Embed Size (px)

Citation preview

1

Liberty Tax Service Online

Basic Income Tax Course.

Lesson 16

2

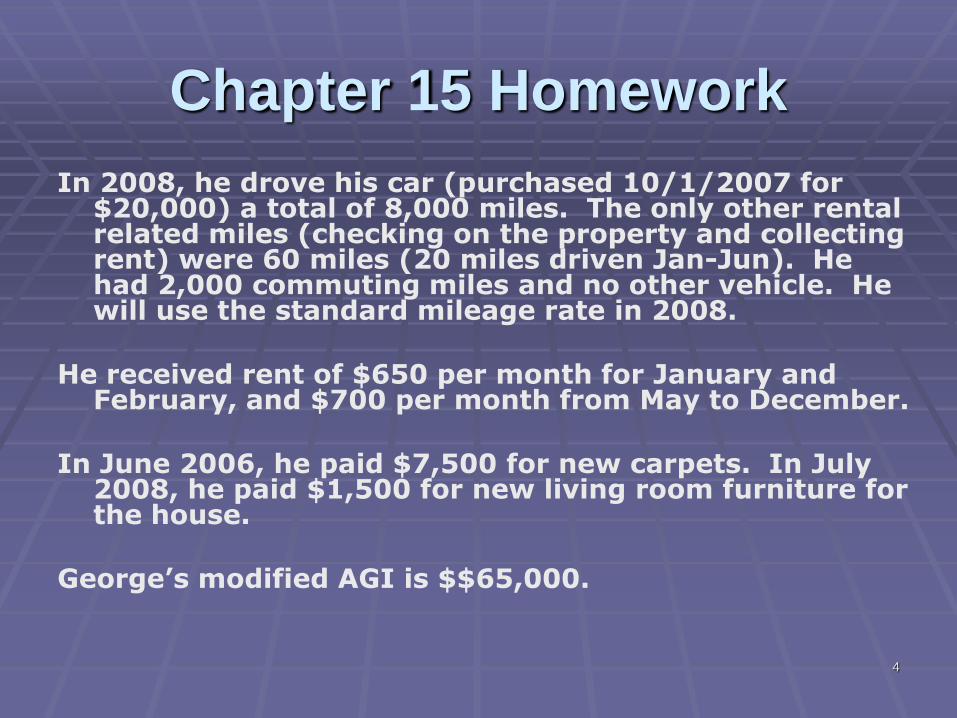

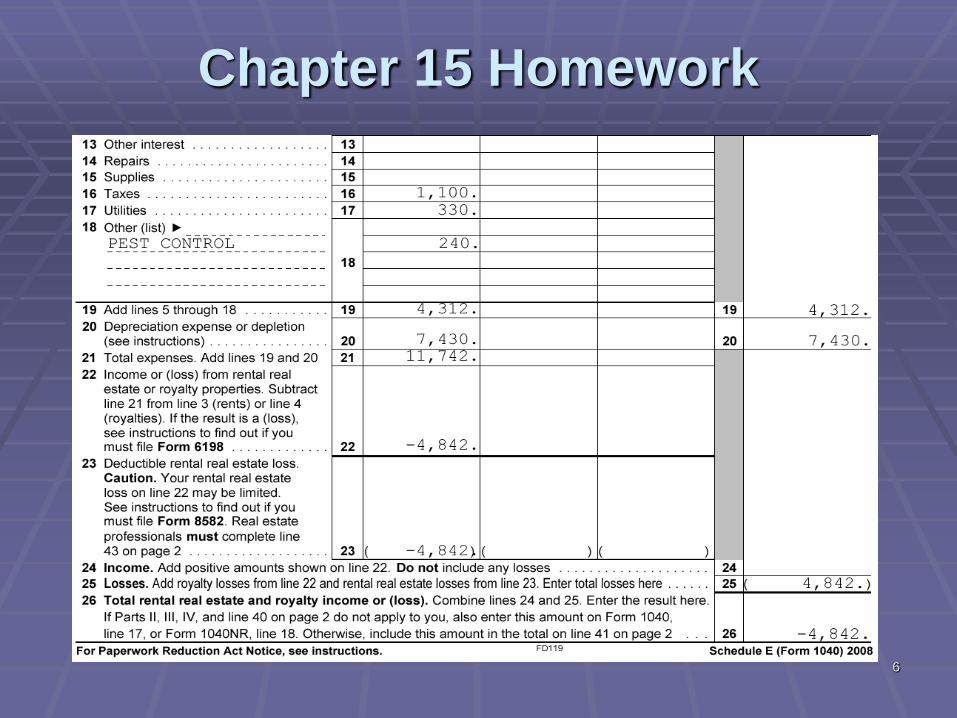

Chapter 15 Homework

HOMEWORK 1: Complete a Schedule E, Form 4562 and a depreciation worksheet for the following:

George B. Brown (SSN 152-22-2111) is single and owns a house that he has been renting out for 5 years. The house is located at 375 M Street, Santa Fe, NM 87501. George purchased the house on March 15, 2004 for $150,000 of which $10,000 was the value of the land.

3

Chapter 15 Homework

In 2008, his expenses are:

• Advertising - $250

• Auto travel to get house ready for new tenant in

April, 2008 - 116 miles

• Pest control - $20 per month

• Insurance - $800 for the year

• Mortgage interest on Form 1098 - $1,375

• Real estate taxes - $1,100

• Utilities while the property was vacant - $330

• Legal fees for new lease - $70

• Tax preparation fee relating to rental property –

$55

4

Chapter 15 Homework

In 2008, he drove his car (purchased 10/1/2007 for $20,000) a total of 8,000 miles. The only other rental related miles (checking on the property and collecting rent) were 60 miles (20 miles driven Jan-Jun). He had 2,000 commuting miles and no other vehicle. He will use the standard mileage rate in 2008.

He received rent of $650 per month for January and February, and $700 per month from May to December.

In June 2006, he paid $7,500 for new carpets. In July 2008, he paid $1,500 for new living room furniture for the house.

George’s modified AGI is $$65,000.

5

Chapter 15 Homework

6

Chapter 15 Homework

7

Chapter 15 Homework

8

Chapter 15 Homework

9

Chapter 15 Homework

10

Chapter 15 Homework

11

Chapter 15 Homework

12

Chapter 15 Homework

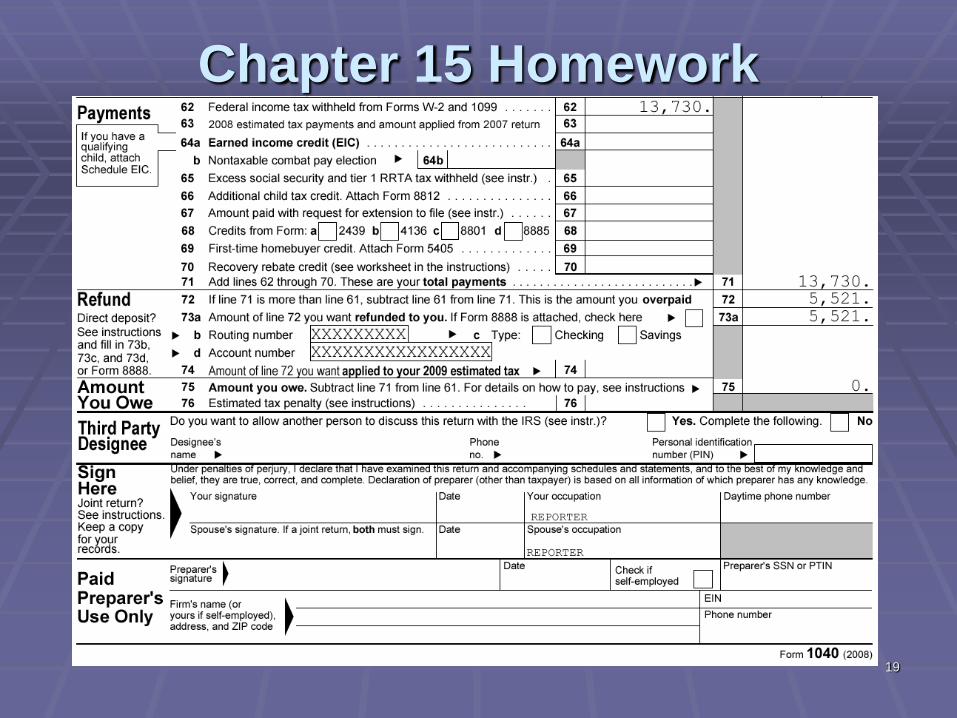

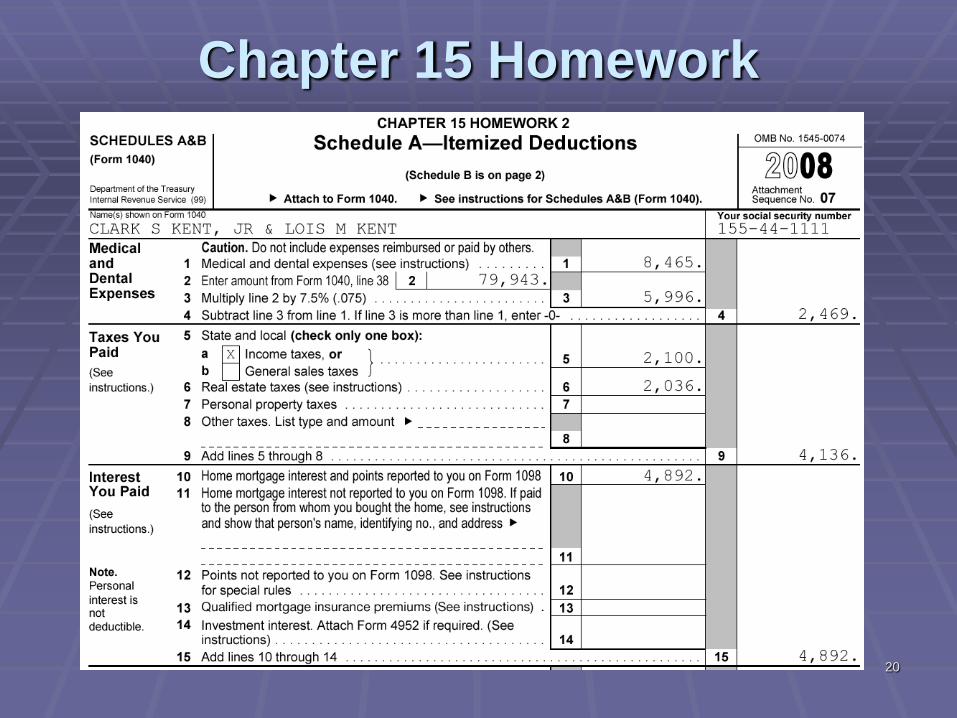

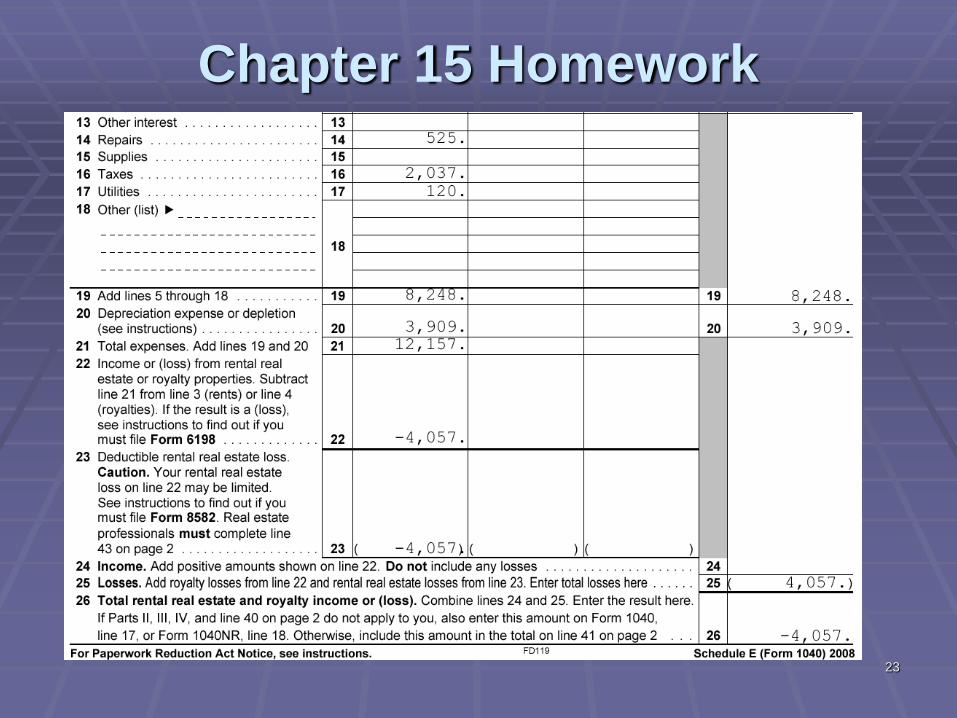

HOMEWORK 2: Clark S. Kent Jr., (born 7/31/1958) owns a duplex where he resides in one half the building and rents the other half. Both units are the same size. He purchased the building on May 12, 2005 for $240,000 (including land value of $25,000).

Clark is married to Lois Marie (born 2/28/1962) and they have no children. Clark and Lois both work as reporters. They will file a joint return and did not itemize their deductions last year.

Clark has a mortgage and the Form 1098 shows $9,785 in interest and $4,073 in real estate taxes paid in 2008.

13

Chapter 15 HomeworkThe address for the rental portion is 1332B Homestead

Lane, Hicksville, NY 10042. The duplex was rented all year for $675 per month. The utilities are paid by the tenant, except for water and sewer. The Kent’s paid $60 per quarter for water and sewer service for both units.

They also pay to have both homes treated by an exterminator for $35 per month. Their homeowner’s insurance costs $925 per year.

The only other expense they had in 2008 for the rental part of their property was a repair on the hot water heater of $525.

In 2008, their out-of -pocket medical expenses were $2,688. They gave $100 per month to their church and one donation of $150 to the Red Cross.

Prepare a 2008 tax return for the Kents.

14

Chapter 15 Homework

15

Chapter 15 Homework

16

Chapter 15 Homework

17

Chapter 15 Homework

18

Chapter 15 Homework

19

Chapter 15 Homework

20

Chapter 15 Homework

21

Chapter 15 Homework

22

Chapter 15 Homework

23

Chapter 15 Homework

24

Chapter 15 Homework

25

Chapter 16: AdjustmentsChapter Content

IRA DeductionStudent Loan Interest DeductionTuition and Fees DeductionMoving ExpensesAdjustments for the Self-Employed

One-Half of Self-Employment TaxKeogh, SEP, and SIMPLE PlansSelf-Employed Health Insurance Deduction

Other AdjustmentsEducator ExpensesPenalty on Early Withdrawal of SavingsAlimony PaidLine 36 AdjustmentsKey Ideas

ObjectivesUnderstand Adjustments and AGI Know How to Figure and Report Adjustments

26

Adjustments

A. Adjustments are deductions from total income taken on lines 23-36 of Form 1040.

B. You do not need to itemize these deductions on Schedule A.

C. Subtracting adjustments from total income results in AGI.

27

IRA DEDUCTION

A. Generally, you can deduct contributions made to a traditional IRA.1. Cannot deduct contributions to 401(k) plan or

Roth IRA as an adjustment to income.2. Contributions are tax-deferred income; taxed

when funds are withdrawn from the IRA.3. Make tax year contributions until the due date of

the tax return.4. Enter on line 32 of Form 1040.

Charlie made a deductible contribution to his IRA on April 12, 2009. Charlie can choose to make this a contribution for 2008 or 2009. If he makes it a 2008 contribution, he can take the IRA deduction as an adjustment on his 2008 tax return.

28

IRA DEDUCTION

Amount You Can Deduct

B. The deduction amount is generally the amount of your contributions.

1. Contributions are limited to the smaller of the amount of your total taxable compensation (earned income and alimony or separate

maintenance payments) or $5,000 ($6,000 if age 50 or over). (See Chapter 9)

29

IRA DEDUCTION

Alice is single and received alimony payments of $1,500. The rest of her income was from interest, dividends and capital gains. Alice’s total income on line 22 of her Form 1040 is $17,000. Her contribution to her traditional IRA is limited to $1,500 (her total income considered to be compensation). Can Alice subtract $1,500 from her total income as an IRA deduction adjustment?

Yes or No?

30

IRA DEDUCTION

Alice is single and received alimony payments of $1,500. The rest of her income was from interest, dividends and capital gains. Alice’s total income on line 22 of her Form 1040 is $17,000. Her contribution to her traditional IRA is limited to $1,500 (her total income considered to be compensation). Can Alice subtract $1,500 from her total income as an IRA deduction adjustment?

Yes

She can subtract $1,500 from her total income as an

IRA deduction adjustment which results in an AGI of

$15,500.

31

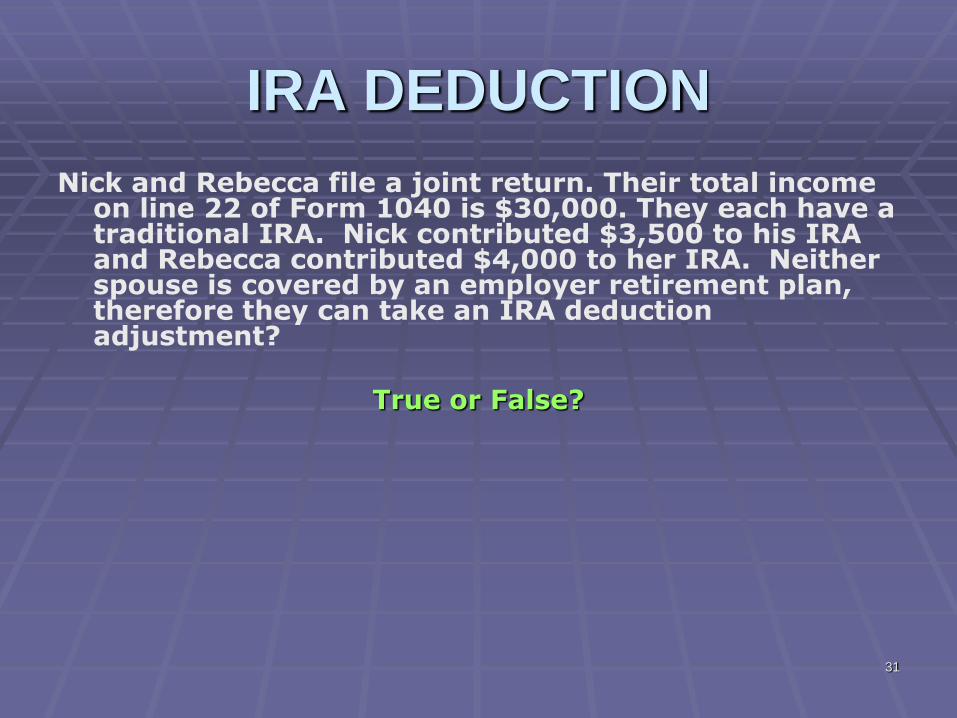

IRA DEDUCTION

Nick and Rebecca file a joint return. Their total income on line 22 of Form 1040 is $30,000. They each have a traditional IRA. Nick contributed $3,500 to his IRA and Rebecca contributed $4,000 to her IRA. Neither spouse is covered by an employer retirement plan, therefore they can take an IRA deduction adjustment?

True or False?

32

IRA DEDUCTION

Nick and Rebecca file a joint return. Their total income on line 22 of Form 1040 is $30,000. They each have a traditional IRA. Nick contributed $3,500 to his IRA and Rebecca contributed $4,000 to her IRA. Neither spouse is covered by an employer retirement plan, therefore they can take an IRA deduction adjustment?

True

They can take an IRA deduction adjustment of $7,500, which results in an AGI of $22,500.

33

IRA DEDUCTION

34

IRA DEDUCTION

Employer Retirement Plans

C. If you (or spouse) are covered by an employer retirement plan, deductible amount is reduced or eliminated depending on filing status and modified

AGI.

1. If you are covered by such a plan, the retirement

plan box in box 13 of your W-2 should be

checked.

2. Refer to Tables 16-1 and 16-2 to see whether you

can take a full deduction, a partial deduction or

no deduction of your IRA contributions.

3. If your deduction is limited, use the IRA Deduction Worksheet in the Form 1040 instructions to

figure the reduced amount of the deduction.

35

IRA DEDUCTION

36

IRA DEDUCTIONUse If You Are Covered By An Employer Retirement Plan

37

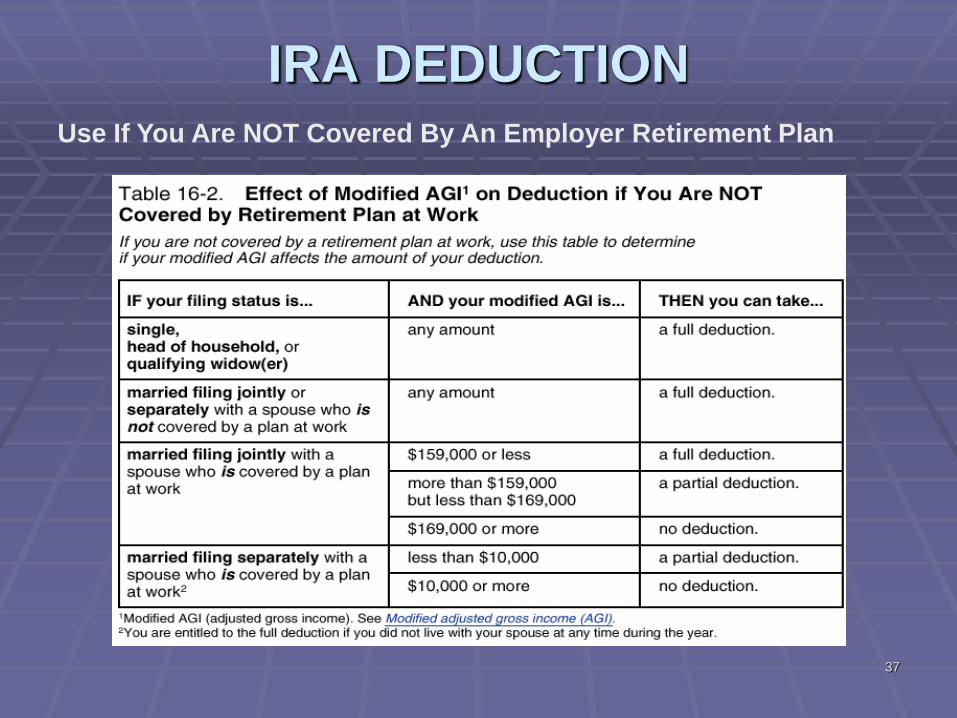

IRA DEDUCTIONUse If You Are NOT Covered By An Employer Retirement Plan

38

IRA DEDUCTION

Chen Hai is single and is covered by a retirement plan at work. His modified AGI is $59,000. Chen contributed $3,000 to his traditional IRA. Is Chen allowed a partial or full deduction as an adjustment

to his AGI?

a. Partial

b. Full

39

IRA DEDUCTION

Chen Hai is single and is covered by a retirement plan at work. His modified AGI is $59,000. Chen contributed $3,000 to his traditional IRA. Is Chen allowed a partial or full deduction as an adjustment

to his AGI?

a. Partial

Because his modified AGI is more than $53,000 but less than $63,000.

40

IRA DEDUCTION

Don and Donna are married and file a joint return. Both are covered by their employers’ retirement plans and both are under age 50. Their modified AGI is $107,000. Don contributed $3,200 to his traditional IRA and Donna contributed $4,000 to hers. How much of a deduction are they allowed?

a. Partial

b. Full

c. None

41

IRA DEDUCTION

Don and Donna are married and file a joint return. Both are covered by their employers’ retirement plans and both are under age 50. Their modified AGI is $107,000. Don contributed $3,200 to his traditional IRA and Donna contributed $4,000 to hers. How much of a deduction are they allowed?

c. None

No deduction is allowed because their modified AGI is $105,000 or more.

42

IRA DEDUCTION

Assume Don’s taxable compensation was $75,000 and Donna earned taxable compensation of $50,000 and she was not covered by a retirement plan at work. Don contributed $2,200 to his traditional IRA and Donna contributed $3,000 to hers.

Their modified AGI is now $125,000. This is less than $159,000, so Donna can deduct the entire $4,000 she contributed to her IRA. Donald’s contributions are not deductible.

Their completed IRA deduction worksheet is on the next slide.

43

IRA DEDUCTION

Donald’s

Answer

44Form 1040, Page 1

IRA DEDUCTION

45

IRA DEDUCTION

Nondeductible ContributionsD. Even if your deduction is reduced or eliminated, you

can still contribute the full permitted amount to your IRA.1. Any part of the contribution you cannot deduct

must be reported on Form 86062. If you do not report nondeductible contributions

on Form 8606, you will be taxed again on these contributions when you withdraw them.

3. Each spouse with a nondeductible contribution must file a separate Form 8606.

4. File Form 8606 even if you do not have to file a tax return.

5. If you do not file Form 8606 when required, you may have to pay a $50 fine.

46

IRA DEDUCTION

Chen Hai is single and is covered by a retirement plan at work. His modified AGI is $59,000. Chen contributed $3,000 to his traditional IRA.

Chen Hai was allowed to deduct $2,000, leaving a nondeductible contribution of $1,000. He must file a Form 8606. In prior years, he also made nondeductible contributions totaling $800. His Form 8606 is shown on the next slide.

47

IRA DEDUCTION

48

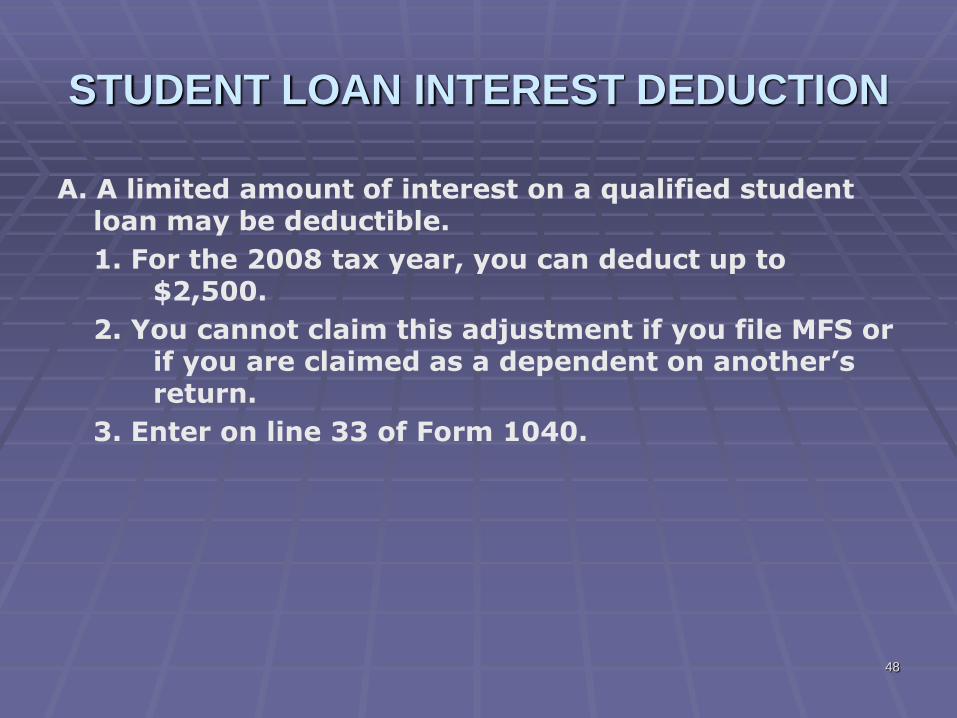

STUDENT LOAN INTEREST DEDUCTION

A. A limited amount of interest on a qualified student loan may be deductible.

1. For the 2008 tax year, you can deduct up to $2,500.

2. You cannot claim this adjustment if you file MFS or if you are claimed as a dependent on another’s return.

3. Enter on line 33 of Form 1040.

49

STUDENT LOAN INTEREST DEDUCTION

Qualified Student LoanB. A qualified student loan is a loan that pays qualified

education expenses at an eligible educational institution for an eligible student.1. The loan must be for you, your spouse, or your

dependent when you took the loan.2. The loan must be used ONLY for qualified

education expenses: tuition, fees, room and board, and other necessary expenses paid to an eligible education institution.

3. The qualified education expenses must be paid within a reasonable period of time before or after you took out the loan.

50

STUDENT LOAN INTEREST DEDUCTION

4. You must reduce expenses by any nontaxable education benefits received.

5. An eligible education institution includes most institutions of higher learning.

6. An eligible student is enrolled in at least 1/2 the normal full-time workload in a program leading to a recognized educational credential (graduate or undergraduate).

51

STUDENT LOAN INTEREST DEDUCTION

Maryanne, an eligible student, took out a personal loan and used part of it to remodel her kitchen and part to pay her qualified education expenses at an eligible educational institution. Can Maryanne take a student loan interest adjustment for this loan?

Yes or No?

52

STUDENT LOAN INTEREST DEDUCTION

Maryanne, an eligible student, took out a personal loan and used part of it to remodel her kitchen and part to pay her qualified education expenses at an eligible educational institution. Can Maryanne take a student loan interest adjustment for this loan?

No

The interest on this loan is not deductible as a student loan interest adjustment because some of the proceeds were used for another purpose.

53

STUDENT LOAN INTEREST DEDUCTION

Income Phase-out

C. The student loan adjustment is reduced or eliminated based on your modified AGI.

1. Refer to Table 16-3 for the income limits on the student loan deduction.

54

Limit on Student Loan Interest Deduction

If your filing status is…

AND your modified AGI is…

THEN…

Single, head of household, or qualifying widow(er)

Not more than $55,000

You can deduct all your interest, up to $2,500.

More than $55,000, but less than $70,000

Your deduction is limited.

$70,000 or more You cannot claim this deduction.

Married filing jointly

Not more than $115,000

You can deduct all your interest, up to $2,500.

More than $115,000 but less than $145,000

Your deduction is limited.

$145,000 or more You cannot claim this deduction.

Table 16-3

55

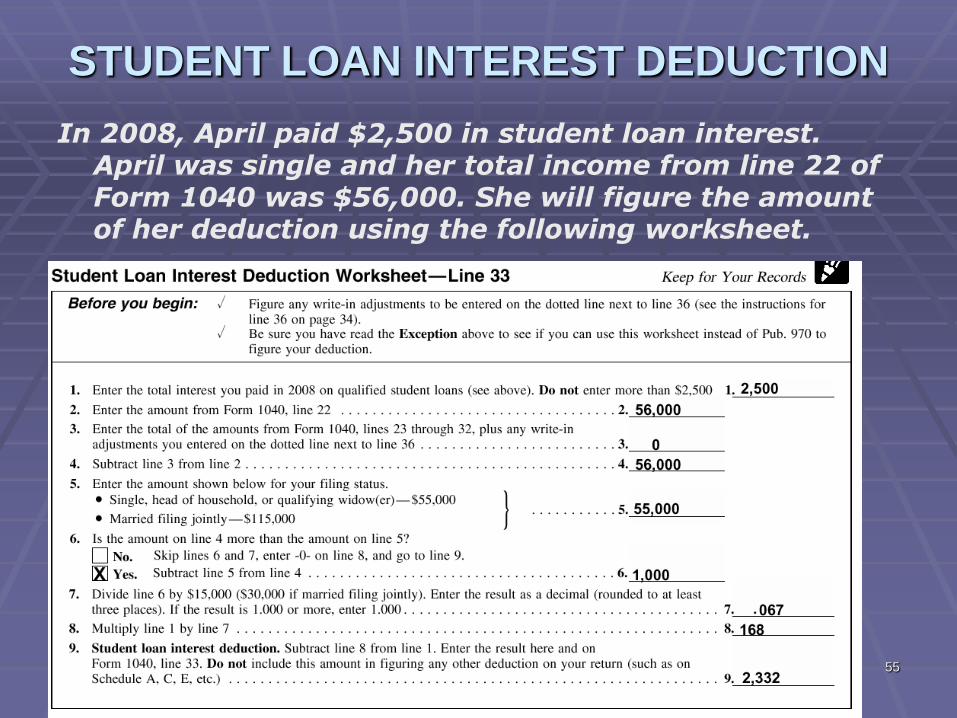

STUDENT LOAN INTEREST DEDUCTION

In 2008, April paid $2,500 in student loan interest. April was single and her total income from line 22 of Form 1040 was $56,000. She will figure the amount of her deduction using the following worksheet.

56

TUITION AND FEES DEDUCTION

A. Can take this deduction only if all of the following apply:1. You paid qualified tuition for yourself, your spouse

or your dependent(s).2. Your filing status is any status except MFS.3. Your MAGI is not more than $160,000 for MFJ and

not more than $80,000 for all other filing statuses.

4. You cannot be claimed as a dependent on another’s return.

5. You are not claiming an education credit for the same student.

57

TUITION AND FEES DEDUCTION

B. Qualified tuition and fees must be required for student attending an eligible educational institute but DO NOT include any of the following:1. Amounts paid for room and board, medical

transportation or similar personal or family expenses.

2. Amounts paid for course-related books, supplies, equipment and nonacademic activities unless paid to the institution as a condition of enrollment or attendance.

3. Amounts paid for sports, games etc., unless part of student’s degree program.

C. The deduction is computed on Form 8917, Tuition and Fees Deduction and enter on line 34 of Form 1040.

58

TUITION AND FEES DEDUCTION

59

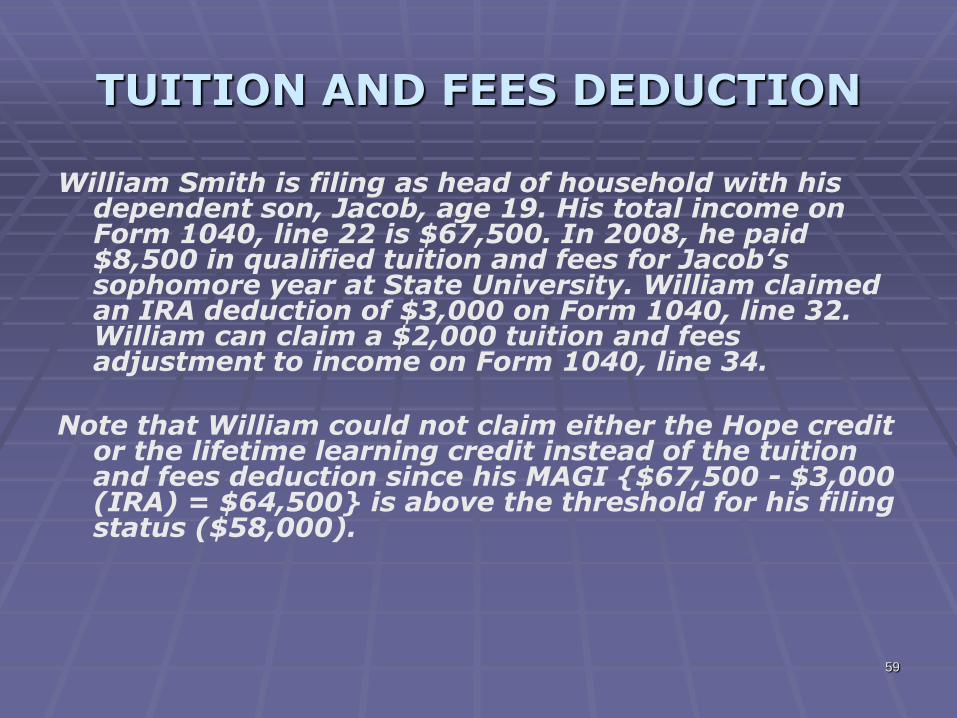

TUITION AND FEES DEDUCTION

William Smith is filing as head of household with his dependent son, Jacob, age 19. His total income on Form 1040, line 22 is $67,500. In 2008, he paid $8,500 in qualified tuition and fees for Jacob’s sophomore year at State University. William claimed an IRA deduction of $3,000 on Form 1040, line 32. William can claim a $2,000 tuition and fees adjustment to income on Form 1040, line 34.

Note that William could not claim either the Hope credit or the lifetime learning credit instead of the tuition and fees deduction since his MAGI {$67,500 - $3,000 (IRA) = $64,500} is above the threshold for his filing status ($58,000).

60

TUITION AND FEES DEDUCTION

61

MOVING EXPENSES

A. You can deduct some of your expenses related to moving because you changed job locations or started a new job.

1. Determine if the move qualifies for the adjustment.

2. Determine which expenses are deductible and the amount of the deduction.

3. Enter on line 26 of Form 1040.

62

MOVING EXPENSES

Requirements For A Qualified Move

To qualify for this deduction, your move must be closely related to starting your new job, your new main job location must be a required distance from your former home, and you must work a required number of weeks.

These requirements are known as the relationship test, the distance test and the time test.

63

MOVING EXPENSES

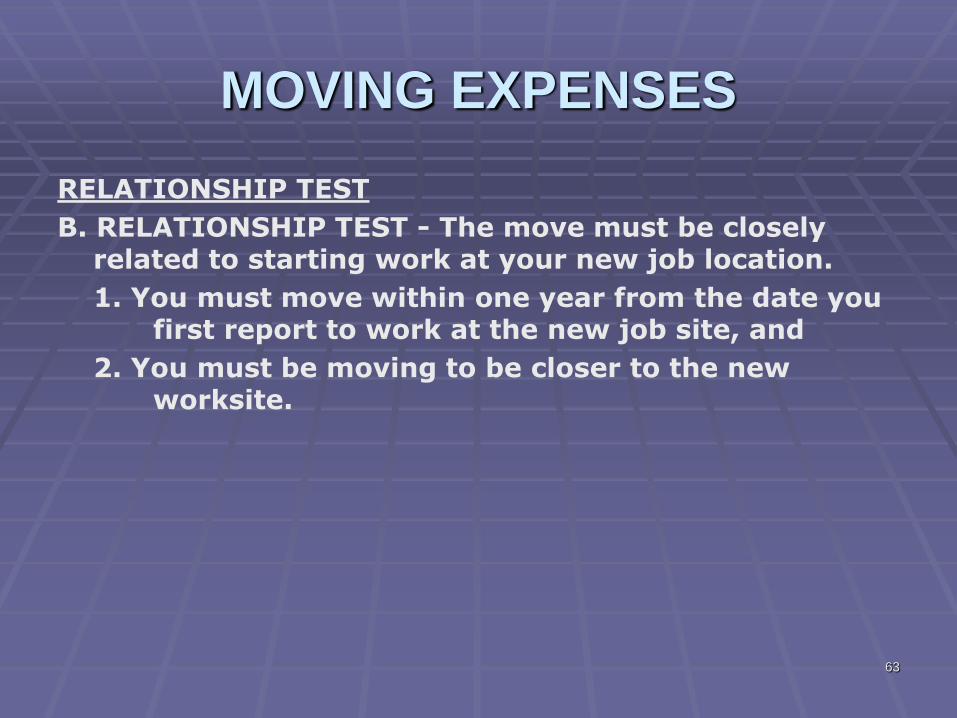

RELATIONSHIP TEST

B. RELATIONSHIP TEST - The move must be closely related to starting work at your new job location.

1. You must move within one year from the date you first report to work at the new job site, and

2. You must be moving to be closer to the new worksite.

64

MOVING EXPENSES

Maggie started a new job at Palm Industries on June 1, 2007. She moved in August 2008 from Johnson City to Thorn Village. Because she did not move within one year from the day she first reported to work at her new job location, her move does not qualifyfor the adjustment and she cannot deduct her moving expenses.

65

MOVING EXPENSES

Suppose Maggie moved to her new home in February 2008. Her former home in Johnson City is 54 miles from her new job. Her new home in Thorn Village is 57 miles from her new job. Does Maggie’s move meet the relationship test?

Yes or No?

66

MOVING EXPENSES

Suppose Maggie moved to her new home in February 2008. Her former home in Johnson City is 54 miles from her new job. Her new home in Thorn Village is 57 miles from her new job. Does Maggie’s move meet the relationship test?

No

Because her new home is farther from her new job location than her old home, her move does not meet the relationship test and Maggie cannot deduct her moving expenses.

67

MOVING EXPENSES

DISTANCE TEST

C. DISTANCE TEST - The move must decrease your commuting distance to the new job location by 50 miles or more.

1. Your new job location must be at least 50 miles farther from your former home than your old job location was from your former home.

2. Table 16-4 illustrates the distance test.

68

MOVING EXPENSES

Now suppose Maggie’s move has passed the relationship test. Her old job at Bayshore Industries was located 3 miles from her old home. Her new workplace at Palm Incorporated is 54 miles from herold home. 54 - 3 = 51. Her old home is at least 50 miles farther from her new workplace than from her old workplace so she meets the distance test.

Note: The location of your new home does not enter into this calculation. You do not have to move 50 miles from your old home to pass this test.

In the above example, Maggie’s new home in Thorn City is 40 miles from her former home. As long as her former home is at least 53 miles from her new job location, she meets the distance test.

69

MOVING EXPENSES

70

MOVING EXPENSES

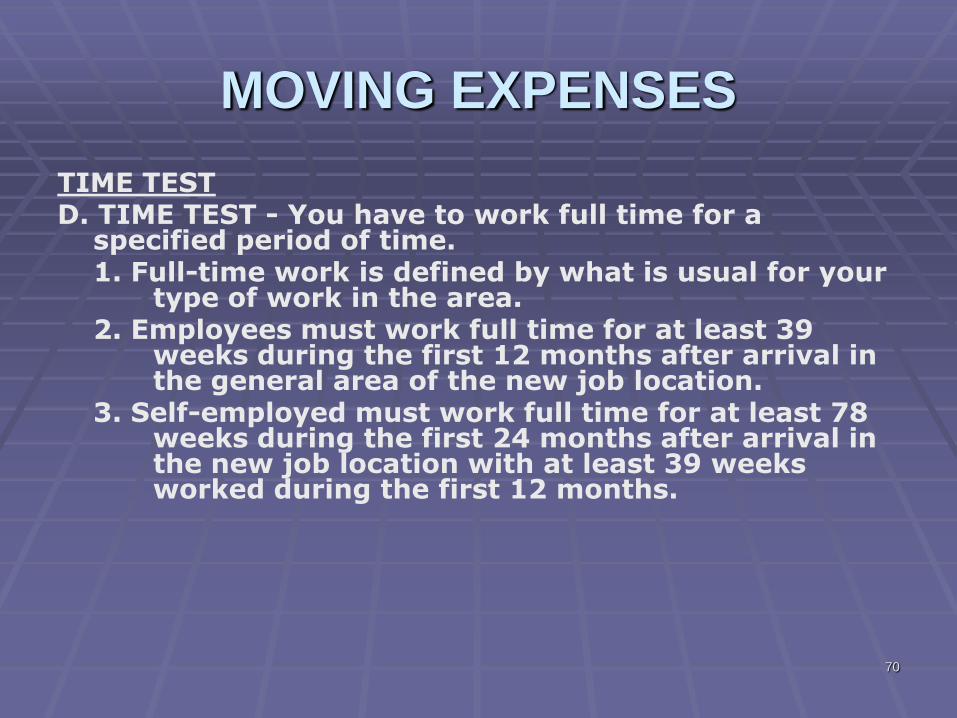

TIME TESTD. TIME TEST - You have to work full time for a

specified period of time.1. Full-time work is defined by what is usual for your

type of work in the area.2. Employees must work full time for at least 39

weeks during the first 12 months after arrival in the general area of the new job location.

3. Self-employed must work full time for at least 78 weeks during the first 24 months after arrival in the new job location with at least 39 weeks worked during the first 12 months.

71

MOVING EXPENSES

4. Refer to Table 16-5 for time test requirements if you are both an employee and self-employed.

72

MOVING EXPENSES

After she moved on February 1, 2008, Maggie worked 30 weeks for Palm Industries as a full-time employee. She then quit to become a self-employed consultant. For her move to qualify for the deduction, she must work full time another 48 weeks beforeFebruary 1, 2010. Nine of those weeks must be worked before February 1, 2009.

73

MOVING EXPENSES

5. If you are MFJ, either spouse can satisfy the time test by working full time for the required number of weeks.

6. You cannot combine the weeks you and your spouse work to meet this test.

Your move in December 2008 meets the relationship and distance tests. By April 15, 2009, you have worked full time at your new job for 16 weeks. You expect to work full time at least 39 weeks before December 2009. You can claim the moving expenses adjustment on your 2008 tax return.

74

MOVING EXPENSES

Deductible Moving ExpensesE. Deductible moving expenses are the reasonable

expenses (directly related to the move) of moving your personal effects and household goods and of traveling.1. Packing, crating, and shipping your household

goods and personal effects to your new home.2. Storing and insuring your goods and effects within

a period of 30 consecutive days after the day your things are moved from your former home and before they are delivered to your new home.

3. Connecting and disconnecting utilities.4. Shipping your car and household pets to your new

home.

75

MOVING EXPENSES

5. Transportation and lodging while you travel from your former home to your new home, including expenses on the day of arrival.

6. Lodging in the area of your former home within one day after your furniture has been moved out.

7. Car expenses of either actual expenses (not including depreciation, repairs, or insurance) or 18 cents a mile.

8. Parking fees and tolls paid while traveling to your new home whether you use actual expenses or mileage.

76

MOVING EXPENSES

F. Many items related to your move are not deductible.1. Purchase price of your new house2. Loss on the sale of your former home3. Expenses of buying or selling a home4. Meal expenses5. Pre-move house hunting expenses6. Security deposits7. Temporary living expenses8. Expenses of entering into or breaking a lease9. Home improvements to help sell your house10. Security deposits (including any given up due to

the move)11. Driver’s license and car tags 12. Mortgage penalties 13. Return trips to former residence

77

MOVING EXPENSES

Figuring The Amount Of The Deduction

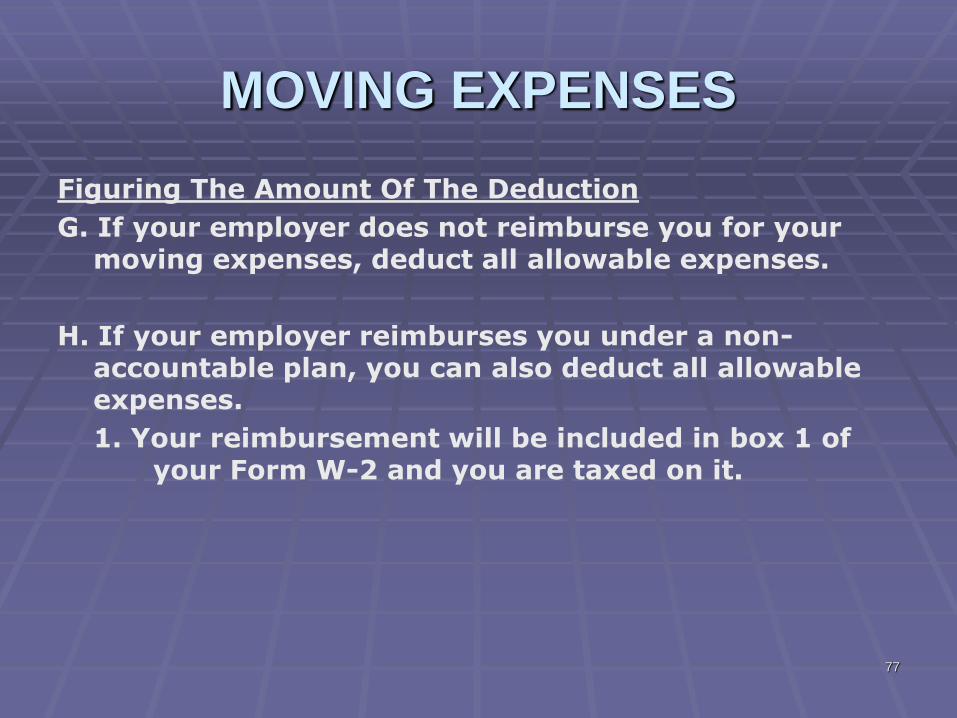

G. If your employer does not reimburse you for your moving expenses, deduct all allowable expenses.

H. If your employer reimburses you under a non-accountable plan, you can also deduct all allowable expenses.

1. Your reimbursement will be included in box 1 of your Form W-2 and you are taxed on it.

78

MOVING EXPENSES

I. If you are reimbursed under an accountable plan, you can deduct only those expenses that are in excess of the reimbursement amount.1. Reimbursement is excluded from taxable income.2. Amount excluded usually shown in box 12 of the

W-2 with the letter P.3. If your expenses are less than the reimbursement,

report the difference as income on line 7 of Form1040.

J. Use Form 3903 to figure and report your moving expenses.

79

MOVING EXPENSES

In the example shown below, the taxpayer was not reimbursed so all his deductible costs can be taken as an adjustment to income.

Carson’s move to be near his new job location on September 15, 2008 and has met all three tests. He paid $4,000 to pack and ship his household goods to his new home. The total fees for connecting anddisconnecting his utilities were $250. The $250 is considered a cost related to moving his household goods and personal effects. He drove his car 800 miles to his new home. He uses the mileage rate of 27 cents a mile. His motel bill while traveling to his new home was $89. He also paid tolls totaling $22.

80

MOVING EXPENSES

81

ADJUSTMENTS FOR THE SELF-EMPLOYED

A. These adjustments can only be claimed if you are self-employed.

One Half Of Self-Employment TaxB. You can deduct one half of self-employment tax you

owe.1. Self-employment tax is figured on Schedule SE.2. Enter the amount from line 6 or 13 of Schedule

SE on line 27 of Form 1040.3. There is no limit to the amount you can deduct.

82

ADJUSTMENTS FOR THE SELF-EMPLOYED

Self-Employed Health Insurance DeductionC. If you pay health insurance premiums for a plan

established under your business, you may be able to deduct part of the premiums paid for yourself, your spouse or your dependents.1. Must have had a net profit for the year.2. Cannot deduct premiums for any month that you

(or spouse) were eligible to participate in an employer-paid health plan.

3. Can include long-term care premiums up to the lesser of the amount you pay or set amounts based on your age.

83

ADJUSTMENTS FOR THE SELF-EMPLOYED

Jack owns his own business and pays premiums for health insurance for himself and his wife Jill to a plan established under his business. Jill was unemployed until August 2008. On August 1, she began work with an employer who provided health insurance. Jill became eligible to receive the health insurance benefit on September 1, 2008 and enrolled in the plan. To figure his deduction, Jack can use the premiums he paid from January through September 2008.

True or False?

84

ADJUSTMENTS FOR THE SELF-EMPLOYED

Jack owns his own business and pays premiums for health insurance for himself and his wife Jill to a plan established under his business. Jill was unemployed until August 2008. On August 1, she began work with an employer who provided health insurance. Jill became eligible to receive the health insurance benefit on September 1, 2008 and enrolled in the plan. To figure his deduction, Jack can use the premiums he paid from January through September 2008.

False

He an use only the premiums he paid from January through August 2008.

85

ADJUSTMENTS FOR THE SELF-EMPLOYED

4. Deduction is limited to the smaller of 100% of the cost of the premiums or your net profit minus adjustments taken on lines 27 and 28 of Form 1040.

5. Figure the deduction on the worksheet in the Form 1040 instructions and enter the result on line 29 of Form 1040.

6. Any amount you cannot take as an adjustment is deductible as a medical expense deduction on Schedule A.

86

ADJUSTMENTS FOR THE SELF-EMPLOYED

Jamie owns a lawn care business. His net profit in 2008 was $20,000. His self-employment tax is $2,826. He paid $3,000 in premiums for his health insurance in 2008. Jamie will use the following worksheet to figure the amount of the premiums he can deduct. Note that on line 2 of the worksheet, he must reduce his net profit by any deductions he claims on Form 1040, lines 27 and 28; in this case, by 50% of his self-employment tax {$20,000 – ($2,826 x 50%) = $18,587}.

87

ADJUSTMENTS FOR THE SELF-EMPLOYED

88

ADJUSTMENTS FOR THE SELF-EMPLOYED

Keogh and Self-Employed SEP and SIMPLE Plans

D. Contributions to Keogh and self-employed SEP and SIMPLE retirement plans are deductible.

1. These are retirement plans for small business owners.

2. Each plan has different contribution and deduction rules.

3. The amount you can deduct depends on the plan you have.

4. Enter on line 28 of Form 1040.

5. See Publication 560 for more information.

89

OTHER ADJUSTMENTS

These adjustments are either easy to figure or do not apply to many taxpayers.

Educator Expenses

Qualified education expenses of up to $250 can be deducted on line 23 of Form 1040 by an eligible educator.

90

OTHER ADJUSTMENTS

Penalty On Early Withdrawal Of SavingsThe interest penalty charged by a financial institution

for early withdrawal of savings from a time deposit account is deductible.1. Report the entire amount of interest earned

shown in box 1 of Form 1099-INT as income on line 8a of Form 1040.

2. The interest penalty is shown in box 2 of Form 1099-INT.

3. Enter the box 2 amount on line 30 of Form 1040.4. There is no limit on the amount you can deduct.

91

OTHER ADJUSTMENTS

92

OTHER ADJUSTMENTS

Alimony PaidYou can deduct any payments you make to or on behalf

of a spouse or former spouse, if your spouse must report the payments as alimony income.1. See Chapter 5 for a discussion of alimony.2. Enter the amount of your payments on line 31a of

Form 1040.3. Enter the recipient’s social security number on line

31b.4. There is no limit to the amount you can deduct.

93

OTHER ADJUSTMENTS

Line 36 Adjustments

E. There are a number of other deductions you are allowed to include in the total on line 36 of Form 1040.

1. Enter the amount of the adjustment and identify it on the dotted line next to line 36.

2. Form 1040 instructions list these adjustments and refer you to the applicable form or publication.

94

Adjustments

KEY IDEAS

♦ Adjustments are certain amounts you are allowed to deduct from your total income. The result is adjusted gross income (AGI).

♦ If you (and your spouse) are not covered by an employee retirement plan at work, your entire contribution to a traditional IRA, up to $5,000 ($6,000 if age 50 or older), is deductible as an adjustment regardless of your modified AGI.

♦ If you (or your spouse) are covered by an employer retirement plan at work, all, part, or none of your contributions to a traditional IRA are deductible dependingon your modified AGI and filing status.

95

Adjustments

KEY IDEAS

♦ Up to $2,500 of qualified student loan interest is deductible as an adjustment.

♦ Up to $4,000 of qualified tuition and fees is deductible as an adjustment

♦ To qualify for the moving expense adjustment, your move must be closely related to the start of work, your new main job location must be at least a required distance from your former home, and you must work a required number of weeks after arriving at your new job location.

♦ If you are self-employed, you can deduct half your self-employment tax as an adjustment. You may also be able to deduct 100% of your health insurance costs and certain contributions to small business retirement plans.

96

Adjustments

CLASSWORK 1: True or False.

(1) Pauline is single. Her modified AGI is $60,000. She is covered by her employer’s retirement plan. In 2008, she contributed $4,000 to her traditional IRA. No part of this contribution is deductible.

(2) Cam, age 25, contributed $2,000 of his wages to his traditional IRA in December 2008. In March 2009, he contributed an additional $2,000. He is not covered by an employer retirement plan. Cam can deduct $4,000 on his 2008 tax return.

(3) Ferris is making payments to his former wife under a divorce decree. Under the terms of the decree, Ferris can stop making payments when their son reaches age 21. Ferris cannot deduct these payments as alimony.

97

Adjustments

CLASSWORK 1: True or False.

(4) Janis took out a student loan in 2006. She was not required to begin monthly payments until June 1, 2007. She is single and her AGI is $55,000. Janis can deduct as an adjustment the full $4,500 in interest she paid on her loan in 2008.

(5) In August 2007, Suzette got a new job. Instead of commuting 2 miles as she did to her old job, she now had to drive 54 miles to her new job. In September 2008 she moved to a new home that was closer to her new job location. Suzette will be able to deduct the reasonable costs of her move as an adjustment on her 2008tax return.

(6) In 2008, Mr. Kramer took out a home equity loan to pay for his son’s qualified education expenses. Mr. Kramer also used part of the loan to buy a new car. He can deduct, as an adjustment on line 33 of his Form 1040, the interest on the part of the loan that he used for education expenses.

98

Adjustments

CLASSWORK 1: True or False.

(7) If you are self-employed and you and your spouse were noteligible to participate in an employer paid health plan, the entirecost of your health insurance premiums for a plan establishedunder your business may be deductible as an adjustment toincome on line 29 of Form 1040.

(8) In 2008, Anthony and Virginia each contributed to a traditionalIRA. Both are covered by retirement plans at work. Their filingstatus is MFJ and their modified AGI is $102,000. To report theirnondeductible IRA contributions, they will file one Form 8606.

(9) In January 2008, Edgar got a new job and moved to a new homecloser to the new job location. Edgar’s move met the relationshipand distance tests. In November 2008, Edgar was laid off and hebecame a self-employed consultant. Edgar must now meet the78-week time test for self-employed persons.

99

Adjustments

CLASSWORK 1: True or False.

(10) Liza does not report any income on line 7 of her Form 1040. Her total income is from interest, dividends and alimony payments. She cannot contribute to a traditional IRA.

(11) The amount of a penalty on early withdrawal of savings that you can deduct is reduced or limited as your modified AGI increases.

(12) If you are self-employed and had a net profit in 2008, you may be able to deduct, as an adjustment to income, up to 70% of the amount paid for health insurance on behalf of you, your spouse, and dependents. The plan must be established under your business.

100

Adjustments

CLASSWORK 1: True or False.

(13) Sid’s net profit from self-employment reduced by his deduction on line 27 for ½ his self-employment tax is $2,600. His deduction on line 29 for self-employed health insurance cannot exceed $2,600.

(14) If you choose to use the standard mileage rate rather than actual car expenses, you cannot deduct your parking fees and tolls as moving expenses.

(15) You can claim a deduction for qualified tuition and fees that you paid for with the proceeds from a loan.

(16) Jim is a sophomore at State U’s degree program in dentistry. In addition to tuition, he is required to pay a fee to the University for the rental of dental equipment he will use in this program. The equipment fee is a qualified related expense for the purpose of the tuition and fees deduction.

101

Adjustments

CLASSWORK 1: True or False.

(1) Pauline is single. Her modified AGI is $60,000. She is covered by her employer’s retirement plan. In 2008, she contributed $4,000 to her traditional IRA. No part of this contribution is deductible. F

(2) Cam, age 25, contributed $2,000 of his wages to his traditional IRA in December 2008. In March 2009, he contributed an additional $2,000. He is not covered by an employer retirement plan. Cam can deduct $4,000 on his 2008 tax return. T

(3) Ferris is making payments to his former wife under a divorce decree. Under the terms of the decree, Ferris can stop making payments when their son reaches age 21. Ferris cannot deduct these payments as alimony. T

102

Adjustments

CLASSWORK 1: True or False.

(4) Janis took out a student loan in 2006. She was not required to begin monthly payments until June 1, 2007. She is single and her AGI is $55,000. Janis can deduct as an adjustment the full $4,500 in interest she paid on her loan in 2008. F

(5) In August 2007, Suzette got a new job. Instead of commuting 2 miles as she did to her old job, she now had to drive 54 miles to her new job. In September 2008 she moved to a new home that was closer to her new job location. Suzette will be able to deduct the reasonable costs of her move as an adjustment on her 2008tax return. F

(6) In 2008, Mr. Kramer took out a home equity loan to pay for his son’s qualified education expenses. Mr. Kramer also used part of the loan to buy a new car. He can deduct, as an adjustment on line 33 of his Form 1040, the interest on the part of the loan that he used for education expenses. F

103

Adjustments

CLASSWORK 1: True or False.

(7) If you are self-employed and you and your spouse were noteligible to participate in an employer paid health plan, the entirecost of your health insurance premiums for a plan establishedunder your business may be deductible as an adjustment toincome on line 29 of Form 1040. T

(8) In 2008, Anthony and Virginia each contributed to a traditionalIRA. Both are covered by retirement plans at work. Their filingstatus is MFJ and their modified AGI is $102,000. To report theirnondeductible IRA contributions, they will file one Form 8606. F

(9) In January 2008, Edgar got a new job and moved to a new homecloser to the new job location. Edgar’s move met the relationshipand distance tests. In November 2008, Edgar was laid off and hebecame a self-employed consultant. Edgar must now meet the78-week time test for self-employed persons. F

104

Adjustments

CLASSWORK 1: True or False.

(10) Liza does not report any income on line 7 of her Form 1040. Her total income is from interest, dividends and alimony payments. She cannot contribute to a traditional IRA. F

(11) The amount of a penalty on early withdrawal of savings that you can deduct is reduced or limited as your modified AGI increases. F

(12) If you are self-employed and had a net profit in 2008, you may be able to deduct, as an adjustment to income, up to 70% of the amount paid for health insurance on behalf of you, your spouse, and dependents. The plan must be established under your business. F

105

Adjustments

CLASSWORK 1: True or False.

(13) Sid’s net profit from self-employment reduced by his deduction on line 27 for ½ his self-employment tax is $2,600. His deduction on line 29 for self-employed health insurance cannot exceed $2,600. T

(14) If you choose to use the standard mileage rate rather than actual car expenses, you cannot deduct your parking fees and tolls as moving expenses. F

(15) You can claim a deduction for qualified tuition and fees that you paid for with the proceeds from a loan. T

(16) Jim is a sophomore at State U’s degree program in dentistry. In addition to tuition, he is required to pay a fee to the University for the rental of dental equipment he will use in this program. The equipment fee is a qualified related expense for the purpose of the tuition and fees deduction. T

106

AdjustmentsCLASSWORK 2: Multiple Choice.

1. Which of the following is not a deductible moving expense? a. The cost of connecting or disconnecting utilities

required because you are moving your household goods

b. The cost of shipping your dog to your new homec. The meals you paid for while you were traveling to

your new homed. The cost of parking fees and tolls and your car

expenses at the standard mileage rate.

2. In 2008, Julian moved to be closer to his new job. His old job is 10 miles from his old house. To meet the distance test for moving expenses, his new job location must be at least:

a. 60 miles from his old houseb. 10 miles from his new housec. 50 miles from his old job location.d. 50 miles from his old house

107

AdjustmentsCLASSWORK 2: Multiple Choice.

3. You cannot take the student loan interest deduction if: a. You can be claimed as a dependent on another’s

returnb. Your filing status is MFJ and your modified AGI

$140,000 or morec. Your filing status is married filing separatelyd. All of the above.

4. Bill received a 1099-INT from Diamond Bank showing he received $5,000 interest from his Certificates of Deposit and that he paid an early withdrawal penalty of $500. On his Form 1040, Bill should:

a. Enter $4,500 on line 8a of his Form 1040b. Take a $500 deduction for the penalty on

Schedule Ac. Deduct the $500 as an adjustment on line 30 of

Form 1040d. First figure his AGI to see if there is a limit on

the amount he can deduct.

108

AdjustmentsCLASSWORK 2: Multiple Choice.

5. You cannot deduct payments to a former spouse as an adjustment for alimony if you:

a. Are required to make payments after the death of your former spouse

b. Are legally separated under a separate maintenance decree

c. Pay by money orderd. File as single or head of household.

6. You cannot take the tuition and fees deduction if:a. Your filing status is MFSb. You can be claimed as a dependent on another

returnc. Your filing status is single and your modified

AGI is more than $80,000d. All of the above.

109

Adjustments

CLASSWORK 2: Multiple Choice.

1. Which of the following is not a deductible moving expense? c. The meals you paid for while you were traveling to your new home

2. In 2008, Julian moved to be closer to his new job. His old job is 10 miles from his old house. To meet the distance test for moving expenses, his new job location must be at least: b. 60 miles from his old house

3. You cannot take the student loan interest deduction if:

d. All of the above

110

Adjustments

CLASSWORK 2: Multiple Choice.

4. Bill received a 1099-INT from Diamond Bank showing he received $5,000 interest from his Certificates of Deposit and that he paid an early withdrawal penalty of $500. On his Form 1040, Bill should: c. Deduct the $500 as an adjustment on line 30 of Form 1040

5. You cannot deduct payments to a former spouse as an adjustment for alimony if you: a. Are required to make payments after the death of your former spouse

6. You cannot take the tuition and fees deduction if:d. All of the above

111

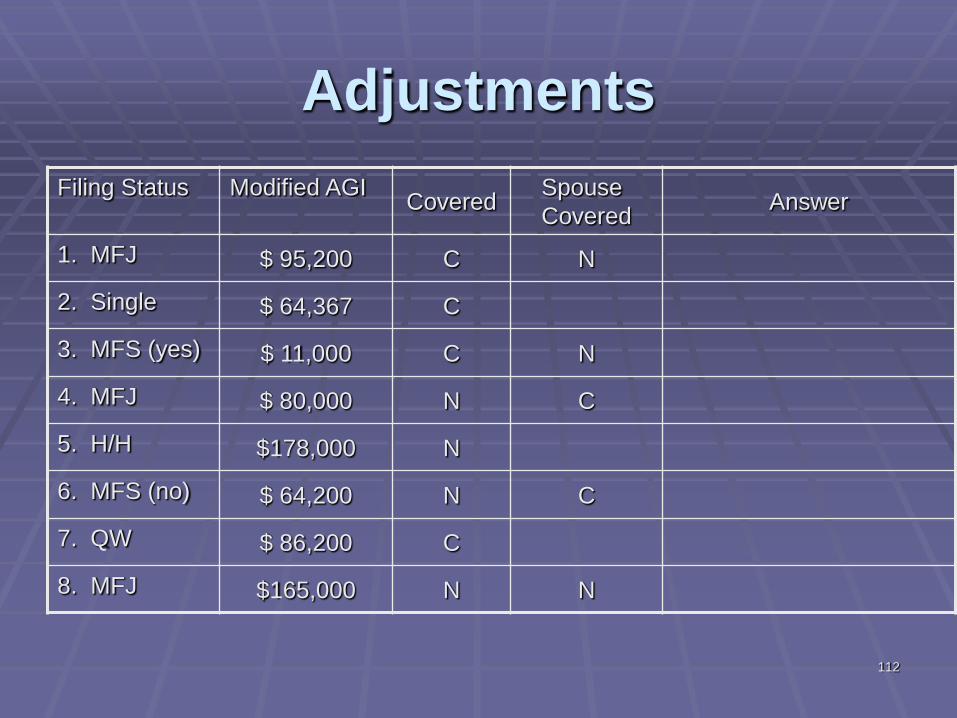

Adjustments

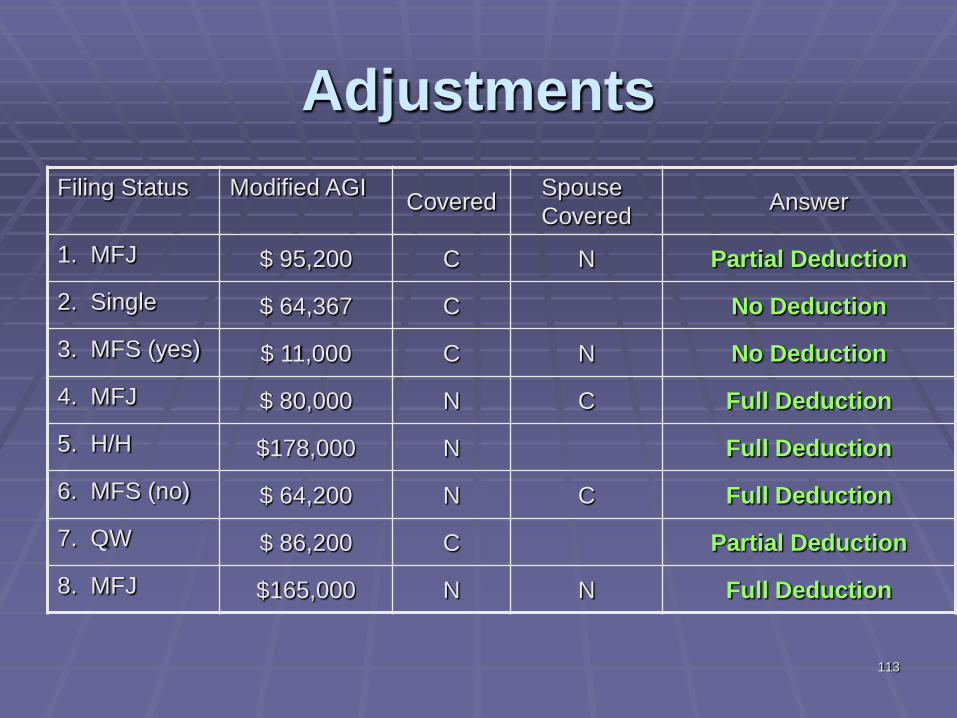

CLASSWORK 3: Determine whether each of the following taxpayers can take a full IRA deduction, a partial deduction or no deduction. Under the “covered” and “spouse covered” columns, C indicates covered by a retirement plan at work and N indicates not covered by such a plan. For the MFS taxpayers (yes) indicates they lived with their spouse; (no) indicates they did not.

112

Adjustments

Filing Status Modified AGICovered

Spouse

CoveredAnswer

1. MFJ $ 95,200 C N

2. Single $ 64,367 C

3. MFS (yes) $ 11,000 C N

4. MFJ $ 80,000 N C

5. H/H $178,000 N

6. MFS (no) $ 64,200 N C

7. QW $ 86,200 C

8. MFJ $165,000 N N

113

Adjustments

Filing Status Modified AGICovered

Spouse

CoveredAnswer

1. MFJ $ 95,200 C N Partial Deduction

2. Single $ 64,367 C No Deduction

3. MFS (yes) $ 11,000 C N No Deduction

4. MFJ $ 80,000 N C Full Deduction

5. H/H $178,000 N Full Deduction

6. MFS (no) $ 64,200 N C Full Deduction

7. QW $ 86,200 C Partial Deduction

8. MFJ $165,000 N N Full Deduction

114

Questions & Answers