Embed Size (px)

Citation preview

1

MASB 25

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIAMALAYSIAN ACCOUNTING STANDARDS BOARD

MASB Standard 25

Income Taxes

Any correspondence regarding this Standard should be addressed to:

The ChairmanMalaysian Accounting Standards BoardSuites 5.01 – 5.03, 5th FloorNo. 338 Jalan Tuanku Abdul Rahman50100 Kuala Lumpur

Tel No : 03 – 2715 9199Fax No: 03 – 2715 9212

E-mail address : [email protected] address : http://www.masb.org.my/

© Malaysian Accounting Standards Board 2001

MASB 25

2

Summary of the Differences between this Standard andthe Original IAS 12

Introduction

This Standard supersedes MASB Approved Accounting Standard IAS 12,Accounting for Taxes on Income (‘the original IAS 12’) as an approvedaccounting standard. The major changes from the original IAS 12 are asfollows.

1. The original IAS 12 required an enterprise to account for deferred taxusing either the deferral method or a liability method which issometimes known as the income statement liability method. ThisStandard prohibits the deferral method and requires another liabilitymethod which is sometimes known as the balance sheet liability method.

The income statement liability method focuses on timing differences,whereas the balance sheet liability method focuses on temporarydifferences. Timing differences are differences between taxable profitand accounting profit that originate in one period and reverse in one ormore subsequent periods. Temporary differences are differences betweenthe tax base of an asset or liability and its carrying amount in thebalance sheet. The tax base of an asset or liability is the amountattributed to that asset or liability for tax purposes.

All timing differences are temporary differences. Temporarydifferences also arise in the following circumstances, whichdo not give rise to timing differences, although the originalIAS 12 treated them in the same way as transactions that dogive rise to timing differences:

(a) assets are revalued and no equivalent adjustment is made for taxpurposes; and

(b) the cost of a business combination that is an acquisition isallocated to the identifiable assets and liabilities acquired, byreference to their fair values but no equivalent adjustment is madefor tax purposes.

3

MASB 25

Furthermore, there are some temporary differences which are nottiming differences, for example those temporary differences that arisewhen:

(a) the non-monetary assets and liabilities of a foreign operationthat is integral to the operations of the reporting entity aretranslated at historical exchange rates;

(b) non-monetary assets and liabilities are restated under theinternational best practice on financial reporting inhyperinflationary economies; or

(c) the carrying amount of an asset or liability on initial recognitiondiffers from its initial tax base.

2. The original IAS 12 permitted an enterprise not to recognise deferredtax assets and liabilities where there was reasonable evidence thattiming differences would not reverse for some considerable period ahead.This Standard requires an enterprise to recognise a deferred tax liabilityor (subject to certain conditions) asset for all temporary differences,with certain exceptions noted below.

3. The original IAS 12 required that:

(a) deferred tax assets arising from timing differences should berecognised when there was a reasonable expectation ofrealisation; and

(b) deferred tax assets arising from tax losses should be recognisedas an asset only where there was assurance beyond anyreasonable doubt that future taxable income would be sufficientto allow the benefit of the loss to be realised. The original IAS12 permitted (but did not require) an enterprise to deferrecognition of the benefit of tax losses until the period ofrealisation.

This Standard requires that deferred tax assets should be recognisedwhen it is probable that taxable profits will be available against whichthe deferred tax asset can be utilised. Where an enterprise has a historyof tax losses, the enterprise recognises a deferred tax asset only to theextent that the enterprise has sufficient taxable temporary differencesor there is convincing other evidence that sufficient taxable profit willbe available.

MASB 25

4

4. As an exception to the general requirement set out in paragraph 2 above,this Standard prohibits the recognition of deferred tax liabilities anddeferred tax assets arising from certain assets or liabilities whosecarrying amount differs on initial recognition from their initial tax base.Because such circumstances do not give rise to timing differences, theydid not result in deferred tax assets or liabilities under the original IAS12.

5. The original IAS 12 did not refer explicitly to fair value adjustmentsmade on a business combination. Such adjustments give rise totemporary differences and the Standard requires an enterprise torecognise the resulting deferred tax liability or (subject to theprobability criterion for recognition) deferred tax asset with acorresponding effect on the determination of the amount of goodwill ornegative goodwill. However, this Standard prohibits the recognition ofdeferred tax liabilities arising from goodwill itself (if amortisation ofthe goodwill is not deductible for tax purposes) and of deferred taxassets arising from negative goodwill that is treated as deferred income.

6. The original IAS 12 permitted, but did not require, an enterprise torecognise a deferred tax liability in respect of asset revaluations. ThisStandard requires an enterprise to recognise a deferred tax liability inrespect of asset revaluations.

7. The tax consequences of recovering the carrying amount of certainassets or liabilities may depend on the manner of recovery orsettlement, for example the amount that is deducted for tax purposes onsale of an asset is greater than the amount that may be deducted asdepreciation.

The original IAS 12 gave no guidance on the measurement of deferredtax assets and liabilities in such cases. This Standard requires that themeasurement of deferred tax liabilities and deferred tax assets shouldbe based on the tax consequences that would follow from the manner inwhich the enterprise expects to recover or settle the carrying amount ofits assets and liabilities.

8. The original IAS 12 did not state explicitly whether deferred tax assetsand liabilities may be discounted. This Standard prohibits discountingof deferred tax assets and liabilities.

5

MASB 25

9. The original IAS 12 did not specify whether an enterprise shouldclassify deferred tax balances as current assets and liabilities or as non-current assets and liabilities. This Standard requires that an enterprisewhich makes the current/non-current distinction should not classifydeferred tax assets and liabilities as current assets and liabilities.

10. The original IAS 12 stated that debit and credit balances representingdeferred taxes may be offset. This Standard establishes more restrictiveconditions on offsetting, based largely on those for financial assets andliabilities in MASB 24, Financial Instruments: Disclosure andPresentation.

11. The original IAS 12 required disclosure of an explanation of therelationship between tax expense and accounting profit if not explainedby the tax rates effective in the reporting enterprise’s country. ThisStandard requires this explanation to take either or both of thefollowing forms:

(i) a numerical reconciliation between tax expense (income) andthe product of accounting profit multiplied by the applicable taxrate(s); or

(ii) a numerical reconciliation between the average effective tax rateand the applicable tax rate.

The Standard also requires an explanation of changes in the applicabletax rate(s) compared to the previous accounting period.

12. New disclosures required by the Standard include:

(a) in respect of each type of temporary difference, unused tax lossesand unused tax credits:

(i) the amount of deferred tax assets and liabilitiesrecognised; and

(ii) the amount of the deferred tax income or expenserecognised in the income statement, if this is notapparent from the changes in the amounts recognised inthe balance sheet;

MASB 25

6

(b) in respect of discontinued operations, the tax expense relatingto:

(i) the gain or loss on discontinuance; and

(ii) the profit or loss from the ordinary activities of thediscontinued operation; and

(c) the amount of a deferred tax asset and the nature of the evidencesupporting its recognition, when:

(i) the utilisation of the deferred tax asset is dependent onfuture taxable profits in excess of the profits arising fromthe reversal of existing taxable temporary differences; and

(ii) the enterprise has suffered a loss in either the current orpreceding period in the tax jurisdiction to which thedeferred tax asset relates.

7

MASB 25

Income Taxes

Contents

Objective

Scope Paragraphs 1 - 4

Definitions 5 - 11

Tax Base 7 - 11

Recognition of Current Tax Liabilities andCurrent Tax Assets 12 - 13

Recognition of Deferred Tax Liabilities andDeferred Tax Assets 14 - 43

Taxable Temporary Differences 14 - 25

Business Combinations 18

Assets Carried at Fair Value 19 - 21

Goodwill 22

Initial Recognition of an Asset or Liability 23 - 25

Deductible Temporary Differences 26 - 36

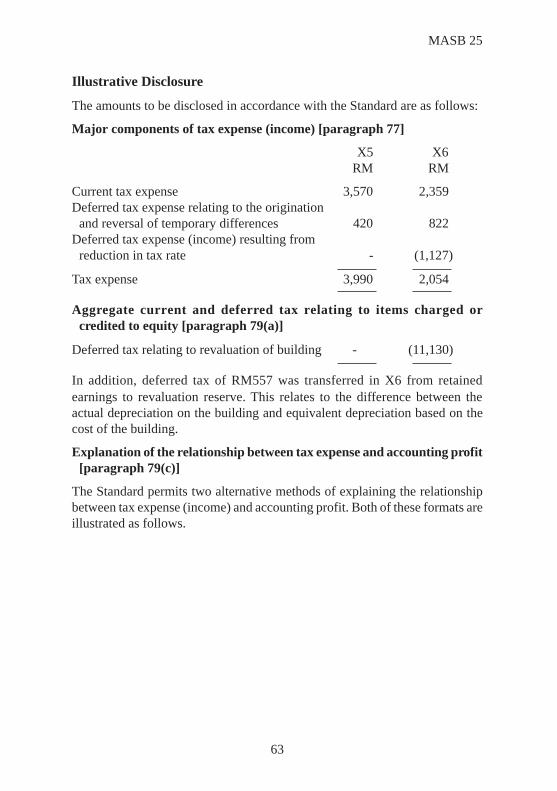

Negative Goodwill 34

Initial Recognition of an Asset or Liability 35 - 36

Unused Tax Losses and Unused Tax Credits 37 - 39

Re-assessment of Unrecognised DeferredTax Assets 40

Investments in Subsidiaries, Branches andAssociates and Interests in Joint Ventures 41 - 43

Measurement 44 - 54

MASB 25

8

Recognition of Current and Deferred Tax 55 - 66

Income statement 56 - 58

Items Credited or Charged Directly to Equity 59 - 63

Deferred Tax Arising from a BusinessCombination 64 - 66

Presentation 67 - 76

Tax Assets and Tax Liabilities 67 - 68

Offset 69 - 74

Tax Expense 75 - 76

Tax Expense (Income) related to Profit orLoss from Ordinary Activities 75

Exchange Differences on Deferred ForeignTax Liabilities or Assets 76

Disclosure 77 - 87

Transitional Provision 88

Effective Date 89

Compliance with International AccountingStandards Appendix 1

Examples of Temporary Differences Appendix 2

Illustrative Computations and Presentation Appendix 3

9

MASB 25

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIAMALAYSIAN ACCOUNTING STANDARDS BOARD

Income TaxesThe standards, which have been set in the bold type, should be read in thecontext of the background material and implementation guidance in thisStandard, and in the context of the Foreword to MASB Standards. MASBStandards are not intended to apply to immaterial items.

Objective

The objective of this Standard is to prescribe the accounting treatment forincome taxes. The principal issue in accounting for income taxes is how toaccount for the current and future tax consequences of:

(a) the future recovery (settlement) of the carrying amount of assets(liabilities) that are recognised in an enterprise’s balance sheet; and

(b) transactions and other events of the current period that are recognisedin an enterprise’s financial statements.

It is inherent in the recognition of an asset or liability that the reportingenterprise expects to recover or settle the carrying amount of that asset orliability. If it is probable that recovery or settlement of that carrying amountwill make future tax payments larger (smaller) than they would be if suchrecovery or settlement were to have no tax consequences, this Standardrequires an enterprise to recognise a deferred tax liability (deferred tax asset),with certain limited exceptions.

This Standard requires an enterprise to account for the tax consequences oftransactions and other events in the same way that it accounts for thetransactions and other events themselves. Thus, for transactions and other eventsrecognised in the income statement, any related tax effects are also recognisedin the income statement. For transactions and other events recognised directlyin equity, any related tax effects are also recognised directly in equity.Similarly, the recognition of deferred tax assets and liabilities in a businesscombination affects the amount of goodwill or negative goodwill arising inthat business combination.

MASB 25

10

This Standard also deals with the recognition of deferred tax assets arisingfrom unused tax losses or unused tax credits, the presentation of income taxesin the financial statements and the disclosure of information relating to incometaxes.

Scope

1. This Standard should be applied in accounting for income taxes.

2. This Standard supersedes MASB Approved Accounting Standard, IAS12, Accounting for Taxes on Income.

3. For the purposes of this Standard, income taxes include all domesticand foreign taxes which are based on taxable profits. Income taxes alsoinclude other taxes, such as withholding taxes, which are payable by aforeign subsidiary, associate or joint venture on distributions to thereporting enterprise, and real property gains taxes payable on disposalof properties.

4. This Standard does not deal with the methods of accounting forgovernment grants or investment tax credits. However, this Standarddoes deal with the accounting for temporary differences that may arisefrom such grants or investment tax credits.

Definitions

5. The following terms are used in this Standard with the meaningsspecified:

Accounting profit is net profit or loss for a period before deductingtax expense.

Current tax is the amount of income taxes payable (recoverable) inrespect of the taxable profit (tax loss) for a period.

Deferred tax assets are the amounts of income taxes recoverable infuture periods in respect of:

(a) deductible temporary differences;

(b) the carryforward of unused tax losses; and

(c) the carryforward of unused tax credits.

Deferred tax liabilities are the amounts of income taxes payable infuture periods in respect of taxable temporary differences.

11

MASB 25

Tax expense (tax income) is the aggregate amount included in thedetermination of net profit or loss for the period in respect ofcurrent tax and deferred tax.

Taxable profit (tax loss) is the profit (loss) for a period, determinedin accordance with the rules established by the taxationauthorities, upon which income taxes are payable (recoverable).

Temporary differences are differences between the carrying amountof an asset or liability in the balance sheet and its tax base.Temporary differences may be either:

(a) taxable temporary differences, which are temporarydifferences that will result in taxable amounts indetermining taxable profit (tax loss) of future periods whenthe carrying amount of the asset or liability is recovered orsettled; or

(b) deductible temporary differences, which are temporarydifferences that will result in amounts that are deductible indetermining taxable profit (tax loss) of future periods whenthe carrying amount of the asset or liability is recovered orsettled.

The tax base of an asset or liability is the amount attributed to thatasset or liability for tax purposes.

6. Tax expense (tax income) comprises current tax expense (current taxincome) and deferred tax expense (deferred tax income).

Tax Base

7. The tax base of an asset is the amount that will be deductible for taxpurposes against any taxable economic benefits that will flow to anenterprise when it recovers the carrying amount of the asset. If thoseeconomic benefits will not be taxable, the tax base of the asset is equalto its carrying amount.

MASB 25

12

Examples

1. A machine costs RM1,000. For tax purposes, capitalallowances of RM300 have already been deducted in the currentand prior periods and the remaining cost will be deductible infuture periods, either as annual capital allowances or through abalancing allowance on disposal. Revenue generated by usingthe machine is taxable, any gain or loss on disposal of themachine will be subject to a balancing charge or allowance fortax purposes. The tax base of the machine is RM700.

2. Interest receivable has a carrying amount of RM100. Therelated interest revenue will be taxed on a cash basis. The taxbase of the interest receivable is nil.

3. Trade receivables have a carrying amount of RM100. Therelated revenue has already been included in taxable profit (taxloss). The tax base of the trade receivables is RM100.

4. Dividends receivable from a subsidiary have a carrying amountof RM100. The dividends are not taxable. In substance, theentire carrying amount of the asset is deductible against theeconomic benefits. Consequently, the tax base of the dividendsreceivable is RM100.1

1. Under this analysis, there is no taxable temporary difference. Analternative analysis is that the accrued dividends receivable have a tax baseof nil and that a tax rate of nil is applied to the resulting taxable temporarydifference of RM100. Under both analyses, there is no deferred tax liability.

5. A loan receivable has a carrying amount of RM100. Therepayment of the loan will have no tax consequences. The taxbase of the loan is RM100.

8. The tax base of a liability is its carrying amount, less any amount thatwill be deductible for tax purposes in respect of that liability in futureperiods. In the case of revenue which is received in advance, the taxbase of the resulting liability is its carrying amount, less any amount ofthe revenue that will not be taxable in future periods.

13

MASB 25

Examples

1. Current liabilities include accrued expenses with a carryingamount of RM100. The related expense will be deducted for taxpurposes on a cash basis. The tax base of the accrued expensesis nil.

2. Current liabilities include interest revenue received in advance,with a carrying amount of RM100. The related interest revenuewas taxed on a cash basis. The tax base of the interest receivedin advance is nil.

3. Current liabilities include accrued expenses with a carryingamount of RM100. The related expense has already beendeducted for tax purposes. The tax base of the accrued expensesis RM100.

4. Current liabilities include accrued fines and penalties with acarrying amount of RM100. Fines and penalties are notdeductible for tax purposes. The tax base of the accrued finesand penalties is RM100.2

2. Under this analysis, there is no deductible temporary difference. Analternative analysis is that the accrued fines and penalties payable have a taxbase of nil and that a tax rate of nil is applied to the resulting deductibletemporary difference of RM100. Under both analyses, there is no deferred taxasset.

5. A loan payable has a carrying amount of RM100. Therepayment of the loan will have no tax consequences. The taxbase of the loan is RM100.

9. Some items have a tax base but are not recognised as assets andliabilities in the balance sheet. For example, research costs arerecognised as an expense in determining accounting profit in the periodin which they are incurred but may not be permitted as a deduction indetermining taxable profit (tax loss) until a later period. The differencebetween the tax base of the research costs, being the amount thetaxation authorities will permit as a deduction in future periods, and thecarrying amount of nil is a deductible temporary difference that resultsin a deferred tax asset.

MASB 25

14

10. Where the tax base of an asset or liability is not immediately apparent,it is helpful to consider the fundamental principle upon which thisStandard is based: that an enterprise should, with certain limitedexceptions, recognise a deferred tax liability (asset) whenever recoveryor settlement of the carrying amount of an asset or liability would makefuture tax payments larger (smaller) than they would be if suchrecovery or settlement were to have no tax consequences. Example Cfollowing paragraph 50 illustrates circumstances when it may behelpful to consider this fundamental principle, for example, when thetax base of an asset or liability depends on the expected manner ofrecovery or settlement.

11. In consolidated financial statements, temporary differences aredetermined by comparing the carrying amounts of assets and liabilitiesin the consolidated financial statements with the appropriate tax base.In Malaysia, the tax base is determined by reference to the tax returnsof each enterprise in the group. Therefore, unrealised profits or losseswhich are eliminated on consolidation create temporary differences inthe consolidated financial statements between carrying amounts ofassets and liabilities and their corresponding tax bases.

Recognition of Current Tax Liabilities and Current TaxAssets

12. Current tax for current and prior periods should, to the extentunpaid, be recognised as a liability. If the amount already paid inrespect of current and prior periods exceeds the amount due forthose periods, the excess should be recognised as an asset.

13. In the Malaysian context, current income taxes, which were previouslybased on the preceding year basis, have been changed to the currentyear basis. Therefore, income taxes of current and prior periods should,to the extent unpaid, be recognised as a current tax liability. Conversely,if the amount of income taxes paid for current and prior periodsexceeds the amount assessed for those periods, the excess should berecognised as a current tax asset. Any over or under-provision forcurrent income taxes is accounted for as a change in estimate and isadjusted for when the Inland Revenue Board has made an assessmentof the amount of current income tax payable. The current income taxlaws do not permit a tax loss to be used to recover current tax of aprevious period. The tax loss of a current period may be used to offsettaxable income in a future period, and accordingly, represents onlypotential tax savings in future periods which should be accounted for inaccordance with paragraph 37.

15

MASB 25

Recognition of Deferred Tax Liabilities and Deferred TaxAssets

Taxable Temporary Differences

14. A deferred tax liability should be recognised for all taxabletemporary differences, unless the deferred tax liability arises from:

(a) goodwill for which amortisation is not deductible for taxpurposes; or

(b) the initial recognition of an asset or liability in a transactionwhich:

(i) is not a business combination; and

(ii) at the time of the transaction, affects neitheraccounting profit nor taxable profit (tax loss).

15. It is inherent in the recognition of an asset that its carrying amount willbe recovered in the form of economic benefits that flow to theenterprise in future periods. When the carrying amount of the assetexceeds its tax base, the amount of taxable economic benefits willexceed the amount that will be allowed as a deduction for tax purposes.This difference is a taxable temporary difference and the obligation topay the resulting income taxes in future periods is a deferred taxliability. As the enterprise recovers the carrying amount of the asset, thetaxable temporary difference will reverse and the enterprise will havetaxable profit. This makes it probable that economic benefits will flowfrom the enterprise in the form of tax payments. Therefore, thisStandard requires the recognition of all deferred tax liabilities, exceptin certain circumstances described in paragraph 14.

MASB 25

16

Example

An asset which costs RM150 has a carrying amount of RM100.Cumulative capital allowance for tax purposes is RM90 and the tax rateis 25%.

The tax base of the asset is RM60 (cost of RM150 less cumulativecapital allowance of RM90). To recover the carrying amount of RM100,the enterprise must earn taxable profit of RM100, but will only be ableto deduct capital allowance of RM60. Consequently, the enterprise willpay income taxes of RM10 (RM40 at 25%) when it recovers thecarrying amount of the asset. The difference between the carryingamount of RM100 and the tax base of RM60 is a taxable temporarydifference of RM40. Therefore, the enterprise recognises a deferred taxliability of RM10 (RM40 at 25%) representing the income taxes that itwill pay when it recovers the carrying amount of the asset.

16. Some temporary differences arise when income or expense is includedin accounting profit in one period but is included in taxable profit in adifferent period. Such temporary differences are often described astiming differences. The following are examples of temporarydifferences of this kind which are taxable temporary differences andwhich therefore result in deferred tax liabilities:

(a) interest revenue is included in accounting profit on a timeproportion basis but may be included in taxable profit when cashis collected. The tax base of any interest receivable recognisedin the balance sheet with respect to such revenues is nil becausethe revenues do not affect taxable profit until cash is collected;

(b) depreciation used in determining taxable profit (tax loss) maydiffer from that used in determining accounting profit. Thetemporary difference is the difference between the carryingamount of the asset and its tax base which is the original cost ofthe asset less all deductions in respect of that asset permitted bythe taxation authorities in determining taxable profit of thecurrent and prior periods. A taxable temporary difference arises,and results in a deferred tax liability, when capital allowance isaccelerated (if capital allowance is less rapid than accountingdepreciation, a deductible temporary difference arises, andresults in a deferred tax asset); and

17

MASB 25

(c) development costs may be capitalised and amortised over futureperiods in determining accounting profit but deducted indetermining taxable profit in the period in which they areincurred. Such development costs have a tax base of nil as theyhave already been deducted from taxable profit. The temporarydifference is the difference between the carrying amount of thedevelopment costs and their tax base of nil.

17. Temporary differences also arise when:

(a) the cost of a business combination that is an acquisition isallocated to the identifiable assets and liabilities acquired byreference to their fair values but no equivalent adjustment is madefor tax purposes (see paragraph 18);

(b) assets are revalued and no equivalent adjustment is made for taxpurposes (see paragraph 19);

(c) goodwill or negative goodwill arises on consolidation (seeparagraphs 22 and 34); or

(d) the tax base of an asset or liability on initial recognition differsfrom its initial carrying amount, for example when an enterpriseacquires a non-industrial building or when it benefits fromnon-taxable government grants related to assets (see paragraphs23 and 35).

Business Combinations

18. In a business combination that is an acquisition, the cost of theacquisition is allocated to the identifiable assets and liabilities acquiredby reference to their fair values at the date of the exchange transaction.Temporary differences arise when the tax bases of the identifiableassets and liabilities acquired are not affected by the businesscombination or are affected differently. For example, when thecarrying amount of an asset is increased to fair value but the tax base ofthe asset remains at cost to the previous owner, a taxable temporarydifference arises which results in a deferred tax liability. The resultingdeferred tax liability affects goodwill (see paragraph 64).

MASB 25

18

Assets Carried at Fair Value

19. MASB Standards permit certain assets to be carried at fair value or tobe revalued (see, for example, MASB 15, Property, Plant andEquipment, and MASB ED 31, Investment Property). In Malaysia, therevaluation or restatement of an asset does not affect taxable profit inthe period of the revaluation or restatement and, consequently, the taxbase of the asset is not adjusted. Nevertheless, the future recovery ofthe carrying amount will result in a taxable flow of economic benefitsto the enterprise and the amount that will be deductible for tax purposeswill differ from the amount of those economic benefits. The differencebetween the carrying amount of a revalued asset and its tax base is atemporary difference and gives rise to a deferred tax liability or asset.For a depreciable property, plant or equipment, this is true even if:

(a) the enterprise does not intend to dispose of the asset. In suchcases, the revalued carrying amount of the asset will berecovered through use and this will generate taxable incomewhich exceeds the capital allowance that will be deductible fortax purposes in future periods; or

(b) the tax effect of a balancing charge and/or real property gainstax is deferred until the revalued asset is disposed. In such cases,the tax will ultimately become payable on sale of the revaluedasset.

20. However, for a non-depreciable property, such as a freehold land, thereis no recovery through use as the asset is not subject to depreciation.The tax effect of any upward revaluation for such asset relates only toreal property gains tax. In such circumstances, deferred tax on thetemporary difference (i.e., the revaluation surplus) is recognised on theexpected property gains tax payable if the enterprise has a firmcommitment to dispose of the property in the foreseeable future. If theenterprise has no firm commitment to dispose of the revalued propertyin the foreseeable future, the minimum property gains tax rate of fiveper cent should be used to recognise the deferred tax liability on thesurplus arising from the revaluation. Similarly for an investment orinvestment property, which is not subject to depreciation oramortisation, no tax liability will crystallise through use. Accordingly,a deferred tax liability on a revaluation surplus is recognised if, andonly if, a disposal of the revalued investment or revalued investmentproperty will result in taxes payable and the enterprise has a firmcommitment to dispose the investment or investment property.

19

MASB 25

21. For a building that does not qualify for tax allowances, a temporarydifference arises on its initial recognition as it has a tax base of nil.Paragraph 14 (b) of the Standard does not permit an enterprise torecognise a deferred tax liability on its initial recognition andsubsequently. This exemption, however, does not apply to anyrevaluation surplus arising if the building is revalued upwardsubsequent to its initial recognition. This is because a building is adepreciable asset and therefore tax liability on the revaluation surpluswill crystallise when the carrying revalued amount of the building isrecovered through use or by disposal. In the case when the enterprisehas entered into a firm commitment, such as a binding salearrangement, to dispose the building in the foreseeable future, thedeferred tax liability should be measured by the sum of the income taxrate based on the additional depreciation arising from the surplus in theintervening periods prior to the date of the disposal, if any, plus the realproperty gains tax payable on its disposal. In all other circumstances,the deferred tax liability should be measured by the income tax rate onthe revaluation surplus arising from the revaluation of the building. Thisis because in such cases, the future economic benefits generated fromthe use of the revalued building is subject to income tax.

Goodwill

22. Goodwill is the excess of the cost of an acquisition over the acquirer’sinterest in the fair value of the identifiable assets and liabilities acquired.The Inland Revenue Board does not allow the amortisation of goodwillas a deductible expense in determining taxable profit. Moreover, thecost of goodwill is often not deductible when a subsidiary disposes ofits underlying business. In such circumstances, goodwill has a tax baseof nil. Any difference between the carrying amount of goodwill and itstax base of nil is a taxable temporary difference. However, thisStandard does not permit the recognition of the resulting deferred taxliability because goodwill is a residual and the recognition of thedeferred tax liability would increase the carrying amount of goodwill.

Initial Recognition of an Asset or Liability

23. A temporary difference may arise on initial recognition of an asset orliability, for example if part or all of the cost of an asset will not bedeductible for tax purposes. The method of accounting for such atemporary difference depends on the nature of the transaction whichled to the initial recognition of the asset:

MASB 25

20

(a) in a business combination, an enterprise recognises any deferredtax liability or asset and this affects the amount of goodwill ornegative goodwill (see paragraph 18);

(b) if the transaction affects either accounting profit or taxable profit,an enterprise recognises any deferred tax liability or asset andrecognises the resulting deferred tax expense or income in theincome statement (see paragraph 57);

(c) if the transaction is not a business combination, and affectsneither accounting profit nor taxable profit, an enterprise would,in the absence of the exemption provided by paragraphs 14 and26, recognise the resulting deferred tax liability or asset andadjust the carrying amount of the asset or liability by the sameamount. Such adjustments would make the financial statementsless transparent. Therefore, this Standard does not permit anenterprise to recognise the resulting deferred tax liability orasset, either on initial recognition or subsequently (see exampleon next page). Furthermore, an enterprise does not recognisesubsequent changes in the unrecognised deferred tax liability orasset as the asset is depreciated.

24. For example, a depreciable leasehold property that neither qualifies forindustrial building allowance nor for capital allowances would have atax base of nil on initial recognition and subsequently. Temporarydifference on the leasehold property would, therefore, be the carryingamount on initial recognition and subsequently. However, no deferredtax liability should be recognised on this temporary difference, eitheron initial recognition or subsequently, because the tax effect arises fromthe initial recognition of the leasehold property. Similarly, temporarydifferences arising on initial recognition of other non-qualifying fixedassets, such as amounts in excess RM50,000 for non-commercialvehicles, should be disregarded in the recognition of deferred taxliability of the enterprise.

21

MASB 25

Example Illustrating Paragraph 23(c)

An enterprise intends to use a non-moveable fixture which costsRM1,000 throughout its useful life of five years and then dispose of itfor a residual value of nil. The tax rate is 30%. Depreciation of the assetis not deductible for tax purposes. On disposal, any capital gain wouldnot be taxable and any capital loss would not be deductible.

As it recovers the carrying amount of the asset, the enterprise will earntaxable income of RM1,000 and pay tax of RM300. The enterprise doesnot recognise the resulting deferred tax liability of RM300 because itresults from the initial recognition of the asset.

In the following year, the carrying amount of the asset is RM800. Inearning taxable income of RM800, the enterprise will pay tax of RM240.The enterprise does not recognise the deferred tax liability of RM240because it results from the initial recognition of the asset.

25. In accordance with MASB 24, Financial Instruments: Disclosure andPresentation, the issuer of a compound financial instrument (forexample, a convertible bond or a bond issued with warrants) shouldclassify the instrument’s liability component as a liability and theequity component as equity. In Malaysia, the tax base of the liabilitycomponent on initial recognition is equal to the initial carrying amountof the sum of the liability and equity components. The resulting taxabletemporary difference arises from the initial recognition of the equitycomponent separately from the liability component. Therefore, theexception set out in paragraph 14(b) does not apply. Consequently, anenterprise recognises the resulting deferred tax liability. In accordancewith paragraph 59, the deferred tax is charged directly to the carryingamount of the equity component. In accordance with paragraph 56,subsequent changes in the deferred tax liability are recognised in theincome statement as deferred tax expense (income).

Deductible Temporary Differences

26. A deferred tax asset should be recognised for all deductibletemporary differences to the extent that it is probable that taxableprofit will be available against which the deductible temporarydifferences can be utilised, unless the deferred tax asset arises from:

MASB 25

22

(a) negative goodwill which is treated as deferred income; or

(b) the initial recognition of an asset or liability in a transactionwhich:

(i) is not a business combination; and

(ii) at the time of the transaction, affects neitheraccounting profit nor taxable profit (tax loss).

27. It is inherent in the recognition of a liability that the carrying amountwill be settled in future periods through an outflow from the enterpriseof resources embodying economic benefits. When resources flow fromthe enterprise, part or all of their amounts may be deductible indetermining taxable profit of a period later than the period in which theliability is recognised. In such cases, a temporary difference existsbetween the carrying amount of the liability and its tax base.Accordingly, a deferred tax asset arises in respect of the income taxesthat will be recoverable in the future periods when that part of theliability is allowed as a deduction in determining taxable profit.Similarly, if the carrying amount of an asset is less than its tax base, thedifference gives rise to a deferred tax asset in respect of the incometaxes that will be recoverable in future periods. This includes a generalprovision for doubtful debts which is setoff against the gross carryingamount of trade receivables on presentation in the balance sheet, butthere is no equivalent deduction to the tax base of the trade receivables.

23

MASB 25

Example

An enterprise recognises a liability of RM100 for accrued productwarranty costs. For tax purposes, the product warranty costs will not bedeductible until the enterprise pays claims. The tax rate is 25%.

The tax base of the liability is nil (carrying amount of RM100, less theamount that will be deductible for tax purposes in respect of thatliability in future periods). In settling the liability for its carrying amount,the enterprise will reduce its future taxable profit by an amount of RM100and, consequently, reduce its future tax payments by RM25 (RM100 at25%). The difference between the carrying amount of RM100 and thetax base of nil is a deductible temporary difference of RM100.Therefore, the enterprise recognises a deferred tax asset of RM25(RM100 at 25%), provided that it is probable that the enterprise willearn sufficient taxable profit in future periods to benefit from areduction in tax payments.

28. The following are examples of deductible differences which result indeferred tax assets:

(a) retirement benefit costs may be deducted in determiningaccounting profit as service is provided by the employee, butdeducted in determining taxable profit either when contributionsare paid to an approved fund by the enterprise or whenretirement benefits are paid by the enterprise. A temporarydifference exists between the carrying amount of the liabilityand its tax base; the tax base of the liability is usually nil. Such adeductible temporary difference results in a deferred tax asset aseconomic benefits will flow to the enterprise in the form of adeduction from taxable profits when contributions or retirementbenefits are paid;

(b) research costs are recognised as an expense in determiningaccounting profit in the period in which they are incurred butmay not be permitted as a deduction in determining taxable profit(tax loss) until a later period. The difference between the taxbase of the research costs, being the amount the taxationauthorities will permit as a deduction in future periods, and thecarrying amount of nil is a deductible temporary difference thatresults in a deferred tax asset;

MASB 25

24

(c) in a business combination that is an acquisition, the cost of theacquisition is allocated to the assets and liabilities recognised,by reference to their fair values at the date of the exchangetransaction. When a liability is recognised on the acquisition butthe related costs are not deducted in determining taxable profitsuntil a later period, a deductible temporary difference arises whichresults in a deferred tax asset. A deferred tax asset also ariseswhere the fair value of an identifiable asset acquired is less thanits tax base. In both cases, the resulting deferred tax asset affectsgoodwill (see paragraph 64); and

(d) certain assets may be carried at fair value, or may be revalued,without an equivalent adjustment being made for tax purposes(see paragraph 19). A deductible temporary difference arises ifthe tax base of the asset exceeds its carrying amount.

29. The reversal of deductible temporary differences results in deductionsin determining taxable profits of future periods. However, economicbenefits in the form of reductions in tax payments will flow to theenterprise only if it earns sufficient taxable profits against which thedeductions can be offset. Therefore, an enterprise recognises deferredtax assets only when it is probable that taxable profits will be availableagainst which the deductible temporary differences can be utilised.

30. It is probable that taxable profit will be available against which adeductible temporary difference can be utilised when there aresufficient taxable temporary differences relating to the same taxationauthority and the same taxable entity which are expected to reverse:

(a) in the same period as the expected reversal of the deductibletemporary difference; or

(b) in periods into which a tax loss arising from the deferred taxasset can be carried forward.

In such circumstances, the deferred tax asset is recognised in the periodin which the deductible temporary differences arise. For example, whenthe reporting enterprise operates only in Malaysia and is subject only tothe Malaysian income tax laws, a deferred tax asset is recognised on atax loss or any other deductible temporary differences (such as ageneral provision for warranty expense) if there exists sufficienttaxable temporary differences. This is because the deferred tax liabilityrecognised on the taxable temporary differences will only crystallisewhen there is sufficient taxable profit in the future periods, and this willin itself provide assurance that the deferred tax asset will be realised.

25

MASB 25

31. When there are insufficient taxable temporary differences relating tothe same taxation authority and the same taxable entity, the deferred taxasset is recognised to the extent that:

(a) it is probable that the enterprise will have sufficient taxable profitrelating to the same taxation authority and the same taxableentity in the same period as the reversal of the deductibletemporary difference (or in the periods into which a tax lossarising from the deferred tax asset can be carried forward). Inevaluating whether it will have sufficient taxable profit in futureperiods, an enterprise ignores taxable amounts arising fromdeductible temporary differences that are expected to originatein future periods, because the deferred tax asset arising fromthese deductible temporary differences will itself require futuretaxable profit in order to be utilised; or

(b) tax planning opportunities are available to the enterprise thatwill create taxable profit in appropriate periods.

32. Tax planning opportunities are actions that the enterprise would take inorder to create or increase taxable income in a particular period beforethe expiry of a tax loss or tax credit carryforward. For example, taxableprofit may be created or increased by:

(a) electing to have interest income taxed on either a received orreceivable basis;

(b) deferring the claim for certain deductions from taxable profit;

(c) selling, and perhaps leasing back, assets that have appreciatedbut for which the tax base has not been adjusted to reflect suchappreciation; and

(d) selling an asset that generates non-taxable income (such as agovernment bond) in order to purchase another investment thatgenerates taxable income.

Where tax planning opportunities advance taxable profit from a laterperiod to an earlier period, the utilisation of a tax loss or tax creditcarryforward still depends on the existence of future taxable profit fromsources other than future originating temporary differences.

MASB 25

26

33. When an enterprise has a history of recent losses, the enterpriseconsiders the guidance in paragraphs 38 and 39.

Negative Goodwill

34. This Standard does not permit the recognition of a deferred tax assetarising from deductible temporary differences associated with negativegoodwill which is treated as deferred income because negativegoodwill is a residual and the recognition of the deferred tax asset wouldincrease the carrying amount of negative goodwill.

Initial Recognition of an Asset or Liability

35. One case when a deferred tax asset arises on initial recognition of anasset is when a non-taxable government grant related to an asset isdeducted in arriving at the carrying amount of the asset but, for taxpurposes, is not deducted from the asset’s depreciable amount (in otherwords its tax base); the carrying amount of the asset is less than its taxbase and this gives rise to a deductible temporary difference.Government grants may also be set up as deferred income in whichcase the difference between the deferred income and its tax base of nilis a deductible temporary difference. Whichever method ofpresentation an enterprise adopts, the enterprise does not recognise theresulting deferred tax asset, for the reason given in paragraph 23. Thisnon-recognition principle has traditionally been applied to permanentdifferences, which may include other items, such as a provision for anexpense which is permanently disallowed for income tax purposes.

36. Another case when a deferred tax asset arises on initial recognition ofan asset is when it qualifies for re-investment or other allowances inexcess of its normal capital allowances. In such a case, the carryingamount of the asset is less that its tax base on initial recognition, andthis gives rise to a deductible temporary difference. However, for thereason given in paragraph 23, the enterprise does not recognise theresulting deferred tax asset on initial recognition of the asset andsubsequently.

27

MASB 25

Unused Tax Losses and Unused Tax Credits

37. A deferred tax asset should be recognised for the carryforward ofunused tax losses and unused tax credits to the extent that it isprobable that future taxable profit will be available against whichthe unused tax losses and unused tax credits can be utilised.

38. The criteria for recognising deferred tax assets arising from thecarryforward of unused tax losses and tax credits are the same as thecriteria for recognising deferred tax assets arising from deductibletemporary differences. However, the existence of unused tax losses isstrong evidence that future taxable profit may not be available.Therefore, when an enterprise has a history of recent losses, theenterprise recognises a deferred tax asset arising from unused tax lossesor tax credits only to the extent that the enterprise has sufficient taxabletemporary differences or there is convincing other evidence thatsufficient taxable profit will be available against which the unused taxlosses or unused tax credits can be utilised by the enterprise. In suchcircumstances, paragraph 80 requires disclosure of the amount of thedeferred tax asset and the nature of the evidence supporting itsrecognition.

39. An enterprise considers the following criteria in assessing theprobability that taxable profit will be available against which theunused tax losses or unused tax credits can be utilised:

(a) whether the enterprise has sufficient taxable temporarydifferences relating to the same taxation authority and the sametaxable entity, which will result in taxable amounts against whichthe unused tax losses or unused tax credits can be utilised beforethey expire;

(b) whether it is probable that the enterprise will have taxableprofits before the unused tax losses or unused tax credits expire;

(c) whether the unused tax losses result from identifiable causeswhich are unlikely to recur; and

(d) whether tax planning opportunities (see paragraph 32) areavailable to the enterprise that will create taxable profit in theperiod in which the unused tax losses or unused tax credits canbe utilised.

MASB 25

28

To the extent that it is not probable that taxable profit will be availableagainst which the unused tax losses or unused tax credits can beutilised, the deferred tax asset is not recognised.

Re-assessment of Unrecognised Deferred Tax Assets

40. At each balance sheet date, an enterprise re-assesses unrecogniseddeferred tax assets. The enterprise recognises a previously unrecogniseddeferred tax asset to the extent that it has become probable that futuretaxable profit will allow the deferred tax asset to be recovered. Forexample, an improvement in trading conditions may make it moreprobable that the enterprise will be able to generate sufficient taxableprofit in the future for the deferred tax asset to meet the recognitioncriteria set out in paragraphs 26 or 37. Another example is when anenterprise re-assesses deferred tax assets at the date of a businesscombination or subsequently (see paragraphs 65 and 66).

Investments in Subsidiaries, Branches and Associates, andInterests in Joint Ventures

41. In consolidated financial statements, the temporary difference of aninvestment in a subsidiary, branch, associate or a joint venture may bedifferent from the temporary difference associated with that investmentin the parent’s separate financial statements if the parent carries theinvestment in its separate financial statements at cost or revalued amount.In respect of investments in local subsidiaries, associates or jointventures, it is rare for temporary differences to arise because any suchinvestments are usually carried at cost, which will be the same as its taxbase. Similarly, investments in subsidiaries, associates and jointventures are capital in nature, which are not tax-deductible or taxableon a subsequent disposal. Accordingly, no deferred tax asset or liabilityshould be provided on initial recognition and subsequently. In theinvestor’s separate financial statements, which must account for theseinvestments under the cost method, no deferred tax liability would arise.Tax effects may, however, arise in respect of dividend receivable fromoverseas subsidiaries, associates and joint ventures and only when thereexists a difference in the income tax rates between Malaysia and theoverseas jurisdictions. Any such tax effect is normally accounted as acurrent tax expense (or tax income) in the period in which the dividendincome is recognised. Accordingly, no deferred tax should berecognised in the separate accounts of the investor in respect ofundistributed profits of overseas subsidiaries, associates or jointventures.

29

MASB 25

42. As a parent controls the dividend policy of its overseas subsidiary, it isable to control the timing of the reversal of temporary differencesassociated with that investment (including the temporary differencesarising not only from undistributed profits but also from any foreignexchange translation differences). Furthermore, it would often beimpracticable to determine the amount of income taxes that would bepayable when the temporary difference reverses. This is because theamount of income tax payable, if any, is dependent on numerouscomplex factors, such as whether there exist tax treaties between theoverseas jurisdictions and Malaysia, the differential income tax rates,and the intended period(s) in which the profits would be remitted.Therefore, when the parent has determined that those profits will not bedistributed in the foreseeable future, or when remittance of thoseprofits will not attract additional income tax liability, the parent doesnot recognise a deferred tax liability. The same considerations apply toinvestments in branches.

43. An enterprise accounts in its own currency for the non-monetary assetsand liabilities of a foreign operation that is integral to the enterprise’soperations (see MASB 6, The Effects of Changes in Foreign ExchangeRates). Where the foreign operation’s taxable profit or tax loss (and,hence, the tax base of its non-monetary assets and liabilities) isdetermined in the foreign currency, changes in the exchange rate giverise to temporary differences. Because such temporary differencesrelate to the foreign operation’s own assets and liabilities, rather than tothe reporting enterprise’s investment in that foreign operation, thereporting enterprise recognises the resulting deferred tax liability or(subject to paragraph 26) asset. The resulting deferred tax is charged orcredited in the income statement (see paragraph 56).

Measurement

44. Current tax liabilities (assets) for the current and prior periodsshould be measured at the amount expected to be paid to(recovered from) the taxation authorities, using the tax rates (andtax laws) that have been enacted or substantively enacted by thebalance sheet date.

45. Deferred tax assets and liabilities should be measured at the taxrates that are expected to apply to the period when the asset isrealised or the liability is settled, based on tax rates (and tax laws)that have been enacted or substantively enacted by the balance sheetdate.

MASB 25

30

46. Current and deferred tax assets and liabilities are usually measuredusing the tax rates (and tax laws) that have been enacted. In Malaysia,announcements of tax rates (and tax laws) by the Government in theyearly Budget have the substantive effect of actual enactment, whichmay follow the announcement by a period of several months. In thesecircumstances, tax assets and liabilities are measured using theannounced tax rate (and tax laws).

47. When different tax rates apply to different levels of taxable income,deferred tax assets and liabilities are measured using the average ratesthat are expected to apply to the taxable profit (tax loss) of the periodsin which the temporary differences are expected to reverse.

48. For enterprises with sufficient tax credits, distribution of profits in theform of dividends would not attract additional tax liabilities.Consequently, no current or deferred tax liabilities should berecognised for the undistributed profits. For enterprises that have no orinsufficient tax credits, the distribution of some or all of its retainedprofits may attract additional tax liabilities. Consequently, when areporting enterprise has recognised a declared or proposed dividend asa component of equity in its balance sheet, a current liability should berecognised to the extent of the declared or proposed distribution notfranked by its available tax credits. Paragraph 81 requires an enterpriseto disclose whether it has sufficient tax credits to frank the distributionof its retained profits.

49. The measurement of deferred tax liabilities and deferred tax assetsshould reflect the tax consequences that would follow from themanner in which the enterprise expects, at the balance sheet date,to recover or settle the carrying amount of its assets and liabilities.

50. The manner in which an enterprise recovers (settles) the carrying amountof an asset (liability) may affect either or both of:

(a) the tax rate applicable when the enterprise recovers (settles) thecarrying amount of the asset (liability); and

(b) the tax base of the asset (liability).

In such cases, an enterprise measures deferred tax liabilities anddeferred tax assets using the tax rate and the tax base that are consistentwith the expected manner of recovery or settlement.

31

MASB 25

Example A

A machine has a carrying amount of RM1,000 and a tax base of RM600.The machine can be sold for cash of RM900. A balancing charge of30% would apply if the machine were sold for cash, and similarly, atax rate of 30% would apply to other income.

The enterprise recognises a deferred tax liability of RM90 (RM300 at30%) if it expects to sell the asset without further use and a deferred taxliability of RM120 (RM400 at 30%) if it expects to retain the asset andrecover its carrying amount through use.

Example B

An asset with a cost of RM100 and a carrying amount of RM80 isrevalued to RM150. No equivalent adjustment is made for tax purposes.Cumulative capital allowance is RM30 and the tax rate is 30%. If theasset is sold for more than cost, the cumulative capital allowance ofRM30 will be included in taxable income but sale proceeds in excess ofcost will not be taxable.

The tax base of the asset is RM70 and there is a taxable temporarydifference of RM80. If the enterprise expects to recover the carryingamount by using the asset, it must generate taxable income of RM150,but will only be able to deduct depreciation of RM70. On this basis,there is a deferred tax liability of RM24 (RM80 at 30%). If theenterprise expects to recover the carrying amount by selling the assetimmediately for proceeds of RM150, the deferred tax liability iscomputed as follows:

Taxable DeferredTemporary Tax TaxDifference Rate Liability

RM RM

Cumulative capital allowance 30 30% 9Proceeds in excess of cost 50 nil -

Total 80 9

(Note: in accordance with paragraph 59, the additional deferred taxthat arises on the revaluation is charged directly to equity)

MASB 25

32

Example C

The facts are as in example B, except that if the asset is sold for morethan cost, the cumulative capital allowances will be included in taxableincome (taxed at 30%) and the sale proceeds will be taxed at 40%, afterdeducting an indexed cost of RM110.

If the enterprise expects to recover the carrying amount by using theasset, it must generate taxable income of RM150, but will only be ableto deduct depreciation of RM70. On this basis, the tax base is RM70,there is a taxable temporary difference of RM80 and there is a deferredtax liability of RM24 (RM80 at 30%), as in example B.

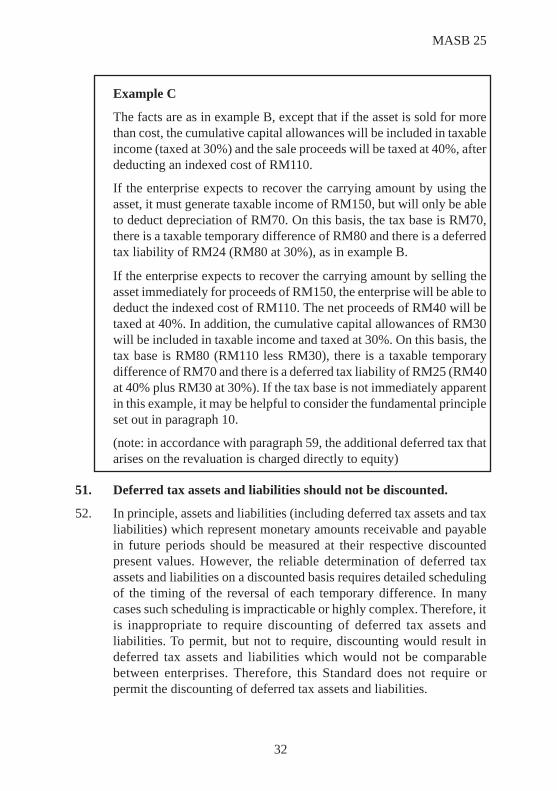

If the enterprise expects to recover the carrying amount by selling theasset immediately for proceeds of RM150, the enterprise will be able todeduct the indexed cost of RM110. The net proceeds of RM40 will betaxed at 40%. In addition, the cumulative capital allowances of RM30will be included in taxable income and taxed at 30%. On this basis, thetax base is RM80 (RM110 less RM30), there is a taxable temporarydifference of RM70 and there is a deferred tax liability of RM25 (RM40at 40% plus RM30 at 30%). If the tax base is not immediately apparentin this example, it may be helpful to consider the fundamental principleset out in paragraph 10.

(note: in accordance with paragraph 59, the additional deferred tax thatarises on the revaluation is charged directly to equity)

51. Deferred tax assets and liabilities should not be discounted.

52. In principle, assets and liabilities (including deferred tax assets and taxliabilities) which represent monetary amounts receivable and payablein future periods should be measured at their respective discountedpresent values. However, the reliable determination of deferred taxassets and liabilities on a discounted basis requires detailed schedulingof the timing of the reversal of each temporary difference. In manycases such scheduling is impracticable or highly complex. Therefore, itis inappropriate to require discounting of deferred tax assets andliabilities. To permit, but not to require, discounting would result indeferred tax assets and liabilities which would not be comparablebetween enterprises. Therefore, this Standard does not require orpermit the discounting of deferred tax assets and liabilities.

33

MASB 25

53. Temporary differences are determined by reference to the carryingamount of an asset or liability. This applies even where that carryingamount is itself determined on a discounted basis, for example in thecase of retirement benefit obligations (see MASB ED 33, EmployeeBenefits).

54. The carrying amount of a deferred tax asset should be reviewed ateach balance sheet date. An enterprise should reduce the carryingamount of a deferred tax asset to the extent that it is no longerprobable that sufficient taxable profit will be available to allow thebenefit of part or all of that deferred tax asset to be utilised. Anysuch reduction should be reversed to the extent that it becomesprobable that sufficient taxable profit will be available.

Recognition of Current and Deferred Tax

55. Accounting for the current and deferred tax effects of a transaction orother event is consistent with the accounting for the transaction or eventitself. Paragraphs 56 to 66 implement this principle.

Income Statement

56. Current and deferred tax should be recognised as income or anexpense and included in the net profit or loss for the period, exceptto the extent that the tax arises from:

(a) a transaction or event which is recognised, in the same or adifferent period, directly in equity (see paragraphs 59 to 63);or

(b) a business combination that is an acquisition (see paragraphs64 to 66).

57. Most deferred tax liabilities and deferred tax assets arise where incomeor expense is included in accounting profit in one period, but isincluded in taxable profit (tax loss) in a different period. The resultingdeferred tax is recognised in the income statement. Examples are when:

(a) interest, royalty or dividend revenue is received in arrears and isincluded in accounting profit on a time apportionment basis inaccordance with MASB 9, Revenue, but is included in taxableprofit (tax loss) on a cash basis; and

MASB 25

34

(b) development costs have been capitalised in accordance withMASB 4, Research and Development Costs, and are beingamortised in the income statement, but were deducted for taxpurposes when they were incurred.

58. The carrying amount of deferred tax assets and liabilities may changeeven though there is no change in the amount of the related temporarydifferences. This can result, for example, from:

(a) a change in tax rates or tax laws;

(b) a re-assessment of the recoverability of deferred tax assets; or

(c) a change in the expected manner of recovery of an asset.

The resulting deferred tax is recognised in the income statement,except to the extent that it relates to items previously charged orcredited to equity (see paragraph 61).

Items Credited or Charged Directly to Equity

59. Current tax and deferred tax should be charged or credited directlyto equity if the tax relates to items that are credited or charged, inthe same or a different period, directly to equity.

60. MASB Standards require or permit certain items to be credited or chargeddirectly to equity. Examples of such items are:

(a) a change in carrying amount arising from the revaluation ofproperty, plant and equipment (see MASB 15, Property, Plantand Equipment);

(b) an adjustment to the opening balance of retained earningsresulting from either a change in accounting policy that isapplied retrospectively or the correction of a fundamental error(see MASB 3, Net Profit or Loss for the Period, FundamentalErrors and Changes in Accounting Policies);

(c) exchange differences arising on the translation of the financialstatements of a foreign entity (see MASB 6, The Effects ofChanges in Foreign Exchange Rates); and

(d) amounts arising on initial recognition of the equity componentof a compound financial instrument (see paragraph 25).

35

MASB 25

61. In exceptional circumstances it may be difficult to determine the amountof current and deferred tax that relates to items credited or charged toequity. This may be the case, for example, when:

(a) there are graduated rates of income tax and it is impossible todetermine the rate at which a specific component of taxable profit(tax loss) has been taxed;

(b) a change in the tax rate or other tax rules affects a deferred taxasset or liability relating (in whole or in part) to an item that waspreviously charged or credited to equity; or

(c) an enterprise determines that a deferred tax asset should berecognised, or should no longer be recognised in full, and thedeferred tax asset relates (in whole or in part) to an item that waspreviously charged or credited to equity.

In such cases, the current and deferred tax related to items that arecredited or charged to equity is based on a reasonable pro rataallocation of the current and deferred tax of the entity in the taxjurisdiction concerned, or other method that achieves a moreappropriate allocation in the circumstances.

62. MASB 15, Property, Plant and Equipment, does not specify whether anenterprise should transfer each year from revaluation surplus to retainedearnings an amount equal to the difference between the depreciation oramortisation on a revalued asset and the depreciation or amortisationbased on the cost of that asset. If an enterprise makes such a transfer,the amount transferred is net of any related deferred tax. Similarconsiderations apply to transfers made on disposal of an item ofproperty, plant or equipment.

63. When an asset is revalued for tax purposes and that revaluation isrelated to an accounting revaluation of an earlier period, or to one thatis expected to be carried out in a future period, the tax effects of boththe asset revaluation and the adjustment of the tax base are credited orcharged to equity in the periods in which they occur. However, if therevaluation for tax purposes is not related to an accounting revaluationof an earlier period, or to one that is expected to be carried out in afuture period, the tax effects of the adjustment of the tax base arerecognised in the income statement.

MASB 25

36

Deferred Tax Arising from a Business Combination

64. As explained in paragraphs 18 and 28(c), temporary differences mayarise in a business combination that is an acquisition. In accordancewith MASB 21, Business Combinations, an enterprise recognises anyresulting deferred tax assets (to the extent that they meet therecognition criteria in paragraph 26) or deferred tax liabilities asidentifiable assets and liabilities at the date of the acquisition.Consequently, those deferred tax assets and liabilities affect goodwillor negative goodwill. However, in accordance with paragraphs 14(a)and 26(a), an enterprise does not recognise deferred tax liabilitiesarising from goodwill itself (if amortisation of the goodwill is notdeductible for tax purposes) and deferred tax assets arising fromnon-taxable negative goodwill which is treated as deferred income.

65. As a result of a business combination, an acquirer may consider itprobable that it will recover its own deferred tax asset that was notrecognised prior to the business combination. For example, the acquirermay be able to utilise the benefit of its unused tax losses against thefuture taxable profit of the acquiree. In such cases, the acquirerrecognises a deferred tax asset and takes this into account indetermining the goodwill or negative goodwill arising on theacquisition.

66. When an acquirer did not recognise a deferred tax asset of the acquireeas an identifiable asset at the date of a business combination and thatdeferred tax asset is subsequently recognised in the acquirer’sconsolidated financial statements, the resulting deferred tax income isrecognised in the income statement. In addition, the acquirer:

(a) adjusts the gross carrying amount of the goodwill and therelated accumulated amortisation to the amounts that would havebeen recorded if the deferred tax asset had been recognised as anidentifiable asset at the date of the business combination; and

(b) recognises the reduction in the net carrying amount of thegoodwill as an expense.

However, the acquirer does not recognise negative goodwill, nor doesit increase the carrying amount of negative goodwill.

37

MASB 25

Example

An enterprise acquired a subsidiary which had deductible temporarydifferences of RM300. The tax rate at the time of the acquisition was30%. The resulting deferred tax asset of RM90 was not recognised asan identifiable asset in determining the goodwill of RM500 resultingfrom the acquisition. The goodwill is amortised over 20 years. 2 yearsafter the acquisition, the enterprise assessed that future taxable profitwould probably be sufficient for the enterprise to recover the benefit ofall the deductible temporary differences.

The enterprise recognises a deferred tax asset of RM90 (RM300 at 30%)and, in the income statement, deferred tax income of RM90. It alsoreduces the cost of the goodwill by RM90 and the accumulatedamortisation by RM9 (representing 2 years’ amortisation). The balanceof RM81 is recognised as an expense in the income statement.Consequently, the cost of the goodwill, and the related accumulatedamortisation, are reduced to the amounts (RM410 and RM41) that wouldhave been recorded if a deferred tax asset of RM90 had beenrecognised as an identifiable asset at the date of the businesscombination.

If the tax rate has increased to 40%, the enterprise recognises adeferred tax asset of RM120 (RM300 at 40%) and, in the incomestatement, deferred tax income of RM120. If the tax rate has decreasedto 20%, the enterprise recognises a deferred tax asset of RM60 (RM300at 20%) and deferred tax income of RM60. In both cases, the enterprisealso reduces the cost of the goodwill by RM90 and the accumulatedamortisation by RM9 and recognises the balance of RM81 as anexpense in the income statement.

Presentation

Tax Assets and Tax Liabilities

67. Tax assets and tax liabilities should be presented separately fromother assets and liabilities in the balance sheet. Deferred tax assetsand liabilities should be distinguished from current tax assets andliabilities.

MASB 25

38

68. When an enterprise makes a distinction between current andnon-current assets and liabilities in its financial statements, it shouldnot classify deferred tax assets (liabilities) as current assets(liabilities).

Offset

69. An enterprise should offset current tax assets and current taxliabilities if, and only if, the enterprise:

(a) has a legally enforceable right to set off the recognisedamounts; and

(b) intends either to settle on a net basis, or to realise the assetand settle the liability simultaneously.

70. Although current tax assets and liabilities are separately recognised andmeasured they are offset in the balance sheet subject to criteria similarto those established for financial instruments in MASB 24, FinancialInstruments: Disclosure and Presentation. An enterprise will normallyhave a legally enforceable right to set off a current tax asset against acurrent tax liability when they relate to income taxes levied by the sametaxation authority and the taxation authority permits the enterprise tomake or receive a single net payment.

71. In consolidated financial statements, a current tax asset of oneenterprise in a group is offset against a current tax liability of anotherenterprise in the group if, and only if, the enterprises concerned have alegally enforceable right to make or receive a single net payment andthe enterprises intend to make or receive such a net payment or torecover the asset and settle the liability simultaneously. However, in theMalaysian tax environment, such a legally enforceable right does notexist. Accordingly, a current tax asset of one enterprise in a group shouldnot be offset against a current tax liability of another enterprise in thegroup.

72. An enterprise should offset deferred tax assets and deferred taxliabilities if, and only if:

(a) the enterprise has a legally enforceable right to set offcurrent tax assets against current tax liabilities; and

(b) the deferred tax assets and the deferred tax liabilities relateto income taxes levied by the same taxation authority oneither:

39

MASB 25

(i) the same taxable entity; or

(ii) different taxable entities which intend either to settlecurrent tax liabilities and assets on a net basis, or torealise the assets and settle the liabilitiessimultaneously, in each future period in whichsignificant amounts of deferred tax liabilities orassets are expected to be settled or recovered.

73. To avoid the need for detailed scheduling of the timing of the reversalof each temporary difference, this Standard requires an enterprise to setoff a deferred tax asset against a deferred tax liability of the sametaxable entity if, and only if, they relate to income taxes levied by thesame taxation authority and the enterprise has a legally enforceable rightto set off current tax assets against current tax liabilities.

74. In rare circumstances, an enterprise may have a legally enforceable rightof set-off, and an intention to settle net, for some periods but not forothers. In such rare circumstances, detailed scheduling may be requiredto establish reliably whether the deferred tax liability of one taxableentity will result in increased tax payments in the same period in whicha deferred tax asset of another taxable entity will result in decreasedpayments by that second taxable entity.

Tax Expense

Tax Expense (Income) related to Profit or Loss fromOrdinary Activities

75. The tax expense (income) related to profit or loss from ordinaryactivities should be presented on the face of the income statement.

Exchange Differences on Deferred Foreign Tax Liabilitiesor Assets

76. MASB 6, The Effects of Changes in Foreign Exchange Rates, requirescertain exchange differences to be recognised as income or expense butdoes not specify where such differences should be presented in theincome statement. Accordingly, where exchange differences on deferredforeign tax liabilities or assets are recognised in the income statement,such differences may be classified as deferred tax expense (income) ifthat presentation is considered to be the most useful to financialstatement users.

MASB 25

40

Disclosure

77. The major components of tax expense (income) should be disclosedseparately.

78. Components of tax expense (income) may include:

(a) current tax expense (income);

(b) any adjustments recognised in the period for current tax of priorperiods;

(c) the amount of deferred tax expense (income) relating to theorigination and reversal of temporary differences;

(d) the amount of deferred tax expense (income) relating to changesin tax rates or the imposition of new taxes;

(e) the amount of the benefit arising from a previouslyunrecognised tax loss, tax credit or temporary difference of aprior period that is used to reduce current tax expense;

(f) the amount of the benefit from a previously unrecognised taxloss, tax credit or temporary difference of a prior period that isused to reduce deferred tax expense;

(g) deferred tax expense arising from the write-down, or reversal ofa previous write-down, of a deferred tax asset in accordance withparagraph 54; and

(h) the amount of tax expense (income) relating to those changes inaccounting policies and fundamental errors which are includedin the determination of net profit or loss for the period inaccordance with the allowed alternative treatment in MASB 3,Net Profit or Loss for the Period, Fundamental Errors andChanges in Accounting Policies.

79. The following should also be disclosed separately:

(a) the aggregate current and deferred tax relating to items thatare charged or credited to equity;

(b) tax expense (income) relating to extraordinary itemsrecognised during the period;

(c) an explanation of the relationship between tax expense(income) and accounting profit in either or both of thefollowing forms:

41

MASB 25

(i) a numerical reconciliation between tax expense(income) and the product of accounting profitmultiplied by the applicable tax rate(s), disclosing alsothe basis on which the applicable tax rate(s) is (are)computed; or

(ii) a numerical reconciliation between the averageeffective tax rate and the applicable tax rate,disclosing also the basis on which the applicable taxrate is computed;

(d) an explanation of changes in the applicable tax rate(s)compared to the previous accounting period;

(e) the amount (and expiry date, if any) of deductibletemporary differences, unused tax losses, and unused taxcredits for which no deferred tax asset is recognised in thebalance sheet;

(f) in respect of each type of temporary difference, and inrespect of each type of unused tax losses and unused taxcredits:

(i) the amount of the deferred tax assets and liabilitiesrecognised in the balance sheet for each periodpresented;

(ii) the amount of the deferred tax income or expenserecognised in the income statement, if this is notapparent from the changes in the amounts recognisedin the balance sheet; and

(g) in respect of discontinued operations, the tax expenserelating to:

(i) the gain or loss on discontinuance; and

(ii) the profit or loss from the ordinary activities of thediscontinued operation for the period, together withthe corresponding amounts for each prior periodpresented.

MASB 25

42

80. An enterprise should disclose the amount of a deferred tax assetand the nature of the evidence supporting its recognition, when:

(a) the utilisation of the deferred tax asset is dependent onfuture taxable profits in excess of the profits arising fromthe reversal of existing taxable temporary differences; and

(b) the enterprise has suffered a loss in either the current orpreceding period in the tax jurisdiction to which the deferredtax asset relates.