Embed Size (px)

DESCRIPTION

Container shipping markets in 2014.Presented at the TOC Asia conference8 April 2014

Citation preview

Web: www.alphaliner.com E-mail: [email protected]

Liner Research Services

TOC Container Supply Chain : Asia 8 April 2014

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

EPISODE I – THE LINER WARS (2009-10)

EPISODE II – THE MAERSK EMPIRE STRIKES BACK (2011-13)

EPISODE III – RETURN OF THE LINER ALLIANCES (2014-16)

Page 1

Not too long ago, in a galaxy far, far away…

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

EPISODE I – THE LINER WARS (2009-10)

EPISODE II – THE MAERSK EMPIRE STRIKES BACK (2011-13)

EPISODE III – RETURN OF THE LINER ALLIANCES (2014-16)

Page 2

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

EPISODE I – THE LINER WARS (2009-10)

EPISODE II – THE MAERSK EMPIRE STRIKES BACK (2011-13)

EPISODE III – RETURN OF THE LINER ALLIANCES (2014-16)

Page 3

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services Page 4

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

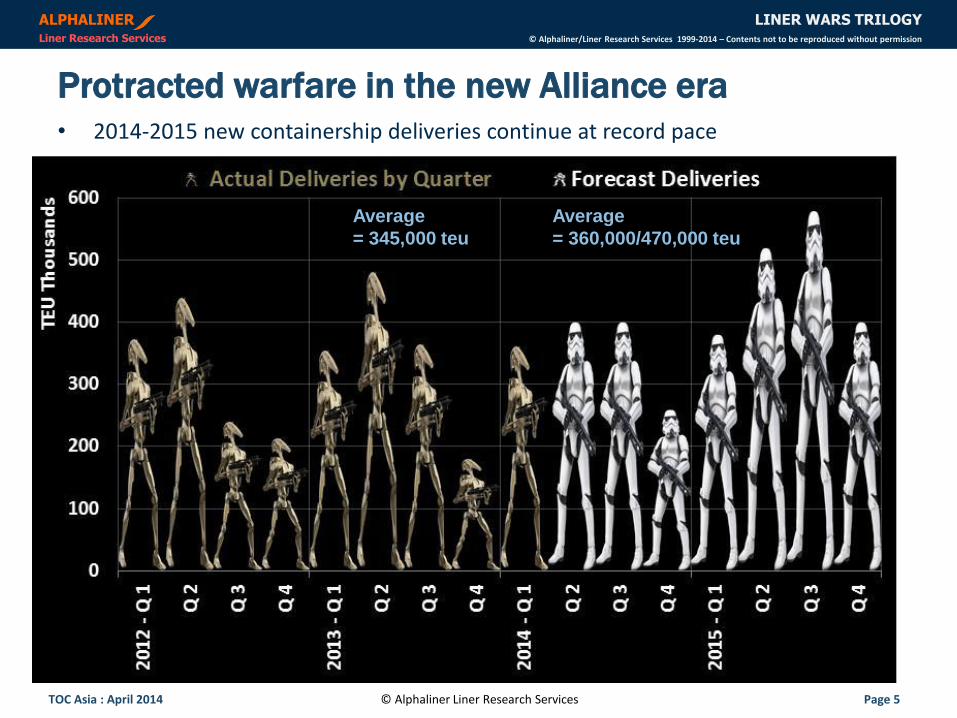

Protracted warfare in the new Alliance era

Page 5

• 2014-2015 new containership deliveries continue at record pace

Average

= 315,000 teu

Average

= 345,000 teu

Average

= 360,000/470,000 teu

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

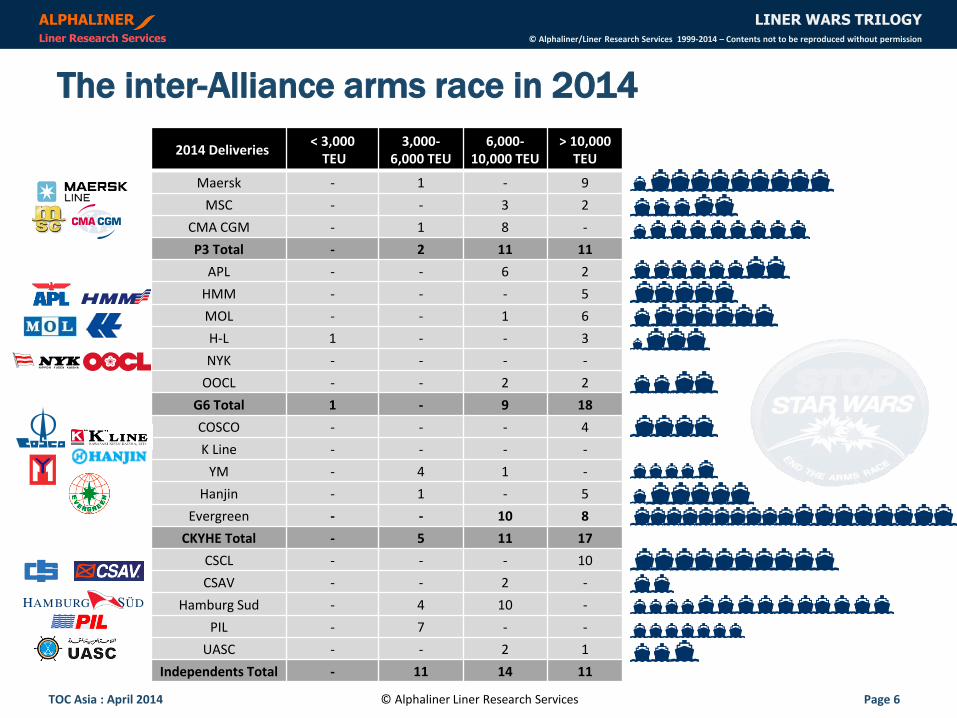

The inter-Alliance arms race in 2014

Page 6

2014 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk - 1 - 9

MSC - - 3 2

CMA CGM - 1 8 -

P3 Total - 2 11 11

APL - - 6 2

HMM - - - 5

MOL - - 1 6

H-L 1 - - 3

NYK - - - -

OOCL - - 2 2

G6 Total 1 - 9 18

COSCO - - - 4

K Line - - - -

YM - 4 1 -

Hanjin - 1 - 5

Evergreen - - 10 8

CKYHE Total - 5 11 17

CSCL - - - 10

CSAV - - 2 -

Hamburg Sud - 4 10 -

PIL - 7 - -

UASC - - 2 1

Independents Total - 11 14 11

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

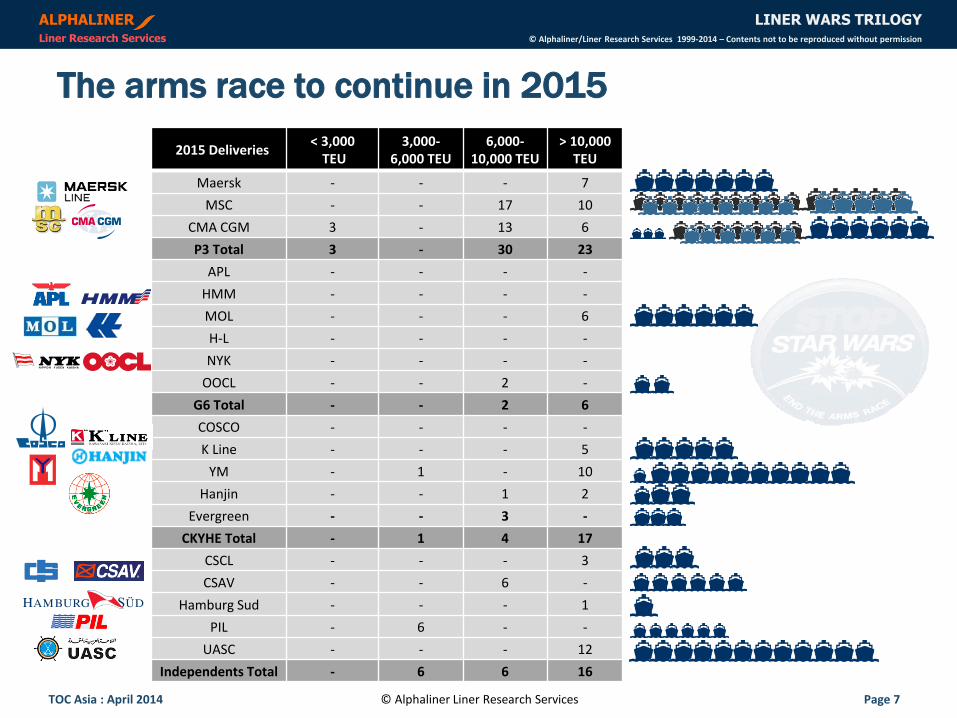

The arms race to continue in 2015

Page 7

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk - - - 7

MSC - - 17 10

CMA CGM 3 - 13 6

P3 Total 3 - 30 23

APL - - - -

HMM - - - -

MOL - - - 6

H-L - - - -

NYK - - - -

OOCL - - 2 -

G6 Total - - 2 6

COSCO - - - -

K Line - - - 5

YM - 1 - 10

Hanjin - - 1 2

Evergreen - - 3 -

CKYHE Total - 1 4 17

CSCL - - - 3

CSAV - - 6 -

Hamburg Sud - - - 1

PIL - 6 - -

UASC - - - 12

Independents Total - 6 6 16

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

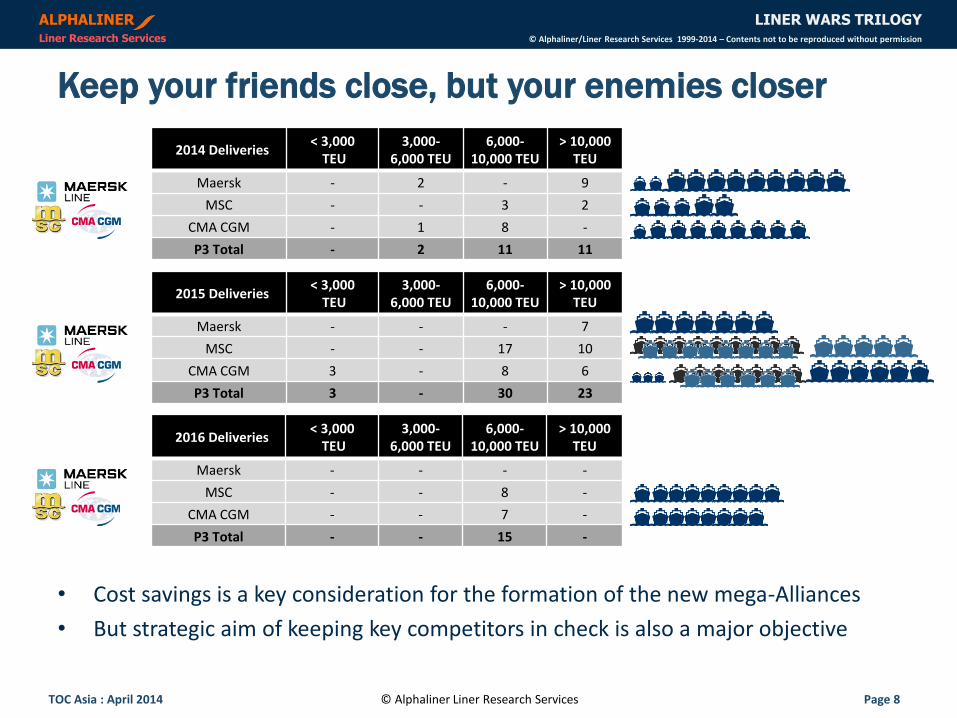

Keep your friends close, but your enemies closer

Page 8

• Cost savings is a key consideration for the formation of the new mega-Alliances

• But strategic aim of keeping key competitors in check is also a major objective

2014 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk - 2 - 9

MSC - - 3 2

CMA CGM - 1 8 -

P3 Total - 2 11 11

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk 0 0 0 7

MSC 0 0 17 10

CMA CGM 3 0 8 6

P3 Total 3 0 25 23

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk - - - 7

MSC - - 17 10

CMA CGM 3 - 8 6

P3 Total 3 - 30 23

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk 0 0 0 7

MSC 0 0 17 10

CMA CGM 3 0 8 6

P3 Total 3 0 25 23

2016 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk - - - -

MSC - - 8 -

CMA CGM - - 7 -

P3 Total - - 15 -

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

If you cant beat them, join them

Page 9

2014 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

COSCO - - - 4

K Line - - - -

YM - 4 1 -

Hanjin - 1 - 5

Evergreen - - 10 8

CKYHE Total - 5 11 17

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk 0 0 0 7

MSC 0 0 17 10

CMA CGM 3 0 8 6

P3 Total 3 0 25 23

APL 0 0 0 0

HMM 0 0 0 2

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

COSCO - - - -

K Line - - - 5

YM - 1 - 10

Hanjin - - 1 2

Evergreen - - 3 -

CKYHE Total - 1 4 17

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

Maersk 0 0 0 7

MSC 0 0 17 10

CMA CGM 3 0 8 6

P3 Total 3 0 25 23

APL 0 0 0 0

HMM 0 0 0 2

2016 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

COSCO - - 3 -

K Line - - - -

YM - - - 5

Hanjin - - 4 -

Evergreen - - - 10

CKYHE Total - 1 4 17

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

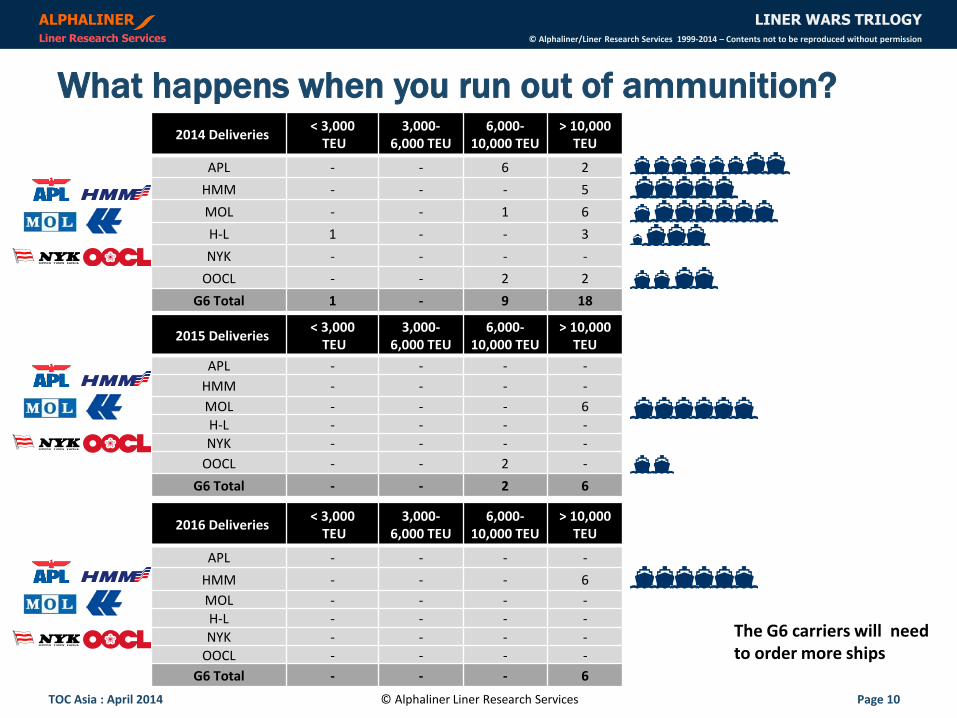

What happens when you run out of ammunition?

Page 10

2014 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

APL - - 6 2

HMM - - - 5

MOL - - 1 6

H-L 1 - - 3

NYK - - - -

OOCL - - 2 2

G6 Total 1 - 9 18

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

APL - - - -

HMM - - - -

MOL - - - 6

H-L - - - -

NYK - - - -

OOCL - - 2 -

G6 Total - - 2 6

2016 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

APL - - - -

HMM - - - 6

MOL - - - -

H-L - - - -

NYK - - - -

OOCL - - - -

G6 Total - - - 6

The G6 carriers will need to order more ships

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

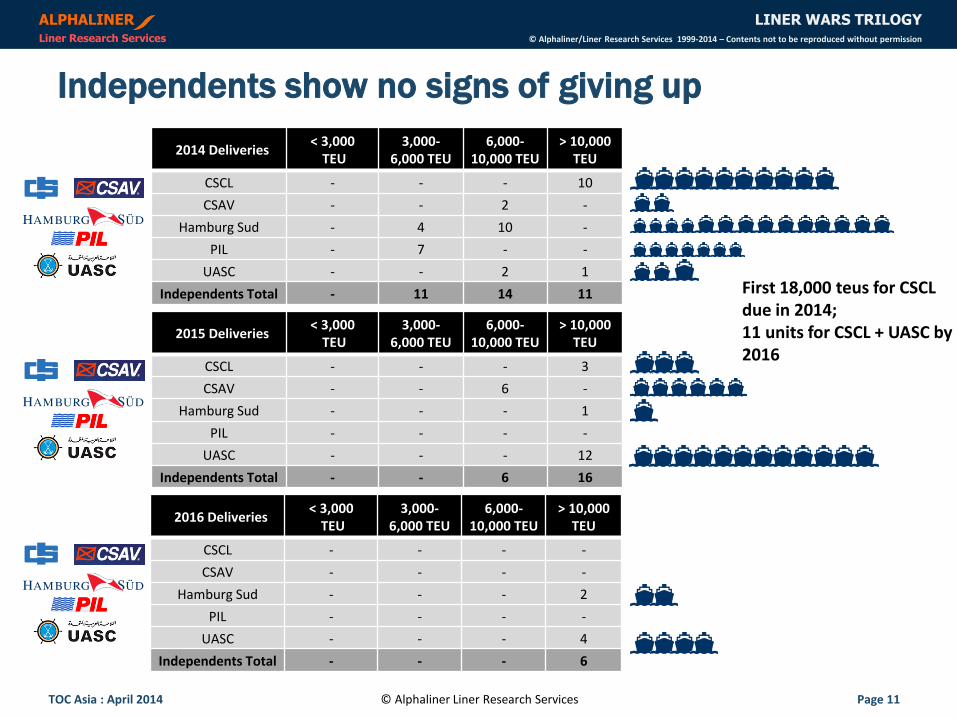

Independents show no signs of giving up

Page 11

First 18,000 teus for CSCL due in 2014; 11 units for CSCL + UASC by 2016

2014 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

CSCL - - - 10

CSAV - - 2 -

Hamburg Sud - 4 10 -

PIL - 7 - -

UASC - - 2 1

Independents Total - 11 14 11

2015 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

CSCL - - - 3

CSAV - - 6 -

Hamburg Sud - - - 1

PIL - - - -

UASC - - - 12

Independents Total - - 6 16

2016 Deliveries < 3,000

TEU 3,000-

6,000 TEU 6,000-

10,000 TEU > 10,000

TEU

CSCL - - - -

CSAV - - - -

Hamburg Sud - - - 2

PIL - - - -

UASC - - - 4

Independents Total - - - 6

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

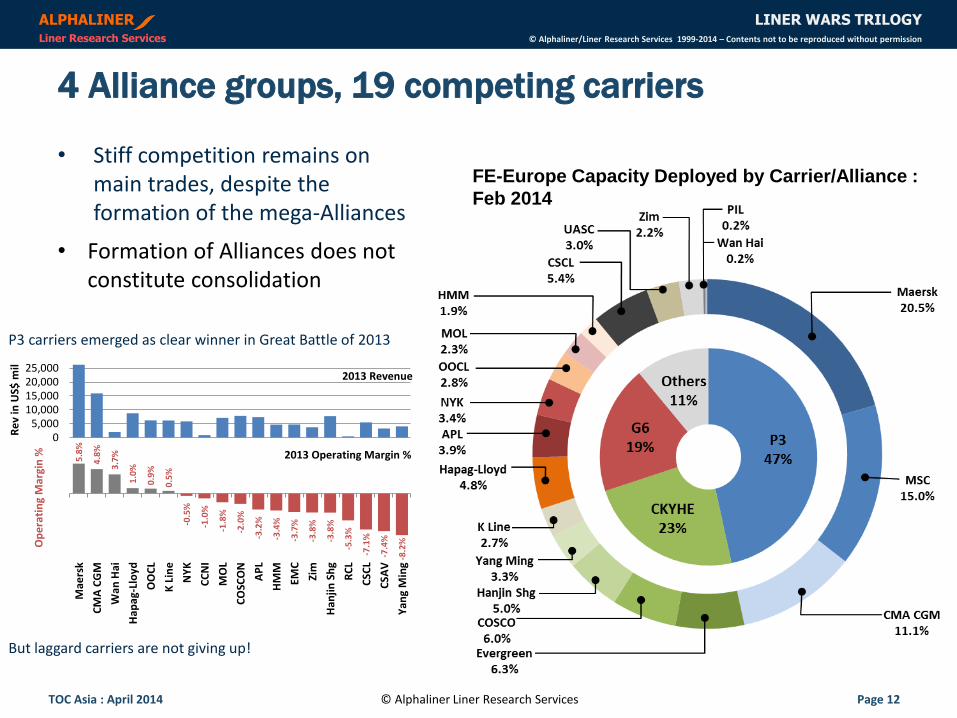

4 Alliance groups, 19 competing carriers

Page 12

• Stiff competition remains on main trades, despite the formation of the mega-Alliances

FE-Europe Capacity Deployed by Carrier/Alliance :

Feb 2014

P3 carriers emerged as clear winner in Great Battle of 2013

But laggard carriers are not giving up!

• Formation of Alliances does not constitute consolidation

05,000

10,00015,00020,00025,00030,000

Re

v in

US$

mil

2013 Revenue

5.8

%

4.8

%

3.7

%

1.0

%

0.9

%

0.5

%

-0.5

%

-1.0

%

-1.8

%

-2.0

%

-3.2

%

-3.4

%

-3.7

%

-3.8

%

-3.8

%

-5.3

%

-7.1

%

-7.4

%

-8.2

%

Mae

rsk

CM

A C

GM

Wan

Hai

Hap

ag-

Llo

yd

OO

CL

K L

ine

NY

K

CC

NI

MO

L

CO

SCO

N

AP

L

HM

M

EMC

Zim

Han

jin

Sh

g

RC

L

CSC

L

CSA

V

Yan

g M

ing

Op

era

tin

g M

argi

n %

2013 Operating Margin %

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

War of attrition – not achieving its goals

Page 13

• a strategy in which a belligerent side attempts to win a war by wearing down its enemy to the point of collapse through continuous losses in resources and materiel

28

%

61

%

53

%

38

%

58

%

46

%

32

%

69

%

32

% 45

%

48

%

8%

26

%

99

%

23

%

10

%

34

%

22

%

76

%

-10

%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

AP

M-M

aers

k

MSC

CM

A C

GM

Eve

rgre

en

CO

SCO

N

Hap

ag-L

loyd

AP

L

Han

jin S

hg

CSC

L

MO

L

Ham

bu

rg S

üd

NYK

Lin

e

OO

CL

PIL

Yan

g M

ing

K L

ine

Hyu

nd

ai M

.M.

Zim

UA

SC

CSA

V G

rou

p

Cap

acit

y O

pe

rate

d in

TEU

Mill

ion

s

Fleet as at Feb 2014Fleet as at Jan 2009

• No major carrier exits since 2009

• 19 of Top 20 registered capacity increases

• Average 5 year growth rate of 40% or 7% CAGR

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

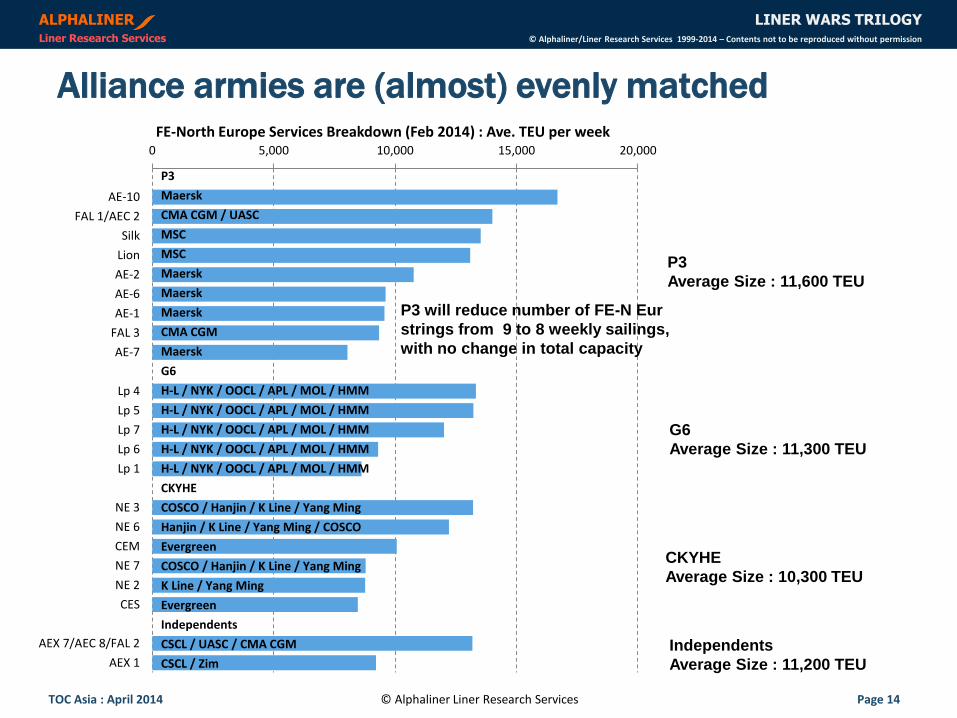

Alliance armies are (almost) evenly matched

Page 14

0 5,000 10,000 15,000 20,000

AE-10

FAL 1/AEC 2

Silk

Lion

AE-2

AE-6

AE-1

FAL 3

AE-7

Lp 4

Lp 5

Lp 7

Lp 6

Lp 1

NE 3

NE 6

CEM

NE 7

NE 2

CES

AEX 7/AEC 8/FAL 2

AEX 1

FE-North Europe Services Breakdown (Feb 2014) : Ave. TEU per week

P3

Maersk

CMA CGM / UASC

MSC

MSC

Maersk

Maersk

Maersk

CMA CGM

Maersk

G6

H-L / NYK / OOCL / APL / MOL / HMM

H-L / NYK / OOCL / APL / MOL / HMM

H-L / NYK / OOCL / APL / MOL / HMM

H-L / NYK / OOCL / APL / MOL / HMM

H-L / NYK / OOCL / APL / MOL / HMM

CKYHE

COSCO / Hanjin / K Line / Yang Ming

Hanjin / K Line / Yang Ming / COSCO

Evergreen

COSCO / Hanjin / K Line / Yang Ming

K Line / Yang Ming

Evergreen

Independents

CSCL / UASC / CMA CGM

CSCL / Zim

P3

Average Size : 11,600 TEU

G6

Average Size : 11,300 TEU

CKYHE

Average Size : 10,300 TEU

Independents

Average Size : 11,200 TEU

P3 will reduce number of FE-N Eur

strings from 9 to 8 weekly sailings,

with no change in total capacity

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

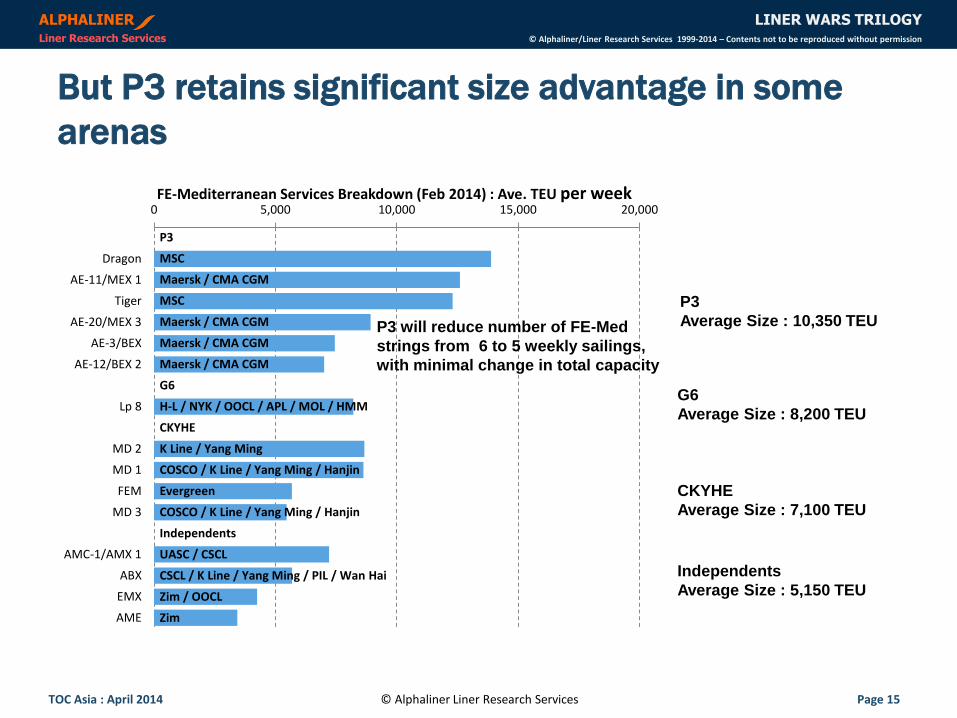

But P3 retains significant size advantage in some

arenas

0 5,000 10,000 15,000 20,000

Dragon

AE-11/MEX 1

Tiger

AE-20/MEX 3

AE-3/BEX

AE-12/BEX 2

Lp 8

MD 2

MD 1

FEM

MD 3

AMC-1/AMX 1

ABX

EMX

AME

FE-Mediterranean Services Breakdown (Feb 2014) : Ave. TEU per week

Page 15

P3

Average Size : 10,350 TEU

G6

Average Size : 8,200 TEU

CKYHE

Average Size : 7,100 TEU

Independents

Average Size : 5,150 TEU

P3

MSC

Maersk / CMA CGM

MSC

Maersk / CMA CGM

Maersk / CMA CGM

Maersk / CMA CGM

G6

H-L / NYK / OOCL / APL / MOL / HMM

CKYHE

K Line / Yang Ming

COSCO / K Line / Yang Ming / Hanjin

Evergreen

COSCO / K Line / Yang Ming / Hanjin

Independents

UASC / CSCL

CSCL / K Line / Yang Ming / PIL / Wan Hai

Zim / OOCL

Zim

P3 will reduce number of FE-Med

strings from 6 to 5 weekly sailings,

with minimal change in total capacity

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

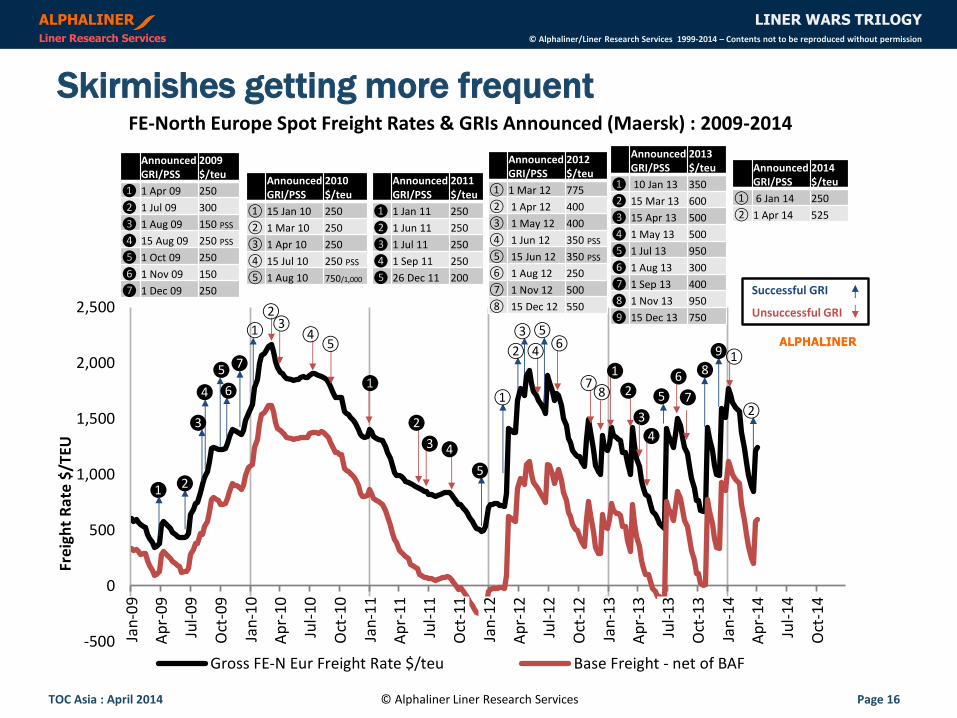

Skirmishes getting more frequent

Page 16

-500

0

500

1,000

1,500

2,000

2,500

Jan

-09

Ap

r-09

Jul-

09

Oct

-09

Jan

-10

Ap

r-10

Jul-

10

Oct

-10

Jan

-11

Ap

r-11

Jul-

11

Oct

-11

Jan

-12

Ap

r-12

Jul-

12

Oct

-12

Jan

-13

Ap

r-13

Jul-

13

Oct

-13

Jan

-14

Ap

r-14

Jul-

14

Oct

-14

Fre

igh

t R

ate

$/T

EU

Gross FE-N Eur Freight Rate $/teu Base Freight - net of BAF

SSEFC Forward Curve

Successful GRI

Unsuccessful GRI

Announced GRI/PSS

2009 $/teu

❶ 1 Apr 09 250

❷ 1 Jul 09 300

❸ 1 Aug 09 150 PSS

❹ 15 Aug 09 250 PSS

❺ 1 Oct 09 250

❻ 1 Nov 09 150

❼ 1 Dec 09 250

❶ ❷

❸

❹

❺

❻

❼

①

② ③

④ ⑤

❶

❷

❸ ❹

❺

①

②

③

④

⑤ ⑥

⑦ ⑧

❶

Announced GRI/PSS

2010 $/teu

① 15 Jan 10 250

② 1 Mar 10 250

③ 1 Apr 10 250

④ 15 Jul 10 250 PSS

⑤ 1 Aug 10 750/1,000

Announced GRI/PSS

2011 $/teu

❶ 1 Jan 11 250

❷ 1 Jun 11 250

❸ 1 Jul 11 250

❹ 1 Sep 11 250

❺ 26 Dec 11 200

Announced GRI/PSS

2012 $/teu

① 1 Mar 12 775

② 1 Apr 12 400

③ 1 May 12 400

④ 1 Jun 12 350 PSS

⑤ 15 Jun 12 350 PSS

⑥ 1 Aug 12 250

⑦ 1 Nov 12 500

⑧ 15 Dec 12 550

Announced GRI/PSS

2013 $/teu

❶ 10 Jan 13 350

❷ 15 Mar 13 600

❸ 15 Apr 13 500

❹ 1 May 13 500

❺ 1 Jul 13 950

❻ 1 Aug 13 300

❼ 1 Sep 13 400

❽ 1 Nov 13 950

❾ 15 Dec 13 750

❷

❸

❹

❺

FE-North Europe Spot Freight Rates & GRIs Announced (Maersk) : 2009-2014

❻

❼

❽

❾

Announced GRI/PSS

2014 $/teu

① 6 Jan 14 250

② 1 Apr 14 525

①

②

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

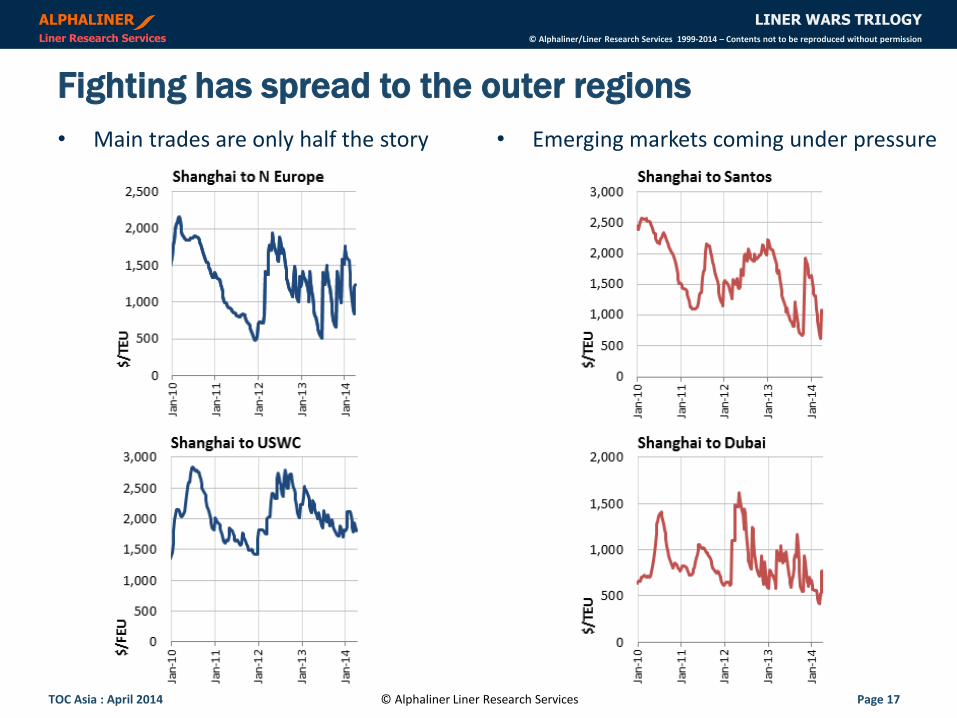

Fighting has spread to the outer regions

Page 17

• Main trades are only half the story

• Emerging markets coming under pressure

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

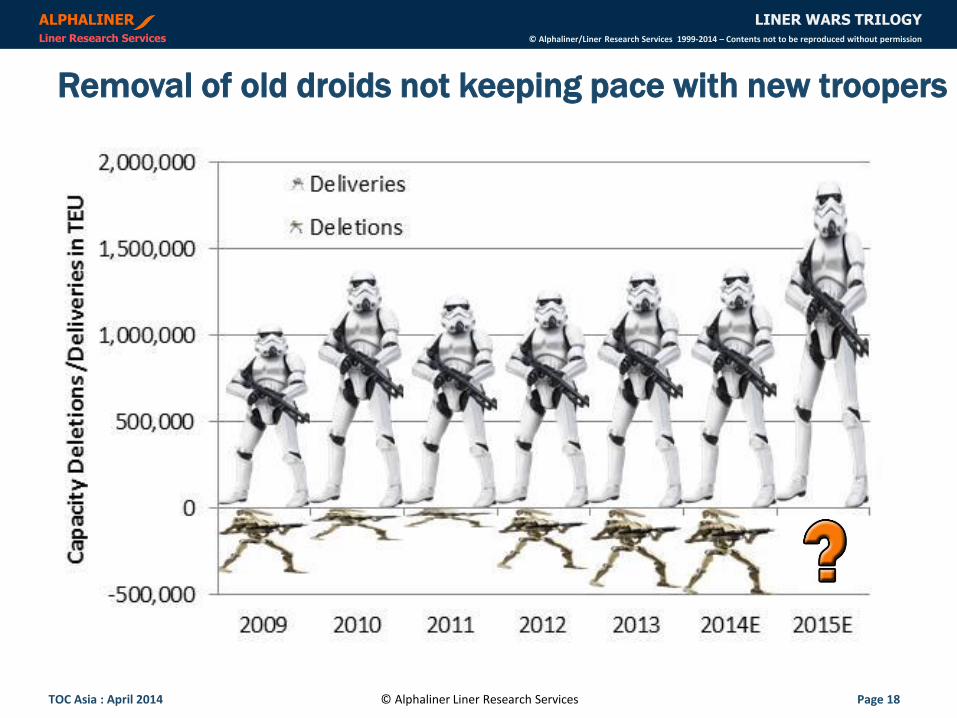

Removal of old droids not keeping pace with new troopers

Page 18

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

Peace is not upon us

Page 19

• CSAV/Hapag-Lloyd : Significant hurdles still to be cleared, merger benefits not apparent

• COSCO/CSCL : Pact a politically driven half measure, doesn’t help either party

• Hanjin/HMM : Selling family silver, but holding on to container assets

• Zim : Debtors pay price, but no exit from container shipping

• NYK/MOL/KL : Held back in last few years, MOL has just committed to Seaspan charters while NYK will need to order new tonnage soon

• Evergreen : Sticking to its guns – new capacity injections will disturb market

• UASC : 14,000/18,000 teu orders – even more aggressive expansion ahead

• Hamburg Sud/PIL : defending niche markets

• APL/OOCL : running out of ideas; could corporate action be imminent?

• MSC/CMA CGM : massive fleet rebuilding with 9,000/18,000 teu orders

• Maersk – how will it react?

• Expect Liner Wars to last until 2016 if capacity build up cannot be curbed this year

ALPHALINER LINER WARS TRILOGY Liner Research Services © Alphaliner/Liner Research Services 1999-2014 – Contents not to be reproduced without permission

TOC Asia : April 2014 © Alphaliner Liner Research Services

End

Please send any queries to [email protected]

Page 20

Alphaliner clients include the following top shipping lines :