Embed Size (px)

Citation preview

LENDER’S PERSPECTIVE ON FINANCING A GROUND LEASE

DIANA R. PALECEK

Smith Moore Leatherwood LLP 101 North Tryon Street, Suite 1300

Charlotte, NC 28246 704.384.2609

This manuscript was presented in connection with a panel discussion titled “Ground Leases” as a part of a Continuing Legal Education Program sponsored by the North Carolina Bar Association in 2009. This manuscript has not been updated since it was first written.

Lender’s Perspective on Financing a Ground Lease

By: Diana R. Palecek Smith Moore Leatherwood LLP Charlotte, NC I. Introduction1 Though no rigid standards or definitions exist to distinguish a ground lease from a space lease, typically a ground lease is a lease of an entire tract of land that confers on the tenant control over the land that is functionally the equivalent of ownership for a long period of time. In addition to other indicia of ownership, the ground lease tenant usually has the right to develop the land and sublease it to third parties. By contrast, under a traditional space lease, the landlord retains more control over the land, and the tenant leases only a portion of the land or space within a building for a relatively short period of time. Though risks to the landlord and tenant are inherent with any ground lease, a properly drafted ground lease can be advantageous to both the landlord and the tenant. Benefits to the landlord might include (a) avoidance of capital gains which would be taxed upon the sale of the property, (b) potential increase in the value of the reversionary interest in the land by the improvement made to the land, without the cost of development and construction, (c) an income stream, much like an annuity, without the burdens of ownership of the land, (d) retention of ownership of land that is likely to appreciate in value, such as oceanfront property, (e) retention of ownership of land that the landlord has a sentimental attachment to and/or a desire to pass to heirs, or (f) an income stream from the land for a landowner lacking legal capacity to transfer the property, such as a trustee of a trust prohibited from transferring the land under the terms of a trust. Benefits to the tenant might include lower cost of development of the land by avoiding purchase expenses, rent deduction from income, and depreciation of the improvements from income. (For this reason, some ground leases provide that during the term of the lease any improvements on the land are the property of the tenant, allowing the tenant to depreciate the cost of the improvements. Upon termination of the lease, ownership of the improvements reverts to the landlord.) The fundamental differences between a ground lease and a space lease dictate that the lease drafter not simply take a space lease form in toto without carefully considering changing certain provisions. The primary issues that often underlie negotiation of ground leases are as follows: (a) the tenant’s intention to construct improvements on the land, (b) the tenant’s lender’s need to be able to prevent the forfeiture of the leasehold estate, (c) the landlord’s need for receipt of uninterrupted rent and preservation of its fee estate, and (d) whether the landlord will “subordinate” its fee interest in the land to the tenant’s lender. The term “subordinate” is a misnomer: it means the landlord will subject the fee estate to the lien of the tenant's lender’s mortgage2. Conversely, "unsubordinated fee" means the landlord will not subject the fee estate to the lien of the tenant's lender's mortgage. Though misnomers, the terms “subordinated leasehold financing” and “unsubordinated leasehold financing” will be used throughout this manuscript because they are the commonly used terms. The landlord and tenant should pay close attention to all terms of the lease, not only to ensure that the landlord's and tenant's rights and obligations are clearly described but also to set out the tenant’s lender's rights and obligations. In the arena of

1This manuscript is updated from the manuscript published in the N.C. Bar Association, Commercial Real Property Update CLE Program (2001). The writer expresses her appreciation to Ken Moser, Esq. for his guidance in the preparation of the original manuscript and her appreciation to Jordan Nance, Esq. for his able assistance in updating the manuscript for this program. 2 The term “mortgage” is used throughout this manuscript to mean any security instrument securing an estate in land as collateral for a debt such as a mortgage, deed of trust or security deed.

IIC-1

ground lease financing there are few clearly established guidelines, and each lender will have its own internal requirements on what it deems acceptable. The way the lender views the lease may depend much on the degree of reliance the lender is placing on the collateral for repayment of the loan versus the financial strength of the borrower and any guarantors independent of the success of the financed project. If possible, the lender should participate in the lease negotiations. Since leases are often executed prior to the tenant seeking financing, joinder of the lender in negotiations is not always possible. The tenant may want to negotiate a clause in the ground lease whereby the landlord agrees to modify the lease if the tenant’s lender requests reasonable, non-economic changes to the lease. See Form 1 for a lease clause requiring certain future amendments to the ground lease. While a ground lease might be utilized for many different reasons, a common context under which a lender is presented with ground leased land as collateral arises in the context of a borrower/tenant who plans to develop the land for subleasing. This manuscript will focus on the financing issues that arise in this context and when the leasehold lender is relying upon the leasehold estate and subleases derived from it for payment of the loan. II. Unsubordinated Leasehold Financing Unsubordinated leasehold financing describes a loan structure in which a loan is made to a ground lease tenant that is secured by a mortgage on only the leasehold estate. The leasehold estate is volatile and risky collateral for the lender because it is subject to disappearing should the lease be terminated, and because the terms of the lease must be marketable to potential buyers at or after foreclosure. The discussion below will address key lease terms and issues from the leasehold lender’s perspective and will cover the concerns that leasehold lender’s are likely to have when considering extending financing secured by an unsubordinated leasehold estate. The leasehold lender will probably analyze the lease on two levels to determine if it is mortgageable. The first level is whether the lease adequately protects the interests of the tenant and future tenants (and thus the leasehold lender if it acquires the leasehold estate and steps into the shoes of the tenant). The second level is whether the lease protects the interest of the lender and future lenders (who might provide refinancing of the leasehold lender’s loan). To be mortgageable, the lease should not be terminated for any reason outside the leasehold lender’s knowledge and control, and the lease should be assignable by the tenant and the leasehold lender. See Form 2 for a leasehold lender’s lease review checklist. See Form 3 for a leasehold lender’s mortgage review checklist.

A. Value of Leasehold Estate In most cases when real estate is taken as collateral for a loan, financial institutions subject to federal oversight are required to obtain property appraisals or evaluations prepared in conformance with certain standards and by qualified persons. The Office of the Comptroller of the Currency (hereinafter “OCC”) publishes its rules for national banks under Real Estate Lending Standards, 12 C.F.R. Pt. 34, Subpt. D, App. A (2008). The OCC requires national banks to establish comprehensive policies consistent with safe and sound lending practices, including requiring certain specified loan-to-value ratios. Insurance companies are regulated by the state in which the company is domiciled. Most states, including North Carolina, prescribe some statutory parameters for the types of loans, including structure and collateral, that insurance companies are allowed to make. The leasehold lender, whether a national bank, state bank or insurance company, will most likely engage the services of a qualified appraiser to determine the value of the leasehold estate. Volumes have been written on the art of appraising property, and there are many approaches and factors the appraiser considers. Very simply and usually, when an appraiser determines the value of a leasehold estate, the appraiser first determines the fair market value of the fee

IIC-2

estate unencumbered by the lease, then calculates the present worth of the rent payments required by the lease, and then subtracts the present worth of the rent payments from the fair market value of the fee simple estate. Pertinent to the appraisal are the tenant’s costs of the improvements, the tenant’s expected net income from the sub-rents, the term of the lease, the amount of the tenant’s rental payments, and the useful life expectancy of the improvements on the property. The appraiser should be given a copy of the lease, rather than a summary of the financial terms of the lease, so the appraiser can analyze all terms of the lease that might impact its marketability. The appraiser’s review of the lease is, in this respect, similar to the leasehold lender’s review of the lease. The more favorable the lease is to the tenant, the higher the value of the lease will be.

1. Term of Lease

The lease term must at a minimum be long enough to meet any statutory minimum lease terms imposed on the leasehold lender. The tenant should consider all types of lenders from which the tenant may seek financing when negotiating the lease term. At one time, Federal law prohibited national banks from securing loans with leasehold estates that expired less than ten (10) years after the loan maturity. This bright-line requirement was removed with the passage of the Garn-St Germain Depositing Institution Act of 1982, Pub. L. 97-320, Section 403 which amended 12 U.S.C. § 371 by removing certain statutory restrictions on real estate lending by national banks and authorizing the OCC to adopt standards for real estate lending. The comments received by the OCC when it was promulgating regulations addressed whether a specific rule should be adopted to require minimum lease terms, and a minimum lease term requirement was rejected in lieu of the requirement that national banks adopt safe and sound lending practices. See Real Estate Lending by National Banks, 48 Fed. Reg. 40,698 (1983). Various states impose minimum lease terms on certain lenders. In North Carolina, N.C. Gen. Stat. § 58-7-179(a) prohibits insurance companies domiciled in North Carolina from securing a loan with a leasehold estate unless the lease has a term of at least thirty years, inclusive of enforceable renewal options, and the loan matures at least twenty years prior to the expiration of the lease. North Carolina practitioners representing tenants may also need to be aware of other states’ laws (particularly those states in which the major insurance companies are domiciled) so that the tenant’s financing options can include out-of-state lenders. For example, under N.Y. Ins. Law § 1404(a)(4) (McKinney 2008), New York permits insurance companies to make loans on leasehold estates if the unexpired term of the lease is not less than twenty-one years from the maturity date of the loan and principal payments are structured so the principal is repaid within the lesser of forty years or a period equal to eighty percent of the unexpired term of the lease. Under Mass. Gen. L. 175 § 63(7) (2008), Massachusetts permits insurance companies to make loans on leasehold estates if the unexpired lease term is twenty-one years. Even if the leasehold lender is not subject to statutory proscriptions concerning the length of the lease term relative to the loan term, the leasehold lender should require the lease term to be sufficiently long enough to cover the amortization schedule of the loan. The leasehold lender may also require additional time beyond the amortization of the loan to allow for the possibility of lapses in the payment of the debt and to foreclose and dispose of the leasehold estate to a buyer willing to pay the balance of the debt. One rule of thumb is for the lease term to be long enough to permit the debt to be fully amortized from the cash flow of the property in less than eighty percent of the remaining lease term. Some lenders may have internal policy requirements for minimum lease terms beyond the loan amortization term. The policy requirements may coincide with statutory limits placed on insurance companies on the basis that permanent financing from an insurance company should be available to take out the leasehold lender’s loan. If the lease contains renewal terms, the renewal terms may be counted for the purpose of determining the length of the term if the exercise of the renewal terms is not conditional and the leasehold lender is given the right, in addition to the tenant, to exercise the renewal term. As added protection, the leasehold lender may require that the renewal options actually be exercised at the time the loan is closed.

IIC-3

2. Rental Payments The rental payments under a ground lease are usually net to the landlord, with the tenant being responsible for the usual expenses of property ownership, such as property taxes and assessments, utilities, repairs and insurance premiums. Leasehold lenders prefer the rent under a ground lease be a fixed amount. Rent based on a percentage of sales is often not acceptable to a leasehold lender because percentage rents are uncertain, making it impossible for the leasehold lender and appraiser to determine the value of the leasehold estate. A problem with a fixed rental rate (including fixed escalations of rent) over a long period of time is that this type of rent structure does not address the increases (or decreases) in the rental value of the land. Therefore, the landlord may wish to negotiate a mechanism for increasing the rental payment over time. The landlord, tenant and leasehold lender have competing interests in whether there are to be rental increases, and if so, how the increase is to be determined: the landlord wishes to maximize its income off the property; the tenant wishes to minimize its rent cost and avoid increases that are not related to changes in the rental value of the property; and the leasehold lender, while sharing the tenant's concerns, also needs the rent to be a definite amount in order to appraise the value of the leasehold estate. Escalations based on the Consumer Price Index (hereinafter “CPI”) are not generally acceptable to leasehold lenders because the amount of the increase is not ascertainable at closing and because the CPI is not usually an accurate measure of market rents, particularly over the term of a long-term lease. Escalations based solely on percentage rents based on income generated by the property are also generally not favored by leasehold lenders. In this regard, the leasehold lender’s concerns are (a) the potential difficulty of assigning the lease to a new tenant who may want to dramatically change the use to one that is not conducive to percentage rents (for example a change from a retail store to a bank branch), (b) the possibility that the percentage rent clause constitutes an implied obligation to operate the property or use the property for a particular purpose, (c) disagreement over the exclusion or inclusion of certain items from the calculation of the percentage rent, and (d) the exclusion from rent of operating costs so that increases in costs are taken into account. Increases in rent that are based upon objectively ascertainable criteria may be acceptable to leasehold lenders. For example, a fixed base rent with periodic step up provisions for additional rent based on net income of the tenant in excess of a minimum net income may address the tenant's concern that increases be tied to the cash flow of the property and costs of operation and, at the same time, may be acceptable to a leasehold lender. Another possible formula for increases in rent is a fixed base rent with periodic step up provisions for additional rent based on a percentage of the increased appraised value of the land or fair rental value of the land (excluding the improvements) based on the tenant’s actual use of the property rather than the highest and best use.3

B. Termination of the Leasehold Estate

Leases can terminate because of tenant default, condemnation, surrender or rejection of the lease in the bankruptcy of either the landlord or tenant, or voluntary agreement between the landlord and tenant. The leasehold lender will want to analyze the lease for provisions that allow for the termination of the lease. This analysis is of central importance to the leasehold lender because the leasehold lender's collateral disappears upon the termination of the lease. Unfortunately for leasehold lenders, the lease usually can be terminated more quickly than the leasehold lender can foreclose.

3 The interest of the landlord for rental increases, of course, conflicts with the leasehold lenders’ desire for an ascertainable rental. Once way to address these conflicting interests, while probably difficult to negotiate, might be to subordinate rental increases to the leasehold lender’s mortgage.

IIC-4

1. Tenant's Default The lease should specifically set out the obligations of the tenant and what, if any, notice the landlord must provide the tenant prior to terminating the lease. Tenant defaults can be divided into three types of defaults: monetary default, non-monetary default curable by the leasehold lender and non-monetary default not curable by the leasehold lender. The lease should require the landlord to give both the tenant and the leasehold lender notice of the tenant’s default and give the leasehold lender a right to cure or otherwise address the tenant’s defaults, including specifically stating that the landlord will accept the leasehold lender’s performance as if the cure were undertaken by the tenant. The length of time to cure lease defaults should give the tenant sufficient time to cure any default. The leasehold lender may prefer that the lender’s time for curing defaults be longer than the tenant’s cure period and that the leasehold lender’s cure period not run concurrently with the tenant’s cure period so that the leasehold lender does not find itself in the middle of disputes between the tenant and landlord regarding any defaults. From the landlord’s perspective, providing the leasehold lender with time to address the tenant's defaults, while delaying the landlord's ability to exercise its own remedies, should nevertheless increase the likelihood that the landlord will be made whole because the leasehold lender has a strong incentive to cure or otherwise address the defaults to prevent termination of the lease. The leasehold mortgage should obligate the tenant to perform its obligations under the lease and to immediately provide the leasehold lender with copies of any notices of default the tenant receives from the landlord. If the tenant fails to perform its obligations under the lease, the leasehold mortgage should confer on the leasehold lender the right to cure the tenant's defaults under the lease and allow the leasehold lender to charge any sums to the tenant and to secure such sums by the mortgage. The leasehold lender's cure of the tenant's lease default should not operate to cure the ensuing default that occurred under the mortgage. The converse is not recommended, however. The lease should not contain a provision stating that a default in a leasehold mortgage constitutes a default in the lease. Otherwise, the leasehold lender could find itself in the unenviable position of having to waive defaults in its loan in order to preserve the lease from termination. See Form 4 for a leasehold mortgage provision concerning lease defaults. See Form 5 for a lease provision concerning the leasehold lender’s right to cure defaults.

a. Monetary Default The tenant’s failure to make rental payments on time can be cured by the leasehold lender easily and in relatively short time. Therefore, the leasehold lender is generally given a relatively short period of time to cure monetary defaults.

b. Curable Non-monetary Default

The tenant’s failure to maintain certain covenants, such as maintaining the property in good condition or restoring the property following a hazard loss, are capable of being cured by the leasehold lender. In order to cure such a default, the leasehold lender may have to gain possession of the property through the appointment of a receiver and/or foreclosure. Therefore, the leasehold lender should have adequate time to address curable non-monetary defaults, and the landlord should agree not to terminate the lease if the leasehold lender is diligently pursing a cure of the default and is making monetary payments that might be due during the prescribed cure period.

IIC-5

c. Uncurable Non-monetary Default Certain defaults of the tenant are not capable of being cured by the leasehold lender, such as the tenant failing to maintain a financial condition satisfactory to the landlord.4 Other examples of defaults not capable of being cured by the leasehold lender are failure of the tenant to deliver financial reports or failure to comply with a personal covenant, such as a requirement that a specific person maintain a controlling ownership interest in the tenant. Such events should either not be events of default in the lease, or if events of default, the landlord should agree not to terminate the lease so long as the leasehold lender is diligently proceeding to foreclose and all monetary obligations of the tenant under the lease are kept current. See Form 6 for a lease provision exculpating the leasehold lender from curing uncurable tenant defaults.

2. Voluntary Termination by Tenant

The lease must not be voluntarily terminated by the landlord or the tenant during any period in which a leasehold mortgage exists. The leasehold mortgage should prohibit the tenant from terminating the lease without the leasehold lender’s consent. Likewise, the lease should contain a similar clause binding the landlord not to accept a termination from the tenant as long as a leasehold mortgage exists.

3. Bankruptcy

The commencement of a bankruptcy action, either voluntary or involuntary, by either the landlord or the tenant can have profound implications for the leasehold lender. The leasehold mortgage should require the tenant to give the leasehold lender immediate notice upon the commencement of its own bankruptcy or the bankruptcy of the landlord. Two sections of the United States Bankruptcy Code, 11 U.S.C. §101 et. seq. (hereinafter “Bankruptcy Code”) of particular importance to leasehold lenders are the automatic stay section and the section dealing with rejection/assumption of a lease. Immediately upon the commencement of a bankruptcy action, an automatic stay takes effect pursuant to Section 362 of the Bankruptcy Code. The stay prohibits enforcement of the lease obligations against the debtor-in-bankruptcy. If the debtor-in-bankruptcy is the tenant, then the landlord cannot pursue eviction, and the leasehold lender cannot pursue foreclosure of its mortgage. The debtor-in-bankruptcy, whether the landlord or the tenant, has the right under Section 365 of the Bankruptcy Code to accept or reject executory contracts and any unexpired lease. Section 365 of the Bankruptcy Code sets out certain restrictions on the debtor-in-bankruptcy’s ability to reject unexpired leases and the rights of other parties to the unexpired leases. There are two contexts relevant to this manuscript in which rejection of a lease can occur: (1) the debtor-in-bankruptcy is the tenant who has granted a leasehold mortgage, and (2) the debtor-in-bankruptcy is the landlord and the tenant has granted a leasehold mortgage.

4 While the financial condition of a tenant of a space lease is of paramount importance, it generally is not as important to the ground landlord of income producing property. In such a case, the ability of the property to produce income is of greater importance than the ground tenant’s financial condition.

IIC-6

a. Bankruptcy of Tenant Section 365(a) protects tenants and leasehold lenders by making options to terminate most leases by the landlord upon the tenant’s bankruptcy unenforceable. Section 365(b) permits the tenant/debtor-in-bankruptcy to assume or reject the lease for the bankruptcy estate. If the tenant/debtor-in-bankruptcy assumes the lease, any defaults under the lease must be cured and “adequate assurance of future performance” must be provided to the landlord. For properties not used as shopping centers, no definition of “adequate assurance” is provided in the Bankruptcy Code. For “shopping centers”5 the tenant/debtor-in-bankruptcy must give assurances (a) of the source of rent, (b) that the percentage rent “will not decline substantially”, (c) that the assumption is subject to all provisions of the lease, including use, radius, and exclusivity provisions, and (d) that the assumption will not disrupt the tenant mix in the shopping center. For any lease, shopping center or otherwise, assumed by the tenant/debtor-in-bankruptcy, the tenant/debtor-in-bankruptcy may assign the lease pursuant to Section 365(f) upon providing additional assurances that the financial condition and operating performances of the assignee are similar to that of the tenant/debtor-in-bankruptcy at the time the lease was originally effective. If the tenant/debtor-in-bankruptcy rejects the lease or the lease is deemed rejected by the lapse of time6, then the landlord has an unsecured claim against the tenant/debtor-in-bankruptcy that is limited to an amount equal to the greater of rent for one year or fifteen percent (not in excess of three years) of the remaining lease term.7 If the lease is rejected, then the lease may be deemed terminated by the bankruptcy court8, resulting in the termination of the leasehold mortgage. One method of addressing the problem of the termination of the lease from the leasehold lender’s perspective is to have a clause in the lease and/or in a separate agreement between the landlord and leasehold lender requiring the landlord to enter into a new lease (also called a “pick-up lease” or a “come back” lease) with the leasehold lender on the same terms as the old lease (excluding any provisions of the old lease that have been satisfied, such as any construction obligations, and any personal obligations of the tenant). New lease clauses, however, are not fail-safe. See Section II.B.6. below for a discussion of new lease clauses.

b. Bankruptcy of Landlord

If the landlord is the debtor-in-bankruptcy, it too has the right, under Section 365(h) of the Bankruptcy Code, to accept or reject the unexpired term of the lease. If the landlord/debtor-in-bankruptcy rejects the lease, the tenant

5 The Bankruptcy Code does not define “shopping center”, but one case has held that a group of three buildings on Main Street with a single owner may be considered a shopping center. In re Joshua Slocum, Ltd., 922 F.2d 1081 (3d Cir. 1990). 6 Of note here, is that under Section 356(d)(4) a lease of non-residential property (not defined in the Bankruptcy Code) is deemed to have been rejected if it is not assumed or rejected within one hundred twenty (120) days after the order for relief unless the court extends such time for one additional ninety (90) days. 7 This limitation is found in Section 502(b)(6). There is no similar limitation on the liability owed to the tenant in the landlord’s bankruptcy. 8 There is a line of cases holding that the tenant/debtor-in-bankruptcy’s rejection of the lease does not result in the termination of the leasehold estate, but results in merely a breach of the lease. Under such a view, the leasehold lender ‘s rights under the lease (including, the right to cure tenant defaults and the right to enter into a new lease with the landlord) survive. See In re Austin Development Co., 19 F.3d 1078 (5th Cir. 1994), cert. denied, 513 U.S. 874 (1994), In re Locke, 180 B.R. 245 (Bankr. C.D. Cal. 1995) and Mclaughlin v. Walnut Properties, Inc., 14 Cal. Rptr. 3d 369, 119 Cal. App. 4th 293 (Cal. Ct. App. 2004). There is, however, another line of cases holding the opposite view: that rejection of the lease results in the termination of the lease and thus any leasehold mortgage. See Commercial Fin., Ltd. v. Hawaii Dimensions, Inc. (In re Hawaii Dimensions, Inc.), 39 B.R. 606 (Bankr. D. Haw. 1984), aff’d 47 B.R. 425 (D. Haw. 1985). The second line of cases is more consistent with general principles of real estate law, and is therefore, in this writer’s opinion the more logical line of reasoning. For further discussion of this issue, see Stein, Guide to Ground Leases, § 3.2 (2005).

IIC-7

has the right either to accept the rejection (thus terminating the lease) and file a claim against the landlord/debtor-in-bankruptcy’s estate, or to continue in possession of the lease. Section 365(h) of the Bankruptcy Code allows the tenant to accept the landlord/debtor-in-bankruptcy’s rejection of the lease and thus terminate the lease if such termination of the lease is allowed under the leasehold mortgage. The leasehold mortgage, therefore, should include a clause prohibiting the tenant from accepting the landlord’s rejection of the lease without the leasehold lender’s consent and giving the leasehold lender the right to exercise on behalf of the tenant the tenant’s option to elect to remain in possession or to accept the rejection of the lease. Even if the tenant does not accept the landlord/debtor-in-bankruptcy’s rejection of the lease, the Bankruptcy Code provides that the landlord/debtor-in-bankruptcy is released from its obligations under the lease. The tenant may, however, under the Bankruptcy Code set-off against rents for post-petition defaults of the landlord. A wrongful set-off by the tenant will likely be a default in the lease allowing the landlord/debtor-in-bankruptcy to terminate the lease at that time. In order to protect itself against this type of termination, the leasehold lender’s mortgage may require the leasehold lender’s consent prior to the tenant exercising its right of set-off. In addition to the landlord/debtor-in-bankruptcy’s rights under Section 365(h) of the Bankruptcy Code, practitioners representing leasehold lenders should also be familiar with the potential rights of a landlord/debtor in bankruptcy under Section 363(f) of the Bankruptcy Code. Section 363(f) permits a debtor to sell property “free and clear” of any interest in such property if any one of the following five tests are satisfied: (1) applicable non-bankruptcy law (i.e, state law) permits the sale of such property free and clear of such interest; (2) the entity possessing the interest consents; (3) the interest is a lien and the property is being sold for a price in excess of all liens on the property; (4) such interest is in bona-fide dispute; or (5) the entity holding the interest could be compelled in a legal or equitable proceeding to accept a money satisfaction of such interest. The Seventh Circuit’s opinion in the case of Precision Industries v. Qualitech9 aroused a substantial outcry among many commentators who view this case as opening the door for a landlord in bankruptcy to sell a property encumbered by a leasehold mortgage to a third party “free and clear” of the leasehold mortgage. In Precision Industries, the landlord leased land to the tenant for 10 years for one dollar per year. The ground lease was not encumbered by a leasehold mortgage. Precision was to provide on-site warehouse supply services for the landlord’s steel mill operations. After tenant constructed a warehouse on the property, landlord filed for Chapter 11 bankruptcy protection.10 The landlord petitioned the bankruptcy court for authorization to sell the leased land, free and clear, of the ground lease pursuant to Section 363(f) of the Bankruptcy Code. The bankruptcy court authorized this sale by the landlord, and the Seventh Circuit ultimately upheld this decision. It should also be noted that the tenant only objected to the sale of the property after the sale had taken place and the landlord had changed the locks on the warehouse when tenant brought an action against the landlord for, among other claims, trespass and wrongful eviction based on an assertion that the tenant’s possessory interest in the leased premises survived the bankruptcy sale pursuant to Section 365(h) of the Bankruptcy Code.11 The question on appeal to the Seventh Circuit was basically whether or not a tenant’s rights under Section 365(h) to continue in possession after the landlord has rejected the lease preempt the rights of a landlord under Section 363(f) to sell a property free and clear of certain interests. In the wake of Precision Industries, there is a split among bankruptcy courts regarding the interplay between Section 363(f) and Section 365(h) of the Bankruptcy Code, and which section should determine when and how a debtor-landlord may terminate its interest in a lease.12 To date, there have not been any bankruptcy cases within the Fourth Circuit addressing a debtor-landlord’s rights under Section 363(f) of the Bankruptcy Code. However, given the possibility that a debtor-landlord may sell its property free and clear of a ground lease and any leasehold

9 327 F.3d 537 (7th Cir. 2003). 10 Id. at 540. 11 Id. at 541. 12 See In re MMH Automotive Group, LLC, 385 B.R. 347 (Bankr. S.D. Fla. 2008).

IIC-8

mortgage encumbering such ground lease if the debtor-landlord can meet one of the five tests set forth in Section 363(f) of the Bankruptcy Code, lender’s counsel should take a few fairly simple measures to minimize this possibility. One of the problems in Precision Industries was the silence of the tenant who failed to object to the sale conducted pursuant to Section 363(f) until well after the sale had occurred. According to one commentator, this silence amounted to consent in the Seventh Circuit’s view. See Stein, Guide to Ground Leases, (2005). Therefore, leasehold lenders should guard against the possibility of tenant silence in the face of a Section 363(f) sale by including provisions in the leasehold mortgage requiring a tenant to object to any proposed Section 363(f) sale and granting the leasehold lender the right to object to any proposed Section 363(f) sale on behalf of the tenant and for itself. So long as a tenant does not expressly consent or waive its rights by remaining silent in the face of a proposed Section 363(f) sale and the ground lease in question is an otherwise valid instrument under applicable state law, a bankruptcy court should be hard pressed to find grounds that the tenant’s leasehold interest in a property meets any one of the five applicable tests set forth in Section 363(f) of the Bankruptcy Code. See Form 7 for a leasehold mortgage provision relating to bankruptcy. See Form 8 for a leasehold mortgage provision relating to the tenant’s right to off-set rents after the landlord/debtor-in-bankruptcy’s rejection of the lease.

4. Merger of Fee Estate and Leasehold Estate

If the tenant acquires the fee estate, the leasehold estate might merge into the fee estate, causing the leasehold mortgage to terminate. In order for such a merger not to occur, there must be intent by the parties to the transaction for a merger not to occur. Because intent, whether express or implied, for merger is an element of the operation of the doctrine of merger, the leasehold lender should require that both the lease and the leasehold mortgage contain an anti-merger clause. See Form 7 for a leasehold mortgage anti-merger clause. See Form 9 for a lease anti-merger clause.

5. Priority of other liens

It is a basic tenet of North Carolina law that in order to establish the priority of a lease of more than three years against other liens or encumbrances against the fee estate, the lease or a memorandum of lease must be recorded.13 See N.C. Gen. Stat. § 47-18. It may be of interest to some practitioners that the recordation of a long-term lease in some states, such as Virginia, triggers recordation taxes based on the value of the leasehold estate, and is therefore an additional cost to be anticipated. See VA. Code Ann § 58.1-807 (2008). The North Carolina excise tax on conveyances is not charged on recorded leases. See N.C. Gen. Stat. § 105-228.29. The leasehold lender may, therefore, require that the lease (or a memorandum thereof) be recorded and may also require that the title to the fee estate be searched to determine that there are no unacceptable encumbrances against the fee estate that have priority over the leasehold estate. Priority is of particular importance when the leasehold estate is the collateral because the foreclosure of any prior lien could result in the termination of the lease. Therefore, if there should exist a fee mortgage against the property prior to the lease, the leasehold lender will probably insist that the fee mortgage be either satisfied or subordinated to the lease or that payment of the fee mortgage be otherwise assured. See section II.D.4. below for further discussion on this topic.

13 On a practical note, one commentator has suggested that for long-term ground leases, the entire lease should be recorded in order to ensure that its entire text could be found generations after it was initially executed. This practical suggestion should be balanced against any desire or need to maintain the confidentiality of the terms of the lease.

IIC-9

The leasehold lender will most likely require title insurance as it would for a mortgage on a fee estate. In 2001, the American Land Title Association (hereinafter “ALTA”) decommissioned the old Leasehold Lender’s Policy and instead began providing a Leasehold Form Endorsement and a Leasehold Loan Form Endorsement. These endorsements were also commissioned with the 2006 revisions to the ALTA forms and are endorsements 13-06 and 13.1-06, respectively. These endorsements provide coverage in the event that the tenant is deprived of loss of possession unless the tenant is dispossessed pursuant to the terms of the lease or in the event that a use permitted in the lease and the tenant is lawfully prevented from using the premises for such use. For both of these areas of coverage, the issue which causes the eviction or prevents the uses permitted by the lease must arise out of a matter covered by the standard ALTA Title Insurance Policy form. The coverage amount consists of two components, capped at the amount of coverage purchased: (a) the value of the remaining lease term, and (b) the value of any tenant leasehold improvements existing on the date of eviction. The method for valuing the remaining lease term and the tenant leasehold improvements is not prescribed in the endorsement. The leasehold endorsement forms also provide for additional items of cost to be covered by the policy, including the reasonable cost of removing and relocating personal property, rent or damages for use and occupancy of the land prior to the eviction which the insured may be obligated to pay to any person having paramount title to that of the landlord, etc.

6. New Lease Provision

Though the lease may contain satisfactory provisions designed to protect the leasehold lender against the premature termination of the lease, the leasehold lender may still require a “new lease” clause to be applicable to any termination of the lease, particularly if the lease contains default clauses not curable by the leasehold lender. Questions exist as to the effectiveness of new lease clauses, and, therefore, such a clause should not be a substitute for satisfactory lease terms aimed at preventing the termination of the lease. The new lease clause should be viewed only as a safety net. Since the termination of the lease has such dire consequences for the leasehold lender, such a safety net is not unreasonable. Concerns about new lease clauses include (a) whether the new lease would have priority over any intervening liens on the fee, (b) whether the new lease clause, which is itself an executory contract, may be rejected if the landlord is in bankruptcy, and (c) whether the new lease clause violates the rule against perpetuities since the option to enter into a new lease might not vest within the perpetuities period. In addition, there may be contractual issues as to the exercise of the new lease clause.14

C. Provisions Affecting Marketability of Leasehold Estate

The leasehold lender should analyze the lease to determine whether or not under its terms a third party should be willing to purchase the remainder of the lease and thus step into the shoes of the tenant. This is of importance to the leasehold lender because it does the leasehold lender no good to have a lease with a long enough term and protections against termination if at or after foreclosure it is impossible or unreasonably difficult to find a willing buyer for the remainder of the lease's term due to other unfavorable lease provisions. The leasehold lender’s

14 One court, strictly construing contractual language, finding in favor of the landlord held that a leasehold lender had failed to properly exercise its right to demand a new lease. The leasehold lender was given a copy of a termination notice giving the leasehold lender thirty days to obtain a new lease. Prior to the expiration of the thirty-day period, the tenant obtained a temporary injunction staying the termination of the lease pending a determination of whether a default existed. The leasehold lender waited until a determination was made prior to electing the new lease. On appeal, the court held that the leasehold lender was too late in exercising its option to enter into a new lease because the stay order obtained by the tenant did not restrain a third party lender’s contractual rights. See Berger-Tilles Leasing Corp. v. York Associates, Inc., 53 Misc. 2d 490, 279 N.Y.S. 2d 62 (Sup. Ct. 1967), rev’d, 28 A.D. 2d 1132, 284 N.Y.S. 2d 486 (2d Dept. 1967), aff’d, 22 N.Y. 2d 837, 293 N.Y.S. 2d 102 (Ct. App. N.Y. 1968).

IIC-10

review of the lease in this respect is to make sure the obligations and restraints placed on the tenant are reasonable and do not unduly restrict the potential future use of the property.

1. Construction Rights and/or Obligations Some ground leases require the tenant to construct improvements on the land and/or require the landlord’s approval of plans and specifications and other construction related items. From the leasehold lender’s perspective, such clauses should not unreasonably or subjectively restrict the tenant in the type of improvements, from rebuilding, making alterations, or changing the use of the property. If the lease requires the landlord's approval of construction related items, the leasehold lender should require evidence that all approvals have been obtained at the appropriate times during the progress of construction as conditions to the leasehold lender’s obligation to disburse funds.

2. Operating Covenants The leasehold lender should scrutinize any operating covenants in a ground lease to determine whether the operating covenants are reasonable and to determine whether the leasehold lender or any assignee can comply with such covenants. If there are covenants that are capable of being performed by only the initial tenant (such as a covenant that certain persons have controlling ownership interests in the tenant) or unreasonably limit the use of the property (such as requiring a specific franchise be operated) such covenants should not apply to any leasehold lender or to its assignees.

3. Use Limitations and Sign Clauses The leasehold lender is interested in the tenant being able to use (or sublet for use) the property for any lawful use to maximize the pool of potential subtenants or assignees and to be able to take advantage of changes in land uses over time. All future economically viable uses cannot be anticipated over the term of a long-term lease. For example, fast food restaurants, cell phone towers and drive through dry cleaners could not have been foreseen years ago. After a foreclosure, the leasehold lender would not want to be limited to selling or assigning the lease to those willing to try to make the site successful with a use that may have already failed. Unless the landlord owns the adjacent property that could be affected by an incongruent neighboring use or has some other compelling reason for limiting the use of the property, allowing the tenant unconditional lawful use of the property should not harm the landlord. To the extent the ground lease contains use limitations, the permitted uses should be defined as broadly, objectively and reasonably as possible. Changes in a use should not be conditioned on receipt of the landlord’s consent, even if the landlord’s consent is not to be unreasonably withheld. Such a limitation is tantamount to a restriction on assignments and is likely to be unacceptable to leasehold lenders. See section II.C.4. below. Similarly, though clauses allowing the landlord to approve signs placed on the property are common in space leases, such clauses are objectionable in ground leases if such clauses allow the landlord, in effect, to control the use of the property by controlling the signs.

4. Assignment and Subletting

The tenant should have the unconditional right to assign and sublet the lease subject only, if at all, to reasonable, objectively determinable conditions. It is the tenant’s ability to assign and/or sublet that allows it to recoup its investment in improving the property. The ability to assign the lease after foreclosure is also critical to the

IIC-11

leasehold lender for the lease to be meaningful collateral. Ideally, the lease should contain an affirmative provision granting the tenant an unconditional right to assign or sublet the leasehold estate. If the lease is silent on this point, courts have generally interpreted the silence as allowing the unconditional right of the tenant to assign and sublet the lease. The right to assign should not be conditioned upon the seemingly reasonable “consent of the landlord which shall not be unreasonably withheld, conditioned or delayed.” Such a condition introduces uncertainty into the right to assign the lease. The subjective word “unreasonable” allows for the possibility of disputes over the reasonableness of the proposed assignment. Such a condition is also not practical for the tenant or leasehold lender. Over the course of a long-term lease, the landlord could change and/or move and not be easily reachable. This is especially likely if the landlord is an individual who later dies leaving the fee estate to multiple heirs. In addition, it would be impossible for the leasehold lender to know and, in effect, pre-qualify with the landlord all potential known and unknown bidders at a foreclosure sale. The assignment clause should include a release of the leasehold lender and future assignors from compliance with the lease upon the recordation of an assignment. Without a specific release from liability, the tenant/assignor will remain liable to the landlord for the remainder of the lease term. If a release of the leasehold lender’s liability is not granted, then, it will likely be difficult for the tenant to obtaining financing for no leasehold lender will be willing to assume liability beyond the period of time it owned the leasehold estate.

D. Miscellaneous Lender Concerns

1. Ability to Encumber the Leasehold Estate

In order for the lease to be mortgageable, it cannot contain a prohibition on leasehold mortgages. Ideally, the lease should contain an affirmative provision granting the tenant the unconditional right to encumber the leasehold estate. If the lease is silent on this point, the silence has been interpreted as allowing the unconditional right of the tenant to mortgage the lease. A North Carolina court, citing American Jurisprudence, acknowledged that in the absence of a covenant to the contrary, the landlord and tenant each has the right to sell or mortgage the fee estate or leasehold estate, respectively. See Miller v. Lemon Tree Inn of Roanoke Rapids, Inc., 32 N.C. App. 524, 233 S.E.2d 69 (1977). If the lease prohibits or conditions encumbrances, then the leasehold mortgage may be deemed void unless the landlord consents to the leasehold mortgage in a separate agreement. The better practice is for the lease to specifically authorize the tenant to encumber the leasehold estate and provide that the leasehold lender may acquire the leasehold estate through foreclosure or an assignment-in-lieu of foreclosure and grant to the leasehold lender the right to assign the lease at or after foreclosure subject only, if at all, to reasonable, objectively determinable conditions.

2. Application of Insurance Proceeds The absence of a requirement in the lease for the tenant to maintain appropriate insurance will not render the lease unmortgageable; the leasehold lender will impose its own requirements on the tenant. An insurance clause in the lease not drafted to take into account the leasehold lender’s concerns, however, may render a lease unmortgageable. The application of insurance proceeds in the event of full or partial destruction of the improvements is an area of frequent negotiation between the landlord, tenant and leasehold lender. The lease should not contain a provision allowing the lease to be terminated in the event of a hazard loss unless the insurance proceeds are sufficient to pay a leasehold lender in full and such proceeds must in fact be applied to the payment in full of the loan. In addition the leasehold lender should be allowed to require that it be named as mortgagee and loss payee in order to protect its interest. Ideally the leasehold lender would prefer to have the sole discretion to determine whether insurance proceeds are used to pay down the debt or to rebuild the improvements. The landlord and tenant will likely find this position to be unacceptable. The leasehold lender’s primary concerns will be to ensure that there are adequate funds to undertake rebuilding, that there are controls

IIC-12

in place to ensure that the funds will be so applied, the quality of construction and that the tenant can and is legally required to continue to make loan payments during the period of rebuilding. A reasonable compromise is for the insurance proceeds to be payable to the leasehold lender and/or to a trustee for all parties and be used to rebuild the improvements, subject to reasonable rebuilding criteria. Such criteria may include a determination that the tenant has sufficient funds (from insurance and otherwise) to undertake the rebuilding, approval of the contract, approval of the plans and specifications, approval of the general contractor, and an ability to continue making ground rental payments if the rental payments are not abated. It is common for leases to allow the tenant to terminate the lease and pocket the insurance proceeds if a total or substantially total hazard loss occurs in the later years of the lease. Such a clause should be acceptable to the leasehold lender as long as the insurance proceeds exceed the unpaid balance of the loan and are applied first to the payment of the loan. If the lease requires the continuance of rental payments during any period in which the property is not usable due to a casualty loss, the leasehold lender should analyze whether the tenant has the financial wherewithal (either through insurance or separate funds) to continue making rental payments.

3. Allocation and Application of Condemnation Proceeds As with insurance proceeds, the allocation of and application of condemnation awards are the topic of frequent negotiation among the landlord, tenant and leasehold lender. The lease should provide that the leasehold lender and the tenant have the right to participate in the condemnation proceedings. The leasehold lender has a particular interest in making sure the tenant receives a fair allocation of any award. The manner in which to determine the value of the fee estate and the leasehold estate and improvements is the subject of much commentary. The method of valuing the estates should be addressed in the lease rather than being left to the determination of the condemning authority or court. The condemnation clause should be tailored to the use of the property and the length of the lease term. A couple of the most common approaches are set out below. Division of award: One approach (and perhaps the most common) is that the award should be divided as follows: the landlord should receive the value of the land as if it were unimproved and unencumbered by the lease, and the tenant should receive the value of the balance of the term of the leasehold estate and any improvements on the land. This approach has the benefit of being simple to follow with the values of the various estates being capable of determination on the date of the taking. However, this approach may result in a windfall to one party if there has been a substantial change in the value of the land from the time the lease was originally executed. Alternatively, if the landlord anticipates there to be a determinable value to the improvements at the time the lease ends, then the landlord may wish to adjust the above referenced formula so that the landlord also receives the present value of the reversionary interest in the improvements. The leasehold lender should not object to this if the value of the tenant’s interest is anticipated to equal or exceed the loan amount. Another approach is to provide a formula in the lease for a division of the award that takes into account the fact that the landlord has given up its interest in the land except for the rent payable until the expiration of the lease term and the absolute ownership of the reversionary estate with improvements. Such a formula for the landlord’s award is the capitalized value of the rent at the rate of interest equal to that which investments of comparable security earn at the time of the taking, plus or minus (as applicable) the discounted difference between the fair market value of the reversionary estate at the expiration date of the lease and the capitalized value of the rent. The tenant is entitled to the balance of the award. The downsides to this formula are its complexity, including determining the rate at which to capitalize the rent payments and the speculative nature of the fair market value of the reversionary estate. See Anderson, The Mortgagee Looks at the Ground Lease, 369 Practising L. Inst. Real Est. L. & Prac. Course Handbook Series 347, 360-370 (1991).

IIC-13

Whole or substantially whole taking: The lease should not terminate upon a condemnation until any existing leasehold lender is paid in full. The lease should specify that any leasehold lender has the right to share in the tenant’s award. In addition, the leasehold mortgage should provide for a lien on the tenant’s portion of the condemnation award. If the tenant or landlord has the right to terminate the lease upon a condemnation of the substantially whole leasehold estate, then "substantially whole" should be carefully defined in the lease. Partial taking: As with insurance proceeds, the leasehold lender would prefer that it have the discretion to determine whether the tenant’s portion of the condemnation award be applied to the loan or to the rebuilding of the property. Neither the landlord nor the tenant is likely to agree to giving the leasehold lender such discretion. The lease will likely require the tenant to restore the premises after a partial taking. If so, the award should be held and disbursed by the leasehold lender or a trustee for all parties in much the same manner as insurance proceeds. See section II.D.2. above. The balance of the award, if any, after restoration should be divided between the landlord and tenant according to one of the formulas set forth above, and rent should be abated on a pro rata basis to the portion of the property taken

4. Mortgage of the Fee Estate by the Landlord The leasehold lender’s preference is that mortgages against the fee estate be prohibited. Even if the fee mortgage is subordinate to the lease, there could arise conflicts in the covenants required in the fee mortgage, the lease and the leasehold mortgage such that it is impossible for the landlord to comply with the fee mortgage, causing the fee mortgage to be in default. For example, it is common for fee mortgages to require the fee owner to name the fee mortgagee as loss payee under insurance policies and allow the fee mortgagee to determine whether insurance proceeds shall be used to pay down the fee mortgage or rebuild the improvements following a loss. Such a provision would likely be in conflict with both the lease and the leasehold mortgage. If fee mortgages are allowed, the leasehold lender should insist that the fee mortgage (both its lien and its covenants and obligations) be subordinate to the lease. A mere non-disturbance agreement from the fee mortgage (without additional protective language) is not sufficient for several reasons. First, a non-disturbance agreement is normally effective only if the ground lease is not in default. For example, if the landlord’s source of income is the ground rentals and the ground tenant is in default causing the landlord to default under the fee mortgage, then the non-disturbance agreement, by its terms, would ordinarily be ineffective. Second, under a non-disturbance agreement the covenants and conditions of the fee mortgage are typically paramount to the lease. Thus, unless the non-disturbance agreement provides otherwise, to the extent such covenants and conditions conflict with the lease (such as application of insurance proceeds), then the leasehold lender friendly and tenant friendly provisions in the lease are rendered meaningless (with insurance proceeds being administered pursuant to the fee mortgage). Third, the non-disturbance agreement could be rejected as an executory contract under the Bankruptcy Code if the fee mortgagee were to become bankrupt.

5. Lender’s Right to Consent to Amendments to the Lease

The leasehold lender has an interest in amendments to the lease for obvious reasons. The leasehold lender’s pre-closing review of the lease could easily be rendered meaningless if the lease is amended after closing. The leasehold lender should be protected by agreements with both the landlord and the tenant against amendments to the lease made without the leasehold lender’s consent.

IIC-14

6. Limitation of Lender's Liability to Landlord The lease should provide that any leasehold lender is not liable for the obligations of the tenant under the lease unless and until the leasehold lender acquires the leasehold estate through foreclosure or assignment-in-lieu of foreclosure. Even when the leasehold lender assumes liability for the tenant’s obligations after foreclosure or an assignment-in-lieu of foreclosure, the leasehold lender's liability should cease at the time it assigns to another party and should be limited in amount to the value of the leasehold estate.

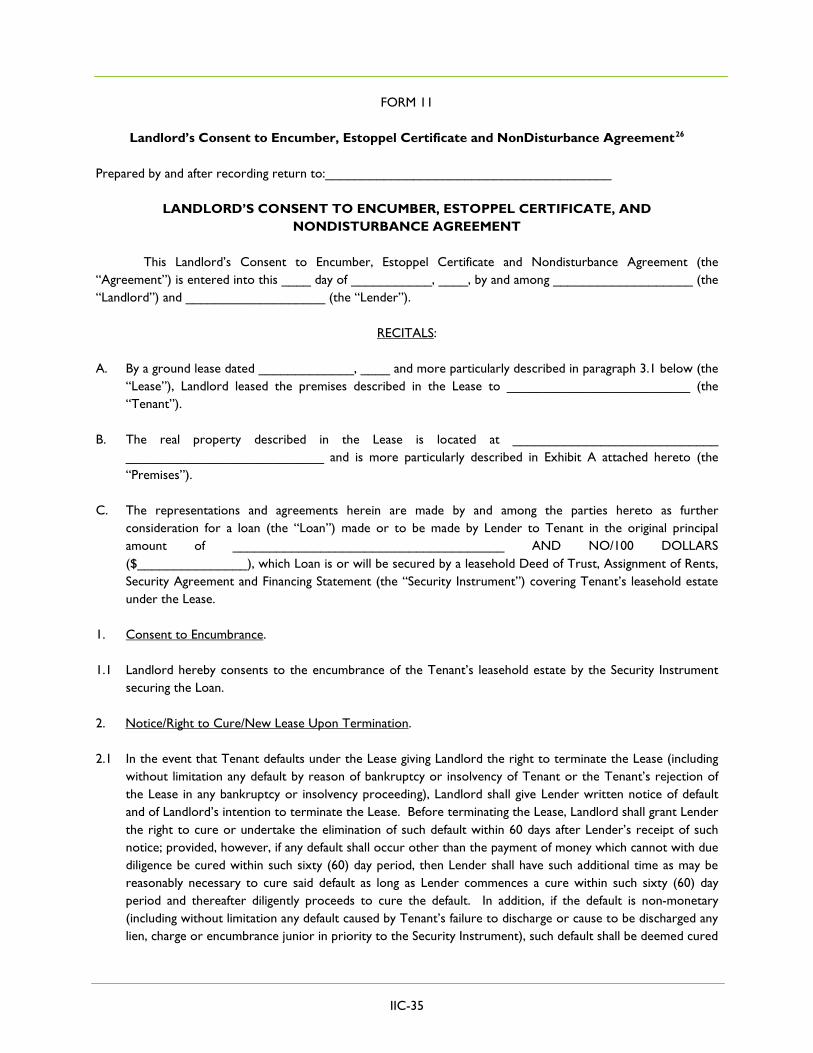

7. Estoppel Certificate and Non-Disturbance Agreement from Landlord Though the lease may contain many lender friendly terms, the leasehold lender may also seek a separate agreement with and estoppel certificate from the landlord which may be a repetition of the some key lease terms affecting the relationship between the landlord and leasehold lender. In addition, such an agreement can be a simple and efficient way to amend the lease for the benefit of the leasehold lender if the lease terms are not acceptable to the leasehold lender. The key provisions that may be in such an agreement are as follows: consent to encumber, notices of default and the right to cure, agreement to enter into a new lease, consent to assign and sublet the lease, and estoppel certifications from the landlord concerning factual matters such as a recitation of the lease documents, lease term, existence of defaults, the date to which rent has been paid, and acknowledge receipt of notice of the identity of the leasehold lender and the address of the leasehold lender for notice purposes. It is also recommended that the leasehold lender periodically request estoppel certificates from the landlord throughout the term of the loan. The lease should require the landlord to provide an estoppel certificate periodically within a reasonable time after it is requested. See Form 10 for a sample Landlord’s Consent to Encumber, Estoppel Certificate and Non-Disturbance Agreement. 8. Tenant’s Acquisition of the Fee Estate If the lease gives the tenant the option to purchase the land, the lease should allow the leasehold lender to exercise the option to purchase on behalf of the tenant. Likewise the mortgage should assign such option to the leasehold lender and give the leasehold lender the authority to exercise the option as attorney-in-fact for the tenant. In addition, the leasehold mortgage should include an after-acquired property clause (or "spreader" clause) and a legal description of the fee in order to secure the fee estate in the event it is acquired by the tenant. Such clauses would prevent the awkward and unacceptable possibility that the leasehold lender should foreclose the leasehold mortgage only to find the former tenant (its defaulted borrower) as its landlord because the tenant had acquired the fee title to the land. In addition to including a spreader clause and description of the fee in the leasehold mortgage, the leasehold lender would need to comply with the registration requirements of N.C. Gen. Stat 47-20.5 at the time the tenant acquired the fee estate in order to establish the mortgage’s priority as to the fee estate.

9. Rent Escrow The leasehold lender may consider requiring a rent escrow account for the payment of ground rents to ensure that the ground rents are timely paid. Leasehold lenders will likely vary on whether such an escrow is required based on the leasehold lender’s ability to cost effectively handle such an escrow account weighed against the leasehold lender’s comfort level with the financial strength of the tenant.

IIC-15

10. Tenant’s Representations and Warranties to the Lender The leasehold mortgage should contain representations and warranties from the tenant concerning the lease: that it is in full force and effect, that rents due to date have been paid, that there exists no defaults, and that the lease has not been modified or amended, except as had been disclosed to the leasehold lender. The leasehold mortgage should also require the tenant to perform its obligations under the lease. III. Subordinated Leasehold Financing Subordinate leasehold financing describes a loan structure in which a loan is made to a ground lease tenant secured by a mortgage on both the fee estate and the leasehold estate. This structure often arises when there is some common ownership between the landlord and tenant. It can, however, arise when there is no common ownership between the landlord and tenant. A landlord may agree to pledge its fee estate as an accommodation to the tenant in order to facilitate the tenant’s ability to obtain financing with a favorable interest rate or longer loan term or to obtain a larger loan.15 The proper way for the landlord to subordinate its fee estate is for the landlord to execute a mortgage on the fee estate. A lease clause appointing the tenant as the landlord’s attorney-in-fact for the purpose of executing a fee mortgage generally should not be relied upon by the lender. While such a clause would allow for the proper instrument to be executed at the time of the loan is obtained, an instrument executed in such a manner is subject to all of the defenses which may be asserted against an attorney-in-fact, including that the attorney-in-fact acted outside the scope of his or her authority or that the power of attorney is void due to a defect in its execution. Because the term "subordination" is used to describe the pledge of the fee for the tenant's loan, some mistakenly think that the manner of accomplishing the "subordination" is for the landlord to sign a subordination agreement or to include a self-operating subordination provision in the lease. Neither of these approaches should be acceptable to a lender.16 A self-executing subordination clause in the lease purporting to subordinate the fee estate to future leasehold mortgages should not be relied upon because, in addition to a subordination agreement not being the proper manner to pledge real estate as collateral, the agreement to subordinate may be invalid for lack of specificity. See MCB Ltd. v. McGowan, 86 N.C. App. 607, 359 S.E. 2d 50 (1987). The lease terms, though certainly important to the landlord and tenant, are of less importance to the lender when the fee estate is pledged as collateral for the tenant’s loan. The lender may still require that some or all of the lease provisions addressed above for unsubordinated leasehold financing be included in a ground lease in order to maximize the lender’s ability to assign the leasehold estate after foreclosure or an assignment-in-lieu of foreclosure to another party who may need to obtain financing on an unsubordinated basis.

A. Lender's Concerns

At first glance, one might think that the lender should have few concerns, other than the concerns associated with any other real estate secured loan, when the landlord mortgages the fee estate for the tenant’s loan. The lender should, however, review the lease to understand the business relationship between the landlord and the tenant

15 From the tenant’s perspective, it is recommended that the lease contain a clause requiring the landlord to mortgage the fee estate in favor of the tenant's lender. In exchange for the landlord’s significant risk in pledging its fee estate as an accommodation for the tenant, the landlord may demand a higher rent and/or collateral to secure its risk. 16 One court, interpreting the language of an estoppel certificate and subordination agreement, held that the subordination of the landlord’s interest in the lease to the mortgage thereon was not sufficient to grant a lien on the fee estate because the agreement contained no language granting a lien on the fee estate or subordinating the fee estate to the leasehold mortgage. See Balch v. Leader Federal Bank, 315 Ark. 444, 868 S.W.2d 47 (1993).

IIC-16

and to determine whether any lease provisions have an impact on the loan or mortgage. Since the landlord risks either losing its property upon the foreclosure of the fee mortgage or incurring the cost of curing the tenant’s loan defaults, the landlord may negotiate lease terms aimed at controlling the terms of the tenant’s loan, the use of the loan proceeds and the development of the property. The following sections address some of the lease provisions the landlord may negotiate for its protection and how such provisions may impinge upon the lender.

1. Limitations on Financing

The landlord may define and limit the type of financing for which it will pledge the fee estate as collateral to ensure that the proposed project and loan are economically viable. If the limitations are too restrictive the tenant may have difficulty finding a lender willing to make a loan with subordinated leasehold collateral. Common limitations are set forth below.

a. Identity of Lender

It is common for landlords to agree to subordinate only to financing provided by institutional lenders. The reasons are that institutional lenders presumably have the expertise to make a sound loan and, tempered by business judgment rather than emotion, may be more likely to attempt to workout a problem loan than to rush to foreclosure. Care should be taken that the definition of “lender” is broad enough to include all types of financial service providers, particularly as the financial services industry has experienced great changes in recent years. The following is a sample of a broad definition of “institutional lender”:

“Institutional lender” means a bank, insurance company, pension fund, pension trust, foundation, savings and loan association, college or university, real estate or mortgage investment trust, the shares of which are traded on a national stock exchange or “over the counter”, or the stock of a management company which is owned by one of the foregoing institutions and any other person or entity who or which is generally regarded in the real estate financing field, at the time in question, as an “institutional lender”. See Subcommittee on Leasehold Encumbrances, Committee on Leasing, ABA Real Property Probate & Trust Law Section, Model Leasehold Encumbrance Provisions, 15 Real Prop., Prob. & Tr. J. 395, 401 (Summer 1980).

b. Loan-to-Value Ratio

The subordinating landlord may limit the total amount of all loans secured by the fee estate at any given time by specifying either a maximum dollar amount or a loan-to-value ratio. The landlord may also require the tenant to put in a specified amount or percentage of its own funds as equity into the development of the land. The lender should determine whether or not any such limitation on the loan amount applies to principal only or includes interest, funds expended by the lender to preserve the collateral and the lender’s attorneys' fees. A lender may be reluctant to accept the risk that interest and costs may be secured only by the leasehold estate and not both the fee and leasehold estates.

IIC-17

c. Interest Rate Limitations The subordinating landlord may condition its subordination of the fee estate on setting a maximum interest rate for the tenant’s loan. The lender should determine whether any maximum interest rate is too low for the lender’s loan terms, including taking into account the default rate of interest and possible rate modifications over the life of a long-term loan. Rather than setting a fixed maximum interest rate, a variable rate index (or indexes) plus a generous spread is more likely to be preferred by a lender. Any maximum interest rate provision in the lease should specifically provide that it would not apply to the interest rate charged by the lender after a default in the loan.

d. Liability of the Landlord The subordinating landlord is likely to require that it have no personal liability under the tenant’s loan. If there is no common ownership between the landlord and the tenant and if the lender did not have make its lending decision based on the landlord’s credit worthiness, exculpating the landlord from liability for the loan should not be an issue with the tenant’s lender. In such case, the fee mortgage should contain a clause exculpating the landlord from personal liability under the loan.

2. Notice of Tenant's Defaults and Right to Cure The subordinating landlord who does not share common ownership with the tenant is in a precarious position when it comes to tenant’s loan defaults. Because the landlord has an interest in preserving its fee estate, it may require that the lender give the landlord notice of the tenant’s loan defaults and the right to cure the defaults prior to the lender commencing foreclosure. It is likely that the landlord will also request copies of all notices of defaults given to the tenant and an additional period to cure the defaults. The landlord has an interest in not allowing the defaults to accumulate, making it more costly to cure the defaults to forestall foreclosure. The greater the common ownership between the landlord and tenant, the less likely the lender will be to agree to giving the landlord additional time to cure the tenant’s default as there will probably be little, if any, justification for additional time to cure. The landlord’s legitimate interest in receiving notices of the tenant’s defaults under the loan must be balanced against the lender’s legitimate interest in not giving the landlord so much time to cure defaults that the lender’s ability to exercise its remedies is unreasonably delayed. In order to further protect the landlord, the lease and the mortgage should specifically allow the landlord to cure the tenant’s loan defaults without obligating the landlord to do so. Like the unsubordinated leasehold lender, the landlord of a subordinated lease may be concerned about defaults of the tenant under the loan that are not susceptible to being cured by the landlord. In order to ensure that the lender’s lien on the fee estate is not compromised, however, the lender will likely not be willing to remove non-curable defaults from the loan.

3. Improvement on the Property The subordinating landlord may wish to be involved in the construction process because if the tenant mismanages construction, abandons construction, or after construction is complete is unable to obtain or retain subtenants thereby rendering the project not economically viable, then the landlord risks forfeiture of its fee ownership through the lender’s foreclosure or may be forced to cure the defaults under the loan to preserve its fee estate. If the landlord establishes controls for the feasibility of the proposed project (for example, approval of the plans and specifications and the contractor, pro forma rent analysis, the completion date, and the conditions upon which the tenant will request loan disbursements), the lender should review such controls to determine if any are in conflict with the lender’s requirements.

IIC-18

a. Prerequisites and Conditions to Construction The lease may contain construction prerequisites and ongoing conditions to construction, which may be designed to assure the landlord that construction is being undertaken in a prudent manner. If the lease contains construction covenants, the lender should ensure that it is clear that compliance with such conditions is the sole responsibility of the tenant. In addition the lender should require that the lease or mortgage clearly state that the subordination of the fee estate is not conditioned on the continued compliance with any ongoing construction covenants in the lease. See National Mortgage Corporation v. American Title Insurance Company, 299 N.C. 369, 261 S.E.2d 844 (1980) in which the court held that the title insurer was not liable for losses suffered by the plaintiff after a court determined that the landlord’s subordination to the plaintiff’s deed of trust was null and void for failure to assure that the loan funds were used for construction on the leased land.

b. Restoration After Loss

i. Application of Insurance Proceeds

The landlord, tenant and lender have similar concerns regarding insurance proceeds regardless of whether the lease is subject to subordinated or unsubordinated financing. See discussion in Section II.D.2. above for a discussion of insurance proceeds.

ii. Application of Condemnation Award Allocation of any condemnation award between the landlord and tenant should be addressed in the lease in the same manner as it would be for an unsubordinated lease. When the lease is subordinated, however, the lender should entitled to the entire condemnation award up to the balance of the loan. In case of a partial condemnation, the lender’s preference will be to have discretion to apply the award to the balance of the loan or to use the award to restore the property. The landlord and tenant may negotiate some ability to determine whether the award is used to reduce the loan or to restore the property. The same issues and solutions are applicable as with unsubordinated leasehold financing. See Section II.D.3. above for a discussion of condemnation awards.

B. Leasehold Mortgage Clauses Subordinated leasehold financing is preferred by lenders for the obvious reason: the lender is in essentially the same position as with any other fee financing and does not bear the risk of losing its collateral upon a premature termination of the lease. Though the lender may use one mortgage form to encumber both the leasehold estate and the fee estate, the mortgage form should include some clauses not usually included in the standard fee mortgage. The following sections discuss provisions for the lender to include in the subordinated fee mortgage.

1. Description of the Debt, Fee Estate and Leasehold Estate

As with any other accommodation mortgage, the mortgage must clearly identify the secured indebtedness as being that of the tenant and not the landlord to be enforceable. See In re Enderle, 110 N.C. App. 773, 431 S.E. 2d 549 (N.C. App. 1993). Though the fee estate is most likely to be more valuable than the leasehold estate, the lender may nonetheless wish to retain the option to foreclosure the fee estate and/or the leasehold estate. It is possible that at the time of foreclosure, the fee estate may have a problem rendering it undesirable, such as environmental contamination. Therefore, both the landlord and tenant should be identified as grantors under the mortgage, and the mortgage should identify both the fee estate and the leasehold estate in the granting clause of the mortgage.

IIC-19

2. Marshalling of Estates Unless addressed to the contrary, at foreclosure the tenant and the landlord each would have the right to require the lender to foreclose on the other’s estate first. Therefore, the mortgage should include a clause whereby the landlord and tenant each waive their right to require the lender to marshal the leasehold estate and the fee estate at a foreclosure sale. This also allows the lender the maximum flexibility at the time of foreclosure.

3. Anti-merger Clause Many ground lease tenants develop the land with the intention to sublease it. For this reason, the lender should ensure that the leasehold estate and the fee estate will not merge upon the lender or other purchaser at foreclosure purchasing both estates. A merger of the estates may cause the termination of potentially valuable subleases because there exists no privity of estate or contract between the subtenants and the fee owner. As an added precaution, the lender should consider requiring the subleases to contain an agreement to attorn to the purchaser of the fee at any foreclosure sale and to the owner of the fee estate should the fee and the leasehold estates merge.