Embed Size (px)

Citation preview

Lend For America SummitNovember 15, 2014

Protecting Your Portfolio

Christopher Mendezona Executive DirectorAlex Gewecke Director of FinanceConnor Baskin Executive Director (2015-2016)AJ Farr Director of Finance (2015-2016)

Why should I care?

Collections, Contract, and Clients

Collections

Some keys to having “control” of your collections:

1 Empathy2 Know your client3 Be organized4 KNOW YOUR CONTRACT5 Innovation

Source: Small Business Administration -- Arizona Profile

Contract

o Know the vital aspects of the contracto Late fees

o When do they take affect?o What is the penalty (flat fee or percentage of balance)?

o Principal Amounto Principal dueo Principal remaining

o Interest Amounto Interest dueo Interest remaining

o Make sure the client knows too

Source: Small Business Administration -- Arizona Profile

Client

Empathy: What is it?

Client

o Know the vital aspects your Client and who they areo Preferred communication channelo Personal info (phone, email, business address,

personal address)o Who are they?

o What are their interests?o What do you have in common?(sports, food,

community, etc.)

Source: Small Business Administration -- Arizona Profile

3 Client categories of AMI:

Ideal AVERAGE HIGH RISK

HIGH RISK

Communication

Poor/inconsistent

Inconsistent

PaymentsLate

Payments

Late Fees

Delinquenc

yDefault

Split/multiple payments

Cash

Check

Payment plan

AVERAGE

Communication

More than 1 Channel

Last Minute

Consistent

Payments

Late Payments

On occasion

Multiple Methods for

Payment

Cash

Check

IDEAL

Communication

Very responsive

Consistent channel

Contacts you directly

Payments

On-time Payments

Pays full amount

Does not pay fees

Case Studies

High-Risk Client: Delinquent Client

Problems:

• No communication channels or consistent meetings established

• No specific payment method• Weak late fee structure• Absence of structured payment schedule and loan budget

Example:

What was the result of these problems?

Innovation

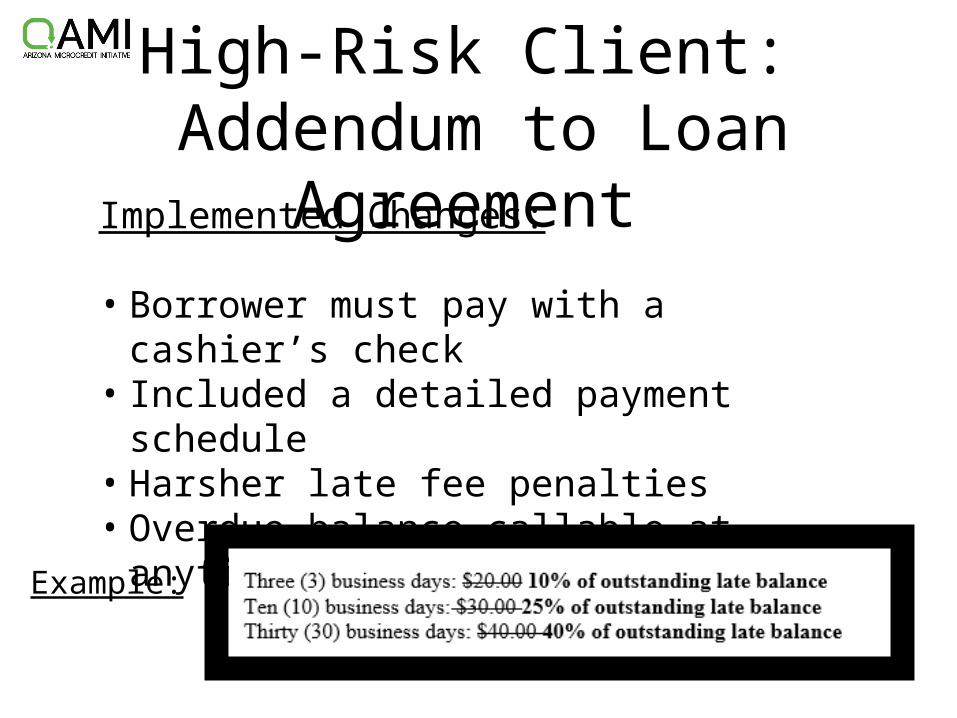

High-Risk Client: Addendum to Loan Agreement

Implemented Changes:

• Borrower must pay with a cashier’s check• Included a detailed payment schedule• Harsher late fee penalties• Overdue balance callable at anytime, once

delinquent

Example:

Lesson Learned

Solve the problem before it arises

Ideal Client: Farmers’ Market Seasonings

Contract Improvements & Client Management:

• Due to seasonality of farmers’ markets, reduced payments during “Summer” months while boosting payments during peak months

• Highly responsive and flexible to the client’s requests• Organized multi-communication channels • In-depth “Use of Funds” budget breakdown

Ideal Client: Farmers’ Market Seasonings

Average Client:Bus Transportation Services

Contract Improvements:

• Required proof of vehicle insurance and title• Agreement to share current tax returns upon

completion• Frequent follow-ups and consistent meetings• Liabilities clause – loan cannot pay other outstanding

liabilities• Loan budget and payment schedule• Two AMI (lender) and two company representatives

(borrower) signatures required

Average Client:Bus Transportation Services

Example:

Questionable Client: Oil Retention System

Contract Improvements & Client Management:

• Multi-channel communication • Stemming from an inconsistent revenue stream,

implemented a revenue hurdle • Provisional extension of loan capital contingent upon

revenue hurdle• Analyzed both business and personal bank statements• Reactive and attentive to client needs

Future Innovations

1. Uniform Commercial Code (UCC) – 1 Lien

2. Security Agreement

3. Confidentiality Clause

Questions?

Christopher Mendezona Chris@azmicrocreditAlex GeweckeAlex@azmicrocreditConnor BaskinConnor@azmicrocreditAJ Farr Aj@azmicrocredit

Contact Information

Azmicrocredit.org

Christopher Mendezona Chris@azmicrocreditAlex GeweckeAlex@azmicrocreditConnor BaskinConnor@azmicrocreditAJ Farr Aj@azmicrocredit

Azmicrocredit.org