Embed Size (px)

Citation preview

Lessons from the Financial Liberalization Experience of

Turkey, 1990 - 2005

A. Erinç Yeldan

Bilkent University

IDEAs Network

With the completion of capital account liberalization in 1989, Turkey is trapped into

• high real rates of interest and

• an overvalued exchange rate (cheap foreign currency)

Worsening of macroeconomic fundamentals led by capital inflows: The Dornbusch-Taylor cycle

Rise in the domestic interest rate:

Stimulate capital inflows

Domestic currency appreciates

Imports expand, current account deficit widens

To finance the foreign deficit, invite even more capital inflows, raise the interest rate

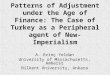

Inflation is on a falling trend, yet the real interest rate proves to be inertial...

Inflation (WPI, 1994=100) and Real Interest Rates

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

Wholesale Price Inflation (1994=100)

Real GDI Interest Rate

Real Credit Interest Rate

Interest Expenditures on Public Debt / Tax Revenues (Targets and Realizations, %)

0

20

40

60

80

100

120

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Interest Expenditures / Tax Revenues (Target)

Interest Expenditures / Tax Revenues (Realization)

Macroeconomic Prices of the IMF Programme

2001 2002 2003 2004 2005 2006

Inflation 68.5 35.0 20.0 12.0 8.0 5.0

Nominal Rate of Interest on Domestic Debt 99.7 69.6 46.0 32.4 27.4 23.9

Ex Ante Real Interest Rate on Domestic Debt 18.5 25.6 21.7 18.2 18.0 18.0

Speculative Financial Arbitrage on the Interest Rate and Depreciation (%)

(1+R)/(1+e)-1

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Jan.92 Jan.93 Jan.94 Jan.95 Jan.96 Jan.97 Jan.98 Jan.99 Jan.00 Jan.01 Jan.02 Jan.03 Jan.04 Jan.05

Large scale of Capital Inflows lead to currency Mis-alignment...

Turkey: Real Exchange Rate Index (1982 = 100) (Deflated by Fixed 1987 Wholesale Prices)

40

50

60

70

80

90

100

110

120

130

Index of the Real Exchange Rate (TL/$)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Jan.01 May.01 Sep.01 Jan.02 May.02 Sep.02 Jan.03 May.03 Sep.03 Jan.04 May.04 Sep.04 Jan.05 May.05 Sep.05

Balance of Payments Finance Account + Net Errors and Omissions (Millions $) and Real Growth Rate of GDP (%)

-10000

-5000

0

5000

10000

15000

1992Q1 1993Q1 1994Q1 1995Q1 1996Q1 1997Q1 1998Q1 1999Q1 2000Q1 2001Q1 2002Q1 2003Q1 2004Q1 2005Q1

Mill

ion

s U

S$

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Gro

wth

Ra

te (

%)

Total Financing (Million $) (Left Axis)

GDP Real Growth (%) (Right Axis)

Large Current Account Deficits:

2003 Total:

$8.0 billion (3.4% of GNP)

2004 Total:

$15.7 billion (5.2% of GNP)

2005 First 9 months:

$15.8 billion (6.2% of GNP)

The current account deficit problem emerges not because of its sheer size, but because of the mode of financing

Short Term Debt Stock/ FX Reserves of the Central bank

0.400

0.600

0.800

1.000

2001Q4 2002Q4 2003Q4 2004Q1 2004Q2 2004Q3 2004Q4 2005Q1 2005Q2 2005Q3

Characteristics of new varieties of crises

• International capital market has been the major source of shocks

• Flows have largely originated from and been received by the private sector

• The financial crises have mostly hit emerging market economies that were considered to be highly credible and successful

• The rise of capital inflows has been characterized by a lack of regulation, on both the supply and the demand sides.

In the summarizing words of the UNCTAD’s 1998 Trade and Development Report,

“ Economic crises are often associated with deterioration of the macroeconomic fundamentals in the recipient country. However, such deterioration often results from the effects of capital inflows themselves as well as from external developments, rather than from shifts in domestic macroeconomic policies”.

“the ascendancy of finance over industry together with the globalization of finance have become underlying sources of instability and unpredictability in the world economy. (…) In particular, financial deregulation and capital account liberalization appear to be the best predictor of crises in developing countries”

(pp.v and 55).

Policy implications

•Prudential regulation and new financial architecture (though necessary, will not suffice to break the Dornbusch-Taylor cycle)

•The Role of the Central Bank (Independent or Irrelevant?)

•Management of capital inflows

•Management of the real exchange rate