Embed Size (px)

Citation preview

Life Insurance Professional Analysis and Review

Presented By:

Matt Woodson

Zenith Marketing Group, Inc.

Charlotte, NC

Is your client’s insurance up to P.A.R?

To ensure that all clients have the best possible life insurance solutions

available.

Paramount Principle

Purpose

• Assure that the insurance need hasn’t changed• Uncover changes in underwriting status, good or

bad• Review policy performance• Review policy provisions• Review beneficiary status• Review loan status (if appropriate)

Who Needs A Review?

Personal Clients

• Younger and Middle-Aged Clients Changing Family Needs Supplemental Income, make insurance

permanent

• Older Clients Need to keep policies in-force Estate Planning and TOLI

Who Needs A Review?Business Clients• Benefits – need to support promises

Deferred Comp.Sec. 162 Bonus PlansSERP

• Business Continuation and Key PersonMore or Less OwnersOwnership Properly Structured?Buy-Out PossibilitiesBusiness Properly Valued?

Who Needs A Review?

Trust Owned Life Insurance (TOLI) Survey

• Professional Trustees83.5% - No Procedures or Guidelines for TOLI95.3% - No Procedures for Variable Life Policies

• Family and Friends as Trustees94.7% - No Procedures for Variable Life Policies71.2% - Have not reviewed Life Policies in past 5

years.

Survey published in Trusts & Estates magazine, May 2003, page 63.

Who Needs A Review?

Code of Federal Regulations Title 12 Sec. 9.6

• Mandates requirements for National Banks dealing with Trust Assets, including Life Insurance.

• ReviewsPre-Acceptance, Post Acceptance, Ongoing

Annual

Some Policies May be in Danger of Lapsing Because:

Low interest rate environment/ low interest crediting rate

Lower than anticipated investment performance (VUL)

review subaccount allocations Increased Cost of Insurance

More premium may be needed to fulfill the original goal.

Issues You May Uncover

Interest Rate History

Interest Rates

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Some Policies May be in Danger of Lapsing Because:

Reduction in Dividend Rates (WLP) Increasing Premium (Term) Policy Loans Excessive Withdrawals Skipped Premium Payments

More premium may be needed to fulfill the original goal

Issues You May Uncover

If Under-Funded…

Possible Solutions Increase the future premiums to make up for

the shortfall. Improve underwriting class, if eligible Drop unnecessary riders Decrease face if need has decreased

Problems With These Solutions

Clients may not want to pay more Increased premiums to ILIT’s may create

taxable gifts Reluctance to contribute to policy in

economic environment of low interest rates (UL) or low subaccount growth (VUL)

If Under-Funded…

Problems With These Solutions

If policy has existing loan and client making further loans to make premium and interest payments, problem only becomes worse

Need for current level of insurance remains Desired changes may not be available nor

meet planning objectives

If Under-Funded…

Potential Solutions

Reasons to Keep Current Policy

Surrender of an existing policy may incur a surrender charge; purchase of a new policy would impose yet another surrender schedule

Need for life insurance is temporary Higher guaranteed minimum interest crediting

rates may not be available

Reasons to Keep Current Policy

Adverse health change New contestable and suicide periods Limits on transferring loans Tax consequences Tax benefits issues New acquisition costs

Potential Solutions

Reasons to Consider Exchange or Replacement Company strength – has the existing Insurer had significant recent drops in ratings Extended maturity

Available since @ 1999 New benefits/riders may not be available on older

plans Term insurance getting expensive and need

continues

Potential Solutions

Why a Review?

Secondary No-Lapse Guarantees

Extended Maturity Riders & features

Long Term Care Critical illness

coverage Return of Premium

Estate Tax Repeal Riders/Options

Pref. Plus Underwriting Classes

Policy Loan Provisions

Improved Loan Rates– Zero Net Cost Loans

Policy Options/Benefits Not Previously Available

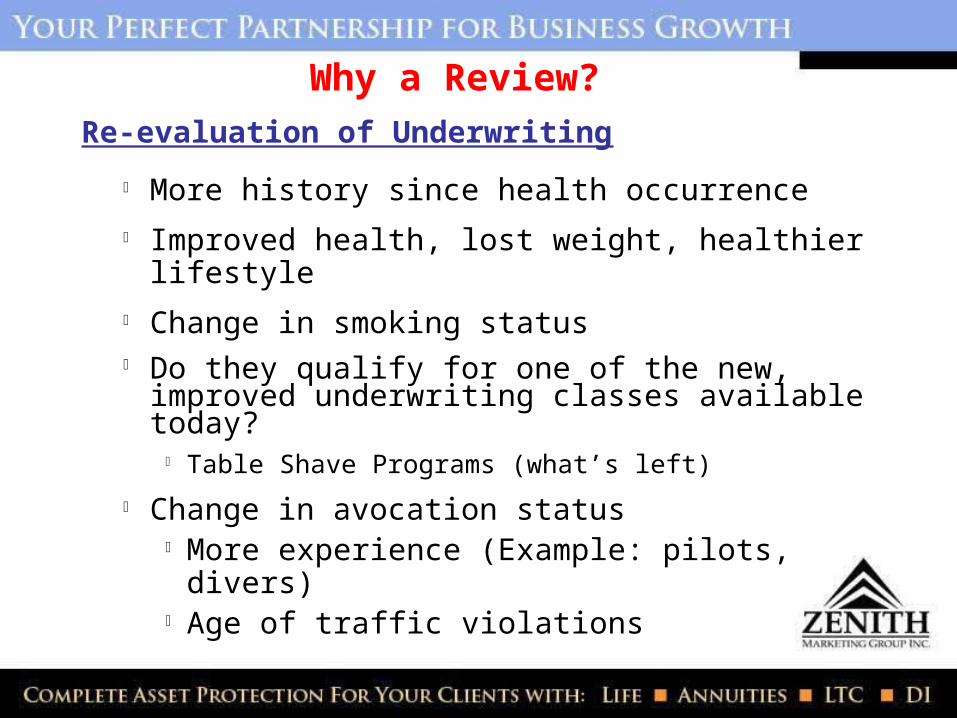

Re-evaluation of Underwriting

More history since health occurrence Improved health, lost weight, healthier lifestyle Change in smoking status Do they qualify for one of the new, improved

underwriting classes available today? Table Shave Programs (what’s left)

Change in avocation status More experience (Example: pilots, divers) Age of traffic violations

Why a Review?

Why Review Now?• Reinsurance – The 800lb. Gorilla

8 Major Reinsurers left in the North American market.

Less Reinsurers = Less Risk Diversification = Higher Pricing and Stricter Underwriting

Very difficult to get exceptions, especially in Preferred and better categories.

Max capacity @ $125 Million Immediate Effect on Ages 70+

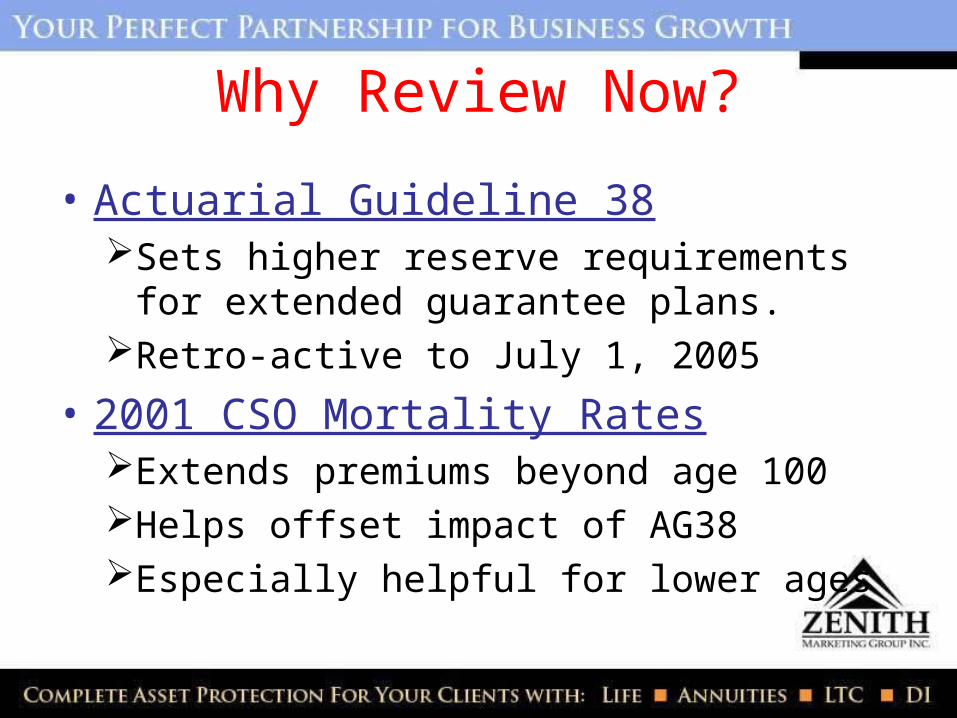

Why Review Now?

• Actuarial Guideline 38Sets higher reserve requirements for

extended guarantee plans.Retro-active to July 1, 2005

• 2001 CSO Mortality RatesExtends premiums beyond age 100Helps offset impact of AG38Especially helpful for lower ages

Potential Solutions

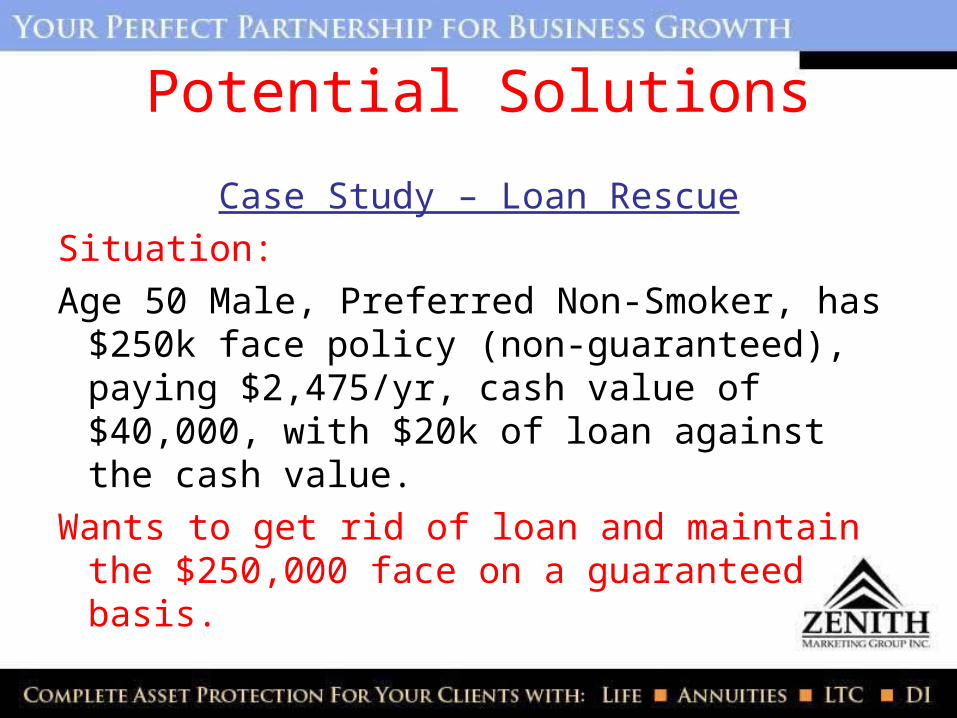

Case Study – Loan Rescue

Situation:

Age 50 Male, Preferred Non-Smoker, has $250k face policy (non-guaranteed), paying $2,475/yr, cash value of $40,000, with $20k of loan against the cash value.

Wants to get rid of loan and maintain the $250,000 face on a guaranteed basis.

Potential Solutions

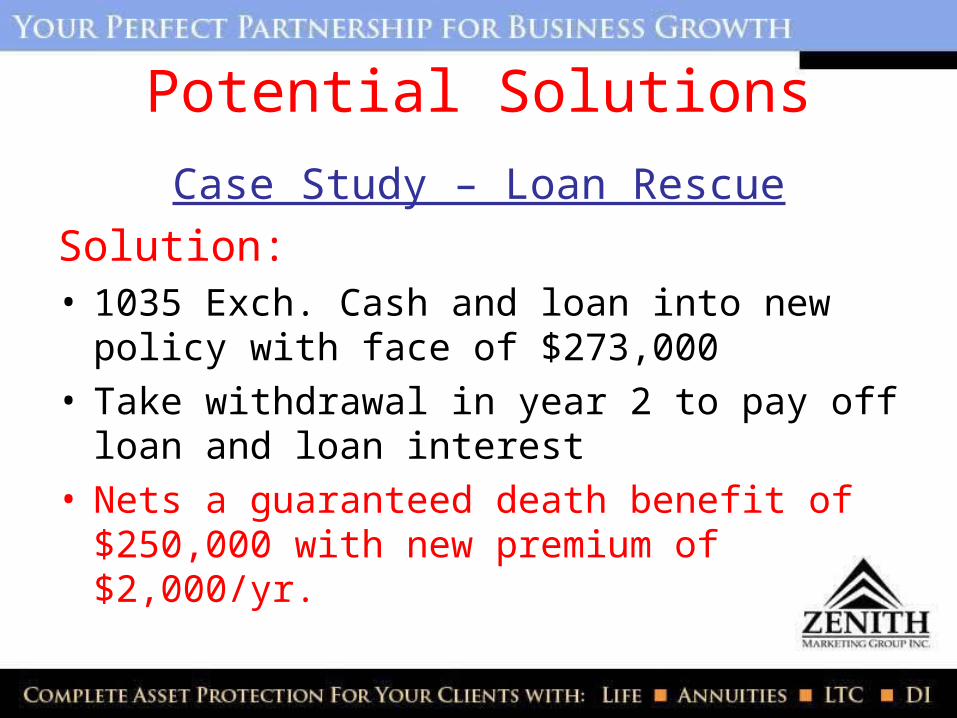

Case Study – Loan Rescue

Solution:• 1035 Exch. Cash and loan into new policy with

face of $273,000• Take withdrawal in year 2 to pay off loan and

loan interest• Nets a guaranteed death benefit of $250,000

with new premium of $2,000/yr.

Jumbo Loan Rollover

• Male, Age 66, SNT, $75M face policy, $25M CV– $12.5M outstanding loan– Policy reprojections show lapse within 5 years

on current factors– Goals: avoid “phantom income” and maintain

net level db of $62.5M• 1035 in Legend 300LR – no loan repayment

Case Study

Jumbo Loan Rollover

Results– Maintained guaranteed net level db of $62.5– No phantom income with guaranteed db!

• Annual Cash outlay to keep guaranteed level death benefit at $62.5M ($75M - $12.5M) = $855,255

• Paid as primarily loan interest ($687,500) + premium $167,755 in years 1-20

Case Study

Potential SolutionsLeveraging Strategies

• Putting Turbo in the 1035Exchange to SPIAOther options:

Installment Refund or Cash Refund to protect principal

Age rated if adverse health conditions

Can be paid directly from carrier to carrier

Potential SolutionsLeveraging Strategies

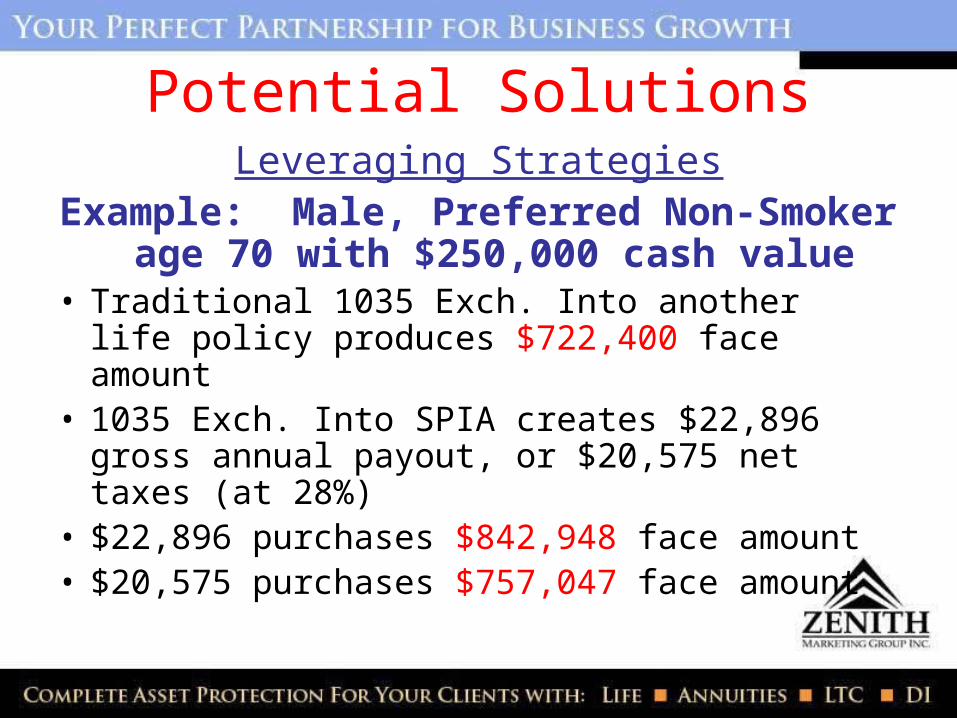

Example: Male, Preferred Non-Smoker age 70 with $250,000 cash value

• Traditional 1035 Exch. Into another life policy produces $722,400 face amount

• 1035 Exch. Into SPIA creates $22,896 gross annual payout, or $20,575 net taxes (at 28%)

• $22,896 purchases $842,948 face amount• $20,575 purchases $757,047 face amount

Potential SolutionsLeveraging Strategies

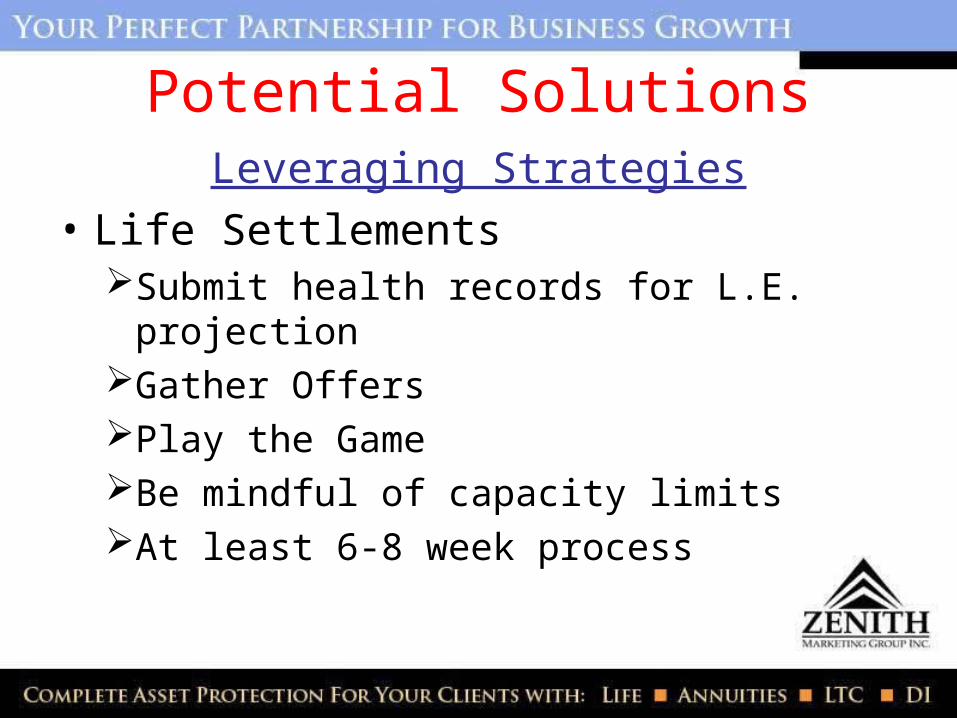

• Life SettlementsSubmit health records for L.E. projectionGather OffersPlay the GameBe mindful of capacity limitsAt least 6-8 week process

The Review Process

The Review Process

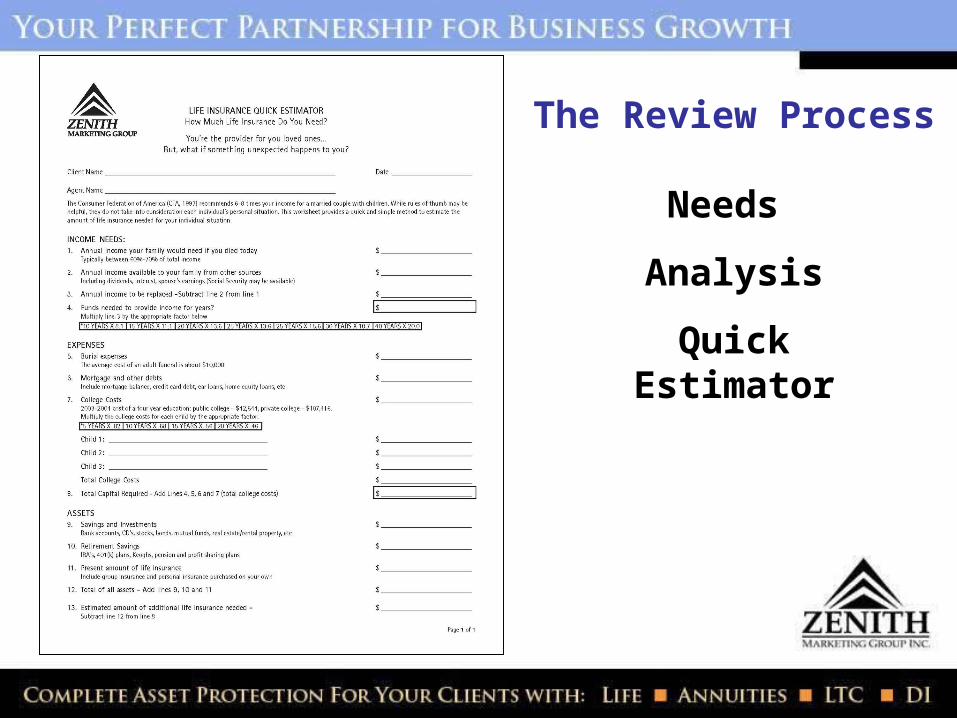

The Review Process

Needs

Analysis

Quick Estimator

The Review Process

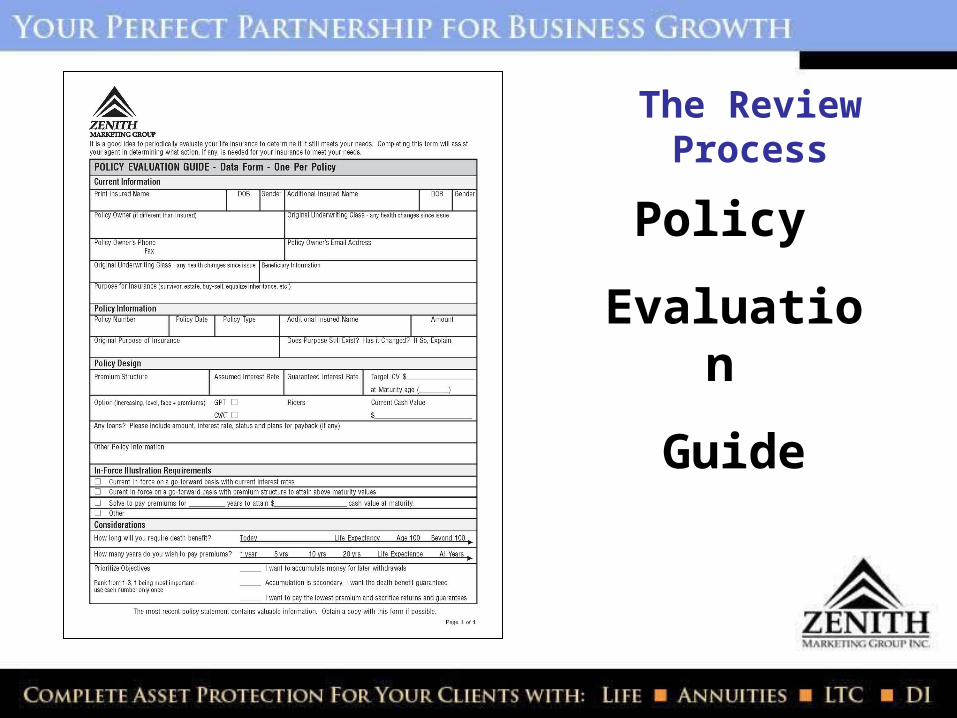

Policy

Evaluation

Guide

The Review Process

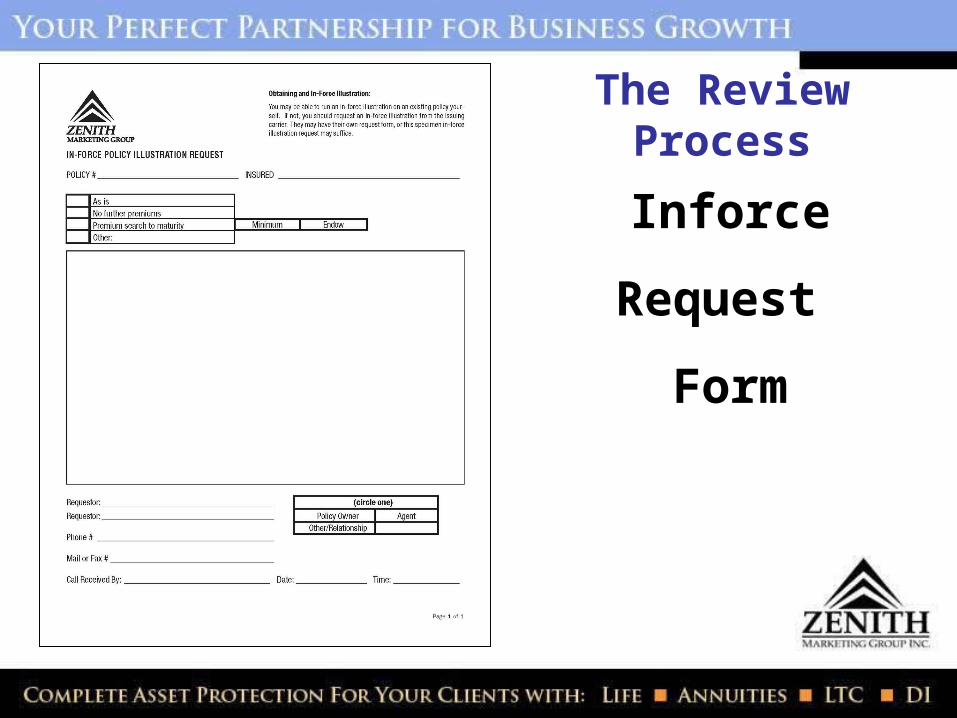

Inforce

Request

Form

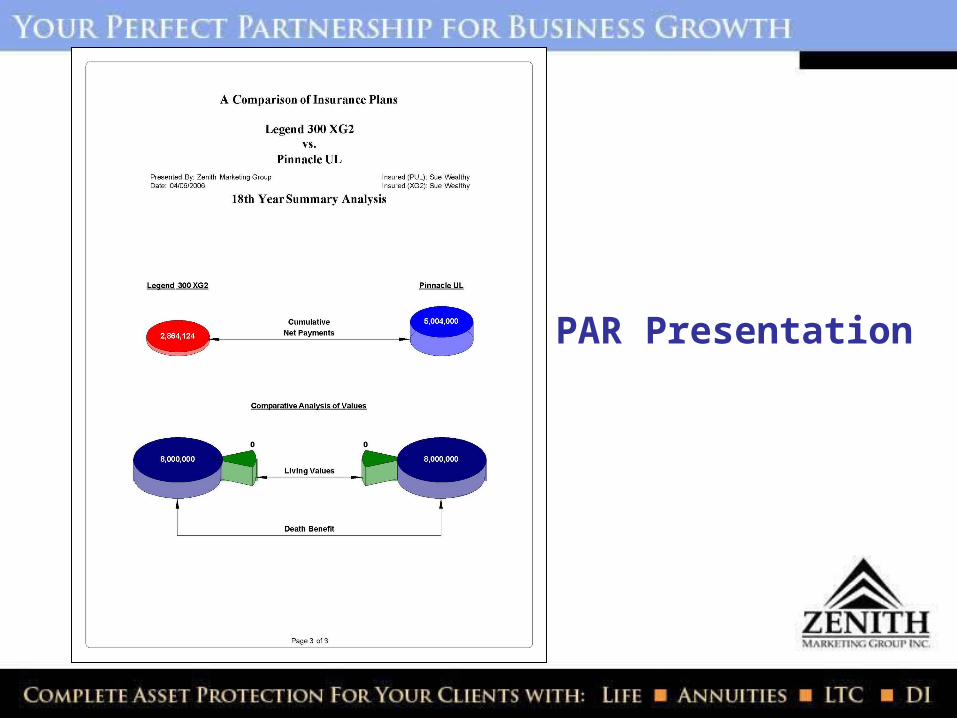

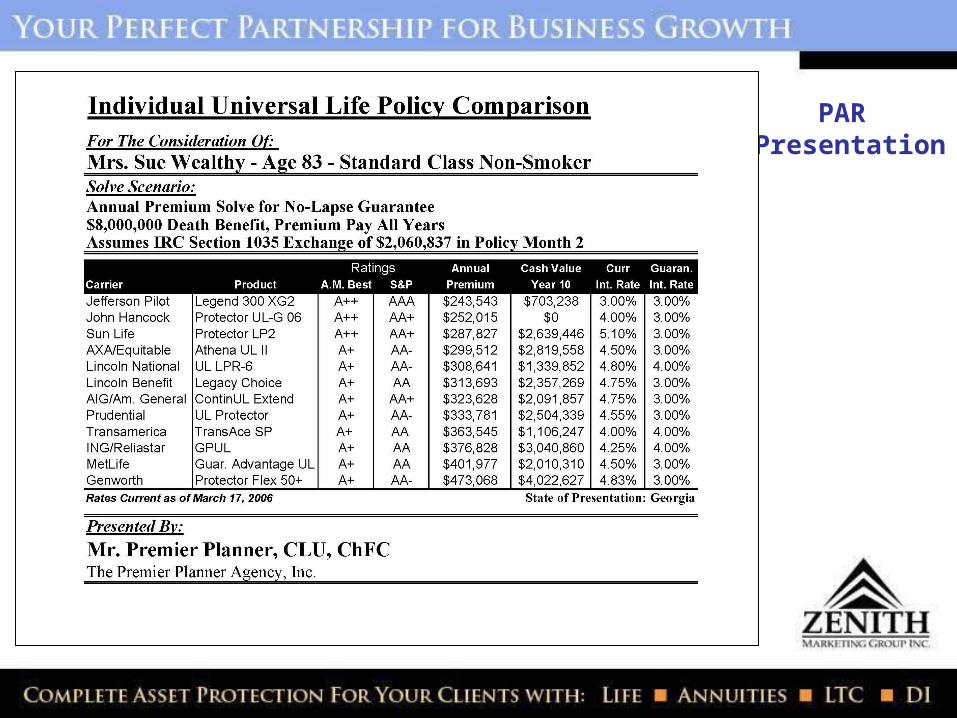

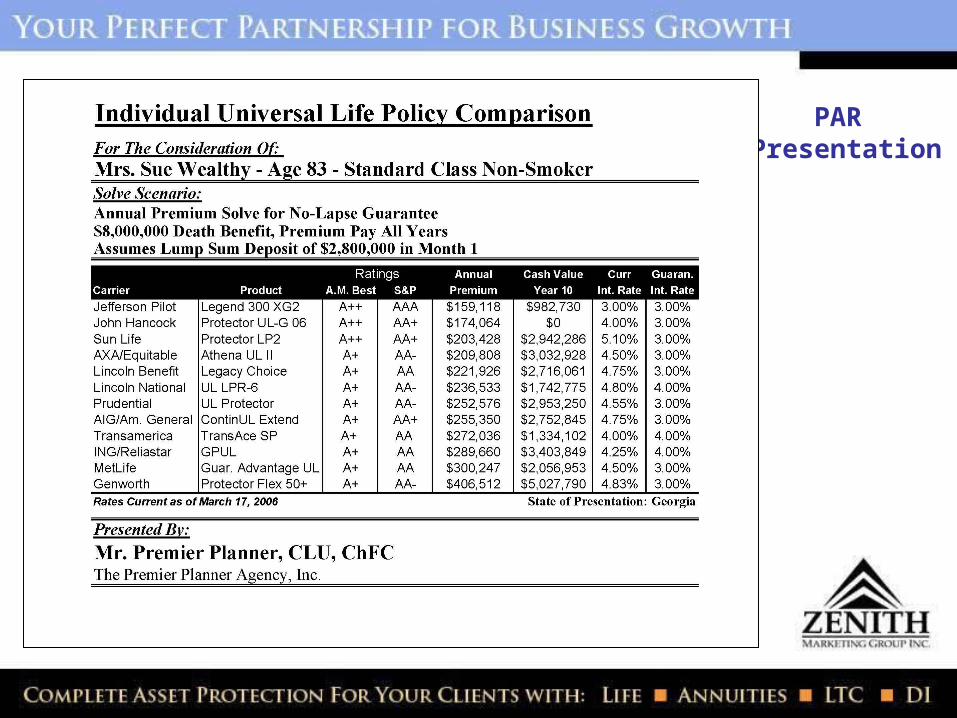

PAR Presentation

PAR Presentation

PAR Presentation

PAR Presentation

PAR Presentation

PAR Presentation

Life Insurance Professional Analysis and Review...

Why offer one?

• Deliver Value → Client satisfaction

• Deliver Value → Client retention

• Deliver Value → More referrals

• Deliver Value → Enhance your professionalism

Life Insurance Professional Analysis and Review…

Ensuring you’re up to PAR.