Embed Size (px)

Citation preview

fll~!fck-5Jf7 ItJ15'L/()

* LGU FINANCING PRESENT SOURCES,

AVAILABILITY AND TERMS

by

CARLOS B. GAVINO LGU BOT Financial Adviser

CCPAP BOT Center June 1998

United States Agency for International Development (USAID) Philippine Host Country Contract

• Local Government Umt (LGU)

LGU Financing Present Sources, Avazlabzlzty and Terms

TABLE OF CONTENTS

Preface 1

Introduction 3

Objectives 5

Chapter I - Framework for LGU Financing 7 Government's New VIsion and Policy Framework 9

Chapter II - Current Sources and Assessment of LGU Financing 13 Internal Revenue Allotments 13 Local Resource Mobilization 14 Debt FinanCing 15 Public Sources 15

- Government Financial Institutions 15 - OffiCial Development ASSistance 19 - Municipal Development Fund 20 - Bilateral Sources 22

Private Sources 22 - Pnvate Commercial Banks 23 - Municipal Bond Flotations 26

Other Pnvate Sources 29 - BUlld-Operate-Transfer Schemes 29 - Provincial EqUity Funds 35 - LGU Guarantee Corporation (LGUGC) 35 - Other Forms of Private Sector PartiCipation 36 - Joint Ventures 37

New Proposed Multilateral Initiatives on LGU FinanCing 38 - LGU Infrastructure FaCility (LGUIF) 38 - LGU Infrastructure Finance and Development Project 38

Bilateral Programs Involving LGU FinanCing 39 - Governance and Local Democracy Project (GOLD) 39 - Growth with EqUity In Mindanao Project (GEM) 40

Chapter III - Constraints to LGU Access to Private Capital 41

Chapter IV - Recommendations 45

Conclusions 49

Annexes 51

LGU Fmancing- Present Sources, Availability and Terms

ABBREVIATIONS AND ACRONYMS

ADB BAC BOT BSP CCPAP COA CPVDC DBP DOF GEM GFI GOLD GSIS HIGC ICC LBP LGC LOGOFIND LGU LGUGC LGUIF LWUA MDF NCR NEDA ODA PIDS PNB ROI SSS USAID

ASian Development Bank Batangas Assets Corporation Build-Operate-Transfer Bangko Sentral ng Pillplnas Coordinating Council of the Philippine Assistance Program Commission on Audit Cebu Property Ventures Development Corporation Development Bank of the Philippines Department of Finance Growth with Equity In Mindanao Government Financial Institution Governance and Local Democracy Project Government Service Insurance System Home Insurance Guarantee Corporation Investment Coordination Committee Land Bank of the Philippines Local Government Code LGU Finance and Development Project Local Government Unit Local Government Unit Guarantee Corporation Local Government Unit Infrastructure FaCility Local Water Utilities Administration Municipal Development Fund National Capital Region National Economic and Development Authonty Official Development Assistance Philippine Institute for Development Studies Philippine National Bank Rate of Return on Investments SOCial Secunty System United States Agency for International Development

LGU Financing Present Sources, Availabillty and Terms

PREFACE

This paper presents a compilation

and assessment of current

sources of financing for Local

Government Unit (LGU) Infrastructure

projects It was derived mainly from the

presentations of speakers at the 1997 year

long Regional LGU Flnancmg Seminar se

ries sponsored by the Bureau of Local Gov

ernment Fmance (BLGF) of the Department

of Finance (DOF) and the Coord mating

Council of the Philippine Assistance Pro

gram (CCPAP) BUild-Operate-Transfer Cen

ter. The semmar series IS the brainchild of

the Department of Fmance and the CCPAP.

Inspired by the SPirit of the Local Govern

ment Code, the message was clear "Devo

lution has brought the burden of flnancmg

basIc services and development squarely

on the shoulders of each LGU. Let's help

ease the burden through an Information

campaign by brlngmg the LGU flnancmg

programs of both public and private sector

fmancmg agencies directly to LGUs, start

Ing from region to region until the whole

country IS covered" Profound gratitude

IS due to the three sponsoring financial in

stitutions, the Development Bank of the

Philippines (DBP), the Land Bank of the

Phlllppmes (LBP) and the PhilipPine Na

tional Bank (PNB) whose support has made

the seminar series possible. Gratitude is

also due to my co-speakers m the seminar

series, mcludmg Ms CeCilia Borromeo of

the Land Bank, Mr. Josefmo R. Gamboa of

1

the Philippine National Bank, Mr Armando

O. Samla of the Development Bank of the

Philippines, Mr. Raul Nlvera of the Multina

tional Investment Bancorporatlon, and

Director Erllto Pardo of BLGF, and others

too numerous to cite. Special thanks goes

to Undersecretary CeCilia G. SOriano of the

Department of Finance (DOF) for frammg

the Government's new Vision for LGU financ

mg whose implementation she IS vigorously

pursumg The author also Wishes to recog

nize the assistance provided by Mr Jorge

M Briones, Deputy Executive Director of

the BOT Center, and Mmes. Soledad J Cruz

and Rosalia V. de Leon, Directors of DOF,

who proVided comments on the drafts of

the paper Gratitude IS also expressed to

Messrs. Michael S. Gould and Joseph S

Ryan, Jr of the USAID for their mvaluable

support to the project. Fmally, a word of

thanks to Rommel A. Canuto of the CCPAP

and Mmes Vilma Lopez, Lam P. Barlongay

and Ayan Hazelle L. Flores of the BOT Cen

ter who helped In the production of thiS

document Any shortcomings m the paper

are purely my own.

Carlos B. Gavino

LGU BOT Financial Adviser

CCPAP BOT Center

LGU Fmancing Present Sources, Availability and Terms

INTRODUCTION

The enactment of Republic Act

No 7160 otherwise known as

the Local Government Code of

1991(LGC) represents a major shift In local

governance In the Philippines It mandates

the devolution to the local government

Units (LGUs) of many functions previously

carried out by the National Government

Implementing Agencies (lAs) SpeCifically,

the LGC's policy declaration states: ". The

State shall proVide for a more responsive

and accountable local government

structure instituted through a system of

decentralization whereby local government

Units shall be given more powers, authority,

responsibility, and resources "1 The LGC

prOVides greater autonomy to the LGUs In

mobiliZing resources and allocating these

for the efficient delivery of basIc serVices,

facilities and other needs To carry out

these functions, the LGC calls for the es-

tabllshment In every local government Unit,

an efficient and dynamic organizational

structure and operating mechanism that

will deliver the basIc services and meet the

Priority needs and reqUirements of ItS

communities.

financing LGUs have traditionally relied on

their share of national government wealth

through the internal revenue allotments

(IRA), their own local resource generation,

and loans from the Government Financial

Institutions (GFls) and the Municipal

Development Fund (MDF). While these

sources adequately served the financing

needs of the 80's and the early 90's, they

have proven to be Inadequate In responding

to the increasing needs of the LGUs today

and In the future This IS eVidenced by the

growing popularity of non-traditional

sources offlnanclng such as Bulld-Operate

Transfer schemes (BaTs), mUnicipal bonds,

JOint ventures, and lately, the emergence

of an LGU guarantee facility to guarantee

private commercial loans. In addition, a

private sector provincial equity fund has

been established for the first time In the

country While the private sector LGU credit

market IS gradually evolving, the Govern

ment continues to playa key role In LGU

credit markets by providing the overall

policy framework for LGU financing and

vigorously promoting private sector parti

cipation In LGU Infrastructure financing.

The paper discusses these tOPICS In detail,

The history of LGU financing and prOVides a directory of sources of LGU

demonstrates the need for new avenues of financing at the end of the paper.

1 Local Government Code of 1991 (Repubhc Act No 7160), SectIOn 2

Previous Pag~ Blank 3

LGU Financing Present Sources, Avmlabllzty and Terms

OB.lECTIVES

The audience of the paper IS

directed mainly to the chief

executives, planning and

development officers, treasurers, assessors

and members of the Sanggunlan Body of

the LGUs and all other local officials

Involved In financing basIc services and

Infrastructure projects of LGUs Through

o

o

proVide an assessment of the current

sources of LGU finanCing terms and

prospects;

d,scuss the constraints In LGU access

of expanded fInanCing sources,

pnmanly from the pnvate sector; and,

these individuals, the commUnities at large 0 formulate recommendatIOns to en

In the countryside would benefit most from hance financing of LGU basIc services

the Information on the resources available

to LGUs for funding projects In their

respective communities The specific

objectives of the paper are four-fold

and Infrastructure reqUIrements,

The paper IS diVided Into four chapters'

Chapter I sets the framework and the

Government's new vIsion for LGU finanCing,

o update the LGUs on the fmanclng Chapter II descnbes the different sources

programs and polICies of major of long-term finance for LGU projects and

InstttutlOns Involved In LGU flnancmg, proVides an assessment of these sources

including the NatIonal Government and and future prospects Chapter III discusses

Its agencIes, GFls, commercIal banks, the constraints to LGU access of pnvate

multtlateral and bilateral agencies, capital markets, and Chapter IV gives the

mUnicIpal bond underwriters, and summary recommendations and

public and pnvate finanCing sources; conclUSion

PreVious Page ':IIQ'n J,. 5

LGU Financing Present Sources, Availability and Terms

Chapter I - Framework for LGU Financing

, ,

local Government Code of 1991 financial autonomy provided to LGUs, many

(lGC) innovative approaches In financing and

Implementation are now being explored by

Prior to the passage of the LGC, the the more progressive LGUs.

delivery of basIc services and other activi-

ties ofthe LGUs were financed from resour

ces provided by the National Government

(NG) Thus, Investment plans and PriOrity

development programs were determined by

the national agencies with minimal

consultation and Involvement of the LGUs.

Development In the countryside was

essentially a national activity. This arrange

ment and budgeting system proved to be

cumbersome and ineffiCient, and subject

to political lobbYing In Manila. The lAs,

rather than the LGUs, determined pnorlties

and plans Realizing this predicament, the

country's legislators drafted the LGC.

To ensure the effective and timely

delivery of basIc services and other

activities, the LGC decentralized the

functions of basIc service delivery,

investment planning and development, and

program formulation, consolidating most

ofthe eXisting laws and regulations covering

local government operations and

Intergovernmental relationships With

decentralized planning, local offiCials have

taken the lead In shaping the pattern of

local development, and Implementing

Priority projects and delivery of basIc

Infrastructure, health, social and

environmental services. Inspired by the

Devolution of basIc services and other

activities as provided for In the LGC IS

expected to lead to a more effective means

for addreSSing the minimum basIc needs

of the local communities. The devolved

activities Include the provIsion of mUnicipal

Infrastructure such as public markets, bus

terminals and roads, water supply and

Sanitation, solid waste management, school

construction, basIc health services, social

welfare, environmental protection and

agricultural extension. While the medium

and long-term prospects for delivering these

basIc services are bright, so far, most

devolved projects that have been or are

being Implemented by LGUs Involve public

markets, water supply and bus terminals

However, many LGUs are now developing

projects In other PriOrity areas such as

airports, land reclamation, small power

projects, and environmental projects

Legal Framework. The legal framework

for LGU financing lies In the LGC, which

provides for the sharing of LGUs In the

proceeds of national taxes, local taxation

and fiscal matters, credit financing, and

build-operate-transfer schemes These

resources and forms of financing are

described as follows

PreyfoWi Page Blank 7

LGU Financing Present Sources, AVailability and Terms

o Internal Revenue Allotments (IRAs) -

These consist of local governments'

share In the proceeds of national taxes

which constitute 40% of total national

Internal revenue taxes, with fixed

percentage allocations to LGUs:

provinces (23%); cities (23%);

municipalities (34%) and barangays

(20%), and for each LGU, on the basIs

of population (50%), land area (25%)

and equal sharing (25%),

o Local Taxation and FIscal Matters -

Local governments have been given the

authority to exerCise their power to

create their own sources of revenue,

and to levy taxes, fees, and charges

subject to specific provIsions,

consistent with the basIc policy of local

autonomy. They also have been given

more responsibility for operating the

real property tax system;

o CredIt Financmg - The LGC provides

more liberal rules for LGU borrowing

loans, credits and other forms of

indebtedness with any government or

domestic private bank and other

lending institutions, deferred payment

and other Investment schemes, bonds

and other long-term securities, Inter

LGU loans, grants and subsidies, and

loans from foreign sources onlent by

the National Government The process

for availing of credit financing has also

been liberalized No longer are LGUs

required to seek Department of Finance

(DOF) approval before seeking bank

credit approval. Furthermore, they no

longer need Commission on Audit

(COA) certification of their borrowing

capacity prior to applYing for a loan

However, the Code sets a limit on LGU

Indebtedness "the amount of

appropriatIOn for debt servlcmg shall

not exceed 20 percent of the regular

Income of the LGU concerned" 2,

effectively putting a cap on the total

Indebtedness capacity of LGUs,

The basIc policy provides for any LGU 0 BUlld-Operate-Transfer(BOT) Schemes

to create Indebtedness, and avail of

credit facilities to finance local

Infrastructure and other SOCIO

economic development projects In

accordance With the approved local

development plan and publiC

Investment program The policy allows

2 Local Government Code of 1991 (Republic Act No 7160), SectIOn 324 (b)

8

- The LGC also allows LGUs to enter

Into contracts for financing, construc

tion, operation, and maintenance of

Viable Infrastructure projects under the

bUild-operate-transfer schemes as

proVided by R.A No 7718 (BOT Law).

LGU Fznancing Present Sources, Avazlabllzty and Terms

Government's New Vision and Policy The vIsion and policy framework

Framework for LGU Financing statement rests on two mam premises

Spurred by the mcreasmg need by 0

LGUs to fmance the devolved services

within the framework of the LGC, the DOF

formulated a new vision and policy

LGUs have varying levels and records

of credItworthiness and bankabillty,

and theIr financing needs are huge; and

framework for fmanclng local governments' 0 the private sector (BOT Investors,

basIc services and development projects

predicated on promoting self-reliance for

LGUs 3. The policy framework defmes the

respective roles of various players Involved

In LGU fmanclng, I.e. the NG, government

financial Institutions (GFls), private

commercial banks and fmanclal sources,

municipal bond market players, the

multilateral agencies, the Municipal

Development Fund (MDF), and BOT

proponents.

The ultimate objective IS to encourage

LGUs to rely less on transfers from the NG,

and more on locally generated resources,

and to mcrease LGU access to private

funds. In order to do thiS, the policy

framework makes recommendations on

rationalizing Official Development

Assistance (ODA), encouragmg LGUs to

raise more locally-generated funds,

enhancmg pnvate sector participation m

flnancmg LGU mfrastructure projects,

building-up project management capacity,

and promotmg LGU creditworthiness.

bondholders, commercIal banks), the

GFls and MDF all have an Important

role to play In meeting LGU financing

reqUIrements.

Taking these Into account, the

Government passed a resolution (the

Investment Coordination Committee or ICC

resolutlon 4) that governs national

government grants, I e that these grants

will be given selectively on the baSIS of

equity, externalities, and economies of

scale

In addition, the Government is puttmg

m place a program to rationalize lendmg of

GFls to LGUs as well as ODA assistance.

The program IS premised on re-focuslng GFI

and ODA lendmgto less-creditworthy LGUs

with limited access to pnvate sources of

financing, and to finance SOCial and

environmental projects. Finally, the

Government IS actively pursuing a program

to expand LGU access to private capital

markets to complement the traditional

3 LGU Financmg of BasIc ServIces and Infrastructure Projects, A New VISIOn and Policy Framework, Department of Fmance, October 1996

4 The ICC resolutIOn prOVIdes NatIOnal Government (NG) support III the form of matching, speCIfic and close-ended grants for LGU devolved

actlvltles WIth SOCtal and/or envIronmental obJectlves III four sectors water supply, health, envIronment and ru~al Illfrastructure (rural roads, communal lITIgatIOn, public markets and slaughterhouse) The grants are gIven to LGUs on a matchmg baSIS by Illcome class and type of devolved aCtlvlty, e.g. for watershed protectIOn or mumclpal fishery management, 4th - 6th class LGUs WIll receIVe NG grants on a 70 30 shanng baSIS

9

LGU Financing Present Sources, AvailabilIty and Terms

sources of LGU financing. The program

Includes the following specific courses of

action·

a. Increase LGUs' use of BOT - like

arrangements and other forms of

private sector participation. BOT

arrangements provide unique

advantages to LGUs which are not

found In other sources of financing.

Among these are little or no initial

Investment requirements; proper risk

allocation where the financing, design

and construction risks are borne by the

private sector; transfer of technology;

effiCiency In operations and financing

of capital requirements through the

long-term concession agreement.

Other forms of privatization (page 36)

are also being promoted by the

Government

b. Develop the LGU municipal bond

market. The Government has

recognized the potential of one

untapped finanCial source - the

muniCipal bond market. Thus, the

Government IS keen on developing,

through the private sector, a credit

rating system for LGUs to support an

LGU muniCipal bond market, and

supporting the credit guarantee

corporation being spearheaded by the

Development Bank of the Philippines

and the Bankers Association of the

Philippines which would provide

guarantees to muniCipal bonds and

commercial credit Instruments

c. Promote LGU access to private

sources. The Government considers

LGU access to private sources of

financing as a key measure In

sustaining long-term economic growth

In the countryside One Issue raised

by pnvate sources IS the lack of a

business relationship between

commercial sources offlnance and the

LGUs due to the eOA ruling on LGU

deposlts5 . To address thiS, two market

based measures are being explored by

the Government to Improve access to

private sources: (I) liberalizing the LGU

depOSitory bank regulations to explicitly

allow LGUs to establish depOSitory

banking relationships with Bangko

Sentral ng Pillplnas (BSP)-accredlted

private banks, and (II) extending the IRA

Intercept mechanism (allOWing GFls to

hold LGUs' I RAs against debt service

obligations) to Include accredited

private banks.

d. Optimize the involvement of GFls in

LGU financing. Although GFls'

Involvement In LGU finanCing IS

extensive, some measures can be

undertaken to further optimize the GFls

Involvement such as (I) adopting a

graduation scheme to move the more

creditworthy LGUs to the pnvate credit

markets; (II) developing co-financing

5 COA CIrcular 92 mstructs LGUs to open and mamtam depOSItory accounts wIth banks "preferably government-owned" located m or nearest

to thelr respectIve areas of JunsdIctIOn

10

LGU Financing' Present Sources, Avallabiltty and Terms

schemes with private commercial

banks; (III) Improving LGU credit

worthiness through technical assIs

tance; (IV) coordinating GFI LGU credit

programs with the MuniCipal

Development Fund (MDF). and (v) g

structuring ODA- sourced lending

programs for non-revenue generating

SOCial projects or for revenue

generating but long-gestating projects

and (IV) proposing amendments to the

LGC to strengthen local treasury

operations and prOViding incentives for

greater local revenue mobilization

e. Restructure and reorient the MOE

As a disbursement mechanism for

ODA-supported loans and grants

administered by the Bureau of Local

Government Finance under the DOF,

the MDF's role can be enhanced to

Implement an LGU graduation policy,

I.e. graduating more creditworthy LGUs

from concesslonal MDF funds toward

GFls or the private sector, and helping

LGUs build a track record of

creditworthiness.

Tap ODA technical assistance and

financing. ODA financing plays a key

role In the Implementation of economic

development programs of LGUs.

Closer coordination between the

donors and the concerned government

agencies and LGUs will faCIlitate the

flow of funds to the LGUs. The

Government IS contemplating ways of

uSing ODA funds to Increase the

partnership with the private sector, and

to target ODA funds so that creditworthy

LGUs are encouraged to tap

commercial sources of funds, and

financial and managerial capacity is

gradually bUilt-up In the less

creditworthy LGUs.

f Improve the capacity of LGUs to

raise their own rev~nues. The

Government recognizes that an

Important factor In enhancing LGU

The Government IS vigorously pursuing

the Implementation of these actions and

recommendations to ensure access of

LGUs to a Wider range offinanclng sources,

and to develop LGU capability for

creditworthiness IS to Increase the Implementing Priority Infrastructure

capacity and Willingness of LGUs to projects.

raise local revenues. Steps are being

taken by the Government to achieve

thiS objective, including: (I) Improving

the mOnitoring of LGU revenues and

expenditures; (il) IntensifYing the

training and supervIsion of local

finance offiCials; (IIi) reviewing real

property taxation rules and procedures,

11

With regard to National Government

guarantees, the Government's poliCY IS

clear toward risk management and

guarantee provIsions for projects

undertaken by LGUs In cooperation with the

private sector Consistent with ItS vIsion

and poliCY framework to wean away the

LGU Fmancmg Present Sources. AVa/labllity and Terms

LGUs from dependence on the National

Government and to support the principle

of devolution espoused by the Local

Government Code, the National

Government IS advocating a proper

unbundling of risk and appropnate nsk

sharing between the pnvate sector and the

LGUs concerned. For example, In the water

sector, It IS advocating to limit concesslonal

funding and National Government

resources to those smaller I marginal water

dlstncts which are unable to attract pnvate

Investors, but which will eventually graduate

to creditworthy status sometime In the

future. Water dlstncts which are able to

attract pnvate sector investments, would

be directed to tap the private credit market,

the GFls and the pnvate sector for financing

dlstnbutlon system Improvements and bulk

water supply. Advocating the pnnclples of

project finance, the Government believes

that projects with strong private sector

Interest should rely on project cash flows

and project-related credit enhancements

(e.g. escrow accounts, assignment of

receivables and "step-in" nghts) to proVide

comfort to ItS Investors.

12

LGU Fmancing Present Sources, Availability and Terms

Chapter II - Current Sources and Assessment of LGU Financing

The passage of the 1991 Local sources of financing. The current sources

Government Code signaled the emergence of LGU Financing are shown In Chart A

of a new market for credit financing - the

LGUs No longer confined to sourcing their Internal Revenue Allotments (IRA)

requirements from the GFls and the

MUnicipal Development Fund, which over

the years, has been the LGUs' major source

of long-term credit finance, the LGUs have

taken a keen Interest In tapping vanous

other sources of financing to meet their

financial requirements. The Code allows

the LGUs to directly Incur Indebtedness on

their own account without pnor clearance

from the National Government Thus, LGUs

have floated their own bonds, entered Into

BOT contracts and JOint ventures, and

signed lease agreements with private

Chart A. LGU Financing Options

'--_--' G

13

As a result of devolution, the main

source of LGU finances has been the IRA,

the share of LGUs In the national taxes. In

1996, over P56 billion was transferred to

the LGUs as their share of the national

taxes Over the years, the share of IRA as

a percentage of total LGU revenues

(combined for prOVinces, cities and

municipalities) has been increasing as

shown In Chart B.

In 1991, the percentage of IRA to total

revenues was only 40.7%, gradually nSlng

to 61.9% In 1993, and 61 4% In 1995,

Signaling the LGUs' reliance on the IRA to

fund ItS expenditures However, the

situation has reversed as of late. In 1996,

the share of IRA to total revenues has fallen

to 53.8%, slgnrfylng that LGUs have started

to mobilize financing from other sources

(local resource mobilization and loans). The

annual percentage of IRA to total Income

for the penod 1991-1996 IS shown In Annex

1. If this trend continues, LGUs will, In

future, rely less on the National Government

for financing basIc services and

Infrastructure requirements and more on

other sources of flnancln!5 However, the

LGU Financing Present Sources. AVailability and Terms

Chart B.

Source

Note

Chart C.

IRA as Percentage of Total LGU Revenues (%)

55.9 61.9 61.2 61.4

1991 1992 1993 1994 1995 1996

Bureau of Local Government Fmance (OOF)

Barangay data are not mcluded m the chart

53.8

IRA allocation formula continues to favor

large highly urbanized LGUs For example,

the City of Makatl, which IS finanCially self

suffiCient, continues to receive substantial

amounts of IRA. Another city In Metro

Manila was able to borrow more than P1.5

billion last year from a GFI while stili

receiVing substantial IRA Many LGUs, on

Local Resources as Percent of Total LGU Revenues (%)

1991 1992 1993 1994 1995 1996

Source:

Note

Bureau of Local Government Fmance (OOF).

Barangay data are not Included m the chart

the other hand, which have limited access

to private resources, receive much less IRA

than these cities. The other Issue with

regard to the IRA formula IS the lack of

incentives for LGUs to generate more local

resources as the formula IS based on

population, land area and equal shanng

Therefore, there has been clamor from

some LGUs for the Government to review

the IRA allocation formula to promote equity

and effiCiency

Local Resource Mobilization

LGUs' local resource mobilization

followed a pattern consistent with that of

the IRA. As shown In Chart C, the LGUs'

local resources In 1991 were about 56.1%

of theIr total Income. The succeeding years

witnessed a gradual decline In the

percentage share of local resources to

36.9% In 1993 and In 1995 Among the

reasons for the decline are the Increases

In IRA allocations and the decline In

revenues from low tax assessments. In a

preliminary study conducted by the World

Bank6, the paper concluded that many large

cities and small towns rely substantially on

non-tax revenues and IRA allocations for

sourcing revenues, and that tax

assessments and business tax compliance

appear to be extremely low. However, the

analYSIS shows that there IS ample

opportunity for LGUs to greatly Improve

financial performance. In fact, the LGUs'

revenue generating performance In 1996

6 LGU Urban Water and SamtatIons Project PreparatIOn MISSIon, World Bank Alde-MemOlre, June 1997

14

LGU Financzng' Present Sources, AVallabzlity and Terms

bears this observation, where LGUs' own

resources as a percentage of total

resources made a dramatic Improvement

to 45 3% from 36 8% the year before. The

annual percentage of locally generated

funds to total LGU Income by type of LGU

IS shown In Annex 2.

considering plans for expanding Into direct

LGU financing.

Private sources consist of financing

provided by the commercial banks

[primarily by the Philippine National Bank

(PNB) which was a GFI until recently

privatized], and mUniCipal bond flotations,

In general, many mUniCipalities also which so far has been In the hOUSing sector

tend to horde surpluses In cash, foregOing but IS now geared to prOVide funding for

the opportunity to leverage funds Into other LGU Infrastructure projects.

higher yielding Investments Furthermore,

Increases In local revenues through more Public Sources of Debt Financing effiCient taxation could prOVide the

necessary resources for LGUs to make Government Financial Institutions

worthwhile Investments In baSIC services (GFls)

such as water and sanitation, health,

education and rural Infrastructure. Thus, Background. Traditionally, the LGUs

opportunities are there for LGUs to expand have turned to the GFls for their short to

their local resource base and benefit from intermediate credit finance requirements

leveraging eXisting resources. GFI lending served the LGUs well until the

mld-1980s, when many LGUs began to

Debt Financing

Apart from IRAs and local revenues,

LGUs have availed of debt finanCing to

finance their capital requirements. Debt

finanCing for LGU projects come from two

main sources

o publiC sources; and,

o private sources

Public sources of debt finanCing

continue to come primarily from the GFls,

I e. the Land Bank of the Philippines (LBP)

and the Development Bank of the

default on their obligations due to the severe

economic slump resulting from the political

uncertainty In the country. Despite the IRA

Intercept mechanism, unpaid obligations to

the GFls rose to as much as P2 1 billion In

1985, which led to the cessation of lending

by GFls to the LGUs. As a result, the

National Government had to carry out a

debt relief program for the LGUs. Since

then, however, With the Increase In IRA

allocations and better fiscal management,

the repayment track record of LGUs has

Improved, allOWing GFls to resume lending

to LGUs.

Philippines (DBP) However, pension funds, To carry out the government's mandate

notably the Government Service Insurance to promote sustainable development In the

System, and the Social Security System are countryside, and encouraged by the

15

LGU FInancing Present Sources, Availability and Terms

Chart D.

8000

7000

6000

5000

4000

3000

2000

1000

decentralization and the greater autonomy

accorded the LGUs, the GFls established

loan funds specifically targeted to LGU

lending The Land Bank of the Philippines'

LGU financing program was In place from

the time of establishment of the Bank In

1963 To date, It has lent over Pll.6 billion

In the country with total resources of some

P134 billion, has been lending actively to

LGUs over the years It has a social mission

of promoting countryside development and

has been a major contributor to rural credit

delivery in the Philippines Though LBP's

main portfolio of loans IS In the agrarian

to LGUs. The Development Bank of the sector, It has a very active LGU finanCing

Philippines established its Countryside

Lending (Window III) to extend loans

exclusively to countryside projects. Two

other government agencies, the Social

Security System (SSS) and the Government

Service Insurance System (GSIS) were also

active, but did not finance capital or

Infrastructure projects The SSS targeted

livelihood and hOUSing projects, while the

GSIS proVided Insurance coverage for LGU

Investments as well as hOUSing loans for

government service personnel

Land Bank ofthe Philippines. Created

In 1963, the Land Bank of the Philippines

(LBP), one of the top five universal banks

Land Bank LGU Financing Portfolio as of March 1997 In Peso Millions

16

program consistent With ItS mission.

Foremost In LBP's LGU finanCing program

IS ItS "Total Development Options - Unified

Land Bank Approach to Development or

TODO-UNLAD program." The program

offers a comprehenSive package of loans

that links farmers' cooperatives, private

companies, rural banks, non-governmental

institutions and LGUs around an Income

generating project In a speCifiC area

The Land Bank's LGU program has

financed projects In various sectors

amounting to over Pll 6 billion as of March

1997, primarily In Infrastructure, bus

terminals, public markets, telecommu

niCations, hOUSing, water systems, road

construction and traffiC systems Chart D

shows the distribution of the LGU portfoliO

of Land Bank.

The chart indicates that majority of

Land Bank lending to LGUs has been

directed to Infrastructure finanCing (61%).

These projects Included Integrated

development projects In Metro Manila and

Metro Cebu consisting of roads,

reclamation, ports, schools, mUniCipal and

commercial bUildings, etc. The next major

exposure of Land Bank was In heavy

machinery (15%), which are used by LGUs

In carrYing out their development and

LGU Fznancing Present Sources, Avazlabilzty and Terms

Infrastructure projects Lending to Land Bank assistance. Eligible loans

construction projects amounted to 7% and

the rest were for sport complexes, public

markets, bus terminals and others Annex

3 shows the geographical distribution of

Land Bank's LGU lending To assist Land

Bank In making their Investment deCISions,

It has developed a creditworthiness ranking

system for LGUs. This system claSSifies

LGUs Into four credit categories:

LGU Number of

Classification LGUs

Prime 41 J (17.4%) High Grade 252

Medium Grade 666 (395%)

Low Grade 726 (431%)

Total 1685 (100.0%)

Land Bank utilizes a set of criteria for

ItS LGU credit rating system, including

financial capability, socio-economlc profile,

political stability and the technical,

economic and financial Viability of the

proposed project. As shown In the above

table, about 17% of LGUs are classified by

the LBP as prime clients and high grade,

while 40% are claSSified as medium grade.

Land Bank's lending policy IS limited to

LGUs With a medium-grade or higher

claSSification

Terms of Credit. As mentioned In the

prevIous paragraph, Land Bank lends to

proVinces, cities and municipalities that are

rated medium-grade or higher. USing thiS

criterion, some 960 LGUs are eligible for

finance local Infrastructure and other SOCIO

economic development projects under

LGUs' local development plans. The

maximum loan amount IS based on the

reqUirement of the project but does not

exceed the "Net BorrOWing Capacity"

calculated for LGUs as defined In the Local

Government Code. LGUs tYPically will

contribute 25% of the total project cost; the

terms of the loan will not exceed 5 years

and the maximum grace period on principal

IS two years. Interest rate charged IS the

prevailing market rate. Collateral

requirements can Include a holdout on LGU

depOSits; real estate property, machinery

and equipment and a deed of assignment

on IRA, regular taxes or net Income. The

LGU lending program requirements and

procedures of Land Bank are reproduced

In Annex 4.

Development Bank of the Philippines

(DBP). The Development Bank of the Philip

pines has been lending to LGUs since its

inception The centerpiece of DBP's coun

trYSide assistance strategy IS ItS Window III

program which assists activities that

facilitate the delivery of baSIC services that

enhance the quality of life of Filipinos, parti

cularly those of the disadvantaged groups

In the rural areas. To fulfill ItS commitment

to countryside development, DBP sets aSide

30% of ItS annual net after-tax Income for

ItS Window III program As of the end of

March 1997, a total of 1,517 loans had been

approved under the Program and total loan

releases amounted to P3.4 blillon7 •

7 Although DBP's Wmdow III aSSIsts projects m the countrysIde, only about 15% IS actually lent to LGUs

17

LGU Financing Present Sources, Availabllily'and Terms

Some of the LGU projects supported

by the DBP Include:

0 Expanded Public Transportation

Boundary Hulog Program

0 Schools and Hospitals Financing

0 Rural Electnc Cooperatives Special

Program

0 Damayan sa Pamumuhunan

Program

U Cattle Financing Program

0 Flshenes Sector Financing Program 0 LGU Financing Program

Compared to loans extended to coun

tryside projects, DBP's direct loans to LGUs

have been fairly limited. As of March 1997,

It has financed some 20 projects amoun

ting to P395 million as shown In Chart E.

Majonty of DBP's LGU assistance were

for projects Involving heavy equipment or

Chart E. Development Bank of the Philippines LGU Financing Portfolio As of March 1997 In Peso Millions

18

for construction projects amounting to

P85.0 million (21.5%). Next to these are

public market projects amountingto P54 3

million (138%) The DBP also lent for a

diagnostic center (P58 0 million), a major

resettlement project of P50.0 million and

water supply systems costing P45 5 million

(11.5%). The LGU lending program

requirements and procedures of the DBP

are reproduced In Annex 5.

Assessment of GFI Lending

Current Volume and Prospects for

Growth. The portfolio of loans granted to

LGUs between the DBP and the LBP as of

March 1997 amounted to some P12 0

billion, majonty of which was lent by the

Land Bank GFls remain the major source

of credit finance for LGUs Furthermore,

the LGU programs remain a profitable

portfolio for GFls and current recovery rates,

as well as prospects for longer-term

profitability, are good. LGUs have begun to

pursue new Investments In Infrastructure

as the economic development In the

countryside has started to take root The

DBP, In particular, IS a major force behind

the establishment of the LGU Guarantee

Corporation (discussed later In the paper),

which Will enhance commercial lending to

LGUs. The Land Bank, for ItS part,

continues to be a major source of financing

for LGU projects. Because of the presence

of GFI branches In most localities In the

countryside, GFls have established close

relationships with LGUs. Thus, GFI lending

to LGUs IS expected to expand dramatically

LGU Fmancing' Present Sources, Avmlablhty and Terms

over the next couple of years, because of

the market niche It has established.

Loan Distribution and Terms. The

GFls have lent to all classes of

municipalities. Geographically, the

distribution is skewed towards Luzon and

In particular the National Capital Region

(NCR) with over 50% of total LGU lending

because ofthe concentration of commerce

and Industry. The terms of lending ranges

from 3 years to 5 years (In some cases, up

to 7 years) which IS stili short to medlum

term 8. ThiS IS a major constraint to

Infrastructure project finanCing as the

gestation period of many Infrastructure

projects IS longer In the case of BOT

projects, the concession period goes

beyond (up to 25 years), although cash flow

recovery may be for a much shorter period.

In thiS case, the GFI loans, If availed, Will

need to be re-flnanced or rolled over at the

time the loan repayment IS due

The GFls at the moment are not

Inclined to lend beyond seven years until

such time as the repayment track record

of LGUs IS fully established or once credit

enhancements are In place. One way of

accomplishing thiS IS the establishment of

an LGU credit rating system, which Will

mOnitor, among others, the repayment

capability of LGUs The Government IS

currently pursuing the establishment of an

LGU credit rating agency. As far as the cost

of borroWing IS concerned, market Interest

rates Will continue to favor the more credit-

worthy LGUs (first to third class mUniCipa

lities). Fourth and fifth class mUniCipalities

Will have to access the more concessionary

terms of the MUniCipal Development Fund

discussed In succeeding paragraphs.

Sector Coverage. For the time being,

the sectoral focus of GFI lending (In terms

of number of projects) continues to be the

small-scale, traditional projects such as

publiC markets, heavy eqUipment/machi

nery, bus terminals, small waterworks

systems, and others. However, Land Bank

has lent to major Infrastructure projects In

the NCR and In the Vlsayas. As GFls

become more and more comfortable

lending to LGUs, we should expect other

sectors to benefit from GFI lending and the

size of projects to Increase. These sectors

Include transportation, airports, solid waste

management and bigger waterworks

systems or bulk water supply from the

private sector Collateral and loan security

Will continue to figure prominently In LGU

lending and assignment of IRA Will be the

main form of security. However With the

advent of BOT schemes and as more LGUs

and GFls alike become familiar With project

finance, It IS expected that cash flows from

revenue-generating projects Will be the

main criterion for extending GFI loans.

Official Development Assistance

(ODA)

Another major source of public debt

finanCing for LGUs IS OffiCial Development

8 The DBP however, has a limIted loan program for LGUs under Its Wmdow III program that can extend terms up to 12 years

19

LGU Financing Present Sources. AVallabllity and Terms

Assistance (ODA) from multilateral financial

institutions such as the World Bank and

the ASian Development Bank (ADB) which

are channeled through the MUnicipal

Development Fund (MDF). In addition,

there IS also loan funding available through

financial Intermedlanes and counterpart

agencies, and from Bilateral Fmanclal

Agencies such as the Overseas Economic

Cooperation Fund (OECF) of Japan.

Board chaired by the DOF with three other

Government agencies as members, I e. the

National Economic and Development

Authority (NEDA), the Department of Interior

and Local Government (DILG) and the

Department of Budget and Management

(DBM). The MDF consists of two major

units, the Financial Unit, headed by the

Executive Director of the BLGF and the

Central Projects Office (CPO), the project

Implementation Unit for each project located

Municipal Development Fund (MDF) In participating agencies In the MDF ASide

from providing loans, the MDF also

Multilateral lending sources for LGU proVides technical assistance to LGUs for

projects have pnnclpally come from three project Identification and feasibility studies

main sources, the World Bank, the ASian and for other projects such as the Real

Development Bank and the Overseas Property Tax Administration Project, which

Economic Cooperation Fund of Japan aSSisted more than 800 LGUs In Improving

(OECF). The funds have been channeled their real property tax collection

through the MDF, a revolVing fund created

by a Presidential Decree in March 1984 to

consolidate the fragmented and

uncoordinated borrowing and grant system

to the LGUs The MDF is administered by

the Bureau of Local Government Finance

(BLGF) under the DOF Before the creation

of the M OF, the donor agencies reqUired a

central agency for monitonng the foreign

loans and grants With the establishment

of the MDF, a separate monitoring agency

was no longer needed, and thus, the MDF

became the condUit for foreign loans and

grants The MDF also played the role of a

monltonng unit and project accounting

support for foreign funds directed to the

LGUs.

Organization. The MDF operates

under the direction of a Policy Governing

20

Lending Operations. The MDF was

created as a revolVing fund and made

available to LGUs In undertaking their SOCIO-

economic development programs. It was

active in prOViding loans to LGUs In the

1980s when the GFls stopped lending to

the LGUs on account of mounting

uncollectible accounts Dunng thiS time,

the MDF channeled some P79 billion of

long-term finance to LGUs. LGU projects

that have benefited from assistance from

the MDF Include'

0 public markets

0 heavy eqUipment and machinery

0 bus terminals

0 sla ughterhouses

0 drainage and waterworks

0 roads

LGU Financzng Present Sources, Avaziability and Terms

o solid waste

o telephone systems

o health centers

At present, nine loans have been

provided by the World Bank, ADB, OECF

and Eximbank of Korea through the MDF

as shown In Annex 6.

Total loans extended under the nine

projects for all regions amounts to $290

million (PIO.7 billion at current exchange

guarantees the loan repayment. ASide

from providing loans, the MDF can also

provide a package of a loan and a grant,

which effectively lowers the LGUs'

borroWing costs. The loan component

carries the terms and conditions set by the

lender through the MDF Because of the

liberal terms of the MDF, particularly the

long-term prinCipal repayment feature, the

MDF has been extremely attractive to LGUs

Funding Limitation. At the moment,

rates) The greater access by higher MDF funding to the LGUs IS experiencing

Income LGUs to the MDF credit facility can constraints for several reasons:

be attributed to the requirement of financial

capacity and the ability ofthe LGU to repay 0 the Increased demand for MDF credits

the loans Other criteria also favor the

higher Income LGUs, such as urban

population minimum reqUirements and

annual population growth rates, annual

Income and equity requirements, and

by other developing countnes;

o funding limitations of the multilateral

institutions that support the MDF;

commitment to establish a separate project 0 constraints Imposed by the government

office With full-time staff With thiS In mind, budgetary process, and

and considering that the higher Income

LGUs have access to other sources of

funding, the Government, In Implementing

ItS new vIsion for LGU finanCing, IS

diSCUSSing With the multilateral finanCing

agencies, re-focuslng MDF assistance

toward less creditworthy LGUs.

Terms of Credit. The MDF IS, at

present, the only source of credit finance

that IS offering long-term finanCing With a

maturity penod of 15-25 years The Interest

rate IS currently set at 2 percent above the

weighted average Interest rate of 61-90 day

domestic time depOSits. No collateral IS

required since the IRA intercept mechanism

21

o Increasingly limited eligibility for MDF

assistance to the Philippines due to the

Increased economic development of

the country.

First, the worldwide demand for MDF

assistance and the Increase In

requirements by other less-developed

countries In the world has constrained the

availability of funds to meet the Increased

demand for MDF~funds from the

Philippines. The multilateral agencies, In

the pursuit of poverty alleViation objectives,

are shifting attention to poorer regions of

the world such as Africa. Second, the

LGU Financing' Present Sources, AVailability and Terms

multilateral mstltutlons that support the

MDF are expenencmg fundmg limitations

themselves and are encouragmg LGUs to

tap private sources of financing for

development assistance worldWide. Third,

the MDF's present lending capacity IS

constramed by the budgetary process of

the Government Each department of the

national government observes a budgetary

ceiling Imposed by Congress and the

Development Budget Coordinating

Government for LGU fmanclng, the MDF IS

bemg re-onented to be a more effective

Instrument In lending to lower class

municipalities, which have limited access

to pnvate sources of capital Reform of the

MDF IS bemg undertaken with World Bank

assistance. Because of the favorable terms

of MDF lendmg, the MDF IS expected to

continue to be attractive to LGUs for

fmancmg basIc services and mfrastructure

Committee. In practice, the budget Bilateral Sources of Debt Financing

submissions of the National Government

departments, which mclude budgetary

requests for MDF counterpart funds, are

subject to the ceilmg Fmally, as the

Philippine economy progresses, ItS

eligibility for mcreased MDF assistance IS

adversely affected, as one of the principal

cnterla for MDF assistance IS the economic

standing of the recIpient country

Assessment

Prospects for Growth. The MDF

continues to be a major source of

concessionary credit finance for LGUs

Smce ItS first loan (MUnicipal Development

Project I of the World Bank), the MDF has

been actively contnbutmg to the economic

development of LGUs by provldmg long

term fmanclng for LGU projects. It IS the

Another source of flnancmg for LGU

projects IS proVided by bilateral agencies

such as the Overseas Economic

Cooperation Fund of Japan (OECF) which

channels funds to national Implementmg

agencies for national projects In addition

to ItS assistance to agnculture and transport

projects at the local level, the OECF has

been active m proViding concessionary long

term lendmg to Water Dlstncts (WDs) all

over the country through the Local Water

Utilities Administration (LWUA) as described

m Box A. Although the WDs are stnctly not

a part of the LGUs (although ItS Board

members are appomted by the LGU chief

executive), they proVide basIc water services

to LGUs by constructmg, operating and

mamtammg the water systems of LGUs.

long-term feature of MDF loans and the Private Sources of Debt Financing

concessionary rate that has attracted the

LGUs Lately, however, some LGUs have Before the passage of the LGC, pnvate

vOiced concern regarding the long fmancmgfor LGU projects has been virtually

processmg time of MDF loans Therefore, non-existent as the LGU credit market was

steps need to be taken to streamline the dominated by the traditional "offiCial"

approval process. At the same time, sources offmancmg, I e the GFls and ODA

consistent With the new Vision of the However, smce then, pnvate fmanclng has

22

LGU Financing' Present Sources, AVailability and Terms

Box A

Local Water Utilities Administration (LWUA)

In order to promote, develop and finance local water utilities, optimIze public service water operations, and facIlitate the Improvement of local water servIces, the Local Water UtilitIes AdministratIOn (LWUA) was created m September 1972 under the Provincial Water Utilities Act. The LWUA is a specialized lending institution, which provides financing to water districts for water supply development, expansion and improvement. L WUA has evolved to be primarily a financmg agency wIth the following functions: .

• provide loans to quahfied local water utlhtles for theIr capital expenditure programs;

• establish standards for local water utIlities such as water quahty, design and construction of new or addItional facilities for water supply, treatment, transmission and dIStribution, and for wastewater collection, treatment and disposal;

• furnish technical assIstance and personnel traming programs for local water utilities;

• effect systems integratIOn, joint investments, water district annexatIOn and de-annexatIOn.

L WUA has, over the years, on-lent funds from ODA sources at concessionary rates. As of February 1998, L WUA has given loans of about P12.3 billion to 462 water districts. LWUA has also extended loans to rural waterworks and sanitation associations, whIch are non-stock, non-profit cooperative associatIOns, and franchised to operate rural water supply systems in remote areas where access to a water district is dIfficult. Many water distrIcts have benefited from low-interest, long-term loans of up to twenty-five years with ample grace periods. However, because of funding source constramts from its Donor agencies, L WUA has not been able to accommodate fundmg requests from all the water districts. As a result, some water districts (Bulacan, Metro Cebu, Puerto Princesa and Batangas CIty) have turned to alternative sources of financing such as BOT schemes and jomt ventures.

23

began to gain a foothold In the LGU credit

market as a result of the expanded

borrowing powers under the LGC, and as

the resource requirements of the LGUs

grew, creating a new, untapped market

With these developments, the LGU credit

market has opened up vast financing

opportunities for the private sector. For the

first time, the LGUs have a variety of private

funding sources for their projects. These

Include commercial bank lending which IS

expected to materialize with the creation

of a guarantee faCility, lending from the

Philippine National Bank, now clasSified as

a private commercial bank, and mUniCipal

bond flotations With adequate credit

enhancements these funding sources are

expected to fill a major gap In LGU

financing. These sources are discussed In

the follOWing paragraphs

Private Commercial Banks

Commercial Banks' Lack of

Interest in LGU Financing. In the past

and to some extent the present, there was

little Interest by the private banks In LGU

financing There were vanous reasons

including:

o the lack of expenence In dealing with

LGUs. Traditionally, private commercial

banks served pnvate corporate clients

who formed part of their deposit base.

The relationship resulted In a regular

exchange of information regarding

projects and the banks were able to

periodically assess the continued

finanCial viability of the clients'

business With the absence of a

LGU Financing' Present Sources, Avallabllzty and Terms

Chart F.

6000

4000

2000

0

~ ~.~ '" " ~ C' :t:<'l

banking relationship, the commercial

banks had little Incentive to lend to

LGUs;

o the dearth of information about the

creditworthiness of LGUs. An LGU

credit rating agency IS yet to be

established which could provide

Information on the credit-worthiness of

LGUs which IS one of the basIc

requirements of commercial lenders;

o the short-term orientation of most

commercial banks' lending policies.

Commercial bank loans are mostly

short-term (letters of credit, export

credits, working capital loans) which

do not suitthe long-term nature of LGU

Infrastructure projects,

poses unnecessarily high risks because

of the political succession Issue

However, one commercial bank

(previously a GFI) that has been very active

in lending to the LGUs IS the Philippine

National Bank.

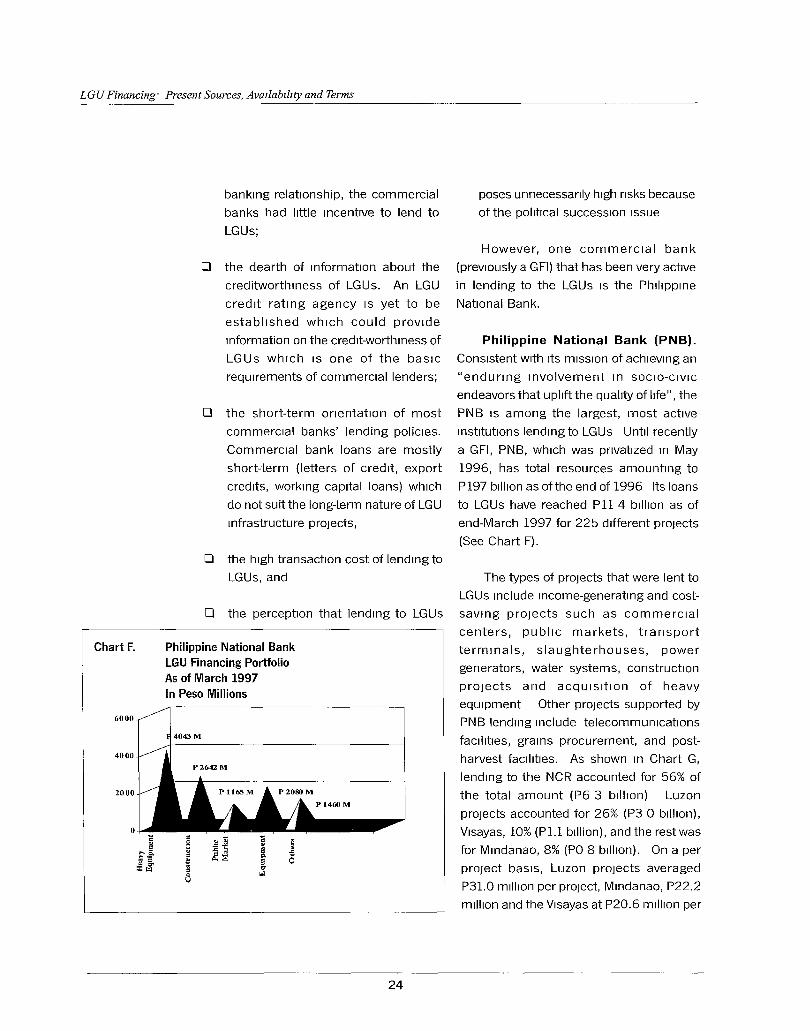

Philippine National Bank (PNB).

Consistent With ItS mission of achieving an

"endUring Involvement In SOCIO-CIVIC

endeavors that uplift the quality of life", the

PNB IS among the largest, most active

institutions lending to LGUs Until recently

a GFI, PNB, which was privatized In May

1996, has total resources amounting to

P197 billion as ofthe end of 1996 Its loans

to LGUs have reached Pll 4 billion as of

end-March 1997 for 225 different projects

(See Chart F).

o the high transaction cost of lending to

LGUs, and The types of projects that were lent to

LGUs Include Income-generating and cost

o the perception that lending to LGUs saving projects such as commercial

centers, public markets, transport Philippine National Bank LGU Financing Portfolio As of March 1997 In Peso Millions

~ ~ • ~ :E~ .

5 . .f~ ""

;S

= 0

".

'"

P 1460M

24

terminals, slaughterhouses, power

generators, water systems, construction

projects and acquIsition of heavy

eqUipment Other projects supported by

PNB lending Include telecommunications

facIlities, grains procurement, and post

harvest facilities. As shown In Chart G,

lending to the NCR accounted for 56% of

the total amount (P6 3 billion) Luzon

projects accounted for 26% (P3 0 billion),

Vlsayas, 10% (Pl.l billion), and the rest was

for Mindanao, 8% (PO 8 billion). On a per

project basIs, Luzon projects averaged

P3l.0 million per project, Mindanao, P22.2

million and the Vlsayas at P20.6 million per

Chart G.

LGU FmancIng' Present Sources, AVailability and Terms

project Majority of the loans lent to LGUs

were for heavy eqUipment, Infrastructure

and publiC markets Annex 7 'shows the

geographical distribution of PNB's LGU

lending.

term If Justified. The Interest rate IS pnme

rate-based subject to periodic Interest

resetting. Collateral requirements can

Include the assignment of applicable

regular Income of the LGU, IRA share and

the revenues generated by the project

Terms of Credit. Eligible loans for financed. Other collateral can Include the

PNB finanCing under ItS LGU finanCing chattel mortgage of eqUipmentflnanced by

program Include those which finance the the loan and real estate mortgage on

establishment, development or expansion patrimonial property of LGUs. The LGU

of income-generating projects. Other lending program requirements and

projects that qualify Include Irrigation, procedures of the PNB are reproduced In

construction of municipal halls, sports Annex 8

complex, medical diagnostic eqUipment,

road construction, hospitals and school Prospects for Commercial Bank

buildings. Lending to LGUs. Recently, commercial

banks' attitude toward LGU finanCing has

undergone a transformation. Indications

Philippine National Bank LGU Lending as of March 1997

Mindanao - 8%

The maximum loanable amount can

from commercial banks are that a shift In

attitude towards LGU lending IS In the offing.

Some commercial banks now recognize

that LGUs represent a potential market for

credit lending because ofthe large finanCing

requirements of LGUs associated With the

devolutIOn of baSIC services and

Infrastructure requirements Other reasons

for the attractiveness of LGUs as a growing

market for commercial lending are.

o the Increase In LGUs' share of the

national wealth;

be as much as 100% of the project 0 presence of a legal framework for LGU

requirements but Will not exceed the

aggregate of five times the sum of the 20%

portion of the annual regular Income and

the IRA share of the LGU The term of the

loan IS generally up to 7 years, but the

finanCing;

o flexibility and expanded borrOWing

powers of LGUs under the LGC,

Board of Directors may consider a longer 0 increasing finanCial sophistication of

25

LGU Fznancing Present Sources, AVailability and Terms

some LGUs (some provinces are regulations of the Bangko Sentral ng

exploring private foreign financial Plilplnas (BSP) and the Securities and

Instruments), and Exchange Commission (SEC), to "Issue

bonds, debentures, secuntles, collateral,

o the growing market opportunity In notes and other obligatIOns to finance self

financing LGU Infrastructure requlre- liqUidating, income-producing development

ments (some P20 billion are In the or livelihood projects pursuant to the

project pipeline of LGU BOT Projects). pnontles established In the approved local

Commercial lending to LGUs will also

get a boost from the establishment of the

LGU Guarantee Corporation, which will gua

rantee commercial loans to LGUs. In the

past, the lack of a guarantee faCility was a

major factor that inhibited commercial

lending to LGUs as commercial banks were

concerned with the certainty of repayment.

As the guarantee faCIlity will prOVide the

repayment "comfort" to commercial banks,

It IS expected that private commercial

lending to LGUs Will finally develop.

Municipal Bond Flotations

Municipal bond flotation IS another

pnvate source of debt finanCing that IS gene

rating a lot of Interestfrom LGUs. MUniCipal

bonds represent an additional source of

finanCing for LGUs, which hitherto had not

been tapped. To date, SIX LGU bond flota

tions have been successfully floated, the

first one In Infrastructure development

(Cebu equity bonds), and the rest In

hOUSing

Legal Framework for Bond

Flotations. The 1991 Local Government

Code allows, subject to the rules and

9 Local Government Code of 1991 (Republic Act No 7160), SectIOn 299

26

development plan or the public Investment

program"9. ProVinces, cities and

mUniCipalities are authOrized under the

LGC to Issue mUniCipal bonds under two

conditions: (I) the obligation should finance

self-liqUidating, Income prodUCing

development or livelihood projects; and (II)

the projects to be financed must be In

accordance With pnontles established In the

approved local development plan or the

public Investment program.

Thus, at the moment, LGUs cannot

utilize a bond flotation for recurrent

obligations or general obligations of LGUs

and other non-revenue earning expen

ditures such as the construction of a City

or muniCipal hall or payment of staff

salaries. In addition, the LGU concerned

IS obligated to formally adopt a public

Investment program for the province, City

or muniCipality, and the project to be

financed through a bond flotation must be

part of the publiC Investment program.

Bond flotations require endorsement;

approval of the BSP.

National ~overnment Guarantee.

In order to enhance the market prospects

of bond flotations, some LGUs, such as the

LGU Fznanczng Present Sources, AVa/labilzty and Terms

province of Palawan, have requested a

national government guarantee for their

planned foreign bond flotations, However,

the national government IS not empowered

to grant a guarantee to LGU foreign bond

Issues by virtue of R.A. 4860 (Foreign

Borrowings Act) which limits the Issuance

of sovereign guarantees to loans of

government-owned or government

controlled corporations and government

financial institutions With regard to local

bond flotations, there have been Instances

where a national government agency has

guaranteed the obligations of an LGU. Of

the fl ve LGU housing bond Issues floated

In the country, four have carned a partial

guarantee from the Home Insurance

Guarantee Corporation (HIGC), a national

successfully float the first few non-hOUSing

mUnicipal bond flotations.

Bond Flotations Issued. The

Province of Cebu pioneered LGU bond

flotations In the country when they floated

the first bond Issue in July 1990 (Cebu

Equity Bond Unit). The P300 million Issue

had a term of three years, tax free Interest

Income at 16 percent and called for

principal repayments In five (5) equal semi

annual installments In the form of class "A"

shares of Cebu Property Ventures and

Development Corporation (CPVDC), a JOint

venture of Cebu Province and Ayala Land,

Inc (ALI) Cebu had contributed land and

ALI contributed cash for their shares In

CPVDC. With the tax-free feature, the

government agency. The hOUSing bond Investors effectively earned 20% on their

issue floated In Sto Domingo, Nueva ECIJa,

however, did not carry an H IGC guarantee,

but nevertheless was fully subscribed.

For non-hOUSing bond Issues, It IS

unlikely that a National Guarantee would

be granted primarily because such

guarantees run counter to the principles

laid down In the Local Government Code,

I.e. with the Increase In the share of LGUs

In the national wealth, and allOWing LGUs

the freedom to obtain finanCing from

various sources, the LGUs should assume

responsibility for finanCing baSIC services

and Infrastructure requirements In

addition, the Government's fiscal poliCY IS

to limit extension of guarantees In order to

protect ItS fiscal position. Because of the

absence of a National Government

guarantee, one can surmise that only the

most creditworthy LGUs would be able to

27

Investment plus the capital appreciation

prospects of the CPVDC shares.

Since the Cebu bond flotation, there

have been five more Issues (all In the

hOUSing sector):

o Victorias Pabahay Bonds - Negros

OCCidental (P8.0 million)

o Legazpl Suerte Bonds - Albay (P26 0

million)

o Clavena HOUSing Bonds - Mlsamls

Oriental (P20.0 million)

o Sto. Domingo HOUSing Bonds - Nueva

Ecija (PlO 0 million)

o Puerto Pnncesa HOUSing Bond -

Palawan (P20 0 million)

LGU Financmg Present Sources, Avazlabilzty and Terms

These bonds were issued on a taxable

basIs with Interest rates ranging from 14-

16%. The term of the Issues ranged from

2-3 years. All Issues carned the guarantee

of HIGC except the Sto. Domingo housing

bonds. A description of the bond Issuance

process IS presented by the Multinational

Investment Bancorporatlon, one of the

major underwriters in the mUnicipal bond

market (Annex 9). Since the bonds floated

were of relatively small size and short in

maturity, It IS clear that additional Incentives

are needed to promote development of a

broader mUnicipal bond market. In this

regard, the Government IS taking concrete

steps through ItS policy initiative, New VIsion

and PoliCY Framework for LGU Financing,

to initiate poliCies that Will develop the

mUnicipal bond market.

Assessment

that It could be a cheaper source of

financing, for example, when bank lending

Interest rates are very high.

One Issue that has been raised by

some quarters IS the taxation of mUnicipal

bonds At the moment, Interest Income

from bond flotations IS subject to a 20%

withholding tax. Proponents of the tax

exemption of municipal bonds cite the

experience In the United States, where most

municipal bonds are tax-exempt The

Government IS presently looking Into the

revenue Implications to the national

treasury of the tax exemption. Another Issue

IS the short-term nature of the mUnicipal

bonds so far floated (2-3 years). Better

terms have to be sought for the bonds to

finance long-gestating Infrastructure

projects However, there eXists the POSSI

bility that credit enhancements such as the

proposed LGU Guarantee Corporation can

Prospects for Growth. As shown be used to lengthen the maturity of bonds

above, municipal bonds that have been

Issued so far have been limited to housing

projects. ThiS was partly because there

was a government agency that guaranteed

part or all of the repayment of the bond

Issues The other reason IS that many

Investors have a greater propensity to Invest

In time-tested treasury bills or in housing

and property development However, the

situation IS changing. From a social

ViewpOint, many LGUs are beginning to see

the advantages of floating project revenue

bonds (the project will likely get community

support If ItS members partiCipate In the

finanCing of the project), the addltlonality

of an untapped source of financing for

Infrastructure projects, and the possibility

28

through the guarantee mechanism Finally,

the lack of a secondary market for bond

flotations limits the liqUidity of the bonds

In many cases, the bondholders have to

hold on to the bonds until maturity because

of the absence of a secondary market.

Despite these factors, bond flotation offers

great advantages for LGUs ASide from the

community support mentioned earlier,

mUnicipal bonds offer a distinctly separate

and additional source of financing for LGU

Infrastructure projects, and could be a

cheaper source of financing depending on

the terms of the bond flotation

Sector coverage. Municipal bond

Issues offer good prospects for projects In

LGU Financing' Present Sources, AVaIlability and Terms

sectors other than housing Based on bond system In the United States, where

recent mandates received by private sector most municipal projects are financed

municipal bond underwriters, different through mUnicipal bonds.

Box B

sectors are now being explored for

municipal bond offerings, Including

airports, water supply, and food terminals.

For example, a P40 million bond flotation

IS now being packaged to finance general

Infrastructure requirements of the province

of Aklan It IS expected that once poliCY

issues are resolved, (tax exemption, credit

rating agency, etc ) municipal bond

flotations Will go the way of the mUnicipal

Characteristics and Advantages of BOT Schemes

Characteristics:

A private company or consortium is given the right to bUlld and operate a facility previously provided for by the government; The private company is responsIble for financing, designing, constructing, operatlllg and mallltaining the project; Lenders look to the project's assets and revenue stream for repayment; Concession period is agreed (typically 20-25 yrs.) afterwhich the facilIty IS transferred to the LGD.

Advantages:

BOT offers an alternative source of financing; A transparent legal framework already exists for BOT financing; LGUs benefit from a project wIth typically no or very lIttle imtiallllvestment; BOT schemes offer proper allocation of risks; BOT projects usually result in better and reliable service and consistent supply; Long conceSSIOn period and contractual agreements assure project sustainability; Technology and skills transfer usually result from BOT projects; BOT Projects may stimulate local capital market development.

29

Other Private Sources of LGU Financing: BOT Schemes and Provincial Equity Funds

Build-Operate-Transfer (BOT)

Schemes

Background. BOT or "Bulld-Operate

Transfer" IS a project finanCing scheme that

uses private Investment to undertake

mfrastructure projects histOrically fmanced

and Implemented by the public sector Box

B Illustrates some characteristics and

advantages of a BOT scheme.

BOT schemes are generally

charactenzed by the participation of the

pnvate sector as the major sponsor of the

project The pnvate sector proponent IS

given the nghts and pnvlleges by the publiC

sector (the LGU) to build and operate the

faCility, transferring the faCility to the LGU

after the concession penod. One very

Important characteristic of BOT schemes

IS that they allow proper allocation of nsks.

The pnvate sector proponent assumes

certam nsks, which are traditionally borne

by the public sector, e g the finanCing risk,

the deSign, construction, and operating and

maintenance nsks

In addition, BOT schemes, by virtue of

requiring little or no upfront Investments,

prOVide local governments With a Viable

vehicle to overcome their budgetary

resource constramts and accelerate the

LGU Financing Present Sources, AVailability and Terms

Implementation of Infrastructure projects.

With BOTs, local govemment Units need not

depend on financial assistance from the

National Government. If a local

government Unit can develop and package

a financially viable project, It only needs to

solicit Investor Interest in the project and

undergo the processing procedures

prescribed under the BOT Law and the

LGC

Legal Framework of the LGU BOT

Scheme. The Local Government Code of

1991 allows the LGUs to tap both

Government and private sources of capital

to finance basIc serVices, local

Infrastructure and other development

projects Reallzlngthatthe cost offlnanclng

these services and Infrastructure projects

IS huge and consldenngthatthe Philippines