Embed Size (px)

Citation preview

Lesson 8 Announcements

1. Group Quiz. Sit in your groups today

2. Lecture Slides (PPTs) can be retrieved from:[email protected]: Canada

1. Group Quiz. Sit in your groups today

2. Lecture Slides (PPTs) can be retrieved from:[email protected]: Canada

Lesson 8 Chapter 3 (Textbook)

Setting Goals and the Financial Planning ProcessSetting Goals and the Financial Planning Process

Planning for Successful Money Management

Daily spending and saving decisions are the heart of financial planning.

Decisions must be coordinated with needs, goals, and personal situations.

3-2

Money management is the day-to-day financial activity needed to manage personal economic resources, while working toward long-term financial security.

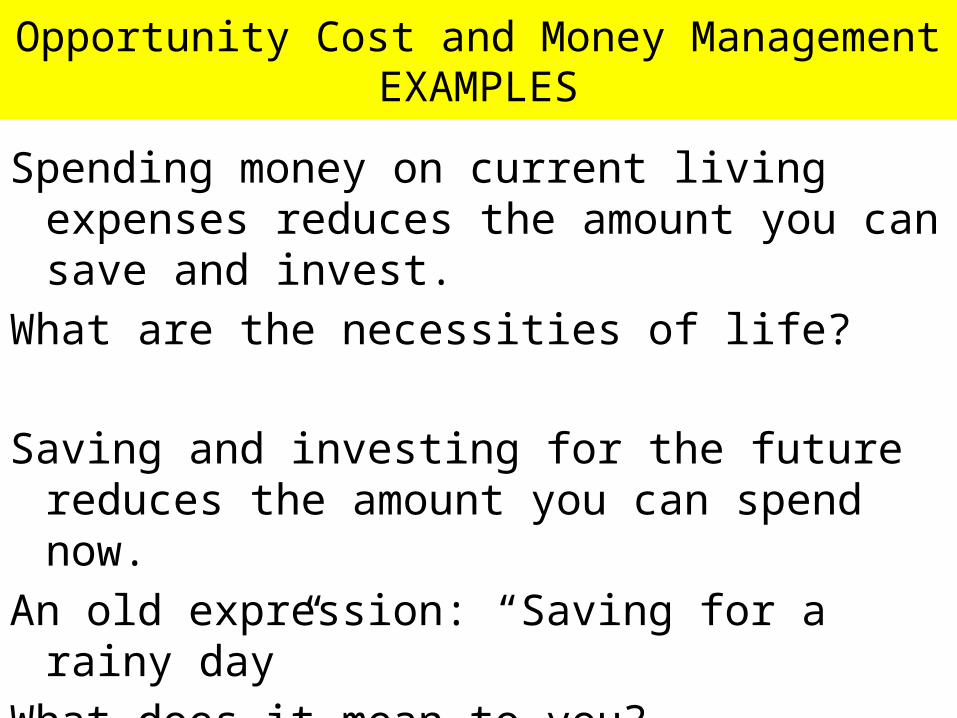

Opportunity Cost and Money ManagementEXAMPLES

Spending money on current living expenses reduces the amount you can save and invest.

What are the necessities of life?

Saving and investing for the future reduces the amount you can spend now.

An old expression: “Saving for a rainy day”What does it mean to you? To keep something, esp. money, for a time in the future when it might

be needed.

Opportunity Cost / Money Management (cont’d)

Buying on credit ties up future income. How?Using credit = borrowing money = using future income to pay

for something now. = giving up future income.Example: Cell phone. 800 RMB or 200 RMB.If I use credit to pay for the 800 RMB cell phone and it takes

me 1 ½ years to pay for it at 15% interest, the opportunity cost is 1.25% per month, of 800 RMB. (if I wait 18 months to pay it off)

FV of 800 RMB = 800 * (1.0125) ^ 18 Future value = 800RMB * 1.25% interest * 18 months.

= 1000.46 I will have to pay 200.46 RMB EXTRA! Is it worth it?

Using savings for purchases results in lost interest and depletes savings.

EXMAPLE: If I purchased a 200 RMB cell phone and used the 800 RMB towards some future expenditure, it would be worth, for example:

=800*(1.05)^20=2,122.64 Was it worth it to have a fancy cell phone that

probably only lasted two years, but had an opportunity cost of 2122.64 RMB?

Imagine if you lost this Opportunity Cost every 2 years!Expression: Keeping up with the Jones

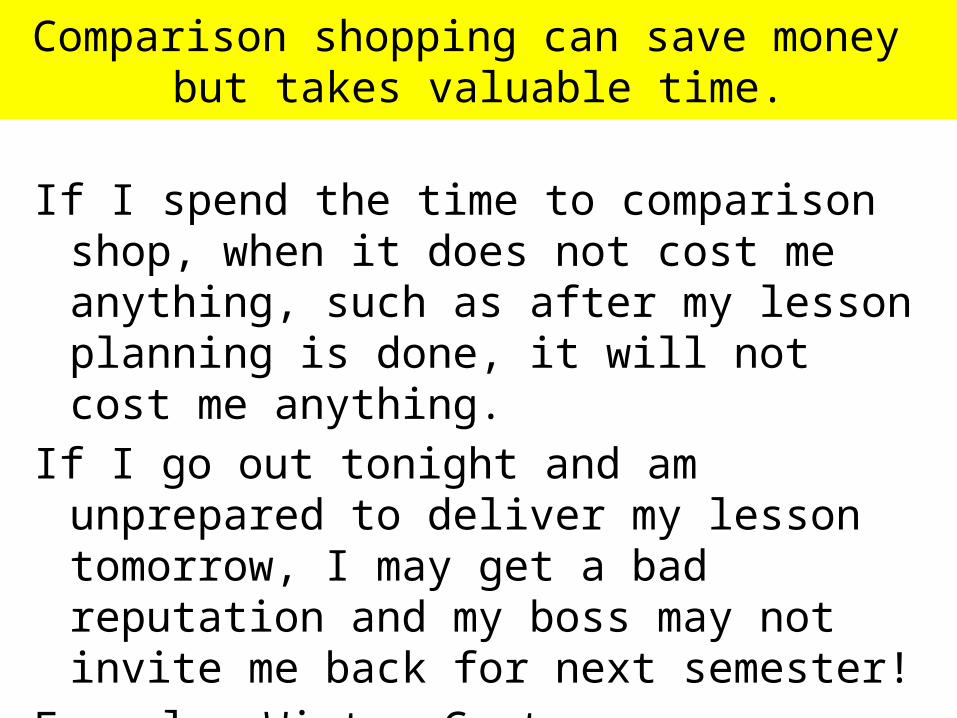

Comparison shopping can save money but takes valuable time.

If I spend the time to comparison shop, when it does not cost me anything, such as after my lesson planning is done, it will not cost me anything.

If I go out tonight and am unprepared to deliver my lesson tomorrow, I may get a bad reputation and my boss may not invite me back for next semester!

Example: Winter Coat.

Major Money Management Activities

Creating and implementing

a plan forspending, and saving (budgeting).

Creatingpersonalfinancial

statements(balance

sheets andcash flow

statements of income

and outflow).

3-4

Storingand

maintainingpersonalfinancialrecords

anddocuments.

Benefits of an Organized System of Financial Records

• Handling daily business affairs, including payment of bills on time.

• Planning and measuring financial progress.• Reporting and paying your taxes on time.• Making effective investment decisions. Evaluating

the risks of different investments. EMOTIONAL.• Determining available resources for current and

future buying. TIMING.

What to Keep in Your Home FileItems you refer to often.Personal and employment records (employment contracts, annual

letter of performance evaluation and increases in salary)Money management records. Tax records.Financial services records (bank statements, credit card

statements, loan statements, etc).Consumer purchases (ownership papers for auto) Warranty

records for cars – (example of Smart Car repairs) , tools, appliances, etc)

Housing records (mortgage contract or rental agreement, home maintenance improvements – roof, foundations repairs, siding, windows, furnace, central air conditioning).

What to Keep in Your Home File (cont’d)

Insurance records: home – know the different types – contents, replacement vs.

depreciated value, owner vs. renter, riders for luxury items such as jewelry; car; motorcycle; boat; life; disability; travel health, stay at home health, etc.

Investment records:mutual funds; stocks; bonds (private or government), etc.

Estate planning and retirement records:Will and Last Testament; retirement plans through employers,

etc.

What to Keep in a Safety Deposit Box

Safety deposit box is for records that would be hard to replace. The reference to a Safety Deposit Boxes usually means a small box in a bank vault.

Some people have fire proof safe’s at home, bolted to the concrete floor of their basement.

Birth, marriage and death certificates, copy of Last Will and TestamentCitizenship and military papers.Adoption and custody papers.Serial numbers and photos of valuables.Credit and banking account numbers.Mortgage papers and titles.List of insurance policy numbers.Stock and bond certificates.Coins and other collectibles.

Records on Personal ComputerHome computer (password protected).

Current and past budgets.Summary of checks written and other banking

transactions.Past income tax returns prepared with tax preparation

software.Account summaries and performance results of

investments.Computerized versions of wills, estate plans, and other

documents.

How Long to Keep RecordsNever dispose of these records:

Birth certificates; wills; and Social Security information; documents related to the purchase and sale of real estate.

Records of personal items and investments as long as you own them.

Tax returns and supporting data should be kept seven years.

Purpose of Personal Financial Statements

To report your current financial position in relation to the value of the items you own and the amounts you owe.

To provide data you can use when a) preparing tax formsb) applying for credit to borrow (this information is

necessary for the lender to make a decision).

To allow you to measure your progress toward your financial goals. To know your current position of strength or weakness.

Components of a Balance Sheet(net worth statement)

Assets - what you own.– Liquid assets (chequing / savings account)– Real estate (can take time to cash in or borrow against)– Personal possessions (might have to be sold at a

considerable discount)– Investment assets (taxes on the profit must be paid

when cashed)Liabilities - what you owe

– Current liabilities (< 1 year) (loans, credit cards) – Long term liabilities (house, rental property)

Compute your net worth.– Assets minus liabilities.

In-class ExerciseShow slides of asset and liabilities mixed up.Sort the assets into one column and liabilities into

another column. Calculate: Assets – Liabilities = Net Worth

Go to next slideTake 2 minutes to complete the exercise

Net Worth will be a test question

Calculate the Net WorthHouse if sold today = 400,000 RMBCar = 50,000 RMBMotorcycle = 35,000 RMBAntiques = 200,000 RMBMortgage on house = 275,000 RMBCar Loan = 12,000 RMBRetirement investments = 400,000 RMBTools = 50,000 RMBJewelry = 30,000 RMB

AssetsHouse 400,000Car 50,000Motorcycle 35,000Antiques 200,000Retirement Investments 400,000Tools 50,000Jewelry 30,000ASSETS = 1,165,000

LiabilitiesMortgage 275,000Line of Credit 15,000Car Loan 12,000Credit Cards 8,000Utilities(gas, electricity) 4,000Student Loans 40,000Liabilities = 354000

Net Worth = Assets – Liabilities= 1,165,000 – 354,000= 811,000

Two Exercises

1. Create your own Net Worth Statement. Go into great detail. Include as much as possible.

2. Create a fictional Net worth statement for a family of 3. The husband and wife are both 35 years old and have one child who is 6 years old. Use your imagination.

Consider this a head start on your first financial plan which is due Friday October 28th

Three tips to improve your Financial Plan

1. Create a Net worth statement for Financial Plan Project. Use the family composition as required for Plan 1 and Plan 2. Net Worth = Assets – Liabilities

2. Demonstrate Future Value of secure investment(s) in another section of your Financial Plan by showing the formula and the calculations.

3. Consider showing the cost of a car, the loan amounts, repayment schedule and depreciated value of the car.

Go to Lesson 9