Embed Size (px)

Citation preview

8/12/2019 Lecture on Percentage Taxes

http://slidepdf.com/reader/full/lecture-on-percentage-taxes 1/4

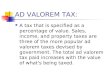

PERCENTAGE TAXES(SECTIONS 116 TO 127 OF THE NIRC OF 1997)

A. 3% percentage tax on persons exempt from VAT because their gross annual salesdo not exceed P1.5m , and who are not re uired to pa! a percentage tax under an!

of "#$ to " $, below.#. Tax on domestic carriers&. Tax on international carriers'. (ranchise tax). *+erseas communications tax(. Tax on ban s and non-ban financial intermediaries performing uasi-ban ing

functions/. Tax on other non-ban financial intermediaries0. Tax on life insurance companies. Tax on agents of foreign insurance companies2. Amusement tax

. Tax on winnings. Tax on stoc transactions.

• *ne who is sub4ect to an! of the percentage taxes can not be sub4ect to the +alue-added tax, howe+er, a registered business ma! ha+e two lines of acti+ities, one ofwhich is sub4ect to the VAT and the other sub4ect to a percentage tax.

• /enerall!, percentage taxes are based on gross receipts.• Percentage taxes are pa!able b! the sellers of the ser+ices, except the o+erseas

communications tax which is pa!able b! the user of the facilities of the seller.• Persons who are exempt from the VAT because their gross annual sales or

receipts do not exceed P1.5m are sub4ect to the 3% percentage tax.• The following are sub4ect to the percentage tax nown as common carrier6s tax78

o &ars for rent or hire dri+en b! the lessee "rent a car$o Transportation contractors, including persons who transport passengers for

hireo *ther domestic carriers b! land for their transport of passengers, except

owners of animal-drawn two-wheeled +ehicles ando eepers of garages- closed shelter for automobiles

VAT or Percentage tax on domestic carriers&ommon carrier b! A9'8

Transporting goods or cargoes - 1:% VATTransporting passengers - 3% common carrier6s tax

&ommon carrier b! A ; or <)A8(rom one point the Phils to another

point in the Philsgoods, cargoes, passengers - 1:% VAT

(rom one point the Phils to a pointoutside the Phils

8/12/2019 Lecture on Percentage Taxes

http://slidepdf.com/reader/full/lecture-on-percentage-taxes 2/4

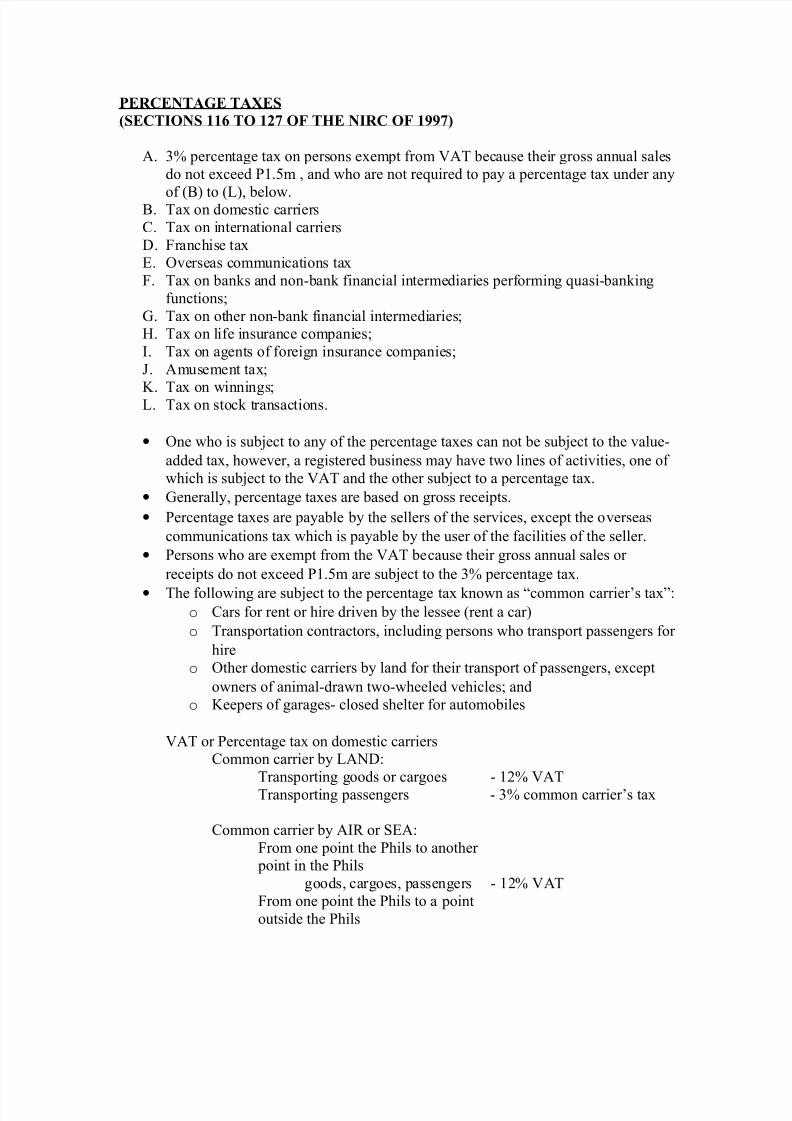

goods, cargoes, passengers - =% VAT• The following are sub4ect to a percentage tax commonl! called franchise tax78

o /as and water utilities - :%o ;adio and >or tele+ision broadcasting companies whose

Annual gross receipts of the preceding

!ear did not exceed P1=,===,=== - 3%

<pecial rule on radio>tele+isiona. if the gross receipts in the preceding !ear

exceeded P1=,===,=== - VAT b. if the gross receipts in the preceding !ear

did not exceed P1=,===,===, but ma!opt to be registered under the VAT s!stem - percentage tax

• *+erseas communications taxo The tax is on o+erseas dispatch message or con+ersation originating from

the Philippines "outgoing message$o The tax is based on the amount paid b! the user to the pro+ider of the

communication facilit!o The tax is imposed on the person pa!ing for the ser+ices rendered, and not

on the pro+ider of the communication facilit!, the latter to be consideredmerel! as collector of the tax

o The tax is 1=% of the amount paido The tax shall not appl! to the /o+ernment of the Philippines or an! of its

political subdi+isions diplomatic ser+ices international organi?ations andnews ser+ices.

• Tax of :% on life insurance companies @ called premium tax.o Tax base @ total life insurance premiums collected "gross receipts$,

whether in mone!, notes, credits or an! substitute for mone!.o Tax rate @ :%o )xemptions8

• Premiums refunded within six months after pa!ment on account ofre4ection of ris or returned for other reasons to a person insured

• ;einsurance premiums paid b! a compan! that has alread! paid atax

• Premiums collected or recei+ed b! an! branch of a domestic

corporation, firm or association doing business in the Philippineson account of an! life insurance of an insured who is a non-resident, if an! tax on such premiums is imposed b! the foreigncountr! where the branch is established

• ;einsurance premiums, if the insured of personal insurance residesoutside the Philippines, if an! tax on such premium is imposed b!the foreign countr! where the original has been issued or perfected

8/12/2019 Lecture on Percentage Taxes

http://slidepdf.com/reader/full/lecture-on-percentage-taxes 3/4

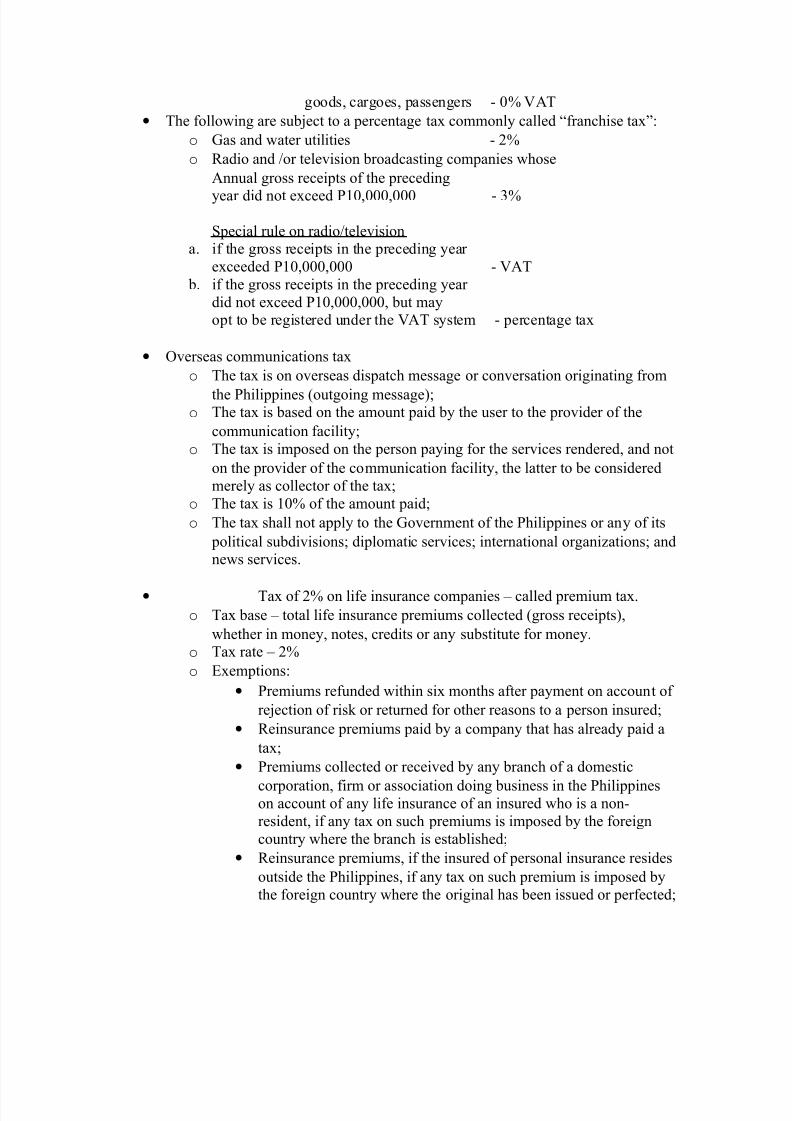

• Portion of the premiums collected or recei+ed b! insurancecompanies on +ariable contracts in excess of the amount necessar!to insure the li+es of +ariable contract owners.

• 9on-life insurance are sub4ect to VAT

• Amusement tax. There are man! inds of amusement places, butnot all are sub4ect to the amusement taxes.

• There are man! acti+ities for amusement, but not all are sub4ect tothe amusement taxes.

• At present, there is an amusement tax which is a local tax.Amusement tax on admissions to theaters, cinematographs, concert halls, circusesand other places of amusement.

• Tax on winnings @ a person who wins in horse races and 4ai lai, based on his winnings or di+idends7 "the tax to be based on the actual amount paid to him for e+er! winning tic et, after deducting the cost of tic et8 and ownerof winning race horses, based on the pri?e.

• ;eturn and pa!ment of percentage taxes.

o Taxpa!er ma! file a separate return for each branch or place of business,or a consolidated return for all.

o /eneral rule @ e+er! person liable to pa! a percentage tax will file a

uarterl! return of the amount of his gross sales, receipts or earnings and pa! the tax thereon, within :5 da!s after the end of each taxable uarter.o )xceptions8

• 3% - within := da!s after the end of the month except when thetax was a final tax, through the withholding tax s!stem.

• *&T - within := da!s after the end of the uarter • Amusement tax - within := da!s after the end of the uarter • Tax on winnings @ remitted to the # ; within := da!s from the

date withheld• <toc transaction tax of of 1%- remitted to the # ; within 5

ban ing da!s from the date withheld b! the bro er • <toc transaction tax B%, :% and 1% - on the primar! offering,

within 3= da!s from the date of listing in the local stoc exchange

EXCISE TAXES

• A national internal re+enue tax to which onl! "a$ manufacturers>producers or "b$importers ma! be sub4ect is the excise tax.

• Two inds of excise taxes8 "a$ specific tax "b$ ad +alorem tax

8/12/2019 Lecture on Percentage Taxes

http://slidepdf.com/reader/full/lecture-on-percentage-taxes 4/4

• An excise tax imposed and based on weight or +olume capacit! or an! other ph!sical unit of measurement is a specific tax .

• An excise tax imposed and based on selling price or other specified +alue of thearticle is an a !a"#$e% tax .

• The following are the articles sub4ect to excise taxes8o 'istilled spiritso Cineso (ermented li uorso Tobacco productso &igarso &igaretteso Automobileso Danufactured oils and other fuelso Dineral products ando 9on essential goods.

• Chen should the excise taxes be paidEo n the case of a locall! manufactured article, the excise tax must be paid

prior to the remo+al of the article from the place of production.o n the case of imported article, the excise tax must be paid prior to the

release of the article from customs custod!.

" Philippine Transfer and #usiness Taxes, a new approach, ;e!es, Virgilio '., 9o+ember:=1= )dition$