Embed Size (px)

Citation preview

Lightweight Options and Forecast of Material Types

April 19, 2016

Global snapshot of lightweight solutions

Presented by Vishwas Shankar

FROST & SULLIVAN

2

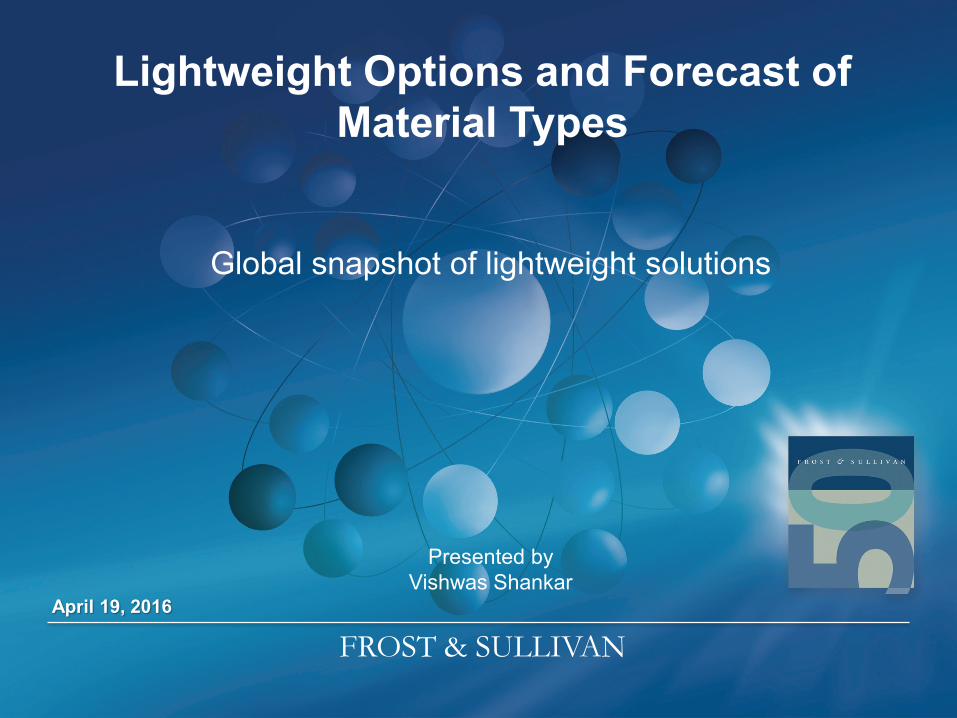

OEMs Identify 350 Kg Weight Reduction (20%) Opportunity Global OEMs have identified to lose upto 350 kg depending on the model, segment, brand of the vehicle—en route to achieve the desired 2020 CO2 emission / 2025 CAFE targets.

0 50 100 150 200 250 300 350 400

Ford

VW

BMW

Hyundai

Weight Reduction (Kg)

OEM

Gro

ups

3-Series 5-Series X5

Golf 7 Touareg

F-150

Elantra Santa Fe

Focus

Source: Frost & Sullivan

Automotive OEMs Identify Up to 350 Kg Weight Reduction, Global, 2013–2020

3

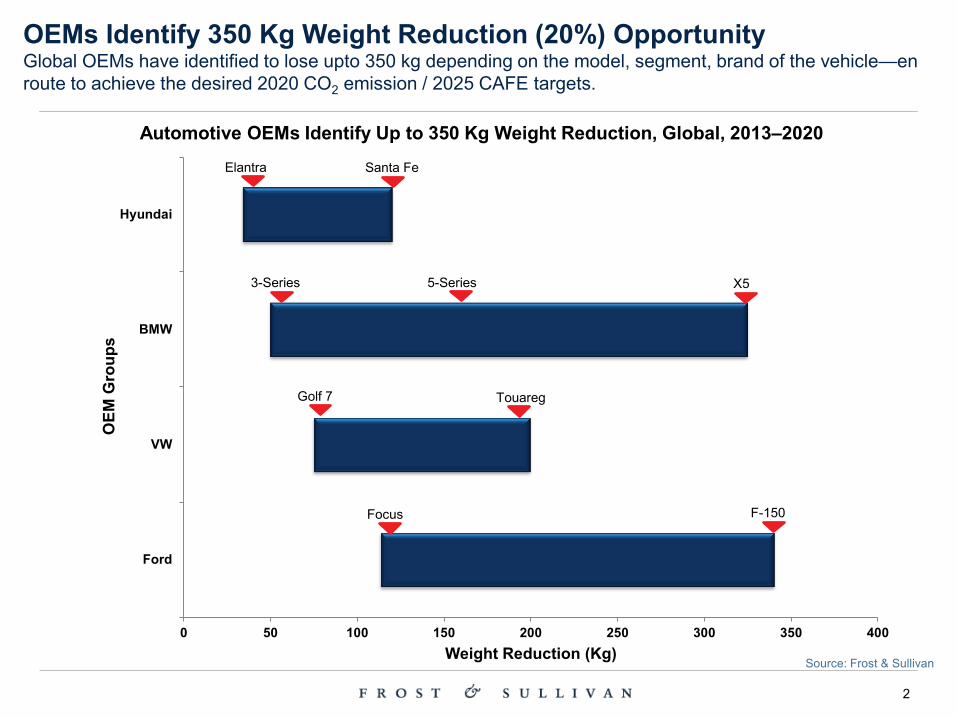

50 years of Weight Trends – Global Best Selling OEM Models 1 in 2 OEMs reduced weight of their best selling model in fleet globally in the last generation.

953

1,022

1,073 1,089

1,035 982

1,042 1,048

1,153

1,065 1,060 1,134

1,197

1,182

720 730

880 855

1,047

1,086 1,052

1,095 1,095

1,300

1,240

1,292 1,328

1,353

1,442 1,409

1,120

1,506

1,434 1,455

1,500

1,524

915 940

1,130

1,210

1,510 1,567

1,310

1,380

1,491 1,537

1,074

1,188 1,190

1,407

700

1,600

1966 2012

Cur

b W

eigh

t of V

ehic

le (k

g)

Year

Automotive Best Seller Model Generations Vs. Weight Reduction, Global, 1966–2013

BMW 3 Series

Chrysler 200

Nissan Altima

Chevrolet Cruze

Ford Focus

Honda Civic

Hyundai Accent

Note: Models that lost weight in the last generation

Toyota Corolla

VW Passat

Sub 1,000 kg Best Sellers

Source: Frost & Sullivan

4

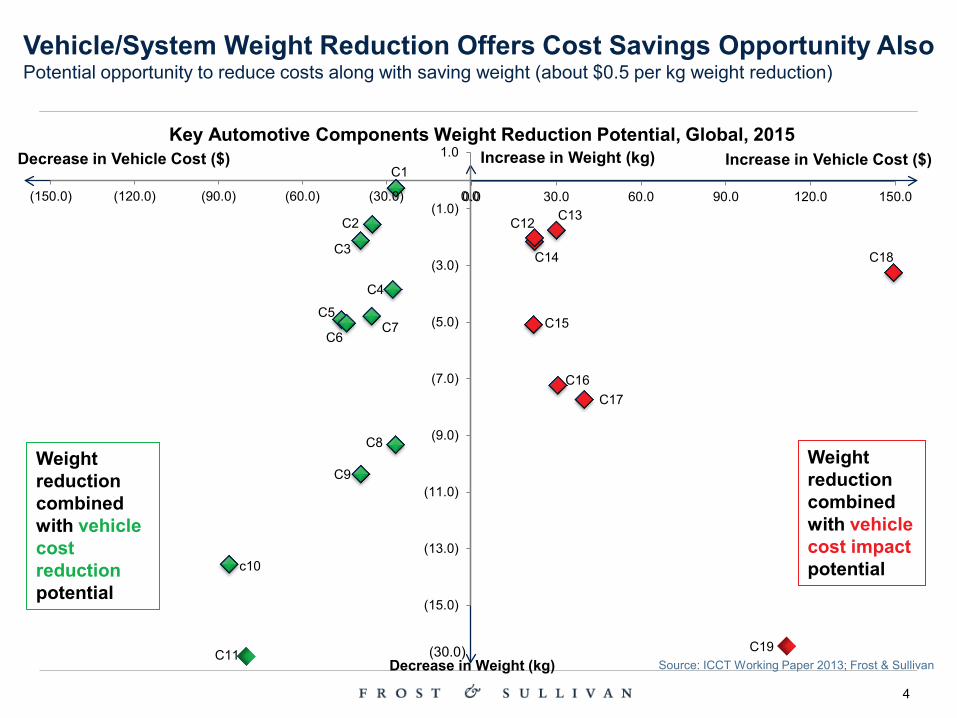

0.0 30.0 60.0 90.0 120.0 150.0

Key Automotive Components Weight Reduction Potential, Global, 2015 Increase in Weight (kg)

Decrease in Weight (kg)

Decrease in Vehicle Cost ($)

(15.0)

(13.0)

(11.0)

(9.0)

(7.0)

(5.0)

(3.0)

(1.0)

1.0

(150.0) (120.0) (90.0) (60.0) (30.0) 0.0

Weight reduction combined with vehicle cost reduction potential

Weight reduction combined with vehicle cost impact potential

C1

C18

C17 C16

C13

C14

C12

C15

Source: ICCT Working Paper 2013; Frost & Sullivan

C2

C3

C5

C6 C7

C4

C8

C9

c10

Increase in Vehicle Cost ($)

(30.0) C11 C19

Vehicle/System Weight Reduction Offers Cost Savings Opportunity Also Potential opportunity to reduce costs along with saving weight (about $0.5 per kg weight reduction)

5

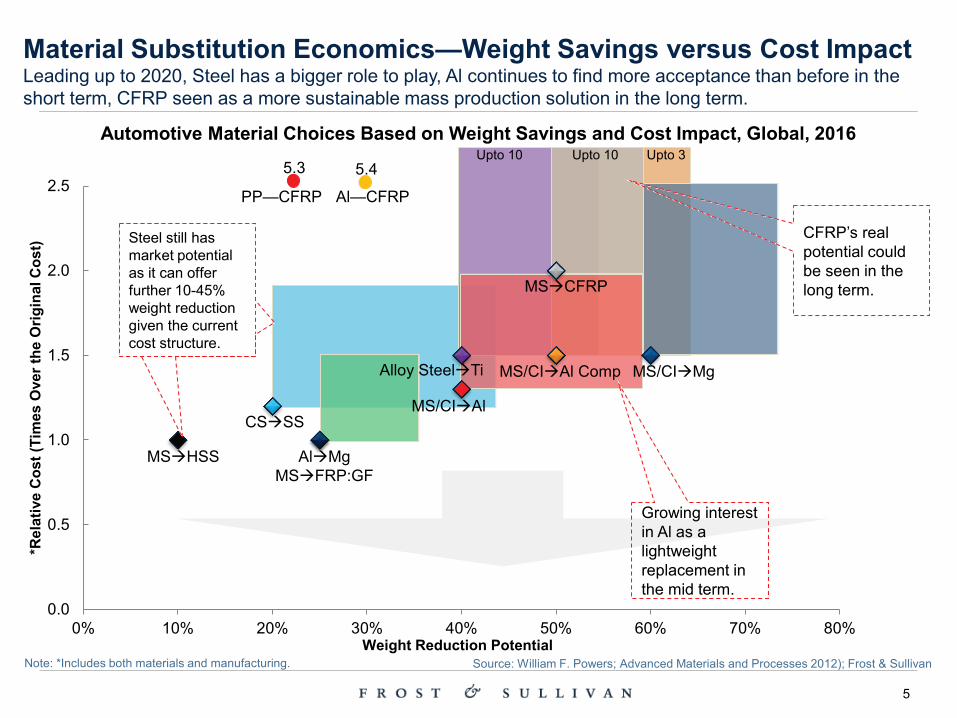

Material Substitution Economics—Weight Savings versus Cost Impact Leading up to 2020, Steel has a bigger role to play, Al continues to find more acceptance than before in the short term, CFRP seen as a more sustainable mass production solution in the long term.

0.0

0.5

1.0

1.5

2.0

2.5

0% 10% 20% 30% 40% 50% 60% 70% 80%

*Rel

ativ

e C

ost (

Tim

es O

ver t

he O

rigin

al C

ost)

Weight Reduction Potential

MSHSS

CSSS

AlMg MSFRP:GF

MSCFRP

Alloy SteelTi

MS/CIAl

MS/CIAl Comp MS/CIMg

Upto 10 Upto 10 Upto 3

Source: William F. Powers; Advanced Materials and Processes 2012); Frost & Sullivan

Automotive Material Choices Based on Weight Savings and Cost Impact, Global, 2016

Steel still has market potential as it can offer further 10-45% weight reduction given the current cost structure.

Growing interest in Al as a lightweight replacement in the mid term.

CFRP’s real potential could be seen in the long term.

PP—CFRP

5.3

Al—CFRP

5.4

Note: *Includes both materials and manufacturing.

6

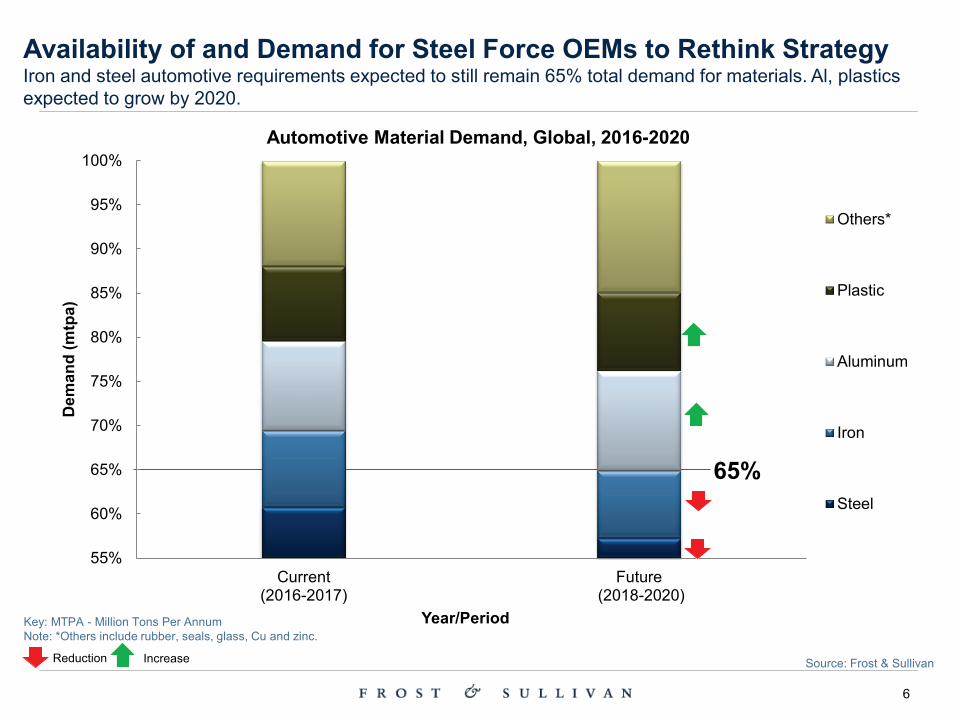

Automotive Material Demand, Global, 2016-2020

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Current(2016-2017)

Future (2018-2020)

Dem

and

(mtp

a)

Year/Period

Others*

Plastic

Aluminum

Iron

Steel

Key: MTPA - Million Tons Per Annum Note: *Others include rubber, seals, glass, Cu and zinc.

Reduction Increase

Availability of and Demand for Steel Force OEMs to Rethink Strategy Iron and steel automotive requirements expected to still remain 65% total demand for materials. Al, plastics expected to grow by 2020.

Source: Frost & Sullivan

65%

7

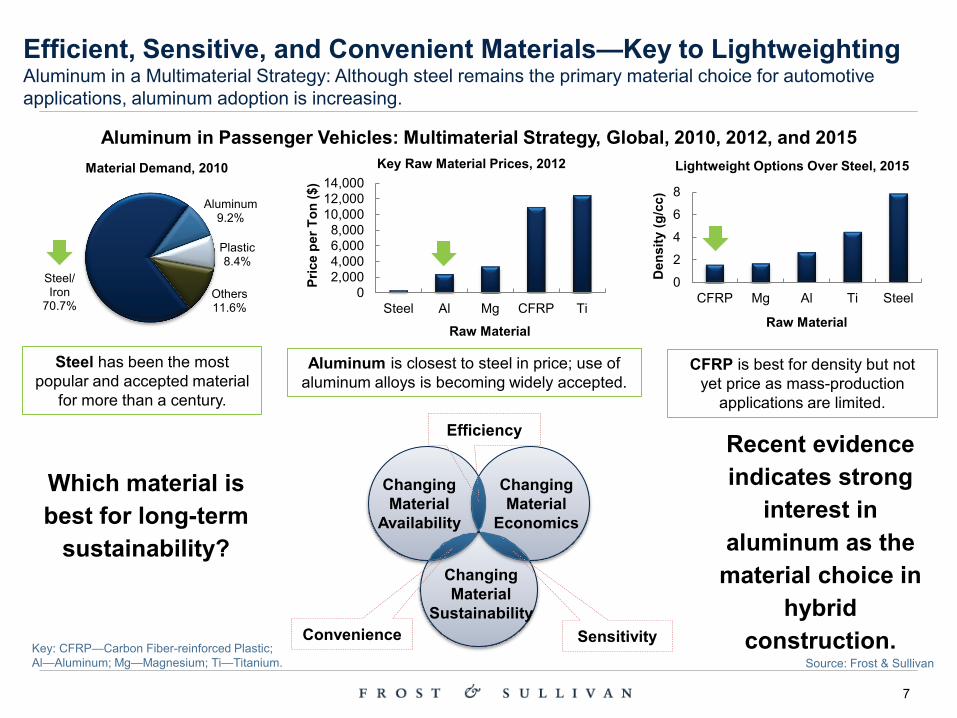

Efficient, Sensitive, and Convenient Materials—Key to Lightweighting Aluminum in a Multimaterial Strategy: Although steel remains the primary material choice for automotive applications, aluminum adoption is increasing.

Source: Frost & Sullivan

02,0004,0006,0008,000

10,00012,00014,000

Steel Al Mg CFRP Ti

Aluminum in Passenger Vehicles: Multimaterial Strategy, Global, 2010, 2012, and 2015

Steel/ Iron

70.7%

Aluminum 9.2%

Plastic 8.4%

Others 11.6%

Material Demand, 2010

Steel has been the most popular and accepted material

for more than a century.

Lightweight Options Over Steel, 2015

Pric

e pe

r Ton

($)

Aluminum is closest to steel in price; use of aluminum alloys is becoming widely accepted.

Raw Material

0

2

4

6

8

CFRP Mg Al Ti Steel

Den

sity

(g/c

c)

Raw Material

Key Raw Material Prices, 2012

CFRP is best for density but not yet price as mass-production

applications are limited.

Changing Material

Availability

Changing Material

Economics

Changing Material

Sustainability Convenience Sensitivity

Efficiency

Which material is best for long-term

sustainability?

Recent evidence indicates strong

interest in aluminum as the

material choice in hybrid

construction. Key: CFRP—Carbon Fiber-reinforced Plastic; Al—Aluminum; Mg—Magnesium; Ti—Titanium.

8

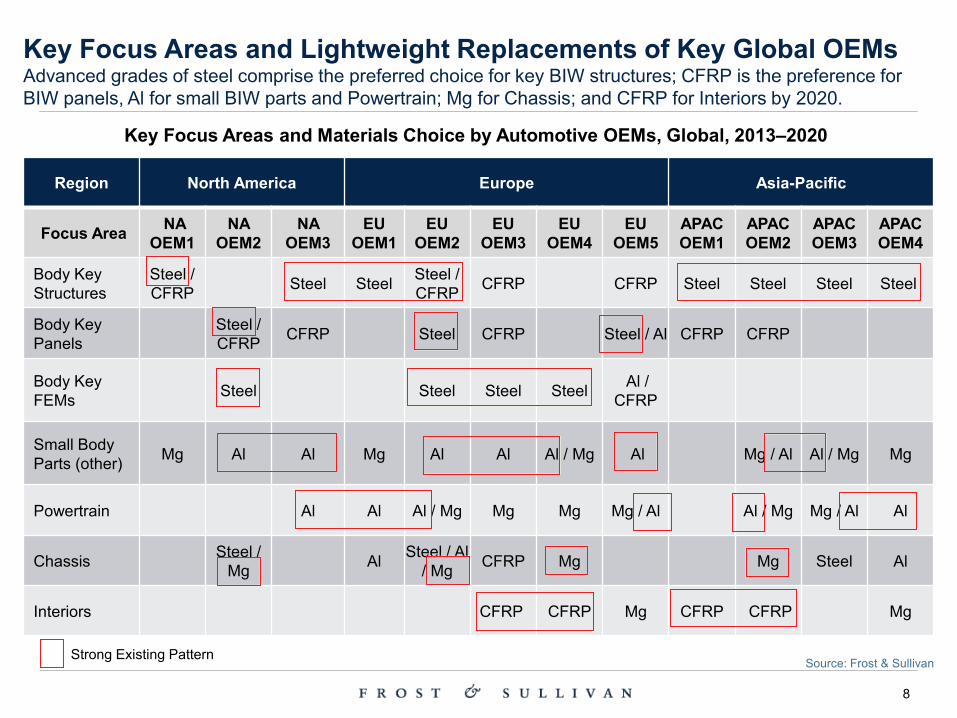

Region North America Europe Asia-Pacific

Focus Area NA OEM1

NA OEM2

NA OEM3

EU OEM1

EU OEM2

EU OEM3

EU OEM4

EU OEM5

APAC OEM1

APAC OEM2

APAC OEM3

APAC OEM4

Body Key Structures

Steel / CFRP Steel Steel Steel /

CFRP CFRP CFRP Steel Steel Steel Steel

Body Key Panels Steel /

CFRP CFRP Steel CFRP Steel / Al CFRP CFRP

Body Key FEMs Steel Steel Steel Steel Al /

CFRP

Small Body Parts (other) Mg Al Al Mg Al Al Al / Mg Al Mg / Al Al / Mg Mg

Powertrain Al Al Al / Mg Mg Mg Mg / Al Al / Mg Mg / Al Al

Chassis Steel / Mg Al Steel / Al

/ Mg CFRP Mg Mg Steel Al

Interiors CFRP CFRP Mg CFRP CFRP Mg

Key Focus Areas and Materials Choice by Automotive OEMs, Global, 2013–2020

Strong Existing Pattern

Key Focus Areas and Lightweight Replacements of Key Global OEMs Advanced grades of steel comprise the preferred choice for key BIW structures; CFRP is the preference for BIW panels, Al for small BIW parts and Powertrain; Mg for Chassis; and CFRP for Interiors by 2020.

Source: Frost & Sullivan

9

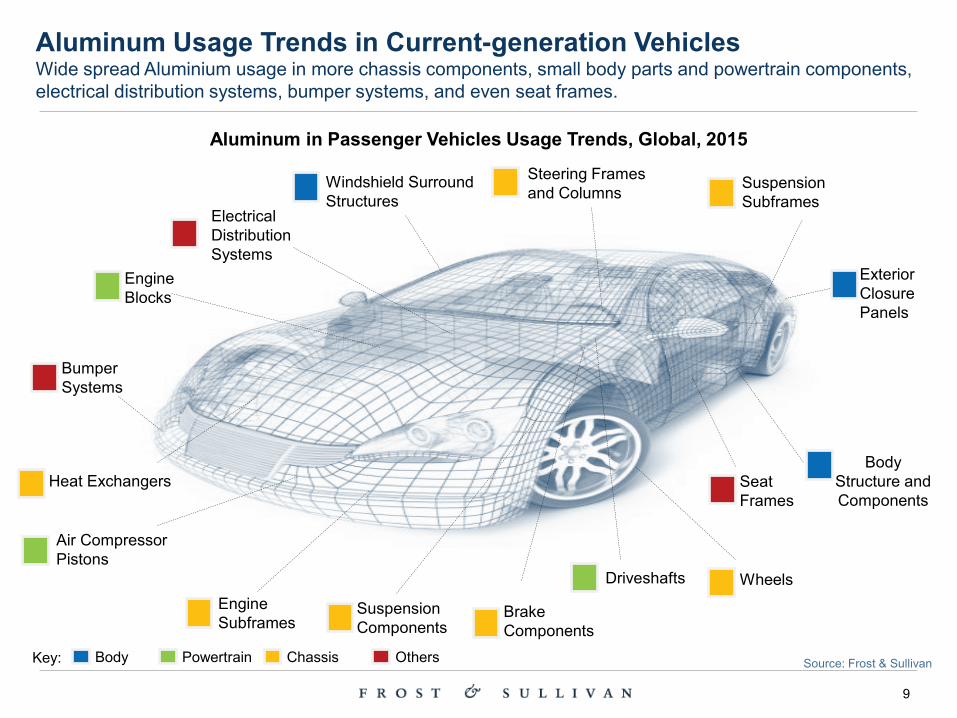

Source: Frost & Sullivan

Aluminum Usage Trends in Current-generation Vehicles Wide spread Aluminium usage in more chassis components, small body parts and powertrain components, electrical distribution systems, bumper systems, and even seat frames.

Aluminum in Passenger Vehicles Usage Trends, Global, 2015

Electrical Distribution Systems

Engine Blocks

Brake Components

Engine Subframes

Heat Exchangers Seat Frames

Body Structure and Components

Driveshafts

Suspension Subframes

Windshield Surround Structures

Air Compressor Pistons

Bumper Systems

Wheels

Exterior Closure Panels

Steering Frames and Columns

Suspension Components

Body Key: Powertrain Chassis Others

10

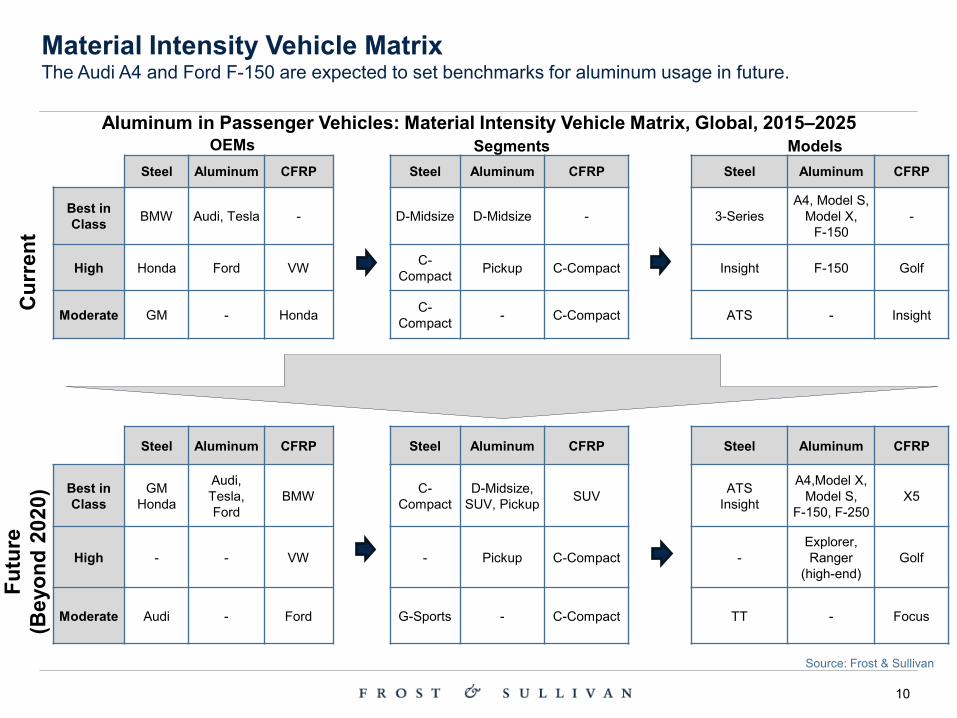

Source: Frost & Sullivan

Material Intensity Vehicle Matrix The Audi A4 and Ford F-150 are expected to set benchmarks for aluminum usage in future.

Aluminum in Passenger Vehicles: Material Intensity Vehicle Matrix, Global, 2015–2025

Steel Aluminum CFRP Steel Aluminum CFRP Steel Aluminum CFRP

Best in Class BMW Audi, Tesla - D-Midsize D-Midsize - 3-Series

A4, Model S, Model X,

F-150 -

High Honda Ford VW C-Compact Pickup C-Compact Insight F-150 Golf

Moderate GM - Honda C-Compact - C-Compact ATS - Insight

Steel Aluminum CFRP Steel Aluminum CFRP Steel Aluminum CFRP

Best in Class

GM Honda

Audi, Tesla, Ford

BMW C-Compact

D-Midsize, SUV, Pickup SUV ATS

Insight

A4,Model X, Model S,

F-150, F-250 X5

High - - VW - Pickup C-Compact - Explorer, Ranger

(high-end) Golf

Moderate Audi - Ford G-Sports - C-Compact TT - Focus

OEMs

Cur

rent

Fu

ture

(B

eyon

d 20

20)

Segments Models

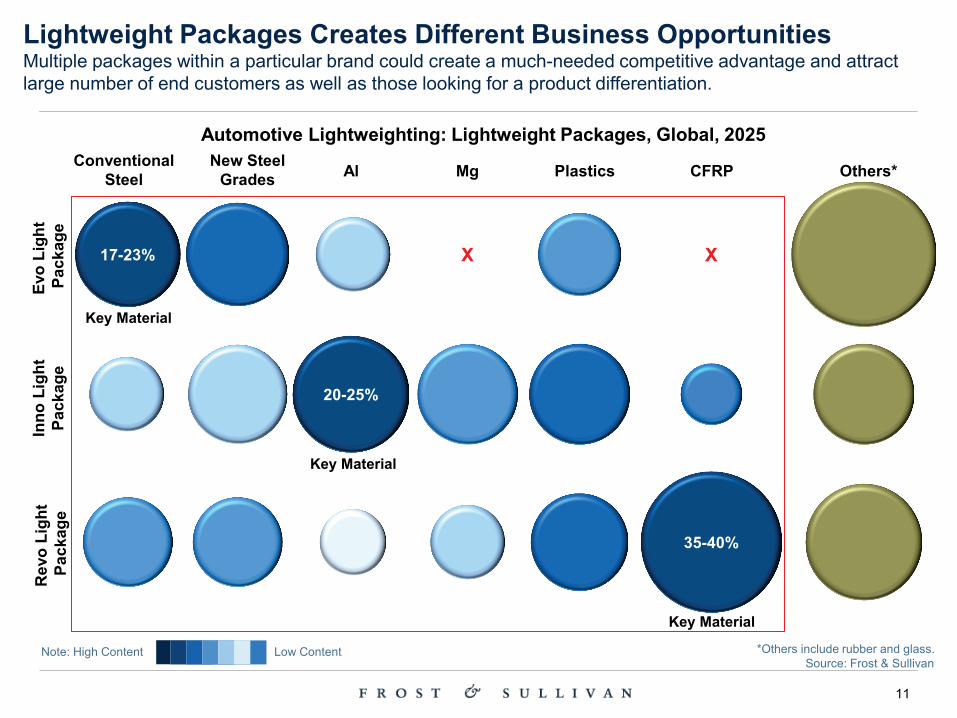

11

Evo

Ligh

t Pa

ckag

e In

no L

ight

Pa

ckag

e R

evo

Ligh

t Pa

ckag

e

17-23%

Conventional Steel Al Mg Plastics CFRP

X X

Others* New Steel Grades

20-25%

35-40%

Automotive Lightweighting: Lightweight Packages, Global, 2025

Note: High Content Low Content

Key Material

Key Material

Key Material

*Others include rubber and glass.

Lightweight Packages Creates Different Business Opportunities Multiple packages within a particular brand could create a much-needed competitive advantage and attract large number of end customers as well as those looking for a product differentiation.

Source: Frost & Sullivan

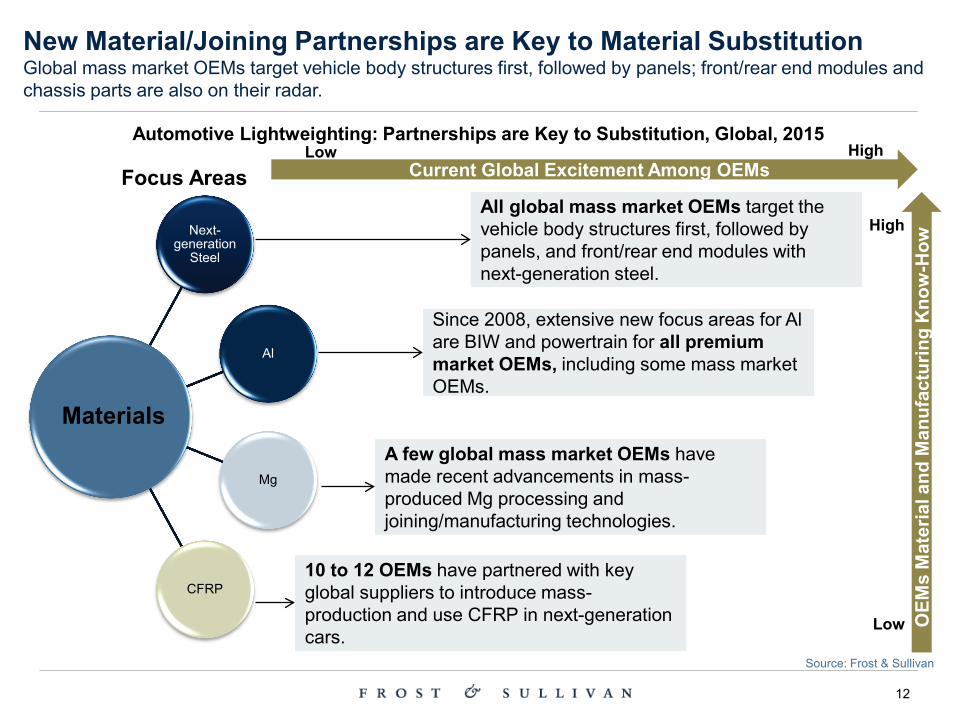

12

Next-generation

Steel

Al

Mg

CFRP

Automotive Lightweighting: Partnerships are Key to Substitution, Global, 2015

All global mass market OEMs target the vehicle body structures first, followed by panels, and front/rear end modules with next-generation steel.

Since 2008, extensive new focus areas for Al are BIW and powertrain for all premium market OEMs, including some mass market OEMs.

A few global mass market OEMs have made recent advancements in mass-produced Mg processing and joining/manufacturing technologies.

10 to 12 OEMs have partnered with key global suppliers to introduce mass-production and use CFRP in next-generation cars.

Current Global Excitement Among OEMs

OEM

s M

ater

ial a

nd M

anuf

actu

ring

Kno

w-H

ow

Low

High

High Low Focus Areas

Materials

New Material/Joining Partnerships are Key to Material Substitution Global mass market OEMs target vehicle body structures first, followed by panels; front/rear end modules and chassis parts are also on their radar.

Source: Frost & Sullivan

13

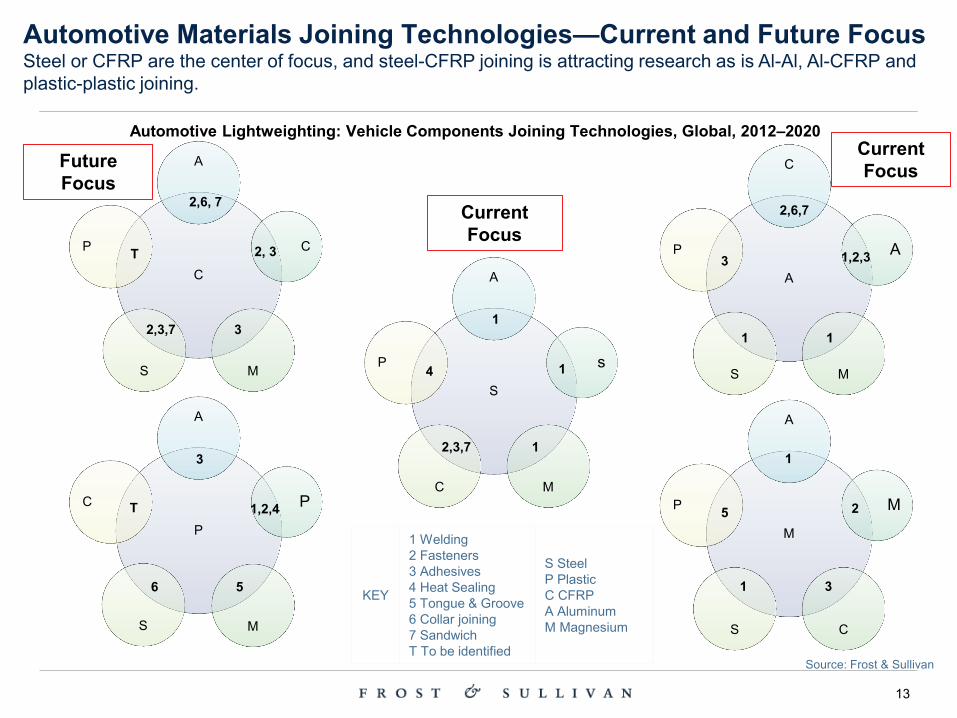

P

A

P

M S

C

S

A

s

M C

P

M

A

M

C S

P

A

C

A

M S

P

C

A

C

M S

P T

2,6, 7

2,3,7

2, 3

KEY

1 Welding 2 Fasteners 3 Adhesives 4 Heat Sealing 5 Tongue & Groove 6 Collar joining 7 Sandwich T To be identified

S Steel P Plastic C CFRP A Aluminum M Magnesium

3

4

1

2,3,7

1

1

3

2,6,7

1

1,2,3

1

5

1

1

2

3

T

3

6

1,2,4

5

Automotive Lightweighting: Vehicle Components Joining Technologies, Global, 2012–2020

Current Focus

Future Focus

Automotive Materials Joining Technologies—Current and Future Focus Steel or CFRP are the center of focus, and steel-CFRP joining is attracting research as is Al-Al, Al-CFRP and plastic-plastic joining.

Source: Frost & Sullivan

Current Focus

14

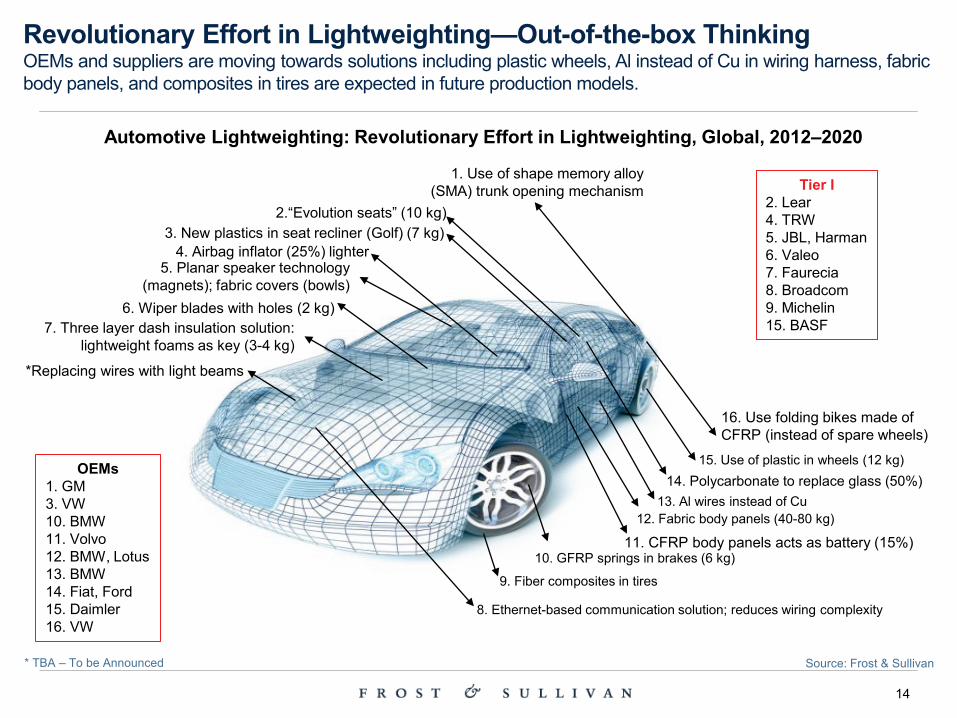

12. Fabric body panels (40-80 kg) 13. Al wires instead of Cu

10. GFRP springs in brakes (6 kg)

15. Use of plastic in wheels (12 kg) 14. Polycarbonate to replace glass (50%)

1. Use of shape memory alloy (SMA) trunk opening mechanism

11. CFRP body panels acts as battery (15%)

3. New plastics in seat recliner (Golf) (7 kg)

16. Use folding bikes made of CFRP (instead of spare wheels)

7. Three layer dash insulation solution: lightweight foams as key (3-4 kg)

5. Planar speaker technology (magnets); fabric covers (bowls)

2.“Evolution seats” (10 kg)

9. Fiber composites in tires

*Replacing wires with light beams

4. Airbag inflator (25%) lighter

6. Wiper blades with holes (2 kg)

Automotive Lightweighting: Revolutionary Effort in Lightweighting, Global, 2012–2020

OEMs 1. GM 3. VW 10. BMW 11. Volvo 12. BMW, Lotus 13. BMW 14. Fiat, Ford 15. Daimler 16. VW

Tier I 2. Lear 4. TRW 5. JBL, Harman 6. Valeo 7. Faurecia 8. Broadcom 9. Michelin 15. BASF

* TBA – To be Announced

8. Ethernet-based communication solution; reduces wiring complexity

Revolutionary Effort in Lightweighting—Out-of-the-box Thinking OEMs and suppliers are moving towards solutions including plastic wheels, Al instead of Cu in wiring harness, fabric body panels, and composites in tires are expected in future production models.

Source: Frost & Sullivan

15

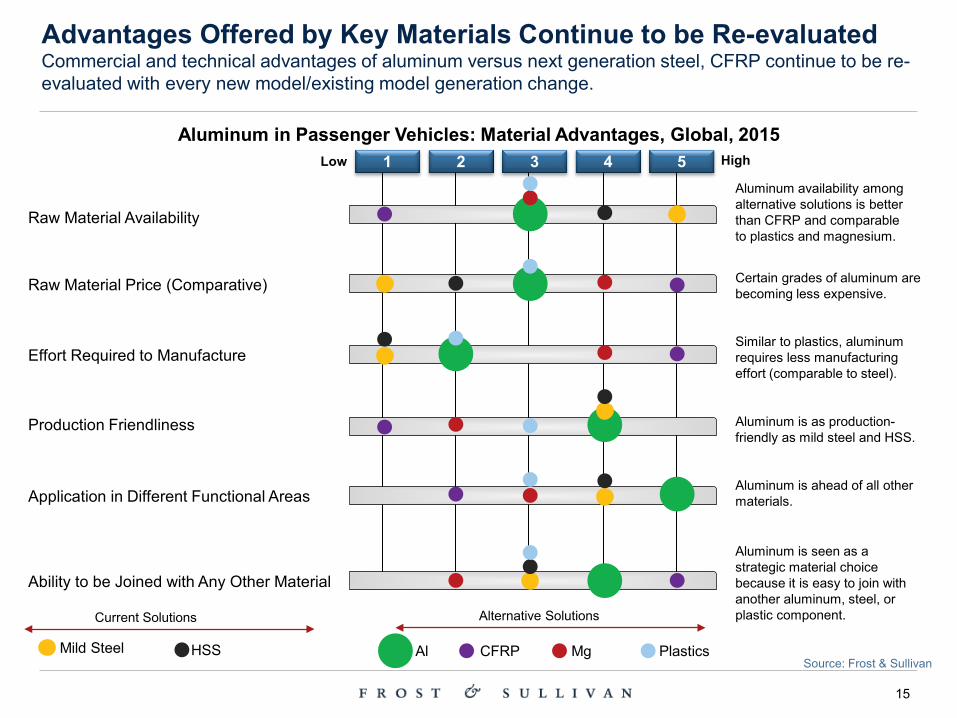

Source: Frost & Sullivan

Advantages Offered by Key Materials Continue to be Re-evaluated Commercial and technical advantages of aluminum versus next generation steel, CFRP continue to be re-evaluated with every new model/existing model generation change.

Aluminum in Passenger Vehicles: Material Advantages, Global, 2015 1 2 3 4 5

Raw Material Availability

Raw Material Price (Comparative)

Effort Required to Manufacture

Production Friendliness

Application in Different Functional Areas

Ability to be Joined with Any Other Material

Low High

Mild Steel HSS CFRP Mg Plastics Al

Current Solutions Alternative Solutions

Aluminum availability among alternative solutions is better than CFRP and comparable to plastics and magnesium.

Certain grades of aluminum are becoming less expensive.

Similar to plastics, aluminum requires less manufacturing effort (comparable to steel).

Aluminum is as production- friendly as mild steel and HSS.

Aluminum is ahead of all other materials.

Aluminum is seen as a strategic material choice because it is easy to join with another aluminum, steel, or plastic component.

16

Thank You!

Vishwas Shankar Research Manager - Business Strategy & Innovation Mobility P: +1 248 536 2004 [email protected]

www.frost.com/mobility