Embed Size (px)

Citation preview

Rangan Banerjee

Forbes Marshall Chair Professor

Department of Energy Science and Engineering

IIT Bombay

Lessons from Green Finance in India

CEP Workshop on Green Finance, IIT Bombay, April 25-26, 2013

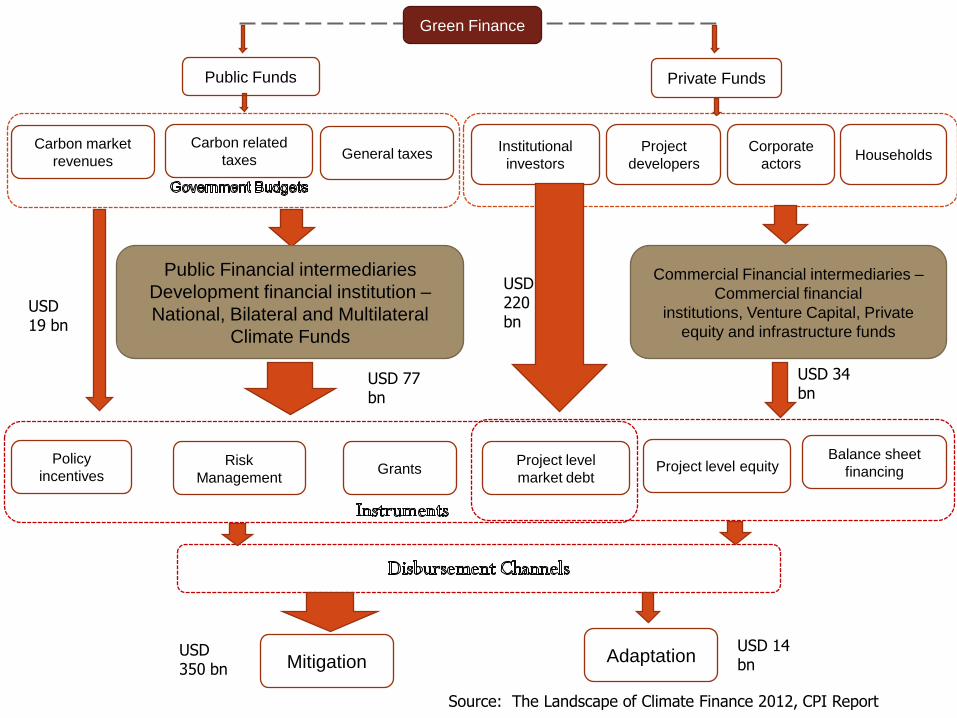

Public Financial intermediaries

Development financial institution –

National, Bilateral and Multilateral

Climate Funds

USD 77 bn

USD 19 bn

General taxesCarbon related

taxesCarbon market

revenuesCorporate

actors

Private Funds

Project

developers

Institutional

investorsHouseholds

Commercial Financial intermediaries –

Commercial financial

institutions, Venture Capital, Private

equity and infrastructure funds

USD 34 bn

USD 220 bn

Risk

Management

Policy

incentivesGrants Project level equity

Balance sheet

financingProject level

market debt

Mitigation AdaptationUSD 14 bn

USD 350 bn

Source: The Landscape of Climate Finance 2012, CPI Report

Public Funds

Green Finance

3

Green Finance

Mitigation Adaptation

Renewable

Energy

DSM

Smart Grids

Energy

Efficiency

CCS

Energy Transport Housing Forestry

Wind Power Biomass

Biofuels

Solar PV Solar Thermal Tidal / Wave Small Hydro

Green Buildings

Forestry Energy Housing

Green Finance by project type

Centralised/Distributed

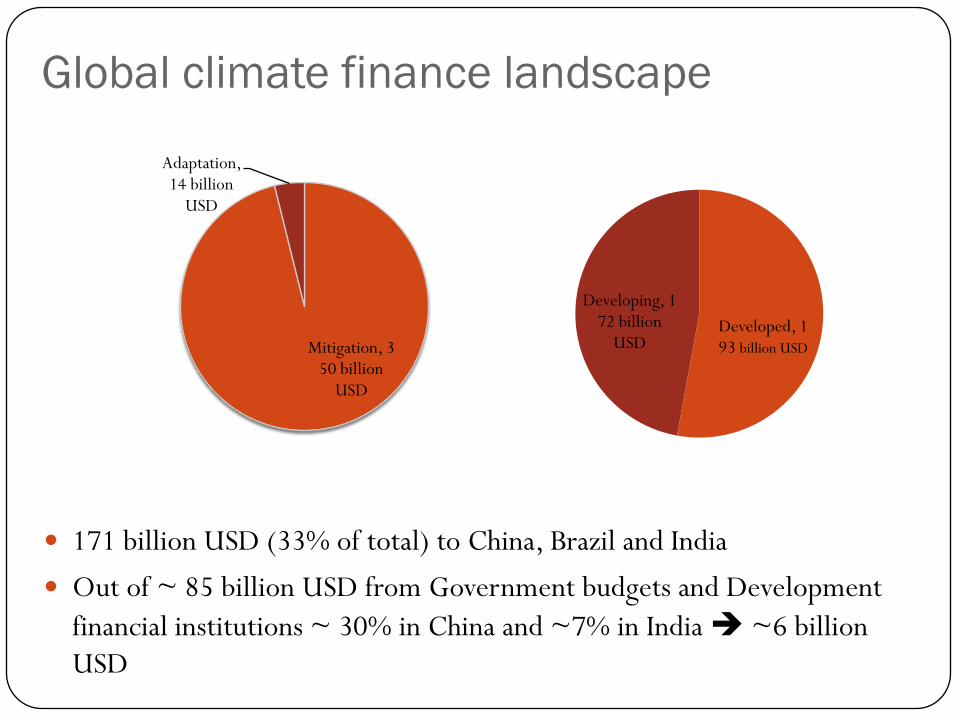

Global climate finance landscape

Mitigation, 350 billion

USD

Adaptation, 14 billion

USD

Developed, 193 billion USD

Developing, 172 billion

USD

171 billion USD (33% of total) to China, Brazil and India

Out of ~ 85 billion USD from Government budgets and Development

financial institutions ~ 30% in China and ~7% in India ~6 billion

USD

Cost Of Finance – India and US

5Source: Nelson et al, 2012

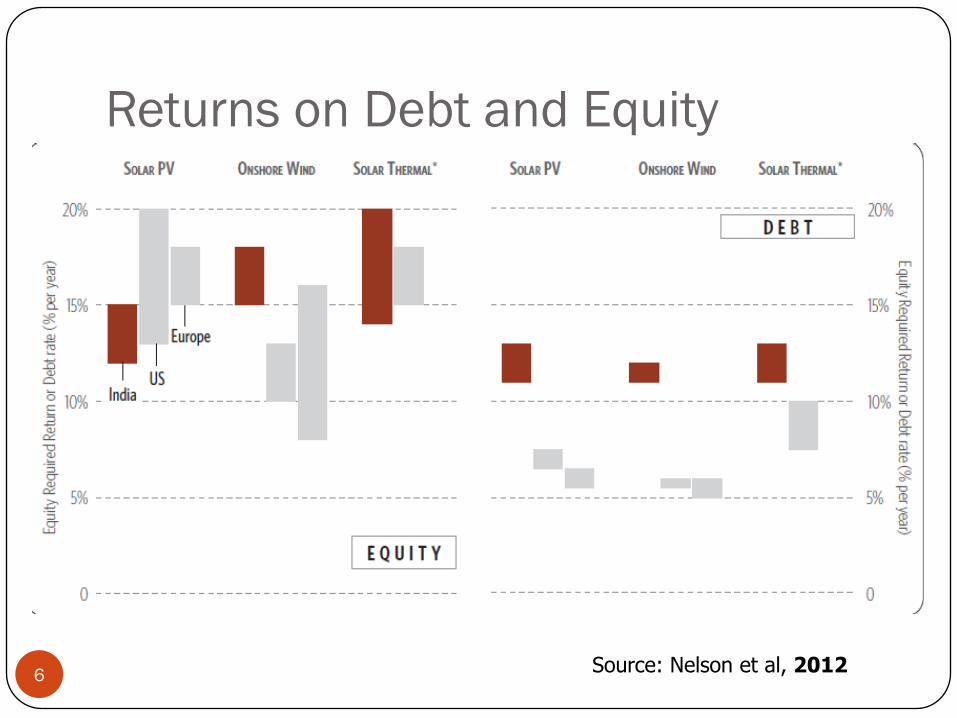

Returns on Debt and Equity

6Source: Nelson et al, 2012

Impact of Debt and Equity

7Source: Nelson et al, 2012

Comparison of Renewable Projects

8 Source: Nelson et al, 2012

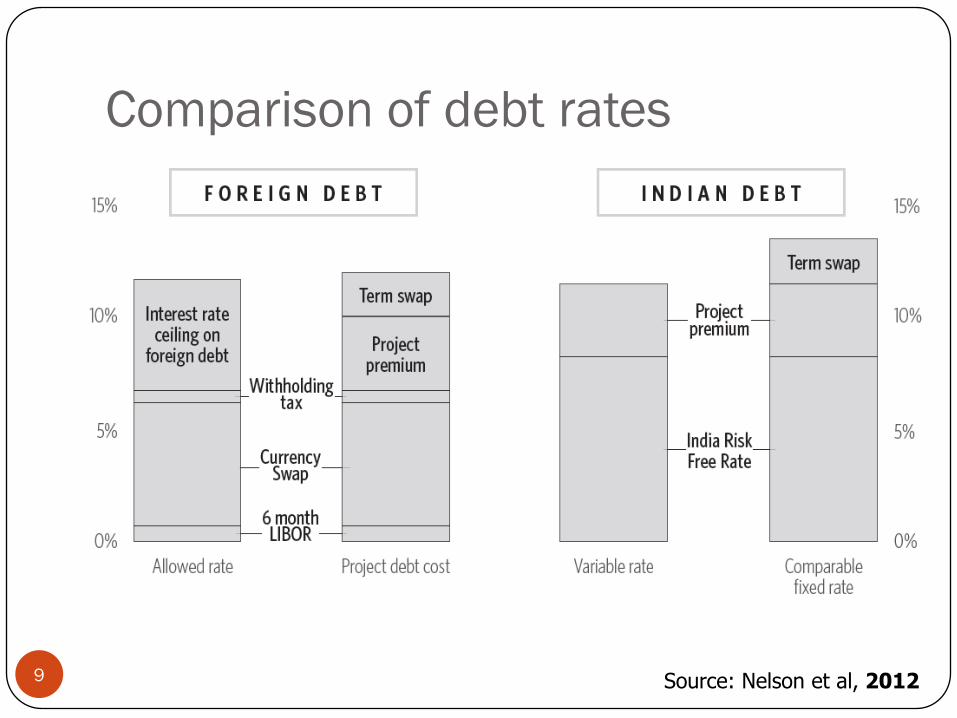

Comparison of debt rates

9 Source: Nelson et al, 2012

10Source: Nelson et al, 2012

Debt : Summary

CO

ST

AN

D T

ER

MS

High general Indian interest rate environment

Longer tenor debt is generally unavailable

Fixed interest rate debt is difficult to find

Debt is usually offered on a relationship basis

Shortage of debt

AV

AIL

AB

ILIT

Y

Bank place limits

Renewable energy debt is often included within power or

energy sector limits

Some banks are not lending to renewable energy

Limits on foreign debt

Technology risk

State-level policy

Fin

an

cia

l

Mark

et

Re

ne

wa

ble

Sp

ecific

Fo

reig

n

Inve

stm

en

t

Te

ch

.

Sp

ecific

Sta

te.

Sp

ecific

C L C L C L C L C L

Low

Medium

High

Very High

C Current

L Long term

11

CO

ST

AN

D

TE

RM

S

Equity returns appear reasonable for good projects

Technology maturity and strategic positioning affects

required project returns

AV

AIL

AB

ILIT

Y

Equity is generally available

Equity from foreign investors is also available

Equity availability is heavily skewed towards a few states

Lack of debt may reduce available equity in the medium

term

Equity : Summary

Source: Nelson et al, 2012

Fin

an

cia

l

Ma

rke

t

Re

ne

wa

ble

Sp

ecific

Fo

reig

n

Inve

stm

en

t

Te

ch

.

Sp

ecific

Sta

te

Sp

ecific

C L C L C L C L C L

Low

Medium

High

Very High

C Current

L Long term

12 Source: Nelson et al, 2012

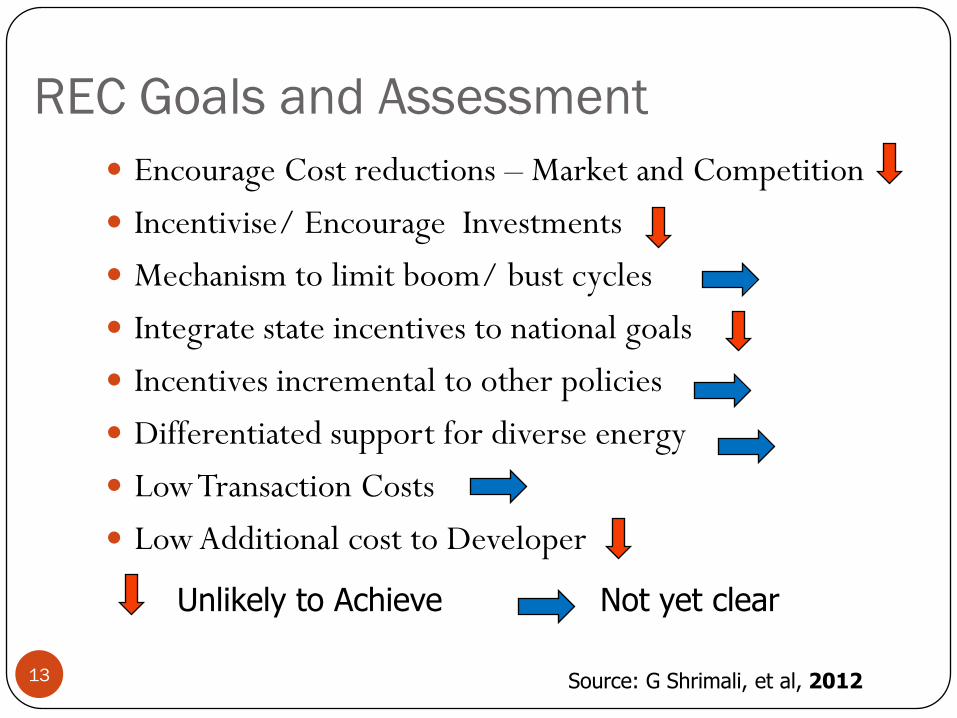

REC Goals and Assessment

13

Encourage Cost reductions – Market and Competition

Incentivise/ Encourage Investments

Mechanism to limit boom/ bust cycles

Integrate state incentives to national goals

Incentives incremental to other policies

Differentiated support for diverse energy

Low Transaction Costs

Low Additional cost to Developer

Unlikely to Achieve Not yet clear

Source: G Shrimali, et al, 2012

14Source: G Shrimali, et al, 2012

15Source: G Shrimali, et al, 2011

Grid connected power case studies

Project Technology Size

(MW)

Estimated

cost

Financing Status

Tuppadahalli

wind park,

Karnataka

Wind power 56.1 INR 339.4

Crore

CDM, Domestic

debt (11.8%, 14

years), IDFC -60%

Completed

construction

Dahanu solar

PV project,

Rajasthan

Solar PV 40 INR 560

Crore

Debt financing by

U.S. EXIM bank and

ADB for tenors of

16.5 and 17.5 years;

12%

Operational

LANCO’s

Chinnu solar

thermal

project

Solar Thermal 100 INR 1800

Crore

Domestic debt,

11%, 13-14 years,

Axis; JNNSM

Request for

Extension

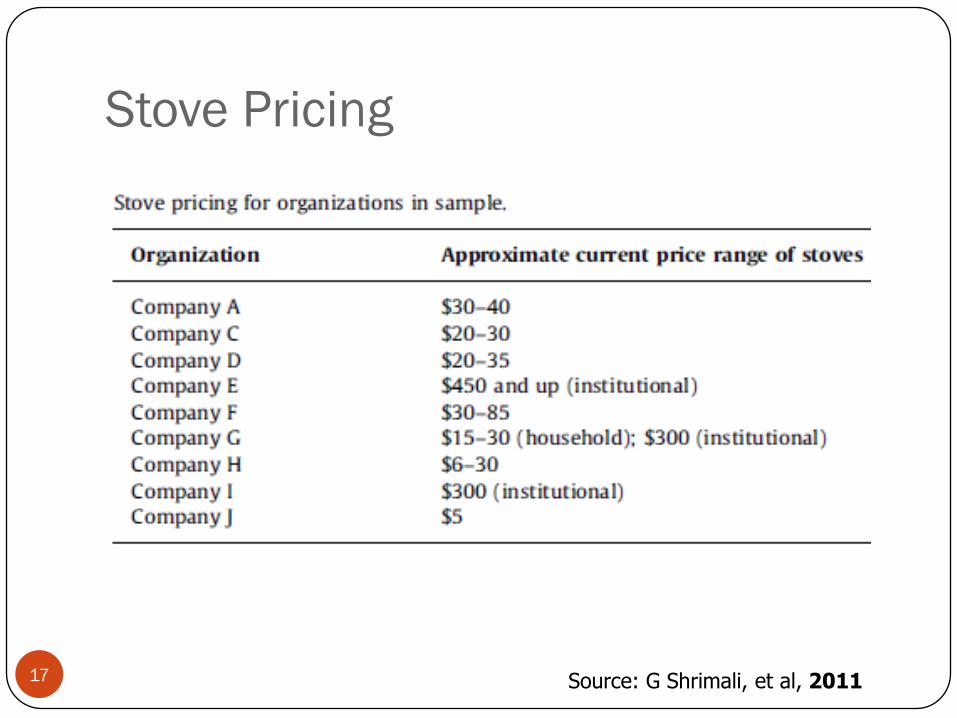

Stove Pricing

17 Source: G Shrimali, et al, 2011

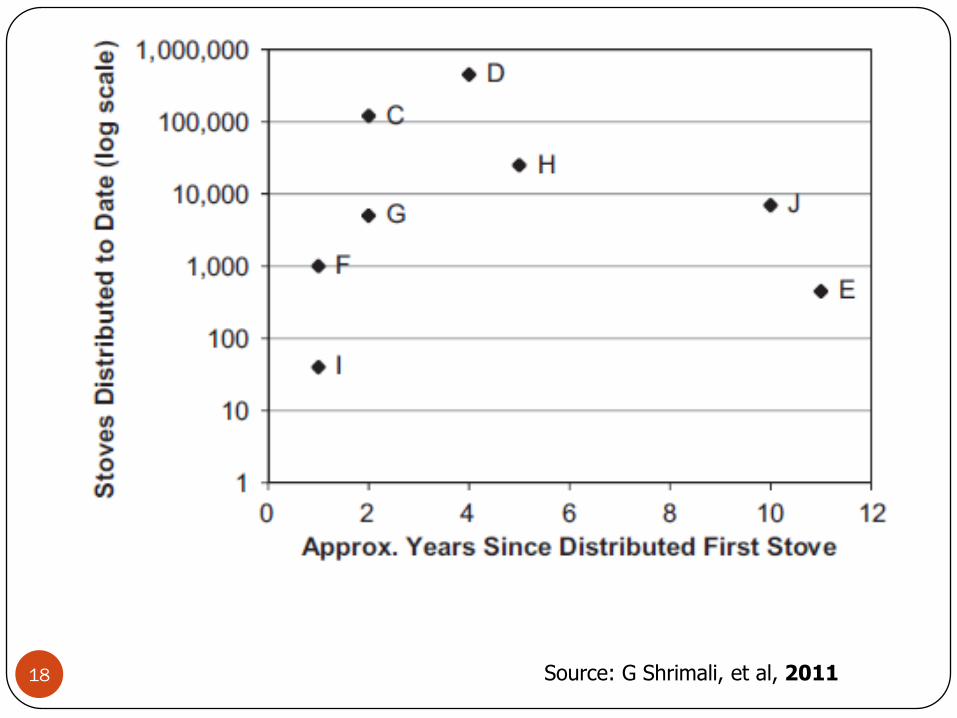

18 Source: G Shrimali, et al, 2011

19Source: G Shrimali, et al, 2011

20 Source: G Shrimali, et al, 2011

Case Study : Capacitor Leasing

21 Source: Taylor et, al, 2008

DSM: Financing through Utility Bill

22 Source: BESCOM, 2006

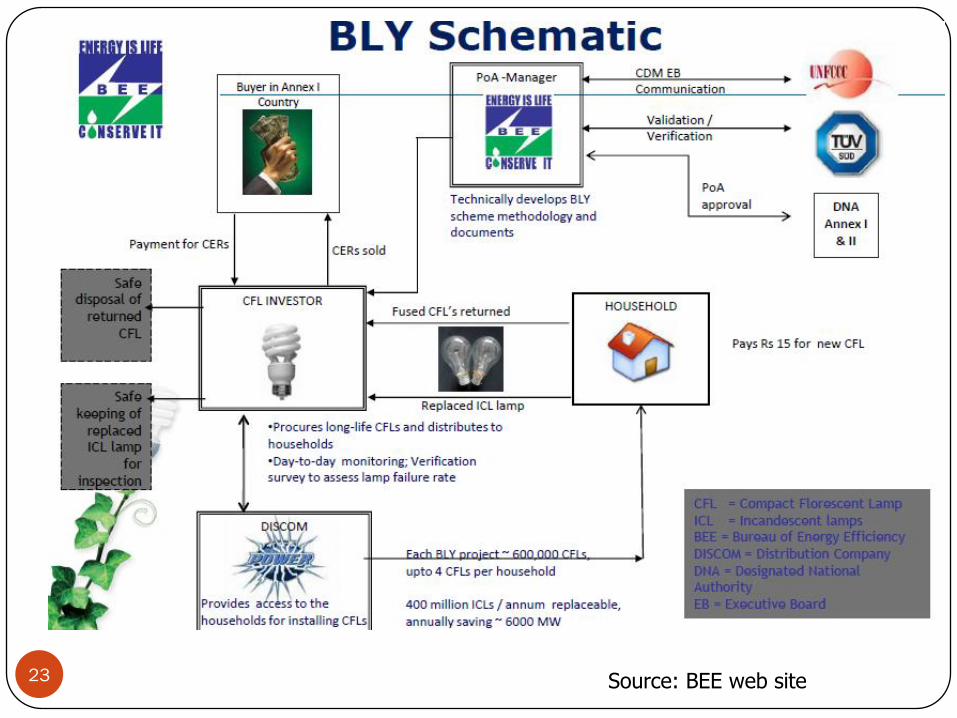

23 Source: BEE web site

Bachat lamp yojana

Dependence on the carbon market ($12/ tonne initial CER

price – reduced to 5$/ tonne)

Payments to CFL manufacturers and/or utilities take 3-4 years

Kerala, Andhra Pradesh, Karnataka, Punjab and Delhi

Target 400 million bulbs

Actual about 25 million bulbs

Lack of investors

24

25

Decentralized

Renewable

Energy: Biomass

and Small Hydro

Solar Home

Systems

Solar Lanterns Energy-Efficient

Cookstoves

Potential Market

/yr

Rs 94.06 billion Rs 1.26 billion Rs 855 million Rs 1.11 billion

Avg Price IRs 8 to 13 /kWh

(B)

INR 2 to 2.5 /kWh

(H)

Rs 7,000 - 20,000 Rs500 -1,600 Rs 150 -1,100

Competitive

Advantage

operational

reliability , low

upfront cost.

Customised

solution.

Kerosene

replacement

Reduced fuel

costs; health

benefits

Business Model B: Company-

owned minigrids;

electricity priced to

existing fuel

expenditure levels.

H:using existing

grid infrastructure;

paid at

government-

tariffs.

Sold on credit, in

partnership with

local banks. Users

typically pay 10 to

25 percent upfront

and the rest in

installments.

Bulk sales to

corporate, NGO,

and (MFI)

partners; sold

directly to

consumers

through local

retailers.

Sold through

multiproducts rural

distributors and

retailers;

partnerships with

MFIs and NGOs.

Source:IFMR- WRI, 2010

Selco Case study

26

For profit company – Solar Home

systems – started 1996 – sold about

100,000 SHS

90% of products – credit schemes

Partnership with 9 banks – interest rates

between 12-17%

Financing Institutions pay 85% of the

amount- monthly payments of Rs 300-

400 over a period of 5 years

Financing/ repayment options –

tailormade to end users – paddy farmers

– repayment schedule based on crop

cycle, street vendors – daily payments –

Rs 10

Funding from REEP – meet margin

amount for poor customers, reduce

interest rate

Source: SELCO, 2011

DESI Power

27

Biomass based power solutions – Bihar- 25 kW to 100 kW

Local distributors – decide pricing

Registered under CDM and sold CERs to Swiss buyer

MNRE funds, Promoters Equity, ICICI Loan

Monthly rate based on no of bulbs / loads, Circuit breaker to limit consumption

Irrigation pump users Rs 50/ hour, Household Rs 120- 150 per month

Underground trunk wiring-distribution

Enabling micro-enterprises –battery charging station, flour mill, workshop etc

Tie up with Telecom towers – increasing capacity factor

Husk Power

28

Initial funding – prize money

30-100 kW – biomass gasifiers- based on rice husk

Energy audit of households

Focus on household demand for lighting

Lower production, operating costs – use of bamboo, asbestos

Overhead pole wiring

Directly reach end user

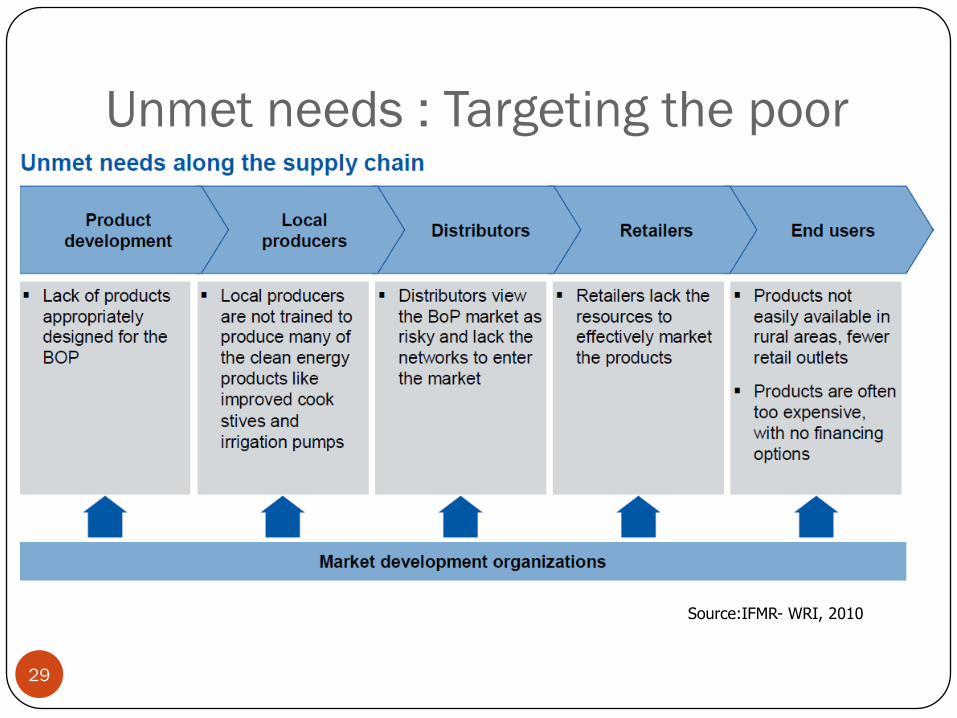

Unmet needs : Targeting the poor

29

Source:IFMR- WRI, 2010

Solar Tower

30

E-Solar – Acme partnership

First grid connected plant in India 2011

2.5 MW out of 10 MW installed Bikaner Rajasthan

Double-axis software-mirror tracking system Lightweight, small size 1 m2 flat mirrors

Plant output not stabilised – insolation, auxiliary consumption

http://acme.in/solar/thermal.html

National Solar Thermal Power Facility – Consortium supported

by MNRE and led by IIT Bombay

Thermal

Storage

Solar Field

Expansion

Vessel

Heat

Exchanger

Generator

Condenser

Turbine

PumpPump

Cooling

Water

Circuit

Water/

Steam

Loop

Thermic

Oil Loop

CLFR

Direct

Steam

Schematic of 1 MW Solar Power PlantSimulator snapshot

Parabolic Trough Solar FieldLinear Fresnel Reflector Solar Field at Gwalpahari site

Consortium Members

KIE Solatherm

31

Summary

32

Problem with debt in India– high interest rates, variable, short tenor (adds 20-28% to cost of project)

Technology uncertainty, Data uncertainty – e.g JNNSM

Policy Mechanism – REC not having desired effect

Innovative business, technology models – cookstoves – large untapped market

Efficiency – CFL – BLY – dependence on CER market, not achieving the scale planned

Untapped – Bottom of Pyramid potential – innovative financing targettedto local needs, end –users

Technology Development- Consortia approaches, Venture capital-Financing early technology

References

33

G Shrimali, et al,Improved stoves in India: A study of sustainable business models Energy Policy, Volume 39, Issue 12, December 2011, Pages 7543-7556

Nelson et al, 2012 Meeting India’s Renewable Energy Targets: The Financing Challenge, Climate Policy Initiative, December 2012

G Shrimali, et al, Falling Short: An Evaluation of the Indian Renewable Energy Certificate Market,Climate Policy Initiative, December 2012

ECO-II Project Design Document, BESCOM Efficient Lighting Programme, 2006

Taylor et al, Financing Energy Efficiency, Lessons from Brazil, China, India and Beyond, World Bank, Washington D.C., USA, 2008

http://www.beeindia.in/schemes/documents/bly/presentations/Presentation-VandanaThakur.pdf (BEE web site)

Case Study: SELCO: Solar Lighting for the Poor- UNDP, 2011

IFMR-WRI-Power to the People, September 2010

http://acme.in/solar/thermal.html