Embed Size (px)

Citation preview

LEDGER

NOVEMBER/DECEMBER 2018 Mazars USA LLP is an independent member firm of Mazars Group.

DECRYPTING CRYPTOCURRENCY

TAXES

2 | Mazars USA Ledger

CONTENTS

November/December 2018 | 3

CONTENTS

*The Mazars USA Ledger contains articles and alerts published from October 1, 2018 - November 30, 2018.

4 | Questions Healthcare Companies Should Ask About the Data Driven Revenue Cycle

6 | What’s Broken in Healthcare

8 | Decrypting Cryptocurrency Taxes

12 | Cryptocurrency Attracting the Next Generation of Renters 14 | Lease Accounting for Broker Dealers

19 | Puts on Non-Controlling Interests: What Changes Are Proposed in the FICE Discussion Paper

23 | Healthcare Policy and Procedure Best Practices

26 | FICE Discussion Paper: The Board's Preferred Approach to Classifying Financial Instruments as Liabilities or Equity

33 | Why Provider Organizations Should Be Proponents of Capitation

37 | IFRS Alerts

39 | Real Estate Alert

41 | Tax Alerts

NOVEMBER/DECEMBER 2018

4 | Mazars USA Ledger

QUESTIONS HEALTHCARE COMPANIES SHOULD ASK ABOUT THE DATA-DRIVEN REVENUE CYCLE

A WHILE BACK, WHEN YOU FIRST READ ABOUT THE EQUIFAX CYBER BREACH WERE YOU SURPRISED? IT SEEMED ODD, CON-SIDERING THEY ARE ONE OF THE LARGEST ORGANIZATIONS IN THE BUSINESS OF HOUSING AND SELLING YOUR PERSONAL AND FINANCIAL DETAILS.

I THINK MANY OF US THOUGHT COMPANIES LIKE THEIRS WERE BULLET-PROOF. THERE MAY HAVE EVEN BEEN A CASUAL CONFIDENCE AND ASSUMPTION THAT COMPANIES LIKE THAT WOULD EMPLOY SOME OF THE STRICTEST DATA PROTECTION MEASURES AVAILABLE. THEY WERE ALSO IN THE BUSINESS OF ACCURATELY ANALYZING YOUR FINANCIAL BEHAVIOR.

THE INTEGRITY OF THIS DATA WAS ENORMOUSLY IMPORTANT, CONSIDERING CREDIT MARKETS RELY ON IT TO MAKE SOUND DECISIONS AS TO WHETHER OR NOT YOU ARE LIKELY TO REPAY A DEBT. THIS BREACH CHANGED THE WAY WE LOOK AT OUR OWN IDENTITY PROTECTION AND LESSENED OUR TRUST IN THE BIG THREE REPORTING AGENCIES.

COMPANIES LIKE EQUIFAX DO MUCH MORE THAN ASSIST THE CREDIT MARKETS. THE BIG THREE - EXPERIAN, TRANS UNION AND EQUIFAX - HAVE GROWN TO BE SIGNIFICANT PLAYERS IN THE HEALTHCARE SPACE. THEY ARE DATA PARTNERS SUP-PORTING EFFORTS TO REFINE WORK-FLOW AND REDUCE COSTS TO COLLECT FOR SOME OF THE LARGEST HEALTH SYSTEMS IN THE COUNTRY.

PROVIDERS EMBRACED ANALYTICS THAT PROVIDED THEM WITH INFORMATION REGARDING A PATIENT’S PROPENSITY TO PAY THEIR BILL. THEY EMBRACED HAVING THE ABILITY TO MOVE INDIGENT PATIENTS OUT OF THEIR COLLECTION TEAMS AND STRAIGHT TO PRESUMPTIVE ELIGIBILITY FOR A CHARITABLE WRITE-OFF. EMPLOYING THESE AUTOMATED MANAGEMENT TECHNIQUES MEANT HOSPITALS COULD COLLECT MORE MONEY AT A LOWER COST.

SO WHAT NOW? THERE ARE NUMEROUS QUESTIONS THAT NEED TO BE ANSWERED. WAS YOUR PATIENT DATA PART OF THE BREACH?

BY DOUG BARRY

HEALTHCARE

November/December 2018 | 5

Most likely there won’t be any implications for the majority of providers with the exception of those hospitals that chose to place their patients who failed to pay timely into one of the three credit bureaus with the hopes of securing payment in the future. But what about patients who are processed through the three credit agencies to determine eligibility or the likelihood of paying their debt?

With so many news stories highlighting a solution or protective measure requiring consumers to “freeze” their credit, it begs the question as to what that will ultimately mean for hospitals and physician practices who utilize this data on a regular basis.

How many patients will opt to take this freezing measure? Will this begin to impact the integrity of the financial modeling you apply today? Doesn’t your automated receivable flow for propensity to pay and presumptive charity el-igibility rely on the financial information provided by these credit agencies? It most certainly relies on a large portion of it.

So what is the potential impact on your operations? Will patients who freeze their personal credit files provide you with incomplete or less accurate data on which to base your decisions? Will it simply reduce the number of patients you can automate into a preferred work flow?

One thing is for sure; you need to explore the impact with your current ven-dor, and you need to plan to address it. A significant reduction in available data could ultimately impact your staffing should you begin reverting back to more manual processes when assessing patients’ abilities to resolve their debts.

It is by now clear that we live in an era in which healthcare organizations are forced to allocate valuable dollars away from delivering patient care and towards improving information systems security.

Facilities must invest heavily to protect their patient’s information from be-ing hacked or accessed by an increasing number of outside threats. More and more we read about attacks on healthcare organizations by foreign and domestic cyber criminals.

Those successful in accessing a provider’s system can bring internal op-erations to a grinding halt. Frequently the attack is coupled with a ransom

demand to stop that facility’s information from being made public. The data can contain medical and demographic information including social security and date of birth, which are frequently sold on the black market for profit. IT Security Officers should frequently be at senior management meetings keeping them informed of potential threats and conveying current steps taken to shore-up defenses.

What about the vendors who provide services to the organization? Health-care providers tend to have numerous buyers of products and services in a single organization. Frequently, receivable vendors are engaged without the level of IT scrutiny needed in order to protect an organization from possible threats. When I was in the provider space, I can’t remember ever having to share a desired tool with an IT Security professional before moving forward.

In Revenue Cycle there are numerous technical applications sold on the market intended to help improve financial performance. The contracting phase usually concludes before the IT professionals get an opportunity to dig into the details. Allowing executives to engage vendors without having their IT Security team dictate the strength and minimum standards required for technology invites trouble.

These products are sought after by Revenue Cycle professionals because of their perceived technical superiority when compared to the offerings of most HIS systems. The perception of advanced technical capability often can be misinterpreted by the buyer to mean they have somehow met very stringent security guidelines. It can leave one with a false sense of security. When we perform assessments of clients, we often see these types of con-tracts have not been appropriately vetted. It is essential to have a qualified cyber security expert assess your situation.

Whether you use data to streamline your workflow, technology to enhance performance, or just want to protect patients’ identities from being compro-mised, the need to be more collaborative and to engage in interdepartmen-tal reviews and discussions prior to making any decisions to provide a third party with your data has never been more important.

Doug is a Principal in our New York Practice. He can be reached at 212.375.6558 or at [email protected].

FEATURED GUIDE2018 Tax Planning Guidelines for Individuals and Businesses In 2018, tax planning was significantly impacted by the Tax Cuts and Jobs Act (TCJA), which contains arguably the most sweeping changes in US tax law since the enactment of the Tax Reform Act of 1986. The TCJA has affected many areas of taxation including international tax, individual and business income tax, estate and gift tax, state and local tax, compensation and benefits, and not-for-profit tax. Scan the barcode to view full guide.

6 | Mazars USA Ledger

WHAT’S BROKEN IN HEALTHCAREBY MARK MARTEN

HEALTHCARE

While many in this nation are confused about the direction of healthcare, we look toward the future. Regardless of the design, one thing is clear – we need more accountability in healthcare. There still isn’t a clear understanding of risk-based contracting in the industry. This value-based payment model is inevitable and will ultimately shape the future of health-care in a way that will be mutually beneficial to patients, providers, and payers. So why are the details still so murky, and where does all this trepidation come from?

As with many visionary endeavors, risk-based payment sharing can require heavy collabora-tion, strategic planning, complex contracts, a slow return on investment, and uncertainty in the near term.

Risk Sharing 101Risk-based payments are meant to provide more accountability by requiring providers and hospitals to share in the risk of treating the entire spectrum of a population. Physicians are required to lower costs by providing quality care to reduce utilization, while hospitals must learn to deliver care more efficiently and coordinate with others.

November/December 2018 | 7

MEDICARE LEADS THE WAYOver the last 50 years, we have seen Medicare take the lead on reforming the delivery of healthcare. Some of their initiatives have already succeed-ed and others are still a work in progress. Medicare introduced DRGs to control costs and better manage the episode of care in a hospital by paying a set amount per diagnosis, thereby reducing the hospital’s incentive to extend stays and encouraging them to provide care more efficiently. More recently, Medicare introduced bundled payments to manage the cost of a case from pre-admission through discharge to follow up.

PARTIAL RISKBoth DRGs and bundled payments are examples of partial risk. If the cost of care is higher than the set payment, the hospital and/or provider will take a loss. This arrangement encourages innovation, quality care, and efficiency in order to drive down medical costs and turn a profit. This is in direct oppo-sition to the fee-for-service (FFS) model, which incentivizes a high quantity of care rather than quality. Many believe that FFS withholds and discounts are risk, but they are not. These models have shared savings, not shared risk. However, even these forms of risk are not true risk because they do not account for the total cost of care for a population.

SHARED RISK POOLSThe first step for many health plans has been to set up shared risk pools, wherein groups of physicians with a payment incentive arrangement work with health plans and other providers in the community to manage costs. When they are successful, they have a reserve in the pool attributed to those members. These reserves allow the group to invest in additional services to prevent diseases and better manage chronic conditions.

This limited shared risk arrangement will evolve into taking global risk where the entity is responsible for physician, hospital and other provider costs for the population. Some of the investments that are put into place with these savings are home-based services, chronic care centers, dedicated nurses for case management and coverage of items needed to ensure a healthy population that often require unique services not covered by insurance.

TRUE RISKTrue risk is accountability for the total cost of care for the lifetime of a pop-ulation. Some members are healthy and rarely access care, while others require intense services provided by multiple professionals. We must get to a point where we as collective providers are responsible for the cost of care for an entire population. This can be done through working with a communi-ty and taking on the payment and administration of services.

One successful true risk model is Medicare Advantage, wherein a plan is paid a monthly capitated fee to provide care for its assigned members. This is most often delivered through a network of physicians and providers who are responsible for some or all of the prepaid amount. They must keep the cost of care less than the payment in order to make a margin so they can continue to reinvest in the lifetime care of their patients.

Generally, using the alternative MTM method is more beneficial to a major-ity of taxpayers. It allows taxpayers who failed to make timely elections to utilize the simpler MTM method and avoid being taxed at maximum rates along with an interest charge. Of course, there are instances in which the alternative MTM method may not be the best option. Taxpayers who did not dispose of, or receive, distributions from their PFIC investments, and taxpayers who disposed of PFIC investments at a loss are two examples of situations that call for a further analysis.

DRAWBACKSCommercial Plans are beginning to implement risk-based payments, but a major drawback of following the Medicare Advantage model is that mem-bership changes often in today’s transient society. When the health plan invests heavily in their member’s treatment and the newly healthy patient changes their insurance, this significantly inhibits the plan’s ability to realize an ROI on that treatment. Why invest in the health of a member that will change plans? Without limiting the patient’s choice in health plans, perhaps there could be a risk-sharing arrangement among commercial plans, wherein a small tax is imposed on all commercial premiums that would fund an incentive pool. This would provide value-based payments to health plans when their member leaves after receiving care that substantially improves their health.

NEXT STEPSSharing risk can be complicated and intimidating, but it’s a step in the right direction for the healthcare industry as a whole.

As Medicare and Medicaid push to shift from fee-for-service to value-based care, we should embrace the change and be proactive in taking on this new responsibility. If you need help with risk-based contracting, contact the Mazars Healthcare Consulting Group at mazarsusa.com/hc.

Mark is a Principal in our Los Angeles Practice. He can be reached at 949.584.7247 or at [email protected].

8 | Mazars USA Ledger

FINANCIAL SERVICES

DECRYPTING CRYPTOCURRENCY TAXES LIMITED GUIDANCE ON TAXATION

DESPITE THE BILLIONS OF DOLLARS (WHICH IS PROJECTED TO BE TRILLIONS IN 2018 ACCORDING TO A SEPTEMBER 2018 SATIS GROUP REPORT) FLOWING IN AND OUT OF THE VARIOUS CRYPTOCURRENCIES SUCH AS BITCOIN, ETHEREUM AND LITECOIN, THE UNITED STATES TAXATION OF THESE PRODUCTS IS GOVERNED MOSTLY BY INTERNAL REVENUE SERVICE (IRS) NOTICE 2014-21 ISSUED BACK ON MARCH 25, 2014. WITH REGARDS TO THE NUANCES AND UNCERTAINTIES NOT COVERED BY THE NOTICE, THE IRS HAS CHOSEN TO REMAIN MOSTLY SILENT.

WHAT IS CRYPTOCURRENCY

What is a cryptocurrency? Unlike United States Dollars, British Pounds or Euros, cryptocurrencies only exist in the virtual universe, meaning there is no tangible paper bill or metal coin that can be physically touched. Nor are they considered legal tender. Instead the Internet and only the Internet is used to transfer Bitcoin or Ethereum tokens from their originators to every subsequent owner. A price is set at an Initial Coin Offering (ICO) or Initial Public Coin Offering (IPCO) and then trading begins in the virtual universe. This is done through a secure Internet portal account sometimes called a coin wallet.

A register, accessible to all owners extemporaneously, tracks everyone’s ownership and is called a blockchain. This register is updated every time ownership changes. The details of your ownership represented in this blockchain that all others can see is sometimes called your public key. Access to spend any of your cryptocurrency in your coin wallet is provided by a private key. This private key is a long list of numbers and letters which needs to be kept secure to prevent losing access.

There are three types of cryptocurrency tokens generally – utility, security and payment:

§ Utility or user tokens enable the holder access to a future service being developed – Filecoin, Flipcoin and Storj are examples.

§ Equity security tokens are similar to stock shares in that they carry an ownership element, may have voting rights and can earn “dividends.” Digix is an example. Debt security tokens act as short-term loans to a company and earn the equivalent of interest – Steem utilizes such a scheme.

§ Currency or payment tokens are used as their name implies – Bitcoin, Litecoin, ZCash and Monero are examples.

HOW CRYPTOCURRENCY IS EXCHANGED

Cryptocurrencies can be exchanged in a few ways. They can be sold for cash on certain websites that act as exchanges such as Coinbase, Bitstamp or Kraken. They can be exchanged for other types of cryptocurrency on sites such as Shapeshift. They can be sold directly to another person at a price you set that is accepted on sites such as LocalBitCoins or BitQuick. They can even be converted to a local currency and withdrawn from an ATM at places found on Coinatmradar.

For investors not wanting to own cryptocurrencies directly or wanting to use a manager to invest in them, options have begun to open up. Privately traded partnerships such as hedge funds or private equity funds have begun to trade in cryptocurrencies and offer investors access to their appreciation (or depreciation) through the private placement of these partnership interests.

Coinbase’s institutional arm has been approved as a qualified custodian by the state of New York and BitGo by South Dakota. This license allows them to securely hold deposits of cryptocurrencies much like a bank account.

ORIGINS

Fluctuations in cryptocurrency value depend mostly on people’s perception of the value and are not necessarily tied to anything – such as earnings of a company, the value of gold or what your dog wants for breakfast that morning. Their creation came from a desire to allow fast, better secured, less costly transfers of value between consumers and producers without

BY GREGORY KASTNER

November/December 2018 | 9

the use of bank accounts or credit cards. Ability to avoid use of trusted intermediaries while retaining anonymity was also coveted.

Ideally, they would be immune to fluctuations in just one country’s currency and to counterfeiting or theft. Obviously, as the market has grown and speculators have stepped in, cryptocurrency’s utility has increased from a way to pay for goods or services to also an avenue for speculative investment. Because of the sometimes extreme volatility in values created by these speculative investments, some merchants or individuals won’t accept these highly fluctuating cryptocurrencies in lieu of more traditional forms of payment.

Cryptocurrencies are generally taxed in one of two ways, depending on how they were acquired. One area the IRS has not addressed is whether their use affects their taxation as well.

MINING CLASSIFIED AS A U.S. TRADE OR BUSINESS

When involved in the “mining” or creating of cryptocurrencies, the taxpayer could be considered as engaged in a trade or business. The implications of such can be significant. Income generated from a United States (U.S.) based trade or business is generally Effectively Connected Income (ECI) – that is, U.S. sourced and subject to federal tax withholding if any profits flow through a partnership or joint venture to a foreign entity or individual.

If a partnership interest involved in producing such income is sold, the proceeds would also be subject to withholding under the new Tax Cuts and Jobs Act (TCJA) changes to Internal Revenue Code (IRC) §864 and §1446 taking effect in 2018. Such income will presumably also be treated as subject to self-employment tax under IRC §1401 if not received by an incorporated entity. If any of the income flows to a pension plan, charity or IRA account, it could also create an unexpected tax liability as this income

10 | Mazars USA Ledger

FINANCIAL SERVICES

will also be classified as Unrelated Business Taxable Income (UBTI) under IRC §512.

For amounts flowing to an individual, such income would be treated as ordinary income and not receive any preferential tax rate such as those available to long term capital gains or qualifying dividends. A limited partner would classify such income as passive under IRC §469 and generally avoid paying self-employment tax on any profits. General partners and limited liability company (LLC) managing members would receive non-passive income subject to the self-employment tax. If the self-employment tax element is a concern, structuring the entity as a limited partnership (LP) instead of as an LLC might be preferable. By statute, limited partners in an LP are not subject to the self-employment tax. LLC members are not distinctly protected by that same statute.

Another possible unexpected consequence of “mining” is that such income could also be classified as state-sourced and have state income taxes and withholdings due. If where customers reside and where the “mining” is done differ, different states’ sourcing rules could possibly subject more than 100% of the income to state income tax as there is not universal uniformity across states with regards to such rules.

Cryptocurrency is not tangible personal property nor is it services and so its sale would not incur sales or use tax as would be due in other retail businesses.

MINING CLASSIFIED AS A HOBBY

If the “mining” of a cryptocurrency does not rise to the level of a trade or business, the IRS could argue any losses incurred should be classified as hobby losses under IRC §183 and not be allowed. Generally, a good faith expectation of profit governs such classification. Usually, a single occurrence does not rise to the level of trade or business.

HELD FOR INVESTMENT

If the taxpayer is not “mining” and only involved in buying and selling cryptocurrency created by others, it is treated as an investment in property. As such, gain or loss is treated as capital in character. For individuals, if it is held one year or less, it is treated as short term capital gain or loss and long term if held longer.

Under the TCJA, long term capital gains carry a maximum federal rate of 20% and short-term capital gains carry a maximum federal tax rate of 37%. Only $3,000 of capital losses in excess of capital gains are allowed to an individual per year and any of these unused losses can be carried forward indefinitely. Such income is also net investment income for purposes of the 3.8% tax on individuals with modified adjusted gross income over $200,000 ($250,000 for married couples filing jointly).

For corporations, no capital losses in excess of capital gains are allowed and there is not a different federal income tax rate for long term versus short term. With some restrictions, capital losses may be carried back three years for corporations and forward only 5 years, dissimilar to the rules for individuals.

Under the TCJA, however, corporations are subject to a maximum federal tax rate of only 21%. In the past, long-term investments were probably held at the individual level because of the tax rate differential providing a more beneficial answer. Now, if long-term investments’ appreciation help fund a business, it may make more sense to leave them in a corporation. Most states do not have a different rate for capital versus other types of income.

Such capital gains or losses on sales of cryptocurrency are presumably portfolio and not passive for purposes of limited partners in a fund that invests in cryptocurrency. As such, income would not be able to be offset against other passive losses such as from a real estate limited partnership interest.

Presumably, if one were to buy and sell cryptocurrency continually throughout the year, losses would be subject to the wash sale rules under IRC §1091. Different types of cryptocurrency probably would not be treated as “substantially identical” for this section but if such a trading strategy were employed, these rules need to be considered.

To avoid having to analyze the historical trading for purposes of such tracking, could the Bitcoin or Ethereum be treated as a security and be eligible for the mark-to-market rules of IRC §475(f) if a timely election is made? Since cryptocurrencies are not traded on what is defined as a qualified exchange at this time, presumably they would not be eligible for IRC §1256 mark-to-market treatment as 60% long term capital gains/losses and 40% short term capital gains/losses. Cryptocurrency does not create foreign currency gains or losses as defined by IRC §988.

Shorting a cryptocurrency (borrowing with the promise to repurchase in the future in the hopes the value will drop) would also require looking at the straddle rules of IRC §1092.

Debt tokens, presumably, would be subject to the market discount and original issue discount rules of IRC §1276 and §1272. Some of the gains might need to be reclassed as ordinary income or a current inclusion of income might be required depending on the interest actually paid.

After the TCJA took effect at the beginning of 2018, only exchanges of real property are eligible for a tax-free exchange under IRC §1031. Prior to the new tax law, this was uncertain as the law did not specify real property, but only property.

Expenses attributable to the trading or investing in Bitcoin as an investment

November/December 2018 | 11

would be subject to the same rules as investing in other securities, i.e. either being classified as an “above-the-line” ordinary deduction or as a miscellaneous itemized deduction whose benefit was eliminated for individuals by the TCJA. For corporations and PFICs, there is no such limit on these expenses and they are essentially treated as deductible expenses.

ASSIGNMENT OF BASIS FOR SALES AND FORKS

In terms of which layer is sold and how to assign a tax basis to such layer held for investment, the default method for sales of stock under Treasury Regulation §1.1012-1 would be first in, first out (FIFO). However, the option to identify the highest priced layer as being sold first is allowed. Such identification must be made at the time of the sale. Despite the regulation referring to sales of stock, many practitioners are applying these rules to cryptocurrency because of the similarities and not the average cost method available to holders of mutual fund (Regulated Investment Company) shares. No Form 1099s are currently issued from cryptocurrency operators, so the taxpayer would have to track the various layers and tax basis of each layer.

Another area of uncertainty with regards to tax treatment is that of forks of cryptocurrency (such as Bitcoin Cash for holders of Bitcoin). Forks generally occur when there is a change in the software that cryptocurrency miners use, sometimes because of a dispute, and owners of the current cryptocurrency receive new keys that give them value on a new blockchain.

Should this transaction be treated the same as a stock split and just some of the cost basis assigned proportionately to it? Is no basis assigned under the argument that no ascertainable value exists for the new cryptocurrency? Is income recognized to the extent that the new fork has a market value? If the old cryptocurrency is eliminated, is this some sort of tax-free exchange similar to those offered for stock under IRC §368, even if this does not all happen all at once? On these questions, the IRS has so far remained silent. However, there is a Supreme Court case from 1955, Commission vs. Glenshaw Glass Co. that many practitioners site as perhaps the governing doctrine.

According to the case, when a taxpayer receives undeniable accessions to wealth, clearly realized, and over which the taxpayer has complete dominion, a recognition of income must occur. If the new cryptocurrency, the fork, has value and can be traded without hindrance immediately, it appears there could be a taxable event upon the fork.

Unlike a stock split where the price has just been altered per share, something new has been created: a new cryptocurrency. If, however, a value cannot be placed on the fork or it cannot be traded now or with any definite timeframe in the future, it may not have to be recognized as income today. The IRS, however, is generally not too keen on deferrals of what they deem to be income and so these restrictions would have to have merit.

Regardless, forks have not been directly addressed by the IRS and so either approach is not definitively correct and each case should be analyzed individually.

USED TO PAY PERSONAL EXPENSES

What if cryptocurrency is directly used to pay for personal expenses? A gain or loss might be incurred. If it’s a loss, the taxpayer would have to argue that the cryptocurrency was held for investment and then a capital loss could be recognized. Personal-use asset losses are not deductible – such as losses on sale of a car or a personal residence like a house or boat.

If it’s a gain, the taxpayer would be required to recognize the gain under IRC §61. Failure to report such a gain could extend the statute of limitations from the normal three years the IRS has to assess additional tax to 6 years if the excess is substantial. Substantial is defined in this context as over 25% of gross income for the year. Some states extend the statute even longer than the federal government. If the omission is deemed fraudulent, however, there is no time limit.

If cryptocurrency is received for services as an employee, income still needs to be recognized for income tax purposes and all required payroll taxes paid by the employee and employer.

REQUIRED DISCLOSURES

Besides properly reporting the income tax consequences of any cryptocurrency transaction, any direct or indirect holdings of cryptocurrency could potentially be subject to information reporting as well. The filing requirements of Form 114, Report of Foreign Bank and Financial Accounts or the so-called FBAR, and Form 8938, Statement of Specified Foreign Financial Assets should both be considered if the cryptocurrencies are held by an offshore vehicle or held in an offshore coin wallet. Failure to file these forms in some cases can be argued as willful and the penalties severe.

Owners of cryptocurrency also need to comply with the Anti-Money Laundering rules initiated by the Bank Secrecy Act of 1970 and possibly file Currency Transaction Reports or Suspicious Activity Reports. All carry stringent recordkeeping requirements.

While there is a lack of specific guidance on the taxability of cryptocurrencies, the proper treatment and consequences can be extrapolated from other sources in most examples. Proper disclosures should be considered to prevent possibly severe penalties for non-compliance.

Gregory is a Director in our New York Practice. He can be reached at 212.375.6583 or at [email protected]

12 | Mazars USA Ledger

CRYPTOCURRENCY ATTRACTING THE NEXT GENERATION OF RENTERS

BY BISNOW, SPONSORED BY MAZARS

Tenants are beginning to pay their rent via a new type of currency.

Bitcoin, Ethereum and other cryptocurrencies have taken the business world by storm over the past year as new forms of payment that run on blockchain technology. Now, landlords and property managers are getting a piece of the pie by incorporating the

emerging trend into their operations to attract and retain a new generation of tenants.

"Our buyer has evolved, they've moved from mom and pops to young people who want to pay with various forms of payment," Magnum Real Estate Group President Ben Shaoul said to CNBC. "Cryptocurrency is something that has been asked of us — 'Can you take cryptocurrency? Can we pay that way?' — and of course when somebody wants to pay you with a different form of payment, you're going to try to work with them and give

them what they want, especially in a very busy real estate market."

REAL ESTATE

November/December 2018 | 13

Shaul is among several owners and developers that believe offering cryptocurrency payment plans will give them an edge over their competition. The real estate industry is constantly looking for new ways to connect with an increasingly millennial

customer-base, and Bitcoin is one way to help them bridge this gap.

As the first generation to grow up using digital technology for everything from hailing a cab to ordering food, millennials have become accustomed to paying for things on their devices. They have embraced emerging technology to make their lives easier, and blockchain is the most recent example.

“Millennials are particularly open to embracing new technology in order to create opportunities for themselves--and blockchain, the tech behind crypto, is no different,” blockchain startup StormX CEO Simon Yu said to Forbes. “As masters of the side hustle and challengers of the traditional 9-5 working lives of previous generations, millennials are welcoming blockchain with open arms.”

Property managers who accept payments in cryptocurrency have two options. They can either keep the payment in the form of cryptocurrency and use it to pay for something else, or they can convert it into dollars. If they opt to convert the payment, it is important to know when to do so. Bitcoin fluctuates significantly in valuation, reaching $20K at the end of 2017 and beginning 2018 at a mere $14K. Today, it has dropped to almost half of what it was a year ago, but that number could change in a matter of days. Landlords and property managers who decide to convert cryptocurrency need to be strategic about when they cash in to ensure they are getting the most bang for their buck.

PropTech companies are also getting in on the action. ManageGo, a Brooklyn-based company that provides a platform for renters to make online payments, now gives tenants the option to make payments using Bitcoin

via the company’s app. When a tenant makes a payment using Bitcoin, ManageGo converts the currency into dollars. This allows tenants to pay the way they want, and landlords to receive payments the way they want.

“Industry players are starting to realize that there is major potential for blockchain technology to challenge the status quo above and beyond accepting cryptocurrency as a form of payment or executing transactions," Mazars USA Digital Asset Group Leader Andre Sterley said. "Other areas being targeted include title management, tokenized ownership and automation through the use of smart contacts around payment and agreements.”

Still, many industry professionals are reluctant to adopt the trend. There is still a stigma around cryptocurrency because it is so new.

"Currently we have had zero interest in paying rent through bitcoin," The Bozzuto Group CEO Toby Bozzuto said to CNBC. "You don't know who owns it, and that's the knock on it. It's been considered black market with a dirty reputation.”

Time will tell whether cryptocurrency will continue to transform the commercial real estate landscape, but all signs are pointing up. Slowly but surely, property managers are adopting these new payment methods into their business model. As the next generation of tenants becomes more acquainted with the use of cryptocurrency as a payment method, property managers are making changes to meet their demands.

This feature was produced in collaboration between Bisnow Branded Content and Mazars. Bisnow news staff was not involved in the production of this content.

Andre is the Digital Asset Group Leader in our New York Practice. He can be reached at 212.375.6629 or at [email protected]

FEATURED VIDEO

Women@Mazars - Good Day To Be Visible featuring Chelsey Trevino and Lisa Osofsky

Welcome to our latest installment of Be Visible! We are taking the conversation outside with intimate one-on-one conversations with our women leaders over coffee and tea at some of NYC's trendiest spots. Our "Good Day To Be Visible" video features Partner Lisa Osofsky interviewing Senior Manager Chelsey Trevino as they discuss the many components of visibility and what drives them to make an impactful change.Scan the barcode to watch our video.

14 | Mazars USA Ledger

FINANCIAL SERVICES

Broker dealers get ready! The Financial Accounting Standards Board’s (FASB) long-anticipated update to lease accounting, Accounting Standards Update No. 2016-02, Leases (Topic 842) (ASC 842), becomes effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. ASC 842 will have a significant impact on most broker dealers’ financial statements and disclosures. If you have not begun the analyses necessitated by ASC 842, there is no time like the present!

BY CHARLES PAGANO, BONNIE MANN FALK AND JASON GUTMAN

LEASE ACCOUNTING FOR BROKER DEALERS

November/December 2018 | 15

The required transition disclosures included in the 2018 financial statements need to reflect the effect on the company’s financial reporting with execution beginning in the January 2019 FOCUS report. While the implementation will require broker dealers to

analyze their leases and recognize potentially material assets and liabilities on the financial statements and increase related disclosures, there is good news in that generally the effect on net capital and aggregate indebtedness should be minimal.

WHAT ARE THE MAJOR IMPACTS?

Lessees need classify their leases as either finance or operating; each classification has its own unique accounting treatment. Finance leases cover arrangements that transfer control of assets at the end of their term, include purchase options, cover most of an asset’s useful life, or involve highly specialized assets. These leases have been previously required to be recorded on the financial statements.

Conversely, operating leases do not transfer ownership at the end of the lease, do not include purchase options, have a lease term as part of the economic life, and do not have assets specialized to the use of the lessee. The Implementation Guidance of the standard (ASC 842-10-55-1) includes a decision tree to assist in the classification. In the broker dealer world, much of leasing transactions expect to be classified as operating leases.

Under the existing guidance, lessees recognize the expense of an operating lease ratably over its life. This “straight line” approach results in a more consistent bottom line. Moving forward, in addition to reporting a straight-line lease expense in their financial results, lessees will need to recognize an asset and a corresponding liability on their balance sheet. One of the most significant sources of lessees’ off-balance sheet financing and risk is now front and center in their financial statements, no longer solely delegated to a footnote disclosure.

Initially, the balance sheet gets grossed up to reflect a liability equal to the present value of the lease payments with a corresponding asset, now known as the “right of use” (ROU) asset, which results from a contract which conveys the right to control an “identified asset” for a period of time in exchange for consideration. Most commonly, in the broker dealer industry, the new standard calls for recording assets and liabilities related to the following leases for the use of:

§ Office rent § Trading, communication and information systems equipment § Offsite document storage § Software solutions for case management, billing, and compliance

One would have to be mindful whether a lease or service contract exists when analyzing the transaction. ASC 842 could affect those situations where

expense sharing or an administrative service agreement exists.

When determining the payments to be included in measuring the ROU assets and lease liabilities, one must consider all optional payments related to the lease. Payments to be made during an option period would be included only if the lessee is reasonably certain to exercise an option to extend or not to terminate a lease. Optional payments to purchase the assets at the end of the lease would be included only if the lessee is reasonably certain to exercise that purchase option. Options to extend or not to terminate that are controlled by the lessor need to be considered as well.

Keep in mind, the nature of lease payments impacts the broker dealer’s balance sheet. Variable lease payments are not included in the measurement of a lease liability and ROU, since this liability is not fixed. Common examples of variable lease payments include rental increases based on CPI or inflation rate.

In both examples, the tenant’s initial base rent may be the only payment which, in substance, is fixed. These variable payments can increase or decrease over time and cannot be estimated. Broker dealers may seek to negotiate greater variable terms in their lease payment structure to take advantage of this accounting treatment.

WHAT ABOUT NON-LEASE COMPONENTS?

Many lease arrangements cover services provided by the landlord, such as janitorial, common area maintenance, or onsite IT support. These typically meet the definition of a “non-lease component,” since they do not grant the lessee control over an asset. Lessees must assign a value to non-lease components based on their relative standalone prices or apply a practical expedient electing to account for the lease and non-lease components as a single liability. Performing an allocation may be time consuming, but applying the practical expedient may result in a significantly greater balance sheet obligation and related asset.

TYPICAL EXAMPLE

Let’s take a typical situation in a broker dealer with an operating lease scenario. Assume the broker dealer rents office space for a three-year period with total lease payments over 36 months of $ 36,000 with lease payments of $10,000, $12,000 and $14,000 for each year respectively. Assume a present value (“PV”) factor of 4.24% and no lease escalations. The lease payments and present values of the payments are as follows:

16 | Mazars USA Ledger

FINANCIAL SERVICES

As payments are made the lease liability is decreased as follows:

Each year the periodic lease expense is recognized using the average lease payment over the life of the lease. The difference between the lease payment and the lease expense is recorded to adjust the ROU asset. See the table and journal entries as follows:

November/December 2018 | 17

The financial statement impact over the lease term is as follows:

WHAT ABOUT DISCLOSURES?

ASC 842 brings about new disclosures related to leases in order to provide users of the financial statement appropriate information to assess the amount, timing, and uncertainty of cash flows arising from leases. Amongst the highlights of the quantitative and qualitative information to be disclosed include, but are not limited to:

§ The Company’s leases o A general description of the leases o Basis, terms, and conditions on which carriable lease payments are determined o Existence, terms, and conditions of all options to extend or terminate a lease (whether or not they are recognized as part of the ROU asset or lease liability) and any residual value guarantees provided by the leases o Any restriction or covenants imposed by leases o Leases between related parties o Relevant information on short term leases

§ Significantassumptionsandjudgementsmade, including but not limited to: o Determination if a contract contains a lease o Allocation of consideration in a contract between lease components and nonlease components and the detail of any election of using a practical expedient o Determination of the discount rate for the lease

§ Amountsrecognizedinthefinancialstatements relating to those leases o Operating lease cost o Short-term lease cost, excluding expenses relating to leases with a lease term of one month or less o Variable lease cost

o Amounts segregated between those for finance and operating leases for the following: • Cash paid for amounts included in the lease liabilities • Supplemental noncash information on lease liabilities arising from obtaining right-of-use assets • Weighted-average remaining lease term (see the implementation guidance) • Weighted-average discount rate (see the implementation guidance) o Five year and beyond annual undiscounted cash flow maturity analysis of its finance lease and operating lease liabilities separately, including a reconciliation of the to the lease liabilities recognized in the balance sheet.

SEC NO ACTION LETTER OF OCTOBER 23, 2018 The SEC recognized the possible disastrous results on net capital and addressed the effect of ASC 842 two years ago. In a letter to SIFMA, from the SEC on October 23, 2018, the SEC rescinded a previously issued letter dated November 8, 2016. Both letters granted relief to broker dealers whereby an operating lease asset can be added back to net capital to the extent of the associated operating lease liability.

Additionally, the Division per the “No Action” letter “will not recommend enforcement action, if a broker-dealer determining its minimum net capital requirement using the AI (aggregate indebtedness method) does not include in its aggregate indebtedness an operating lease liability to the extent of the associated operating lease asset.” The SEC went on to comment that each lease stands on its own; that is, one cannot offset an operating lease asset on one lease with an operating lease liability of another lease.

18 | Mazars USA Ledger

REAL ESTATE

UPCOMING WEBCASTS

We are pleased to announce our Mazars Online Insights webcasts! These informative sessions, led by our service line and industry segment leaders, are designed to educate our connections on the latest developments in the accounting industry and the technical resources needed in today’s business environment. Scan the barcode below to view the 2018/2019 schedule and register!

JANUARY 16TH

Identifying Performance Obligations under ASC 606Time: 12:00 – 1:00 PM EST Speakers: Mike Crown and Ayal Cohn

Are You Ready For Year-End Planning? Everything You Need To Know For Year-End 2018 And BeyondTime: 12:00 – 1:00 PM EST Speakers: Chimudi Egbuna, Sheila Grice and Azmat Hussain

DECEMBER 12TH

Also remember that the amount of the asset may reflect additional costs such as direct initial costs, prepaid lease payments and lease incentives which will cause the asset to not equal the liability.

WHAT ARE THE STEPS TO IMPLEMENTATION?

§ Gather and catalog your current inventory of leases, store lease data in a centralized repository.

§ Design and implement a new lease accounting process to manage your organization’s lease data.

§ Select a software solution that will support your organization’s adoption of the new lease accounting standards, and ongoing lease monitoring and maintenance. In the case of minimal leases Microsoft Excel may suffice.

§ Compute the amount of the asset and liability and be ready to book for those with calendar years beginning on January 1, 2019.

§ Fully train staff on new software solution, design and implement internal controls.

§ Determine the effect on net capital, if any.

With yearend fast approaching now is the time to assess the effects of ASC 842. Companies need to be ready for 2018 transition disclosures and January reporting for your FOCUS filings. You want to implement processes and establish internal controls to capture the necessary data in your books and records and for disclosure in the notes to the financial statements.

The standards include comprehensive guidance to assist companies in applying the requirements of ASC 842. Once an entity completes its analyses, communication between the auditor and management ensures a smooth transition to a successful implementation.

Charles is a Partner in our Long Island Practice. He can be reached at 516.620.8553 or at [email protected].

Bonnie is a Director in our Long Island Practice. She can be reached at 516.620.8554 or at [email protected].

Jason is a Manager in our New York Practice. He can be reached at 646.225.5992 or at [email protected].

November/December 2018 | 19

PUTS ON NON-CONTROLLING INTERESTS:

WHAT CHANGES ARE PROPOSED IN THE FICE DISCUSSION PAPER?

IFRS

20 | Mazars USA Ledger

IFRS

FOLLOWING ON FROM OUR ‘A CLOSER LOOK’ FEATURE ON THE FINANCIAL INSTRUMENTS WITH CHARACTERISTICS OF EQUITY (FICE) DISCUSSION PAPER IN THE JULY-AUGUST ISSUE OF BEYOND THE GAAP, THIS MONTH’S FEATURE WILL LOOK SPECIFICALLY AT PUT OPTIONS GRANTED TO MINORITY SHAREHOLDERS (‘PUTS ON NON-CONTROLLING INTERESTS’). 1. How did the current accounting treatment come about?

When IFRS standards were first implemented in 2005, they did not yet include provisions on changes in percentage holdings in a subsidiary, and the requirement to immediately recognize a liability for their obligation to buy back equity instruments in the future came as a surprise to French companies.

IAS 32 required (and still requires) that put options granted to minority shareholders should be recognized as liabilities at the present value of the strike price of the put option but did not give any further guidance on the contra journal entry. This has resulted in diversity in practice, both at the date of initial recognition and subsequently.

At initial recognition, entities have generally chosen one of two approaches, both of which anticipate the eventual buyback of the shares by the entity:• an approach that involves recognizing an additional goodwill for the

difference between the liability and the value of the shares likely to be repurchased; or

• an approach that involves recognizing the difference in group equity, on the assumption that this is permissible in the absence of any clarifications to the contrary.

Similarly, a variety of different accounting methods have been used for subsequent changes in the value of the liability:• recognition in profit or loss, based on the general assumption that

changes in the value of a financial liability have an impact on profit or loss;

• recognition in equity, based on the argument that an obligation relating to own shares should not have an impact on profit or loss (particularly if the strike price depends on the fair value of the underlying shares, which is quite often the case); or

• recognition in goodwill using the ‘partial goodwill’ method, which is consistent with the approach mentioned above that anticipates the buyback of the shares (all other things being equal).

The French Securities Regulator, the AMF, noted this diversity in practice, stating in its 2005 year-end recommendations that entities should give details of the accounting treatment used at initial recognition of the liability and for subsequent changes in its value.

The IFRIC (now the IFRS IC) also tackled the issue, trying to reach a

consensus but failing. Consequently, it decided in 2006 not to add the topic to its agenda.

In 2008, phase II of the Business Combinations project brought us a step further towards the current accounting treatment for puts on non-controlling interests, by reducing the number of permitted approaches. After this, IAS 27 was amended to stipulate that the impact of changes in percentage holdings in subsidiaries should be recognized in equity.

Logically, following these amendments, the AMF’s year-end recommendations for 2009 clarified that the use of the ‘partial goodwill’ method at initial recognition could still be retained for existing puts, but would no longer be permissible for new put issues. The AMF also stated that its preferred approach for subsequent changes in the value of the liability was recognition in equity, rather than in profit or loss; however, both approaches were still permissible.

In March 2011, the IFRIC tried to resolve the practical issues submitted to it by proposing to exclude put options written on non-controlling interests of subsidiaries, to be settled by the physical delivery of shares, from the scope of IAS 32. This would have meant that these puts would be accounted for under IAS 39 (now IFRS 9) in line with all other derivative instruments, i.e. at fair value through profit or loss.

A few months later, in September 2011, this proposal was rejected by the IASB.

The IFRIC continued its discussions on the subject and in March 2012 it published a draft interpretation that would require subsequent changes in the value of the liability to be recognized in profit or loss.

In January 2013, after receiving comments on the draft interpretation, the IFRIC stated that the draft was a correct interpretation of the existing standard (and specifically of paragraph 23 of IAS 32) but that it remained convinced that its proposal from March 2011 – that these put options should be accounted for like any other derivative – would provide better quality financial information. With this in mind, the IFRIC asked the IASB to reconsider its position on paragraph 23 of IAS 32.

In March 2013, the Board responded by cancelling the IFRIC’s draft interpretation, putting a halt to its efforts to clarify the issue.

Since then, the IFRS IC has still not reached a conclusion, despite receiving further requests for clarification, particularly as regards the accounting treatment of written put options to be settled by a variable number of the parent company’s shares (in 2016). The IFRS IC noted at the time that the issue was too broad for it to address, and that the Board’s ongoing work on the FICE project could provide some answers.

November/December 2018 | 21

Against this background, this summer’s FICE Discussion Paper (DP) proposes a new approach for determining what shall be classified as a liability, applicable to both derivatives and non-derivative instruments. Here, we analyzes the potential repercussions of the DP.

2. What does the FICE DP say about puts on non-controlling interests?

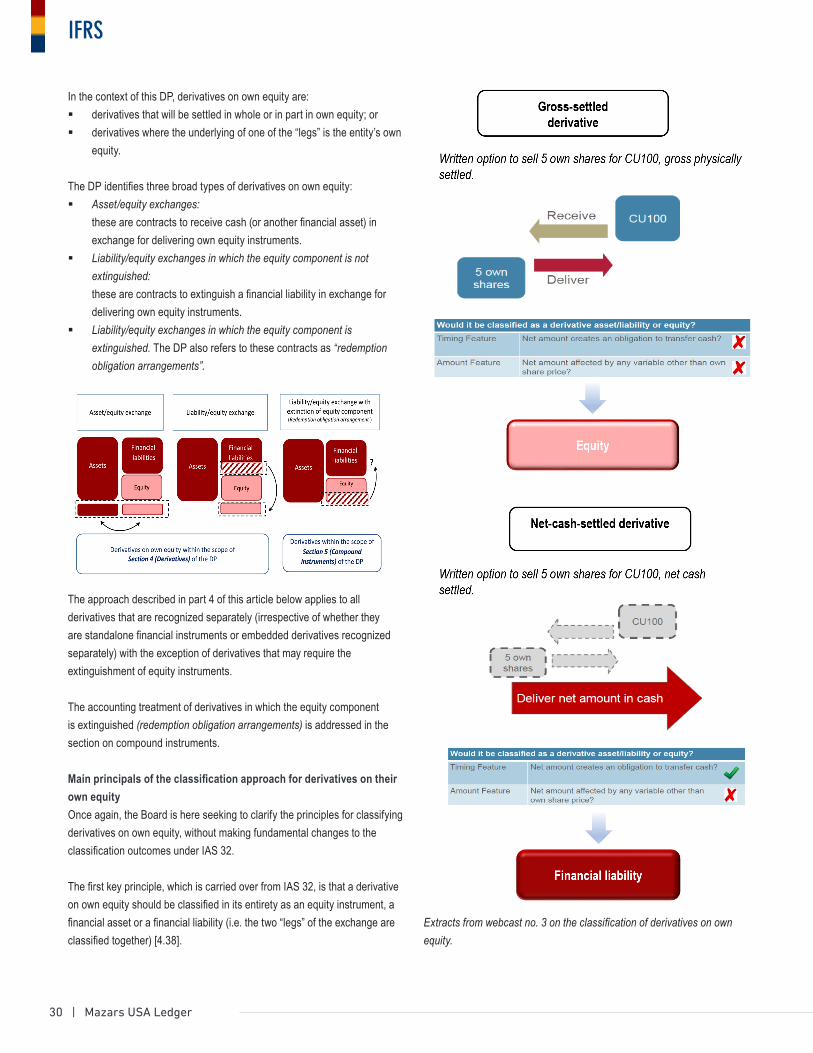

Let’s begin with a reminder of the Board’s preferred approach: an instrument would be classified as a liability if a) the entity has an obligation to transfer economic resources before liquidation (timing feature) or b) the entity has an obligation to transfer an amount independent of the entity’s economic resources (amount feature).

In addition, the Board is proposing a specific accounting treatment for derivatives that are physically settled in the entity’s own shares (meaning they are extinguished in accounting terms). Under the proposed accounting treatment, written put options would be classified together with the underlying own shares as a single transaction.

Thus, in the case of puts on non-controlling interests (NCI puts), the Board notes that the entity faces two potential outcomes:• either the minority shareholders exercise their put options and the

entity is obliged to repurchase its own shares at the price agreed in the contract, resulting in the extinguishment of its own shares;

• or the minority shareholders do not exercise their put options and the shares are not extinguished.

In this case, as the exercise of the puts is at the option of the minority shareholders, it is possible that the entity will have an obligation to transfer economic resources before liquidation. Under the Board’s preferred approach, this would mean that the instrument meets the criterion for the timing feature, and thus should be recognized as a liability. The contra journal entry for the liability would be the extinguishment of the shares held by the non-controlling interests, at the date when the entity issues the put options.

The Board proposes that the existence of NCI puts should be viewed in the same way as a bond convertible to own shares, as both have the same outcomes: either an obligation to transfer economic resources, or own shares still outstanding. The Board believes that this justifies using the same accounting treatment. It should however be noted that this approach ignores one difference: the shares already exist in the case of shares + NCI puts, but are yet to be issued in the case of convertible bonds.

Having looked at the accounting treatment at initial recognition, how should an entity account for subsequent changes in the value of the liability it has recognized? It is interesting, in the light of the past discussions reviewed above, that the Board is proposing that they should by default be booked to profit or loss.

However, the Board has also introduced a new presentation requirement. Liabilities that do not meet the criterion for the amount feature (i.e. the amount transferred is dependent on the entity’s economic resources) are to be presented separately in the balance sheet. Subsequent changes in the value of these instruments would then be recognized in other comprehensive income (OCI) without recycling to profit or loss.

The Board suggests that the separate presentation principle should be applied consistently to derivatives that do not have an underlying variable that is independent of the entity’s economic resources (with the exception of interest rates, which by definition affect all derivatives, and foreign currency exposures under certain circumstances).

Thus, if an entity issues put options on its non-controlling interests with a strike price equal to the fair value of the shares, the separate presentation requirement would de facto apply.

The accounting treatment would thus be as follows:• at the date when the puts are issued, the entity recognizes a liability

for the fair value of the shares (the strike price of the puts) with a contra journal entry for an equivalent reduction in equity. The liability is presented separately in the balance sheet;

• subsequent changes in the share price will require the entity to remeasure the liability, with a contra journal entry as a separate line item in OCI (not recyclable).

To cover all the bases, we also need to look at the accounting treatment for fixed-price puts on non-controlling interests. Once again, we start by analyzing the rights and obligations of the instruments in conjunction with the underlying shares. Effectively, these are treated as fixed-price puttable shares; the holders (i.e. the minority shareholders) have the option

of putting them back to the entity. As the entity cannot avoid the obligation to transfer a fixed amount of economic resources, the IASB’s position in the DP is that the entity should recognize a liability for the present value of the strike price. The Board also believes that underlying own equity should be reduced by an amount equal to the fair value of the shares at the issue date of the put. In the previous case, the amount of the liability was equal to the amount of equity extinguished. But in this case, there is a discrepancy.

The Board acknowledges that it is also possible that the minority shareholders will not exercise the put option. Economically speaking, there is no incentive for a minority shareholder to put its shares back to the entity at a price that is lower than their actual value. Therefore the shares could remain outstanding. Attempting to represent this in financial terms would effectively give us a written call option. The Board considers that the residual amount is a component of the call option, which is a component of equity.

We can represent this as follows:

22 | Mazars USA Ledger

IFRS

Written put option (original instrument) = forward contract (represented by a liability for the amount of the strike price) + written call option (representing the possibility that the put may not be exercised)

It is also interesting to note that recognizing a liability and a written call option in this way corresponds exactly to the accounting treatment of a convertible bond; thus, the Board’s analogies are consistent.

In summary, a fixed-price, physically-settled put on non-controlling interests would be accounted for, under the Board’s proposed approach, as follows:1. the extinguishment of the shares held by the non-controlling interests

at an amount equal to the fair value of the shares at the issue date of the put

2. recognition of a liability for an amount equal to the present value of the strike price of the put

3. a call option written on own shares, with an initial value of the difference between i) and ii).

In conclusion, this Discussion Paper represents a shift in the Board’s position on the complex issue of NCI puts with a strike price equal to the fair value of the underlying shares. In this case, the Board is moving towards the position put forward by the AMF in 2009. In contrast, the Board’s proposal for fixed-price NCI puts is more innovative. We have no doubt that many comments on this topic will be submitted to the Board before the closing date of its consultation on 7 January 2019!

3. Key Points to Remember

• A lot of ink has been spilt on the topic of puts on non-controlling interests since IFRS came into effect in 2005, and in the absence of clear guidance on the subject, a diverse range of accounting methods have been used.

• The IASB has proposed a new accounting treatment as part of its FICE project, differentiating between NCI puts with a strike price equal to the fair value of the underlying shares, and fixed-price NCI puts.

• For NCI puts with a strike price equal to the fair value of the underlying shares, an entity would recognize a liability (presented separately) for the fair value of the shares, with a contra journal entry for a reduction in equity, at the date when the put is issued. Subsequent changes in the value of the liability would be recognized in OCI without recycling to profit or loss.

• For fixed-price, physically-settled NCI puts, an entity would recognize a liability for an amount equal to the present value of the strike price of the put, with a contra journal entry for the extinguishment of the shares held by the non-controlling interests at an amount equal to the fair value of the shares at the issue date of the put, and a call option written on own shares for an amount equal to the difference between the first two components.

For more information contact the Mazars USA Accounting Help Desk at [email protected].

FEATURED SURVEY

Analysis of the Solvency and Financial Condition Reports of European Insurance and Reinsurance Entities For the second successive year, Mazars has conducted a survey of solvency and financial condition reports. Last year’s analysis considered the reports of French companies, but this has now been extended to include 15 European entities subject to the Solvency II directive, which came into force on 1 January 2016, and has fundamentally changed the regulatory framework for European insurance companies and undertakings. Scan the barcode to view this year's survey results.

FEATURED WHITEPAPER

Accounting for Cryptoassets under US GAAP and IFRS The meteoric rise of cryptocurrency and blockchain technology has forward thinking accounting professionals responding to a barrage of questions from clients. Mazars USA’s Andre Sterley and Antoine Leroy share their thoughts for key considerations as it relates to accounting for cryptoassets under both US GAAP and IFRS. Scan the barcode to view full whitepaper.

November/December 2018 | 23

HEALTHCARE POLICY AND PROCEDURE BEST PRACTICES

The touchstone for measuring compliance program effectiveness istheOfficeofInspectorGeneral’sSevenElementsofanEffectiveCompliance Program (Seven Elements) derived from the Organiza-tional Sentencing Guidelines promulgated by the U.S. Sentencing Commission.1

Entire treatises could be written on each of the elements, but they basically boil down to: designation of a compliance officer and committee; written policies, procedures, and a standard, or code, of conduct; open lines of communication; training and education; monitoring and auditing; enforcing standards through well-publicized disciplinary guidelines; and promptly responding to detected offenses and taking corrective action. Arguably, the most underappreciated, overlooked, and important of these elements is that of written policies and procedures (P&Ps). P&Ps are the workhorse of a compliance program, i.e., if done right, they will dependably serve an organization for years. WHY ARE EFFECTIVE P&PS IMPORTANT?

Why are effective P&Ps so valuable from a compliance standpoint? If utilized properly, they:• Establish organizational goals, set tone and culture, describe expected

behaviors, and contribute to other employee accountability tools• Train and educate employees not only at onboarding but on an ongoing

basis• Facilitate succession planning and contribute to sound business conti-

nuity, e.g., the old adage of “what if key employee Sally is hit by a bus, who will do her job?” applies here

• Provide legally defensible documentation that complies with regulatory, accreditation, and contractual requirements, which may help avoid litigation, fines, and loss of business, i.e., function as a critical risk mitigation tool

• Serve as a foundation for business process improvement

In the health care sector, it is not an exaggeration to state that effective P&Ps can also literally save lives. HOW TO START (AND FINISH!)?

Most medium to large-sized organizations have at least some basic written policies and procedures, most likely human resource-related, although their quality, completeness, and currency may be lacking. However, even small business can benefit from having effective P&Ps.

Whether starting from scratch or working to improve existing P&Ps, the entire process and even getting started can be overwhelming IRAC FOR P&PS

Instead of tackling P&P creation and improvement wholesale, or, worse, ignoring it completely, take a step-by-step approach along the lines of the IRAC (Issue, Rule, Analysis, Conclusion) method for briefing a legal issue.

Issue.

First, identify key organizational risks, i.e., what is the issue or concern that needs to be addressed? This process may be as formal as undertaking

BY MELISSA BORRELLI

HEALTHCARE

24 | Mazars USA Ledger

HEALTHCARE

enterprise risk management or as simple as a sense of an organization’s highest risk areas based on the legal and other authority or contracts to which the organization are subject.

Considering what other similarly situated organizations have identified as common risks may also be useful. For most organizations, human resourc-es (think classification issues and wage-and-hour litigation) and information security (what organization does not have at least some confidential data, let alone personally identifiable information?) will be among the highest-risk areas. In health care in particular, add to that safeguarding protected health information and the obligations that come with receiving government money, and you have the start of a good list of organizational risk areas.

Rule.

Second, determine what authority the organization is subject to; that is, what are the rules with which your organization must comply? Think broad-ly—this is one area you do not want to give short shrift. Look to statutes, regulations, opinions and other regulatory guidance, court cases, accred-itation standards, and key contracts, not the least of which is government contracts.

Analysis.

Next, rally the troops. Bring in the business owners, key stakeholders, and subject matter experts that will have to abide by the P&Ps to draft and analyze the requirements and describe how policies are actually imple-mented at your organization. Again, think broadly. With today’s software and process integrations, it may be difficult to know whether the work of one area will impact that of another.

Check for interactions with other departments, software, business process-es, and existing P&Ps. Perhaps most importantly, never reinvent the wheel. Look for samples from colleagues, professional associations, and other similarly situated organizations.

One caveat: while organizational policies may be similar, their procedures most likely are not. For example, the policy of most health care entities is (should be!) to prevent and detect fraud, waste, and abuse. The procedures each organization employs in pursuit of that policy, however, will vary significantly. Leave time for ample and broad review by all stakeholders, including legal, compliance, management, and the line staff that implement the procedures on a day-to-day basis. Management may be chagrined to find that line staff are not following the procedures they thought they were for numerous reasons, including that they are not up-to-date, onerous, inefficient, or are intentionally being skirted for possibly questionable or bad-faith reasons.

Also, avoid falling into the trap of using legalese and overly technical language wherever possible. It is great to have written P&Ps, but not so great if the intended audience (staff, but don’t forget about regulators and accreditors) cannot understand them.

Conclusion.

Unfortunately, even with a polished final product, the work is not finished. Rather, that shiny new P&P must be publicized to those to whom it applies and thorough training and education must be undertaken. Ideally, who received the training and when is documented. Additionally, best practice dictates that all P&Ps be reviewed at least annually and updated as needed; for example, when a law is changed, an accreditation standard tweaked, or new hardware, software, or a business process is implemented. What Should P&Ps Include?

There are literally dozens of P&P templates available online. The most effective will have the following sections at minimum:

Why Are Effective P&Ps Important?

Why are effective P&Ps so valuable from a compliance standpoint? If utilized properly, they:• Scope: What is the scope of the P&P? Who or what does it apply

to? For some organizations, it will be a line of business for another, a particular customer, and others, a department.

• Roles and Responsibilities: Who is responsible for what with regard to that P&P? Roles and Responsibilities are best defined by department and/or job title, and not by a specific employee’s name, for business continuity purposes.

• Responsibilities should also be specific and if at all possible, mea-sureable. For example, a fraud, waste, and abuse P&P may require a claims department manager to review 10% of each claims examiners weekly output. Here, the claims manager’s role is defined and the responsibility is clear and measurable. This section is particularly important to consider when determining whether and how a P&P can be monitored or audited, another of the Seven Elements. Moreover, if staff have questions or concerns, this section provides them with guid-ance on who to consult and aids in enforcing employee accountability.

• DefinitionsandAcronyms:Best practice is to include these near the beginning of the P&P so that the user does not need to page back and forth to understand the multiple acronyms and sometimes highly technical definitions employed in health care.

• Exceptions: Describe any exceptions to the P&P (in some cases, there may be no wiggle room) and how an exception should be requested and whether it should be granted. For example, describe

November/December 2018 | 25

under what circumstances an exception to an employee’s use of paid time off may be allowed and who should review and decide upon that exception.

• Enforcement: Although it may seem heavy-handed, part of the purpose of P&Ps, particularly in helping to ensure an organization has an effective compliance program, is to publicize the consequences for non-compliance with requirements. Those subject to the P&P should understand what may or will happen if they do not follow the rules.

• References/Authority: While sometimes separated into two sections, at least one section should be dedicated to the legal and other author-ity that require the P&P and to any other related documents, whether internal or external. This is especially helpful in determining what P&Ps are impacted and should be updated when changes to the law and other authority occur.

• Revision History and Reviewer: While the information regarding who is responsible for reviewing and approving the P&P and its review cycle can be kept elsewhere, it is simpler to include this information within the P&P itself. Revision history is particularly helpful when deal-ing with a regulatory action or litigation—tracking down the language of prior P&Ps can be time consuming and sometimes impossible, depending on the sophistication of an organization’s record-retention practices.

Maintaining a master list of P&Ps is another best practice that organizations should consider. This can be as simple as an Excel sheet or as complex as governance, risk, and compliance software.

Regardless, tracking information should include a number of data points, such as the P&P’s name and purpose; owner (department, division, man-ager, etc.); authority; version history; and a description of the review cycle. It is also helpful to include an indicator as to whether a particular P&P must be reviewed and approved by a regulator, accreditor, and/or contractor if it is substantively amended.

There is disagreement about whether P&Ps should be separated into two or more documents, i.e., one document setting forth the policy and a second describing the associated procedure. Each approach has pros and cons that may depend on a particular organization and its culture.

For example, if P&Ps are only available to staff in paper form, it may make more sense to have a single document for both the policy and the procedure so they are less likely to get separated, whereas if they are available elec-tronically, multiple documents are easier to manage.

In some instances, two documents may be the way to go where the organi-zation wants to make the policy available to the general staff—e.g., the HR policy on employee classifications—but limit public access to the related procedure.

Another advantage of separate policy and procedure documents is simpli-fication of annual and other reviews. While most policies will not change from year-to-year, for example, an organization’s commitment to preventing and detecting fraud is not likely to alter, the implementing procedures for that policy may be subject to multiple revisions over time. Keeping separate documents may help maximize flexibility in drafting and review.

Effective written P&Ps can help meet multiple of the Seven Elements, if drafted and maintained in a thoughtful manner.

While creating and maintaining P&Ps can be daunting, keep in mind their unequivocal role in supporting an effective compliance program.

As a leading change facilitator in this era of sweeping health care reform, the Mazars Health Care Group offers health care payors and providers a powerful combination of service and results-oriented strategy to help them meet their business goals, overcome challenges, and improve performance.

For more information about their timely, valuable information and insights into policies, best practices and industry developments, visit mazarsusa.com/hc.

Melissa is a Senior Manager in our Sacramento Practice. She can be reached at 916.696.3683 or at [email protected].

1 https://www.ussc.gov/guidelines/2016-guidelines-manual/2016-chapter-8#NaN

26 | Mazars USA Ledger

IFRS

FICE DISCUSSION PAPER: THE BOARD’S PREFERRED APPROACH TO

CLASSIFYING FINACIAL INSTRUMENTS AS LIABILITIES OR EQUITY

On 28 June, the IASB published a Discussion Paper (DP) presenting the current state of its deliberations on the Financial Instruments with Characteristics of

Equity project (FICE). This project, which is not being carried out in conjunction with the FASB, focuses on the classification of financial instruments as liabilities or equity in the issuer’s financial statements. The comments received will help the Board to decide whether to publish an exposure draft to amend or replace

IAS 32, and/or non-mandatory implementation guidance.

Here, Beyond the GAAP summarizes the key concepts presented in the DP, with a particular focus on the questions on which the Board is seeking feedback in

order to decide between the various possible approaches.

November/December 2018 | 27

1.ObjectivesoftheDP Like IAS 32, the scope of the DP is limited to the principles for classifying financial instruments as liabilities or equity from the point of view of the issuer of the instruments [IN2]. Thus, the presentation and measurement principles set out in IFRS 9 – Financial Instruments will not be affected by this DP.

The IASB has identified a number of areas where the current IAS 32 requires improvement. In particular, it wishes to clarify the underlying concepts used to distinguish between liabilities and equity. The Board notes that this lack of clarity has resulted in divergences in the accounting treatment of certain products, such as puts on non-controlling interests or certain types of contingent convertible bonds. Furthermore, the situation makes it difficult to identify the correct accounting treatment for new and increasingly complex financial instruments that are appearing on the market, which combine features of both liabilities and equity.

The IASB has also taken account of feedback from users of financial statements, who have asked for further information to be provided on the features of this type of financial instruments.

The Board wished to address these specific issues without making changes to the classification outcomes for the majority of instruments, which are less complex.

The main objectives of the FICE project are as follows: § to define clear conceptual principles that are consistent with the

current IAS 32; § to improve the consistency of the classification of contractual rights/

obligations linked to an entity’s own equity instruments; § to improve the information provided (through presentation in the

financial statements and disclosures in the notes) about features of financial instruments that are not captured by their classification as liabilities or equity.

2.SummaryoftheclassificationapproachproposedintheDP

The Board’s current preferred approach for classifying a financial instrument as a liability or equity is based on the two following features:

§ Timing feature: there is an unavoidable obligation to transfer economic resources (cash or another financial asset) at a specified time other than at liquidation;

§ Amount feature: there is an unavoidable obligation to transfer an amount independent of the entity’s available economic resources1.