Sovereign issuances, the bread & butter of treasury placements, is far

from sufficient to relieve demand

Top 75 Islamic Bank Assets in 100blns axis

Required level of

issuance

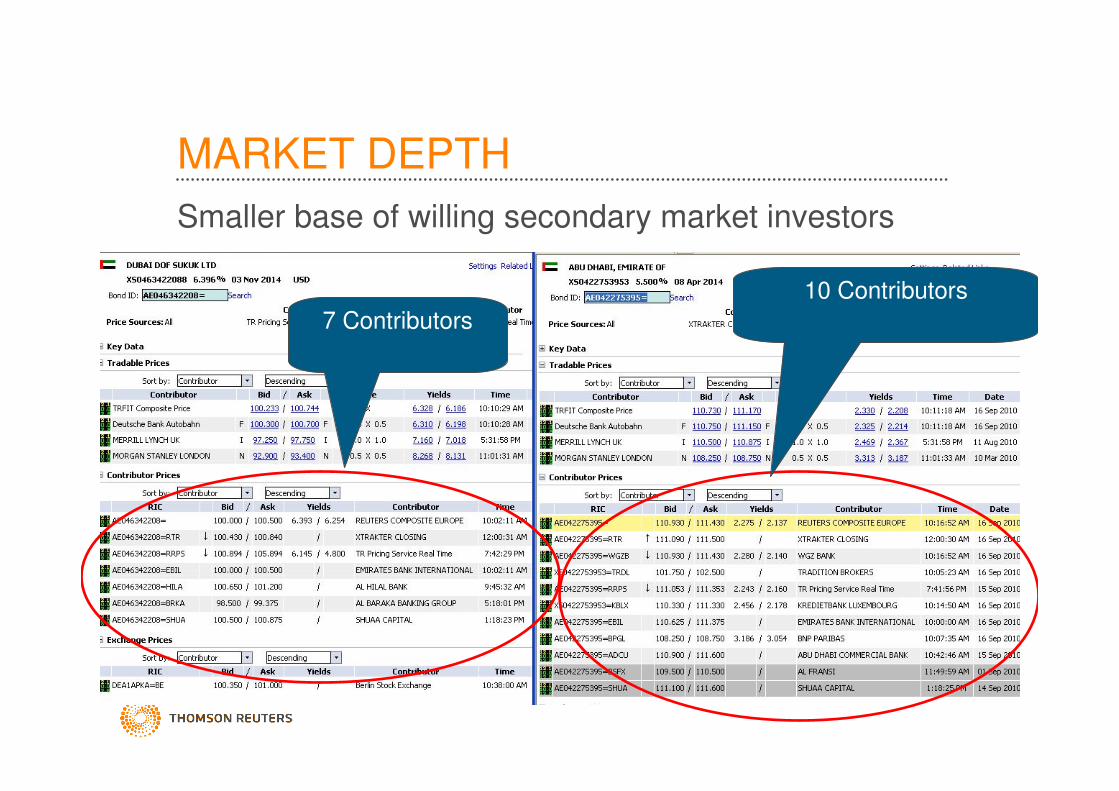

MARKET DEPTH

Smaller base of willing secondary market investors

7 Contributors

10 Contributors

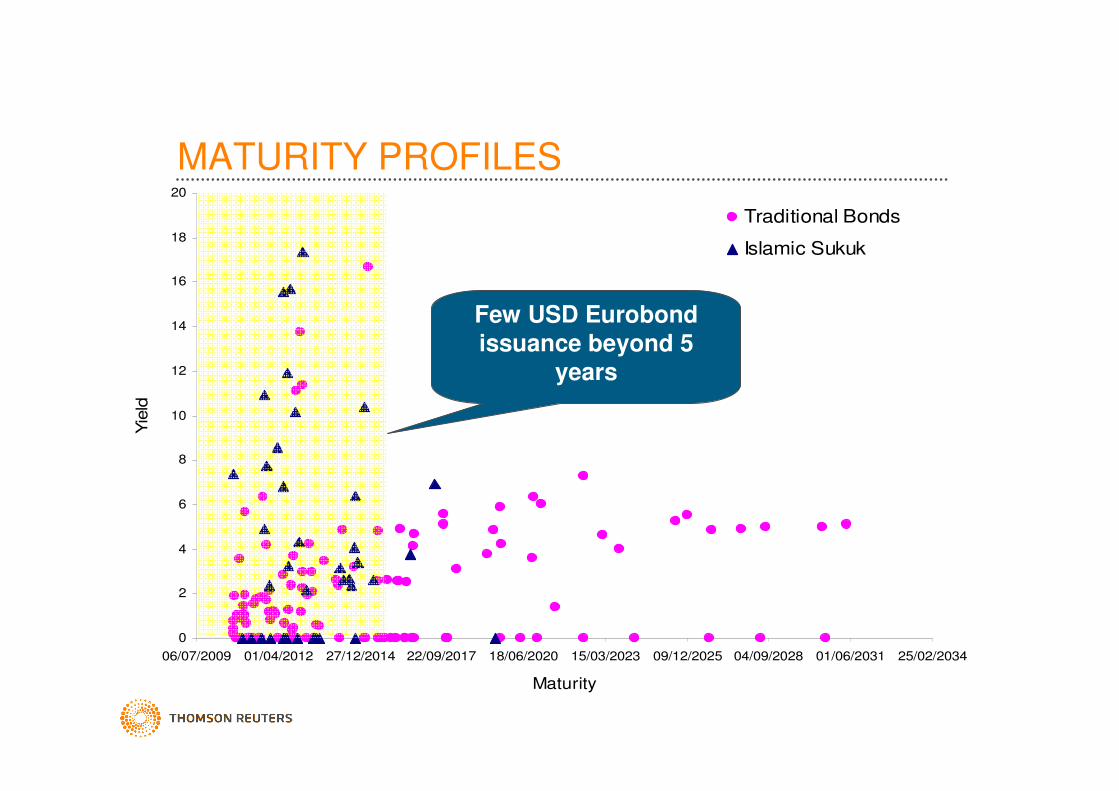

MATURITY PROFILES

0

2

4

6

8

10

12

14

16

18

20

06/07/2009 01/04/2012 27/12/2014 22/09/2017 18/06/2020 15/03/2023 09/12/2025 04/09/2028 01/06/2031 25/02/2034

Maturity

Yie

ld

Traditional Bonds

Islamic Sukuk

Few USD Eurobond issuance beyond 5

years

UNIQUE CHARACTERISTICS OF

ISLAMIC TREASURY & INTERBANK MARKETS

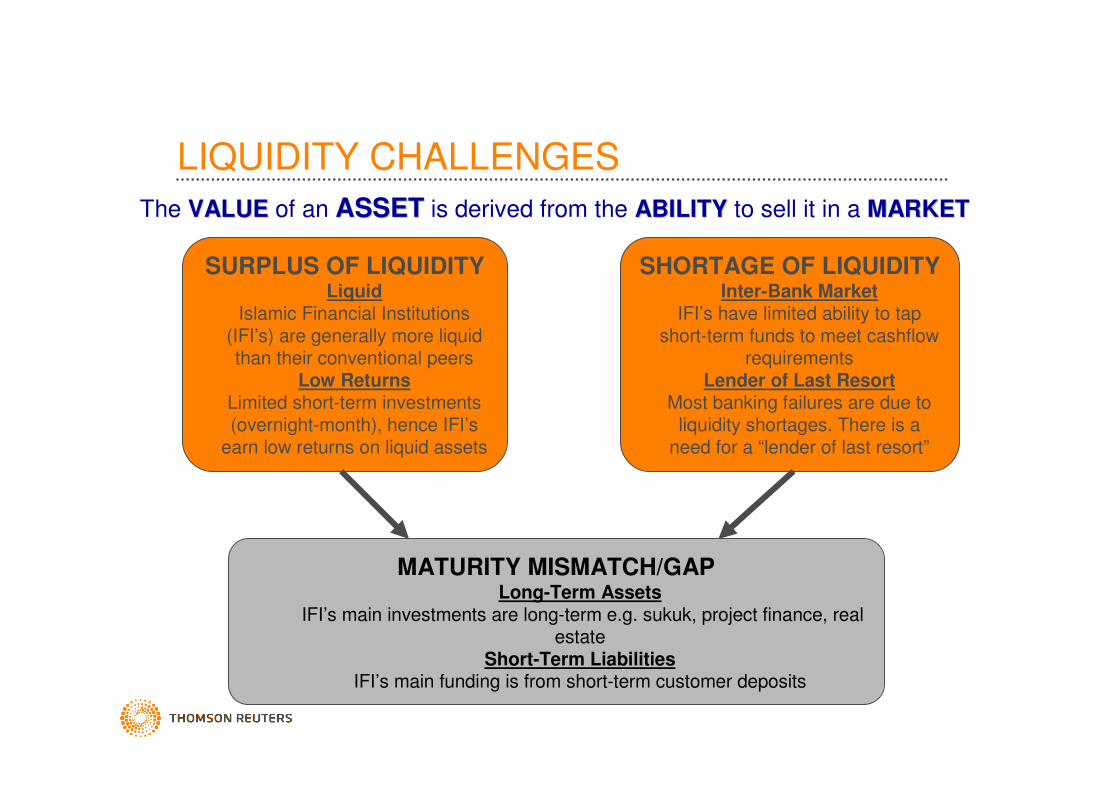

LIQUIDITY CHALLENGES

The VALUEVALUE of an ASSETASSET is derived from the ABILITYABILITY to sell it in a MARKETMARKET

SURPLUS OF LIQUIDITYLiquid

Islamic Financial Institutions (IFI’s) are generally more liquid than their conventional peers

Low ReturnsLimited short-term investments (overnight-month), hence IFI’s

earn low returns on liquid assets

SHORTAGE OF LIQUIDITYInter-Bank Market

IFI’s have limited ability to tap short-term funds to meet cashflow

requirements Lender of Last Resort

Most banking failures are due to liquidity shortages. There is a

need for a “lender of last resort”

MATURITY MISMATCH/GAPLong-Term Assets

IFI’s main investments are long-term e.g. sukuk, project finance, real estate

Short-Term LiabilitiesIFI’s main funding is from short-term customer deposits

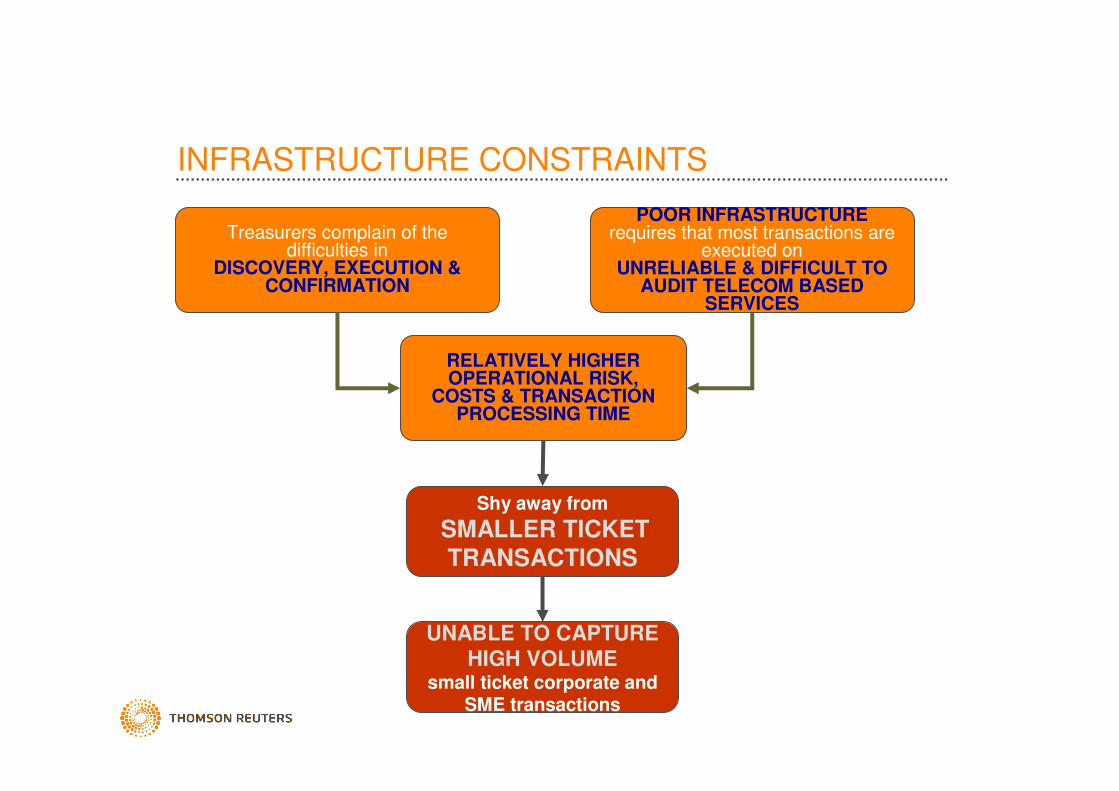

INFRASTRUCTURE CONSTRAINTS

Treasurers complain of the difficulties in

DISCOVERY, EXECUTION & CONFIRMATION

POOR INFRASTRUCTURE requires that most transactions are

executed on UNRELIABLE & DIFFICULT TO

AUDIT TELECOM BASED SERVICES

RELATIVELY HIGHER OPERATIONAL RISK,

COSTS & TRANSACTION PROCESSING TIME

Shy away from

SMALLER TICKET TRANSACTIONS

UNABLE TO CAPTURE HIGH VOLUME

small ticket corporate and SME transactions

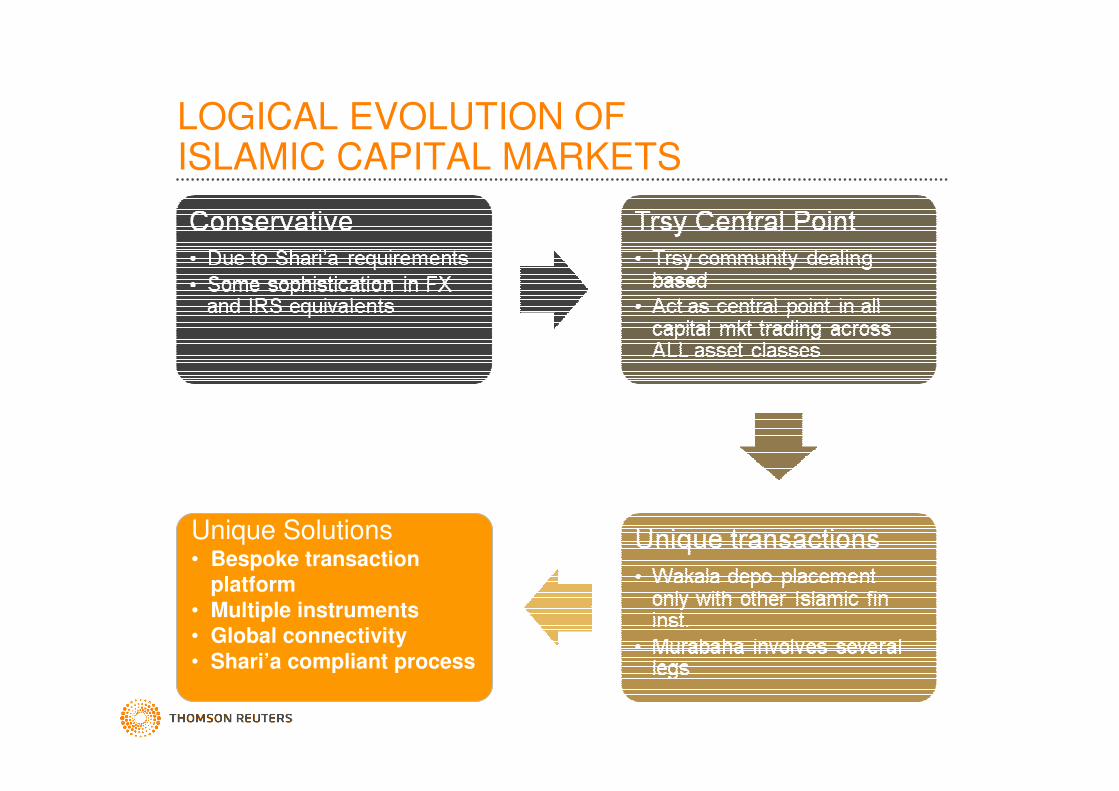

LOGICAL EVOLUTION OF ISLAMIC CAPITAL MARKETS

Unique Solutions• Bespoke transaction

platform

• Multiple instruments• Global connectivity

• Shari’a compliant process

SPURRING LIQUIDITYKEY FACTORS AND IMPEDIMENTS

PR

IVA

TE

SE

CT

OR

IN

ITIA

TIV

E

PU

BL

IC S

EC

TO

R

INIT

IAT

IVE

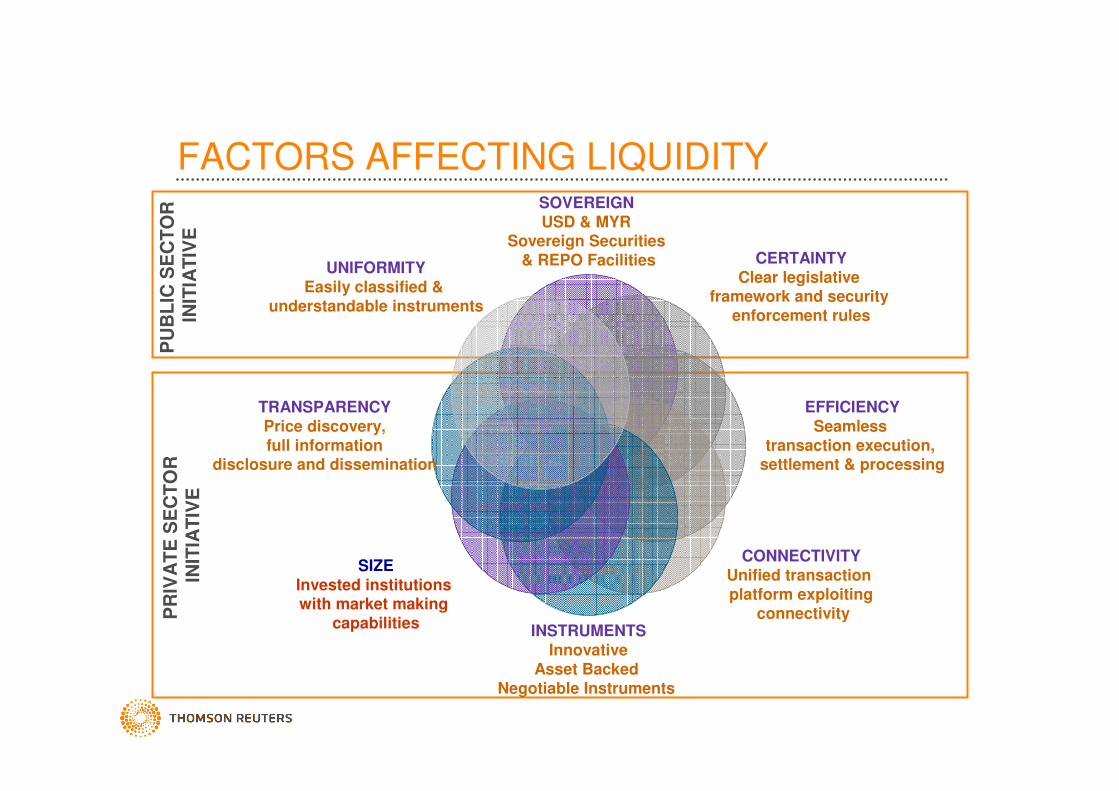

FACTORS AFFECTING LIQUIDITYSOVEREIGN USD & MYR

Sovereign Securities & REPO Facilities CERTAINTY

Clear legislative framework and security

enforcement rules

EFFICIENCYSeamless

transaction execution, settlement & processing

CONNECTIVITYUnified transaction platform exploiting

connectivityINSTRUMENTS

InnovativeAsset Backed

Negotiable Instruments

SIZEInvested institutions with market making

capabilities

TRANSPARENCYPrice discovery,full information

disclosure and dissemination

UNIFORMITYEasily classified &

understandable instruments

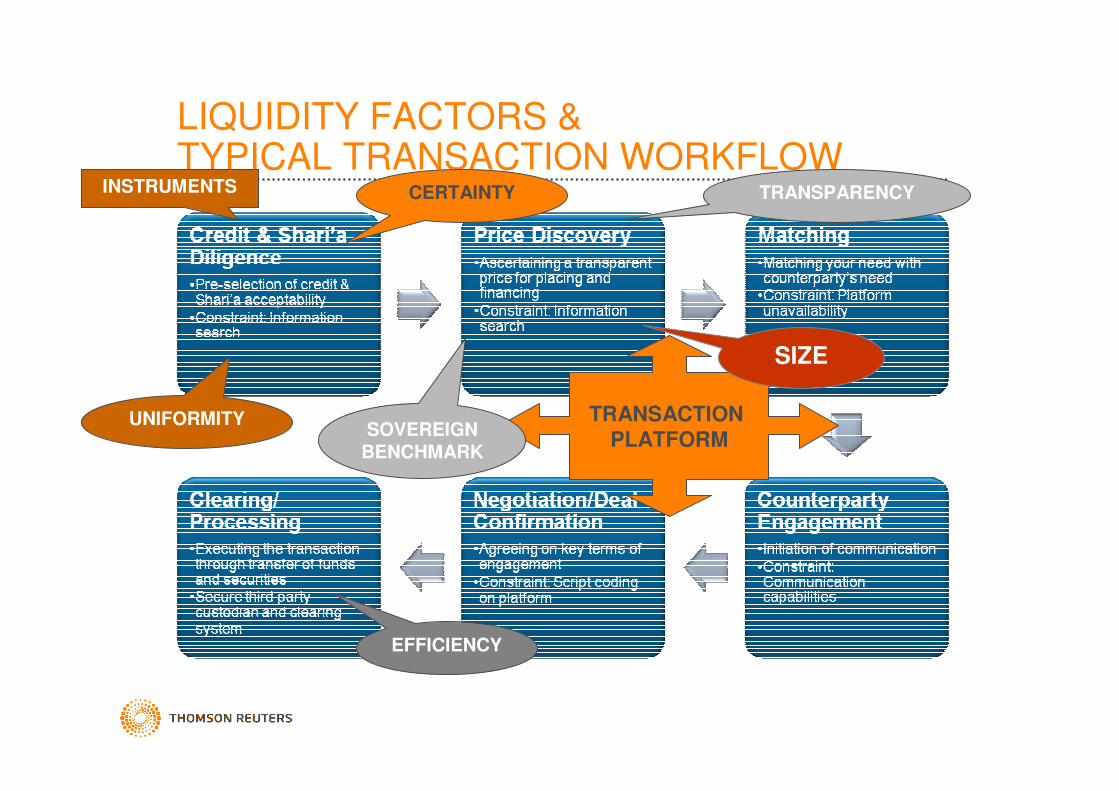

LIQUIDITY FACTORS &TYPICAL TRANSACTION WORKFLOW

EFFICIENCY

UNIFORMITY

CERTAINTY TRANSPARENCY

TRANSACTION PLATFORM

INSTRUMENTS

SOVEREIGN BENCHMARK

SIZE

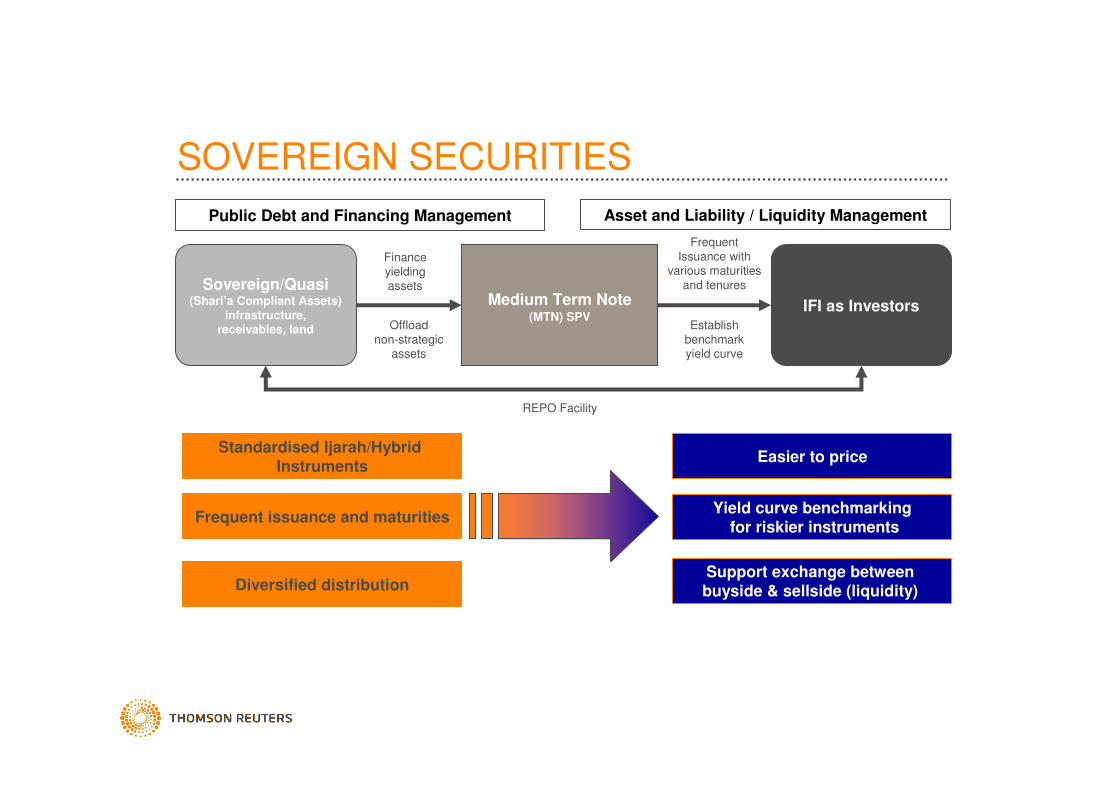

SOVEREIGN SECURITIES

Sovereign/Quasi (Shari’a Compliant Assets)

infrastructure, receivables, land

Medium Term Note(MTN) SPV

IFI as Investors

Public Debt and Financing Management

Establish benchmark yield curve

Frequent Issuance with

various maturities and tenures

Asset and Liability / Liquidity Management

REPO Facility

Finance yielding assets

Offload non-strategic

assets

Standardised Ijarah/Hybrid Instruments

Frequent issuance and maturities

Diversified distribution

Easier to price

Yield curve benchmarkingfor riskier instruments

Support exchange between buyside & sellside (liquidity)

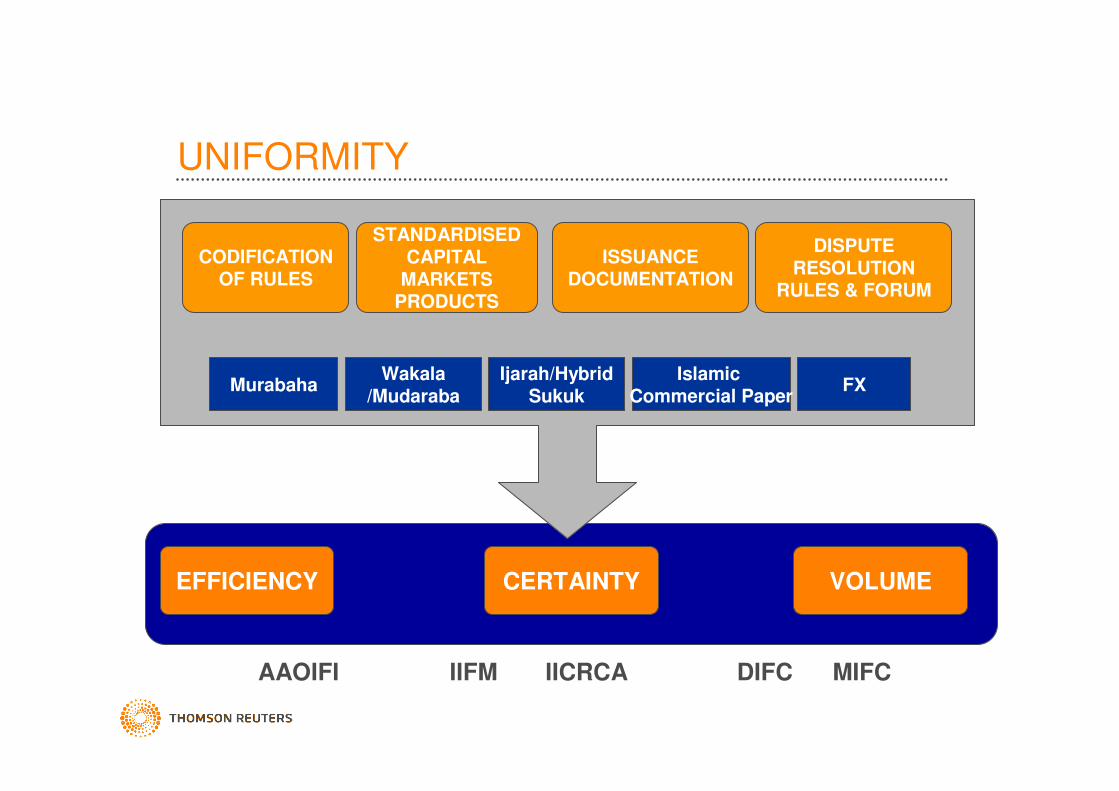

UNIFORMITY

CODIFICATION OF RULES

STANDARDISED CAPITAL

MARKETS PRODUCTS

ISSUANCE DOCUMENTATION

MurabahaWakala

/MudarabaIjarah/Hybrid

SukukIslamic

Commercial Paper

DISPUTE RESOLUTION

RULES & FORUM

FX

EFFICIENCY VOLUMECERTAINTY

AAOIFI IIFM IICRCA DIFC MIFC

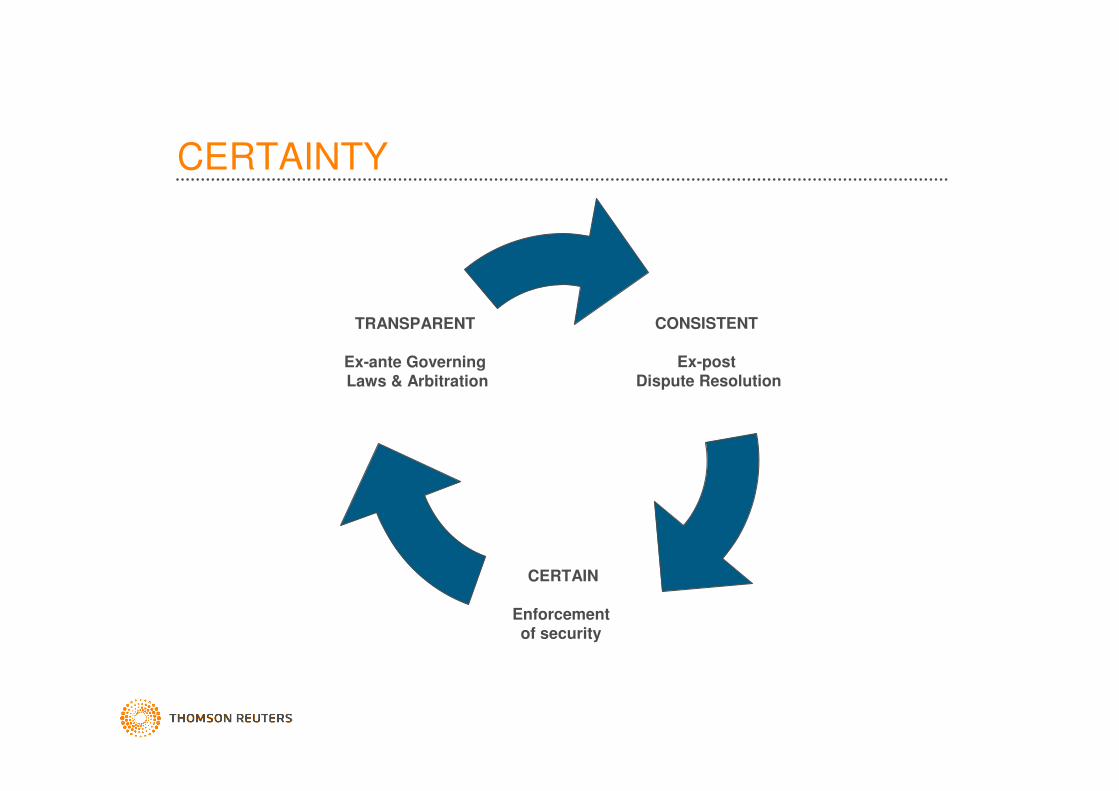

CERTAINTY

CONSISTENT

Ex-post Dispute Resolution

CERTAIN

Enforcement of security

TRANSPARENT

Ex-ante Governing Laws & Arbitration

FEATURES OF AN IDEAL ISLAMIC LIQUIDITY MANAGEMENT INSTRUMENT

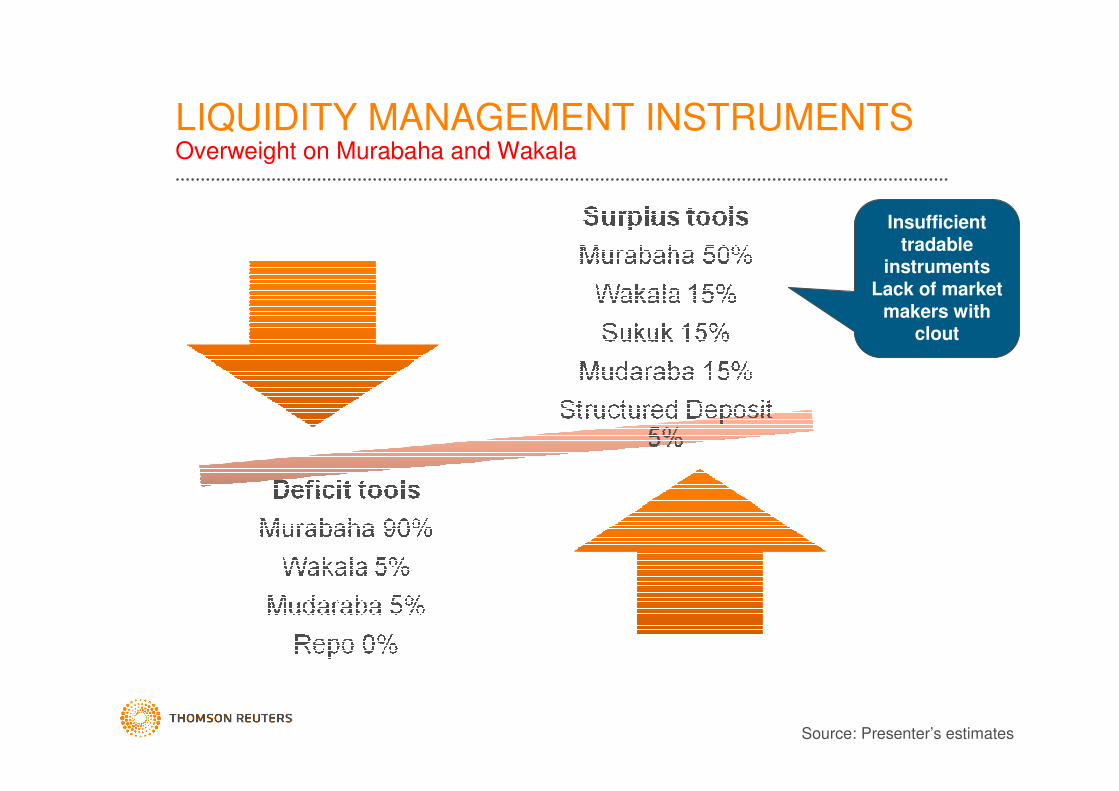

LIQUIDITY MANAGEMENT INSTRUMENTSOverweight on Murabaha and Wakala

Source: Presenter’s estimates

Insufficient tradable

instrumentsLack of market

makers with clout

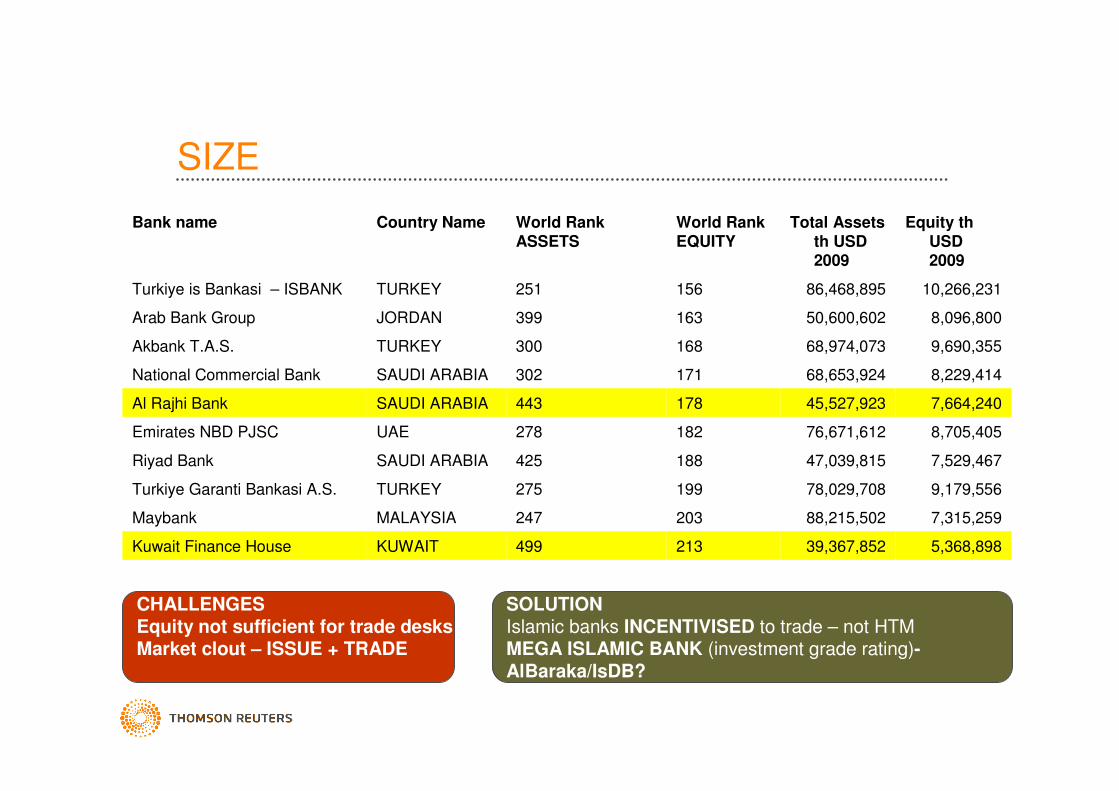

SIZE

5,368,89839,367,852213499KUWAITKuwait Finance House

7,315,25988,215,502203247MALAYSIAMaybank

9,179,55678,029,708199275TURKEYTurkiye Garanti Bankasi A.S.

7,529,46747,039,815188425SAUDI ARABIARiyad Bank

8,705,40576,671,612182278UAEEmirates NBD PJSC

7,664,24045,527,923178443SAUDI ARABIAAl Rajhi Bank

8,229,41468,653,924171302SAUDI ARABIANational Commercial Bank

9,690,35568,974,073168300TURKEYAkbank T.A.S.

8,096,80050,600,602163399JORDANArab Bank Group

10,266,23186,468,895156251TURKEYTurkiye is Bankasi – ISBANK

Equity thUSD 2009

Total Assets th USD 2009

World Rank EQUITY

World Rank ASSETS

Country NameBank name

CHALLENGESEquity not sufficient for trade desksMarket clout – ISSUE + TRADE

SOLUTIONIslamic banks INCENTIVISED to trade – not HTMMEGA ISLAMIC BANK (investment grade rating)-AlBaraka/IsDB?

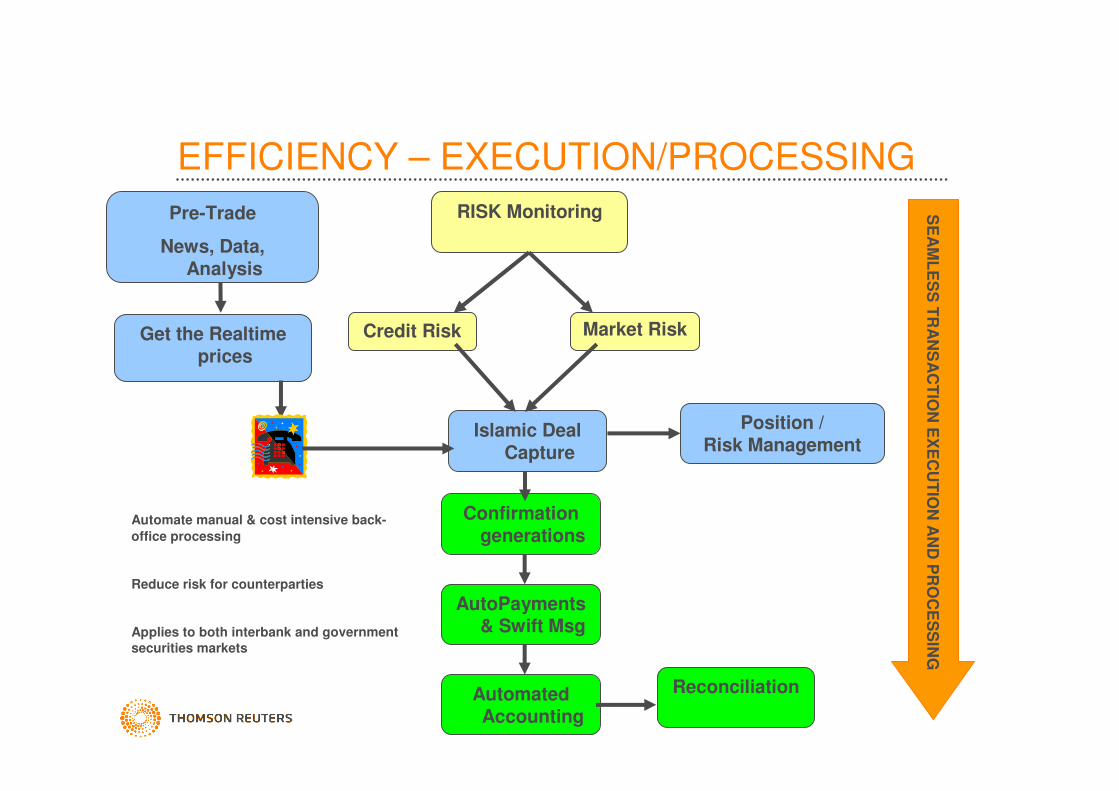

EFFICIENCY – EXECUTION/PROCESSING

Automate manual & cost intensive back-

office processing

Reduce risk for counterparties

Applies to both interbank and government

securities markets

Market RiskGet the Realtimeprices

Credit Risk

Islamic Deal Capture

Pre-Trade

News, Data, Analysis

RISK Monitoring

Position / Risk Management

Confirmation generations

AutoPayments& Swift Msg

Automated Accounting

Reconciliation

SE

AM

LE

SS

TR

AN

SA

CT

ION

EX

EC

UT

ION

AN

D P

RO

CE

SS

ING

CONNECTIVITY

Challenges in Islamic Capital Markets

Information search cost very high(Industry : embryonic stage)

Lack of Global Connectivity(community fragmented)

Lack of Liquidity

++

==Lack of Structured workflow

++

CONCLUSIONFROM LISTING TO LIQUIDITY

GAP: OVER THE COUNTER

SOLUTIONS: SCREEN BASED IF ‘GLOBAL SITUATION ROOM’

CONSEQUENCES

GLOBAL CONNECTIVITY & DIVERSIFICATION