Embed Size (px)

Citation preview

Liftingthe lid oninsurance

The Chartered Insurance InstituteCustomer Service42-48 High RoadSouth WoodfordLondonE18 2JP

e-mail: [email protected]: www.cii.co.uk

Published June 2008Ref: CII_3443

A brief guide to general insurance

Liftingthe

lidon

insurance

© Chartered Insurance Institute 2008

All rights reserved. Material published in this work is copyright and may not bereproduced in whole or in part, including photocopying or recording, for anypurpose without the written permission of the copyright holder. Such writtenpermission must also be obtained before any part of this publication is storedin a retrieval system of any nature.

Every attempt has been made to ensure the accuracy of this text. However, noliability can be accepted for any loss incurred in any way whatsoever by anyperson relying solely on the information contained within it. The text has beenproduced solely for study purposes and should not be taken as definitive ofthe legal position. Specific advice should always be obtained beforeundertaking any action based on the information contained in this text.

This revised and updated edition first published 2008

Previous edition 2003 (ISBN 1 85369 398 7)

Revision by Valerie Jackson, BSc, FCII, Chartered Insurance Practitioner.

Valerie has worked in the industry for 28 years, originally training on thegraduate development programme with Royal Insurance. She then moved towork with Marsh, latterly as a director of the UK Broking Division inManchester. She left Marsh in 1984 to concentrate on training consultancywork, forming her own training company in 1999. Valerie is involved in a widerange of training and development activities, including tuition for theCertificate in Insurance, Diploma in Insurance and Advanced Diploma inInsurance and accreditation of training and competence programmes on behalfof the CII. She is also author of the CII IF6 and P11 coursebooks.

This guide is a revised version of an earlier work written by Professor GordonDickson and Dr Bill Stein, both from Glasgow Caledonian University. That builton an earlier version by Professor Dickson and John Steele.

These boxes throw more light on what’s beensaid, with examples and so on.

These boxes provide extra technical detail.You can ignore them if you wish!

These boxes test your understanding.?Membership benefits – there when you need them

3 > 1 What is insurance?

13 > 2 The insurance market

19 > 3 Different types of insurance

31 > 4 Arranging cover

41 > 5 Handling claims

49 > 6 Regulation

Contents

The CII is the world’s leading professional organisation for insuranceand financial services. It maintains the professional, ethical andtechnical standards of the industry.

The CII works with corporate business to develop organisation widesolutions for ensuring ongoing competitive advantage throughtechnical and professional competence of employees at every level.

Individually, qualified CII members commit to ContinuousProfessional Development (CPD) through enhancing their knowledgeto maintain their professional standing. Its 90,000 members in150 countries make up the largest professional body in thefinancial world.

As a society, we all rely on professionals to maintain accurate andrelevant knowledge and to give appropriate and unprejudiced advice.The CII ensures that we can trust in the competence and conduct ofinsurance and financial services professionals the world over.

The knowledge, and how

Insurance is there to help the unfortunate few whofind themselves the victim of a loss or an accident.

”“

1 What is insurance?

Jane has decided to buy a car. Whatrisks should she be aware of for whichshe may need insurance?

These could include the following:

• Jane’s car may be damaged in anaccident caused by another driver.

• Jane’s car may be stolen.

• Jane may cause an accident injuringother people and/or damaging their property.

Insurance is there to help theunfortunate few who find themselvesthe victim of a loss or an accident.Insurance is carried on all over theworld. It is a multibillion-poundbusiness and very complex.

This brief guide is an introduction to insuranceand avoids the more complex aspects. In thisand the following sections it attempts toprovide answers to the following questions:

• What is insurance?

• How is the insurance market made up?

• What types of insurance are there?

• How is cover arranged?

• How are claims settled?

We will start by considering the most basic ofall questions: Why do people need insurance?

This guide concentrates on general insurance,that is, all forms of insurance other than lifeassurance and related business. It describeslaw and practice in the UK

The need for insuranceAs we go about our day-to-day lives we arecontinually faced with risks. When we talkabout “risk” we mean the possibility thatsomething may happen which we do not wantto happen.

Take for example owning a house. There aremany possible risks associated with this.Consider the chance of:

• the roof blowing off in a storm;

• the children accidentally breaking a windowwith a football;

• decorations being ruined by a burst pipe;

• setting the kitchen on fire whilst cookinga meal.

Some of these risks might give rise to quitemodest losses, such as the window broken bya football. The individuals affected might beable to pay for such damage from their ownresources. However, some incidents might giverise to quite sizeable losses, as in the case ofthe kitchen being set on fire, or the roofblowing off. The costs of making good suchdamage are likely to be beyond the means ofmost individuals. It is impossible, however, tosay in advance what size of loss will occur.This is where the need for insurance arises.

The idea of insurance is to remove uncertaintyby transferring these unknown financialconsequences of a possible loss to someoneelse. Usually the “someone else” will be aninsurance company. By taking out insurance,the individual is able to have peace of mind byknowing that the unknown loss has beentransferred to an insurance company, inexchange for paying a known sum.

3

4

Faced with the many risks they are exposed to,it is sometimes difficult to see why manypeople operate businesses. They are certainlyin need of some financial protection and theycan find it in the purchase of insurance.

So insurance exists because people needsecurity. They want to own houses, run cars,sell goods, build factories, fly planes, sail ships– but at the same time they do not want to beexposed financially to all the risks involved inthese endeavours. Insurance gives them thesecurity they need. It gives them peace ofmind, it relieves them of a great deal offinancial hardship and in some cases helps toavoid bankruptcy.

Insurance does not take away the risk. Thehouse may still burn down, or the car may beinvolved in an accident, but it is reassuring toknow that the financial consequences havebeen transferred to others more willing andable to accept them.

Apart from the need for peace of mind,individuals and businesses are required by lawto take out some forms of insurance – forexample, motor insurance and employer’sliability insurance. These will be consideredfurther in chapter 3.

Q. Think of a toy manufacturer. Whatrisks is the business exposed to forwhich it may need insurance?

A. These could include:

• damage to the buildings, machineryand stock due to malicious damage,fire, flood and other causes;

• loss of income whilst the premises arebeing repaired following damage;

• the legal requirement to paycompensation to employees who areinjured at work through the fault of theemployer;

• the legal requirement to paycompensation to customers who areinjured by faulty toys;

• theft of stock or money from thepremises by employees or others.

The idea of insurance is to removeuncertainty by transferring theunknown financial consequencesof a possible loss to someone else.

”“

So far we have only considered the impact ofrisk upon private individuals. However,insurance is available not only to privateindividuals but also to commercial andindustrial concerns.

?

Some technical termsInsurance is a complex business. Explainedbelow are some of the technical terms used byinsurers which will help your understanding ofthe chapters which follow.

Policy. A document issued by an insurer asevidence that a contract of insurance exists.Often used to refer to the contract itself.

Premium. The amount you pay to insurerswhen you take out an insurance policy, inexchange for the cover provided. It may bepaid in a lump sum or more often in regularmonthly instalments.

Insurer. The person, persons or companythat “insure”, that is, provide the cover.This is usually an insurance company (see page 14).

Insured. The person, persons or company that are insured by the insurer(see page 13).

Policyholder. The person, persons orcompany taking out cover. This is usuallythe same as the insured.

Claim. A request by the insured for paymentunder the terms of a policy, because aninsured loss has occurred, for example,a fire.

Peril. An event, such as storm or flood,which can cause loss or damage.

Risk. We have already said this word refersto the possibility that something willhappen which we do not want to happen. Ininsurance this word is also used with othermeanings: the “peril” insured against (forexample, fire, theft), and the person orthing that is being insured (for example,in life assurance, a person; in propertyinsurance, a factory or house.

5

1666 – Great Fire ofLondon demonstrated the need

for fire insurance. The ‘Fire Office’was formed to insure houses and

other buildings against fire.

Key stages in the development of insurance

3000 BC – Babylonians developed a system of loans on maritime

adventures. These are thebeginnings of marine insurance

as we know it today

The concept of insurance is not a new one. Some of the key stages in its development areshown below.

Ancient Rome – Members paid contributions to burial

societies, which paid the funeralcosts when a member died.

1583 – first modern-style life assurance policy issued

in London.

1762 – first life insurer was formed –

Equitable Life.

End of 17th century –practice of marine insurance

is well established.

1861 – Tooley Street fire– a major fire in London

leading to the formation ofthe Commercial UnionAssurance Company.

Industrial Revolution – the move away from agriculture to

an industrial society brought newrisks and created a demand for

new forms of insurance protection.

19th century –continued growth of new forms

of insurance including cover againstpersonal accident, personal injury,

boiler explosion and theft.

6

As industry has developed and becomeincreasingly sophisticated, the need forinsurance has also continued to grow. In somecases, the cover on offer under existingpolicies has been gradually extended.For example, the extension of household andfire insurance policies to include accidentaldamage cover. In other cases insurancefollowed the development of technology.Aviation insurance grew rapidly with thedevelopment of air travel. New technologyrisks such as communication satellites andcomputers are all now insurable. Thisunderlines the point that as risksemerge, there follows a demand forinsurance protection.

Pooling of risksInsurance, then, is the means by which thoseunfortunate enough to be the victim of someloss can gain compensation.

But how can insurers provide thiscompensation – especially when they knowthere are so many fires, accidents, thefts,injuries and other losses each day? The answer,strangely, lies in that very fact. Where there arelots of similar risks, insurers can predict withsome certainty how many losses there will be.They do not know exactly but, based on theirlong experience of dealing with risk and byusing statistical techniques, they have a verygood idea.

In fact, in any one year only a small proportionof those who are insured actually suffer a loss.Think for a moment of the street where youlive. How many fires can you rememberrecently in the houses around you? It is reallynot all that likely that your house will catchfire, that your car will be in an accident, thatyou will be injured at work. Nevertheless, if itdid happen, it could be a disaster for you.

The insurance company is able to offer you theprotection it does by grouping together a largenumber of people who all feel exposed to thesame form of risk. By collecting an amount ofmoney (a premium) from each person in thegroup, it then can accumulate a fund (called apool) – out of which the losses suffered by thefew can be paid.

How risks are pooled

This seems fine but why not just put the moneyin the bank instead of paying it to an insurancecompany, and wait for the day the loss mighthappen? Think about it! If you own a £100,000house, a £15,000 car, a £30m ship, how muchwill you put in the bank? You just do not knowwhen the risk will happen, and it is unlikelyyou could put away enough money for suchan occurrence.

Premiums collectedfrom all those

needing insurance

Claims paid for the few who suffer a loss

Pool

7

The development of insurance

8

Q. Consider the pool for fire insurance.Which of the following would pay ahigher premium to the pool:

• a warehouse used to storefireworks;

• a factory manufacturing concreteblocks?

A. The higher premium would be paid bythe first risk. Clearly the storage offireworks has a much greater potentialto cause a fire.

The premiums paid by all the people whoseek protection gotowards paying for the losses of the fewwho actually suffer.

”

The money paid to an insurance company is avery small amount in relation to the value of ahouse, car or ship. The only reason theinsurance company requires such a relativelylow premium is because they have gatheredpremiums from a large number of people mostof whom will not suffer a loss – at least not inthe same year as you.

The premiums paid by all the people who seekprotection go towards paying for the losses ofthe few who actually suffer. This does notmean that if you did not suffer a loss, you havepaid your money for nothing. You had thesecurity, you had the peace of mind all throughthe year and, if anything had happened, youwould have been financially protected.

Fair premiumsIt is important to point out here that not all thecontributions to this common pool will be thesame. Take the pool which an insurancecompany might operate for motor accidents. Itwould not be fair for someone with a two-doorfamily saloon to pay the same as the owner ofa multi-ton juggernaut. Nor would it bereasonable for a family man with a smallsaloon to pay the same as an 18-year-old, whohas just passed the driving test, with asports car.

Different members of the pool present differenthazards to the pool itself, and there must besome balance between how much a personputs in and how much the pool is likely to haveto pay that person in the event of a claim. Eachperson wishing to join the pool must pay a fairpremium which reflects the risk which theybring to that pool.

?

“

What risks are insurable?

It is important to understand that not all risks are insurable. To benefit from the advantage ofinsurance protection, a risk has to have certain characteristics.

Insurable risks Uninsurable risks

Measurable The possible loss must be measurable in financialterms. For example, damage to buildings,loss of profits.

Not measurableSome risks that we face are not measurablefinancially. This would apply, for example, to thesentimental value attached to a diamond ring whichhas been handed down as a family heirloom. It canonly be insured for its financial value.

Large number of similar risksThere need to be a sufficient number of similar risksfor insurers to accurately predict likely losses andcalculate accurate premiums, as in the case of motorinsurance, household insurance, fire insurance andso on.

One-off risksWhere the risk is a “one off” it is much more difficultfor insurers to calculate a premium to reflect the risk.Take, for example, the chance of a pop star losing hisor her voice. This is not an absolute rule, however,and some insurers will still offer insurance for certainone-off events, such as a satellite launch.

Chance of loss or break even onlyTake for example insuring your house: there may be afire or flood (loss) or there may not (break even).

Chance of gain, loss or break evenTake for example starting up a new business: youcould lose money, break even or make a profit.Where would the incentive be to make it a success ifyou knew that insurers would pay your losses if thebusiness failed?

Fortuitous eventThis means that the chance of loss must be entirelyaccidental as far as the insured is concerned.

Deliberate or inevitable eventsThis rules out, for example, any advantage peoplemight hope to gain from burning down their ownfactory or shop. Wear and tear on property is anotherexample as all property will eventually wear out – it isinevitable.

Not against public interestIn most cases, it is in the interest of society to haveinsurance, but in a few cases this is not so.

Against public interestIt would not be in the public interest, for example, toallow people to insure themselves against having topay a fine for a criminal offence.

Insurable interestThe person taking out insurance must be the one whowill suffer financially should a loss occur. For example,you can insure your camera against loss or damage,as you are the one who will suffer if it is lost ordamaged.

No insurable interestIf you have no financial interest in what is beinginsured you cannot insure it. Clearly it would bewrong if you could insure a car owned by your friend,as you would then make a profit if anythinghappened to it.

Risks that are personal and localisedThink of insuring a factory against flood damage.The damage is caused by a single event (flood) andaffects only the owners of the factory. The same istrue of all risks which are commonly insured.

Risks that occur on a vast scaleThese are catastrophic risks which have the potentialto produce losses which are too large for insurers tobear. They include war and earthquake, and arenormally considered to be the responsibility ofgovernments rather than insurers.

9

The benefits of insuring The existence of insurance brings with it manybenefits. We have already considered thepeace of mind it can provide to both individualsand businesses. There are other benefits, bothto those who are insured and to society as awhole, including:

• Business people will be more inclined torisk their money by starting newbusinesses or expanding existing ones, asmoney does not need to be set aside incase loss or injury. Without insurance manywould consider the risk of, for example, thefactory burning down in a fire, with thepotential to lose everything, too great a riskto bear. This is an extremely importantbenefit which insurance brings – not only tothe individual insuring but to the wholecountry – as stimulating businesses makesfor a healthy economy.

• Insurance can help in reducing losses.Insurance companies have a great deal ofexperience in risks of all kinds, and overmany years they have found ways in whichcertain risks can be reduced. Sometimestheir findings are not just suggestions butare made a condition of being able to takeout insurance.

One way in which insurers try toreduce losses is by employing surveyorswho go out and look at premises whichpeople may want to insure. Thesesurveyors can often suggest ways in whichthe likelihood of some risk occurring maybe reduced: for example, installing aburglar alarm to reduce the risk of theft.

10

11

One way insurers tryto reduce losses is byemploying surveyors.

”“

• The country benefits from investmentsmade by insurers. Insurers do not useimmediately the money they collect. Theyhold it until one of the members of the poolsuffers a loss. The money they hold isinvested in a wide range of investmentswhich all go towards aiding government,industry, commerce and consequently thewhole country.

A visible symbol of one of the uses towhich insurance funds are directed is thebuilding work being carried out in many ofour cities. Look a little closer at the largesigns surrounding these building sites andnotice how many are being funded byinsurance companies.

• Insurance reduces costs to society.Insurance companies pay out many millionsof pounds every single day of the year incompensation. This means that individualswho are injured, for example in a motoraccident or at work, are less reliant on thestate during the time they cannot work. If itwas not for insurance, this burden, or atleast part of it, would have to be met bysociety at large. That would mean each oneof us would have to contribute much morethan we do now in taxation.

• Insurance increases exports. The UK is heldin high regard as a centre for insurance anda large volume of insurance is purchased inthis country by foreign companies. The UKbenefits from the flow of premiums paid toinsurance companies in this country frompeople and businesses abroad.

The insurance marketis no different to anyother market.

”“

13

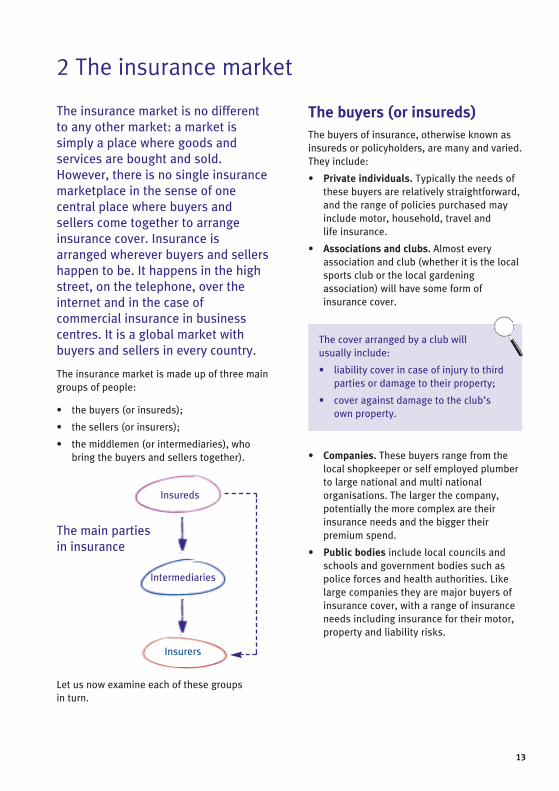

The insurance market is no differentto any other market: a market issimply a place where goods andservices are bought and sold.However, there is no single insurancemarketplace in the sense of onecentral place where buyers andsellers come together to arrangeinsurance cover. Insurance isarranged wherever buyers and sellershappen to be. It happens in the highstreet, on the telephone, over theinternet and in the case ofcommercial insurance in businesscentres. It is a global market withbuyers and sellers in every country.

The insurance market is made up of three maingroups of people:

• the buyers (or insureds);

• the sellers (or insurers);

• the middlemen (or intermediaries), whobring the buyers and sellers together).

Let us now examine each of these groupsin turn.

The buyers (or insureds) The buyers of insurance, otherwise known asinsureds or policyholders, are many and varied.They include:

• Private individuals. Typically the needs ofthese buyers are relatively straightforward,and the range of policies purchased mayinclude motor, household, travel andlife insurance.

• Associations and clubs. Almost everyassociation and club (whether it is the localsports club or the local gardeningassociation) will have some form ofinsurance cover.

• Companies. These buyers range from thelocal shopkeeper or self employed plumberto large national and multi nationalorganisations. The larger the company,potentially the more complex are theirinsurance needs and the bigger theirpremium spend.

• Public bodies include local councils andschools and government bodies such aspolice forces and health authorities. Likelarge companies they are major buyers ofinsurance cover, with a range of insuranceneeds including insurance for their motor,property and liability risks.

2 The insurance market

Insureds

Insurers

Intermediaries

The cover arranged by a club will usually include:

• liability cover in case of injury to thirdparties or damage to their property;

• cover against damage to the club’sown property.

The main parties in insurance

14

In recent years many mutualcompanies have changed status, with theagreement of their policyholders, andbecome proprietary companies withshareholders. This makes it easier forthem to raise new capital to expandthe company.

Some public bodies are exempt fromcompulsory insurance requirements.Police forces, for example, do not have toinsure their motor vehicles.

How do insurance companies make profits?

Income

(premiums + investmentincome)

Profits

Expenditure

(claims + expenses +reserves for claims that

might arise later)– =

The sellers (or insurers) There are several different types of insurersoperating in the insurance marketplace,including:

• insurance companies;

• Lloyd’s;

• reinsurance companies;

• captive insurance companies.

Insurance companiesThe majority of insurance companies areincorporated (or formed) by registration underthe companies acts, and are owned byshareholders. They are sometimes termedproprietary or limited liability companies. Theshareholders have their liability limited to thevalue of their shares, hence the term “limited

liability company”. The profits of thesecompanies belong to the shareholders whoreceive them by way of dividends.

There are also mutual insurance companies,which are owned by the policyholders. Theprofits are shared by the policyholdersthrough lower premiums or bonuses many f the mutual companies specialise in aparticular class of insurance, for example lifeor marine insurance.

Insurance companies which only transact oneclass of business are classified as specialist.Those transacting both general insurance andlife assurance are termed composite.

Lloyd’s of London Lloyd’s itself is not an insurer, but anorganisation which provides a building (theLloyd’s building in London) and the facilitiesfor its underwriting members to do business.Underwriting members were traditionallywealthy individuals who chose to invest theirmoney at Lloyd’s, but now they can be firms. Itis the members who actually carry theinsurance risks. The underwriting membersform themselves into several hundredsyndicates or groups. Each syndicate appointsa managing agency to run the syndicate andemploy underwriters, who assess each risk onbehalf of the members.

Most investors in any business enjoy theprotection of limited liability status, whichlimits their responsibility for debts and otherlosses to the extent of the wealth they haveinvested in the business, in the form of shares.Individual Lloyd’s members have, however,always been personally liable to the full extentof their personal wealth for their share of losseson policies underwritten by their syndicate.

In order to make Lloyd’s available to a widerrange of investor, membership was opened upin 1994 to companies, called corporatemembers, and they now account for the bulk ofthe insurance capacity available. Corporatemembers have limited liability for their share ofthe risks accepted.

Lloyd’s of London has no connection with anybank and is not a shipping company.

At Lloyd’s risks are placed using a slip.This is simply a stiff piece of papershowing the details of the risk to beinsured. The underwriter (an employee ofthe managing agency) will enter on theslip the proportion of the risk he or she isprepared to carry (on behalf of asyndicate) and the terms or price required. The underwriter will then sign it at the foot – hence the term“underwriter”. There has been a gradualmove towards an electronic slip ratherthan traditional paper.

How Lloyd’s works

15

Underwriting member Underwriting member

Syndicate

Managing agency

16

ReinsurersJust as individuals and companies feel the need to transfer risk, so too do insurers. This will happenwhen a risk they are offered is very large or very hazardous, and they feel it would put at risk their poolof money. Insurers decide how much of the risk they can safely insure and then seek cover – calledreinsurance – for the excess amount. A simple example of this is shown below. In reality reinsurancearrangements can be very complex .

The main types of reinsurer are:

• specialist reinsurance companies;

• Lloyd’s syndicates;

• insurance companies that also act as reinsurers.

Captive insurance companiesA development over the last 30 years or so has been the creation of subsidiary companies, by largenational and international companies, to underwrite some of the parent companies’ insurances. Thesesubsidiary companies are known as captive insurance companies. The parent company transfers thewhole of certain selected risks to its captive, which like any other insurance company retains what isfinancially wise, and reinsures the balance.

Captives are set up to provide the parent company with a more cost-effective and tax-efficient way oftransferring risk, instead of buying insurance from a traditional insurer. Many captive companiesoperate from tax-efficient offshore locations such as the Isle of Man, the Channel Islands and Bermuda.

Reinsurer

(provides reinsurance for40% of the risk)

Insurer A

(retains 60% of the risk)

Pays 100%of premium

Pays 40%of premium

Pays 100%of every claim

Pays 40%of every claim

Insured

(100% insured withinsurer A)

A simple reinsurance arrangement

17

The middlemen(or intermediaries)It is possible to buy insurance direct from aninsurer and many private individuals choose todo this. They decide what their insuranceneeds are, they may approach a number ofinsurance companies to obtain premiumfigures and then they decide which company toinsure with. It is also possible for privateindividuals to use the services of a middleman,or intermediary, whose role it is to bringtogether those who want insurance and thosewho sell it.

Commercial or business insurance buyers maybe faced with a more complex spread of risks.They are in need of expert advice to enablethem to assess the risks they have and tomatch their needs to the best seller ofinsurance in the market place. The majority ofcommercial insurance business is thereforehandled by an intermediary of one formor another.

There are a number of different types ofintermediary operating in the insurancemarketplace, including:

• independent intermediaries;

• Lloyd’s brokers;

• appointed representatives;

• introducer appointed representatives.

Independent intermediaries Independent intermediaries are distinguishedby the fact that they are independent of anyinsurance company, and therefore tend to actfor the client in placing their insurances, ratherthan for the insurer in introducing business.For this service, the intermediary may berewarded by a fee paid by the insured or by acommission paid by the insurance company.Independent intermediaries may also callthemselves iinnssuurraannccee bbrrookkeerrss.

It is possible to buyinsurance direct froman insurer and manyprivate individualschoose to do this.

”“

Insurance intermediaries must bedirectly authorised by the FinancialServices Authority or be “exempt” fromregulation. For more on regulation seechapter 6.

Independent intermediaries advisetheir clients on a wide range of insurancematters, including:

• finding the best insurer and policy tomeet their insurance needs;

• claims procedures;

• negotiating renewal;

• mid-term changes;

• risk management;

• recovery of uninsured losses.

Lloyd’s brokers For most types of business, only Lloyd’sinsurance brokers are allowed to placebusiness at Lloyd’s. These brokers must beindependent intermediaries (see above) andregistered with the Council of Lloyd’s. Theymust satisfy the council of their expertise,integrity and financial standing.

Appointed representativesAppointed representatives are appointed by aninsurer or independent intermediary to act ontheir behalf. They operate under a contractwhich specifies their role and responsibilities.They may act on behalf of more thanone company.

Introducer appointed representativesIntroducer appointed representatives areappointed by an authorised insurer orindependent intermediary to act on their behalfin introducing business to them. They are notallowed to provide any advice to customers,and simply act as a marketing channel for aninsurer’s products.

18

The changing nature of theinsurance marketplaceThe insurance marketplace has undergonetremendous changes in the last 15 to 20 years.One of the key developments has been thegrowth of new distribution channels, including:

• Direct insurers. Technologicaldevelopments since the mid-1980s have ledto a dramatic growth in the number ofinsurers actively encouraging people to buyinsurance directly from them rather thanthrough an intermediary. This is particularlyevident in insurance for individuals ratherthan companies, where insurers have usedcall centre technology and the internet tohandle business more efficiently andcost-effectively.

• Bancassurers. Many banks and buildingsocieties have formed subsidiarybusinesses to provide an insurance serviceto their borrowers and depositors. This isoften referred to as “bancassurance”. Thesefirms provide an ever-growing range ofpolicy covers but have particular strengthsin providing personal customers withpolicies such as motor, household andmortgage-related life assurance.

• Supermarkets and high street retailers.A number of major UK retailers, notably thebig supermarket chains, are now majorproviders of insurance as well as otherfinancial services. They have the advantageof being well-regarded brand names as wellas having a huge number of daily contactpoints that are easily accessedby customers.

Appointed representatives include:

• those who have a non-insurance mainoccupation, such as solicitors andmotor garages;

• full-time intermediaries who act onbehalf of just a small number ofinsurers.

Combinedand package

Household

Travel

Commercial package

Commercial combined

19

3 Different types of insurance

In this chapter we will look at the main types of insurance which may be needed by private individualsand businesses. We will concentrate mainly on “general insurance”, that is, non-life insurance, as thatis the focus of this guide.

General insurance can be split into a number of different categories as illustrated below.

General insurance

PropertyFire and special perils

All risks

Theft

Engineering

Glass

Livestock

Money

Marine andaviation

Hull

Cargo

Freight

Liability

PecuniaryBusiness interruption

Fidelity

Legal expenses

Credit

MotorPrivate car

Motor cycle

Commercial vehicle

Motor trade

LiabilityEmployers’ liability

Public liability

Products liability

Professional indemnity

Directors and officers

HealthPersonal accident

Sickness

Medical expenses

Creditor insurance

Another way of categorising general insurance is:

• personal insurances (or “personal lines”) – where the policyholder is a private individual; and

• commercial insurances (or “commercial lines”) – where the policyholder is a firm or someother kind of organisation.

Categories of general insurance

20

Property insurance Property insurance includes a range of coverswhich may be needed by businesses to protecttheir physical property, such as buildings,machinery and stock. Private individuals needproperty insurance too, but this is typicallyprovided in a household policy (see page 26) .

Fire and special perils A basic fire policy covers damage to propertycaused by:

• fire;

• lightning;

• explosion of gas and boilers used fordomestic purposes, such as heatingand cooking.

The basic policy can be extended at extra costto include damage caused by a range of‘special perils’ such as explosion, storm, flood,burst pipes and malicious damage.

All risksUnder a fire and special perils policy, the lossor damage must be a result of a chosen peril,but there are other ways loss on property canbe suffered. An item could be accidentallydropped or knocked, or simply lost or mislaid.

It is now very common for insurers to offerbusinesses an “all risks” policy. This covers theproperty specified against any loss or damagewhich is not specifically excluded.

TheftTrade contents are exposed to the risk of theft,and theft policies give this cover, usually oncondition that entry and/or exit to thepremises is gained by forcible and violentmeans. In other words, the thieves must forcethe normal security fittings of the premises togain entry or exit.

While it is most unlikely that a whole buildingwould be stolen, thieves frequently damage

Engineering policies group equipmentunder the following headings:

• boiler and pressure plant;

• engine plant;

• electrical plant;

• lifting equipment;

• miscellaneous plant;

• computers.

buildings, and this risk is included in the cover.

Engineering Most commercial premises have some items ofplant which could suffer damage. Policies areavailable covering:

• explosion;

• breakdown;

• accidental damage to plant.

The cover varies to reflect the type of plant.Where appropriate, such policies cover damageto surrounding property and injuries tothird parties.

An important feature of engineering insuranceis the inspection service provided by insurersand incorporated in the contract. Many items ofplant must be inspected regularly by law, andthe insurers’ surveyors are accepted ascompetent persons to carry out these periodicsafety inspections.

Policies can also be issued for inspectionservices only.

GlassGlass policies normally cover damage to allforms of fixed glass – for example in windows,doors, and signs – on an “all risks” basis. Thecost of temporary boarding up is also includedif necessary.

It is now verycommon for insurersto offer businesses an‘all risks’ policy.

”“

22

Pecuniary insurance “Pecuniary” means relating to money andpecuniary insurance covers businesses againstpurely financial losses rather than physicaldamage to property and so on. Of course, onlyinsurable risks are covered (see page 9).

Business interruption When damage occurs at a factory, for example,the loss is not limited to the destruction of thebuildings and contents, but also affectsbusiness profits due to:

• a reduction in sales;

• some expenses continuing;

• additional expenses incurred during therecovery process.

Business interruption policies are available toinsure these losses. Such policies are issuedcovering the same perils as for fire, ‘all risks’ orengineering policies (as discussed above), andcan be extended to cover damage at otherpeople’s premises, such as those of suppliersor customers.

Legal expensesLegal expenses insurance is a form of coverbought not only by businesses but also byprivate individuals to cover the costs ofseeking legal advice or pursuing or defendingcivil actions. Sometimes these legal costs arealready covered by other policies. For example,if you cause an accident whilst driving in yourcar, your motor policy will cover the cost ofdefending the claim from the person you havehit. Similarly liability insurance (see below)includes cover for a business for the legal costsof defending an action brought by, forexample, an employee injured at work or a

member of the public injured by a product.However, there are many other circumstanceswhere legal advice and representation may beneeded. For example, an individual mightpursue a claim for wrongful dismissal at work;a business might have a dispute with alandlord or tenant. Cover can be provided forthese and many other situations under a legalexpenses policy. Whilst the motor and liabilitypolicies mentioned above provide cover forboth defence costs and any compensationwhich must be paid to the other party, legalexpense policies cover the costs of legal adviceand representation only – not compensation.

Credit Credit is very often offered by businesses totheir customers when selling goods. It enablescustomers to buy goods without having tomake immediate payment. Credit insurancecovers the business against the credit risk –the risk of a customer being unable to makepayment when the time is due.

Fidelity guarantee Fidelity guarantee policies cover a businessagainst losing money or stock due to the fraudor dishonesty of a member of staff.

The word “fidelity” implies the faithfulor loyal performance of a duty.

23

Motor insurance Motor insurance policies are available for private cars, motor cycles andcommercial vehicles.

Motor is one of the compulsory classes ofinsurance. The road traffic acts require thatanyone who uses a motor vehicle on the“public highway” must have:

• unlimited cover for liability for death orbodily injury to a third party (includingpassengers); and

• cover for at least £250,000 for damage tothird party property caused by an accidentinvolving the vehicle.

This type of cover is termed act only. It isusually only used where an insurer feels that adriver’s record is so bad that this is themaximum cover it is prepared to grant.

The lowest level of cover usually bought isthird party only. This covers liability for death,injury or damage to third-party property, asabove, except that the third-party propertydamage limit is £20m and cover is notrestricted to accidents occurring on the publichighway. Cover applies if the accident occurs

off the road or on private land. The policy alsocovers the liability of a passenger to thirdparties and is not restricted, as in “act only”policies, to the liability of the driver or user.

The next level of cover is third party, fire andtheft, which adds loss of or damage to thepolicyholder’s own vehicle caused by fire and theft.

The widest form of cover available is acomprehensive policy. This covers accidentaland malicious damage to the insured’s vehiclein addition to the third party, fire andtheft risks.

Insurers have also developed some policiesspecifically to meet the needs of businesses:

• Fleet policies. These insure a number ofvehicles under one policy. The premium isbased on the claims history on the policyrather than by rating individual vehicles.

• Motor trade policies. These are designed tomeet the insurance needs of the motortrade – those selling, servicing andrepairing vehicles.

Insurers subdivide commercialvehicles into several categories to reflectthe differing risks associated with them:

• goods-carrying vehicles, such as vansand lorries;

• passenger-carrying vehicles, such astaxis and coaches;

• agricultural and forestry vehicles, suchas tractors and combine harvesters;

• special-type vehicles (which can beused as a tool of trade) such as mobilecranes and ambulances.

Comprehensive policies also includeadditional benefits such as:

• cover for personal belongings andclothing, typically up to £100;

• medical expenses cover, typically up to £100;

• personal accident cover for insuredand spouse.

We all have a legal duty to behave in a reasonablemanner towards others.

”“

25

Liability insurance We all have a legal duty to behave in areasonable manner towards others. If we fail todo so and someone else is injured or theirproperty is damaged we will be legally obligedto pay compensation. Such liabilities may arisethrough the careless or negligent acts ofindividuals or businesses, due to defects inproperty or goods supplied by businesses, orunder certain statutes (acts of Parliament)which impose liabilities.

The purpose of liability insurance is to insureagainst such liabilities. The following forms ofcover are common.

Employers’ liabilityEmployers’ liability insurance covers employersfor any sum which they may be legally liableto pay to any employee in respect of injury,disease, illness or death causedduring employment.

Public liabilityPublic liability insurance covers the liability ofthe insured at law to members of the public forinjuries suffered or property damaged arisingout of the business.

Product liabilityProduct liability insurance covers the liability ofthose who sell, supply and/or manufacturegoods which cause injury or damage to othersor their property. This cover is sometimesincorporated into a public liability policy.

Professional indemnityA professional indemnity policy covers aprofessional person or firm against claims forloss due to wrongful advice or failure to carryout professional duties properly.

Personal liabilityPersonal liability cover insures a privateindividual against claims by the public forcareless acts, other than those involving theinsured’s use of a motor vehicle or anybusiness activities. For example, this wouldcover you if you allowed your dog to run on toa road and cause an accident. This cover isusually incorporated into a household policy(see below).

Directors’ and officers’ liabilityThere has been an increasing tendency forcourts to hold directors and officers personallyresponsible for their negligence in operating acompany. Shareholders, creditors, customers,employees and others can now take actionagainst directors as individuals. Directors’ andofficers’ liability insurance will provide coverfor directors’ defence costs as well as theamount of compensation which they may beliable to pay.

Employers’ liability insurance iscompulsory under the Employers’ Liability(Compulsory Insurance) Act 1969.

26

Combined or package policies Combined or package policies bring together anumber of different types of cover into onepolicy document, saving administration forboth insurers and the insured.

Household There are a variety of different householdpackages available, including:

• buildings only policies, covering thestructure of the building together with itsfixtures and fittings;

• contents only policies, covering thecontents of houses and, where the insuredis a tenant, the fixtures and fittings;

• buildings and contents together within onepolicy document;

• combined policies that include not onlybuildings and contents, but also a range ofoptional extensions that can be added tothe basic cover.

The insured might take out any combination ofthe above based on individual needs, whetheras a landlord, a tenant or an owner-occupier.

The perils (events) covered under a householdpolicy will usually automatically include:

• fire, explosion, lightning, earthquake;

• riot, civil commotion, strikes, labour orpolitical disturbances;

• malicious acts or vandalism;

• aircraft or other aerial devices, or anythingdropped from them;

• storm and flood;

• subsidence, ground heave or landslip;

• theft or damage by attempted theft;

• escape of water or oil;

• collision by aircraft, vehicles or animals;

• falling trees or branches;

• falling aerials, satellite dishes and theirfittings and masts.

A buildings policy or section alsoautomatically covers:

• damage to services;

• damage to fixed glass;

• professional fees and debrisremoval costs;

• loss of rent.

A contents policy or section alsoautomatically covers:

• temporary removal;

• contents in the garden;

• household removal;

• damage to mirrors and glassin furniture;

• accidental damage toentertainment equipment.

There is then the option to add accidentaldamage cover. For buildings, this providesprotection against damage to the fabric of thebuilding by accidents such as your putting afoot through a ceiling, or a nail through a waterpipe. A home contents policy extended in thisway would cover, for example, the accidentaldropping of a pot of paint on a livingroom carpet.

In addition there is liability cover (as describedon page 25):

• under a buildings policy or section – for theinsured’s liability as owner of the property;

• under a contents policy or section – for theinsured’s liability as occupier of theproperty, as well as the insured’s personalliability and liability for injury to employeesas an employer of domestic servants (suchas a cleaner or gardener).

27

The optional extensions that are available in acombined policy usually include:

• “all risks”/personal possessions, coveringyour property away from the home;

• money and credit cards;

• pedal cycles;

• frozen foods;

• legal expenses;

• sports equipment.

Some insurers offer others such as personalaccident, hospital cash benefits, creditorinsurance, caravans and small craft.

TravelTravel policies cover individuals travellingwithin the UK or abroad. Policies are alsoavailable to cover business travel.

The typical sections of a travel policy include:

• personal accident;

• medical expenses;

• loss of deposits;

• baggage personal effects and money;

• personal liability;

• delayed baggage;

• travel interruption and travel delay;

• hospital cash benefits.

There may be optional extensions, such as lossof passport and legal expenses.

Commercial packageCommercial package policies are designed toprovide a range of covers to meet all theinsurance needs of particular trades, such asshopkeepers, hoteliers and offices.

The risks covered will always include:

• damage to business contents (often on an “all risks” basis including theft, moneyand glass);

• business interruption;

• employers’ liability;

• public liability;

• product liability.

Other covers are also available, either asautomatic or as optional extensions,depending on the needs of the particular trade.These could include, for example, buildings,goods in transit, freezer contents, fidelityguarantee and legal expenses.

Package policies typically come withpredetermined sums insured or limits ofliability (see page 32) and predeterminedrestrictions in cover at an all-inclusive price.

Commercial combinedA commercial combined policy is similar to acommercial package policy except that theinsured is free to choose which sections andsums insured or limits of liability apply. Suchpolicies are more suited to medium-sized orlarge firms, which have more varied insuranceneeds. Whilst only one policy document isissued, combined policies are really acollection of individually underwritten coversthat are grouped together. Each section ispriced separately, and will contain its ownterms and conditions, in addition to thosewhich apply to the policy as a whole.

Travel policies can be arrangedto cover:

• a specific trip;

• all trips, on an annual basis.

Annual policies have become morepopular with the growing trend to takemore than one holiday a year.

28

Marine and aviation insurance Marine policies cover the property or “interest”insured against perils of the sea such as badweather, stranding, collision, fire and seizure.

There are three main classes of interest:

• the ship, which includes the hull andmachinery of the ship;

• the cargo;

• freight, which is the charter fee or thecharge for transporting goods.

Hull policies are usually issued for a period of12 months and cover certain liabilities inaddition to damage to the ship.

Cargo is often insured on an “all risks” basisand can be covered either:

• for the period of the voyage;

• from warehouse of departure to warehouseof arrival; or

• on an “open cover” basis, which iscontinuously available to a shipper ofgoods on prearranged terms.

Freight is insured by shipowners if it is at theirrisk, and is included in the value of the cargo ifit has been prepaid.

Aviation Comprehensive aviation policies are availableto aircraft owners and fleet operators coveringdamage to the hull on the ground or in the air,and liabilities for cargo and passengers.Passengers and crew can also be insured.

“All risks” cover is available to those sendinggoods by air.

Airport operators require liability policiescovering their liability to both passengersand aircraft owners due to the operation of the airport.

Product liability in respect of productsincorporated into the construction ofaircraft is usually insured by the aviationdepartment of insurers rather than theirliability department owing to theextremely high potential losses.

Marine policies coverthe property or ‘interest’insured against perilsof the sea

”“

29

Health insurance

Personal accident and sickness Under a personal accident and sickness policyindividuals provide for benefits to be payablein the event of death, permanent totaldisablement or loss of eyes or limbs due toan accident.

Weekly benefits can also be provided if theinsured is temporarily incapacitated from workdue to accident (or sickness).

Employers can arrange similar cover on a groupbasis for the benefit of all their workers.

Medical expensesA private medical insurance policy providescover for individuals to provide medicaltreatment outside the NHS when they are ill.

It covers both inpatient and outpatienttreatment, and typically includes:

• hospital charges for items such asaccommodation and food, theatre feesand dressings;

• surgeons’ and anaesthetists’ fees;

• other costs such as private ambulancesand nursing fees.

Creditor insuranceThe majority of the population today has someform of credit whether it is a mortgage, bankloan, credit card or overdraft. This brings withit a financial commitment to make monthlyrepayments. Creditor insurance (also known as“payment protection insurance”) covers theseregular repayments in the event ofunemployment, accident or sickness.

Some policies also provide life cover, whichpays off the outstanding balance in the eventof death.

An annuity is a special kind of contract usuallyprovided by life assurance companies. Withthe simplest kind of annuity you pay a lumpsum to the insurer, who undertakes to makefixed, periodic payments to you for the rest ofyour life.

A pension scheme tends to be an annuity inreverse, again usually provided by lifeassurance companies. Typically, regularpayments are made up to a certain age, say65, producing a lump sum. You then use thislump sum to buy an annuity, thus providingyourself with an income in retirement.Pensions can be arranged by employers aspart of a remuneration package with thecontributions being paid jointly by employerand employee (or sometimes just by theemployer). Individuals can arrange similarcontracts themselves – called “personal” pensions.

Income protection insurance is strictlyspeaking a form of health insurance but iscommonly classed with life assurance becauseit involves a long-term policy. These policiespay an income to the insured if he or she isunable to work due to accident or sickness.

Life insurance is the same as lifeassurance. Traditionally the word“assurance” has been used as the insuredrisk is certain to happen.

Life assuranceA life assurance (or insurance) policy pays aspecified sum on the death of the personassured (or insured) or upon the personassured surviving a given term of years,depending on the kind of policy.

There are three main types of life cover:

• Whole-life assurance policies pay a fixedsum in the event of death irrespective ofwhen that may be.

• Endowment policies pay a fixed sum ondeath or at the end of the policy term(usually a fixed number of years, say 20 or25 years), whichever occurs first.

• Term insurances give short-term cover andonly pay if death occurs within the period ofthe policy; for example 10 years.

31

In common with other contracts,insurance is arranged by one partymaking an offer to enter into acontract with another party, who canaccept or reject that offer. In the caseof insurance the first party is theproposer – either a private individualor a business – and the second partyis usually the insurer.

In this chapter, we will look at the sequence ofevents in arranging cover. We will also considertwo legal principles applying to insurance.

The proposalInsurers need information from the proposer sothey can assess the level of risk and decidewhat premium to charge. To help the proposerprovide this information many insurers find itconvenient to use standard questionnairescalled proposal forms. These are widely usedfor policies for private individuals, shopkeepersor small businesses.

However, many insurers have reduced the useof proposal forms and conduct the process ofoffer and acceptance of new policies mainly bytelephone. In this case the informationgathered is input directly into a computerisedquotation system, and a copy of the computer-generated proposal form (usually called astatement of fact) is sent to the proposer to bechecked for accuracy.

Most recently there has been considerablegrowth in the use of the internet to provide afast, low-cost service for quotations and newpolicies on a 24-hour basis. Here the proposercompletes the computerised on-screen versionof the proposal form.

For medium and larger commercial risksproposal forms are not appropriate as theinformation required is usually more complex.Other methods are used by insurers to gatherinformation, such as surveys and writtenbroker presentations.

You will recall from chapter 2 that “slips” areused to present information to underwriters at Lloyd’s.

Whatever form the proposal or offer takes, itwill give details of:

• the proposer’s name;

• the proposer’s address;

• the address of the property insured(the “risk address”);

• the proposer’s occupation;

• the period of insurance;

• details of the risk to be insured;

• sums insured or limits of liability;

• insurance history;

• claims history;

• details of any other insurances.

4 Arranging cover

32

Most recently there has beenconsiderable growth in the use of theinternet to provide a fast, low-costservice for quotations and new policieson a 24-hour basis.

”“

Q. Think for a moment about motorinsurance. What additional questionsdo you think insurers will ask whichrelate just to this type of insurance?

A. This could include:

• details of drivers;

• previous convictions;

• type of cover required;

• whether the vehicle is garaged,and if so, where.

Some of these terms need explaining:

• Sums insured or limits of liability.This means how much cover isrequired. All property policies containa sum insured chosen by the insured,which is also the maximum amount aninsurer will pay out in the event of aclaim. For a household buildings policyfor example this would be the cost ofrebuilding the property. Instead of asum insured, liability policies contain alimit of liability.

• Insurance history. This question willask if the risk has been insured before,and if so whether any special termshave been applied and whether aninsurer has refused to renew a policy.

• Claims history. Insurers will want toknow details of all losses or claims,typically within the previous five years.

• Details of any other insurances.This question will ask for details of anyother insurances covering the same risk.

In addition, particular information relevant tothe class of insurance will be included.

If a proposal form is used, the proposer willsign it. In answering the questions, any“material” (or relevant) particulars must bedisclosed. This duty of disclosure is called theduty of utmost good faith. It will be discussedin more detail later in this chapter.

?

33

Modern computer technology has given theunderwriter new ways to assess risks,including the ability to:

• Analyse past claims information to moreaccurately predict the characteristics ofpolicyholders most likely to produce claims.Such increased risk can then be reflected inhigher premiums.

• Relate the addresses of new policyholdersto a digital map. This can be used tohighlight locations that are particularlyprone to flooding, for example.

• Share policyholder information betweeninsurers through common databases. TheClaims and Underwriting Exchange (CUE),for example, is a shared database for allpersonal lines policies. It enables insurersto check the accuracy of informationsupplied by proposers with regard to theirprevious claims.

Based on the information supplied, the insurerwill then assess the risk. If the insurer decidesto accept the risk a premium is calculated,often based on the sum insured or limit ofindemnity, and reflecting all features of therisk. It may be necessary to impose specialterms and conditions.

This quotation will be communicated to theproposer directly or through an intermediary.

Q. Can you think of an example of poormoral hazard in relation to employers’liability insurance?

A. One example is failing to provideprotective equipment to staff who carryout hazardous work.

Q. What special terms and conditions doyou think insurers would apply whenasked to insure a high-powered sports car?

A. It would be common to exclude youngdrivers. Also, a higher “excess” may beapplied. We will look at excesses later.

UnderwritingUnderwriting is the process by which insurers:

• assess a proposal;

• decide whether or not to accept it;

• if it is acceptable, decide on the termsand conditions.

The proposal will be looked at from two mainaspects: “moral hazard” and “physical hazard”.

Moral hazard relates to the likelihood of a lossoccurring or becoming more serious because ofpeople’s actions or attitudes. The most obviousexample of moral hazard is dishonesty on thepart of the insured, such as submittingfraudulent claims. Carelessness is a morecommon example. The social climate may have a bearing on possible claims, for example where there is widespread vandalismand rioting.

Physical hazard relates to the physicalcharacteristics of the risk. For propertyinsurance this would include the construction ofthe building and the nature of the tradeprocesses. For motor insurance this wouldinclude the make and model of the vehicle.

Q. Can you think of an example of goodphysical hazard in relation totheft insurance?

A. This could be good quality locks onall doors and windows or an approvedalarm system.

?

?

?

34

Confirmation of acceptance Assuming the terms and conditions areacceptable to the proposer, the premium will bepaid and a policy document will be preparedand sent out. Quotation details will normally beentered directly into a database so the policycan be despatched quickly.

Complex commercial insurance policies mayrequire more individual policy drafting.

We have already said that the policy isevidence that a contract of insurance exists.The policy contains full details of the coverprovided. Sometimes, however, there maybe a delay before the policy document can beissued. In this case, if there is a need toprovide evidence that cover is in force,insurers will issue a cover note. This providesbrief details of the key features of thecover provided.

The policy is theevidence of thecontract betweeninsured and insurer.

”“

To comply with the Road Traffic Act1988 certificates of motor insurance mustcontain the following information:

• vehicle registration number;

• name of policyholder;

• commencement and expiry date;

• persons entitled to drive;

• limitations as to use;

• confirmation that cover complies withUK statutory requirements.

Cover notes must contain at least thisinformation, and usually include more.

Cover notes are particularly common in relationto motor insurance, where it is compulsory tohave proof that insurance exists as required bythe road traffic acts. Cover notes are usuallyissued for a period of 30 days. At the end ofthis period a continuation cover note is issuedif the permanent certificate of insurance hasstill not been prepared.

The information contained in a policyschedule usually includes:

• the insured’s name and address;

• the period of cover;

• first and renewal premiums;

• details of the property orinterests insured;

• the sum insured or limits of liability;

• policy number;

• which sections of the policy apply.

35

The policyThe policy is the evidence of the contractbetween insured and insurer. It will detail thecircumstances in which the cover operates,setting out the perils insured and anyexceptions to them.

There will be conditions relating to:

• alterations to the risk;

• taking reasonable precautions tominimise risk;

• fraud;

• claims procedure;

• special undertakings (or warranties)imposed on the insured;

• claims disputes.

For most risks the cover is detailed in astandard policy booklet. A schedule is issuedwhich personalises the cover to aparticular insured.

In cases where the description of property andspecial conditions are too many to include inthe single-page schedule, a multi-pagespecification is attached giving such details.

Collective policiesWhere a risk is shared by several insurers, theone with the largest share issues one policy onbehalf of all the others. Each insurer’s share isdetailed. Such sharing of a risk amonginsurers, each with a contractual obligation tothe insured, is termed coinsurance.

Renewal Most policies provide for the contract to berenewed at the end of the year, so there is noneed to issue another policy document eachyear. Instead, a reminder or renewal notice issent to the intermediary or insured. Once theinsurer receives the renewal premium, areceipt is issued stating that the policy willremain in force for another 12 months. If thereare any amendments to cover – such asincreases in sums insured – a new schedule is issued.

Proposal form

Confirmation of acceptance

Underwriting

Renewal notice

Policydocument

Key stages in arranging cover

37

The duty of disclosure applies:

• during all the negotiations leading up to thecompletion of the contract;

• at the time of any alterations tothe contract;

• at the renewal of the contract.

If one party is in breach of the duty, throughmisrepresentation or non-disclosure, theliabilities of the other party can be ‘avoided’(made void or repudiated). If there is any fraud,for example the misrepresentation or non-disclosure was deliberate, the aggrieved partycan additionally sue for damages.

However, the rules issued by the industryregulator the Financial Services Authority (seepage 50) affect the principle of utmost goodfaith. These rules require that where theinsured is a private individual, insurers mustnot repudiate liability on the grounds of:

• misrepresentation unless it was deliberateor negligent;

• non-disclosure, where the insured could notreasonably have been expected to disclosethe information;

• breach of a warranty or condition unless thebreach is connected with the loss

• unless fraud is involved.

Moreover, the principles applied by the FinancialOmbudsman Service in adjudicating on disputedclaims (see page 48) further soften the affects ofthe principle.

The overall objective of both the FSA rules andthe approach adopted by the FinancialOmbudsman Service is to ensure that privateindividuals, in particular, are not penalisedunless there is some conscious intent tomislead insurers.

Examples of material facts include:

• facts which would tend to make therisk of loss more likely or more severe;

• details of previous losses, whetherinsured or not;

• details of special terms imposed byother insurers or proposals declined.

Utmost good faithIn all contracts, each party must observe goodfaith and must not deliberately mislead theother or perform any fraudulent act. However,in the case of insurance a special relationshipexists between the parties and they owe agreater duty to each other, that of “utmostgood faith”.

This means each party must disclose allmaterial facts to the other. A material fact isone which would influence an underwriter indeciding whether to accept a risk or not, and, ifit is accepted, on what terms.

In ordinary contracts, one need only disclosefacts if asked, but in insurance all facts mustbe disclosed whether asked for or not. Thereason for this is that the proposer will knowvarious material facts about the risks to beinsured which the insurer will be “unaware ofunless told”.

The duty is a reciprocal one and applies toinsurers also. They must not lead the insuredinto one type of contract thinking it is anotheror mislead them regarding the benefits.

38

Q. Virtually all policies are contracts ofindemnity. Can you think of any thataren’t?

A. You cannot put a value on someone’slife or limb. Therefore life and personalaccident policies are not subject to theprinciple of indemnity. They are knownas “benefit” policies.

In the past most claims were settled bya cash payment. Insurers now commonlyuse other options in order to:

• discourage fraudulent claims;

• save money by buying in bulk fromrecommended repairers and suppliers.

IndemnityIn chapter 2 we said that for a risk to beinsurable it must be measurable infinancial terms.

The principle of “indemnity” is fundamental toinsurance. Under this principle the insuredmust be put back in the same financial positionafter a loss as he or she would have been if aloss had not occurred. The insured should beneither worse nor better off after a lossthan before.

How indemnity is providedInsurers can choose one of four ways ofproviding indemnity:

• cash – commonly used to settleliability claims;

• repair – commonly used to settle motorclaims, where the insured is encouraged touse one of the insurer’s network ofrecommended repairers;

• replacement – commonly used to replacestolen electrical goods and in relation toglass claims;

• reinstatement – used in relation to largeproperty claims, where insurers undertaketo rebuild or repair a damaged building,for example.

Tom’s carpet was destroyed in a housefire. It would cost £500 to replace it.

The carpet was two years old when itwas destroyed.

To calculate indemnity, insurers mustascertain the expected life span of thecarpet. Let us say this was five years. Thecarpet was therefore 40% worn out whenit was destroyed (two out of five years =2/5 or 40%).

The amount of indemnity would be 60% of£500; that is, £300. In other words, thededuction for wear and tear wouldbe £200.

The original cost of the carpet is immaterial.

The measurement of indemnity In a few cases – motor insurance is the mostcommon example – a second-hand market maybe available so insurers can easily establish thevalue of the insured property in the event of atotal loss. In all other cases, indemnity for totalloss is calculated as:

cost of replacement

less

value of any “wear and tear”.

A deduction is made for wear and tear to allowfor the fact that a new replacement might bebetter than the lost item. In the case of partiallosses, indemnity is the cost of repair less anallowance for wear and tear, as the repaireditem may be worth more than it was before itwas damaged.

?

The term excess is usually used forsmall amounts, for example £25 or £100.Where the amount is larger, for example£1000, £10,000 or even £1m, the termdeductible is generally used.

Example

Bob suffers damage to the roof of hishouse in a storm, which costs £600 torepair. The policy contains an excess of£250. Bob will have to pay £250 towardsthe repair costs, and his insurers will paythe balance of £350.

39

There are also a number of situations wherethe policy wording will limit the amount paid toless than a full indemnity:

• Sum insured/limit of indemnity. If the suminsured is less than the value lost, then thelimit of the insurer’s liability is the suminsured. Where a limit of indemnity iswritten into the policy, that is the insurer’smaximum liability.

• Average. In the event of the sum insuredbeing too low, most property policies are“subject to average”, meaning partiallosses are reduced in proportion to theamount of underinsurance. This will beconsidered further in chapter 5.

• Excess or deductible – an amount that is deducted from each claim and is paid by the insured. Excesses may be voluntary, in return for a premium discount – or compulsory. For example, compulsory excesses apply to young drivers in relation to motor insurance.

Consider again Tom’s carpet which wasdestroyed in a house fire.

If his policy had been arranged on a new-for-old basis no deduction wouldhave been made for wear and tear, andthe full replacement cost of £500 wouldhave been paid.

The effect of value added tax The fact that valued added tax (VAT) is chargedon most goods and services has a bearing onclaims settlements and hence on sums insured.

For private persons and for businesses withexempt VAT status any claims settlement willinclude VAT. For other businesses which areVAT registered, claims settlements and sumsinsured should exclude VAT since the firm willrecover any VAT paid from HM Customsand Excise.

Amendments to the principleof indemnityAs policy wordings have been developed anumber of modifications to the principle ofindemnity have been introduced by insurers:

• Agreed-value policies are used where itwould be difficult to establish the value ofproperty after it has been lost or damaged.Examples include antiques and classic cars.In these cases the value of the propertyinsured is agreed at inception and that isthe value paid in the event of total loss.The principle of indemnity applies forpartial losses.

• New-for-old cover is now the usual way ofarranging household insurance. Noallowance is made for wear and tear, andthe full cost of replacement is paid in theevent of a claim. Sums insured should bebased on the full replacement cost of theitems insured, and a higher premium will becharged. On commercial policies anequivalent form of cover is available,called reinstatement.

The insured must be putback in the same financialposition after a loss as he orshe would have been if aloss had not occurred

“”

One day, the risk you have insuredagainst might occur. Until this point youhave bought an intangible product – apromise that the insurer will pay yourclaim when the time comes. It is onlywhen a claim occurs that the true valueof the product you have bought can bemeasured. All involved in claimshandling – brokers, adjusters andinsurance company staff alike – mustensure that the insured receives thebest attention possible at all times. Theclaim is not an unnecessary burden orintrusion, it is the whole reason whyinsurance and the vast mechanism wecall the insurance market exists. Ifthere was no need to claim, therewould be no need to insure.

How are claims handled? What procedureshave to be followed? Are there any specialprinciples which apply? In this chapter, we willbriefly answer these questions, and others,which are associated with the claims process.

The claims processWhenever the loss occurs, it will be a conditionof most policies that the insurer is informed assoon as reasonably possible. Many commercialpolicies contain specific timescales forreporting claims.

In most cases, this immediate notification is followed up with a claim form – or accidentreport form in the case of motor claims.

This form gives the insured person theopportunity to provide all the details of theloss which the insurer will need in order to dealwith the claim, including:

• when, where and how the loss occurred;

• what injury or damage has been caused,and the likely size of the claim;

• details of any other policies the insuredmay have;

• particulars of anyone who might have beenresponsible for the loss occurring.

Before considering a claim the insurer will firstcheck that there is a valid policy in force at thetime of the loss. If there is, furtherinvestigations are then carried out todetermine how much (if anything) the insurershould pay in settlement, and whether it canrecover this outlay. It is here that the claimspersonnel of the insurer become involved ininvestigating the claim.

5 Handling claims

Notification of claim

Negotiation with claimant(liability claims)

Claim form

Settlement ofclaim

Investigation/processing by

insurer

Loss adjusters’reports

if required

41

Key stages in the claims process

In some cases, claims will be too involved to behandled by the company itself and it willemploy the services of a loss adjuster. The lossadjuster will usually visit the place where theloss has occurred to investigate the claim onthe insurer’s behalf. The adjuster will assist theinsured in the days immediately following theloss, guiding the insured through the workrequired in making a claim and giving all theassistance possible to ensure that the insuredreceives fair treatment.

Once the adjusters have made preliminaryenquiries into the cause and extent of the loss,they usually submit a series of reports to theinsurers. These are followed up later by finalreports with recommendations as to how muchshould be paid by the insurers.

In some cases, where an insured feelsassistance would be helpful in dealing with theloss adjuster, a loss assessor may beemployed to negotiate on his or her behalf.

In losses where the claim can be handled by theinsurance company itself, the documentation isprocessed as quickly as possible to ensure that

the insured does not suffer unnecessarily.Where property is lost or damaged, the insuredis asked to submit proof of the value of lostitems or estimates for repair or replacement. Insome cases, such as jewellery or works of art,an actual valuation is available to base theclaim upon.

In liability claims, the amount to be paid to theinsured is the subject of negotiation betweenthe insurance company and the claimant – theperson who has suffered injury or has hadproperty damaged. Very often a solicitor actsfor the claimant, and the insurance company,on behalf of the insured, negotiates withthe solicitor.

Negotiating liability claims

Claimant Solicitor Insurancecompany

Insured

Negotiation

42

43

This involves some detailed knowledge both ofthe law and of how compensation amounts areassessed. This work is carried out in theinsurance company by claims inspectors, whogo out and visit the offices of solicitorsconducting the negotiations. In a few claims,the company and the claimant’s solicitor willnot be able to reach an agreement and it willbe necessary to go to court. In such cases, theclaims settlement will be the amount awardedby the judge, subject of course to any policylimits, the main one being the limit of indemnity.