Embed Size (px)

Citation preview

L E S S O N S F R O M T H EF I N A N C I A L C R I S I S : T H EI N T E R N A T I O N A L D I M E N S I O N ecaf_1914 22..26

Roland Vaubel

The current financial crisis has arisen as a result of entrepreneurial and businesserror rather than because of inappropriate incentives within the private sector.However, government failure has exacerbated the problem. The case for respondingto government failure by greater international co-ordination of banking regulation isweak. The IMF is particularly ill-suited for this job.

Keywords: Financial crisis, international regulation, market failure, governmentfailure.

Market failure and the bankingcrisis

To draw lessons from the crisis, we have tounderstand its causes. There are two schoolsof thought. According to the first, the crisiswas caused by wrong incentives: the owners ofthe banks took excessive risks because theirliability is limited, and bank managers evenknowingly sought these risks because theirtime horizon is limited and because theirremuneration is conditional on short-runperformance. Thus, this school attributes thecrisis to market failure.

The disadvantages of limited liability havebeen known for centuries. Nevertheless, formany purposes, limited liability has prevailedin the market. The same is true for thedelegation of decision-making to managersand the payment of performance-relatedincome components. True, top-ups in theform of stock options are a fairly recentphenomenon but their advantage is preciselythat they provide an incentive to maximiseexpected long-run profits. In this regard, theyare an improvement on traditional bonusesrelated to current profits. Moreover, if limitedliability and delegation to managers explainedthe excessive risk-taking of bank owners andmanagers, there should be similar incentiveproblems and market crises in otherindustries as well. Why is this not the case?

It is no doubt true that limited liabilitypermits negative external effects. Not allexternalities, however, affect the allocation ofresources. Many are infra-marginal, i.e.irrelevant. Take an example: the pilot of afully-booked aeroplane bears a very small partof the damage if he makes a mistake, theplane crashes and everybody is killed.

Nevertheless, he has an entirely sufficientincentive to avoid the crash as it would costhim his own life. Bankruptcy, with or withoutfull liability, is like a crash. Owners andmanagers have a very strong incentive toavoid it. The irrelevance of many externaleffects is an important topic in welfareeconomics but the prophets of market failurelike to ignore it. I turn to the second school ofthought.

Error

The second school does not attribute the crisisto capricious risk-seeking but to simple error.Not wrong incentives but false expectationscaused the crisis. Why?

1. Many bankers misjudged thedevelopment of real estate prices, notablyin the US sub-prime sector.

2. The chain of credit intermediation wasextended to such a degree that the distantlenders and the credit rating agencies, onwhich they relied, knew too little aboutthe creditworthiness of the finalborrowers.

3. The banking executives overestimated thepredictive power of the statisticalportfolio-risk analyses which theirspecialists provided.

The market, like science, operates by ‘trial anderror’, as noted by Karl Popper. Error isinevitable in any innovative activity. Marketcompetition provides a powerful incentive toinnovate. The deregulation of financialmarkets was bound to unleash the forces ofinnovation and, with them, increase thefrequency and size of errors – at least initially.

Centralbanking,monetarystability andfinancialstability

© 2009 The Author. Journal compilation © Institute of Economic Affairs 2009. Published by Blackwell Publishing, Oxford

The fact that human beings err does not mean that themarket is inefficient. The market is a mechanism ofco-ordination. In that role, it is highly efficient. But the marketcannot eliminate the unpleasant fact that the future isuncertain. To demand perfect information is to demand theimpossible. Imperfect foresight does not qualify as a marketfailure.

The market provides strong incentives to collect andexploit information – especially if compared with public-sectordecision-making. Moreover, a person who is good at makingforecasts will prefer a well-paid job in a commercial bank to amore frugal career in a regulatory authority. The banks whichhave run into problems have all been regulated in one way oranother – to no avail.

An appraisal

Which of the two schools is correct? How can we find outwhether the bankers capriciously sought excessive risks inresponse to distorted market incentives, or whether theysimply misjudged the situation? The evolution of relative riskpremia gives an unambiguous answer. As, for example,Demyanyk and van Hemert (2008) have shown, the absoluterisk premia for sub-prime mortgages in the USA declined from2001 onwards and continued to be low.1 This is consistent withlow and declining risk aversion, due to wrong marketincentives, but it is also consistent with error: the banks mayhave increasingly underestimated the risks. If the low riskpremia indicate low risk aversion, however, the risk premiashould have been low for other US financial assets as well. Asthe authors demonstrate, this has not been the case. In the UScorporate bond market, for example, risk premia stayed high.Thus, the banks underestimated the specific risks of thesub-prime mortgage market. The losses which many bankersare known to have suffered in their private finances tend tosupport this conclusion.

Finally, a thought experiment may be useful. Let us assumethat the banks had correctly foreseen all risks but that limitedliability and delegation to managers persisted. Would thecrisis have erupted nevertheless? Obviously it would not havedone as it would not have been in the interest of managers orshareholders to destroy shareholder value and take decisionsthat ultimately led to the removal of top management. Now,assume the reverse: assume that there had been full liabilityand no delegation to managers but that the banks stillunderestimated the risks as indicated by the low relative riskpremia. Would there have been a crisis? Yes, of course – andmanagers and owners would have lost even more money.Limited liability and delegation to managers have been neithersufficient nor necessary conditions of the outbreak of thecrisis. Necessary were the banks’ errors.

The main lessons from the crisis must be that the size andconsequences of errors may be much larger that most of usthought. For the future, we need more transparency and largercushions in financial markets. Banks have to provide moreinformation about their special vehicles, sellers of securitisedcredits have to indicate the stake which they retain, andcredit-rating agencies have to disclose their non-ratingactivities. Larger cushions would be provided by higher capitalrequirements – at least in normal times.

Government failure

Even though the crisis was not caused by wrong marketincentives, it may have been due to wrong incentives providedby government. This is the moral-hazard hypothesis. It entailsgovernment failure. The banks may have taken excessive risksbecause they expected the government to bail them out. Theyassumed that they could not crash.

I see two objections to this hypothesis. There have beenbank failures. Even a major bank, Lehman Brothers, has beenpermitted to fail (which in hindsight I would regard as amistake – another instance of government failure). Theprobability of being bailed out by the government was nothigh for the US investment banks triggering the crisis, letalone for the smaller banks. Secondly, the executives of thebailed-out banks, too, had to bear highly unpleasantconsequences (in terms of job loss, salary cuts etc.) which theywould have preferred to avoid at almost all cost.

However, severe incentive problems exist within thepolitical system. Politicians, like bank managers, are appointedfor a limited period of time. Like managers, they have a shorttime horizon. Yet, they are not paid according to success, norare they stakeholders, nor is there a political equivalent tobankruptcy.

With regard to the financial crisis, there is widespreadagreement that the US housing bubble was fuelled by ashort-sighted, over-expansionary monetary policy. Interestrates were kept very low in 2003 and 2004 even though the USeconomy had recovered and was growing at annual rates of2.5% and 3.6%, respectively: 2004 was an election year. True,the Fed’s growth forecasts were somewhat lower than theactual rates but this may have been intended to justify theexcessive monetary expansion before the election.

Furthermore, US Congress distorted the incentives of theprivate mortgage banks by inducing Fannie Mae and FreddieMac to purchase huge amounts of sub-prime mortgagesfrom them.

Some authors argue that the governments themselves havebeen exposed to wrong incentives because internationalcompetition among regulators has triggered a race to thebottom. The lesson they draw is that banks have to be regulatedinternationally, i.e. either by an international organisation orby international agreement. I do not share this view.

Race to the bottom?

It is tempting to assume that, if markets are internationallyinterdependent, policies have to be co-ordinatedinternationally as well. However, as Robert Mundell’s‘assignment solution’ demonstrates,2 this conclusion is notwarranted. Even in the presence of intense internationalmarket integration, decentralised national policy-making willbe perfectly efficient if each policy instrument is directed at thetarget for which it is most effective (or, in Mundell’s words, ifit is assigned according to ‘comparative advantage’). Of course,each policy-maker pays attention to what the otherpolicy-makers do, and he or she reacts to their decisions. Thepolicy-makers are also well advised to inform each other. Butthey do not negotiate and conclude agreements. The‘non-cooperative game’ leads to a ‘Nash equilibrium’ which isstable and efficient.

23iea e c o n o m i c a f f a i r s s e p t e m b e r 2 0 0 9

© 2009 The Author. Journal compilation © Institute of Economic Affairs 2009. Published by Blackwell Publishing, Oxford

The assignment solution is not only possible but alsodesirable. Only if one target is assigned to each instrumentand policy-making institution, will the responsibility for policyfailures be sufficiently transparent. Without clearresponsibility, a corrective feedback mechanism will belacking. The citizens have to know who is to be blamed.Otherwise democratic control cannot function.

Even though the assignment solution is optimal or‘first-best’, it may not be feasible because politicians lackmoderation, promising more than they can deliver. Forexample, they may decide to assign the single instrument‘financial market regulation’ to two targets: financial stabilityat home and a large home country share in the world financialmarket. For such a ‘second-best’ world, the quantitative theoryof economic policy holds another technique in store:optimisation with flexible targets. It attributes weights to thecompeting targets and minimises the overall loss due todeviations from these targets.

If each government assigns financial regulation not only toachieving financial stability but also to achieving a largefinancial market share and if financial regulation reduces themarket share, international competition among regulatorslowers the level of regulation. But there will be no race to thebottom, i.e. zero regulation, because each regulator is alsointerested in financial stability. The race is not to thebottom but to the Nash point. In the framework of flexibletarget optimisation, the Nash point is no longer optimal,however.

This raises the question whether financial stability is reallya flexible target. No government is interested in attractingbanks by deregulating if it expects deregulation to cause afinancial crisis. If deregulation leads to a financial crisis, thismust be due to error on the part of the government.Deregulation would be due to false expectations, not theincentives provided by regulatory competition.

Technically, this is equivalent to saying that financialstability is not a flexible target. It is a fixed target, and it haspriority over the potential target of maximising the country’sfinancial market share. Thus, Mundell’s assignment solution isstill applicable. Decentralised competitive regulation works.

However, if the governments regulated jointly, suchcollusion could easily raise regulation above the level requiredfor financial stability. The danger is real because politiciansand bureaucrats derive utility from the exercise of power. Jointregulation tends to go too far. Moreover, if regulatorydecisions are taken by majority vote in an internationalorganisation, the majority of highly regulated countries tendto impose their restrictions on the more liberal minority. Thisis the so-called ‘strategy of raising rivals’ costs’. EU labour andfinancial regulation provides many examples.3

There is another assumption of the flexible target modelthat has to be questioned. Are financial firms interested insettling in a country that is prone to financial crisis due toinadequate regulation? Even if governments assigned financialregulation to two targets, financial stability and achieving alarge financial market share, these targets would not beindependent of each other as the model assumes. With lineardependence of the targets, Mundell’s assignment solution isagain applicable. Each regulator can kill two birds with onestone.

According to another objection, decentralised regulation istoo lenient because the adverse consequences will also hitforeigners who have no vote in the country. However, neitherthe government nor the banks will want to lose their foreignclients due to inadequate financial regulation.

Finally, national regulation may not be sufficientlyrestrictive because the banks and other financial institutionsare a well-organised interest group, whereas their customers,notably the depositors, are too numerous to be organised.True, this asymmetry exists. But at the international level itwould be much more severe. Most interest groups canorganise and lobby at the international or EU level. But mostdepositors or citizens do not even understand what is beingnegotiated in Washington, Brussels or Basel.

As in many other fields, there is a strong case in favour ofdecentralising responsibility for financial regulation:

1. At the national level, the regulatory authorities are betterable to judge their financial institutions. If necessary, theymay exchange information with each other.

2. At the national level, democratic control is more effective.3. At the national level, the differences in preferences and

needs are better taken into account.4. Decentralised regulation leaves the market more freedom.5. Diversification of regulatory policies reduces risk and

encourages innovation.

Competing international organisations

Several international organisations have claimed a decisiverole in financial regulation. The European Commission hassubmitted a package of proposals on bank solvency, capitalrequirements, deposit guarantees, accounting credit-ratingagencies, hedge funds and executive pay. It proposes a‘European Systemic Risk Council’, which would be purelyconsultative, and a ‘European System of Financial Supervisors’(ESFS), which, by qualified majority, would adopt binding‘harmonised’ rules for the national regulators and licensecredit-rating agencies. The ESFS would take the place of threeexisting committees which have been essentially consultativeand decide by unanimous vote. The proposals closely followthe recommendations of a study group appointed by theCommission and chaired by Mr. de Larosière, a formergovernor of the Banque de France. It is quite obvious that themajority of highly regulated member states is trying to imposetheir level of regulation on the more liberal ones. In politicaleconomy, this is called the ‘strategy of raising rivals’ costs’. As Ihave shown elsewhere, it has widely been used in the field ofEU labour market regulation (Vaubel, 2008). None of theseproposals, if implemented, would have prevented the financialcrisis from happening.

Another international organisation which has beensuggested (and which suggested itself ) as an internationalbanking supervisor is the International Monetary Fund (IMF).The IMF has no experience in this field. It lends to, andsupervises, governments. It does not supervise banks. Theinternational organisation that is experienced in matters offinancial regulation is the Bank for International Settlementsin Basel. Attached to it is the ‘Financial Stability Forum’.

A good regulator needs foresight. Like almost all observers,however, the IMF has not foreseen the financial crisis. In a

24 l e s s o n s f r o m t h e f i n a n c i a l c r i s i s : t h e i n t e r n a t i o n a l d i m e n s i o n

© 2009 The Author. Journal compilation © Institute of Economic Affairs 2009. Published by Blackwell Publishing, Oxford

report published in April 2007, it predicted that ‘the amountof potential credit loss in sub-prime mortgages may be fairlylimited’.4

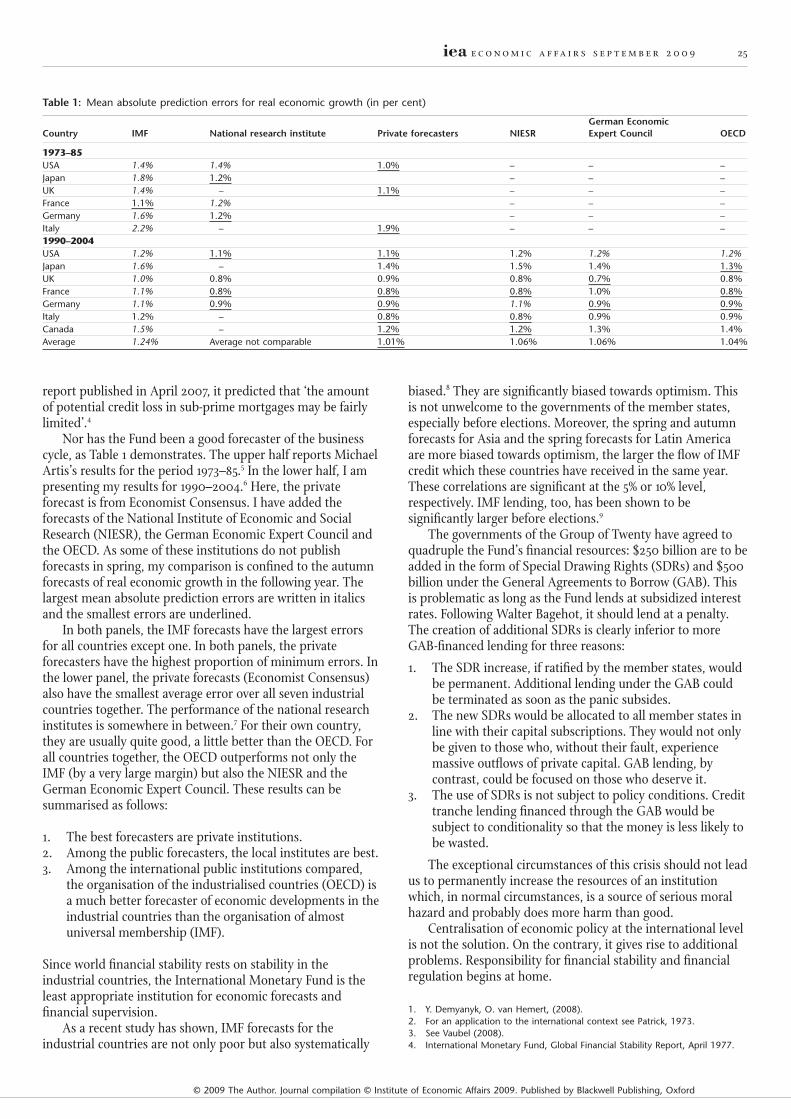

Nor has the Fund been a good forecaster of the businesscycle, as Table 1 demonstrates. The upper half reports MichaelArtis’s results for the period 1973–85.5 In the lower half, I ampresenting my results for 1990–2004.6 Here, the privateforecast is from Economist Consensus. I have added theforecasts of the National Institute of Economic and SocialResearch (NIESR), the German Economic Expert Council andthe OECD. As some of these institutions do not publishforecasts in spring, my comparison is confined to the autumnforecasts of real economic growth in the following year. Thelargest mean absolute prediction errors are written in italicsand the smallest errors are underlined.

In both panels, the IMF forecasts have the largest errorsfor all countries except one. In both panels, the privateforecasters have the highest proportion of minimum errors. Inthe lower panel, the private forecasts (Economist Consensus)also have the smallest average error over all seven industrialcountries together. The performance of the national researchinstitutes is somewhere in between.7 For their own country,they are usually quite good, a little better than the OECD. Forall countries together, the OECD outperforms not only theIMF (by a very large margin) but also the NIESR and theGerman Economic Expert Council. These results can besummarised as follows:

1. The best forecasters are private institutions.2. Among the public forecasters, the local institutes are best.3. Among the international public institutions compared,

the organisation of the industrialised countries (OECD) isa much better forecaster of economic developments in theindustrial countries than the organisation of almostuniversal membership (IMF).

Since world financial stability rests on stability in theindustrial countries, the International Monetary Fund is theleast appropriate institution for economic forecasts andfinancial supervision.

As a recent study has shown, IMF forecasts for theindustrial countries are not only poor but also systematically

biased.8 They are significantly biased towards optimism. Thisis not unwelcome to the governments of the member states,especially before elections. Moreover, the spring and autumnforecasts for Asia and the spring forecasts for Latin Americaare more biased towards optimism, the larger the flow of IMFcredit which these countries have received in the same year.These correlations are significant at the 5% or 10% level,respectively. IMF lending, too, has been shown to besignificantly larger before elections.9

The governments of the Group of Twenty have agreed toquadruple the Fund’s financial resources: $250 billion are to beadded in the form of Special Drawing Rights (SDRs) and $500

billion under the General Agreements to Borrow (GAB). Thisis problematic as long as the Fund lends at subsidized interestrates. Following Walter Bagehot, it should lend at a penalty.The creation of additional SDRs is clearly inferior to moreGAB-financed lending for three reasons:

1. The SDR increase, if ratified by the member states, wouldbe permanent. Additional lending under the GAB couldbe terminated as soon as the panic subsides.

2. The new SDRs would be allocated to all member states inline with their capital subscriptions. They would not onlybe given to those who, without their fault, experiencemassive outflows of private capital. GAB lending, bycontrast, could be focused on those who deserve it.

3. The use of SDRs is not subject to policy conditions. Credittranche lending financed through the GAB would besubject to conditionality so that the money is less likely tobe wasted.

The exceptional circumstances of this crisis should not leadus to permanently increase the resources of an institutionwhich, in normal circumstances, is a source of serious moralhazard and probably does more harm than good.

Centralisation of economic policy at the international levelis not the solution. On the contrary, it gives rise to additionalproblems. Responsibility for financial stability and financialregulation begins at home.

1. Y. Demyanyk, O. van Hemert, (2008).2. For an application to the international context see Patrick, 1973.3. See Vaubel (2008).4. International Monetary Fund, Global Financial Stability Report, April 1977.

Table 1: Mean absolute prediction errors for real economic growth (in per cent)

Country IMF National research institute Private forecasters NIESRGerman EconomicExpert Council OECD

1973–85USA 1.4% 1.4% 1.0% – – –Japan 1.8% 1.2% – – –UK 1.4% – 1.1% – – –France 1.1% 1.2% – – –Germany 1.6% 1.2% – – –Italy 2.2% – 1.9% – – –1990–2004USA 1.2% 1.1% 1.1% 1.2% 1.2% 1.2%Japan 1.6% – 1.4% 1.5% 1.4% 1.3%UK 1.0% 0.8% 0.9% 0.8% 0.7% 0.8%France 1.1% 0.8% 0.8% 0.8% 1.0% 0.8%Germany 1.1% 0.9% 0.9% 1.1% 0.9% 0.9%Italy 1.2% – 0.8% 0.8% 0.9% 0.9%Canada 1.5% – 1.2% 1.2% 1.3% 1.4%Average 1.24% Average not comparable 1.01% 1.06% 1.06% 1.04%

25iea e c o n o m i c a f f a i r s s e p t e m b e r 2 0 0 9

© 2009 The Author. Journal compilation © Institute of Economic Affairs 2009. Published by Blackwell Publishing, Oxford

5. Michael Artis, (1988).6. The calculations are based on data collected by F.O. Aldenhoff.7. The national research institutes in the lower panel are ASA/NBER in the US,

NIESR in the UK, INSEE in France and Institut fuer Weltwirtschaft, Kiel, inGermany.

8. F.O. Aldenhoff, (2007).9. A. Dreher, R. Vaubel, (2004).

ReferencesAldenhoff, F. O. (2007) Are Economic Forecasts of the International

Monetary Fund Politically Biased? A Public Choice Analysis’,Review of International Organizations, 2, 239–260.

Artis, M. (1988) ‘How Accurate is the World Economic Outlook?’, StaffStudies for the World Economic Outlook, Washington, DC: IMF.

Demyanyk, Y. and O. van Hemert (2008) ‘Understanding theSubprime Mortgage Crisis’, Working Paper, Stern School ofBusiness, New York University (http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1020396).

Dreher, A. and R. Vaubel (2004) ‘Do IMF and IBRD Cause MoralHazard and Political Business Cycles? Evidence from Panel Data’,Open Economies Review, 15, 5–22.

International Monetary Fund (1977), Global Financial Stability Report,April, Washington, DC: IMF.

Patrick, J. D. (1973) ‘Establishing Convergent Decentralized PolicyAssignment’, Journal of International Economics, 3, 37–51.

Vaubel, R. (2008) ‘The Political Economy of Labor Market Regulationby the European Union’, Review of International Organizations, 3,435–465.

Roland Vaubel is at the University of Mannheim, Germany([email protected]).

The Journal of Public Economic Theory (JPET) is dedicated to

stimulating research in the rapidly growing field of public economics.

The journal covers a wide range of theoretical approaches, including

general equilibrium theory, game theory, evolution, experimentation,

control theory and dynamics, simulation, axiomatic characterization,

and first order and comparative static methods.

In addition to publishing peer-reviewed, full-length articles, JPET

features short notes, exposita, comments, survey papers and

retrospectives.

Edited byJOHN P. CONLEY andMYRNA WOODERS

Published on behalf of the Association for Public Economic Theory

For more information and to subscribe online visit

www.blackwellpublishing.com/JPET

26 l e s s o n s f r o m t h e f i n a n c i a l c r i s i s : t h e i n t e r n a t i o n a l d i m e n s i o n

© 2009 The Author. Journal compilation © Institute of Economic Affairs 2009. Published by Blackwell Publishing, Oxford