Embed Size (px)

Citation preview

AFRICAN DEVELOPMENT BANK GROUP

LIBERIA

INTEGRATED PUBLIC FINANCIAL MANAGEMENT REFORM PROJECT

PROJECT COMPLETION REPORT

(PCR)

ECGF DEPARTMENT

September 2018

Pu

blic

Dis

clo

sure

au

tho

rize

d

Pu

blic

Dis

clo

sure

au

tho

rize

d

1

I BASIC DATA

A Report data

Report date Date of report: September 11, 201810/9/2017September 11, 2018

Mission date (if field mission)

From: 05/29/2017 To: 06/09/2017

B Responsible Bank staff

Positions At approval At completion

Regional Director Frank Perrault Janvier Litse

Country Manager Margaret Kilo Orison Amu

Sector Director Isaaac Lobe Abdoulaye Coulibaly

Sector Manager Jean-Luc Bernasconi Abdoulaye Coulibaly

Task Manager Kalayu Gebre-Selassie Patricia N. Laverley

Alternate Task

Manager

PCR Team Leader Patricia Laverley

PCR Team Members Alex Yeanay

C Project data

Project name: Integrated Public Financial Management Reform Project

Project code: P-LR-K00-013 Instrument number(s): 5900155003751

Project type: ISP Sector: Multisector

Country: Liberia Environmental categorization (1-3):3

Processing milestones – Bank

approved financing only

(add/delete rows depending

on the number of financing

sources)

Key Events (Bank approved financing

only)

Disbursement and closing dates

(Bank approved financing only)

Financing source/

instrument1:

ADF TSF Grant

Financing source/ instrument1: Financing source/ instrument1:

PROJECT COMPLETION REPORT FOR PUBLIC SECTOR OPERATIONS (PCR)

AFRICAN DEVELOPMENT

BANK GROUP

2

Date approved: 09/12/2012 Cancelled amounts: Original disbursement deadline:

December 31, 2016

Date signed: 09/19/2012 Supplementary financing: Original closing date: December 31,

2016

Date of entry into force:

September 19, 2012

Restructuring (specify date & amount

involved):

Revised (if applicable) disbursement

deadline:

Deadline for last disbursement

revised to March 31, 2017

Date effective for 1st

disbursement: February 12,

2013

Extensions (specify dates): Only one

extension to June 30, 2017

Revised (if applicable) closing date:

Closing date revised to June 30, 2017

Date of actual 1st

disbursement:

Financing source/

instrument2:

Financing source/ instrument2: Financing source/ instrument2:

Date approved: Cancelled amounts: Original disbursement deadline:

Date signed: Supplementary financing: Original closing date:

Date of entry into force: Restructuring (specify date & amount

involved):

Revised (if applicable) disbursement

deadline:

Date effective for 1st

disbursement:

Extensions (specify dates): Revised (if applicable) closing date:

Date of actual 1st

disbursement:

Financing source/instrument

(add/delete rows depending

on the number of financing

sources):

Disbursed amount

(amount, UA):

Percentage

disbursed (%):

Undisbursed

amount (UA):

Percentage

undisbursed (%):

Financing source/

instrument1:

ADF/TSF

3,000,000.00 100%

Financing source/

instrument2:

Government:

Other (eg. co-financiers).

World Bank 3,261,000.00 100%

SIDA 9,848,000.00 100%

USAID 2,511,000.00 100%

TOTAL 18,620,000.00 100%

Executing and implementing agency (ies): Ministry of Finance and Development Planning PFM Reform Coord. Unit

3

D Management review and comments

Report reviewed by Name Date reviewed Comments

Country Manager Orison Amy October 20, 2017

Sector Manager Abdoulaye Coulibaly October 20, 2017

Regional Director (as chair of Country Team)

Janvier Litse

Sector Director Abdoulaye Coulibaly

II Project performance assessment

A Relevance

Relevance of project development objective

Rating* Narrative assessment (max 250 words)

3 The Liberia Integrated Public Financial Management Reform Project (IPFMRP) was launched in

2012 to provide support to PFM operations over a period of four years. The IPFMRP,

underpinned by the results of various diagnostic assessments, was instituted as a vehicle to

implement the PFM Reforms Strategy and Action Plan (2011-2016). The project’s principal

objectives were to improve budget coverage, fiscal policy management, financial control, and

oversight of government finances. At the end of original project completion date of June 30,

2016, the Government’s request for a one year no cost extension was granted by the Bank to

continue with the implementation of programs that were affected by the outbreak of the Ebola

Virus Disease (EVD) in 2014. The overall funding of the project amounted to US 31.5 million:

Initial funds of USD28.5 million came from World Bank, Sida, AfDB and USAID. Additional

funding of USD 3 million was provided by EU to support reform activities in the areas of Civil

Society and Social Accountability and PFM in the Justice System. The IPFMRP officially

closed on June 30, 2017. The project objectives, which identified the need to improve budget coverage,

strengthen fiscal policy management, financial control, and oversight of government finances and the

activities in achieving those objectives, were relevant and remained well on course throughout the period

of the project implementation. The objectives were also consistent with

the Bank’s Country Strategy Paper (2013-2017), which focused on improving public

investment, budget management, efficiency of public finances and a more transparent and

accountable use of public resources.

* For all ratings in the PCR use the following scale: 4 (Highly satisfactory), 3

(Satisfactory), 2 (Unsatisfactory), 1 (Highly unsatisfactory) Relevance of project design

Rating

*

Narrative assessment (max 250 words)

3 The design of the project supported Liberia’s Agenda for Transformation and Medium

Term Development Strategy. The indicators set for monitoring and evaluating the project

outcomes were necessary in contributing to the achievement of the project development

objectives (PDOs).

Lessons learned related to relevance

Key issues

(max 5, add rows as

needed)

Lessons learned Target audience

Institutional

development

Institutionalizing PFM Reform within Government Structures (Use

of Country

System): Implementation of reform within the MFDP and other

government entities hasa long lasting effect on the county’s use of country

system and endeavour to strengthen its PFM system. The level of

capacity, both human and material, that have been

developed during the period of implementation of the project has helped

to promote and sustain the reforms. The use of civil servants in delivering

the reform promotes a lasting effect and sense of ownership of the reform.

GoL and the Bank

4

Change

Management

Change Management & Communication of PFM Reforms:

The absence of a coherent

and robust Change Management and Communication Strategy

posed challenges to the mode of effective communication over the

course of implementing PFM Reforms

However, the PFM Reform Coordination Unit did tremendously

well to change and communicate reforms among key stakeholders.

It is important that going forward, a Change Management and

Communication Strategy should be formulated by the Secretariat

and approved by the Senior Management and relevant stakeholders

for implementation.

GoL and the Bank

Design simplicity Project Design & Coordination of Support: The design of the

project was elaborate and a positive move for Liberia and supported

the country’s medium term development policy, the Agenda for

Transformation and the PFM Strategy and Action Plan (2011-2016).

The reform programs were realistic and implementable. However,

close coordination between donor partners in supporting reforms is

critical to avoiding duplication of support to PFM programs. Partners

should be able to clearly identify their areas of intervention prior to

implementation.

GoL and the Bank

Results and

outcomes

M & E Reporting Template: M&E strategy provided a

framework for reporting on results and outcomes. However, during

some stages in the project implementation, there

were disagreements among the stakeholders especially the

Development Partners on the reporting format. As the result, the

reporting format had to be changed on number of occasions to

satisfy partners’ preferences. This affected reporting on PFM

progress and in some cases delayed the publication of reports. It is

important to develop a harmonizedreporting framework and

template acceptable to all stakeholders including our

development partners.

GoL and the Bank

B Effectiveness

Progress towards the project’s development objective (project purpose)

Comments

Provide a brief description of the Project (components) and the context in which it was designed and implemented. State

the project development objective (usually the project purpose as set out in the RLF) and assess progress. Unanticipated

outcomes should also be accounted for, as well as specific reference of gender equality in the project . The consistency of

the assumptions that link the different levels of the results chain in the RLFshould also be considered. Indicative max

length: 400 words.

Three of the seven PDO level indicators achieved their targets, one improved but fell short

of the target, while three remained unchanged as determined by 2017 PEFA Self-assessment.

While the three indicators did not meet the PEFA criteria for better scores, it is worth noting

that significant progress was made towards achieving each. Summary justification for each

indicator is outlined below:

PI 7: Extent of unreported Government operations:

The score remained unchanged at D+, missing a target of B+ because donor projects

managed by Project Financial Management Unit (PFMU) and other M&As are not

consolidated into the financial statements of the Consolidated Fund account by the

MFDP. However, balances of thirty (30) donor-funded projects, including the IPFMRP,

were brought into IFMIS as part of a wider plan of bringing all DFPs on IFMIS to aid

reporting and accounting and ensure consolidation.

5

PI-12. Multi-year perspective in fiscal planning, expenditure policy and budgeting:

The score improved from D+ to C+ but not enough to meet the target of B+. The current

National Budget provides two outer years’ projections, while the criterion for this PEFA

indicator requires three outer years’ projections for a higher score. Also, changes in the

multi-year expenditure estimates in the rolling MTEF budget are not explained, thus the

reason for a lower score.

PI-18. Effectiveness of payroll controls

This indicator improved from D+ to meet the target score of B+. The improvement

in the score has largely been due to integration of personnel records and payroll data

between CSA and MFDP. Further gains could be made by improving the ability of

the CSA to obtain information on changes to personnel records in a timely manner,

regular routine reconciliation meetings between MFDP and CSA, and a regular

updating of personnel records.

PI-20. Effectiveness of internal controls for non-salary expenditure

PI -20 also improved from the low score of C+ to meet the target score of B+. The

improvement in the score is partly because of the rollout of IFMIS to 50 M&As, the

expansion of the work of the IAA to over 40 M&As and the improvement of internal control

processes in the office of the Comptroller & Accountant General.

PI-25. Quality and timeliness of annual financial statements

Quality and timeliness of annual financial statements improved from a low score of D in

2012 to B+ in 2017, thus exceeding the target score of C+. This marked improvement has

mainly been because of compliance with the reporting requirements of the Cash Basis IPSAS

adopted by the Government of Liberia, coupled with improvement in timely submission

PI-26. Scope, nature and follow-up of external audit

This indicator remained unchanged from the low score of D+, thus missing the target score of

C+. The primary reason for the poor score is delays in submission of audit reports by the

Auditor General to the Legislature, which has also been a result of late response by auditees

to audit queries raised by the Auditor General.

PI-28: Legislative scrutiny of external audit reports

Based on the 2011 PEFA assessment framework, the score remains at a low D+, missing the

project target score of C+. The low score is attributed to delay by the Legislature in

reviewing the audit reports of the Consolidated Fund submitted by the Auditor General for

the fiscal years 2012/13, 2013/14 and 2014/15. The 2011 PEFA assessment framework uses

MI method to calculate this score. The score is however better at C+ if it is based on the 2016

refined PEFA assessment framework which uses M2 method to calculate the score. The

better score is influenced by the coverage of the audit and the use of international standards

by the GAC in the conduct of the audit.

6

Outcome

indicators (as

per RLF; add

more rows as

needed)

Baseline

value

(Year)

(A)

Most

recent

value

(B)

End target (C)

(expected

value at

project

completion)

Progress

towards

target (%

realized)

[(B-

A)/(C-

A)]

Narrative assessment (indicative max length: 50 words per

outcome)

Core

Sector

Indicator (Yes/No)

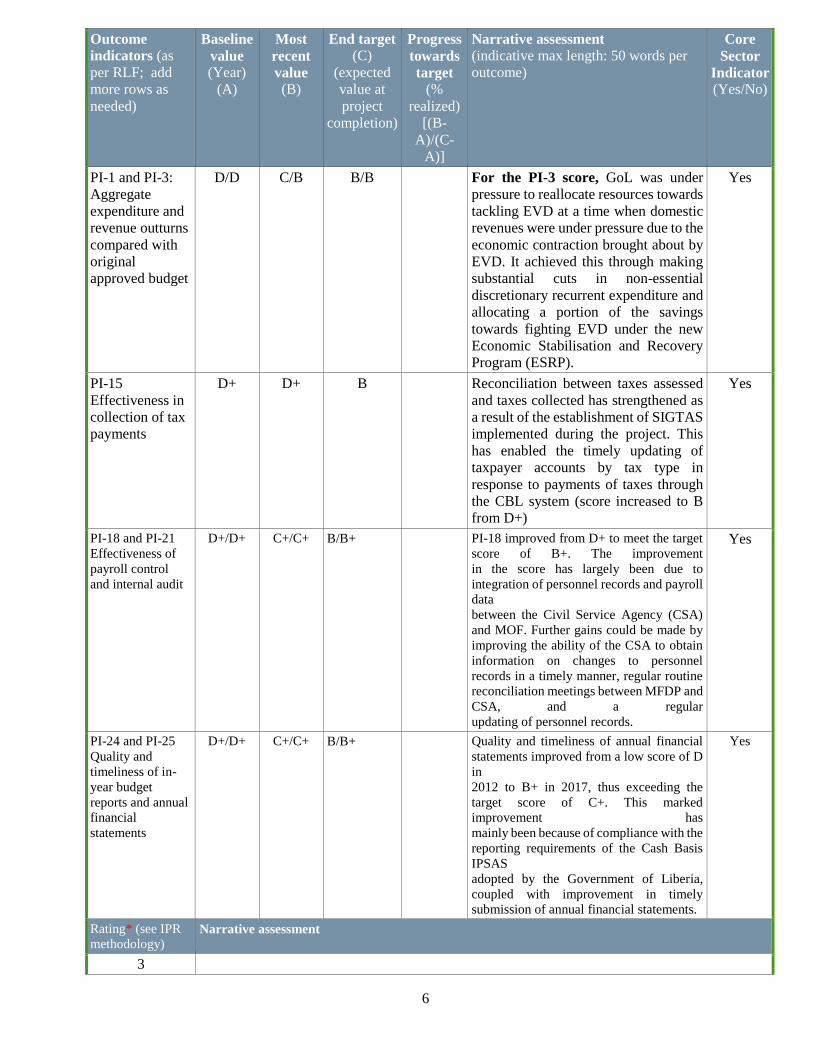

PI-1 and PI-3:

Aggregate

expenditure and

revenue outturns

compared with

original

approved budget

D/D C/B B/B For the PI-3 score, GoL was under

pressure to reallocate resources towards

tackling EVD at a time when domestic

revenues were under pressure due to the

economic contraction brought about by

EVD. It achieved this through making

substantial cuts in non-essential

discretionary recurrent expenditure and

allocating a portion of the savings

towards fighting EVD under the new

Economic Stabilisation and Recovery

Program (ESRP).

Yes

PI-15

Effectiveness in

collection of tax

payments

D+ D+ B Reconciliation between taxes assessed

and taxes collected has strengthened as

a result of the establishment of SIGTAS

implemented during the project. This

has enabled the timely updating of

taxpayer accounts by tax type in

response to payments of taxes through

the CBL system (score increased to B

from D+)

Yes

PI-18 and PI-21

Effectiveness of

payroll control

and internal audit

D+/D+ C+/C+ B/B+ PI-18 improved from D+ to meet the target

score of B+. The improvement

in the score has largely been due to

integration of personnel records and payroll

data

between the Civil Service Agency (CSA)

and MOF. Further gains could be made by

improving the ability of the CSA to obtain

information on changes to personnel

records in a timely manner, regular routine

reconciliation meetings between MFDP and

CSA, and a regular

updating of personnel records.

Yes

PI-24 and PI-25

Quality and

timeliness of in-

year budget

reports and annual

financial

statements

D+/D+ C+/C+ B/B+ Quality and timeliness of annual financial

statements improved from a low score of D

in

2012 to B+ in 2017, thus exceeding the

target score of C+. This marked

improvement has

mainly been because of compliance with the

reporting requirements of the Cash Basis

IPSAS

adopted by the Government of Liberia,

coupled with improvement in timely

submission of annual financial statements.

Yes

Rating* (see IPR

methodology) Narrative assessment

3

7

Outcome reporting

Output reporting

Output

indicators (as

specified in the

RLF; add more

rows as needed)

Most recent

value

(A)

End target

(B) (expected

value at

project

completion)

Progress

towards

target (% realized)

(A/B)

Narrative assessment (indicative max length: 50 words per

output)

Core

Sector

Indicator (Yes/No)

Output 1:

Transition to

medium-term

and policy-based

budgeting

2 year 3 years 67% The MTEF process still remains weak,

because even thought it has

institutionalized, the MTEF budget

still does not provide accurate 3 year

estimates into the future. The PEFA

score improved from D+ to C+ but not

enough to meet the target of B+. The

current

National Budget provides two outer

years’ projections, while the criterion

for PEFA requires three outer year

projections for a higher score. Also,

changes in the

multi-year expenditure estimates in the

rolling MTEF budget are not well

explained, thus the

reason for a lower PEFA score.

Yes

Output 2: IFMIS

fully operational

at MOF

50 MDAs 120 MDAs 42% FreeBalance, the Service Provider

of the IFMIS software, was suspended

by the World Bank in 2013. This

suspension prevented the government

from entering into contracts with

FreeBalance for the

provision of services using the project.

As the result, the upgrade of the IFMIS

from version 6.5 to version 7.0 and the

procurement of additional licenses had

to be financed using government

funding. This affected the timely

completion of the upgrade and

disrupted the IFMIS operations, as

sourcing funding from government to

support the activity was a challenge.

Comprehensive information on donor

projects and end of year outstanding

debt are still not adequately reflected in

the statements.

Yes

Output 3:

Revenue

authority fully

established

Revenue

authority

fully

established

Revenue

authority

fully

established

100% The Liberia Revenue Authority (LRA),

a successor to the Department of

Revenue under the erstwhile Ministry

of Finance, was established in July 1,

2014 by an act of the Legislature. The

LRA moved to a new headquarters, and

has structured its internal systems and

processes for improving efficiency in

revenue generation. Accordingly,

internal manuals and Standard

Yes

8

Operating Procedures (SOPs) for

various operational units were

developed to enhance operational

effectiveness and efficiency.

Significant technical assistance and

logistics were provided to strengthen

the Authority’s tax collection

capabilities. SIGTAS and ASYCUDA

were deployed at various tax and

customs collection centers across the

country. Domestic tax revenue

increased by 14% from FY 2010/11 to

FY2015/16, while Customs increased

by 64% during the same period.

The taxpayers’ services program

was restructured to enable it address

growing customers’concerns, and to

effectively communicate adequate

taxpayers’ education messages. For

2016/17, Call Centers recorded 360

inquiries of which 270 or 75% were

resolved, while the Customer Service

Help Desks also resolved 90% of its

422 customers’ inquiries.

An internal tax appeals office was

setup and made more functional,

building assurances for recourse and

confidence among taxpayers. During

the FY2014/15, five (5) appeals

and dispute cases from the business

community were resolved, and in

2015/16, twelve

(12) protests and objections were also

resolved. Tax compliance rate as

measured by tax payers filing improved

by more than 70% as a result of this

project.

Output 4:

Legislatiave

budget office

reduces delays in

budget approval

No delay No delay 100% The improvement in the budget

approval process is attributed to the

IFMIS deployment and compliance

with IPSAS reporting requirements.

Yes

Output 5:

Number of staff

with recognized

PFM

qualification

318 qualified

PFM

graduates

155 qualfied

PFM

graduates

212% The Financial Management Training

Program was established in 2008 under

the auspices of the University of

Liberia and other counterparts.

Through funding from this project, the

program has graduated 150 students

with MBA degrees, with emphasis in

Public Financial Management. The

Intensive Procurement Component of

the Program also graduated over 120

students with

post-graduate diplomas in

procurement. All of the graduates have

been absorbed within

Yes

9

the civil service and deployed in

various institutions performing critical

functions in their

respective fields. Many of the

graduates have excelled rapidly in

public service: some as

Ministers, Commissioners,

Superintendents, directors among

others. Additional 18 and

30 MBA and procurement students

respectively are nearing completion of

their

respective courses. Women enrollment

in the FMTP increased over time, from

3% in

2007 to 40% in 2017, and IPTP, from

5% to 88% over a period of four years.

Rating* (see IPR

methodology) Narrative assessment

3

Development Objective (DO) rating

DO rating (derived

from updated IPR)*

Narrative assessment (indicative max length: 250 words

3 The objectives were consistent with the Bank’s Country Strategy Paper (2013-2017),

which focused on improving public investment, budget management, efficiency of public

finances and a more transparent and accountable use of public resources. The project

objectives, which identified the need to improve budget coverage, strengthen fiscal policy

management, financial control, and oversight of government finances and the activities in

achieving those objectives, were relevant and remained well on course throughout the

period of the project implementation and the overarching development objective was met.

Beneficiaries (add rows as needed)

Actual (A) Planned

(B) Progress towards target

(% realized) (A/B) % of women Category

(eg. farmers,

students)

Ministry of Finance - PFM Reform

Coordination Unit

This ISP delivered benefits of national significance for the entire country,

and the five direct beneficiary institutions for this project are listed.

Comptroller and Accountant General

Liberia Revenue Authority

Legislative Budget Office

Public Procurement and Concessions

Commission

Gender equality

Assessment on the performance of gender equality in the operation (indicative max length: 250 words)

The operation supported government efforts and plans to enhance gender budgeting and gender mainstreaming

into development programs. IPFMRP supported training in gender budgeting, which Government initiated to

facilitate gender analysis in the formulation of government budgets and allocation of resources. The training

programs delivered through IPFMRP was made available to all middle to senior level women in the beneficiary

institutions. The project ensured gender balance in its activities and ensured women’s participation in the PFM

training sessions included 90% of eligible female employees.

10

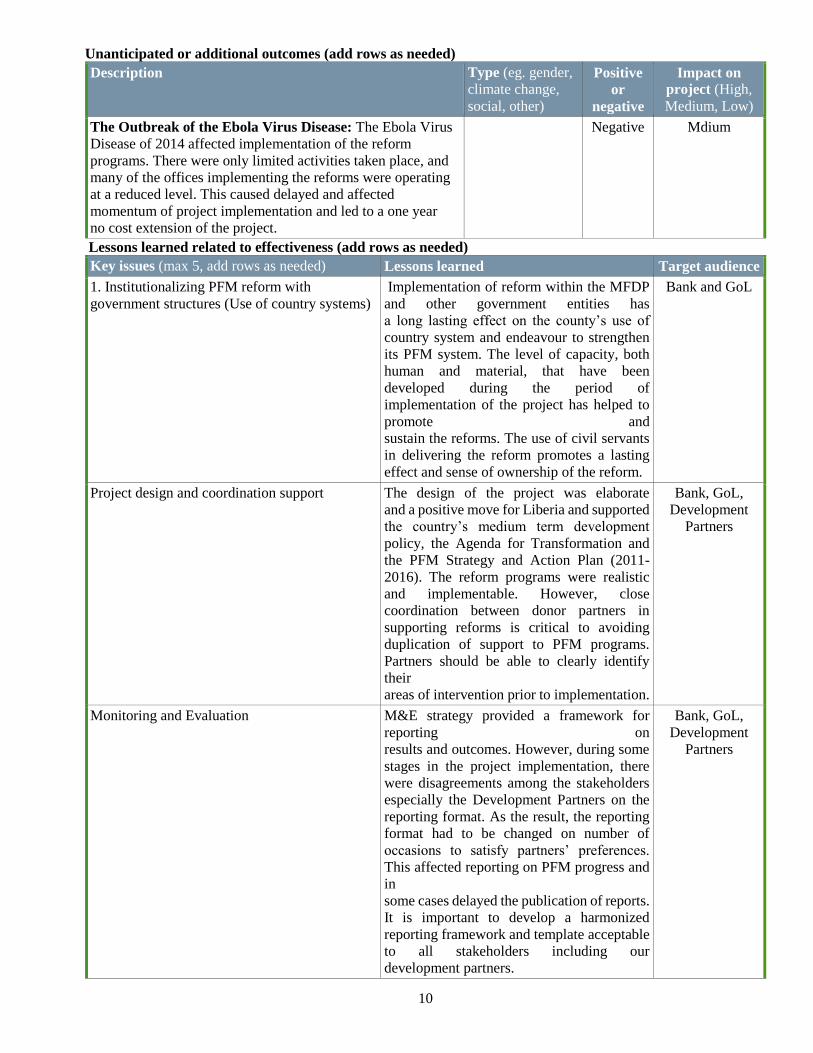

Unanticipated or additional outcomes (add rows as needed)

Description Type (eg. gender,

climate change,

social, other)

Positive

or

negative

Impact on

project (High,

Medium, Low)

The Outbreak of the Ebola Virus Disease: The Ebola Virus

Disease of 2014 affected implementation of the reform

programs. There were only limited activities taken place, and

many of the offices implementing the reforms were operating

at a reduced level. This caused delayed and affected

momentum of project implementation and led to a one year

no cost extension of the project.

Negative Mdium

Lessons learned related to effectiveness (add rows as needed)

Key issues (max 5, add rows as needed) Lessons learned Target audience

1. Institutionalizing PFM reform with

government structures (Use of country systems)

Implementation of reform within the MFDP

and other government entities has

a long lasting effect on the county’s use of

country system and endeavour to strengthen

its PFM system. The level of capacity, both

human and material, that have been

developed during the period of

implementation of the project has helped to

promote and

sustain the reforms. The use of civil servants

in delivering the reform promotes a lasting

effect and sense of ownership of the reform.

Bank and GoL

Project design and coordination support The design of the project was elaborate

and a positive move for Liberia and supported

the country’s medium term development

policy, the Agenda for Transformation and

the PFM Strategy and Action Plan (2011-

2016). The reform programs were realistic

and implementable. However, close

coordination between donor partners in

supporting reforms is critical to avoiding

duplication of support to PFM programs.

Partners should be able to clearly identify

their

areas of intervention prior to implementation.

Bank, GoL,

Development

Partners

Monitoring and Evaluation M&E strategy provided a framework for

reporting on

results and outcomes. However, during some

stages in the project implementation, there

were disagreements among the stakeholders

especially the Development Partners on the

reporting format. As the result, the reporting

format had to be changed on number of

occasions to satisfy partners’ preferences.

This affected reporting on PFM progress and

in

some cases delayed the publication of reports.

It is important to develop a harmonized

reporting framework and template acceptable

to all stakeholders including our

development partners.

Bank, GoL,

Development

Partners

11

C Efficiency

Timeliness

Planned project duration –

years (A) (as PAR) Actual implementation time –

years (B) (from effectiveness for

1st disb.)

Ratio of planned and actual

implementation time (A/B)

Ratin

g*

4 years from 2012 to 2016 4.5 years from 2012 to 2017 89% 3

Narrative assessment (indicative max length: 250 words)

Resource use efficiency

Median % physical

implementation of RLF outputs

financed by all financiers (A)

(see II.B.3)

Commitment rate (%) (B)

(See table 1.C – Total

commitment rate of all financiers)

Ratio of the median percentage

physical implementation and

commitment rate (A/B)

Ratin

g*

Narrative assessment (indicative max length: 250 words)

Cost benefit analysis

Economic Rate of Return

(at appraisal) (A)

Updated Economic Rate of

Return

(at completion) (B)

Ratio of the Economic Rate

of Return at completion and

at appraisal (B/A)

Rating*

Narrative assessment (indicative max length: 250 words)

Implementation Progress (IP)

IP Rating

(derived

from

updated

IPR) *

Narrative comments (commenting specifically on those IP items that were rated

Unsatisfactory or Highly Unsatisfactory, as per last IPR). (indicative max length: 500 words)

3 The Outbreak of the Ebola Virus Disease: The Ebola Virus Disease of 2014 affected

implementation of the reform programs. There were only limited activities taken place, and many of

the offices implementing the reforms were operating at a reduced level. This caused delayed and

affected momentum of project implementation and led to a one yearno cost extension of the project.

Frequent Replacement of Key Government Personnel: During the project implementation, staff

turnover rate in some implementing M&As was high. Many staff left to seek new opportunities and

better wages, while others were replaced or transferred to new positions. Some of these staff were

directly involved with the management and implementation of the reform in their respective

ministries or departments and had undergone some basic PFM training. This affected implementation. Changes in Operational Leadership: Implementation was hampered by three different changes in the

project leadership during the latter part of the project cycle. This contributed to a lack of focus and continuity

of priorities, hampered effective decision making and contributed to delays in project implementation.

Coordination with Implementing Agencies: Delay in providing fund balances affected planning and

spending decisions of components. Adequate adherence to coordination mechanism outlined in Project

Operational Manual will be critical in future project implementations..

Suspension of FreeBalance Inc. by the World Bank: FreeBalance, the Service Provider

of the IFMIS software, was suspended by the World Bank in 2013. This suspension

prevented the government from entering into contracts with FreeBalance for the

provision of services using the project. As the result, the upgrade of the IFMIS from

version 6.5e to version 7.0 and the procurement of additional licenses had to be financed

using government funding. This affected the timely completion of the upgrade and

disrupted the IFMIS operations, as sourcing funding from government to support the

activity was a challenge.

12

Lessons learned related to efficiency

Key issues (max 5, add rows as needed) Lessons learned Target audience

1. Absence of a Harmonized Reporting

Format

Reporting on project implementation

progress was initially constrained due to the

lack of harmonized reporting framework

acceptable to all PFM Development

Partners. Different reporting demands from

individual partners posed serious challenge.

Bank, GoL,

Development

Partners

D Sustainability

Financial sustainability

Ratin

g*

Narrative assessment (indicative max length: 250 words)

3 The Government of Liberia has developed a new fully costed PFM Strategy and Action Plan for 2017-

2021 to deepen and sustain the reform and support new priorities that are consistent with its National

Development Plan. The new strategy contains provisions for strengthening institutional capacity through

sustained training in various PFM Programs, including Planning, budgeting, procurement, Financial

Management, Accounting, Economics, among others.

Institutional sustainability and strengthening of capacities

Ratin

g*

Narrative assessment (indicative max length: 250 words)

3 Same as above

Ownership and sustainability of partnerships

Ratin

g*

Narrative assessment (indicative max length: 250 words)

3 Same as above

Environmental and social sustainability

Ratin

g*

Narrative assessment (indicative max length: 250 words)

N/A

Lessons learned related to sustainability

Key issues (max 5, add rows as needed) Lessons learned Target audience

1. None 1.

III Performance of stakeholders

Bank performance

Ratin

g* Narrative assessment by the Borrower on the Bank’s performance, as well as any other aspects of

the project

(both quantitative and qualitative). See guidance note on issues to cover. (indicative max length: 250

words)

3

Comments to be inserted by the Bank on its own performance (both quantitative and qualitative).

See guidance note on issues to cover. (indicative max length: 250 words)

The Bank through the Liberia Field Office provided support to the implementation of the project. The

Bank’s supervision was considered satisfactory and provided timely and candid guidance to the

Implementing entities on the implementation of the project. The Bank conducted joint supervision missions

with the other development partners which were helpful to the project implementation in helping resolve

some critical issues and providing the needed guidance. Moving forward, it would be useful to have

dedicated Governance and PFM Officer in Liberia to ensure better project implementation of future Bank

projects in the country.

13

Key issues (related to Bank performance, max 5, add

rows as needed) Lessons learned

1. 1.

Borrower performance

Ratin

g* Narrative assessment on the Borrower performance to be inserted by the Bank (both quantitative

and qualitative, depending on available information). See guidance note. (indicative max length: 250

words)

2

Comments to be inserted by the Borrower on its own performance (both quantitative and

qualitative). See guidance note on issues to cover. (indicative max length: 250 words)

There were three changes in the operational leadership of the project during the latter part of the

project. This contributed to a lack of continuity of priorities, hampered effective decision making, and

contributed to delays in project implementation.

Key issues (related to Borrower performance, max 5,

add rows as needed) Lessons learned

1. 1.

Performance of other stakeholders

Ratin

g* Narrative assessment on the performance of other stakeholders, including co-financiers,

contractors and service providers. See guidance note on issues to cover. (indicative max length: 250

words)

3 Close coordination between the World Bank, IMF, EU, and SIDAs during the design and

implementation of the project was critical to avoid duplication of support to PFM.

Key issues (related to

performance of other

stakeholders, max 5, add rows

as needed)

Lessons learned (max 5) Target audience

(for lessons learned)

1. Collaboration among

development partners

1. Partners should be able to identify clearly their areas of

intervention prior to design and implementation of future

programs

Bank and

Development

Partners

IV Summary of key lessons learned and recommendations

Key lessons learned

Key issues (max 5, add rows as needed) Key lessons learned Target audience

Donor collaboration A pooled funding mechanism was used

during the implementation of this project.

The key lesson that emerged from this

project is the need for close coordination on

all aspects of project implementation,

monitoring, and reporting.

Bank, GoL, and

Development

Partners

Key recommendations (with particular emphasis on ensuring sustainability of project benefits)

Key issue (max 10, add rows as needed) Key recommendation Responsible Deadlin

e

1.

14

V Overall PCR rating

Dimensions and criteria Rating*

DIMENSION A: RELEVANCE 3

Relevance of project development objective (II.A.1) 3

Relevance of project design (II.A.2) 3

DIMENSION B: EFFECTIVENESS 3

Development Objective (DO) (II.B.4) 3

DIMENSION C: EFFICIENCY

Timeliness (II.C.1) 3

Resource use efficiency (II.C.2) 3

Cost-benefit analysis (II.C.3)

Implementation Progress (IP) (II.C.4) 3

DIMENSION D: SUSTAINABILITY

Financial sustainability (II.D.1) 3

Institutional sustainability and strengthening of capacities (II.D.2) 3

Ownership and sustainability of partnerships (II.D.3) 3

Environmental and social sustainability (II.D.4)

AVERAGE OF THE DIMENSION RATINGS 3

OVERALL PROJECT COMPLETION RATING 3

15

VI Acronyms and abbreviations

Acronym Full name

ADF African Development Fund

AfDB African Development Bank

CAG Comptroller and Accountant General

CSP Country Strategy Paper

EU European Union

GAC General Auditing Commission

GoL Government of Liberia

IAA Internal Audit Agency

IFMIS Integrated Financial Management Information System

IMF International Monetary Fund

IPFMRP Integrated Public Financial Management Reform Project

ISP Institutional Support Project

LBO Legislative Budget Office

LRA Liberia Revenue Authority

MDAs Ministries, Departments and Agencies

MFDP Ministry of Finance and Development Planning

MTEF Medium Term Expenditure Framework

PEFA Public Expenditure and Financial Accountability

PFM Public Financial Management

PFM RS&AP Public Financial Management Reform Strategy and Action Plan

RCU Reform Coordination Unit

SIDA Swedish International Development Agency

SIGTAS Single Integrated Tax Administration System

UNDP United Nations Development Program

USAID United States Agency for International Development

WB World Bank