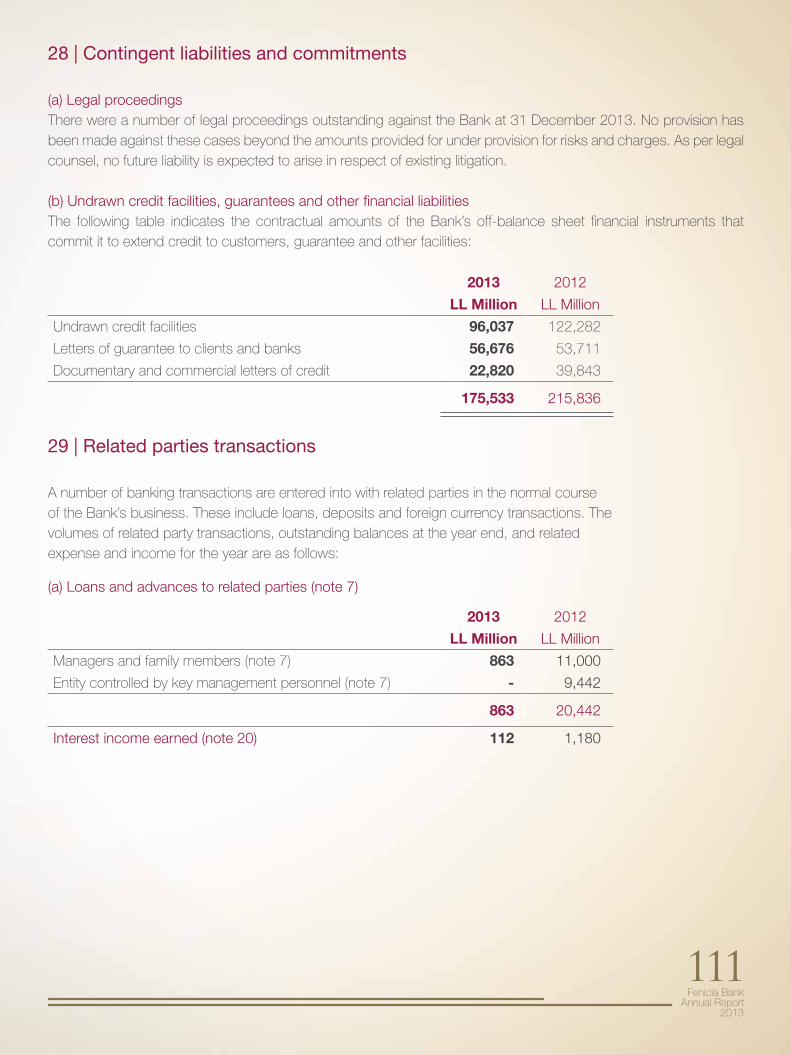

Embed Size (px)

Citation preview

Annual Report2013

Together… wherever

Lifelong Relationship...عالقة ُعُمر...

Fenicia Bank Annual Report

2013

3

FENICIA BANK S.A.L.Annual Report 2013

Fenicia Bank Annual Report2013

4

TABLE OF CONTENTS

Fenicia Bank Annual Report

2013

5

Chairman’s Letter 06

Board of Directors & Management 08

Corporate Governance 14

Highlights, Charts and Performance Review 26

Financial Statements & Notes 38

Correspondent Banks & Addresses 112

Fenicia Bank Annual Report2013

6

INTRODUCTION

Fenicia Bank Annual Report

2013

7

Fifty is the age where we reflect upon our achievements. Where we accept our failures and finally take pride in our successes. Where our soft spots become strengths and our shortcomings, mere stepping stones towards higher grounds. Most of all, we think about the people that have crossed our path, appreciating the way we have grown together and mutually enriched one another.

At Fenicia Bank, we can proudly say after half a century that we build our relationships on the long run, with well-earned trust, constant availability and a flexibility that fits every client’s personal needs. We strive to support you in your achievements and life realizations, guided only by our integrity and high quality standards.

No detail is small enough, no task too difficult when it comes to your satisfaction. Every person that crosses our door is a potential friend, one that we intend to keep close and happy, For generations to come.

Fenicia Bank Annual Report2013

8

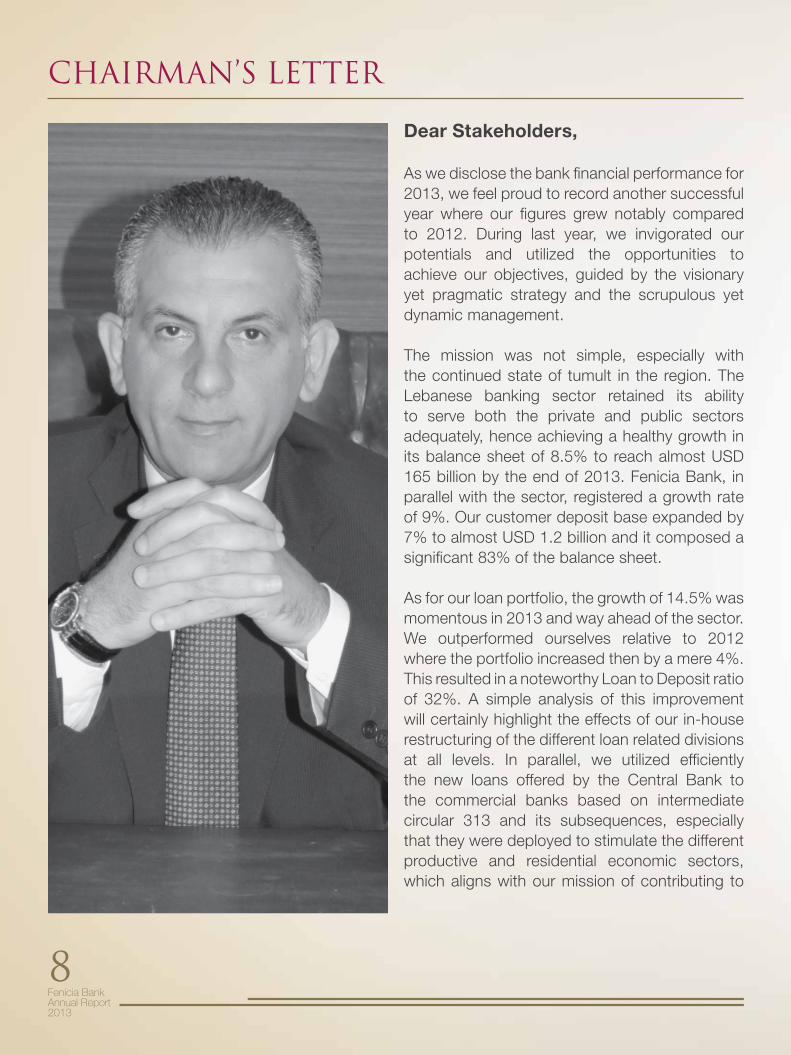

Dear Stakeholders,

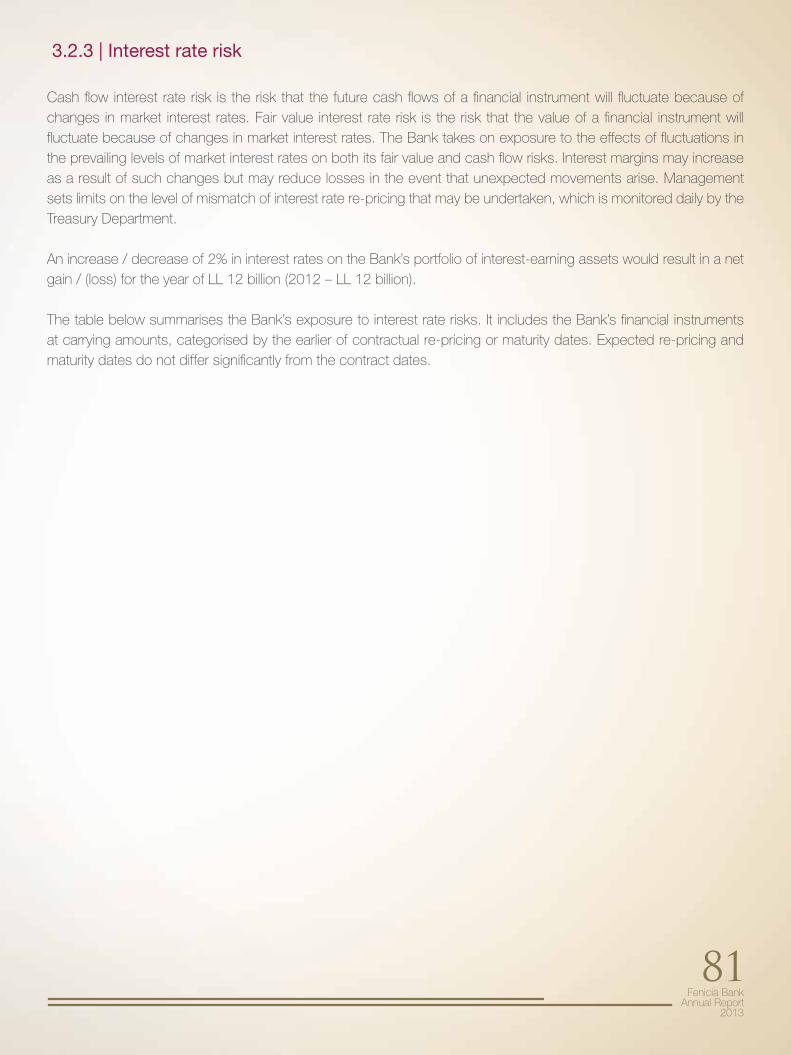

As we disclose the bank financial performance for 2013, we feel proud to record another successful year where our figures grew notably compared to 2012. During last year, we invigorated our potentials and utilized the opportunities to achieve our objectives, guided by the visionary yet pragmatic strategy and the scrupulous yet dynamic management.

The mission was not simple, especially with the continued state of tumult in the region. The Lebanese banking sector retained its ability to serve both the private and public sectors adequately, hence achieving a healthy growth in its balance sheet of 8.5% to reach almost USD 165 billion by the end of 2013. Fenicia Bank, in parallel with the sector, registered a growth rate of 9%. Our customer deposit base expanded by 7% to almost USD 1.2 billion and it composed a significant 83% of the balance sheet.

As for our loan portfolio, the growth of 14.5% was momentous in 2013 and way ahead of the sector. We outperformed ourselves relative to 2012 where the portfolio increased then by a mere 4%. This resulted in a noteworthy Loan to Deposit ratio of 32%. A simple analysis of this improvement will certainly highlight the effects of our in-house restructuring of the different loan related divisions at all levels. In parallel, we utilized efficiently the new loans offered by the Central Bank to the commercial banks based on intermediate circular 313 and its subsequences, especially that they were deployed to stimulate the different productive and residential economic sectors, which aligns with our mission of contributing to

CHAIRMAN’S LETTER

Fenicia Bank Annual Report

2013

9

our economy. The expansion in the loan portfolio was not at the detriment of its quality. The non-performing loans constituted around 6% of total loans with provisions against those NPLs reaching 53% excluding cash collaterals and real estate guarantees. Within the same context and retail wise, we revived a marketing campaign for our products and services and launched a new specialized car-loan program with advantageous conditions.

On the profitability front, our net profits rose by 6% to almost USD 14 million, leading to considerable post-tax ROaE and ROaA of 12.49% and 1.02% respectively. The shareholders’ equity balance boosted by around 10% characterized by its 100% CET1 components. Furthermore, the bank revealed an assuring capital adequacy ratio of 16.06% and a convenient leverage ratio of 7.52%.

2013 was complementary to its precedent in our rigorous efforts to affirm governance practices. We established the Compliance Unit and enriched it with distinguished management from the field, stressing our strategic priority of complying with local regulations and international best practices on one hand, and combating money laundering and crime financing on the other hand. Furthermore, we updated several policies and procedures and smoothly communicated them to our staff, namely “Code of Conduct Policy”, “Whistle blowing Policy” and “Conflict of Interest Policy”. Finally, we restructured our organizational hierarchy to better facilitate the flow of operations and the communication among the various business lines.

Given the dynamic banking industry, we have always considered empowering our human capital with updated knowledge and skills as a strategic objective. Throughout 2013, our staff attended numerous courses and training programs with top notch local and international firms. In addition to the in-house training sessions and workshops which facilitated the exchange of knowledge and expertise among all employees.

Within our business strategies and plans, our corporate social responsibility has always been at the core. In 2013, we were privileged to support several organizations and participate in many events that enhanced social and cultural interaction, educational and academic incentives, and athletic spirit.

As a final note, we are grateful to our shareholders for their support and trust, our employees for their incessant efforts and most importantly our clients for their confidence and loyalty by which we have built a lifelong relationship that we cherish as our utmost wealth.

Abdul Razzak AchourChairman and General Manager

Fenicia Bank Annual Report2013

10

BOARD OF DIRECTORS& MANAGEMENT

Fenicia Bank Annual Report

2013

11

• Lebanese, born in 1938. • Non Executive Board Member at Fenicia Bank s.a.l. and member of the Audit

Committee.• Board Member of Bellevue Company s.a.l. (Real Estate Company). • Driven by ambition and entrepreneurship, he is the owner of a recognizable

company chain in Africa (DRC), (Manufacturing, Electronic Devices, Clothes, and Shoes).

• Pioneer investor in the Lebanese real estate sector through financing the construction of a variety of big projects all across Lebanon.

• Lebanese, born in 1965. • Chairman of the Board of Directors and General Manager of Fenicia Bank s.a.l.

since 1994.• Chairman of several committees namely: Assets and Liabilities (ALCO), Anti Money

Laundry, Credit Rating, and Credit.• Chairman of the Board and General Manager of Bellevue Company s.a.l (Real

Estate Company).• Board member of Trust Construction Company s.a.l. (Construction Company).• Board member in Achour Group (Trade, Manufacturing, Transportation and

Construction).• Member of World Union of Arab Bankers.• Board member of the Lebanese Banking Association for more than 15 years.• Committed to the civil society and to social responsibility, Mr. Achour serves as a

Board Member in the Children Cancer Center – Lebanon (CCCL).• Through his career in the banking and non banking sector, Mr. Achour is recognized

for his strategic vision, leadership skills, and innovative way of doing business.• Holder of Bachelor Degree in Business Administration and Accounting from Lucien

Coormans Institute - Brussels and a degree in International Commerce Studies from ICAD – Paris.

• Lebanese, born in 1958. • Major shareholder at Fenicia Bank s.a.l.• Non Executive Board Member of Fenicia Bank s.a.l.• Board Member at Bellevue Co. s.a.l. (Real Estate Company). Also a Board Member

in Achour Group, managing and co-managing several affiliated companies dealing with different lines of business with international trade exposure.

• Serves as a Board Member in different organizations specifically in sports field. He is currently the president of “Al Sadaka” sporting club (Beirut-Lebanon) and the President of The Handball Federation in Lebanon.

Mr. Abdul Razzak Mahmoud Achour

Mr. AbdallahMahmoud Achour

Mr. YoussefAbbas Merhi

Fenicia Bank Annual Report2013

12

• Lebanese, born in 1940. • Non Executive Board Member at Fenicia Bank s.a.l. and member of the Audit

Committee.• Board Member of Bellevue Company s.a.l. (Real Estate Company). • Being an ambitious businessman and bold entrepreneur, he owns a Farm and Real

Estate agency in the region of Bekaa – Lebanon. Also, Owner of Dada Company in DRC, and owner of a recognizable company chain in Africa (DRC), (Manufacturing, Electronic Devices, Clothes, Shoes).

• Holder of several rewards including the highest reward in DRC: “Chevalier de l’ordre National du Leopard” as an appreciation of his achievements in the commerce and industry sectors.

• Lebanese born in 1938. • Independent Board Member at Fenicia Bank s.a.l.• Chairman of several committees namely: Governance & Remuneration, Audit.• Chairman & General Manager of Intra Investment Co s.a.l.• Member of the Board of Directors of Jammal Trust Bank s.a.l., Byblos Bank DRC

and Casino du Liban.• Member of World Union of Arab Bankers.• Fifty-three years of experience in several banking and financial institutions, where

he served as the general manager or director in the board.• Professor at the Lebanese University, Faculty of Economics and Business

Administration.• Holder of PHD in Business and Economics from Aix-En Provence – France.

• Lebanese, born in 1953. • Assistant General Manager of Fenicia Bank since 2002, executive member of its

Board of Directors since 2012, and member of several committees.• Held leading positions in different local and international banks: Al Ahli Bank of

Qatar- Doha, Mashreq Bank - Doha, Mashreq Bank – Dubai. Also in the non banking sector: Geonex International Incorporated, Florida, USA, and Middle East Banking Company, Beirut, Lebanon.

• Professor in different universities: Lebanese University, Islamic University of Lebanon and Lebanese International University.

• Holder of PHD in Economics from the American University of London, MBA from University of New Hampshire, BA in Accounting & Finance and BA in Marketing & Administration from the Lebanese University, and Diploma in Banking studies and Central Bank Regulations from Saint Joseph University.

Dr. Mohamed AbdulHassan Cheaib

Mr. Aziz Nadra Macaron

dr. Asaad AbdelHassan Koshaish

Fenicia Bank Annual Report

2013

13

• Lebanese, born in 1946. • Assistant General Manager of Fenicia Bank since 2002, executive member of its

Board of Directors since 2012.• Member of several committees namely: Risk and Governance Committies.• Joined Fenicia Bank s.a.l. in July 1992 and held the position of Branches and

Organization Manager.• Held many senior positions in different banks: Jammal Trust Bank s.a.l., Bank of

Beirut s.a.l., Societe Nouvelle de la Banque de Syrie et du Liban. • Holder a Bachelor Degree in Chemistry from the Lebanese University.

• Lebanese, born in 1948. • Independent Board Member of Fenicia Bank s.a.l. since 2012.• Chairman of Risk Committee and member of Governance committee.• He currently holds several senior positions in different Academic institutions

namely: Provost for Faculty Affairs at the Lebanese American University, Professor of strategic Management, Advisor to the President of AACSB (The US-based Business School Accreditation Body) in the Middle East and Africa. Also, member of the Board of trustees of several GCC universities in Bahrain, UAE and Oman.

• Member of the Board of the National Bank of Kuwait (Lebanon).• Holder of PHD in General Management from the University of Southern California,

MBA Degree from the American University of Beirut.• Holder of John Fernandes Strategic leadership award by the academy of Strategic

and Entrepreneurial Leadership in the US for the year 2012.

• Lebanese-French born in 1949. • Independent Board Member of Fenicia Bank s.a.l. since 2012.• Member of the Risk and Audit Committees.• Chairman and General Manager of the Société Financière du Liban (Group of 40

Banks). Also a Board member of Intra Investment Company, Casino Du Liban, Jammal Trust Bank s.a.l., Ameen s.a.l., Société Foncière et Financière du Port de Beyrouth, Société Mixte du Froid, Société Foncière du Liban, and Société Foncière Franco Libanaise.

• Had an extensive financial consulting experience for more than 20 years in Merrill Lynch in Lebanon and France.

• Holder of Bachelor Degree in Business Administration from the American University of Beirut.

Dr. GeorgeKhalil Najjar

Mr. MohsenChafic Naamani

Mr. MichelFouad Ferneini

Fenicia Bank Annual Report2013

14

Mr. Abdul Razzak ACHOURChairman - General Manager

Mr. Mohsen NAAMANIAssistant General Manager

Dr. Asaad KOSHAISHAssistant General Manager

Mr. Muhieddine ARNAOUTLegal Affairs - Senior Manager

Mrs. Hala Achour SAFIEDDINEAdministration & H.R. Manager

Mr. Izzat MSHEIKRisk Manager

Mr. Bilal SBEITYInternal Audit Unit Manager

Dr. Paul MORCOSHead of Compliance Dept.

Shareholders

Achour GroupMaacaron GroupMerhi GroupDr. Mohamad CheaibOthers

Shares in Capital

74.00 %15.00 %10.00 %0.98 %0.02 %

Nationality

LebaneseLebaneseLebaneseLebanese

-

BANK’S OWNERSHIP

MANAGEMENT

Mr. Hachem FADLALLAHInternational Trade Manager

Mrs. Nada KARAKIOperations & Treasury Manager

Mrs Samar HAMDANAccounting Manager

Dr. Antoine KARAMRetail Banking Manager

Mr. Sami BACHIRCorporate & SME Credit Manager

Dr. Samir BARAKATSpecialized Loans Manager

Mr. Houssam RAMADANInformation Technology Manager

Mrs. Rania SAABProduct Development Manager

Fenicia Bank Annual Report

2013

15

ADVISOR TO THE CHAIRMAN

BRANCHES NETWORK

LEGAL ADVISORS

AUDITORS

Me. Charles GHAFARI

Me. Waddah EL-CHAER

Grant Thornton

PricewaterhouseCoopers

Dr. Ibrahim HAMMOUDCredit

Mr. Ali BADRANBranches Network Manager

Mr. Maroun MAKHOULRegional Manager [Bekaa]

Mr. Mohamad HAMADEHRegional Manager [South]

Fenicia Bank Annual Report2013

16

CORPORATE GOVERNANCE

Fenicia Bank Annual Report

2013

17

A legacy worth the whileThe one heritage we are always proud of is a true bond.

At Fenicia Bank, we build on the long run, to keep our clients close, one generation after the other.

Fenicia Bank Annual Report2013

18

CORPORATE GOVERNANCE

I. Corporate Governance Initiatives During 2013

The initiative to reshape the corporate governance structure and upgrade its standards and practices was one of the key milestones achieved by Fenicia Bank S.A.L. in 2013. The Bank embarked on a broad corporate governance restructuring program during the year. The program went in parallel with Fenicia Bank’s ongoing transformation, followed the board level governance revamp that was launched in 2012, and aimed at reinforcing the Bank’s wider commitment to good governance. Following the election of new board members, the reinforcement of board independence, and the establishment of the Governance and Remuneration Committee in 2012, the corporate governance action plan launched and accomplished in its majority in 2013 tackled every pillar of the governance framework. The Bank recognizes that the commitment to governance standards is an ongoing process and will continue to carry out its efforts to nurture a culture of governance across the Bank.

The Corporate Governance Code which sets forth the framework of the governance structure at the Bank and delineates its governance practices was revised during the year to ensure alignment of the Bank’s practices with the latest and leading international standards as well as the regulatory and industry requirements. The revisions tackled the composition of the Board of directors and Board committees and the responsibilities of the major governance organs at the Bank including the Board and its committees, top management, risk management, and internal and external audit, and incorporated the criteria for director independence.

The charter of the Board Risk Committee was reviewed and updated as well to ensure consistency with the revised Corporate Governance Code and alignment with regulatory requirements and international best practices in corporate governance. Within the same framework, the charters of the Audit Committee and the Governance & Remuneration Committee were updated and will be presented to the Board of Directors for discussion and approval.

In order to instill a culture of ethical behavior and compliance with the highest governance and legal principles, the Bank developed a Whistleblowing Policy which was approved by the Board of Directors. The policy encourages proper and prompt dealing with actual or perceived violations of any nature. The Bank also updated its Code of Conduct Policy to ensure consistency of the underlying principles across all codes and policies. These policies were communicated to all staff through correspondence followed by seminars and workshops to promote awareness, highlight their importance, and provide the necessary clarifications.

The Board of Directors approved as well the Conflict of Interest & Related Party Transactions Policy which aims at limiting conflict of interest and related party transactions and promoting transparency, fairness, and disclosure in issues underlying such incidents.

A plan was initiated as well during the year to update the Bank’s Policies and Procedures’ Guide in line with the best industry practices and allowing for efficiency in operations while maintaining proper control and compliance. The new organizational structure at the Bank reflected the establishment of the Compliance Department comprising the Legal Compliance Unit and the Anti-Money Laundry Compliance Unit and having within its mandates the

Fenicia Bank Annual Report

2013

19

responsibility of ensuring the implementation of these policies and monitoring the compliance with the underlying legal, regulatory, and governance principles.

One of the pillars of the governance undertaking tackled the risk management framework at the Bank. A Risk Strategy and a Risk Policy laying down solid foundations for risk management at the Bank were approved by the Board of Directors. The Risk Strategy sets forth the general framework of risk management, the risk management objectives, the risk governance structure, the Bank’s risk tolerance indicators, and the methodologies for identifying, measuring and assessment, monitoring, mitigating, and reporting the various risks.With the aim of ensuring the ongoing development of the Board members and the update of their knowledge and skills in areas essential to the exercise of judgment and decision making, the Bank approved a comprehensive Board Training Program covering topics such as corporate governance, financial statements analysis, risk management, audit, compliance, and strategy. Two sessions aiming at strengthening the Board’s background in the areas of corporate governance and finance were delivered in 2013. The rest of the program is planned to be delivered over the next year.

II. Corporate Governance Plan for the Period 2014 - 2015

Fenicia Bank S.A.L. commits to its ongoing advancement in good governance conduct. Within this framework, the Bank plans to keep on reinforcing the governance principles it had set forth and on upgrading its practices to keep pace of developments in the field. Fenicia Bank’s corporate governance plan for the 2014/2015 period will tackle various governance pillars with primary focus on:• Approving and adopting the updated charters of the Audit Committee and the Governance and Remuneration

Committee by the Board of Directors;• Completing the remaining sessions of the Board Training Program initiated in 2013 and covering the topics of

Corporate Governance, Finance, Risk Management, Audit, Compliance and Strategy;• Accomplishing the Work Plan for updating the Bank’s Policies and Procedures Guide initiated in 2013 and

putting the new Guide into practice; • Ensuring that the recently established Compliance Department is fully functional and has the adequate staff

and other resources, including access to continuous training, in a way that facilitates the proper exercise of its compliance monitoring functions;

• Adopting a Board assessment procedure which would be carried out on an annual basis to evaluate the functioning of the Board and attempt to continuously improve its governance practices;

• Succession planning for the top executive positions at the Bank in order to ensure continuous sustainability in operations;

• Regular review and update of the various corporate governance principles to keep pace of the developments in the regulatory requirements as well as in the industry and international best practices;

• Promoting a culture of good governance across the Bank through the planning of awareness programs and improved communication of governance principles to all employees, among other initiatives.

Fenicia Bank Annual Report2013

20

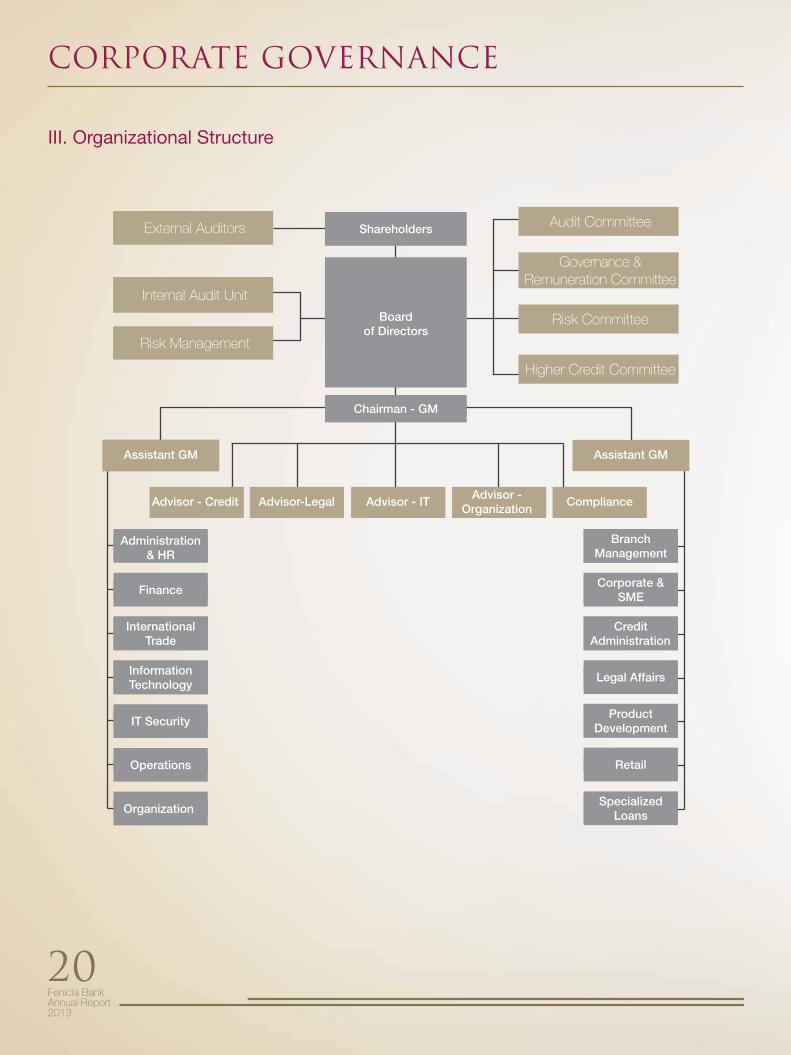

III. Organizational Structure

Higher Credit Committee

Audit Committee

Risk Committee

Governance & Remuneration Committee

Internal Audit Unit

External Auditors

Risk Management

Chairman - GM

Shareholders

Boardof Directors

Assistant GM

Advisor - Credit Advisor - Organization

Advisor-Legal Advisor - IT Compliance

Assistant GM

Branch Management

Product Development

Credit Administration

SpecializedLoans

Corporate & SME

Retail

Legal Affairs

Administration & HR

Information Technology

International Trade

Operations

Finance

IT Security

Organization

CORPORATE GOVERNANCE

Fenicia Bank Annual Report

2013

21

IV. Bank Committees

• BoardCommittees: o Audit Committee o Governance and Remuneration Committee o Risk Committee o Higher Credit Committee

• ManagementCommittees: o Anti-Money Laundry Committee o Assets & Liabilities Committee o Credit Committees (3 sub-committees) o Credit Rating Committee o FATCA Committee o Financial & Estate Placements Committee o Information Security Committee o Procedures & Internal Control Committee o Training Committee o Archiving Committee

V. Fenicia Bank Board Governance

V.1 Board of Directors’ Roles and Responsibilities

Fenicia Bank’s Board of Directors has wide authorities to implement the decisions of the General Assembly and to exercise the non day-to-day activities required to run the business normally. The Board of Directors supervises the setting of the Bank’s strategy and its implementation, oversees the performance of the Bank’s management in alignment with the strategy and objectives, and sets standards for evaluations and remunerations.

The Board ensures proper care of the legitimate interests of the shareholders, depositors, and stakeholders and the building of trust in the Bank and ensures that proper governance procedures are in place and abided by. The Board ensures the proper implementation of the required control procedures and oversees the financial reporting and audit systems and follows up on the work of the internal audit unit and the external auditors.

The Board of Directors sets the general policy of risk management at the Bank and ensures its efficiency and proper implementation. It is responsible for the transparency of its activities’ results and for the Bank’s abidance by the applicable laws and circulars.

Fenicia Bank Annual Report2013

22

CORPORATE GOVERNANCE

V.2 Responsibilities of the Chairman

The Chairman of the Board of Directors represents the Bank to third parties and executes the Board’s decisions and facilitates the daily operations of the Bank, as stated by the bylaws, and under the supervision and control of the Board of Directors. The Chair provides leadership to the Board and is responsible for the Board’s effective overall

functioning.

V.3 Composition of the Board

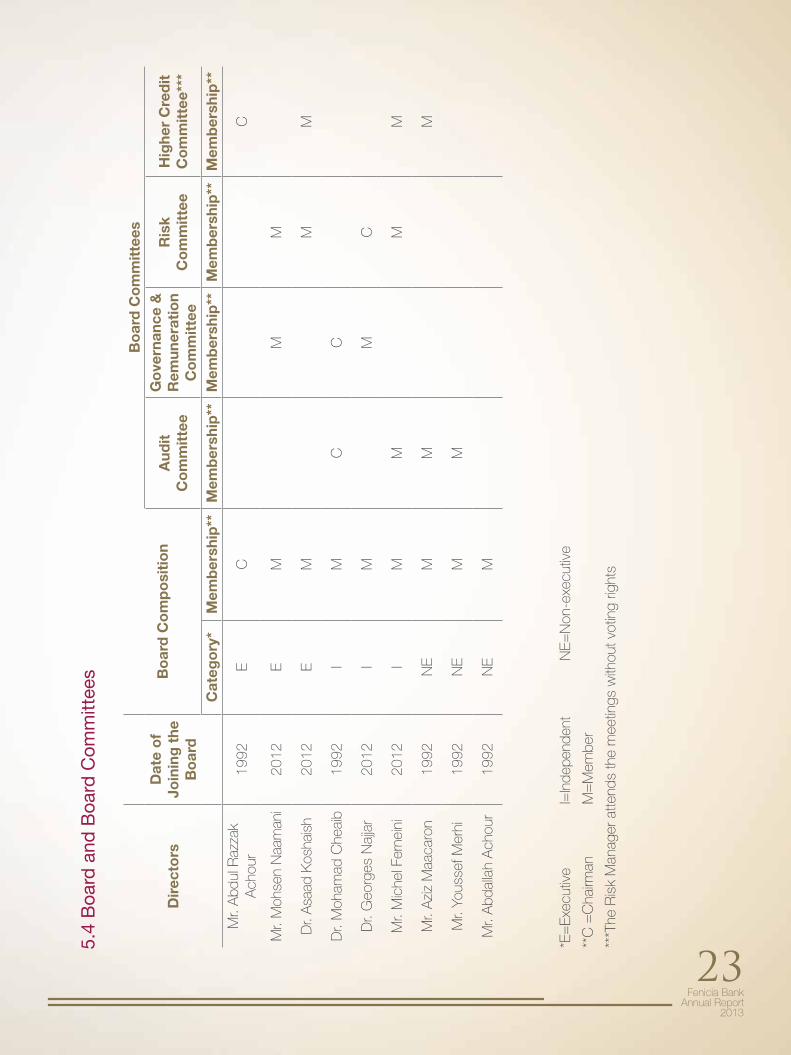

The Bank’s Board of Directors is composed of nine members, of whom three are independent, three are non-executive, and three are executive directors.

We believe that the mix of expertise at the Board level brings a wide range of diversity to the Board and its committees and contributes to a sound and informed judgment and decision making.

Fenicia Bank Annual Report

2013

23

Dir

ecto

rsD

ate

of

Join

ing

the

B

oar

d

Bo

ard

Co

mp

osi

tio

n

Bo

ard

Co

mm

itte

es

Aud

it

Co

mm

itte

e

Go

vern

ance

&

Rem

uner

atio

n C

om

mit

tee

Ris

k C

om

mit

tee

Hig

her

Cre

dit

C

om

mit

tee*

**

Cat

ego

ry*

Mem

ber

ship

**M

emb

ersh

ip**

Mem

ber

ship

**M

emb

ersh

ip**

Mem

ber

ship

**M

r. A

bdul

Raz

zak

Ach

our

1992

EC

C

Mr.

Moh

sen

Naa

man

i20

12E

MM

M

Dr.

Asa

ad K

osha

ish

2012

EM

MM

Dr.

Moh

amad

Che

aib

1992

IM

CC

Dr.

Geo

rges

Naj

jar

2012

IM

MC

Mr.

Mic

hel F

erne

ini

2012

IM

MM

M

Mr.

Azi

z M

aaca

ron

1992

NE

MM

M

Mr.

Yous

sef M

erhi

1992

NE

MM

Mr.

Abd

alla

h A

chou

r19

92N

EM

5.4

Boa

rd a

nd B

oard

Com

mitt

ees

*E=

Exec

utiv

e

I=In

depe

nden

t

NE=

Non

-exe

cutiv

e

**C

=C

hairm

an

M=

Mem

ber

***T

he R

isk

Man

ager

atte

nds

the

mee

tings

with

out v

otin

g rig

hts

Fenicia Bank Annual Report2013

24

CORPORATE GOVERNANCE

V.5 Board Committees

The Board delegates some of its responsibilities to its committees and maintains the duty to follow up on the actions, findings, and recommendations of these committees and taking the actions deemed appropriate.

V.5.1 Audit Committee

V.5.1.1 Membership

The Audit Committee consists of four non-executive directors, two of whom are independent. The Chairman of the Committee is considered by the Board to be independent.The Board has determined that the Committee Chair, Dr. Mohamad Cheaib, possesses relevant financial and audit

experience required for the Audit Committee to fulfill its tasks.

V.5.1.2 Roles and Responsibilities

The main mission of the Audit Committee is to assist the board in fulfilling its supervisory role and responsibilities mainly related to:• The independence and qualifications of the External Auditors and the Internal Audit Unit.• Oversight of the financial reporting process and accounting policies, control of financial statements’ soundness,

and review of the disclosure standards adopted by the Bank.• The adequacy and effectiveness of the audit systems and the internal control policies and procedures.• The follow up on any observations, violations, or recommendations highlighted by the External Auditors, supervisory

authorities, the Internal Audit Unit, or the Compliance Department and follow-up on the implementation of the remedial measures.

• The assurance of proper oversight over the compliance systems and the procedures to address any reported non-compliance.

• The abidance by the Central Bank circulars and the Banking Control Commission circulars and reports and all other applicable regulations.

V.5.2 Governance and Remuneration Committee

V.5.2.1 Membership

The Governance and Remuneration Committee consists of two independent members and one executive member. The Chairman of the Committee is considered by the Board to be independent.

The Board has determined that the Committee Chair, Dr. Mohamad Cheaib, possesses the experience required for the Governance and Remuneration Committee to fulfill its tasks.

Fenicia Bank Annual Report

2013

25

V.5.2.2 Roles and Responsibilities

The main roles of the Governance and Remuneration Committee are as follows:• Assistance in setting the various corporate governance policies at the Bank and follow-up on their implementation.• Clarification of the roles and responsibilities of the Board of Directors and its committees and assurance of their

proper exercise.• Verifying that the Bank is operating within the frame of the corporate governance principles.• Regular review and update of the corporate governance code and principles in compliance with the guidelines

issued by the Basel Committee and the supervisory authorities and in line with international best practices.

V.5.3 Risk Committee

V.5.3.1 Membership

The Board Risk Committee consists of two independent members and two executive members. The Chairman of the Committee is considered by the Board to be independent.The Board has determined that the Committee’s Chair, Dr. George Khalil Najjar, possesses the experience required for the Board Risk Committee to fulfill its tasks.

V.5.3.2 Roles and Responsibilities

The main roles of the Risk Committee are as follows:

• Assisting the Board in setting the risk strategy and policies and in determining, measuring, monitoring, and managing all the risks that the Bank is exposed to.

• Advising the Board on the Bank’s overall current and future risk tolerance. • Verifying that the Bank operations and goals stay within its risk appetite.• Supervising the sound adoption of the risk management principles in abidance by the regulations of the Central

Bank, the Banking Control Commission, and the Basel Committee.• Ensuring the independence and competence of the risk management unit and overseeing its activities. • Verifying that the risk management implementation is compliant with the Bank’s risk strategy.

V.5.4 Higher Credit Committee

V.5.4.1 Membership

The Board Higher Credit Committee consists of two executive, one independent and one non-executive member. The Chairman of the Committee is the Chairman of the Bank.The Board has determined that the Committee’s Chair, Mr. Abdul Razzak Achour, possesses the experience required for the Board Higher Credit Committee to fulfill its tasks.The Risk Manager attends the meetings of the Higher Credit Committee for risk assessment and consultations but

does not have a voting right.

Fenicia Bank Annual Report2013

26

CORPORATE GOVERNANCE

V.5.4.2 Roles and Responsibilities

The main role of the Higher Credit Committee is to examine the credit files that are presented to it based on the criteria set by the Board of Directors. The committee provides opinion on all direct and indirect credit files whose value exceeds USD five millions.

VI. External Auditors

The External Auditors of Fenicia Bank S.A.L. are Grant Thornton and PricewaterhouseCoopers. The External Auditors were appointed by Board of Directors upon a recommendation by the Audit Committee. The External Auditors are independent from the Bank and its directors. The Audit Committee is responsible for ensuring that the External Auditors remain independent.

VII. Conflict of Interest and Related Party Transactions

The Bank has developed a Conflict of Interest Policy that promotes transparency, fairness and disclosure in issues underlying a conflict of interest or related party transactions. The Policy delineates the procedures for avoiding conflicts of interest to the extent possible with the appropriate disclosure mechanisms, and for identifying and dealing

with actual, potential, or perceived conflicts of interest, and disclosing them where un-prevented.

VIII. Professional Conduct Rules

Fenicia Bank S.A.L. ensures that the Bank at all employee levels abides by the highest standards of legal and ethical conduct. The Bank has developed a Code of Conduct and established mechanisms for monitoring compliance by it and all applicable laws and regulations. It has developed procedures for employees to confidentially report any violations and for the Bank to act upon and resolve the faced issues. Fenicia Bank S.A.L. is strongly committed to the following values that frame the scheme of its activities within and outside the work environment:

Fast Service (We satisfy customer needs at the time they need the service)

Efficiency (We execute operations within a small margin of error)

Neutrality (We show no favors and engage in no discriminatory behavior)

Integrity (We act ethically and honestly towards our organization and stakeholders)

Consistency (We maintain uniformity across our products and services to ensure customer satisfaction)

Innovation (We propose new ideas and/or ways of doing things)

Accountability (We hold the responsibility for and consequences of our actions)

Fenicia Bank Annual Report

2013

27

Fenicia Bank Annual Report2013

28

HIGHLIGHTS, CHARTS & PERFORMANCE REVIEW

Fenicia Bank Annual Report

2013

29

The shop around the cornerThat old grocery shop Yasmeen inherited from her stepfather

could not be more exotic to her. But with the support of Fenicia Bank, she can already imagine the gourmet deli shop it will soon turn into.

Fenicia Bank Annual Report2013

30

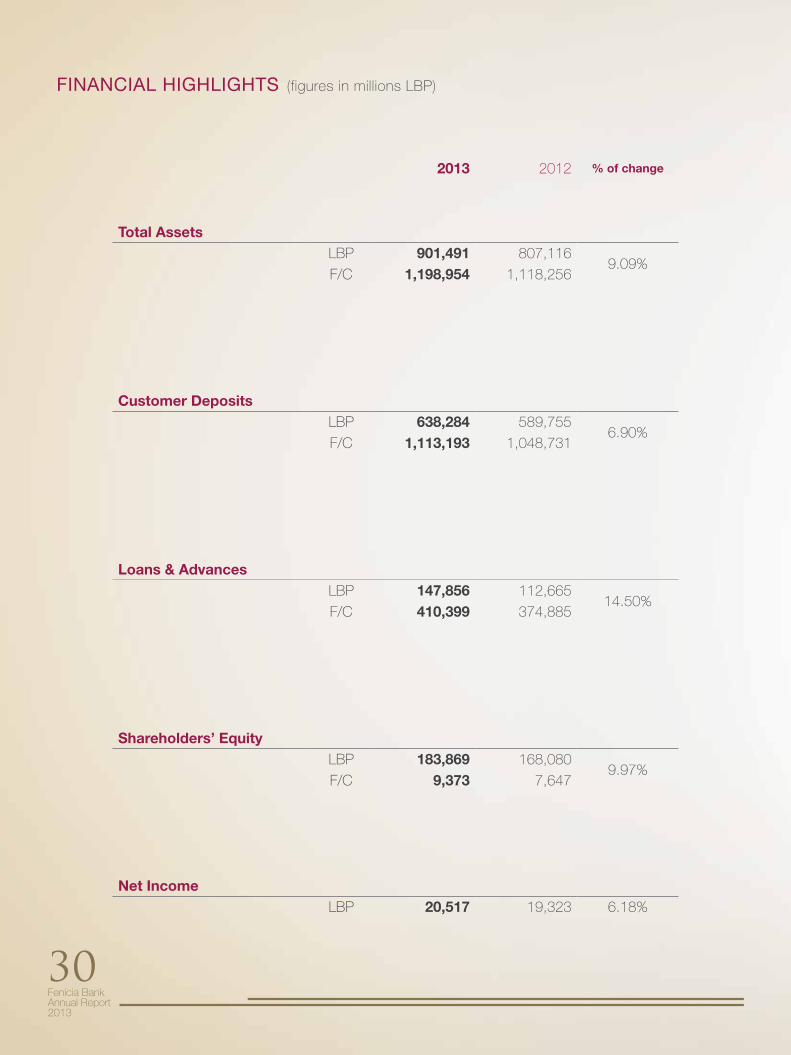

FINANCIAL HIGHLIGHTS (figures in millions LBP)

2013 2012 % of change

Total AssetsLBP 901,491 807,116

9.09%F/C 1,198,954 1,118,256

Customer DepositsLBP 638,284 589,755

6.90%F/C 1,113,193 1,048,731

Loans & AdvancesLBP 147,856 112,665

14.50%F/C 410,399 374,885

Shareholders’ EquityLBP 183,869 168,080

9.97%F/C 9,373 7,647

Net IncomeLBP 20,517 19,323 6.18%

Fenicia Bank Annual Report

2013

31

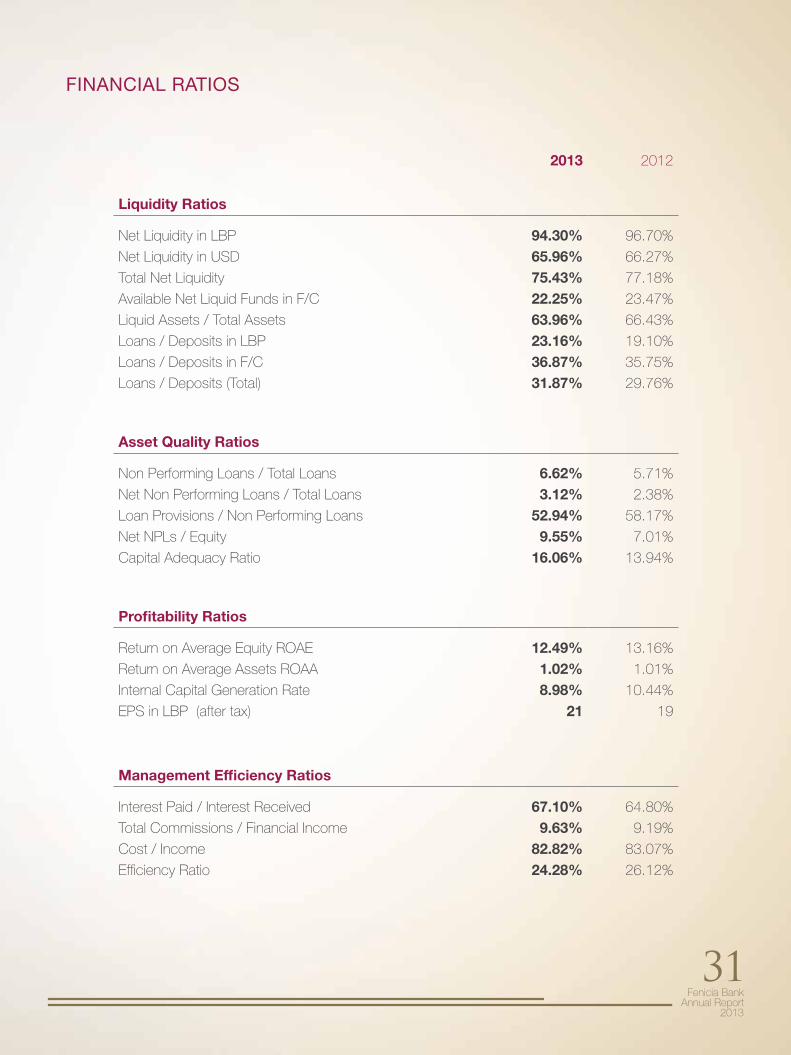

FINANCIAL RATIOS

2013 2012

Liquidity Ratios

Net Liquidity in LBP 94.30% 96.70%

Net Liquidity in USD 65.96% 66.27%

Total Net Liquidity 75.43% 77.18%

Available Net Liquid Funds in F/C 22.25% 23.47%

Liquid Assets / Total Assets 63.96% 66.43%

Loans / Deposits in LBP 23.16% 19.10%

Loans / Deposits in F/C 36.87% 35.75%

Loans / Deposits (Total) 31.87% 29.76%

Asset Quality Ratios

Non Performing Loans / Total Loans 6.62% 5.71%

Net Non Performing Loans / Total Loans 3.12% 2.38%

Loan Provisions / Non Performing Loans 52.94% 58.17%

Net NPLs / Equity 9.55% 7.01%

Capital Adequacy Ratio 16.06% 13.94%

Profitability Ratios

Return on Average Equity ROAE 12.49% 13.16%

Return on Average Assets ROAA 1.02% 1.01%

Internal Capital Generation Rate 8.98% 10.44%

EPS in LBP (after tax) 21 19

Management Efficiency Ratios

Interest Paid / Interest Received 67.10% 64.80%

Total Commissions / Financial Income 9.63% 9.19%

Cost / Income 82.82% 83.07%

Efficiency Ratio 24.28% 26.12%

Fenicia Bank Annual Report2013

32

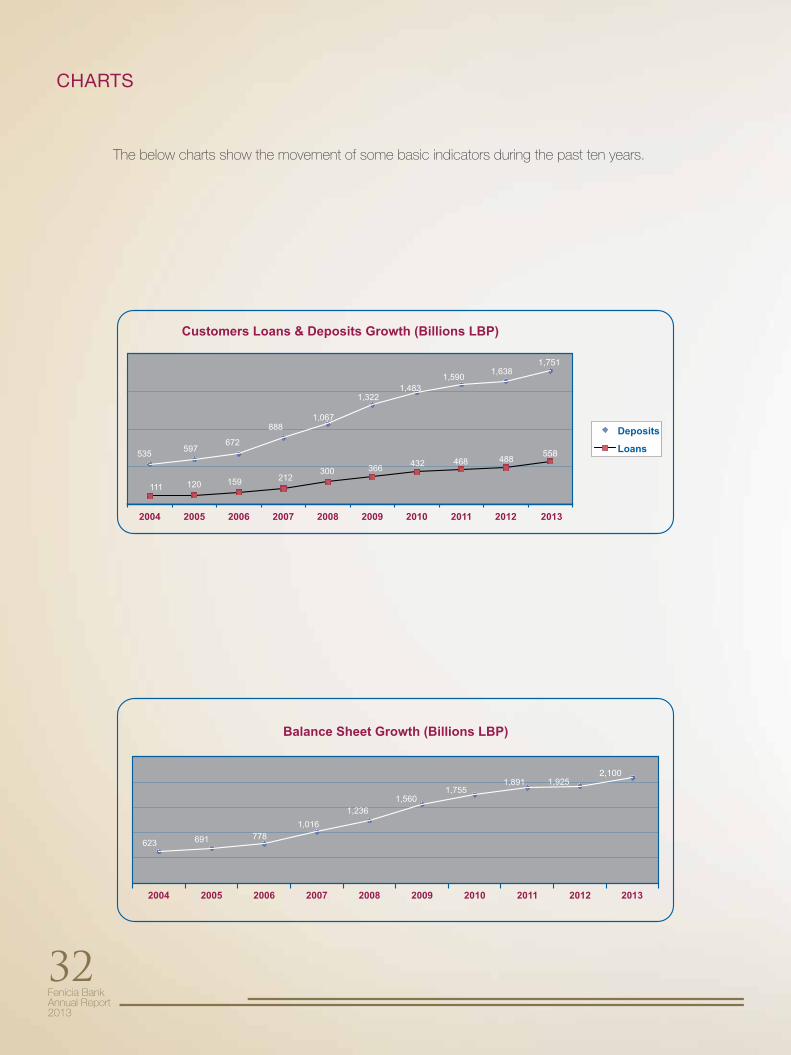

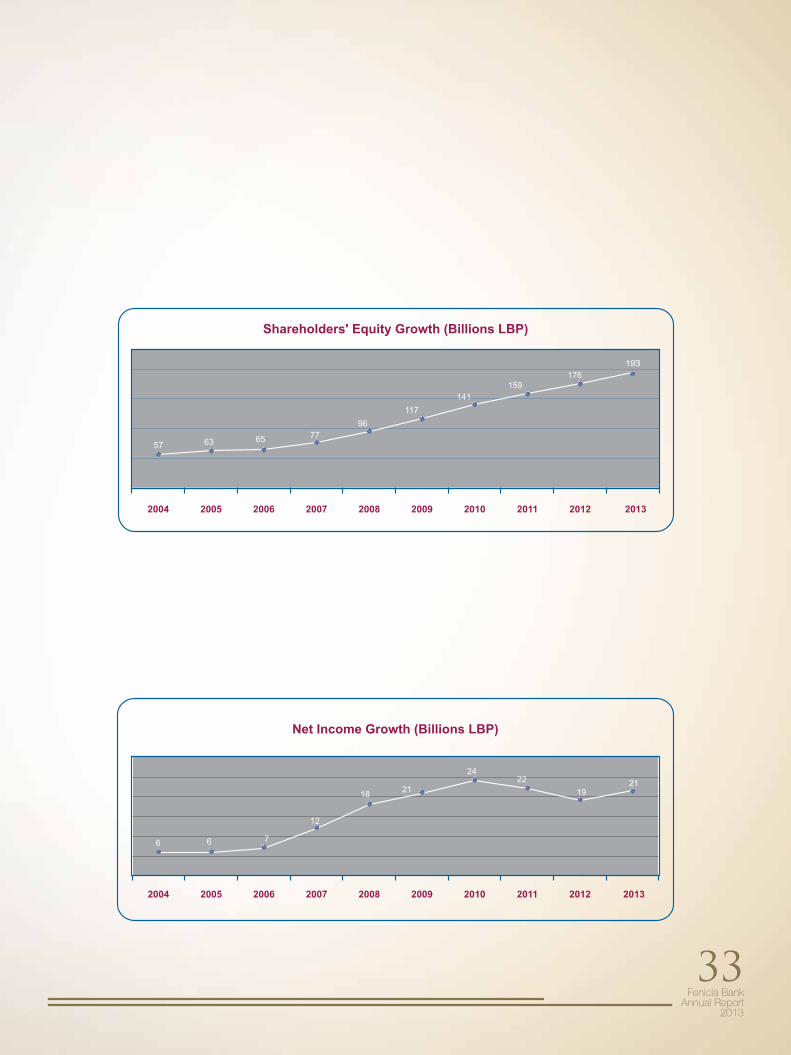

CHARTS

The below charts show the movement of some basic indicators during the past ten years.

558

1,751

2,100

Fenicia Bank Annual Report

2013

33

193

21

Fenicia Bank Annual Report2013

34

Deposits from Central Bank

Deposits from banks

Deposits from customers

Shareholders’ equity

Other liabilities

2012

85%

9%

1%3%

2%

2013

83%

9%

1%4% 3%

FINANCIAL PERFORMANCE REVIEW OF 2013

1- Balance Sheet Analysis

The growth in the balance sheet at end of 2013 exceeded 9%.The following pie charts show the breakdown of the bank major uses and sources of funds in 2013 and 2012:

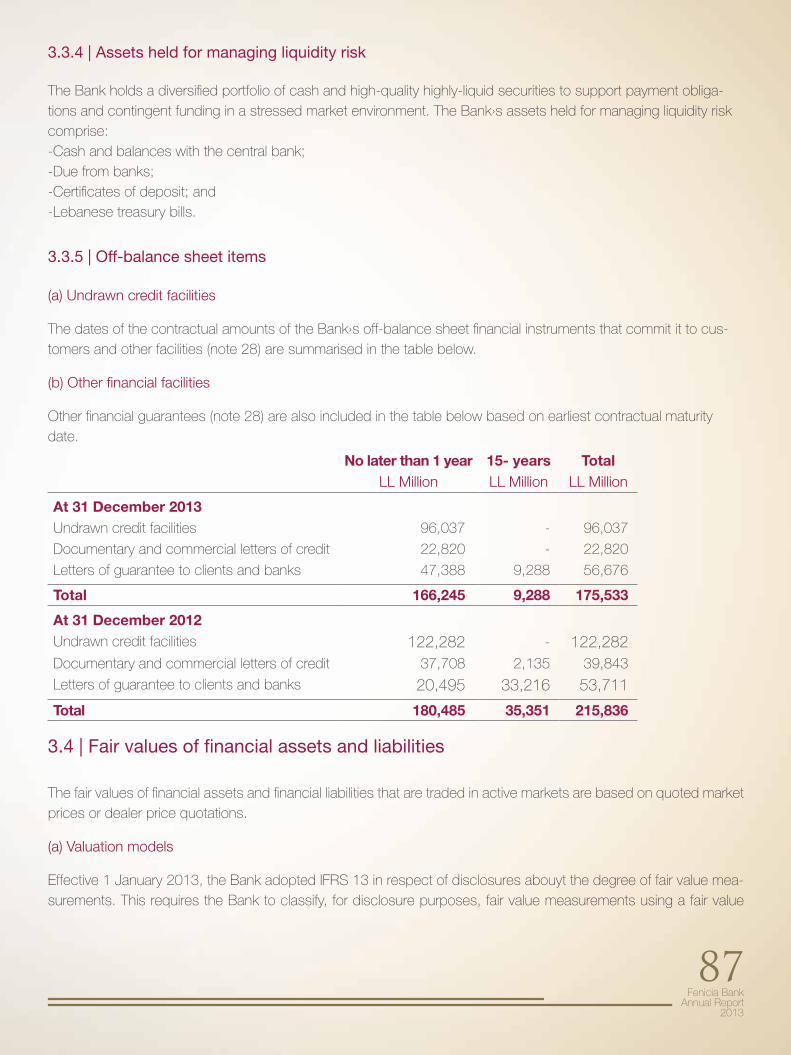

The loans and advances to banks portfolio constitutes 9% of the bank’s uses of funds and it mainly represents the bank term placements and accounts for regular banking operations. Those placements are characterized by: * 55% with investment grade banks* 86% with non-resident banks

Cash and balances with Central Bank

Loans and advances to banks

Loans and advances to customers

Investment securities

Other assets

2012

27%

10%

13%3%

47%2013

29%

9%

14%2%

46%

Uses of Funds [2012 - 2013]

Sources of Funds [2012 - 2013]

Fenicia Bank Annual Report

2013

35

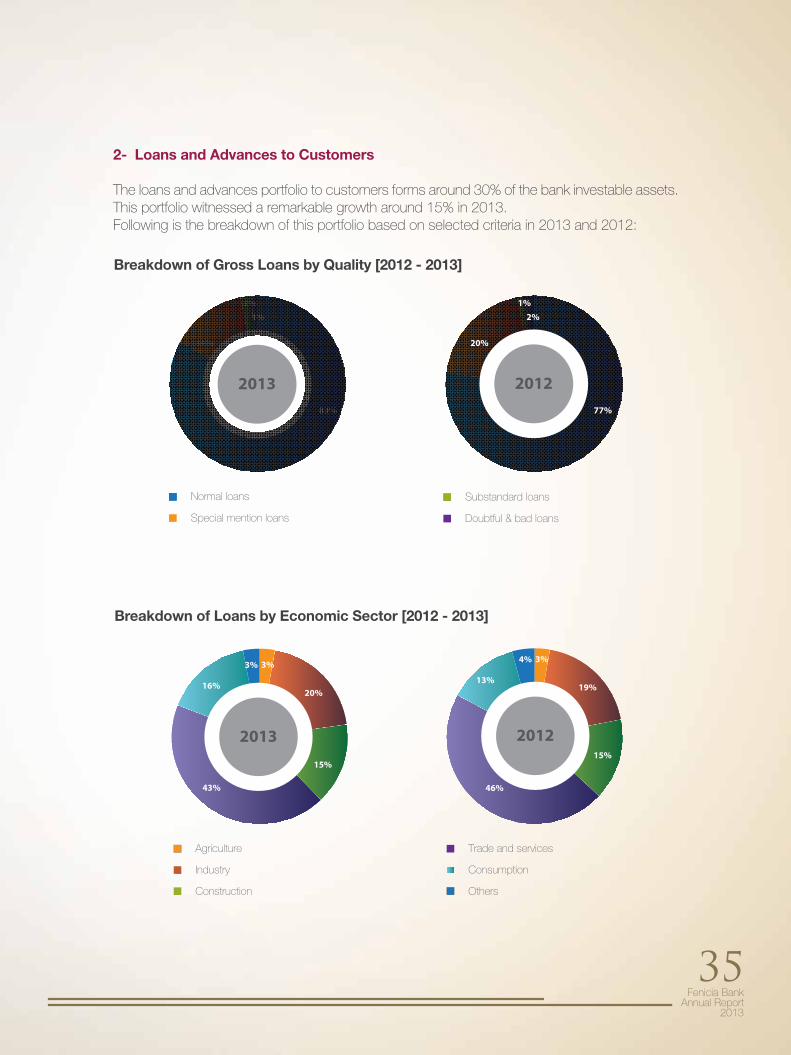

Breakdown of Gross Loans by Quality [2012 - 2013]

2- Loans and Advances to Customers

The loans and advances portfolio to customers forms around 30% of the bank investable assets. This portfolio witnessed a remarkable growth around 15% in 2013.Following is the breakdown of this portfolio based on selected criteria in 2013 and 2012:

201277%

2%1%

20%

Normal loans

Special mention loans

Substandard loans

Doubtful & bad loans

201383%

1%2%

14%

Agriculture

Industry

Construction

Trade and services

Consumption

Others

201315%

20%

3%3%

16%

43%

2012

19%

15%

3%4%

13%

46%

Breakdown of Loans by Economic Sector [2012 - 2013]

Fenicia Bank Annual Report2013

36

FINANCIAL PERFORMANCE REVIEW OF 2013

Breakdown of Loans by Geographical Sector [2012 - 2013]

Lebanon

African Countries

European Countries

Arab Countries

Other Countries

2012

75%

23%1%

1%0%

2013

66%

29%

1% 1%3%

Breakdown of Loans by Type [2012 - 2013]

63%

11%

4%

22% 2012

Corporate

Small & Medium Size Enterprises

Retail

Housing

201363%

22%

3%

12%

Fenicia Bank Annual Report

2013

37

3- Deposits from Customers

Customer deposits constituted the major part of the bank’s sources of funds at a high 83%.The following pie charts show the breakdown of those deposits in 2013 and 2012:

Customer Deposits [2012 - 2013]

Term Saving Accounts

Demand Saving Accounts

Pledged deposits against credit facilities

Margins against L/Cs and L/Gs

Current and checking accounts

Debtors accidentally creditors accounts

term deposits

Related parties

2012

58%

3%

14%

14%

1%

7%

1%

2%

2013

1%

1%

1%

3%

13%

14%

60%

7%

Fenicia Bank Annual Report2013

38

FINANCIAL PERFORMANCE REVIEW OF 2013

Total Expenses [2012 - 2013]

Interest expenses

Fees and Commissions

Loan impairment losses

Personnel expenses

General & administrative expenses

Income tax expenses

2012

68%

4%10%

14%

3%1%

201370%1%

1%

14%

10%4%

4- Net Income

The financial results of 2013 recorded USD 14 millions as net profits. The breakdown of income and expenses was as follows:

Total Income [2012 - 2013]

Interest Income

Fees and Commissions

F/X Trading gains

Loan impairment releases

Other income

2012

88%

9%

1%1%1%

2013

87%

10%1%

2%

Fenicia Bank Annual Report

2013

39

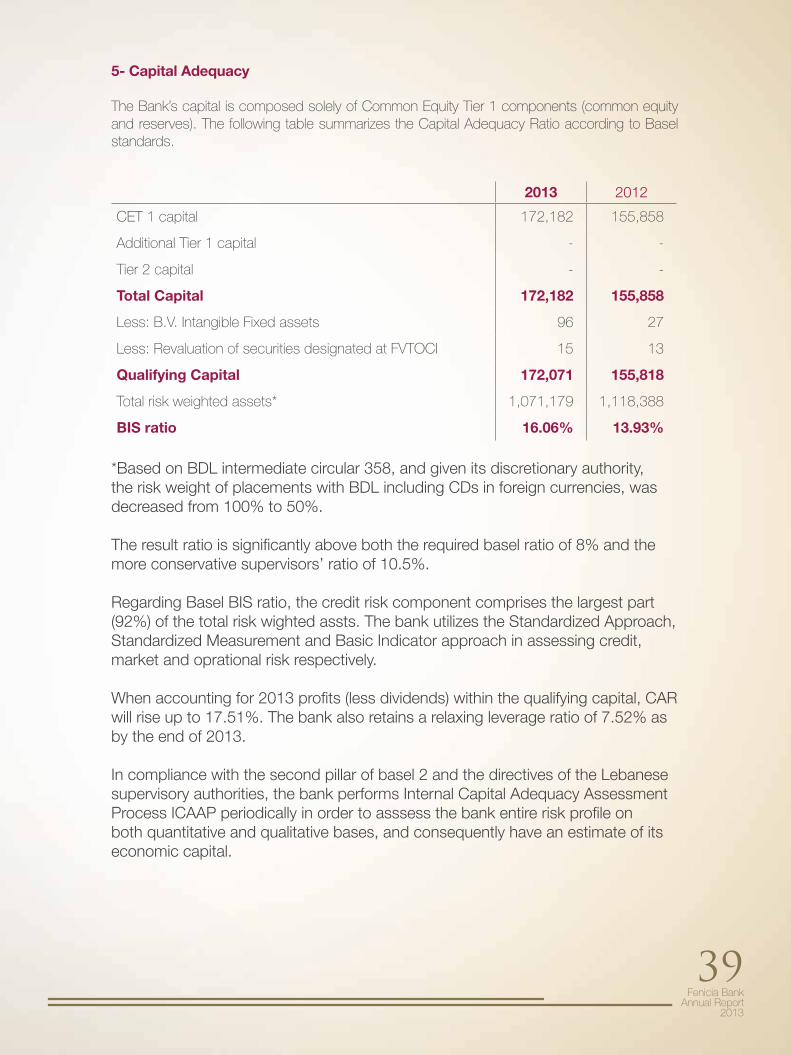

5- Capital Adequacy

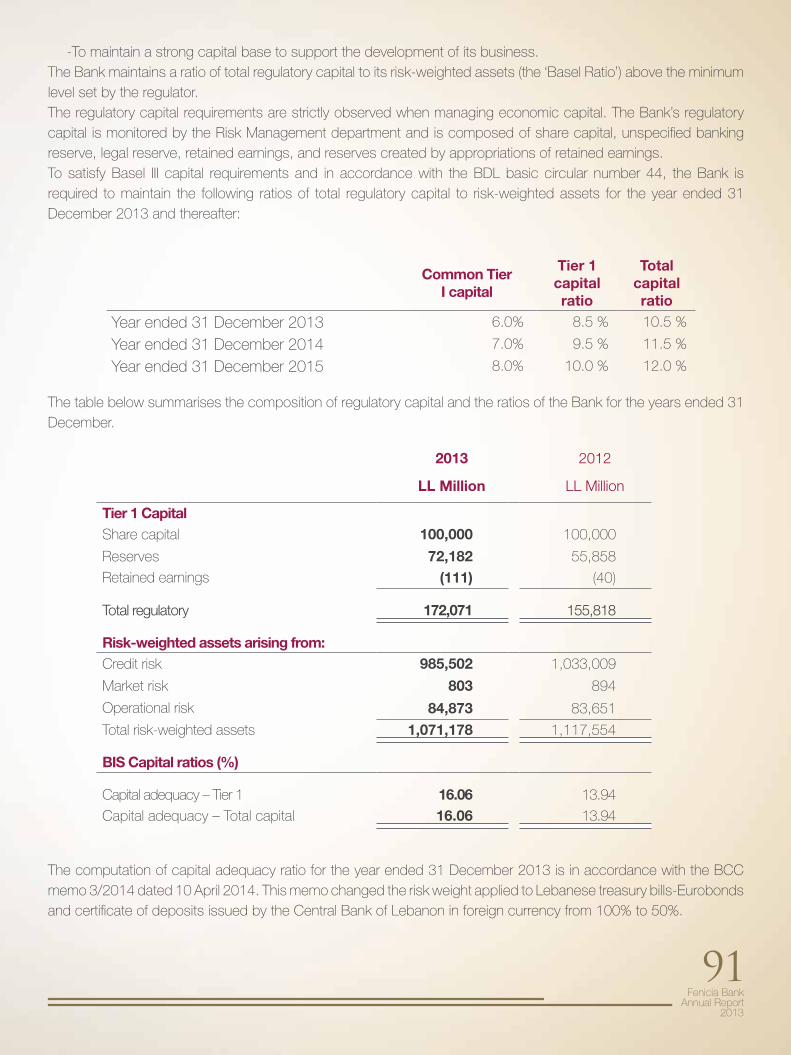

The Bank’s capital is composed solely of Common Equity Tier 1 components (common equity and reserves). The following table summarizes the Capital Adequacy Ratio according to Basel standards.

2013 2012

CET 1 capital 172,182 155,858

Additional Tier 1 capital - -

Tier 2 capital - -

Total Capital 172,182 155,858

Less: B.V. Intangible Fixed assets 96 27

Less: Revaluation of securities designated at FVTOCI 15 13

Qualifying Capital 172,071 155,818

Total risk weighted assets* 1,071,179 1,118,388

BIS ratio 16.06% 13.93%

*Based on BDL intermediate circular 358, and given its discretionary authority, the risk weight of placements with BDL including CDs in foreign currencies, was decreased from 100% to 50%.

The result ratio is significantly above both the required basel ratio of 8% and the more conservative supervisors’ ratio of 10.5%.

Regarding Basel BIS ratio, the credit risk component comprises the largest part (92%) of the total risk wighted assts. The bank utilizes the Standardized Approach, Standardized Measurement and Basic Indicator approach in assessing credit, market and oprational risk respectively.

When accounting for 2013 profits (less dividends) within the qualifying capital, CAR will rise up to 17.51%. The bank also retains a relaxing leverage ratio of 7.52% as by the end of 2013.

In compliance with the second pillar of basel 2 and the directives of the Lebanese supervisory authorities, the bank performs Internal Capital Adequacy Assessment Process ICAAP periodically in order to asssess the bank entire risk profile on both quantitative and qualitative bases, and consequently have an estimate of its economic capital.

Fenicia Bank Annual Report2013

40

Financial Statements & Notes

Fenicia Bank Annual Report

2013

41

Everything starts smallWhen great aunt Edna decided to leave her beloved car to little Samer, little did

she know he would grow into this lovable giant. At Fenicia bank, we know that everything small can grow big, and our car loan will turn any car into the one

you dream of.

Fenicia Bank Annual Report2013

42

INDEPENDENT AUDITOR’S REPORT

Independent Auditors’ Reportto the shareholders of Fenicia Bank S.A.L.

Report on the financial statements

We have audited the accompanying financial statements of Fenicia Bank S.A.L.(“the Bank”) which comprise the balance sheet as of 31 December 2013 and the statementsof comprehensive income, changes in equity and cash flows for the year then ended, and asummary of significant accounting policies and other explanatory notes.

Management’s responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financialstatements in accordance with International Financial Reporting Standards (IFRSs), and forsuch internal control as management determines is necessary to enable the preparation offinancial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ responsibility

Our responsibility is to express an opinion on these financial statements based on our audit.We conducted our audit in accordance with International Standards on Auditing. Thosestandards require that we comply with ethical requirements and plan and perform the auditto obtain reasonable assurance about whether the financial statements are free frommaterial misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The procedures selected depend on the auditors’judgment, including the assessment of the risks of material misstatement of the financialstatements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the Bank’s preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on the effectiveness of theBank’s internal control. An audit also includes evaluating the appropriateness of accountingpolicies used and the reasonableness of accounting estimates made by management, aswell as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate toprovide a basis for our audit opinion.

Fenicia Bank Annual Report

2013

43

Independent Auditors’ Report (continued)to the shareholders of Fenicia Bank S.A.L.

Opinion

In our opinion, the accompanying financial statements present fairly, in all materialrespects, the financial position of Fenicia Bank S.A.L. as at 31 December 2013, and itsfinancial performance and its cash flows for the year then ended in accordance withInternational Financial Reporting Standards

PricewaterhouseCoopers Grand Thornton

Beirut, Lebanon5 June 2014

Fenicia Bank Annual Report2013

44

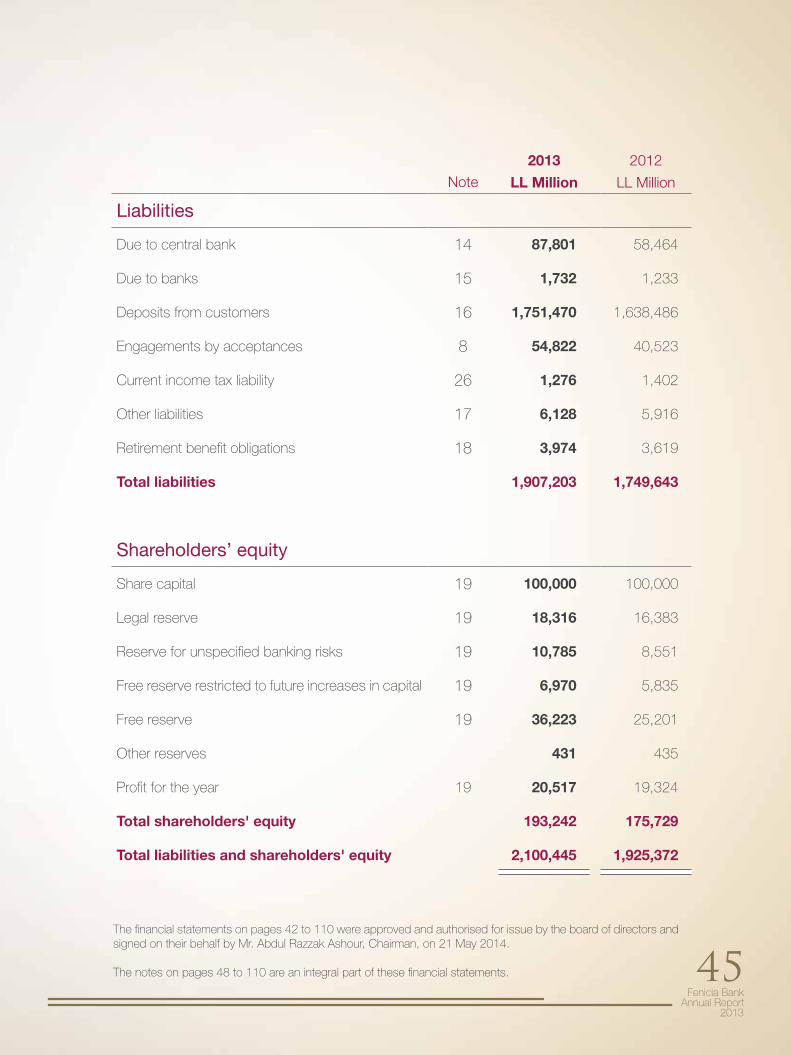

BALANCE SHEET AT 31 DECEMBER 2013

2013 2012Note LL Million LL Million

Assets

Cash and balances with the central bank 5 286,133 256,179

Due from banks 6 184,748 183,471

Loans and advances to customers 7 558,255 487,550

Debtors by acceptances 8 54,822 40,523

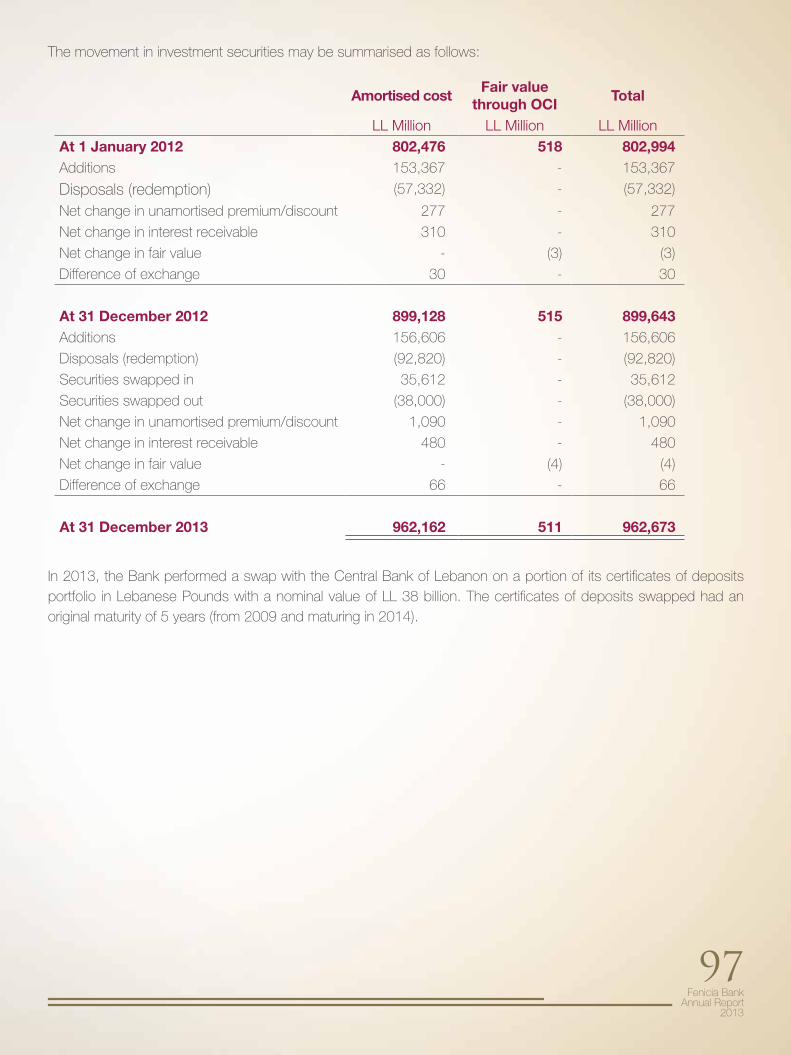

Investment securities:

- At fair value through other comprehensive income 9 511 515

- At amortised cost 9 962,162 899,128

Intangible assets 11 96 28

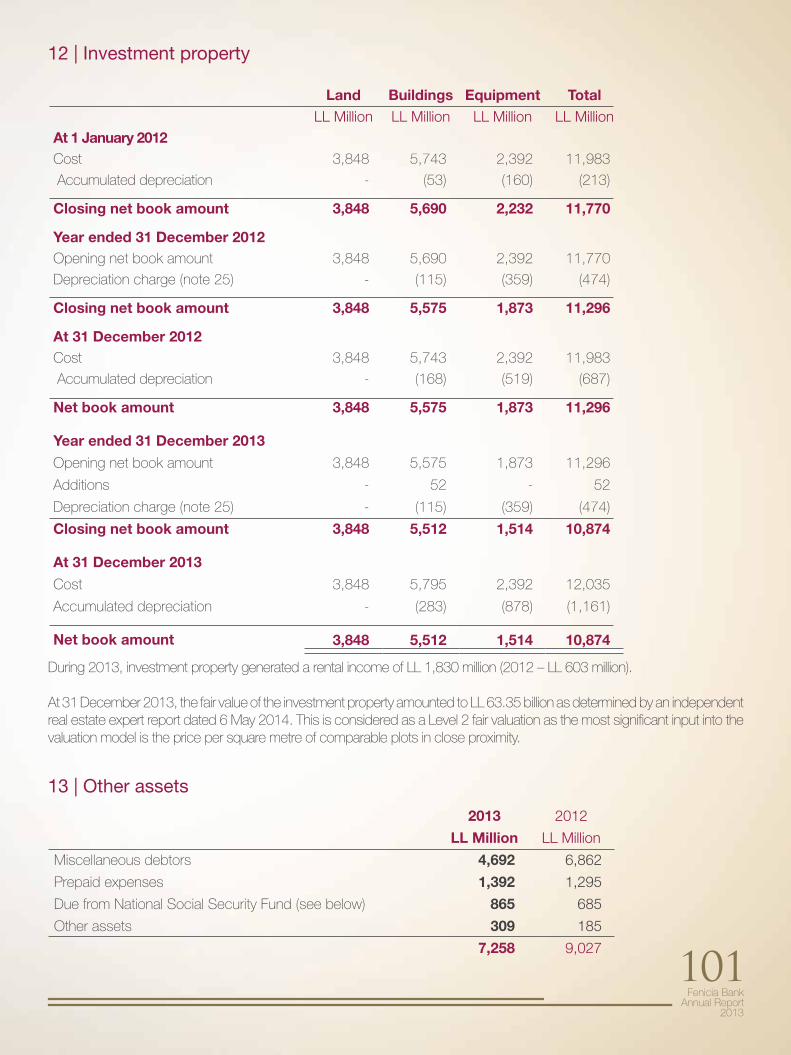

Investment property 12 10,874 11,296

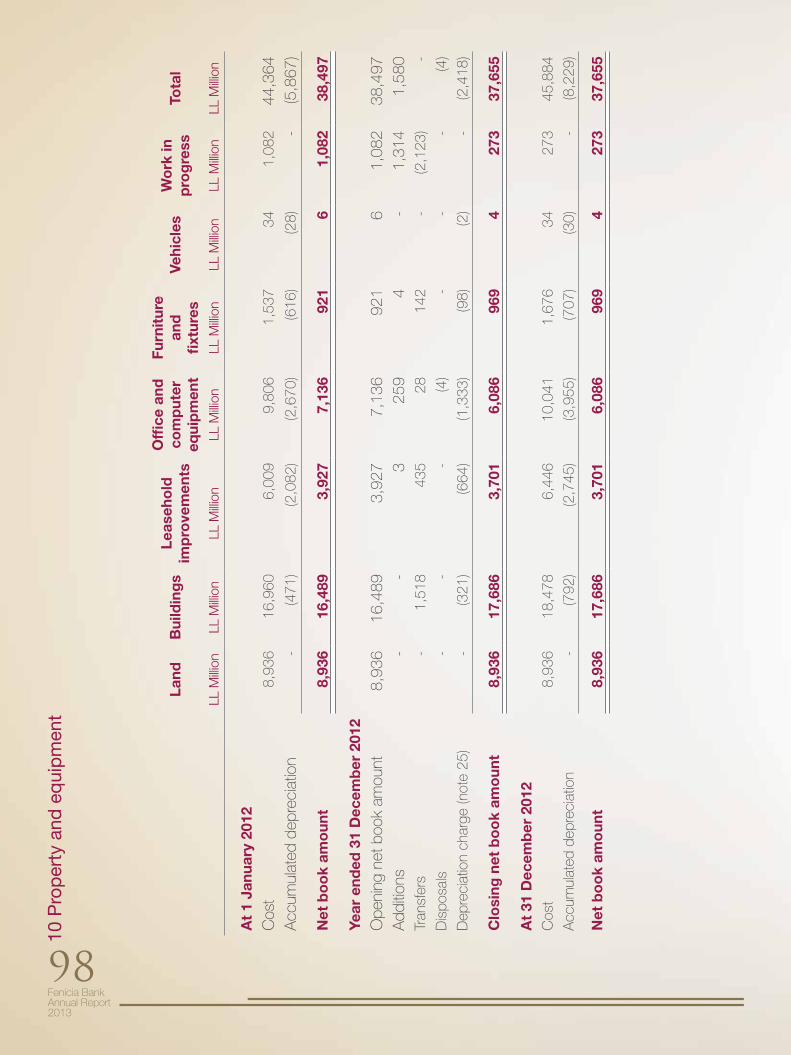

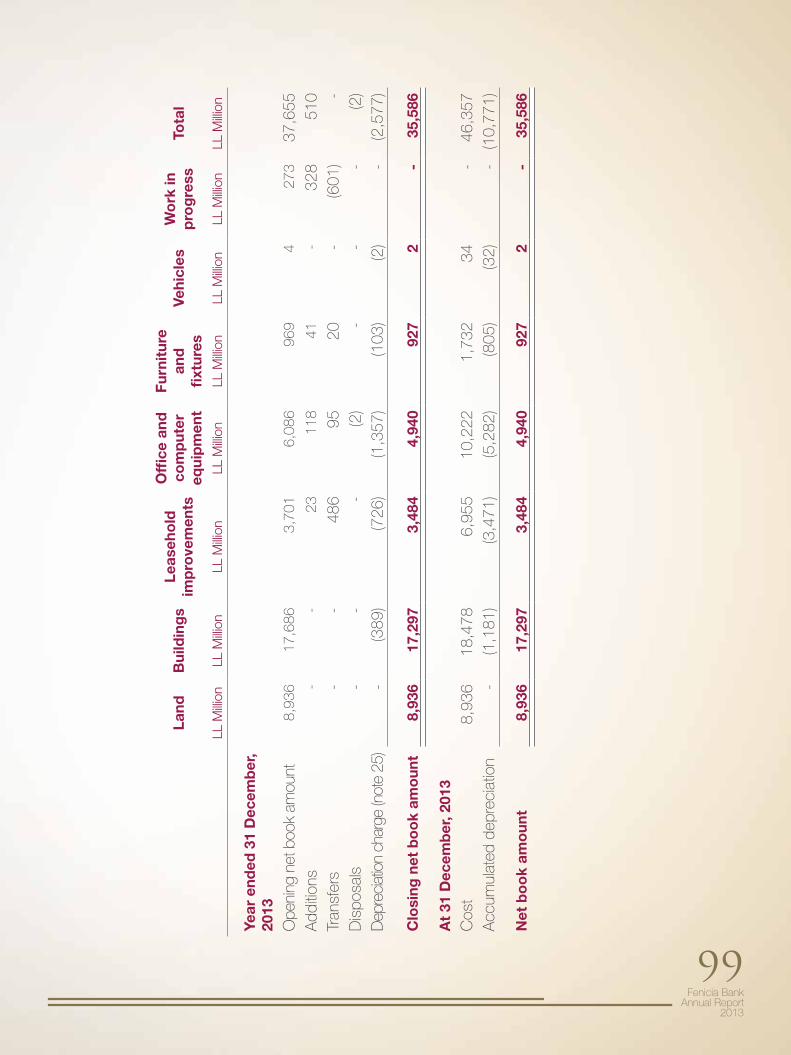

Property and equipment 10 35,586 37,655

Other assets 13 7,258 9,027

Total assets 2,100,445 1,925,372

Fenicia Bank Annual Report

2013

45The financial statements on pages 42 to 110 were approved and authorised for issue by the board of directors and signed on their behalf by Mr. Abdul Razzak Ashour, Chairman, on 21 May 2014.

The notes on pages 48 to 110 are an integral part of these financial statements.

2013 2012Note LL Million LL Million

Liabilities

Due to central bank 14 87,801 58,464

Due to banks 15 1,732 1,233

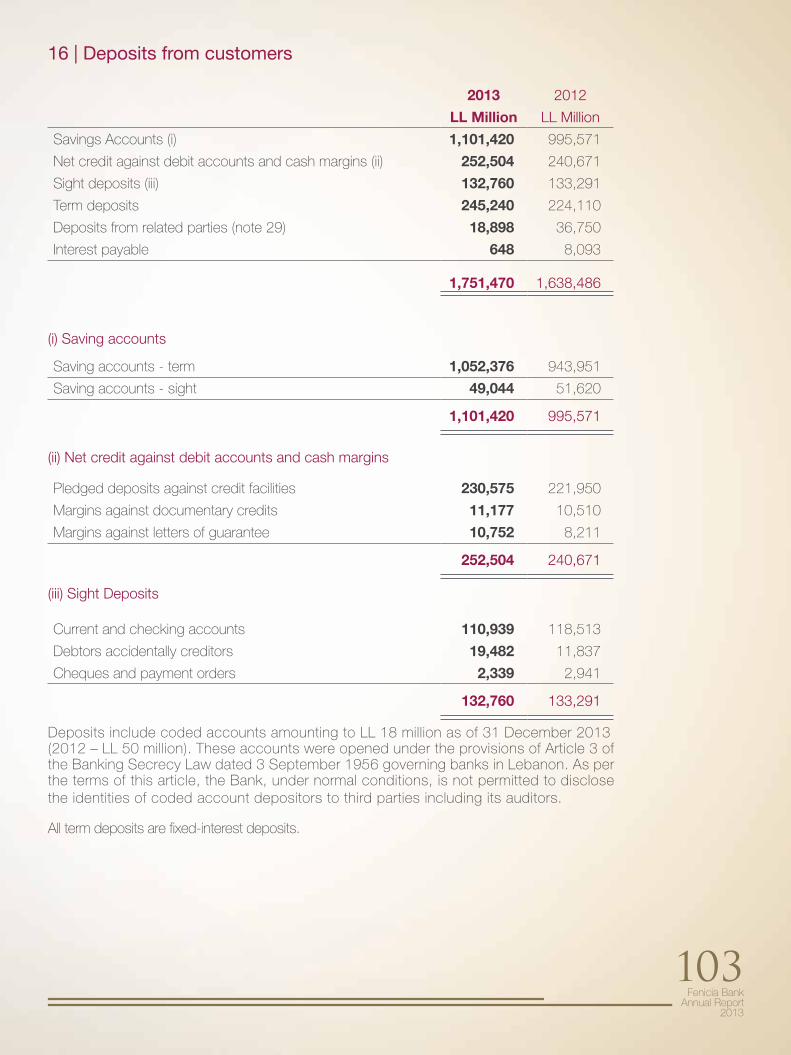

Deposits from customers 16 1,751,470 1,638,486

Engagements by acceptances 8 54,822 40,523

Current income tax liability 26 1,276 1,402

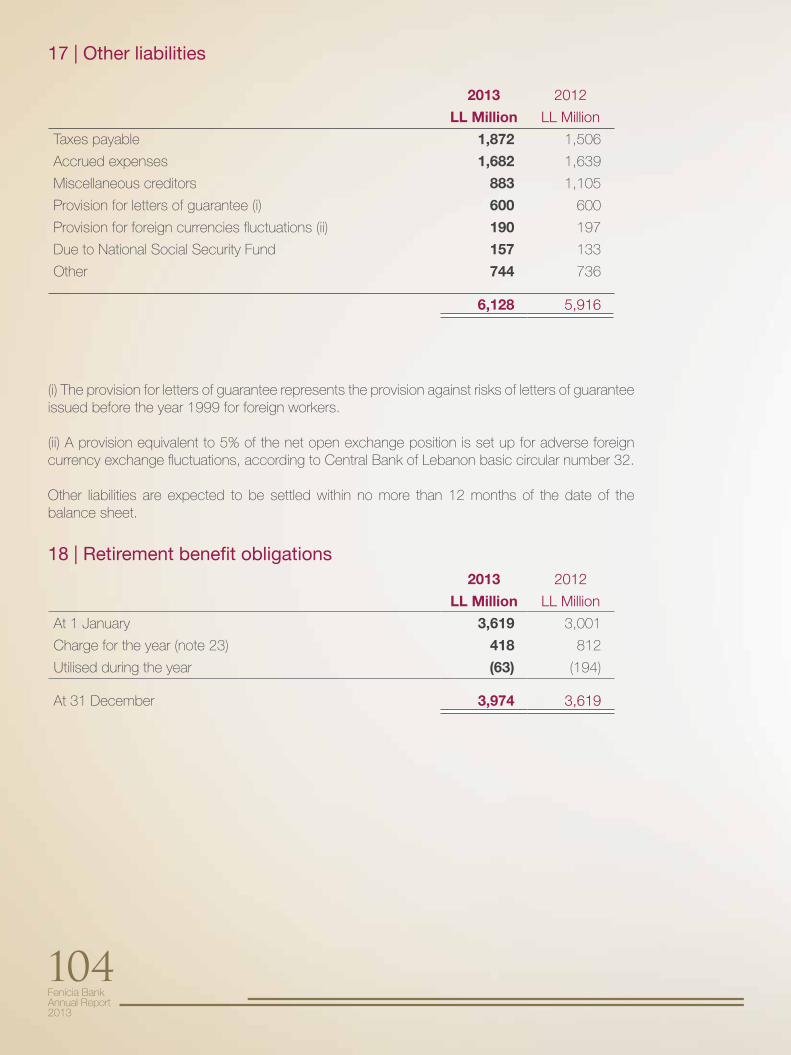

Other liabilities 17 6,128 5,916

Retirement benefit obligations 18 3,974 3,619

Total liabilities 1,907,203 1,749,643

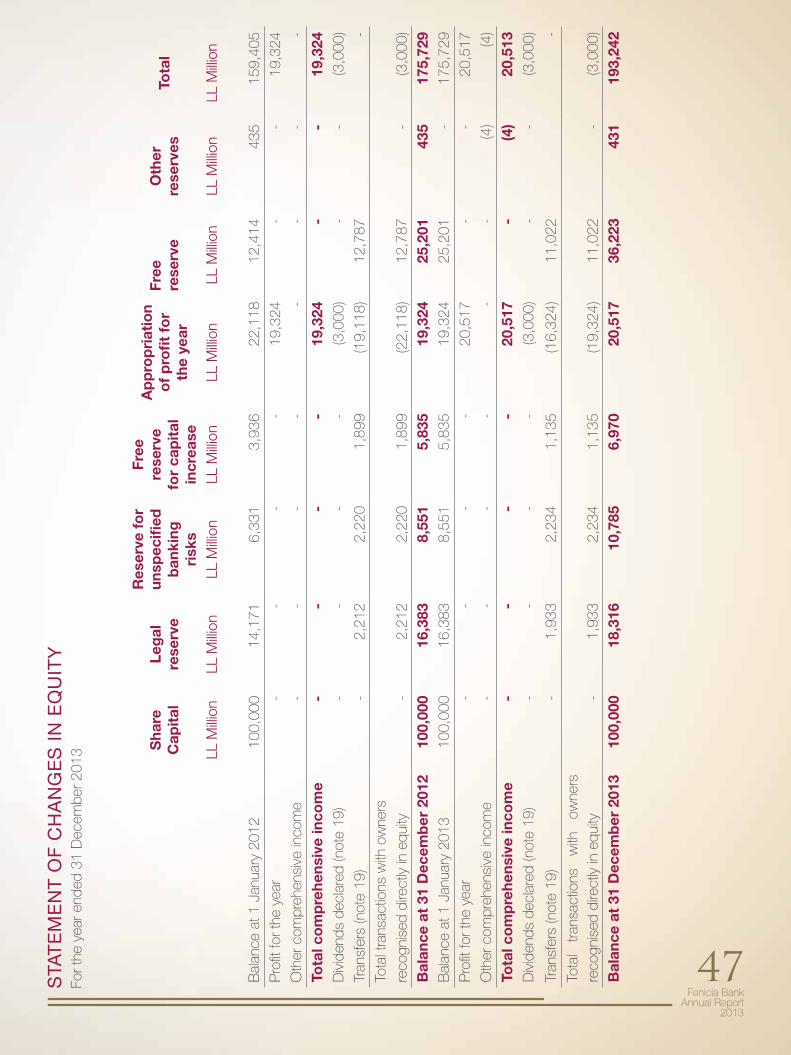

Shareholders’ equity

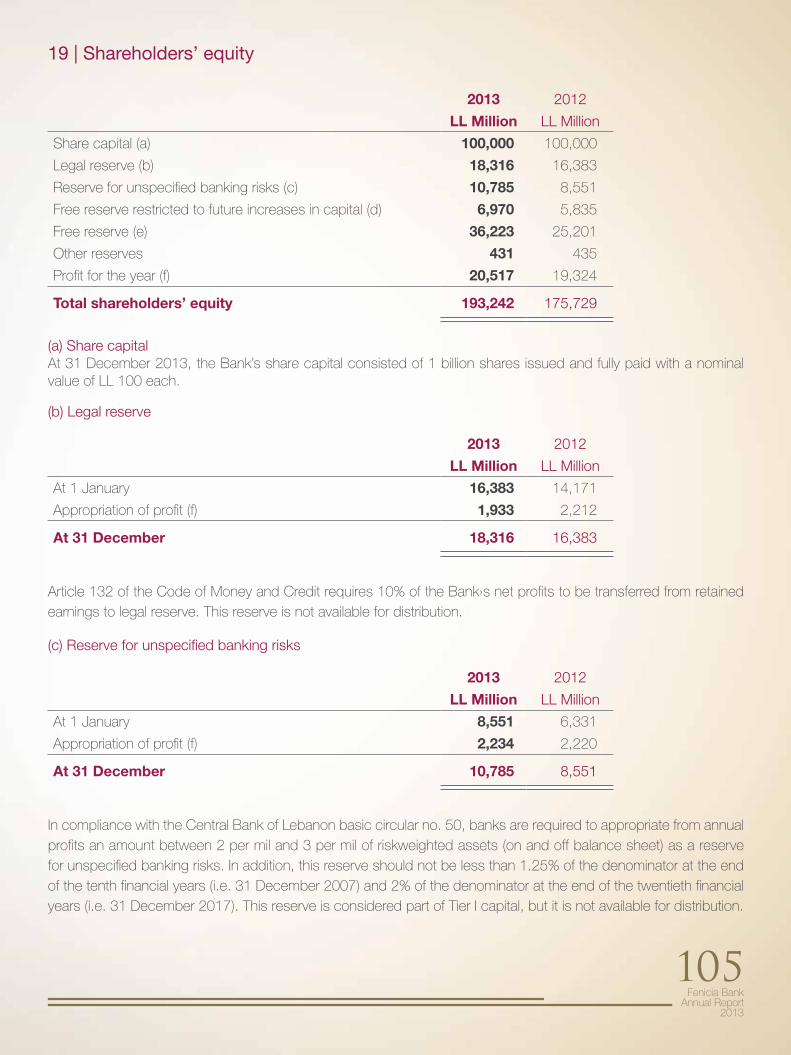

Share capital 19 100,000 100,000

Legal reserve 19 18,316 16,383

Reserve for unspecified banking risks 19 10,785 8,551

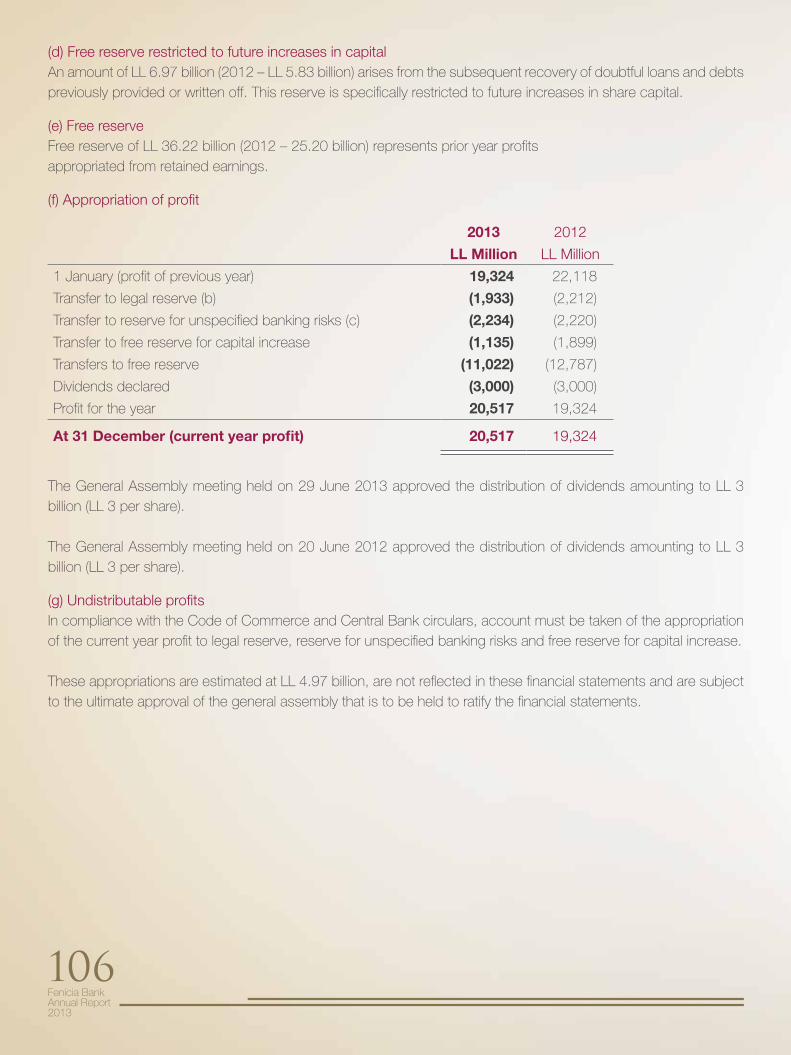

Free reserve restricted to future increases in capital 19 6,970 5,835

Free reserve 19 36,223 25,201

Other reserves 431 435

Profit for the year 19 20,517 19,324

Total shareholders' equity 193,242 175,729

Total liabilities and shareholders' equity 2,100,445 1,925,372

Fenicia Bank Annual Report2013

46

2013 2012Note LL Million LL Million

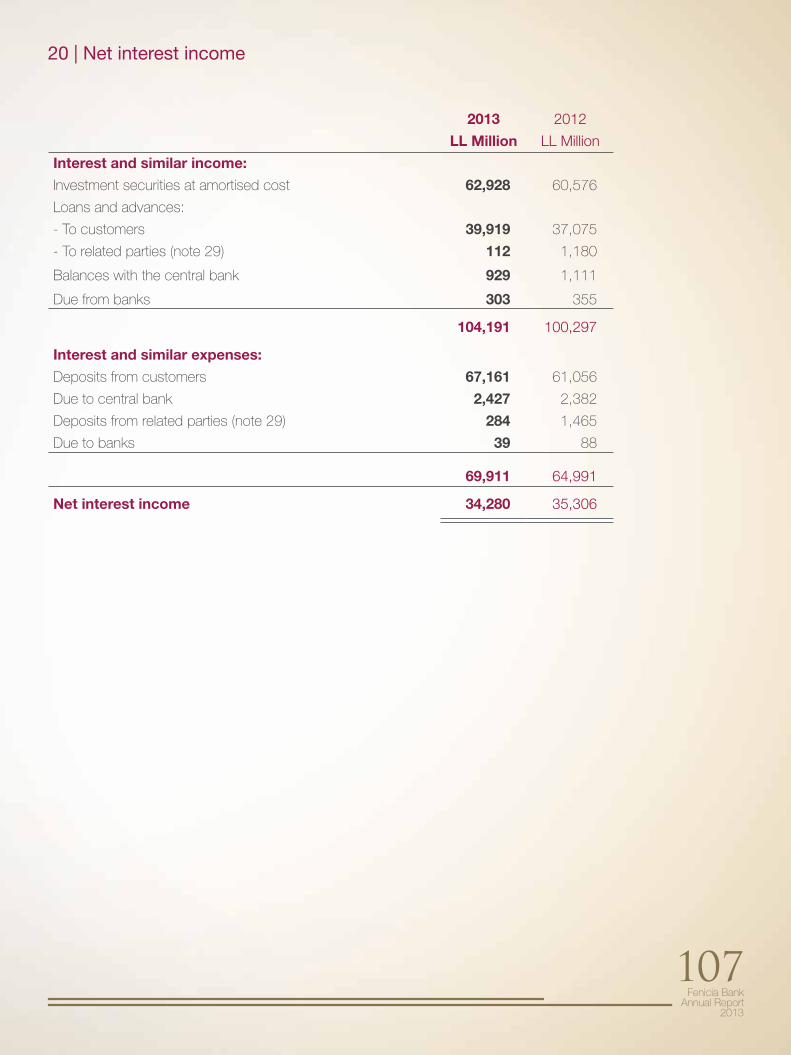

Interest and similar income 104,191 100,297

Interest and similar expenses (69,911) (64,991)

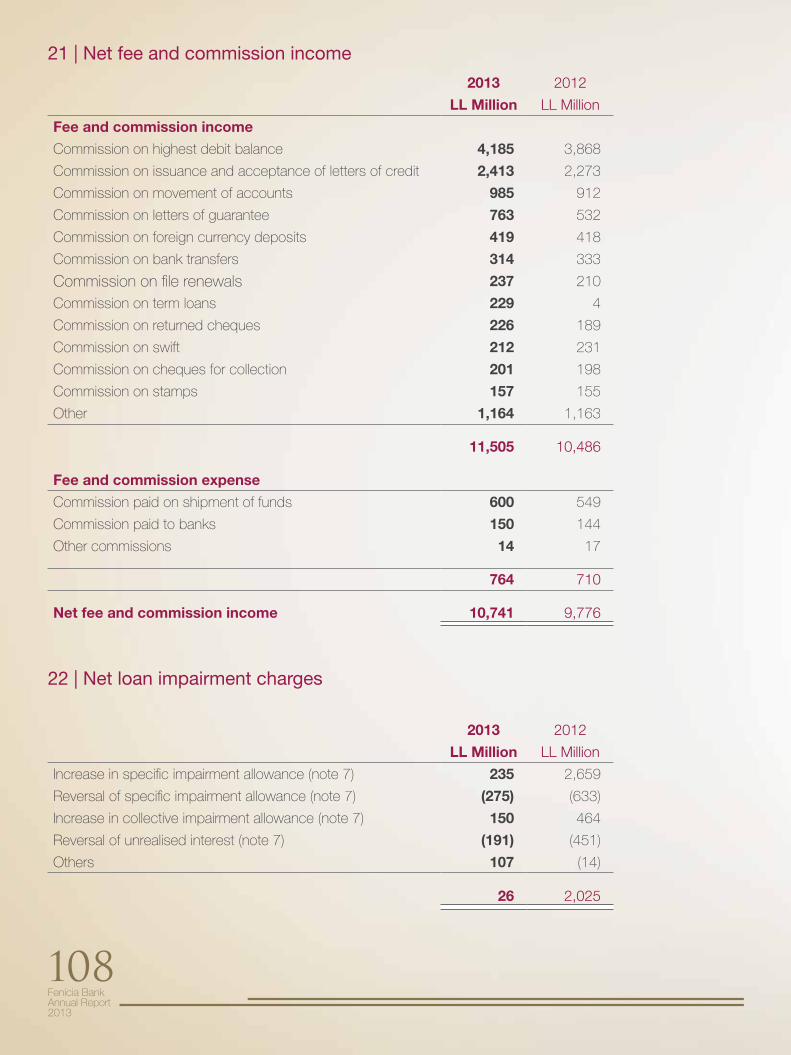

Net interest income 20 34,280 35,306Net loan impairment charges 22 (26) (2,025)

Net interest income after loan impairment charges 34,254 33,281

Fee and commission income 11,505 10,486

Fee and commission expense (764) (710)

Net fee and commission income 21 10,741 9,776

Net trading gains 1,079 1,012

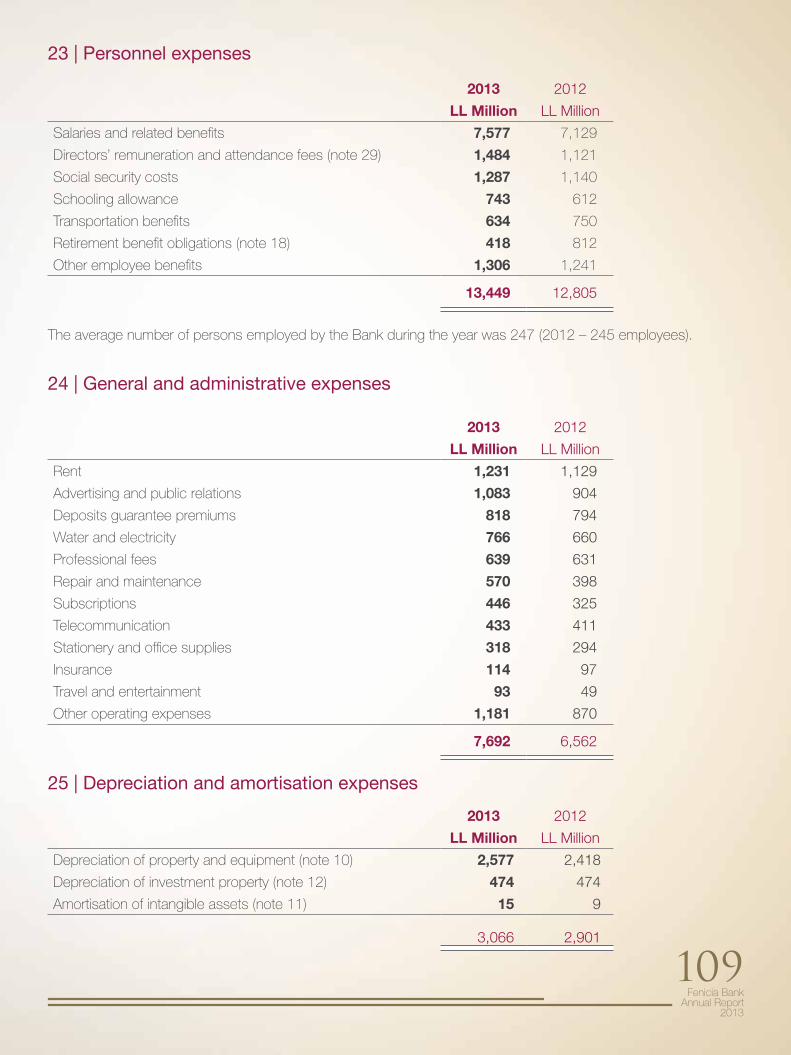

Personnel expenses 23 (13,449) (12,805)General and administrative expenses 24 (7,692) (6,562)Depreciation and amortisation charges 25 (3,066) (2,901)Other operating income 2,178 1,187

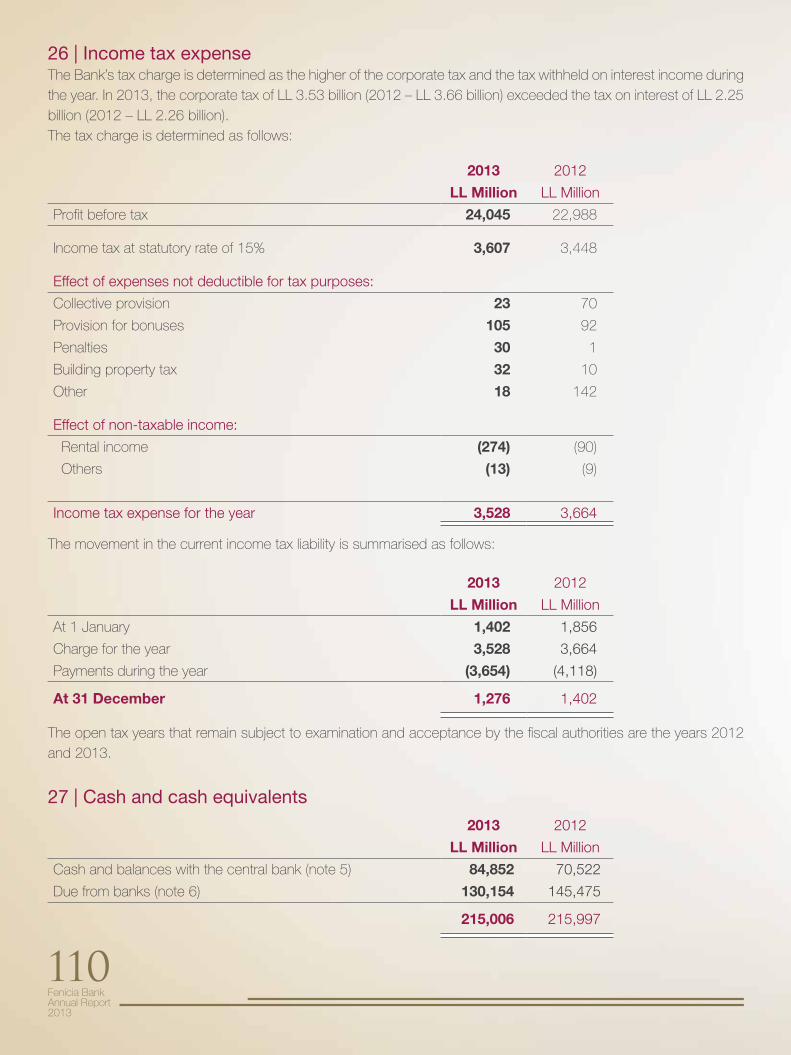

Profit before income tax 24,045 22,988

Income tax expense 26 (3,528) (3,664)

Profit for the year 20,517 19,324

Other comprehensive income

Net unrealised loss on financial assets atfair value through other comprehensive income

(4) -

Total comprehensive income for the year 20,513 19,324

STATEMENT OF COMPREHENSIVE INCOMEFor the year ended 31 December 2013

Fenicia Bank Annual Report

2013

47STA

TE

ME

NT

OF

CH

AN

GE

S I

N E

QU

ITY

For t

he y

ear e

nded

31

Dec

embe

r 201

3 Sha

re

Cap

ital

Leg

al

rese

rve

Res

erve

fo

r un

spec

ified

b

anki

ng

risk

s

Free

re

serv

e fo

r ca

pit

al

incr

ease

Ap

pro

pri

atio

n o

f p

rofi

t fo

r th

e ye

ar

Free

re

serv

eO

ther

re

serv

esTo

tal

LL M

illion

LL M

illion

LL M

illion

LL M

illion

LL M

illion

LL M

illion

LL M

illion

LL M

illion

Bal

ance

at 1

Jan

uary

201

2 10

0,00

0 14

,171

6,

331

3,93

6 22

,118

12

,414

435

159,

405

Pro

fit fo

r the

yea

r -

--

-19

,324

-

-19

,324

Oth

er c

ompr

ehen

sive

inco

me

--

--

--

--

Tota

l co

mp

rehe

nsiv

e in

com

e -

--

-19

,324

-

-19

,324

Div

iden

ds d

ecla

red

(not

e 19

) -

--

-(3

,000

) -

-(3

,000

)

Tran

sfer

s (n

ote

19)

-2,

212

2,22

0 1,

899

(19,

118)

12

,787

-

Tota

l tra

nsac

tions

with

ow

ners

reco

gnis

ed d

irect

ly in

equ

ity

-2,

212

2,22

0 1,

899

(22,

118)

12

,787

-(3

,000

)

Bal

ance

at

31 D

ecem

ber

201

2 10

0,00

0 16

,383

8,

551

5,83

5 19

,324

25

,201

435

175,

729

Bal

ance

at 1

Jan

uary

201

3 10

0,00

0 16

,383

8,

551

5,83

5 19

,324

25

,201

-17

5,72

9

Pro

fit fo

r the

yea

r -

--

-20

,517

-

-20

,517

Oth

er c

ompr

ehen

sive

inco

me

--

--

--

(4)

(4)

Tota

l co

mp

rehe

nsiv

e in

com

e -

--

-20

,517

-

(4)

20,5

13D

ivid

ends

dec

lare

d (n

ote

19)

--

--

(3,0

00)

--

(3,0

00)

Tran

sfer

s (n

ote

19)

-1,

933

2,23

4 1,

135

(16,

324)

11

,022

-

Tota

l tra

nsac

tions

w

ith

owne

rs

reco

gnis

ed d

irect

ly in

equ

ity

-1,

933

2,23

4 1,

135

(19,

324)

11

,022

-(3

,000

)

Bal

ance

at

31 D

ecem

ber

201

3 10

0,00

0 18

,316

10

,785

6,

970

20,5

17

36,2

2343

119

3,24

2

Fenicia Bank Annual Report2013

48

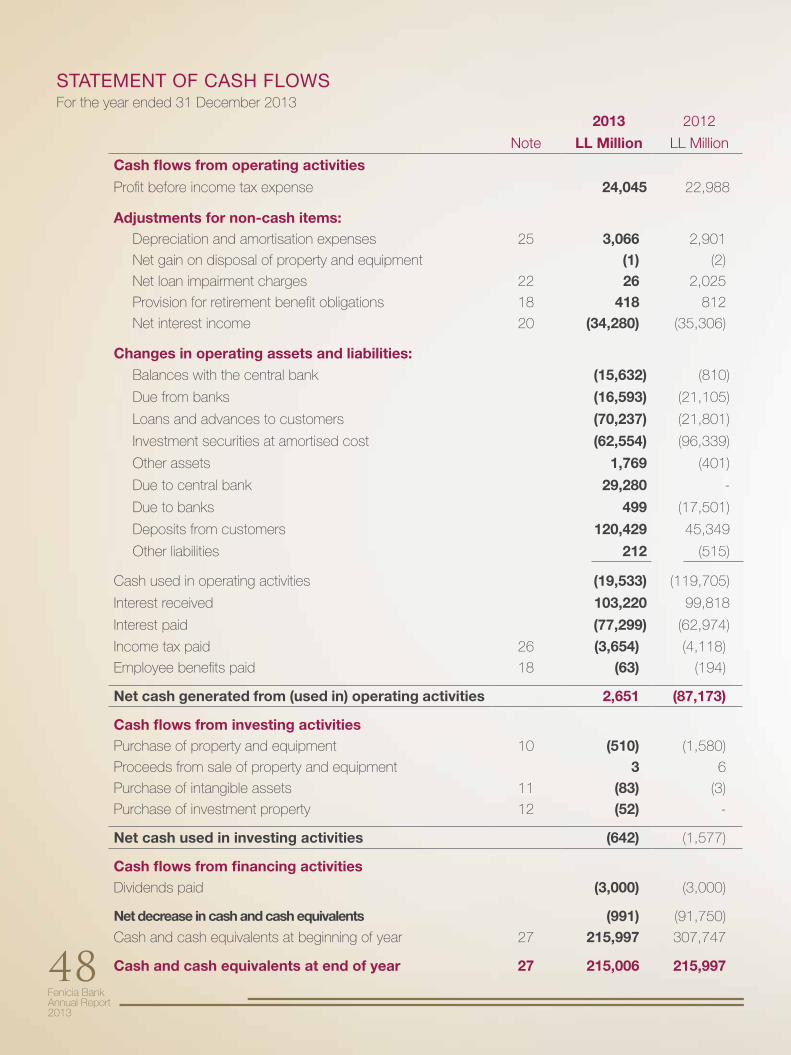

STATEMENT OF CASH FLOWSFor the year ended 31 December 2013

2013 2012

Note LL Million LL Million

Cash flows from operating activities

Profit before income tax expense 24,045 22,988

Adjustments for non-cash items: Depreciation and amortisation expenses 25 3,066 2,901

Net gain on disposal of property and equipment (1) (2)

Net loan impairment charges 22 26 2,025

Provision for retirement benefit obligations 18 418 812

Net interest income 20 (34,280) (35,306)

Changes in operating assets and liabilities: Balances with the central bank (15,632) (810)

Due from banks (16,593) (21,105)

Loans and advances to customers (70,237) (21,801)

Investment securities at amortised cost (62,554) (96,339)

Other assets 1,769 (401)

Due to central bank 29,280 -

Due to banks 499 (17,501)

Deposits from customers 120,429 45,349

Other liabilities 212 (515)

Cash used in operating activities (19,533) (119,705)

Interest received 103,220 99,818

Interest paid (77,299) (62,974)

Income tax paid 26 (3,654) (4,118)

Employee benefits paid 18 (63) (194)

Net cash generated from (used in) operating activities 2,651 (87,173)

Cash flows from investing activitiesPurchase of property and equipment 10 (510) (1,580)

Proceeds from sale of property and equipment 3 6

Purchase of intangible assets 11 (83) (3)

Purchase of investment property 12 (52) -

Net cash used in investing activities (642) (1,577)

Cash flows from financing activitiesDividends paid (3,000) (3,000)

Net decrease in cash and cash equivalents (991) (91,750)

Cash and cash equivalents at beginning of year 27 215,997 307,747

Cash and cash equivalents at end of year 27 215,006 215,997

Fenicia Bank Annual Report

2013

49

Fenicia Bank Annual Report2013

50

through other comprehensive income.

The financial statements comprise the balance sheet, the statement of comprehensive income, the statement of changes in equity, the statement of cash flows and the notes. The Bank classif ies its expenses by the nature of expense method.

The financial statements are presented in Lebanese Pounds, which is the Bank’s functional and presentation currency. The figures shown in the financial statements are stated in mil l ions of Lebanese Pounds (“LL Mil l ion”) except when otherwise indicated. The disclosures on risks from financial instruments are presented in the financial r isk management report contained in note 3.

The statement of cash flows shows the changes in cash and cash equivalents arising during the year from operating activit ies, investing activit ies and financing activit ies. Cash and cash equivalents include highly l iquid investments. Note 27 shows the balance sheet captions in which cash and cash equivalents items are included.

The cash flows from operating activit ies are determined by using the indirect method. Net income is therefore adjusted by non-cash items, such as measurement gains or losses, changes in provisions, as well as changes from receivables and l iabil i t ies. In addition, al l the income and expense from cash transactions that are attr ibutable to investing or f inancing activit ies are eliminated. Interest received or paid is classif ied as operating cash flows.

1 | General information

Fenicia Bank S.A.L. (the “Bank”) offers a ful l range of retai l, private and commercial banking activit ies to its customers. The Bank’s operations cover al l districts in Lebanon.

The Bank was incorporated in Lebanon in 1962 and registered at the Lebanese Commercial Register in Beirut under No. 11923 in the name of Bank of Kuwait and the Arab World S.A.L. It is l isted under number 58 in the l ist of Lebanese banks regulated by the Central Bank of Lebanon. The Bank has changed its name to Fenicia Bank S.A.L. on 20 December 2010.

2 | Summary of significant accounting policies

The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to al l the years presented, unless otherwise stated.

2.1 | Basis of preparation The financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and IFRS Interpretation Committee (“IFRS IC”) as issued by the International Accounting Standards Board (“IASB”). The financial statements have been prepared under the historical cost convention, as modified by the revaluation of f inancial instruments at fair value

Notes to the financial statements for the year ended 31 December 2013

Fenicia Bank Annual Report

2013

51

a signif icant impact on the Bank’s f inancial statements.

– Amendment to IAS 1, ‘Clarif ication of the Requirement for Comparative Information’. The amendment to IAS 1 clarif ies the difference between voluntary additional comparative information and the minimum required comparative information. An entity must include comparative information in the related notes to the financial statements when it voluntari ly provides comparative information beyond the minimum required comparative period.

– An opening statement of f inancial posit ion (known as the ‘third balance sheet’) must be presented when an entity applies an accounting policy retrospectively, makes retrospective restatements, or reclassif ies items in its f inancial statements, provided any of those changes has a material effect on the statement of f inancial posit ion at the beginning of the preceding period.

– The amendment clarif ies that a third balance sheet does not have to be accompanied by comparative information in the related notes. The adoption of this amendment is not applicable and accordingly, did not have any impact on the Bank’s f inancial statements.

– -IFRS 13, ‘Fair Value Measurement’ ( issued in May 2011 and effective for annual periods beginning on or after 1 January 2013) improved consistency and reduced complexity by providing a revised definit ion of fair value, and a single source of fair value

The cash flows from investing and financing activit ies are determined by using the direct method. The Bank’s assignment of the cash flows to operating, investing and financing categories depends on the Bank’s business model (management approach). The preparation of f inancial statements in conformity with IFRS requires the use of certain crit ical accounting estimates. It also requires management to exercise its judgement in the process of applying the Bank’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are signif icant to the financial statements are disclosed in Note 4.

2.1.1 | Changes in accounting policies and disclosures

(a) Standards, amendments and interpretations effective on or after 1 January 2013

The fol lowing standards and amendments, which became effective in 2013, are relevant to the Bank:

– Amendment to IAS 1, ‘Financial statement presentation’ regarding other comprehensive income, (revised in May 2011 and effective for annual period beginning on or after 1 January 2013). The main change result ing from these amendments is a requirement for Banks to group items presented in ‘other comprehensive income’ (OCI) on the basis of whether they are potential ly reclassif iable to profit or loss subsequently (reclassif ication adjustments). The amendment did not have

Fenicia Bank Annual Report2013

52

measurement and disclosure requirements for use across IFRSs. The amendment of this standard did not have a signif icant impact on the Bank’s f inancial statements.

– Amendment to IFRS 7, ‘Financial instruments’: Disclosures’ on derecognition, (effective from 1 July 2012). The amendment requires an entity to disclose information about rights to set-off f inancial instruments and related arrangements (e.g., collateral agreements). The disclosures would provide users with information that is useful in evaluating the effect of netting arrangements on an entity’s f inancial posit ion. The new disclosures are required for al l recognised financial instruments that are set off in accordance with IAS 32. The disclosures also apply to recognised financial instruments that are subject to an enforceable master netting arrangement or similar agreement, irrespective of whether the financial instruments are set off in accordance with IAS 32. As the Bank is not setting off f inancial instruments in accordance with IAS 32 and does not have relevant offsetting arrangements, the amendment does not have any impact on the Bank.

– Amendment to IAS 32, ‘Financial Instruments: Presentation’ clarif ies that income taxes arising from distributions to equity holders are accounted for in accordance with IAS 12 Income Taxes. The amendment removes existing income tax requirements from IAS 32 and requires entit ies to apply the requirements in IAS 12 to any income tax arising from distributions to equity holders. The amendment did not have an impact on the Bank’s f inancial statements.

– Amendment to IAS 27, ‘Separate Financial Statements’ (revised in May 2011 and effective for annual periods beginning on or after 1 January 2013) was changed and its objective is now to prescribe the accounting

and disclosure requirements for investments in subsidiaries, joint ventures and associates when an entity prepares separate financial statements.

– IFRS 12, ‘Disclosure of Interests in Other Entit ies’ ( issued in May 2011 and effective annual periods beginning on or after 1 January 2013) sets out the requirements for disclosures relating to an entity’s interests in subsidiaries, joint arrangements, associates and structured entit ies. The requirements in IFRS 12 are more comprehensive than the previously existing disclosure requirements for subsidiaries. For example, where a subsidiary is controlled with less than a majority of voting rights. The adoption of this amendment did not have any impact on the financial posit ion or performance of the Bank.

b) Standards, amendments and interpretations issued but not yet effective

– Amendment to IAS 36, ‘ Impairment of assets’ ( issued in May 2013 and effective for annual period beginning 1 January 2014), on the recoverable amount disclosures for non-financial assets. This amendment removed certain disclosures of the recoverable amount of CGUs which had been included in IAS 36 by the issue of IFRS 13. This amendment is not expected to have an impact on the Bank’s f inancial statements.

– Amendments to IAS 32, ‘Offsetting Financial Assets and Financial Liabil i t ies’ ( issued in December 2011 and effective for annual periods beginning on or after 1 January 2014). The amendment added application guidance to IAS 32 to address inconsistencies identif ied in applying some of the offsetting criteria. This includes clarifying the meaning of ‘currently has a legally enforceable right of set-off ’ and that some gross settlement systems may be considered equivalent to net

Fenicia Bank Annual Report

2013

53

settlement. This amendment is not expected to have an impact on the Bank’s f inancial performance or posit ion.

– Amendments to IAS 39, ‘Novation of Derivatives and Continuation of Hedge Accounting’. The amendment provided rel ief from discontinuing hedge accounting when novation of a derivative designated as a hedging instrument meets certain criteria. This amendment is not expected to have an impact on the Bank’s f inancial performance or posit ion.

2.2 Foreign currency translation (a) Functional and presentation currency

I tems included in the financial statements of the Bank are measured using the currency of the primary economic environment in which the Bank operates (‘the functional currency’). The financial statements are presented in Lebanese pounds, which is the Bank’s functional and presentation currency.

(b) Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevail ing at the dates of the transactions. Monetary items denominated in foreign currency are translated with the closing rate as at the reporting date. Non-monetary items measured at historical cost denominated in a foreign currency are translated with the exchange rate as at the date of init ial recognition; non-monetary items in a foreign currency that are measured at fair value are translated using the exchange rates at the date when the fair value was determined. Foreign exchange gains and losses result ing from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and l iabil i t ies denominated in foreign currencies are recognised in the statement of comprehensive income.

Changes in the fair value of monetary securit ies denominated in foreign currency are analysed between translation differences result ing from changes in amortised cost of the security and other changes in the carrying amount of the security. Translation differences related to changes in amortised cost are recognised in profit or loss.

Translation differences on non-monetary f inancial assets and l iabil i t ies are recognised in the profit or loss as part of the fair value gain or loss. Translation differences on non-monetary f inancial instruments such as equities measured at fair value through other comprehensive income are included in other comprehensive income.

2.3 | Financial assets and liabilities

In accordance with IFRS 9, al l f inancial assets and l iabil i t ies have to be recognised in the balance sheet and measured in accordance with their assigned category.

2.3.1 | Date of recognition

All f inancial assets and l iabil i t ies are init ial ly recognised on the trade date, i.e. the date that the Bank becomes a party to the contractual provisions of the instrument. This includes purchases or sales of f inancial assets that require delivery of assets within the time frame generally established by regulation or convention in the market place.

2.3.2 | Classification and measurement a. Financial assets

The Bank classif ies its f inancial assets as measured at fair value or at amortised cost. The classif ication depends on the purpose for which the financial assets were acquired. Management determines the classif ication of its f inancial assets at init ial recognition.

Fenicia Bank Annual Report2013

54

(i) Financial assets at amortised cost

Debt instruments are subsequently measured at amortised cost less any impairment loss (except for debt instruments that are designated at fair value through profit or loss upon init ial recognition) if they meet the fol lowing two conditions:

- The asset is held within a business model whose objective is to hold assets in order to collect contractual cash flows; and

- The contractual terms of the instrument give rise on specif ied dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

These financial assets are init ial ly recognised at cost, being the fair value of the consideration paid for the acquisit ion of the investment. All transaction costs directly attr ibuted to the acquisit ion are also included in the cost of investment. After init ial measurement, these financial assets are measured at amortised cost using the effective interest rate method (EIR), less allowance for impairment. Amortised cost is calculated by taking into account any discount of premium on acquisit ion and fees and costs that are an integral part of the effective interest rate. The amortisation is included in “Interest and similar income” in the statement of comprehensive income. The losses arising from impairment are recognised in the statement of comprehensive income in “Net gains/losses on financial assets at amortised cost”.

Gains and losses arising from the derecognition of f inancial assets measured at amortised cost are reflected under “Net gain ( loss) from sale of f inancial assets at amortised cost” in the statement of comprehensive income.

(ii) Financial assets at fair value

Included in this category are those debt instruments that do not meet the conditions in

“Financial assets at amortised cost” above, debt instruments designated at fair value through profit or loss upon init ial recognition, and equity instruments at fair value through profit or loss.

Debt instruments at fair value through profit or loss

The Bank has not designated any debt instruments as measured at fair value through profit or loss to eliminate or signif icantly reduce an accounting mismatch.

Equity instruments at fair value through profit or loss

Investments in equity instruments are classif ied at fair value through profit or loss, unless the Bank designates at init ial recognition an investment that is not held for trading as at fair value through other comprehensive income.

b. Financial l iabil it ies

Liabil it ies are init ial ly measured at fair value plus, in the case of a f inancial l iabil i ty not at fair value through profit or loss, particular transaction costs. Liabil i t ies are subsequently measured at amortised cost or fair value.

The Bank classif ies al l f inancial l iabil i t ies as subsequently measured at amortised cost using the effective interest method, except for:

- f inancial l iabil i t ies at fair value through profit or loss (including derivatives);

- f inancial l iabil i t ies that arise when a transfer of a f inancial asset does not qualify for derecognition or when the continuing involvement approach applies;

- f inancial guarantee contracts and commitments to provide a loan at a below-market interest rate which after init ial recognition are subsequently measured at the higher of the amount determined

Fenicia Bank Annual Report

2013

55

in accordance with IAS 37 Provisions, Contingent Liabil i t ies and Contingent Assets and the amount init ial ly recognised less, when appropriate, cumulative amortisation recognised in accordance with IAS 18 Revenue.

After init ial measurement, due to central bank, due to banks and deposits from customers are measured at amortised cost less amounts repaid using the effective interest rate method. Amortised cost is calculated by taking into account any discount or premium on the issue and costs that are an integral part of the effective interest rate method.

2.3.3 | Derecognition of financial assets and financial liabilities

(i) Financial assets

A financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is derecognised when:

- the rights to receive cash flows from the asset have expired;

- the Bank has transferred its rights to receive cash flows from the asset or has assumed an obligation to pay the received cash flows in full without material delay to a third party under a ‘pass-through’ arrangement; and either:

(a) the Bank has transferred substantially all the risks and rewards of the asset, or

(b) the Bank has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

When the Bank has transferred its rights to receive cash flows from an asset or has entered into a pass-through arrangement, and has neither transferred nor retained substantially all the risks and rewards of the asset nor transferred control of the asset, the asset is recognised to the extent of the Bank’s continuing involvement in the asset. In that case, the Bank also recognizes an associated liability. The transferred asset and the

associated liability are measured on a basis that reflects rights and obligations that the Bank has retained.

Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the Bank could be required to repay.

A financial liability is derecognised when the obligation under the liability is discharged or cancelled or expires. Where an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability. The difference between the carrying value of the original financial liability and the consideration paid is recognized in the statement of comprehensive income.

2.4 | Offsetting financial instruments

Financial assets and liabilities are offset and the net amount is reported in the balance sheet when there is a legally enforceable right to offset the recognised amounts or there is an intention to settle on a net basis, or realise the asset and settle the liability simultaneously.

Income and expenses are presented on a net basis only when permitted under IFRS, or for gains and losses arising from a group of similar transactions such as in the Bank’s trading activity.

2.5 | Fair value measurement

The Bank measures financial instruments and non-financial assets, at fair value at each statement of financial position date. Also, fair values of financial instruments measured at amortised cost are disclosed in the notes.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fair value measurement is based on the presumption that the transaction to sell the asset or transfer the liability

Fenicia Bank Annual Report2013

56

takes place either:

- In the principal market for the asset or liability, or - In the absence of a principal market, in the most advantageous market for the asset or liability

The principal or the most advantageous market must be accessible by the Bank. The fair value of an asset or a liability is measured using the assumptions that market participants would use when pricing the asset or liability, assuming that market participants act in their economic best interest.

A fair value measurement of a non-financial asset takes into account a market participant’s ability to generate economic benefits by using the asset in its highest and best use or by selling it to another market participant that would use the asset in its highest and best use.

The Bank uses valuation techniques that are appropriate in the circumstances and for which sufficient data are available to measure fair value, maximising the use of relevant observable inputs and minimising the use of unobservable inputs.

All assets and liabilities for which fair value is measured or disclosed in the financial statements are categorised within the fair value hierarchy, described as follows, based on the lowest level input that is significant to the fair value measurement as a whole:

- Level 1 – Quoted (unadjusted) market prices in active markets for identical assets or liabilities - Level 2 – Valuation techniques for which the lowest level input that is significant to the fair value measurement is directly or indirectly observable - Level 3 – Valuation techniques for which the lowest level input that is significant to the fair value measurement is unobservable

For assets and liabilities that are recognised in the financial statements on a recurring basis, the Bank determines whether transfers have occurred between Levels in the hierarchy by re¬assessing categorisation (based on the lowest level input that is significant to the fair value measurement as a whole) at the end of each reporting period.

Management determines the policies and procedures for both recurring fair value measurement, such as investment properties and unquoted financial assets, and for non¬recurring measurement.

At each reporting date, the management analyses the movements in the values of assets and liabilities which are required to be re-measured or re-assessed as per the Bank’s accounting policies. For this analysis, the management verifies the major inputs applied in the latest valuation by agreeing the information in the valuation computation to contracts and other relevant documents.

For the purpose of fair value disclosures, the Bank has determined classes of assets and liabilities on the basis of the nature, characteristics and risks of the asset or liability and the level of the fair value hierarchy as explained above.

2.6 | Impairment of financial assets

The Bank assesses at each statement of financial position date whether there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated.

The criteria that the Bank uses to determine whether there is objective evidence of an impairment loss include:

a) significant financial difficulty of the issuer or obligor;

b) a breach of contract, such as a default or delinquency in interest or principal payments;

c) the lender, for economic or legal reasons relating to the borrower’s financial difficulty, granting to the borrower a concession that the lender would not otherwise consider;

d) it becomes probable that the borrower will enter bankruptcy or other financial reorganisation;

Fenicia Bank Annual Report

2013

57

e) the disappearance of an active market for that financial asset because of financial difficulties; or

f) observable data indicating that there is a measurable decrease in the estimated future cash flows from a portfolio of financial assets since the initial recognition of those assets, although the decrease cannot yet be identified with the individual financial assets in the portfolio, including:

(i) adverse changes in the payment status of borrowers in the portfolio; and