Embed Size (px)

Citation preview

Let’s Do the Math!Maximizing your Return

Opportunity CostThe value of the next alternative when

making a decisionIf I did (bought) A instead of B, what would the

cost be?Can have monetary or non monetary value

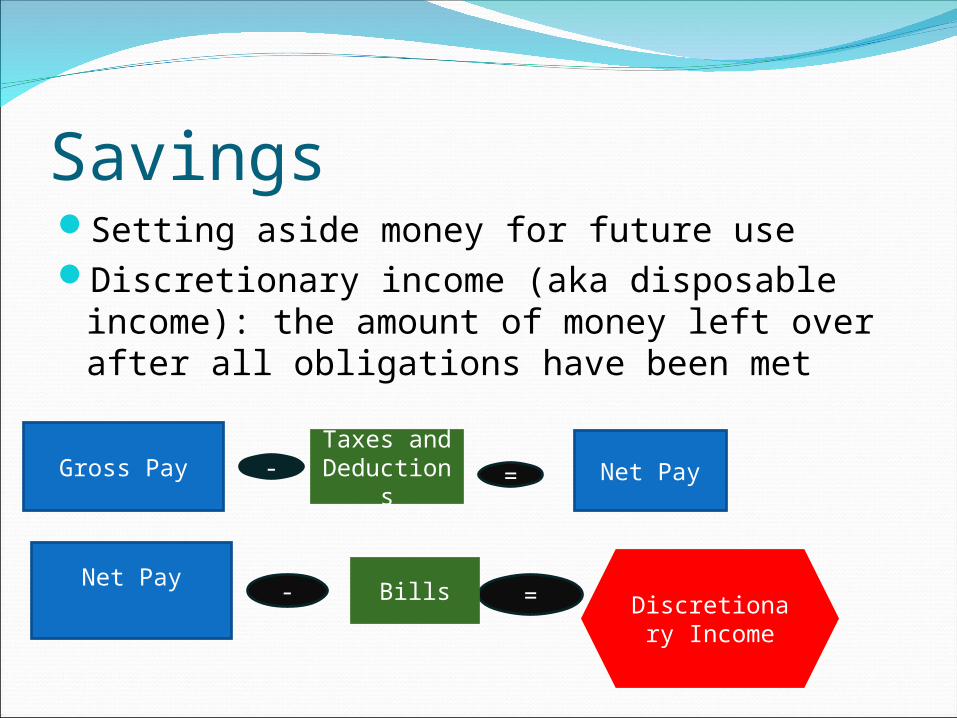

SavingsSetting aside money for future useDiscretionary income (aka disposable

income): the amount of money left over after all obligations have been met

Gross PayTaxes and Deduction

s- = Net Pay

Net PayDiscretionary

Income

- =Bills

InterestInterest is money paid for the use of someone’s money

Simple InterestInterest is computed on amount borrowed or saved only

Accumulated interest doesn’t earn interest

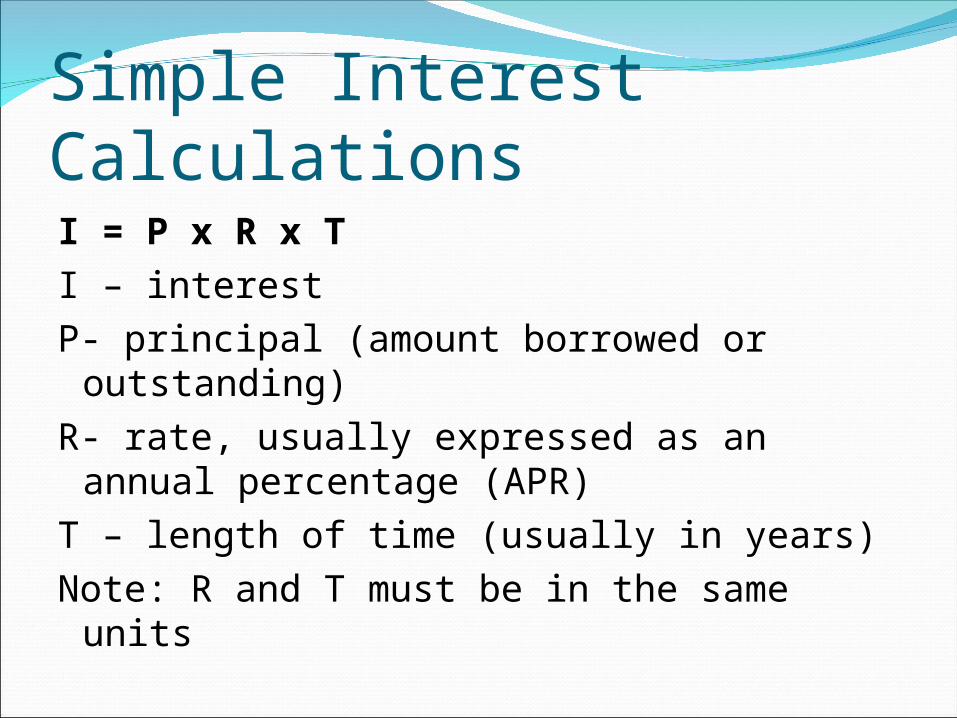

Simple Interest CalculationsI = P x R x TI – interestP- principal (amount borrowed or

outstanding)R- rate, usually expressed as an annual

percentage (APR)T – length of time (usually in years)Note: R and T must be in the same units

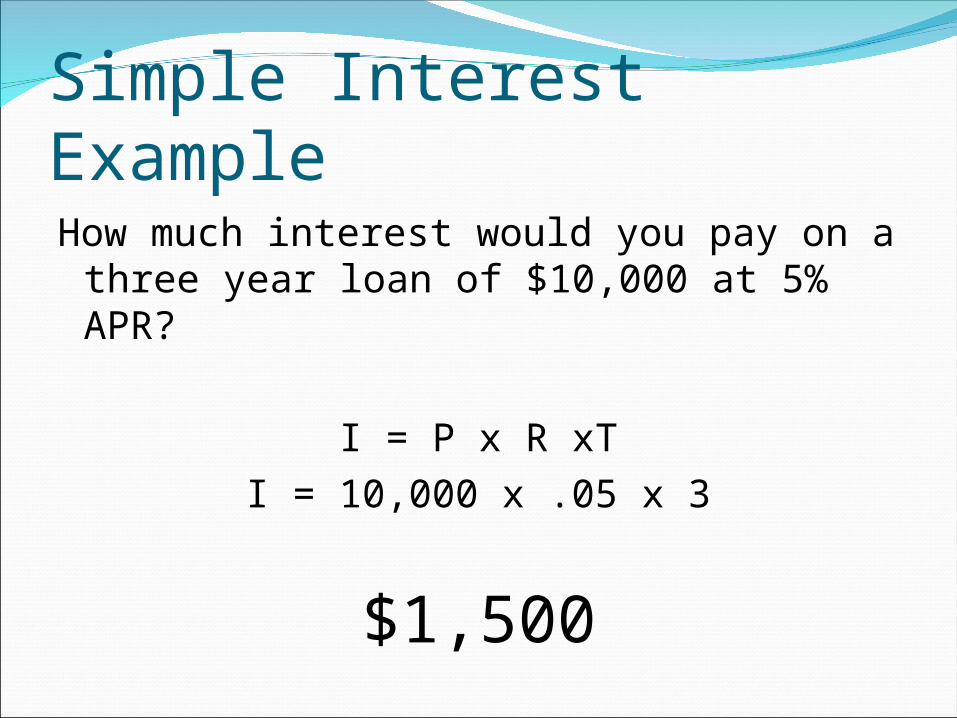

Simple Interest ExampleHow much interest would you pay on a

three year loan of $10,000 at 5% APR?

I = P x R xTI = 10,000 x .05 x 3

$1,500

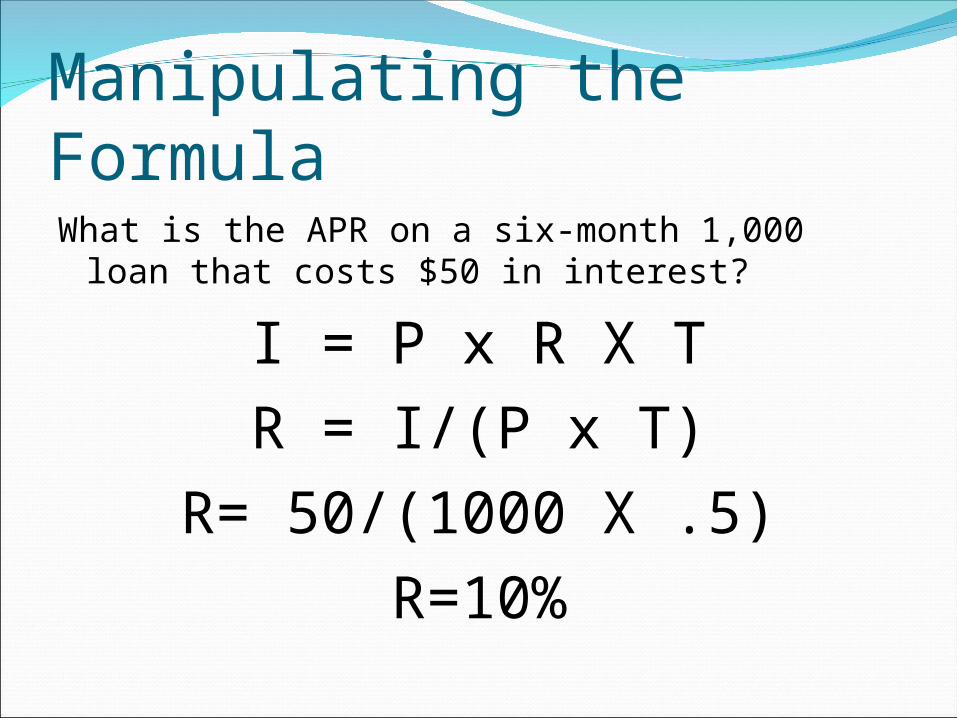

Manipulating the FormulaWhat is the APR on a six-month 1,000 loan that

costs $50 in interest?

I = P x R X TR = I/(P x T)

R= 50/(1000 X .5)R=10%

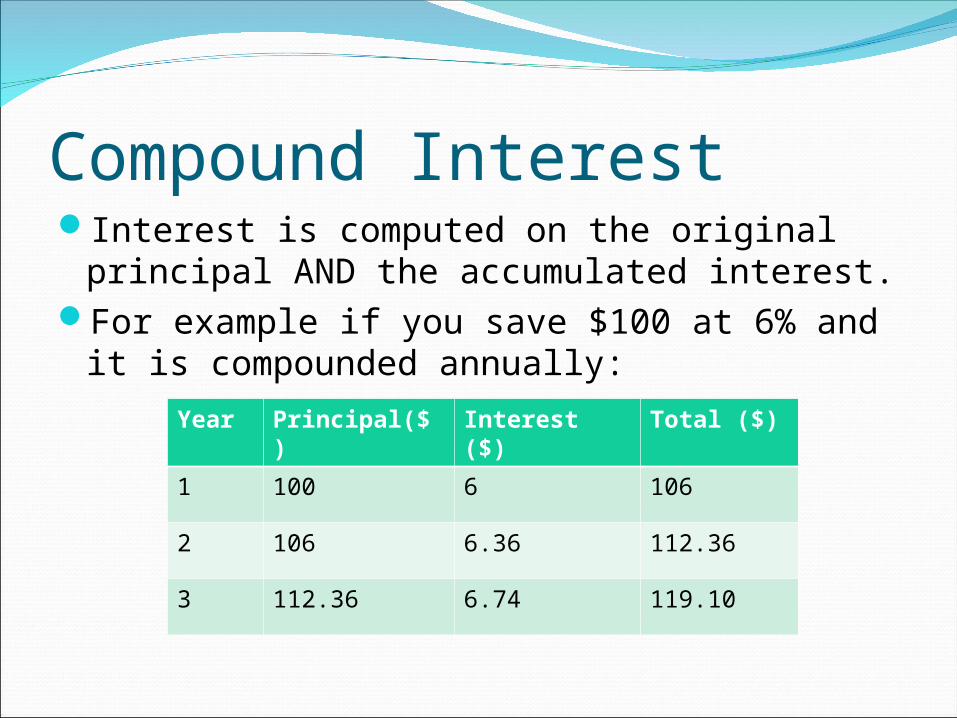

Compound InterestInterest is computed on the original principal

AND the accumulated interest.For example if you save $100 at 6% and it is

compounded annually:

Year Principal($) Interest ($) Total ($)

1 100 6 106

2 106 6.36 112.36

3 112.36 6.74 119.10

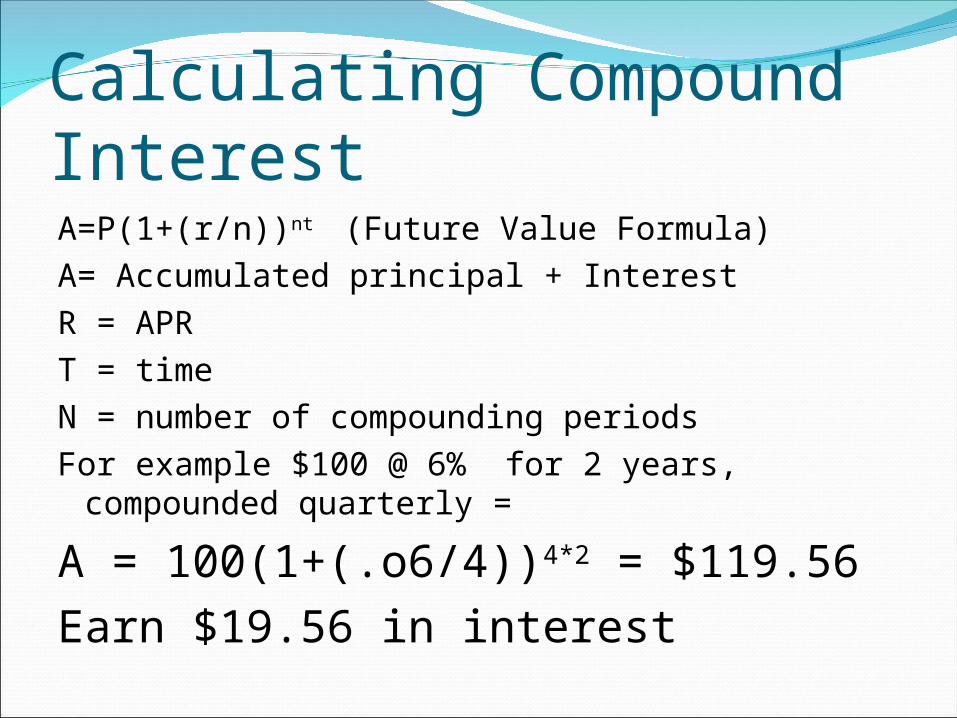

Calculating Compound InterestA=P(1+(r/n))nt (Future Value Formula)A= Accumulated principal + InterestR = APRT = timeN = number of compounding periodsFor example $100 @ 6% for 2 years,

compounded quarterly =

A = 100(1+(.o6/4))4*2 = $119.56Earn $19.56 in interest

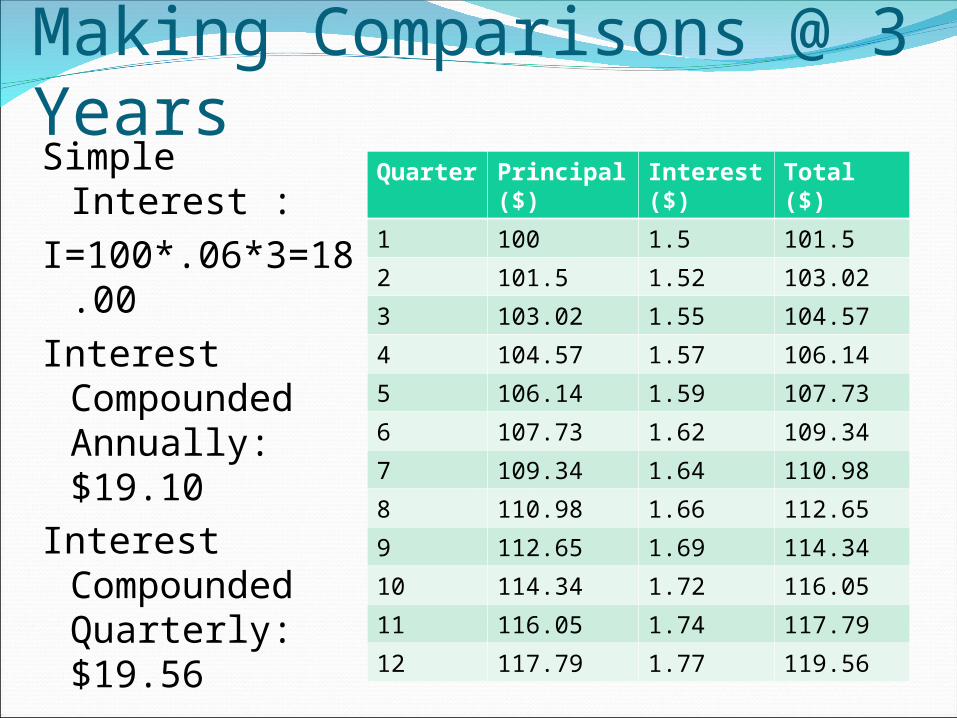

Making Comparisons @ 3 YearsSimple

Interest : I=100*.06*3=18

.00Interest

Compounded Annually: $19.10

Interest Compounded Quarterly: $19.56

Quarter

Principal ($)

Interest ($)

Total ($)

1 100 1.5 101.5

2 101.5 1.52 103.02

3 103.02 1.55 104.57

4 104.57 1.57 106.14

5 106.14 1.59 107.73

6 107.73 1.62 109.34

7 109.34 1.64 110.98

8 110.98 1.66 112.65

9 112.65 1.69 114.34

10 114.34 1.72 116.05

11 116.05 1.74 117.79

12 117.79 1.77 119.56

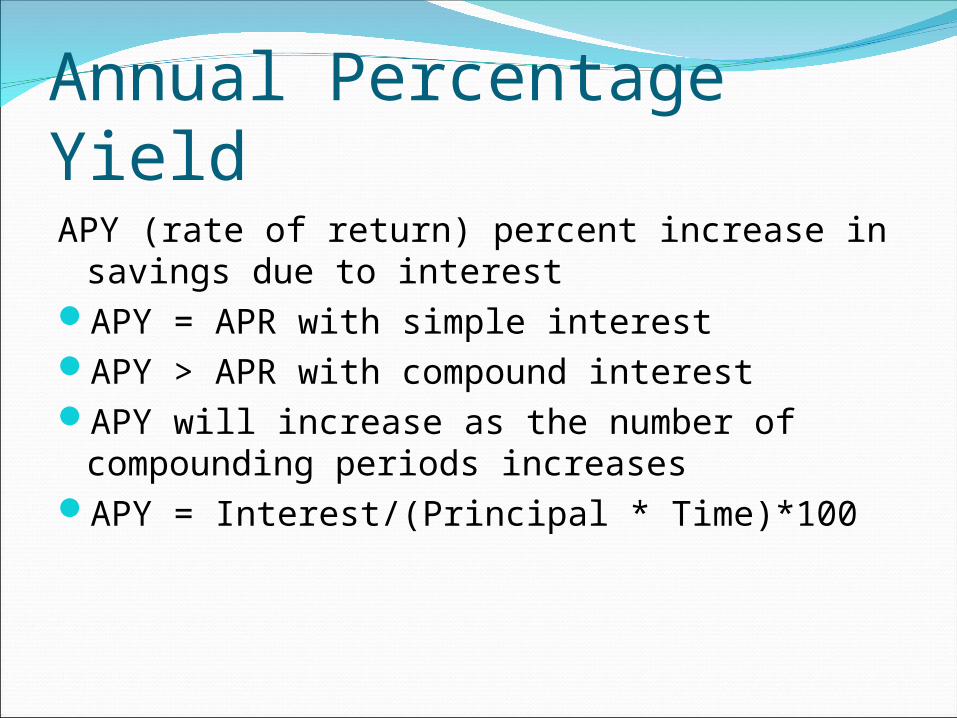

Annual Percentage YieldAPY (rate of return) percent increase in savings

due to interestAPY = APR with simple interestAPY > APR with compound interestAPY will increase as the number of

compounding periods increasesAPY = Interest/(Principal * Time)*100

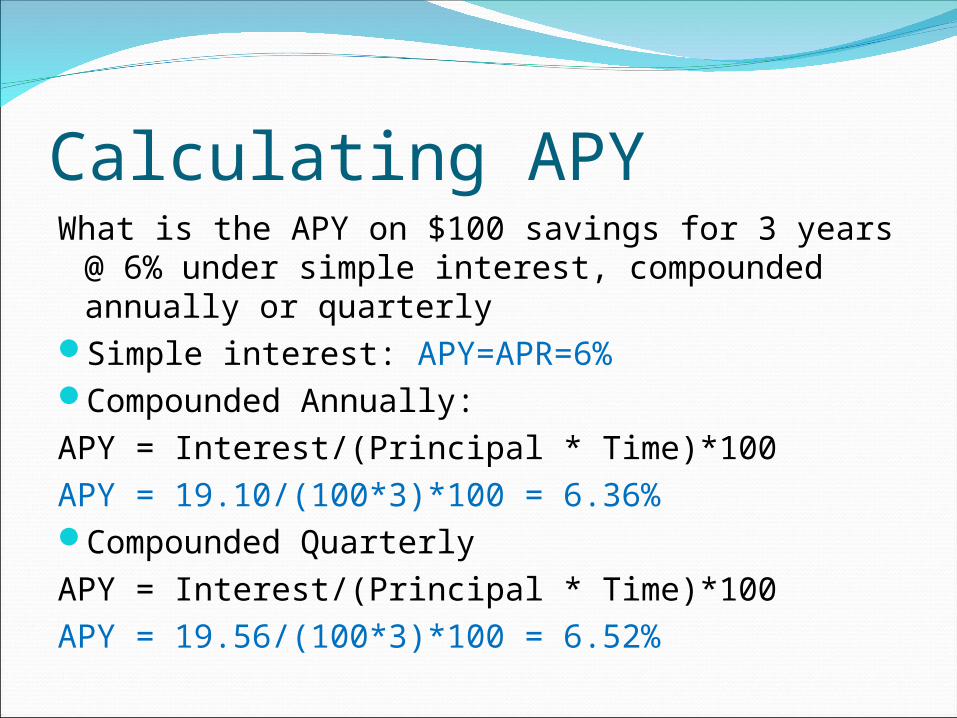

Calculating APYWhat is the APY on $100 savings for 3 years @

6% under simple interest, compounded annually or quarterly

Simple interest: APY=APR=6%Compounded Annually: APY = Interest/(Principal * Time)*100APY = 19.10/(100*3)*100 = 6.36%Compounded QuarterlyAPY = Interest/(Principal * Time)*100APY = 19.56/(100*3)*100 = 6.52%

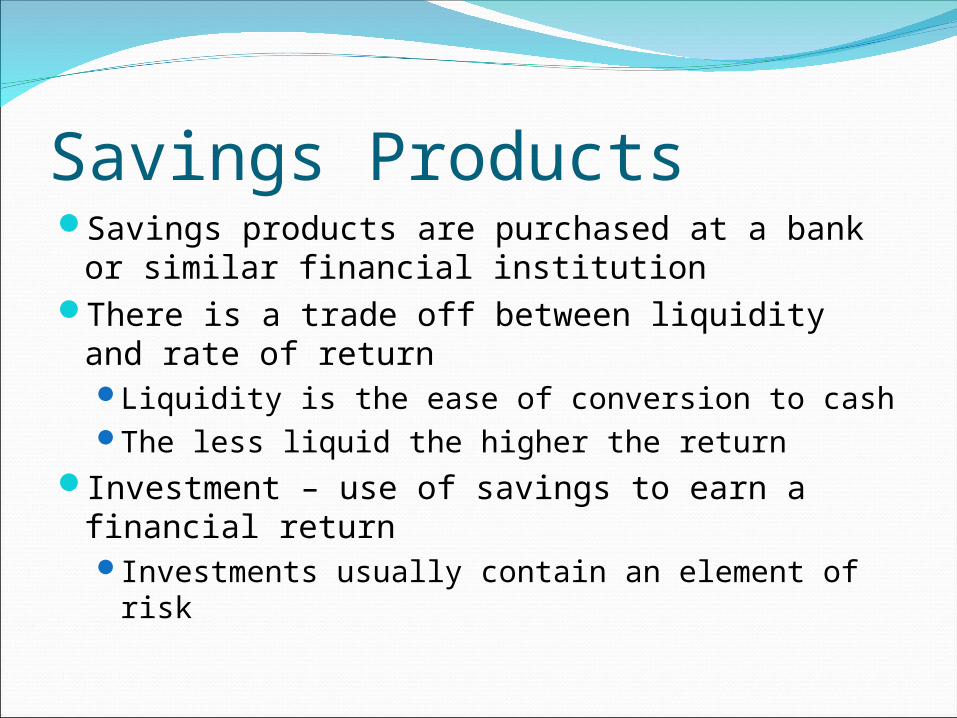

Savings ProductsSavings products are purchased at a bank or

similar financial institutionThere is a trade off between liquidity and rate

of returnLiquidity is the ease of conversion to cashThe less liquid the higher the return

Investment – use of savings to earn a financial returnInvestments usually contain an element of risk

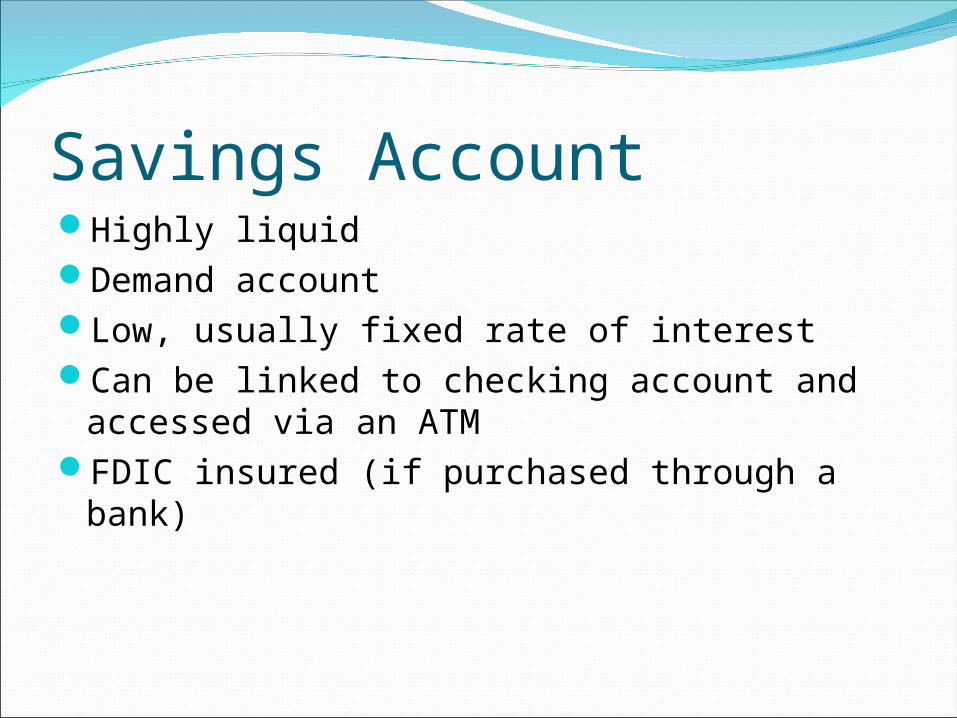

Savings AccountHighly liquidDemand accountLow, usually fixed rate of interestCan be linked to checking account and

accessed via an ATMFDIC insured (if purchased through a bank)

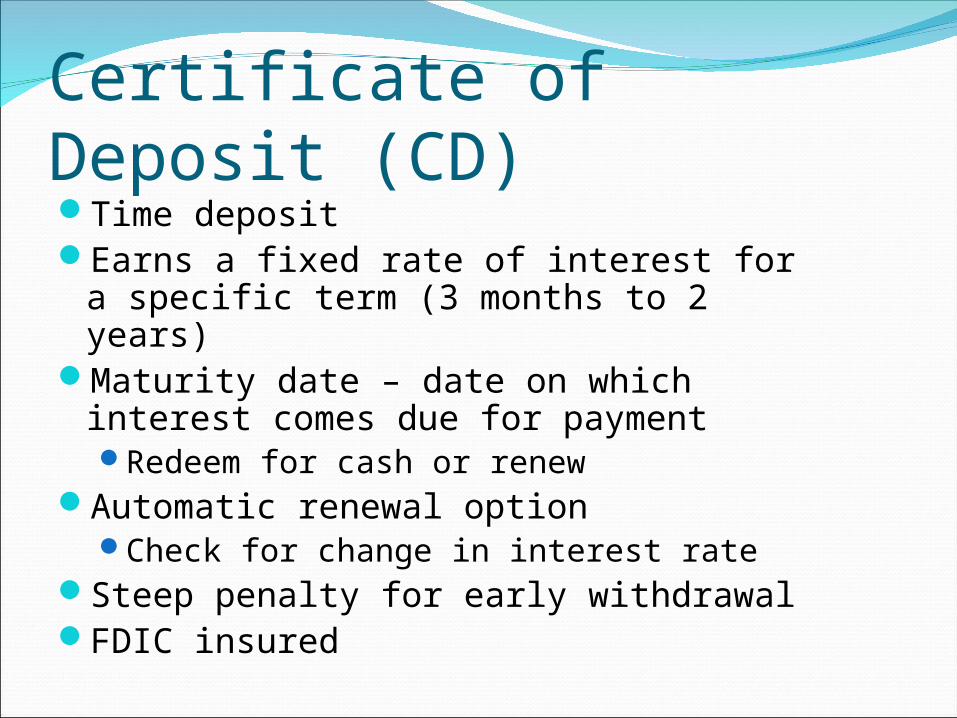

Certificate of Deposit (CD)Time depositEarns a fixed rate of interest for a specific

term (3 months to 2 years)Maturity date – date on which interest

comes due for paymentRedeem for cash or renew

Automatic renewal optionCheck for change in interest rate

Steep penalty for early withdrawalFDIC insured

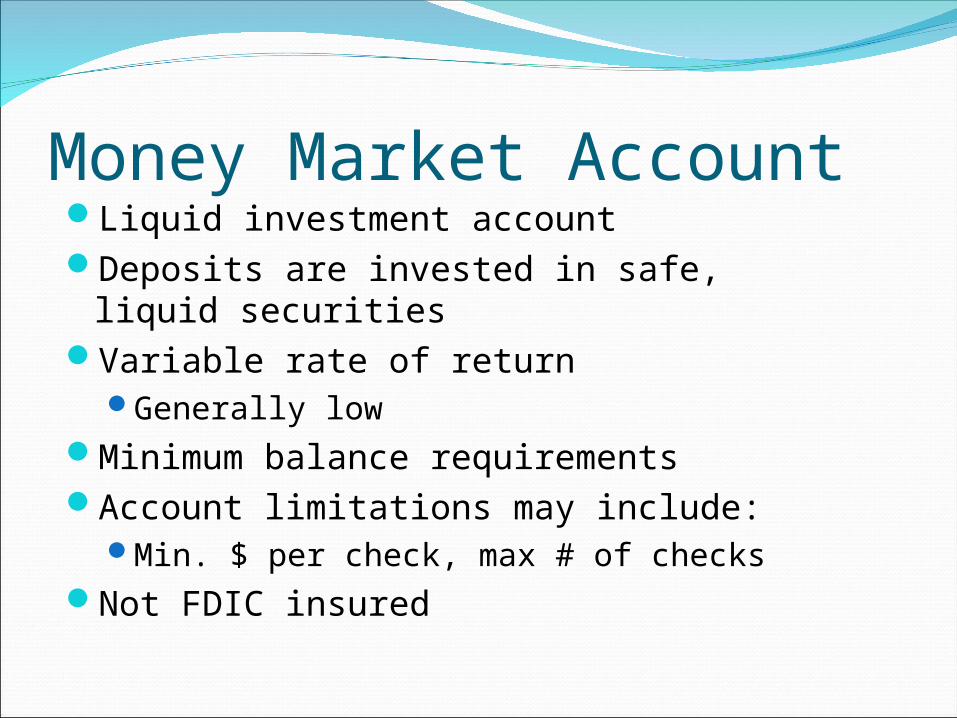

Money Market AccountLiquid investment accountDeposits are invested in safe, liquid

securitiesVariable rate of return

Generally lowMinimum balance requirementsAccount limitations may include:

Min. $ per check, max # of checksNot FDIC insured

Establish a Savings PlanDetermine a specific dollar amount or

percentage of income to invest each pay period

Automatic payments take the pain out of savingYou don’t miss what you don’t see

Direct DepositPayroll Deduction