-

7/27/2019 Liazon White Paper on Afforable Care Act

1/8

New Survey:

Small Businesses May Respond More Positively

to Aordable Care Act Than Larger

Businesses/Corporations

-

7/27/2019 Liazon White Paper on Afforable Care Act

2/8

Practical Considerations About Costs/Beneft Management May

Outweigh Initial Negative Reaction to Reorm

A number o recent studies have suggested that most companies

will continueto oer employee healthcare benefts even ater the

Patient Protection andAordable Care Act (PPACA) is ully implemented

and all Americans are mandatedto obtain coverage.

Most o these studies have ocused on medium-sized and large

businesses,which have greater buying leverage in securing coverage

or their employees.The potential impact o PPACA among small

businesses has been let largelyunexplored.

To fll this gap, Liazon sponsored independent research with

small businesses (nomore than 50 employees) nationwide to

understand what decisions they wouldmake about the Aordable Care

Act particularly their willingness to oerhealth insurance coverage

to their employees versus opting or public or private

exchanges.

While the overarching goal o the research was to explore

awareness levels andthe potential impact o healthcare reorm among

small businesses, the researchwas also designed to stand as a

comparison to earlier published research, whichsuggested the

likelihood o business as a group to continue oering employeehealth

benefts. In many o these other studies, representatives o

businesses andcorporations were asked what they were likely to do

without being presented withdirect choices and sufcient

inormation.

The Liazon study found:

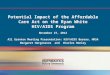

Smallbusinesseshaveapoorunderstandingofhealthcarereformlegislation

even two years ater it passed. Nearly 75% o small businessessay

they are at least somewhat amiliar with PPACA, but awareness

ospecifc eatures o healthcare reorm is limited. In particular,

companieswith 26-50 employees are more likely to be amiliar with

healthcare reormlegislation than frms with 10-25 employees (75% vs.

68%).

Familiarity

with PPACA

NOT AT ALL

FAMILIAR

VERY

FAMILIAR

NOT VERY

FAMILIAR

SOMEWHAT

FAMILIAR

5%

23%

57%

15%

NOT FAMILIAR VERY FAMILIAR

2

Q: How amiliarare you withthe PatientProtection andAordable

CareAct (sometimesreerred to asObamacare)as it relates tohealth

coverageoered bycompanies suchas yours?

-

7/27/2019 Liazon White Paper on Afforable Care Act

3/8

Closetohalfofallsmallbusinesses(47%)saytheyhavedevotedlittleornoeort

to preparing or the healthcare reorms that arise rom PPACA.

Firmswith higher revenue are more likely to have invested a good

deal o eort inplanning or PPACA.

Forcompaniesthatareunsureabouthowtheirbusinesseswillrespondtohealthcare

reorm, the overwhelming majority (70%) say they just dontknow

enough about healthcare reorm to make a decision. These

companieswill be looking or more specifcs about their options.

Beforebeingeducatedaboutvariousdetailsofhealthcarereform,mostsmall

businesses said they were unlikely to discontinue

company-sponsoredhealth coverage as a result o healthcare reorm.

One in ten companieswho are unsure about the path they will ollow

say they will do whatever ischeaper.

Closeto50%ofsmallbusinessdecisionmakersbelievehealthcarereformwillhaveanegativeimpactontheircompanies,ontheU.S.economy,andon

employee satisaction. Others are less sure but dont like the

change,despite having little knowledge about the details. Only 15%

o smallbusinesses harbor avorable views o reorm, while 18% say

their companyseelings about the law are neutral.

EortInvested in

Preparing

or PPACA

Pre-Exposure

Assessment o

Likely PPACA

Impact

3% 6%

27%37%

Some

A lot Not sure

None

Little

or None

43%

48%

49%

52%

48%

Some

49%

41%

40%

33%

37%

A Good Deal

8%

11%

10%

15%

15%

Annual revenue less than $1M

Annual revenue $1M-$2.49M

Annual revenue $2.5M-$4.99M

Annual revenue $5M-$9.99M

Annual revenue $10M+

54% 33% 44% 57%

24%

30%

33%

10%

3% 9%

6%

52%

29%

5%

6%

11%

39%

28%

16%

2%

11%

30%

30%

27%

Definitely not

Probably not

Might

Probably would

Definitely would

Top 2-Box

Unlikely to discontinue

coverage

Total 50% or less 51% to 75% 76% to 100%

% of benefits-eligible employees

3

Q: How much eort hasyour company investedso ar in preparingor

and respondingto healthcare reormresulting rom thePatient

Protection andAordable Care Act?

Q: Given what youknow about thePatient Protectionand

AordableCare Act, how likelydo you think yourcompany would be

todiscontinue employeehealth coverage?

Likelihood of Discontinuing Employee Health Coverage as a Result

of PPACA

-

7/27/2019 Liazon White Paper on Afforable Care Act

4/8

Afterlearningmoreaboutthedetailsofhealthcarereformpotentiallylower

costs, less administrative work, most premiums paid by

thegovernment, no one denied coverage the attitudes o many

smallbusiness decision makers change. Greater levels o awareness o

specifcPPACA eatures lead to an increased likelihood o a positive

impressiono PPACA overall. Lower levels o awareness result in a

higher number o

negative impressions. Together, these fndings suggest that

resistance tohealthcare reorm dissipates as small businesses learn

about the details.When understood, the economics o reorm are seen

as more compelling.

Infact,whengivenaseriesofhealthbenetscenariosunderPPACAvs.company-sponsored

health plans, nearly 50% o respondents now oeringemployer-sponsored

plans are likely to opt or public or other exchanges a much higher

than expected percentage, especially in light o responsesound in

other surveys o larger businesses and corporations.

Fortythreepercentofsmallbusinessesarelikelytodiscontinuecompany-sponsored

health plans or their employees primarily because they ear thecost

o private plans will spiral out o control.

Basedonthesurvey,wecanseethatsmallbusinessdecisionmakersinitially

spoke emotionally about healthcare reorm responding to political

disagreementsportrayed in the media but react rationally when they

have a deeperunderstanding o the coverage options and their related

fnancial impact. We believelack o knowledge explains a great deal o

the animosity toward reorm.

Tax incentives are the health reorm eature most likely to entice

some

smallbusinessestocontinueofferingemployeehealthcarecoverage.Butthefearofpaying

higher insurance rates in traditional programs and the promise o

lower costs are theeatures most likely to encourage small frms to

discontinue oering coverage.

Individual Exchange vs. Company-Sponsored Plan

4

Individual Healthcare Exchange (Option A)

All carriers, all plan types

Includes ACO option

$0 deductible plan available

Deductible as high as $6,000

Cost or $2,000 deductible plan is 20% less than$0 deductible

plan

Cost or $6,000 deductible plan is 60% less

Your company does not oer healthcare so there areno

administrative requirements or your company

Government subsidies or qualifed employees

Paid or with Post-Tax dollars by employees

Company-sponsored health coverage (Option B)

2 plan options rom 1 carrier

Deductible as high as $6,000

Cost or $2,000 deductible plan is 20% lessthan $0 deductible

plan

Cost or $6,000 deductible plan is 60% less

Your company administers the plan

No Government subsidies

Paid or with Pre-Tax dollars

44% 56%

Q: Assume your company was aced withthe two employee healthcare

optionsdescribed above and these were youronly choices. Which would

you select?

Option A

57%

47%

40%

46%

36%

Option B

43%

53%

60%

54%

64%

Annual revenue less than $1M

Annual revenue $1M-$2.49M

Annual revenue $2.5M-$4.99M

Annual revenue $5M-$9.99M

Annual revenue $10M+

-

7/27/2019 Liazon White Paper on Afforable Care Act

5/8

Two Scenarios

Here are two hypothetical cases that indicate why small

businesses are morelikely to go with public exchanges:

Bothcompaniesareequalineveryrespect,having30enrolledemployeeswith

$260,513 in total spend on health insurance 18 males and

12femaleswithagesrangingfrom22to64(averageageof37)andwithsalariesthatrangefrom$28,000to$210,000(averagesalaryof$50,467).Coverage

break down: Employee only 9; employee and spouse 5;Employee and

amily 16.

Company X continues to pay or health insurance, covering 75%

othe health insurance cost. Employees on average have a tax rate

o21%.Inthisscenario,theemployeepost-taxcostis$51,451,andthe

employer pays $195,385, pre-tax.

Company Y sends its employees to the public exchange.

Eightypercent o employees would be eligible or a subsidy rom the

publicexchange.Totalsubsidyamountforindividualsis$137,830.Subsidyamountsrangefrom$43-$12,910withanaveragesubsidyof$4,594.Employeeposttaxcostis$122,683.Employerwillprovideadditional

compensation to oset any pre-tax beneft.

At frst glance, Company X appears to have the better outcome

with a

totalpre-taxcostof$195,385andemployeepost-taxcostof$51,451.

Company Y comes with $137,830 in government subsidies and

appears toshit the ull post-tax cost o $122,683 to the employee.

However, CompanyY would oset any pre-tax beneft amount with

additional

compensationof$90,167(Savings:$122,683$51,451ofemployeecostata79%tax

rate). This results in a savings o $105,218 ($195,385 $90,167

=$105,218).

Ater you consider government subsidies AND the additional

compensation

to oset any pre-tax beneft, Company Y will enjoy a 54%

savings.

5

-

7/27/2019 Liazon White Paper on Afforable Care Act

6/8

Regional Dierences

Regional dierences in responses are also telling about how

political and

culturalviewpointscoloropinions.FirmsintheSoutharemorelikelytoreactnegatively

toward PPACA, while those in the West and Northeast are

signifcantly more likely tobe neutral or positive about the

reorm.

IntheSouthandMidwest,57%and52%,respectively,hadstrongnegativeimpressions

o healthcare reorm beore learning details about available

options.ThiscontrastswithlowernegativeimpressionsintheNortheast(34%)andWest(31%).

Whenmoreinformationwaspresented,negativeimpressionsintheSouthdroppedto48%,whichsuggeststhatmoreinformationhelpedbreakdownearlierbiases.Nevertheless,

impressions o healthcare reorm remain predominantly negative,both

beore and ater exposure to key benefts o the healthcare reorm plan.

More

inormation did not substantially change impressions in the

Northeast and West.

Knowledge Helps Decision Making

Smallbusinessesthathaveapositiveimpressionofhealthcarereformaremorelikely

to be aware o key eatures and benefts o the legislation, including

theestablishment o public and private exchanges through which

employees canindependently choose their own healthcare plans with

employer support. Those withnegative impressions are less likely to

be aware o most eatures, but they believerates will be higher.

Nevertheless, once small business owners and operators do the

calculationsand understand that exchanges could lower their costs

and save administrativetime, exchange options become more

acceptable, suggesting that peoples initialimpressions are driven

by politics and media hype, well beore they calculate whatmight be

best practically or their businesses and their communities.

Nearly a quarter o small frms say they will drop their private

coverage i thegovernment-sponsored plans proves to be a more

cost-eective option or i thepenalties they are subject to end up

being less o an expense than their contributiontowards the

coverage.

6

-

7/27/2019 Liazon White Paper on Afforable Care Act

7/8

Sticking with the Status Quo

Whilealargerpercentage(43%)ofsmallbusinessesaremorelikelytodropcoveragefor

individual exchanges than initially expected, the majority o

small businesses even

ater being exposed to details about healthcare reorm still

believe PPACA will

beharmfulfortheircompaniesandtheU.S.economy.Morethan50%ofsmallbusinessessay

that, given what they know o PPACA, they will continue to oer

employee healthcoverage.Severalreasonswilldrivethedecision:

Manyofthesecompaniesbelievethatemployeewell-beingismoreimportantthancost,

asserting that employees need and depend on the coverage the

companyprovides.

Thesecompaniesplantocontinueofferingcoveragebecauseitisanimportantpart

o their compensation package, and they are committed to oering

thebeneft.

Unlikelargecorporations,wherepersonalrelationshipsarelimited,smallbusinesses

tend to have a deep-seated loyalty to their employees, many o

whomthey know personally, and want to provide or them directly.

Somesmallbusinessrespondentswillcontinuetoofferplansprimarilybecausethey

believe that healthcare benefts signifcantly help to attract and

retain talentand that the benefts they oer are more extensive than

competitors plans.

Within the small business segment surveyed, companies with

higher income and higheremployee salaries were less likely to

consider giving up employee beneft plans, in partbecause they are

not eligible or subsidies, than businesses with lower income and

loweremployee salaries and wages that are eligible or

subsidies.

Firms with revenue o at least $10 million are the most likely to

say they will continueoering health coverage; the likelihood o

continuing coverage tends to decline with salesrevenue. In all o

the trade-os, preerence or Individual or other exchange options

ishighest or lower revenue companies.

7

-

7/27/2019 Liazon White Paper on Afforable Care Act

8/8

A Tidal Wave?

While one-third o small businesses are not sure how their

competitors will respond toPPACA reorms, many believe the

competition will wait and see what other companies do

beore making any decisions.

Basedonthesurveyndings,andgivenhumannature,wecanassumethatoncetheearly

adopters choose to stop providing coverage, and decision makers

begin to see thatemployees will be well-covered through exchanges

at a potentially lower cost and withoutthe administrative

headaches, many more small businesses will opt to abandon

privatecoverage and move to individual exchanges than previously

thought

With these shiting attitudes among small businesses, carriers

and brokers will be orcedto adjust and fnd new ways to keep them

satisfed.

Small-businessdecisionmakersarenotinthehealthinsurancebusinessandshouldntbeexpectedtounderstandallthecomplicatedchangesthatareforthcoming.Brokers,

thereore, have an opportunity to educate and guide their clients

through the maze sothey can understand the available choices and

the impact on their businesses. It is nolonger good enough or

brokers just to maintain the status quo, because there is nonstatus

quo, at least or a while.

The time has come or brokers to gather independent inormation

rom carriers and otherexperts, demonstrate their knowledge,

communicate clearly and eectively, and lead thebusiness community

as a trusted partner in a changing world. This is the only path

toretain relevance.

How the Survey was Conducted

Theresultsofthe2012LiazonPPACAImpactandAwarenessSurveyarebasedon601online

interviews conducted by Phoenix Marketing International between

December 10and December 21, 2012, with 601 benefts decision-makers

at companies with no morethan 50 employees.

To minimize political bias, the survey was perormed ater the

outcome o the 2012Presidential Election had eliminated much o the

uncertainty surrounding implementationo PPACA.

Participants were selected on the basis o their role in

healthcare benefts decision-making or their company. The sample

included a random selection o 501

frmsnationwide,plusanoversampleof100smallbusinessesinNewYorkState.Intheory,

in 95 cases out o 100, overall results based on a national

sample o this size will

dierbynomorethan4.4percentagepointsineitherdirectionfromwhatwouldhavebeenobtainedbyseekingtointerviewallsmallbusinessesintheUnitedStates.

8