Embed Size (px)

Citation preview

2013 CFA Level II – Alternative Investments

Presented by: Arif Irfanullah

www.arifirfanullah.com

Private Equity Valuation

Contents

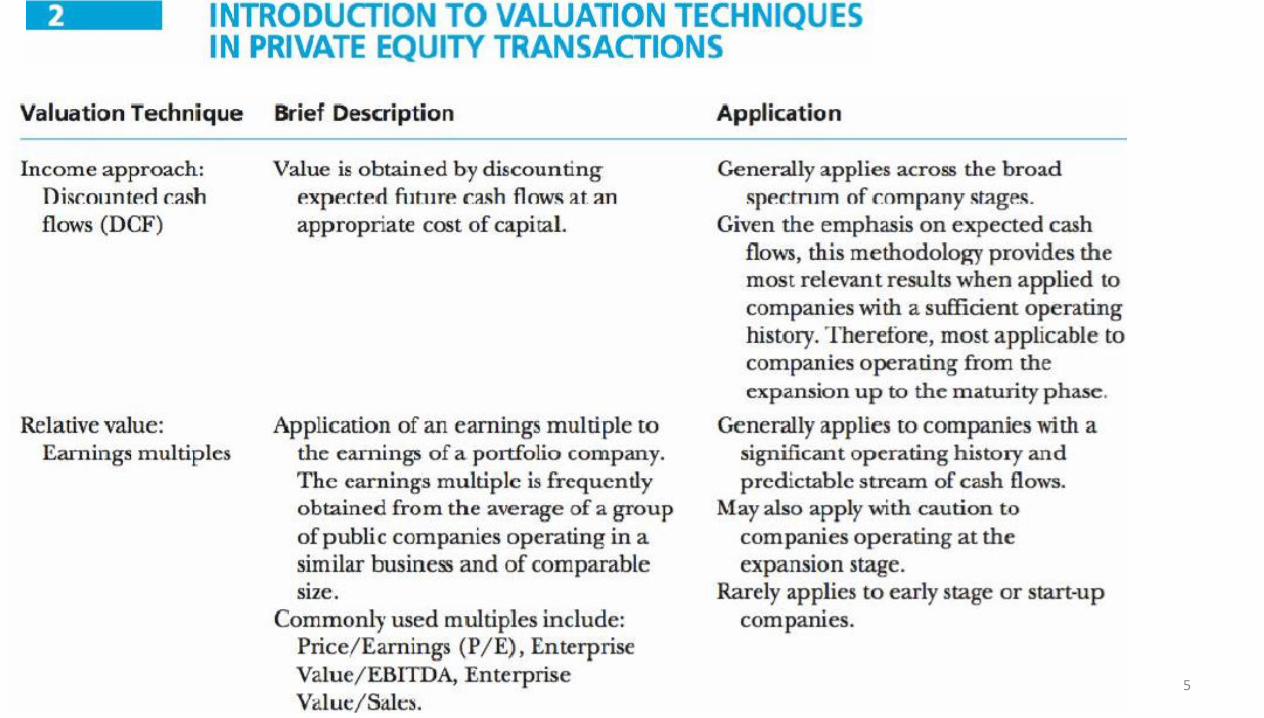

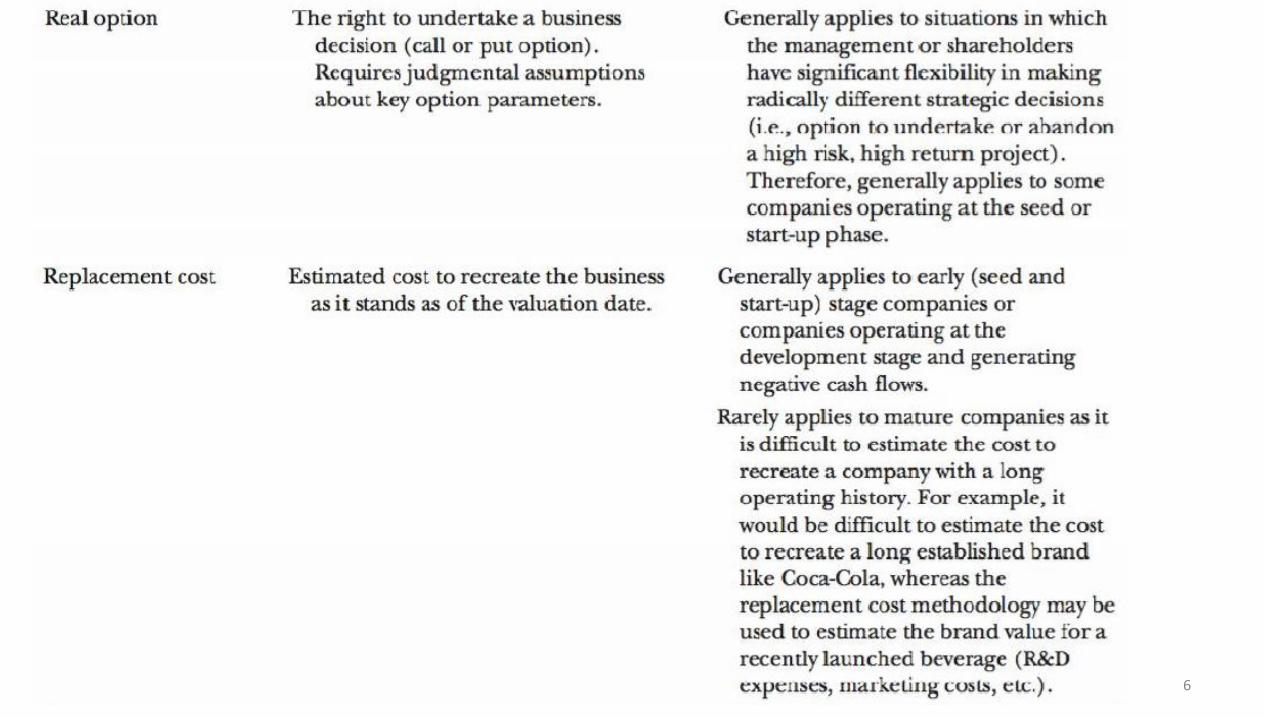

1. Introduction

2. Valuation Techniques

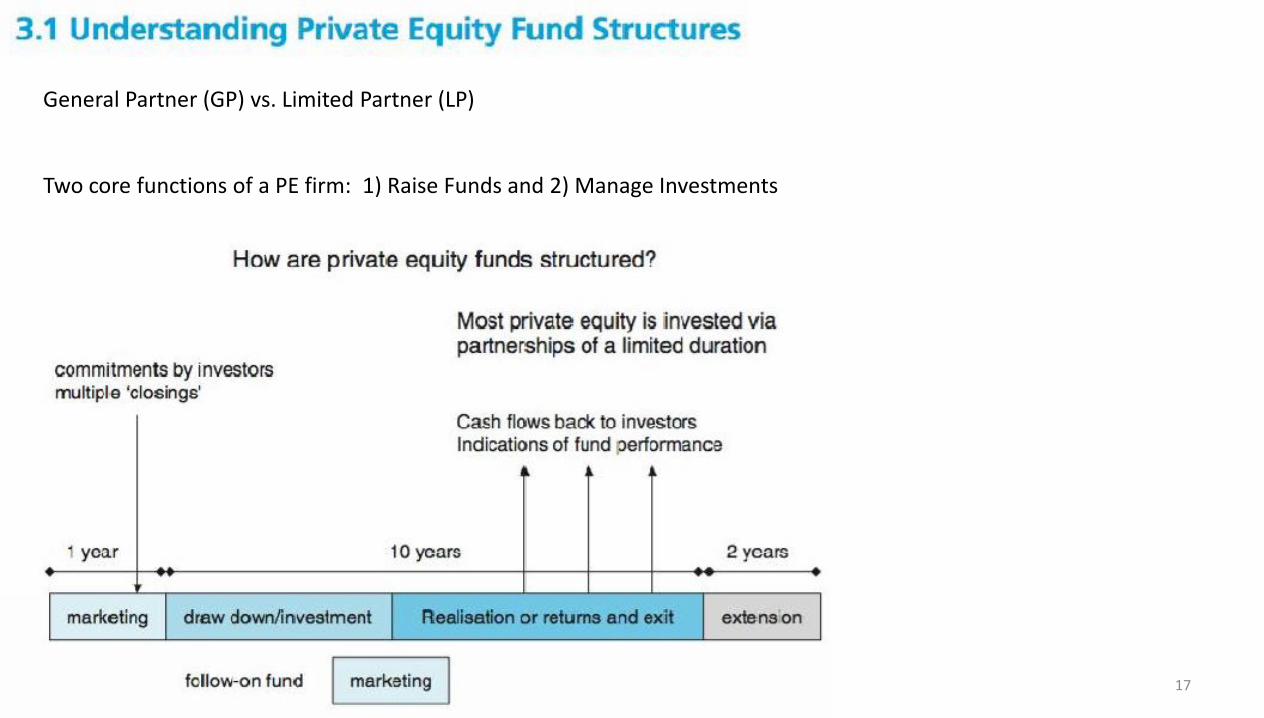

3. Private Equity Fund Structures and Valuation

4. Evaluating a Private Equity Fund

5. Case Study

www.arifirfanullah.com 2

1. Introduction

www.arifirfanullah.com 3

www.arifirfanullah.com 4

www.arifirfanullah.com 5

www.arifirfanullah.com 6

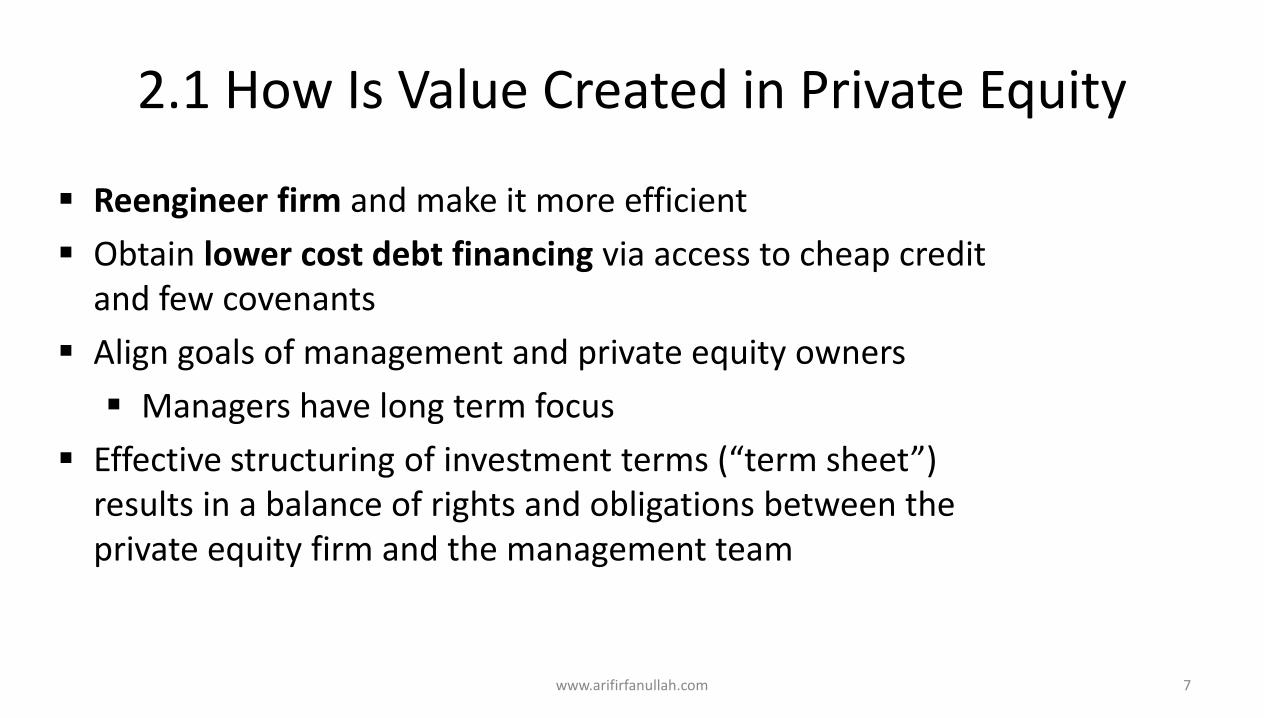

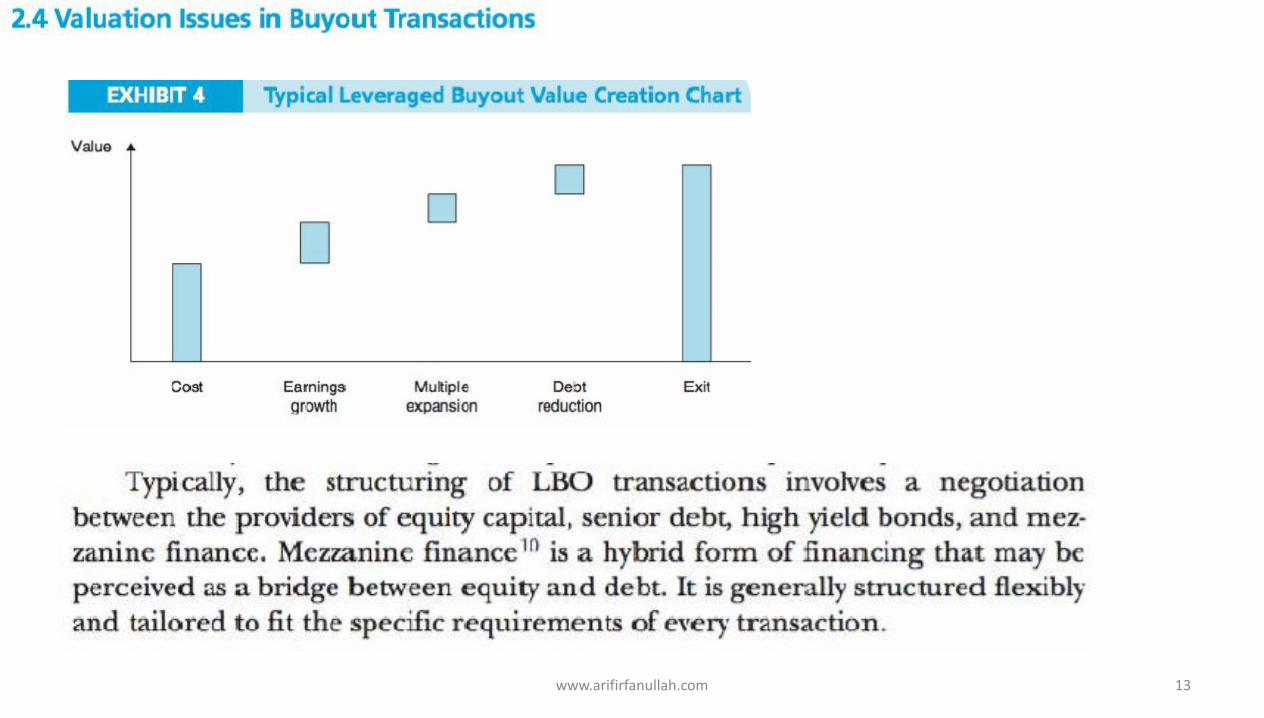

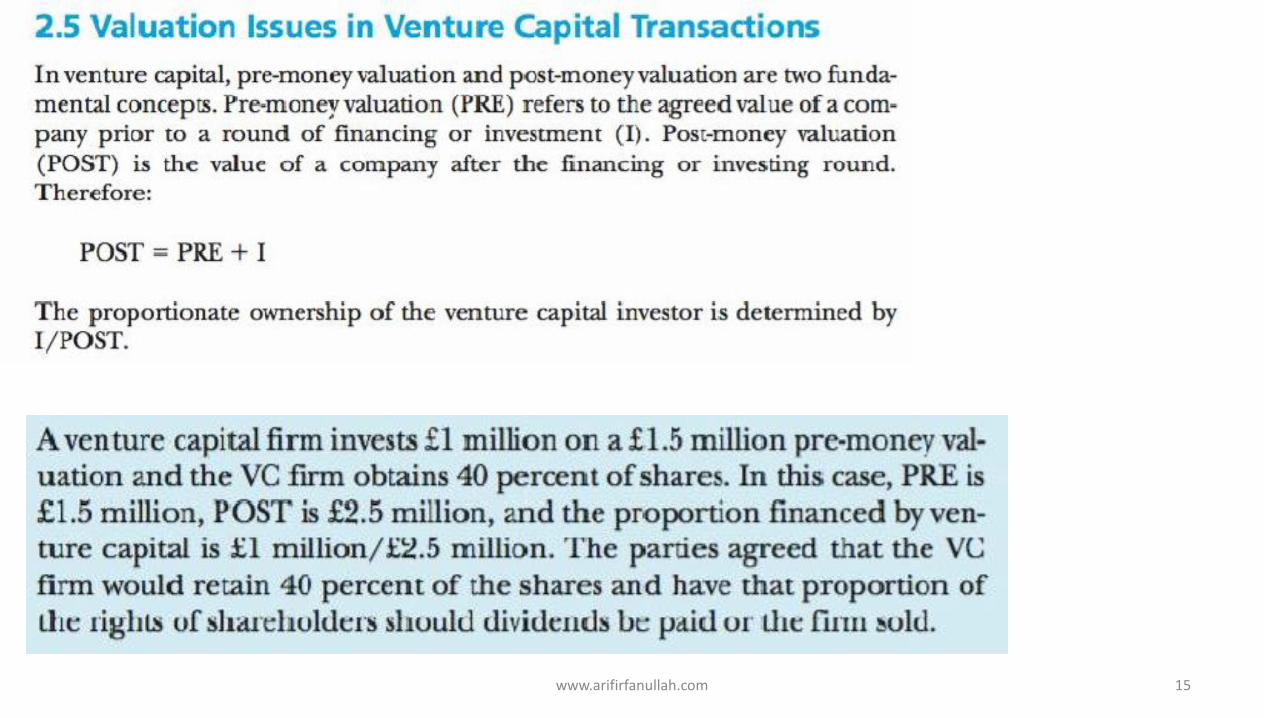

2.1 How Is Value Created in Private Equity

www.arifirfanullah.com 7

Reengineer firm and make it more efficient

Obtain lower cost debt financing via access to cheap credit and few covenants

Align goals of management and private equity owners

Managers have long term focus

Effective structuring of investment terms (“term sheet”) results in a balance of rights and obligations between the private equity firm and the management team

www.arifirfanullah.com 8

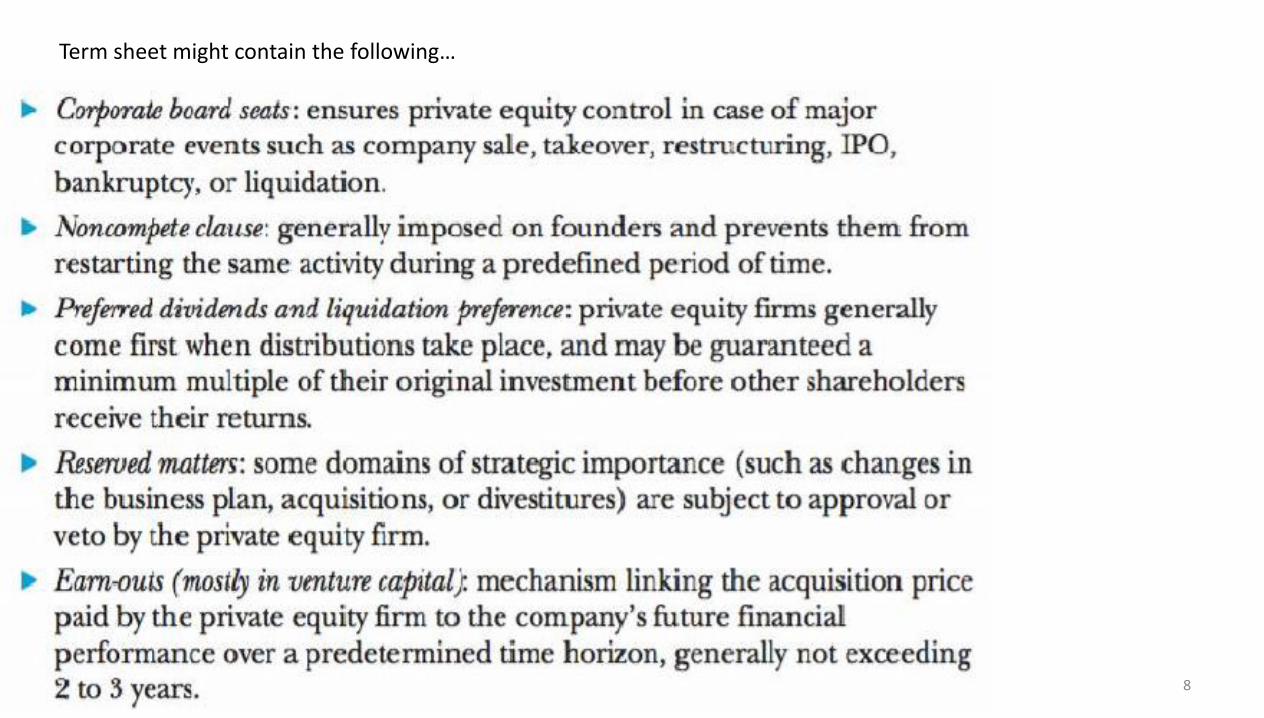

Term sheet might contain the following…

www.arifirfanullah.com 9

EBITDA multiples are frequently used

www.arifirfanullah.com 10

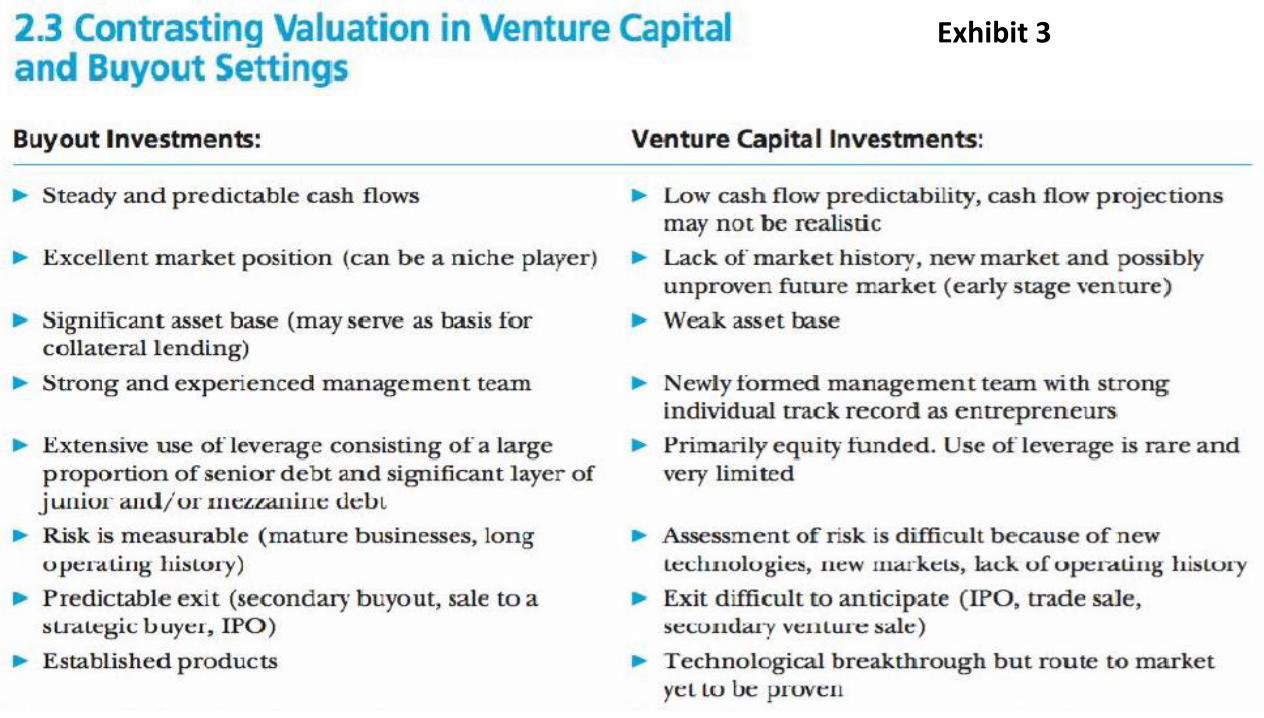

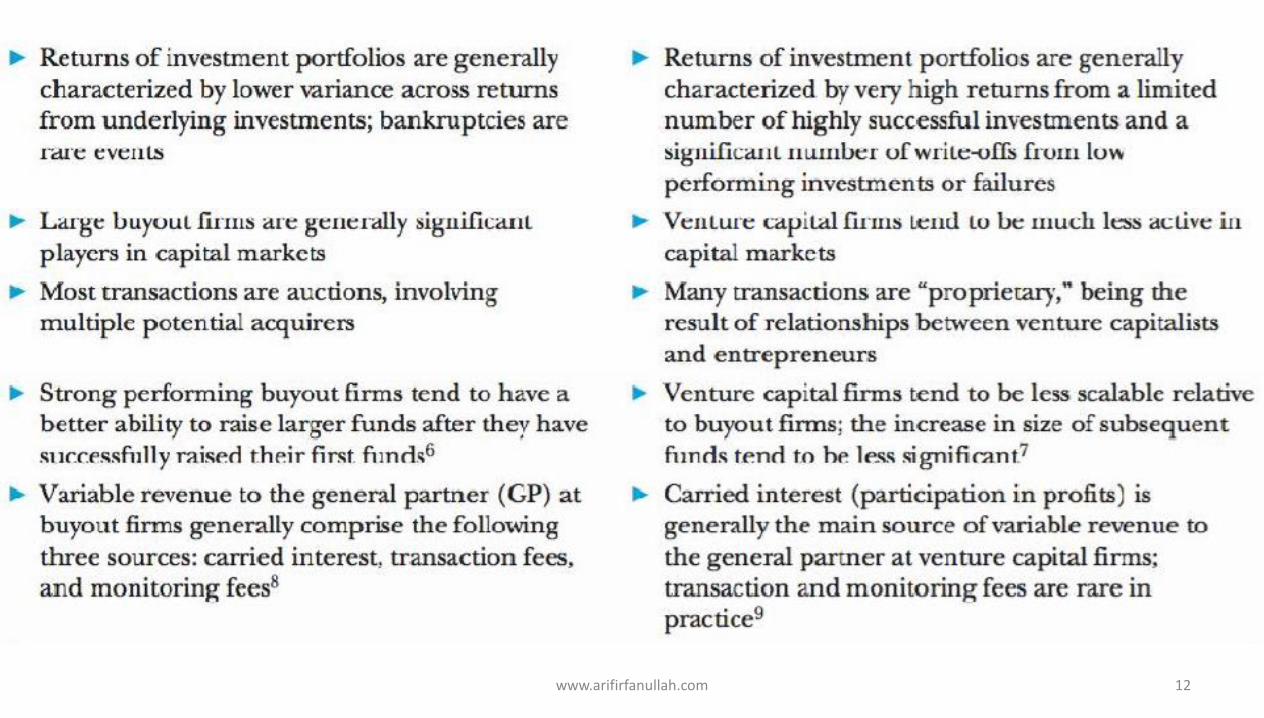

Exhibit 3

www.arifirfanullah.com 11

www.arifirfanullah.com 12

www.arifirfanullah.com 13

www.arifirfanullah.com 14

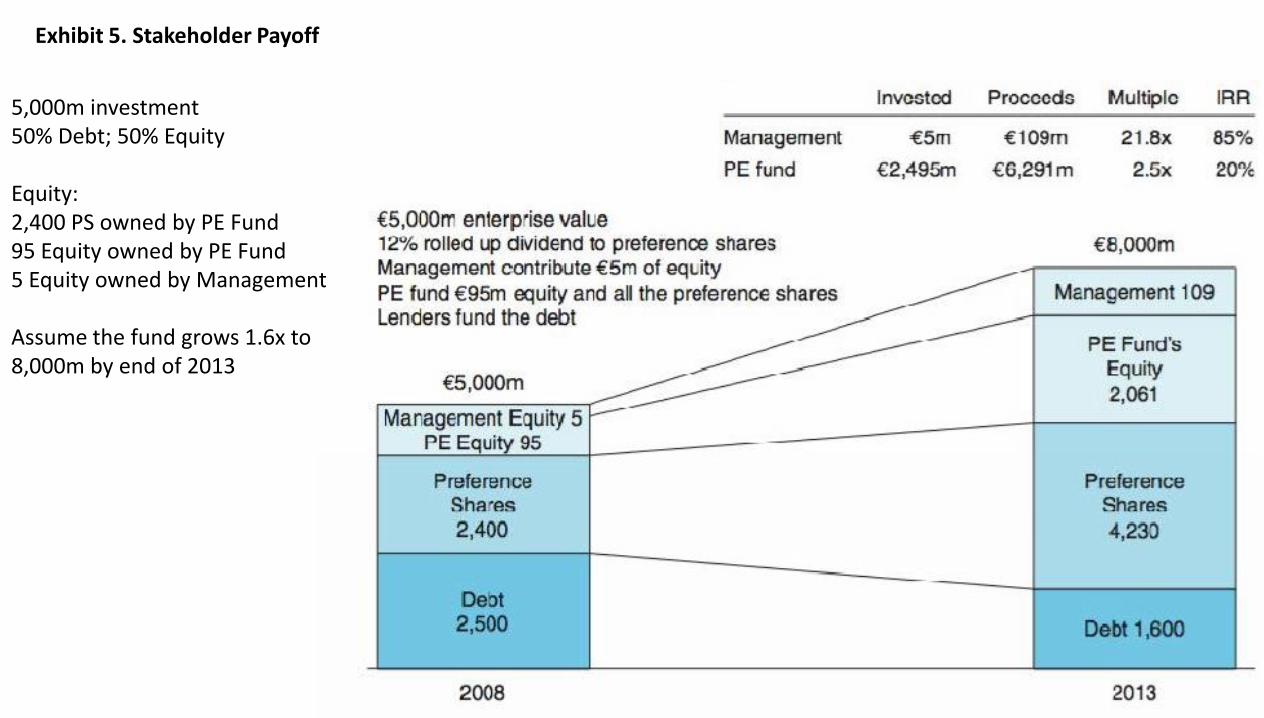

Exhibit 5. Stakeholder Payoff

5,000m investment 50% Debt; 50% Equity Equity: 2,400 PS owned by PE Fund 95 Equity owned by PE Fund 5 Equity owned by Management Assume the fund grows 1.6x to 8,000m by end of 2013

www.arifirfanullah.com 15

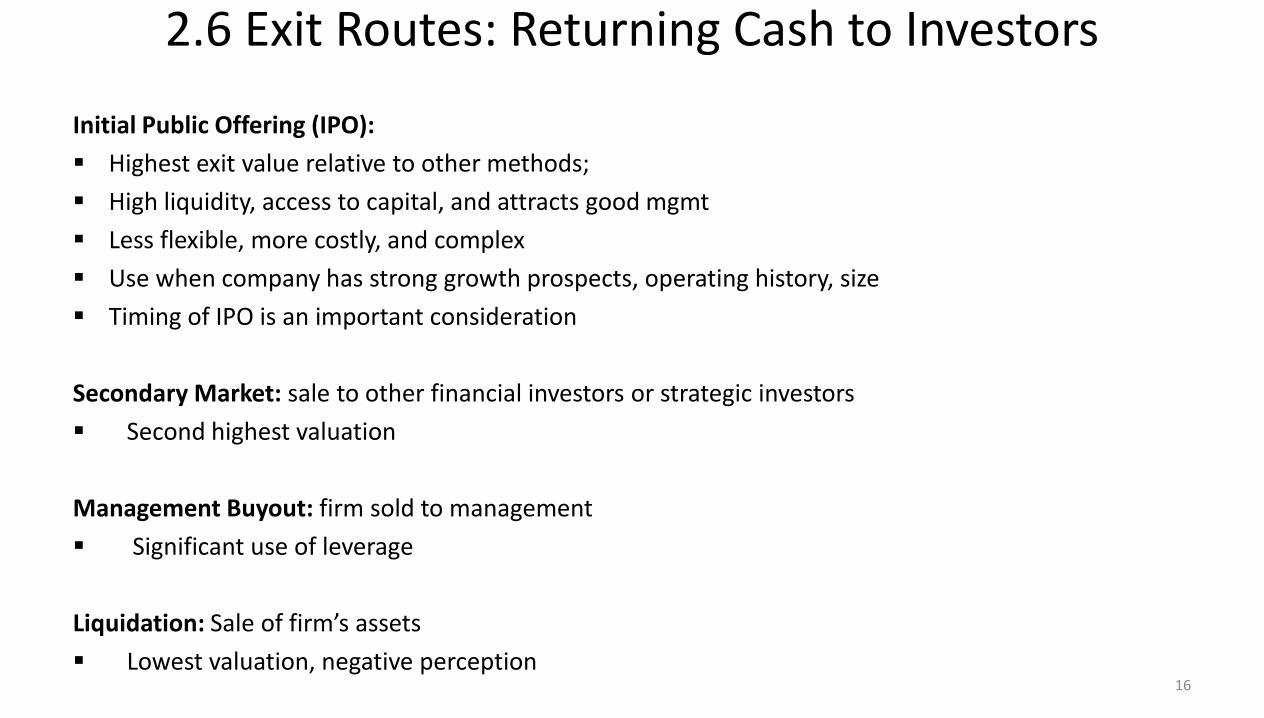

2.6 Exit Routes: Returning Cash to Investors

Initial Public Offering (IPO):

Highest exit value relative to other methods;

High liquidity, access to capital, and attracts good mgmt

Less flexible, more costly, and complex

Use when company has strong growth prospects, operating history, size

Timing of IPO is an important consideration

Secondary Market: sale to other financial investors or strategic investors

Second highest valuation

Management Buyout: firm sold to management

Significant use of leverage

Liquidation: Sale of firm’s assets

Lowest valuation, negative perception

16

www.arifirfanullah.com 17

General Partner (GP) vs. Limited Partner (LP) Two core functions of a PE firm: 1) Raise Funds and 2) Manage Investments

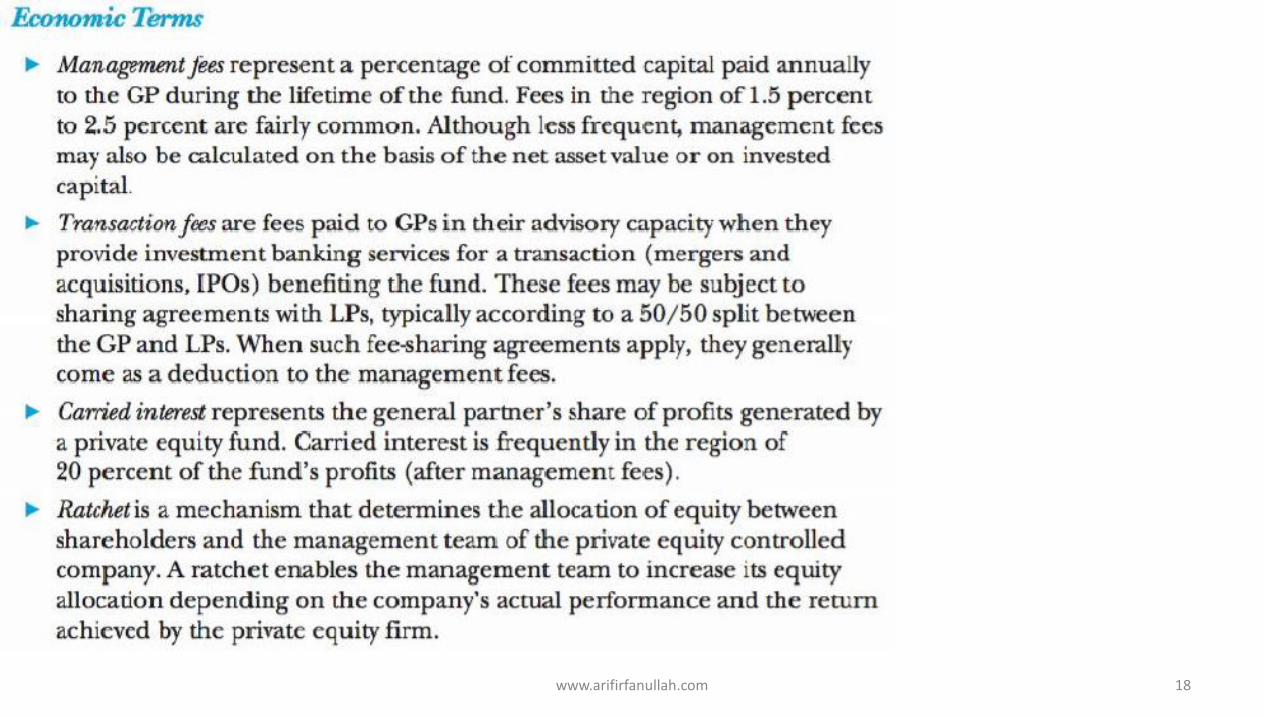

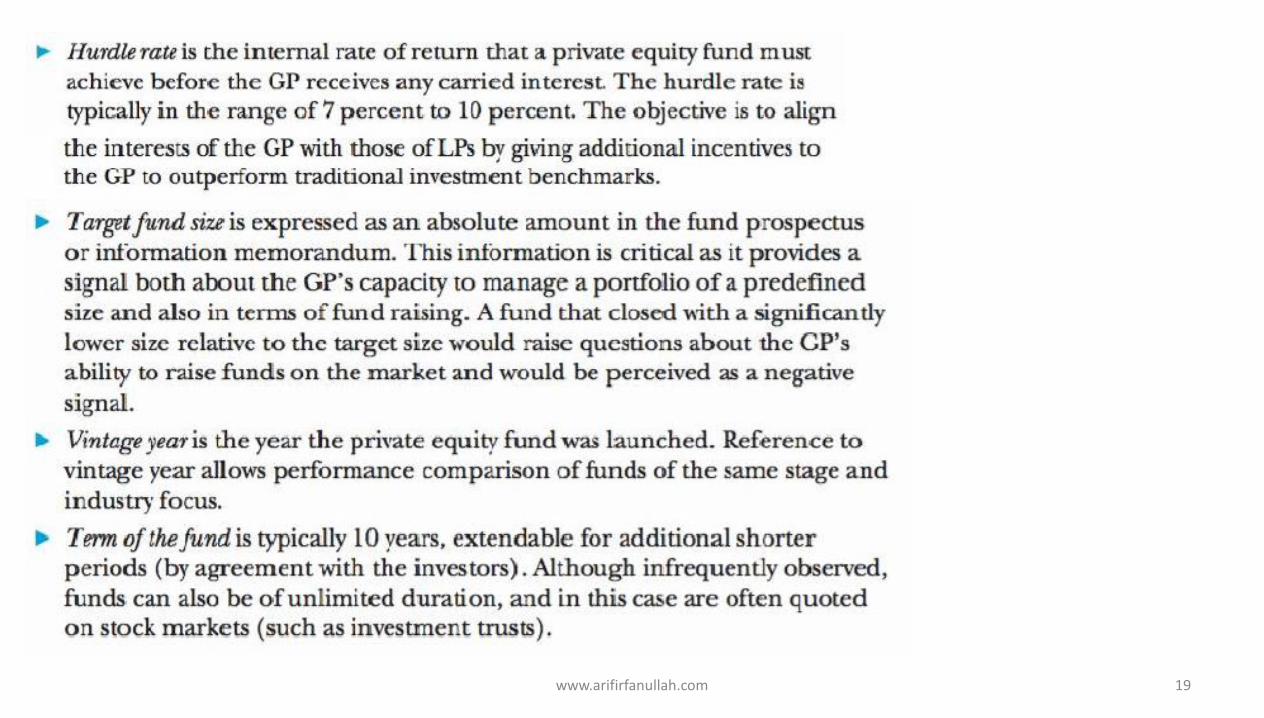

www.arifirfanullah.com 18

www.arifirfanullah.com 19

www.arifirfanullah.com 20

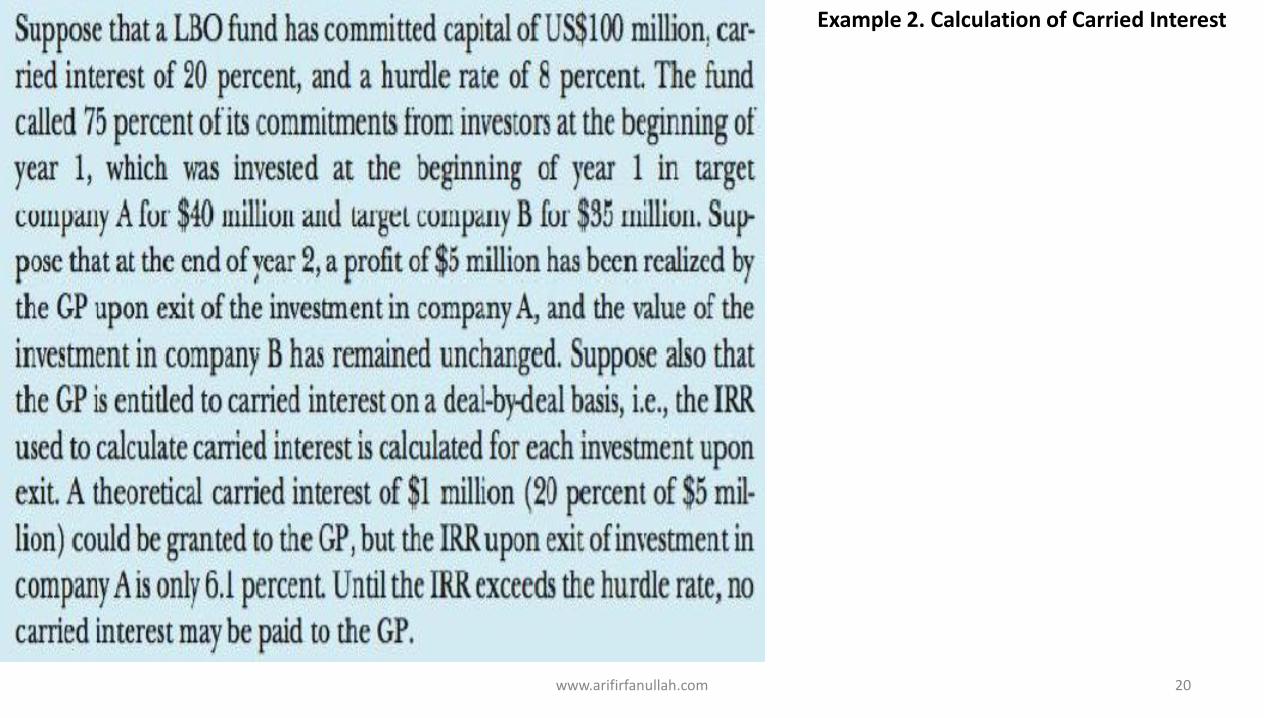

Example 2. Calculation of Carried Interest

www.arifirfanullah.com 21

www.arifirfanullah.com 22

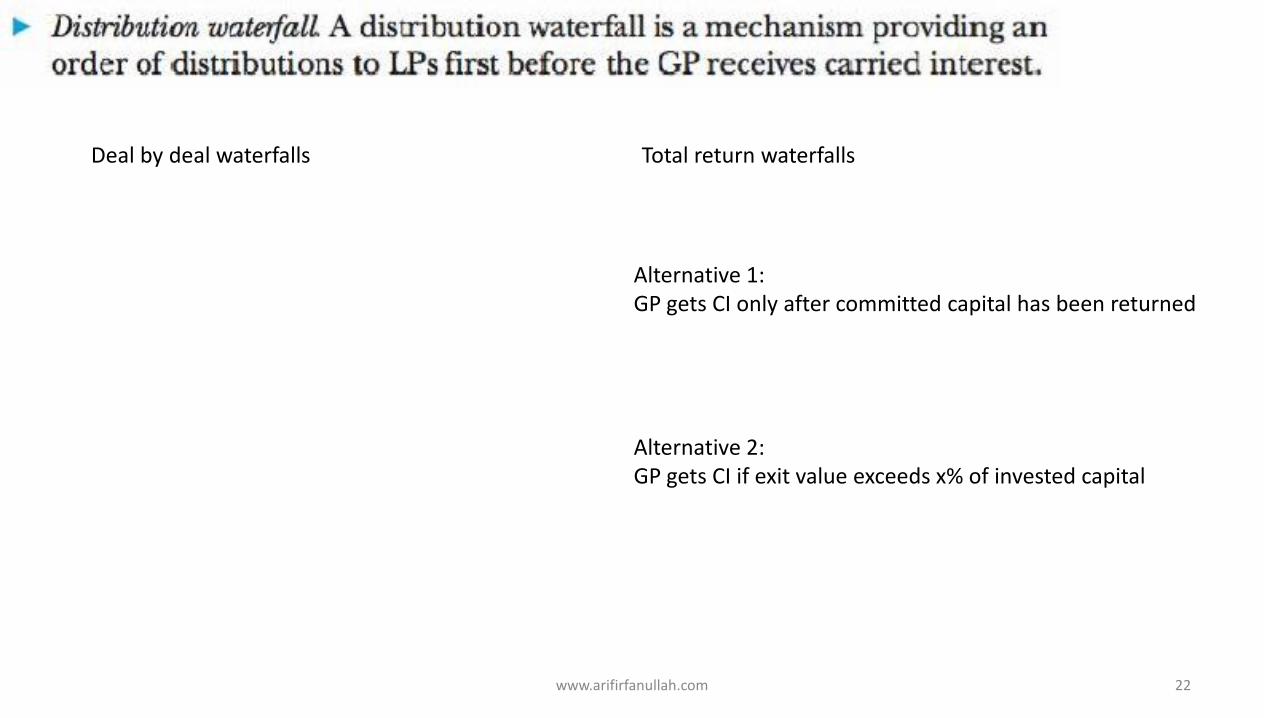

Deal by deal waterfalls Total return waterfalls

Alternative 1: GP gets CI only after committed capital has been returned Alternative 2: GP gets CI if exit value exceeds x% of invested capital

www.arifirfanullah.com 23

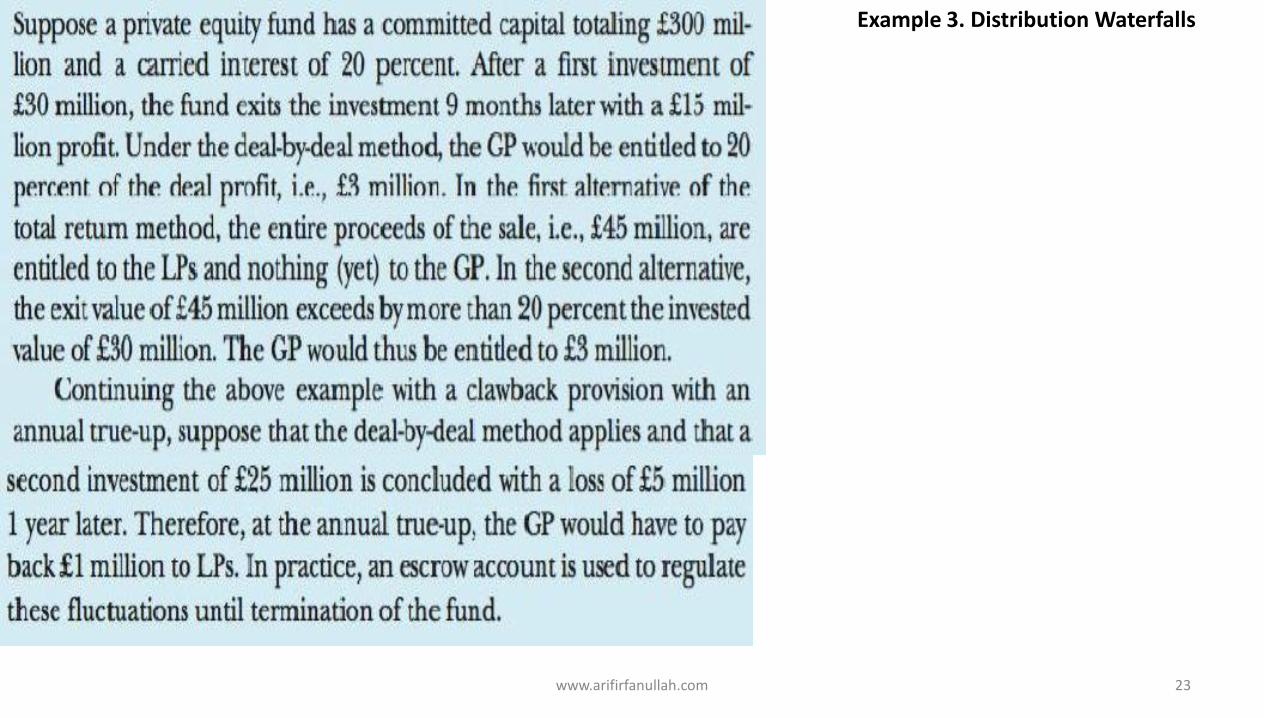

Example 3. Distribution Waterfalls

www.arifirfanullah.com 24

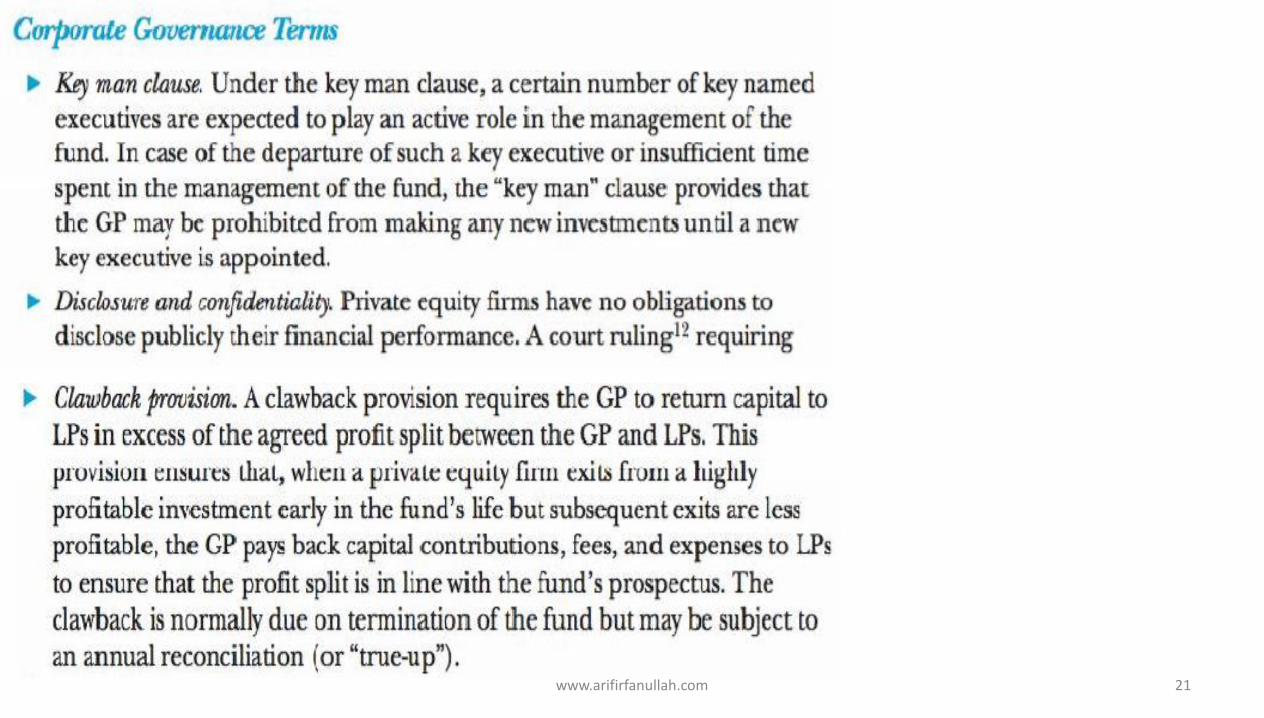

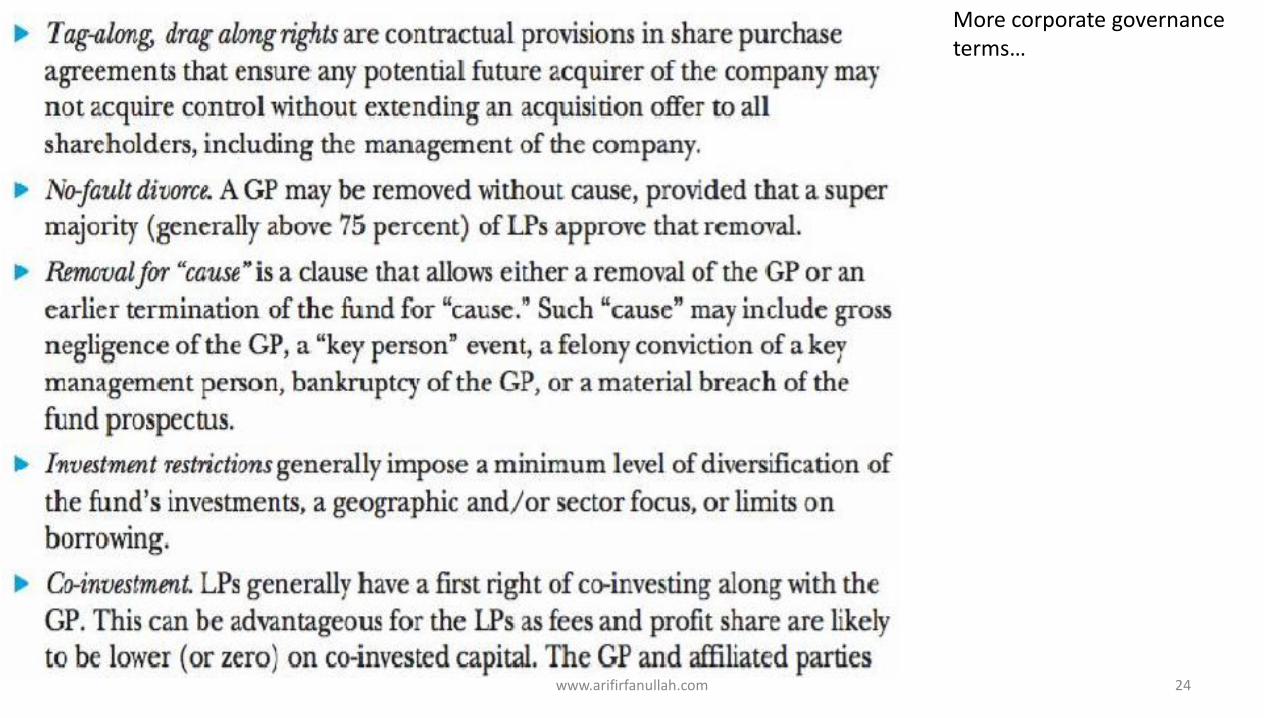

More corporate governance terms…

www.arifirfanullah.com 25

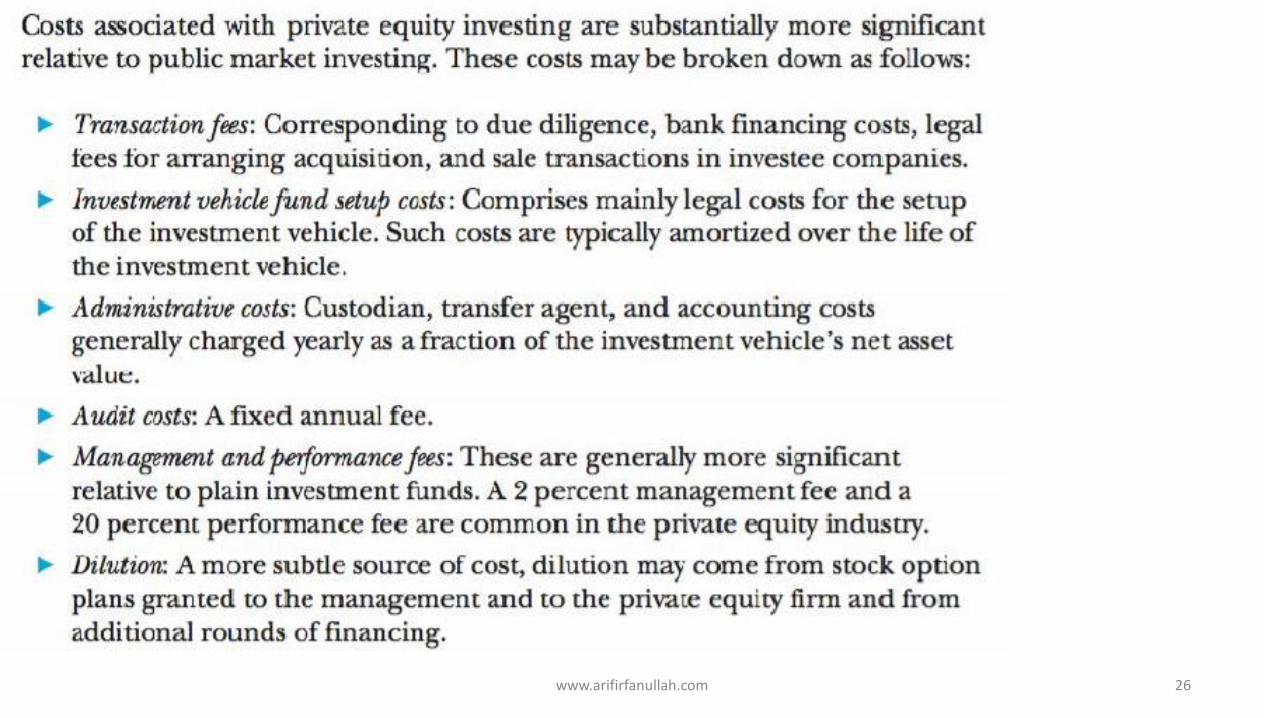

www.arifirfanullah.com 26

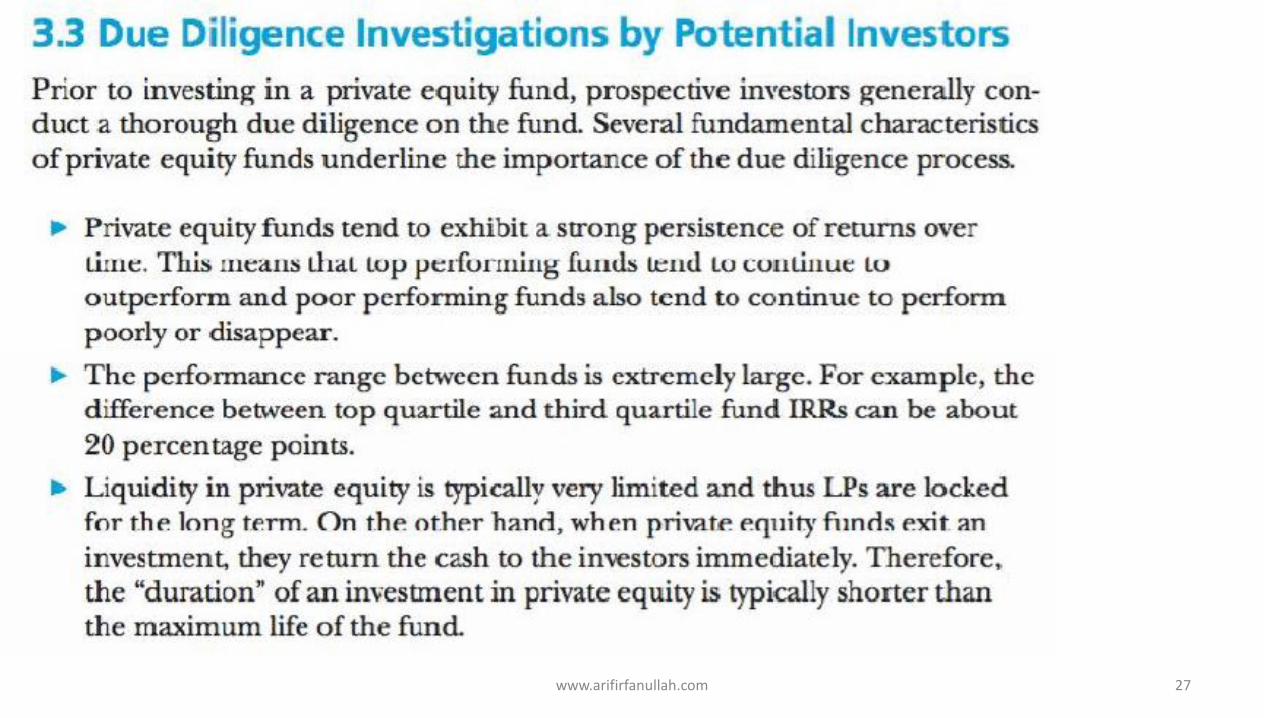

www.arifirfanullah.com 27

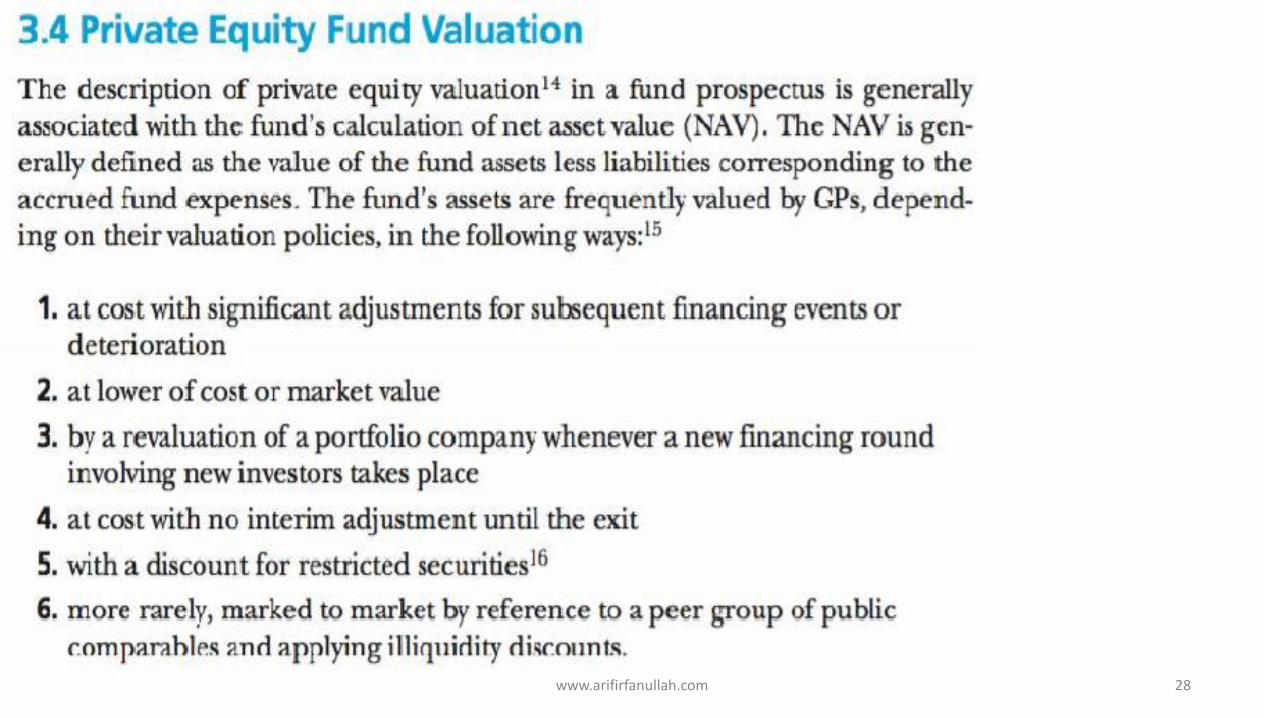

www.arifirfanullah.com 28

www.arifirfanullah.com 29

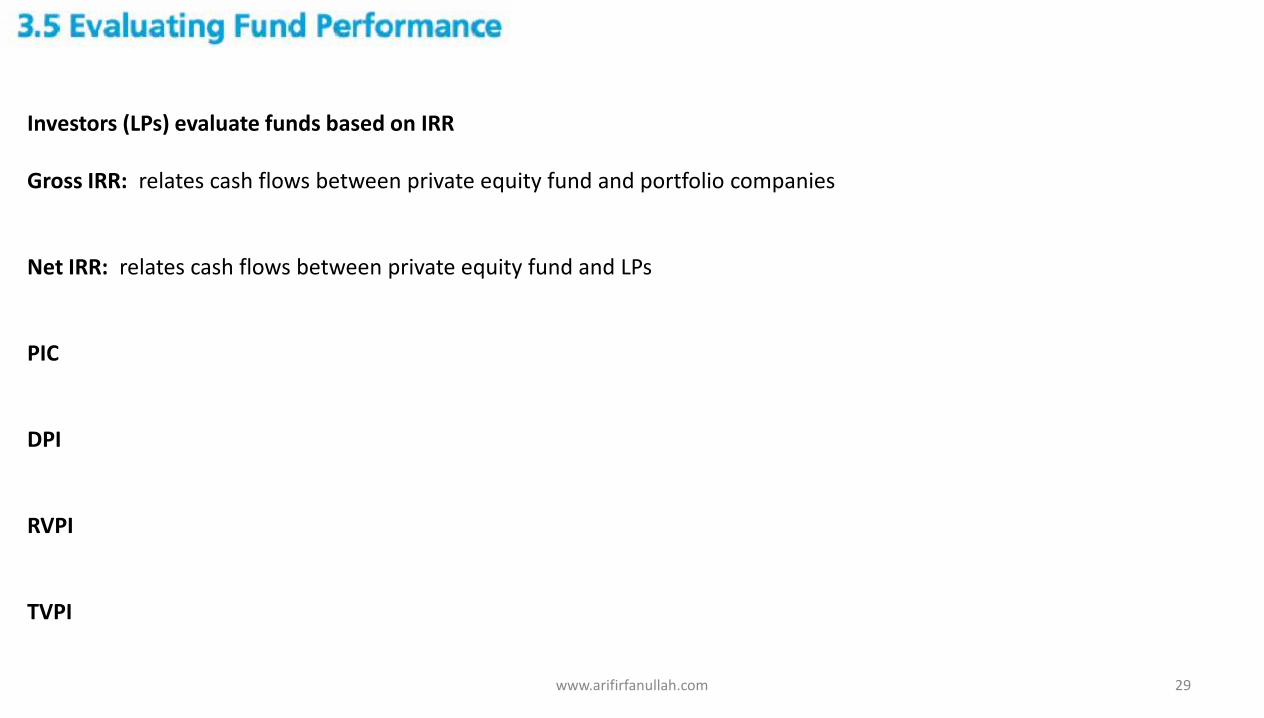

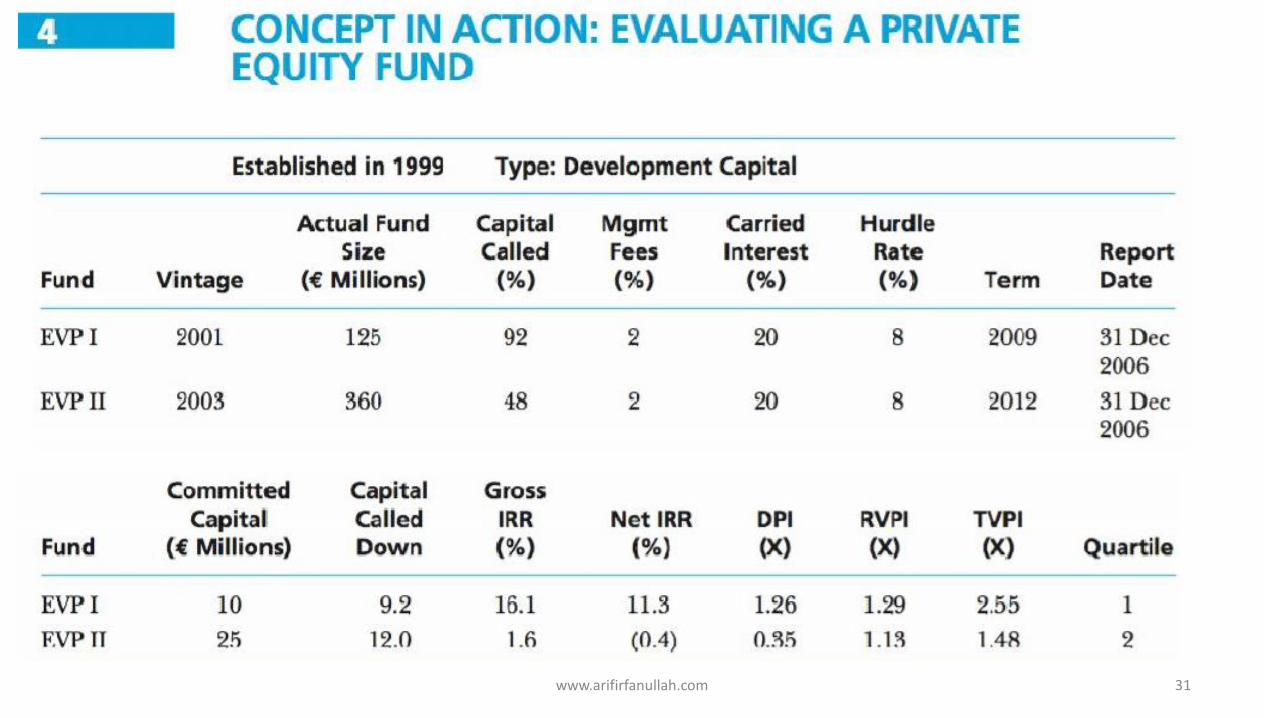

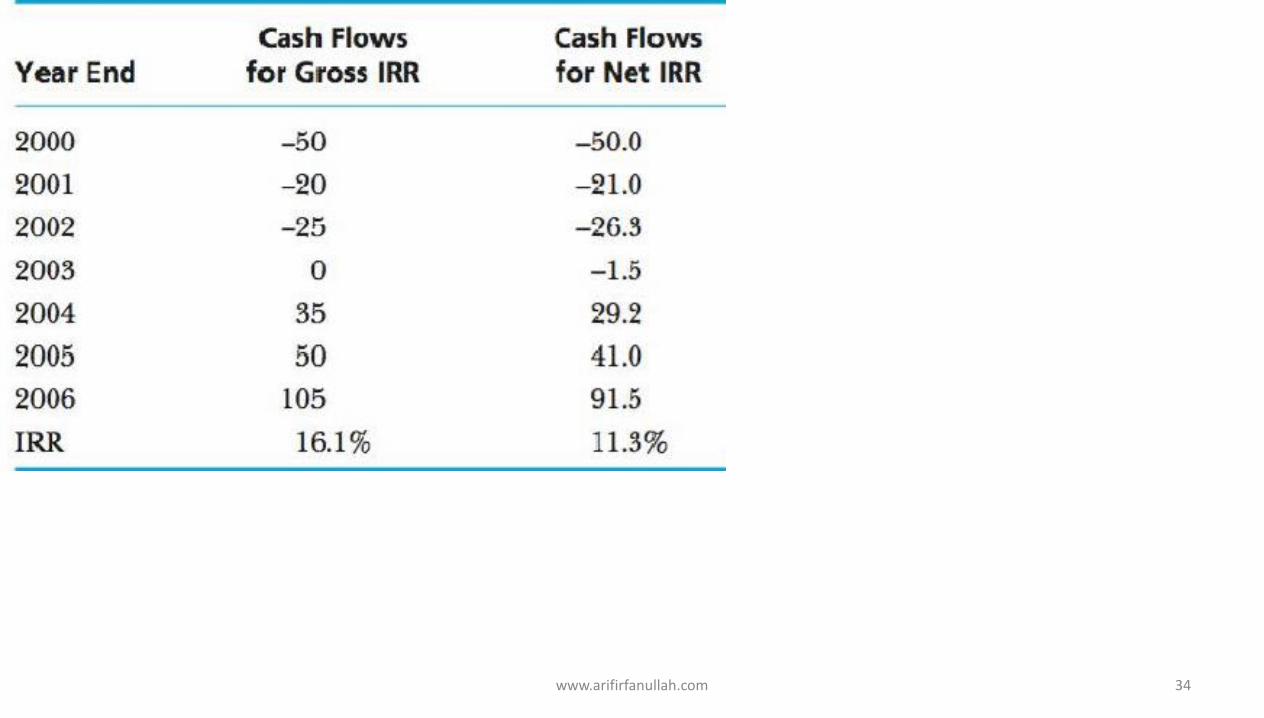

Investors (LPs) evaluate funds based on IRR Gross IRR: relates cash flows between private equity fund and portfolio companies Net IRR: relates cash flows between private equity fund and LPs PIC DPI RVPI TVPI

www.arifirfanullah.com 30

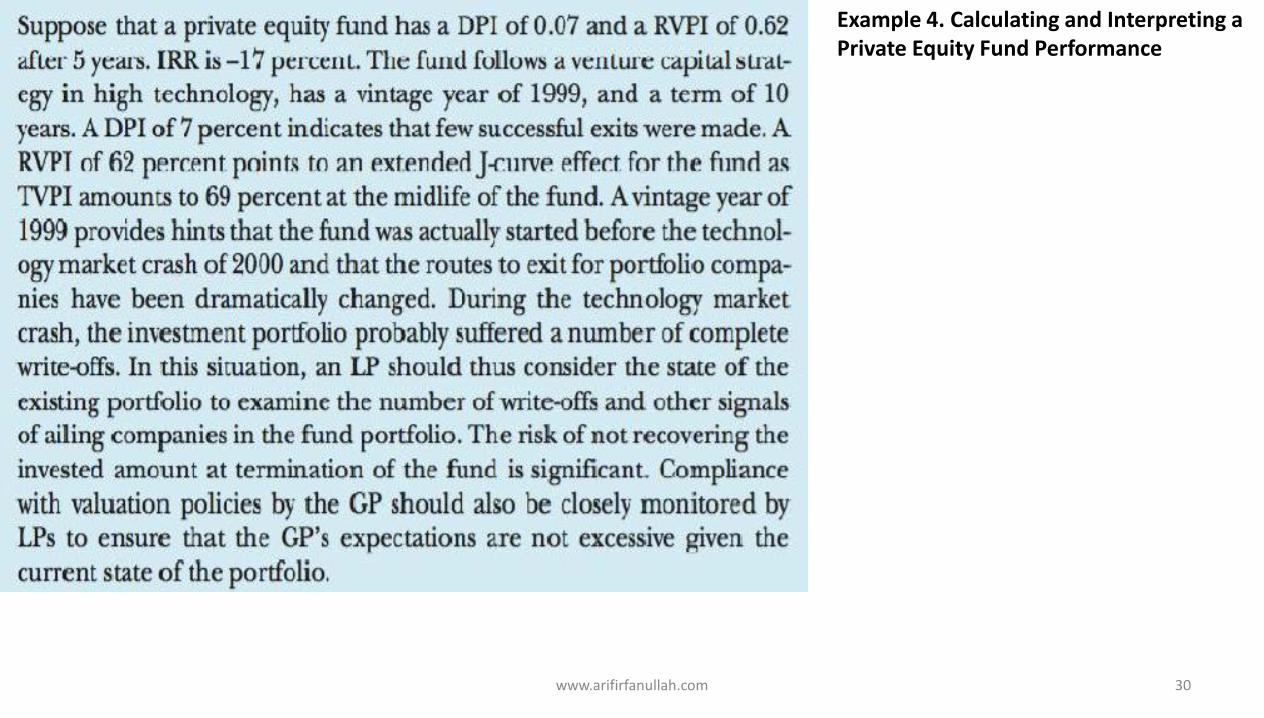

Example 4. Calculating and Interpreting a Private Equity Fund Performance

www.arifirfanullah.com 31

www.arifirfanullah.com 32

www.arifirfanullah.com 33

www.arifirfanullah.com 34

www.arifirfanullah.com 35

www.arifirfanullah.com 36

www.arifirfanullah.com 37

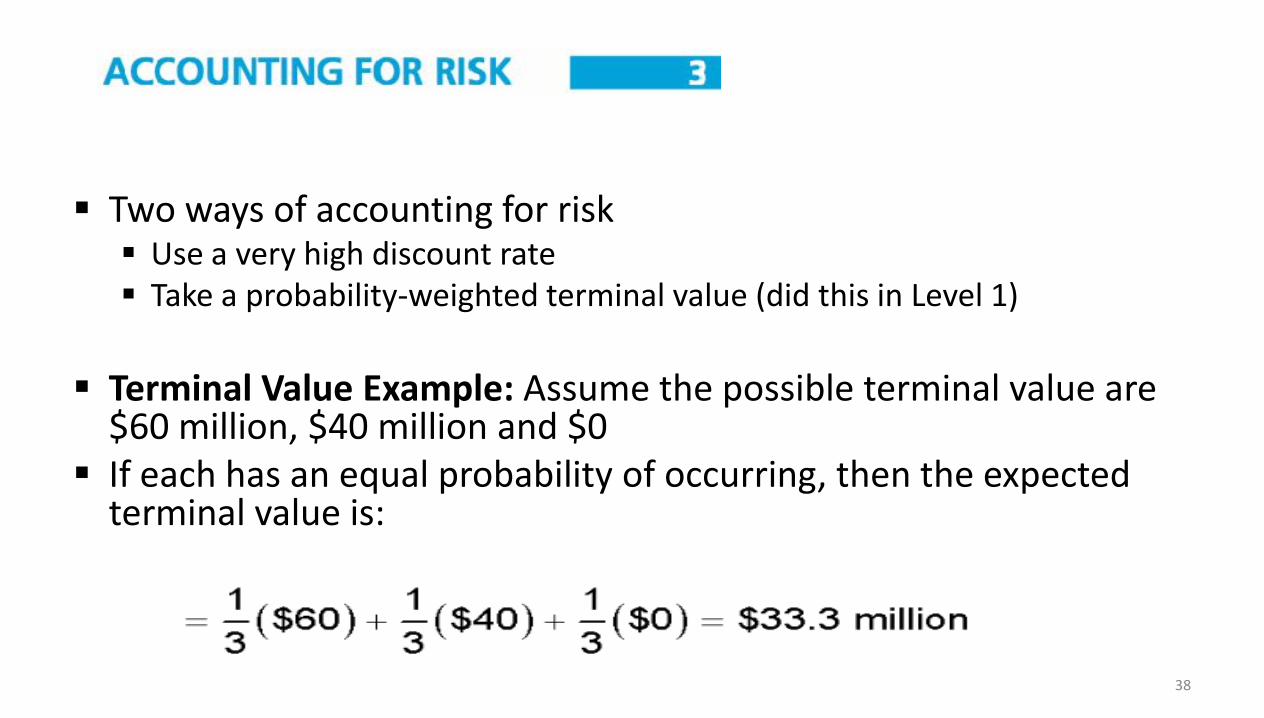

Two ways of accounting for risk Use a very high discount rate Take a probability-weighted terminal value (did this in Level 1)

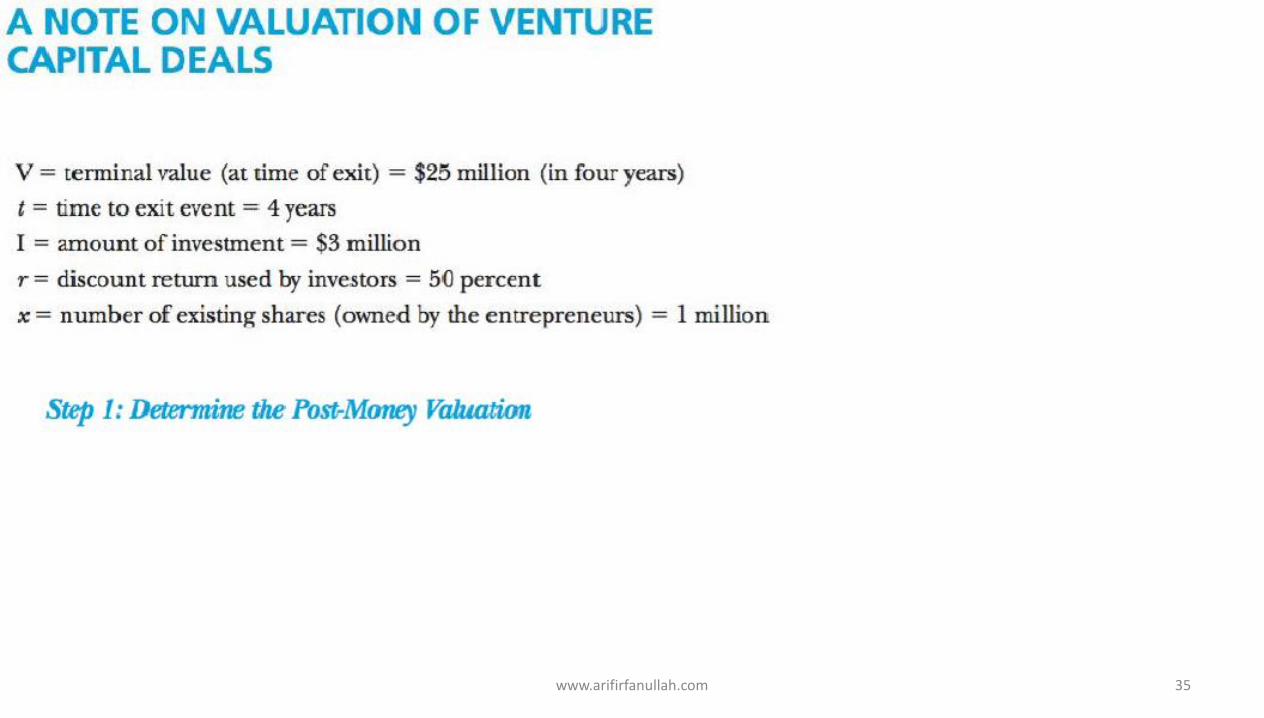

Terminal Value Example: Assume the possible terminal value are

$60 million, $40 million and $0 If each has an equal probability of occurring, then the expected

terminal value is:

38

Conclusion

www.arifirfanullah.com 39