Embed Size (px)

Citation preview

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 1/30

Lecture note 9

Ch12

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 2/30

Outline

Cost of equity capital

Estimating beta from historical data

Cost of capital with debt (1) - Adjusted Present Value

Cost of Capital with debt (2) - Weighted average

cost of capital

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 3/30

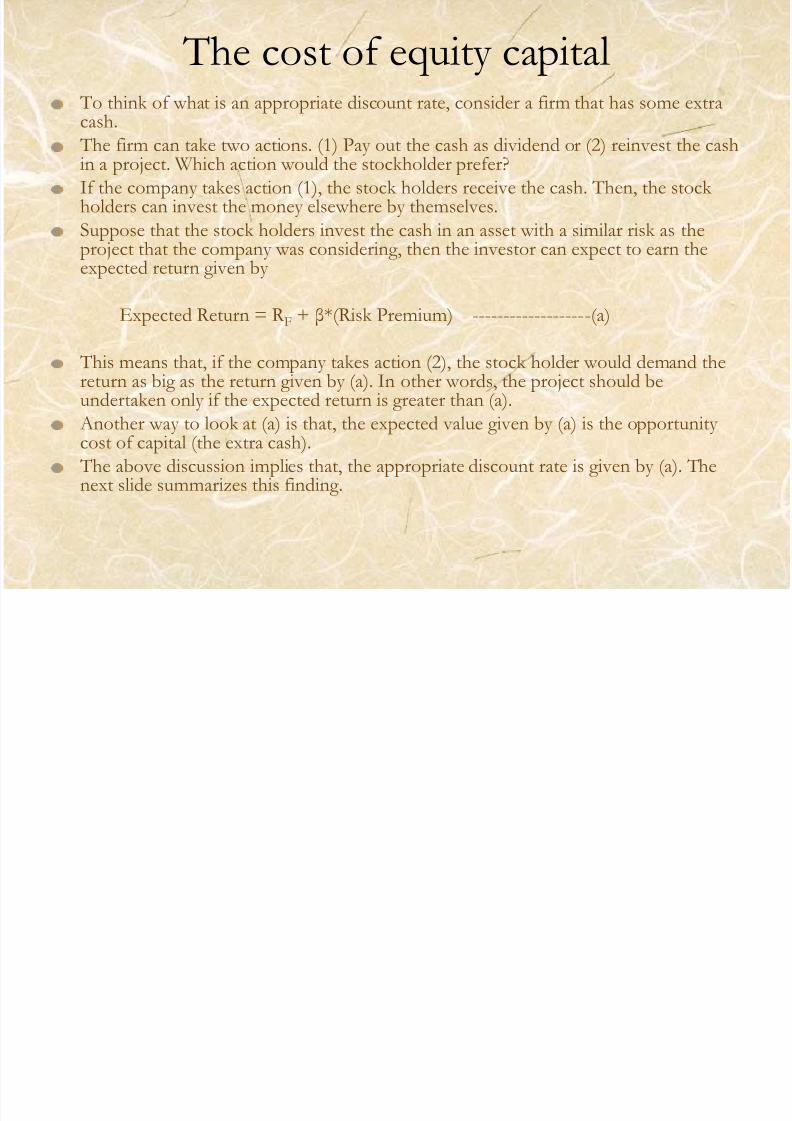

The cost of equity capital To think of what is an appropriate discount rate, consider a firm that has some extracash.

The firm can take two actions. (1) Pay out the cash as dividend or (2) reinvest the cashin a project. Which action would the stockholder prefer?If the company takes action (1), the stock holders receive the cash. Then, the stock holders can invest the money elsewhere by themselves.Suppose that the stock holders invest the cash in an asset with a similar risk as theproject that the company was considering, then the investor can expect to earn the

expected return given by

Expected Return = R F + β*(Risk Premium) -------------------(a)

This means that, if the company takes action (2), the stock holder would demand thereturn as big as the return given by (a). In other words, the project should beundertaken only if the expected return is greater than (a). Another way to look at (a) is that, the expected value given by (a) is the opportunity cost of capital (the extra cash). The above discussion implies that, the appropriate discount rate is given by (a). Thenext slide summarizes this finding.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 4/30

The cost of equity (contd)

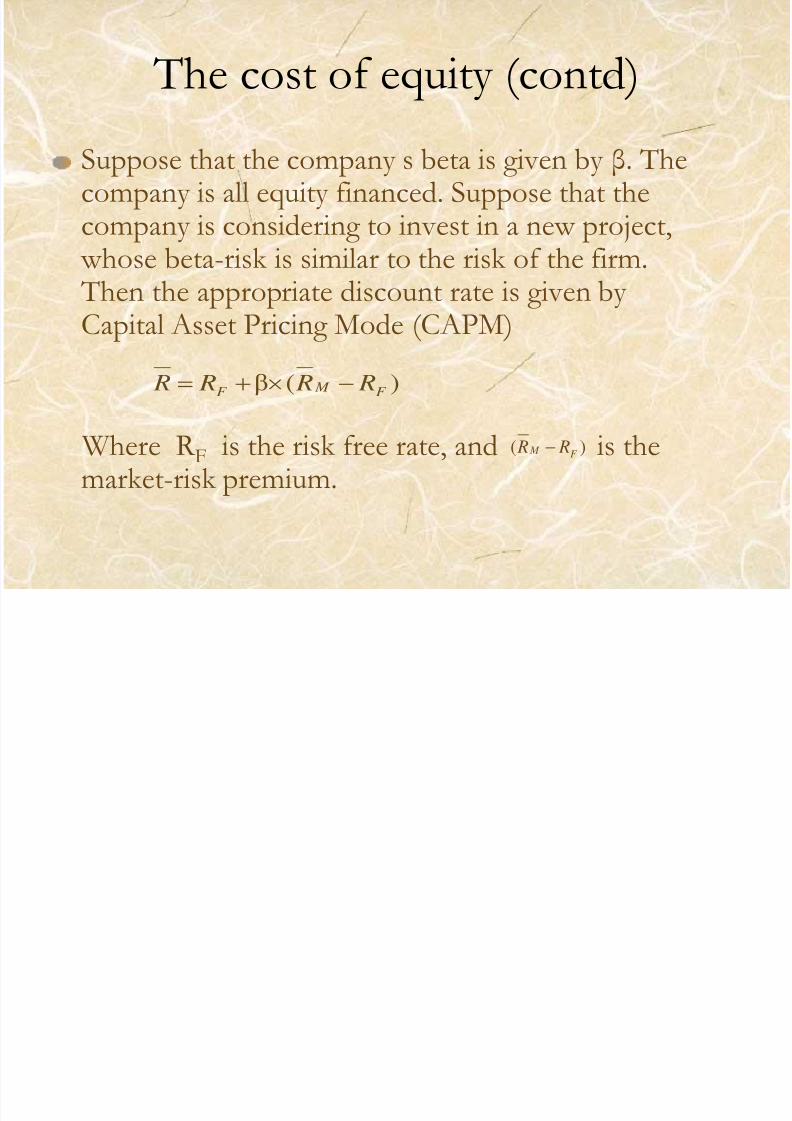

Suppose that the company ’s beta is given by β. Thecompany is all equity financed. Suppose that thecompany is considering to invest in a new project,

whose beta-risk is similar to the risk of the firm. Then the appropriate discount rate is given by Capital Asset Pricing Mode (CAPM)

Where R F is the risk free rate, and is themarket-risk premium.

)(βF

M F

R R R R

)( F M R R

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 5/30

Cost of equity capital, (contd)

-Example-

Suppose the stock of Stansfield Enterprises, a publisherof PowerPoint presentations, has a beta of 2.5. Thefirm is 100-percent equity financed. The company isconsidering a new project.

The new project is similar to the firm’s existing ones,thus the beta of the new project can be assumed to be

equal to Stransfield’s existing beta.

Assume a risk-free rate of 5-percent and a market risk premium of 10-percent. What is the appropriatediscount rate for the new project.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 6/30

Cost of equity capital, (contd)

-Example-

Two key assumptions we have made so far are(1) the beta risk of the new project is the sameas the risk of the firm, and (2) the firm is all-

equity financed. We will discuss later the case when the company has some debt.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 7/30

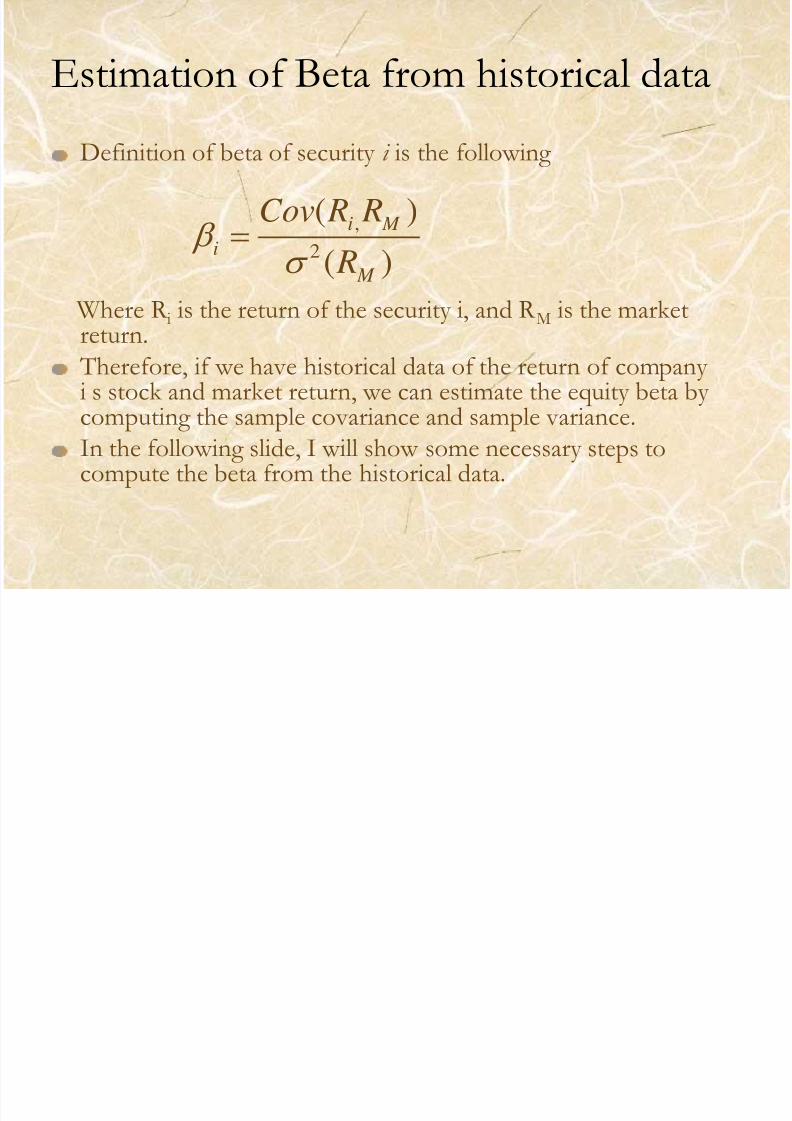

Estimation of Beta from historical data

Definition of beta of security i is the following

Where R i is the return of the security i, and R M is the marketreturn.

Therefore, if we have historical data of the return of company i’s stock and market return, we can estimate the equity beta by

computing the sample covariance and sample variance.In the following slide, I will show some necessary steps tocompute the beta from the historical data.

)(

)(2

,

M

M i

i

R

R RCov

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 8/30

Estimation of Beta from historical data

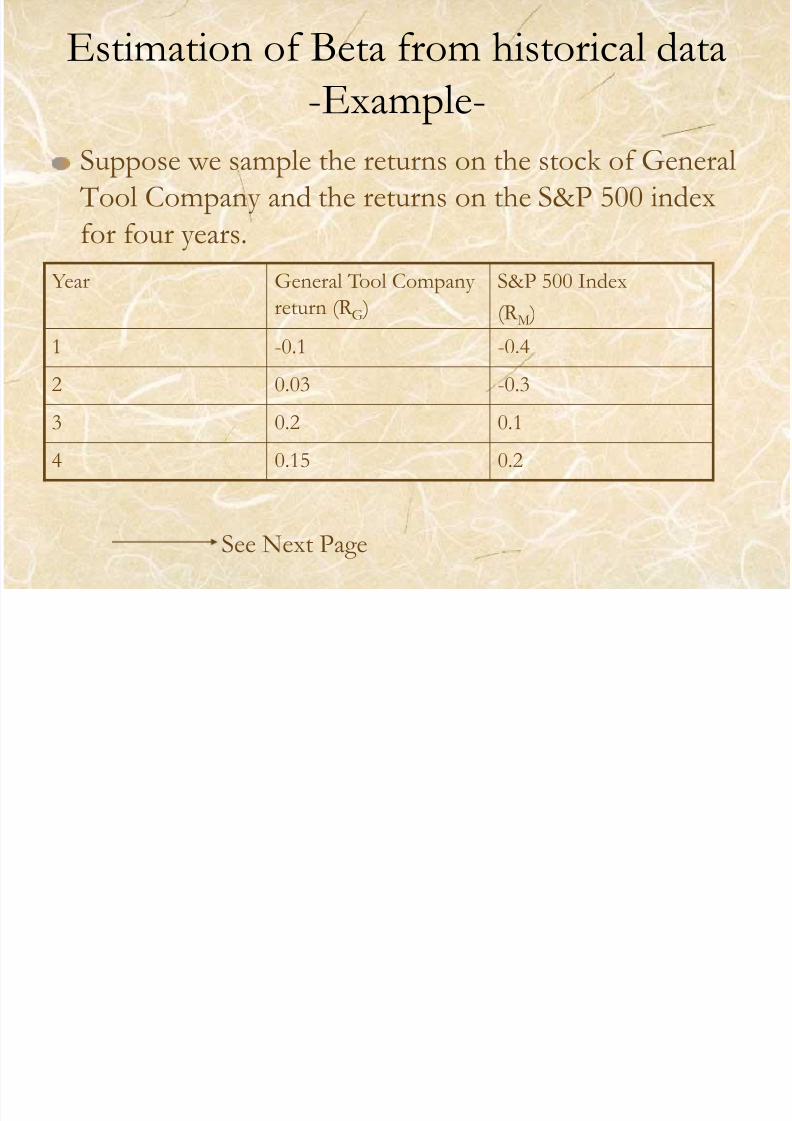

-Example-

Suppose we sample the returns on the stock of General Tool Company and the returns on the S&P 500 indexfor four years.

Year General Tool Company return (R G )

S&P 500 Index

(R M )

1 -0.1 -0.4

2 0.03 -0.3

3 0.2 0.1

4 0.15 0.2

See Next Page

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 9/30

Estimation of Beta from historical data-Example, Contd-

There are two ways to estimate the beta: (1) simply to apply thedefinition of beta or (2) to run regression R G=α+β(R M ) using Ordinary Least Square estimation. OLS result for the β is theestimate of the beta. Both methods should give you an identicalresult

Using the data in the previous page, compute the General Tool’sequity beta using both method.

You should be careful when you use the excel function covar( , ) to

compute covariance. This function computesinstead of where the latter is the correct covariance.If you want to use the excel function, you have to correct it by multiplying it by n/(n-1). Alternatively, you can compute thecorrect covariance by yourself. The excel function for variance

computes the correct variance.

n

Y Y X X

n

i

ii

1

))((

1

))((1

n

Y Y X X

n

i

ii

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 10/30

Real World Beta

P324-P325 provides estimates of some real world beta.

The choice regarding how many years of data one usesto compute beta is arbitrary. If we use too few

observations, the estimate becomes less accurate. If there had been a structural change in the risk of thefirm, using data from distant-past may give you a biasedestimate. Thus, such choice should be based on the

situation you are analyzing. Nonetheless, five years of monthly data are said to be a common choice.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 11/30

Stability of the beta

How stable is the beta? If the beta changessignificantly overtime, we may not want to usedata from distant past. But this decreases the

amount of data to compute beta, thus decreasesthe accuracy of the beta estimation. Many analysts argue that betas are generally stable for

firms staying in the same industry.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 12/30

Using industry betaUsing its own past data to compute the beta seems to

be commonsensical. However, the beta estimated this way may be subject to a large measurement errors dueto lack of observations, etc.

It is frequently argued that one can better

estimate a firm’s beta by involving the wholeindustry.

If you believe that the operations of the firm are

similar to the operations of the rest of theindustry, you should use the industry beta.See next page

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 13/30

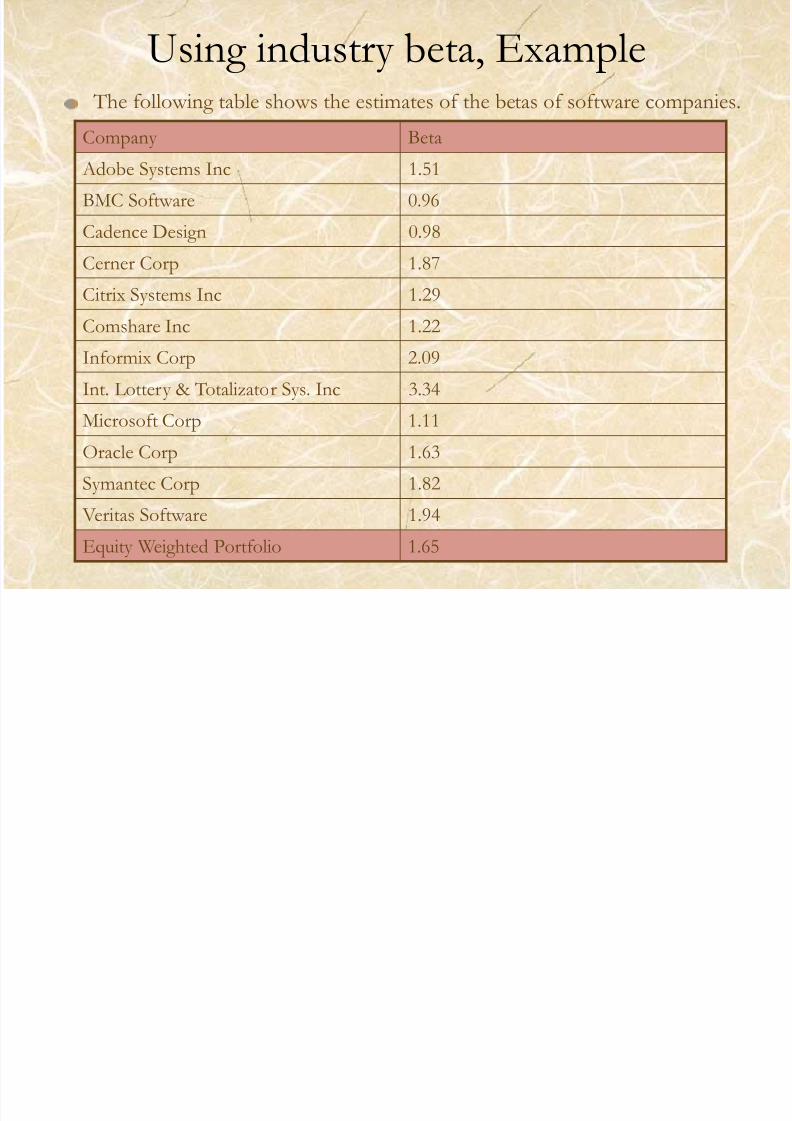

Using industry beta, Example The following table shows the estimates of the betas of software companies.

Company Beta Adobe Systems Inc 1.51

BMC Software 0.96

Cadence Design 0.98

Cerner Corp 1.87

Citrix Systems Inc 1.29

Comshare Inc 1.22

Informix Corp 2.09

Int. Lottery & Totalizator Sys. Inc 3.34

Microsoft Corp 1.11

Oracle Corp 1.63

Symantec Corp 1.82

Veritas Software 1.94

Equity Weighted Portfolio 1.65

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 14/30

Using industry beta (contd)

Software industry may be a volatile industry. Thus, forexample, the financial executive of Adobe System may be uncomfortable to use the beta (1.51) estimated using its own past data only. In such case, industry beta of

1.61 may be a more accurate estimates of the risk.Industry beta is also useful when a company just wentto public, and thus does not have much historical data.

When using industry beta, one has to make sure that

the operation of the firm is similar to the operations of the rest of the firms in the industry.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 15/30

Financial Leverage and beta

Financial Leverage is the extent to which a firmrelied on debt. Levered firm is a firm with somedebts in its capital structure.

When a firm has a debt, this gives rise to thebeta for the overall asset.

See next page.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 16/30

Financial Leverage and beta (contd)

In a similar way we computed the beta for equity capital, we can define the beta for debt capital asa sensitivity of the yield of the debt to the

market return. Let βDebt and βEquity be the betasfor debt and equity respectively. Then the β Asset,the beta for the overall asset, is defined as the

equation in the next slide.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 17/30

Financial Leverage and beta (contd)

)1(

Equity Debt Asset Equity Debt

Equity

Equity Debt

Debt

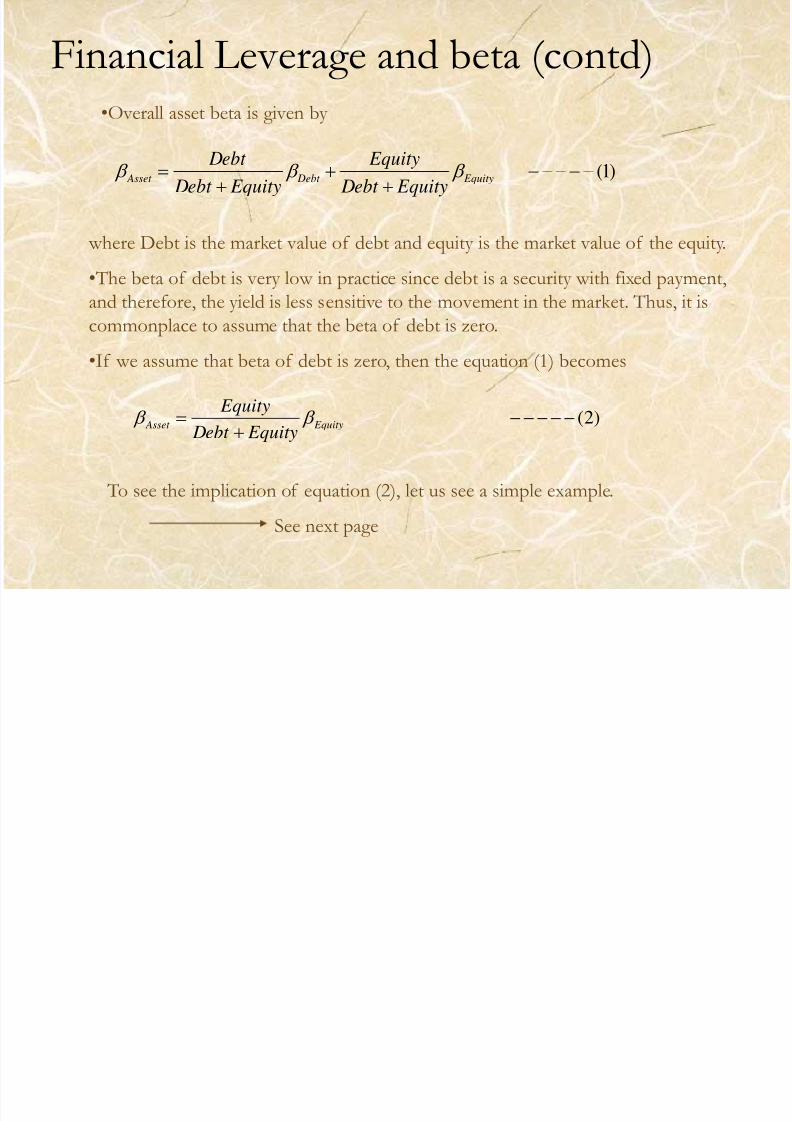

•Overall asset beta is given by

where Debt is the market value of debt and equity is the market value of the equity.

• The beta of debt is very low in practice since debt is a security with fixed payment,and therefore, the yield is less sensitive to the movement in the market. Thus, it iscommonplace to assume that the beta of debt is zero.

•If we assume that beta of debt is zero, then the equation (1) becomes

)2(

Equity Asset Equity Debt

Equity

To see the implication of equation (2), let us see a simple example.

See next page

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 18/30

Financial Leverage and beta (contd)-Example-

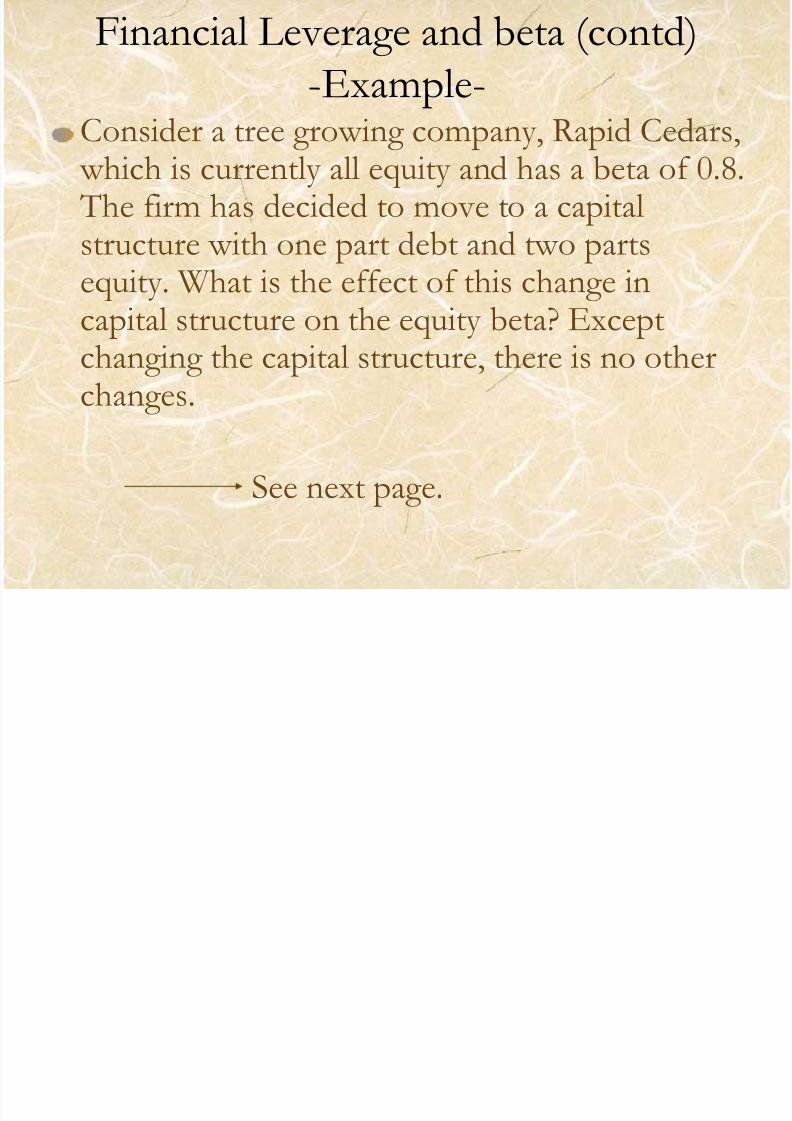

Consider a tree growing company, Rapid Cedars, which is currently all equity and has a beta of 0.8. The firm has decided to move to a capitalstructure with one part debt and two parts

equity. What is the effect of this change incapital structure on the equity beta? Exceptchanging the capital structure, there is no otherchanges.

See next page.

Fi i l L d b ( d)

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 19/30

Financial Leverage and beta (contd)

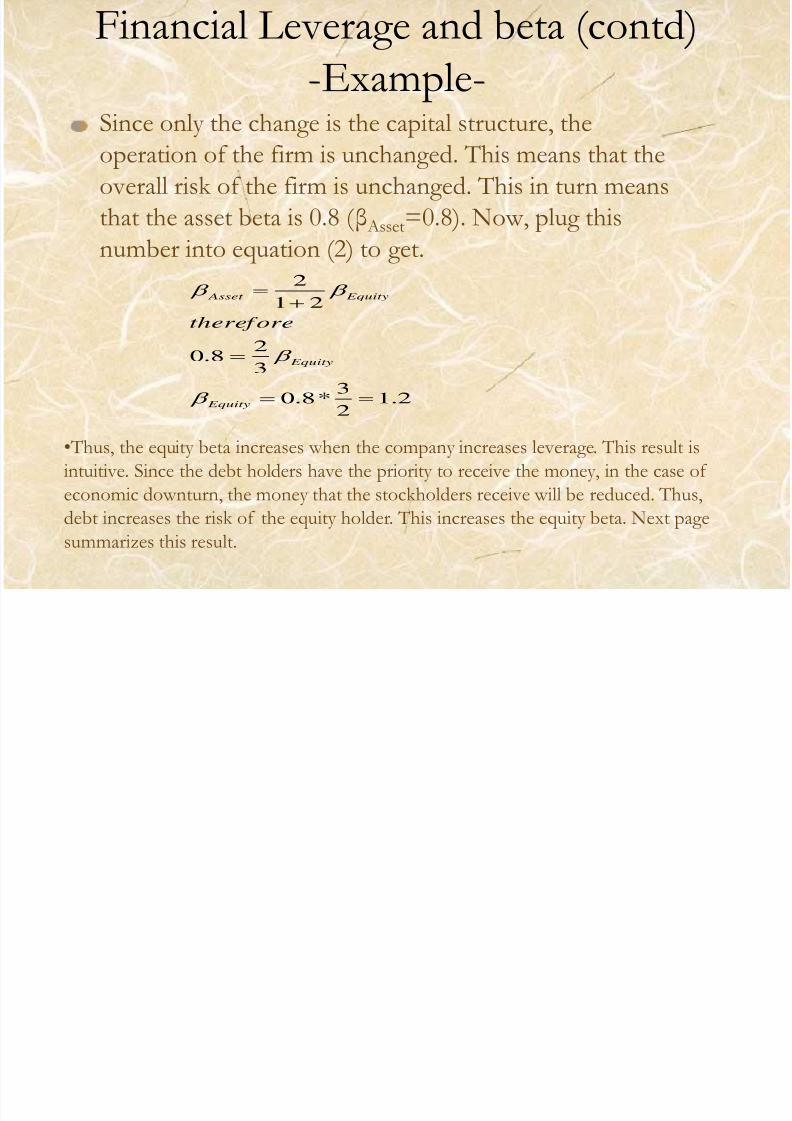

-Example-Since only the change is the capital structure, theoperation of the firm is unchanged. This means that theoverall risk of the firm is unchanged. This in turn meansthat the asset beta is 0.8 ( β Asset=0.8). Now, plug thisnumber into equation (2) to get.

2.12

3*8.0

3

28.0

21

2

Equity

Equity

Equity Asset

therefore

• Thus, the equity beta increases when the company increases leverage. This result isintuitive. Since the debt holders have the priority to receive the money, in the case of economic downturn, the money that the stockholders receive will be reduced. Thus,debt increases the risk of the equity holder. This increases the equity beta. Next pagesummarizes this result.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 20/30

Financial Leverage and beta (contd)

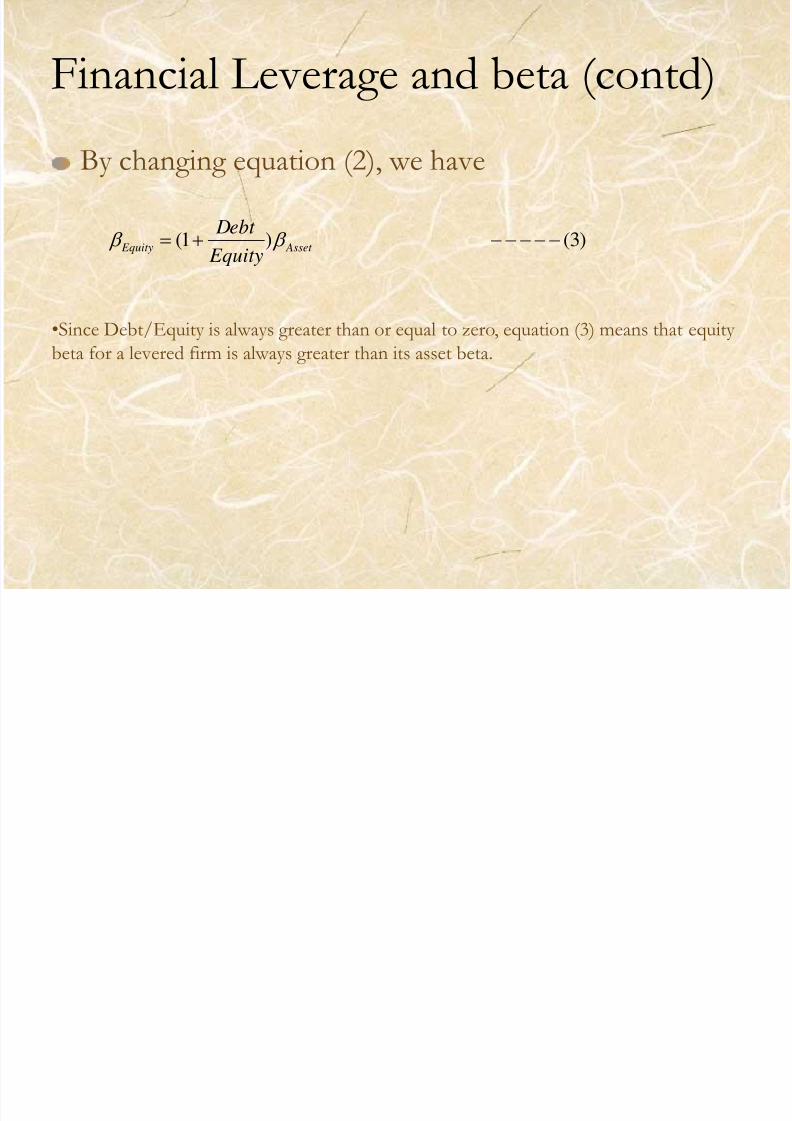

By changing equation (2), we have

)3( )1( Asset Equity Equity

Debt

•Since Debt/Equity is always greater than or equal to zero, equation (3) means that equity beta for a levered firm is always greater than its asset beta.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 21/30

Cost of capital with debt (1)

-Adjusted Net Present Value-

Previous discussions indicate that, when we computethe discount value for a levered firm, simply applying the equity beta the CAPM model may not produce an

appropriate cost of capital.Using asset beta instead of equity beta is one of asolution. Adjusted Net Present Value is the NPV using the discounted rate thus computed.

Next slide shows a typical way to compute thediscounted value for Adjusted Net Present Value.

C f i l i h d b ( ) C d

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 22/30

Cost of capital with debt (1), Contd-Adjusted Net Present Value-

The case we consider is the case where the company does not know its own equity beta or asset beta.

1. For such case, first, we obtain the equity beta of acomparable company. Let βEq

Comp be the equity beta

of the comparable company.2. Now, let B and S be the market value of the debt and

equity of the comparable company.

3. Next, compute the Asset beta of the comparablecompany in the following way.

See Next slide

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 23/30

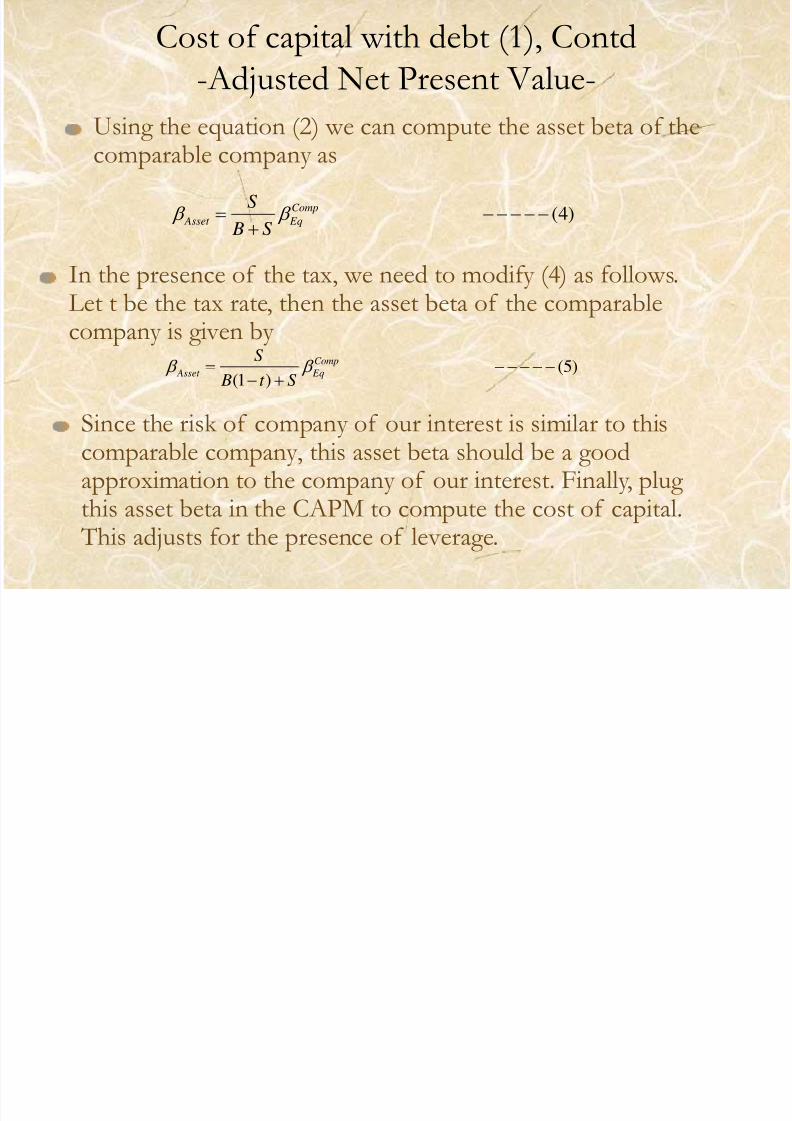

Cost of capital with debt (1), Contd-Adjusted Net Present Value-

Using the equation (2) we can compute the asset beta of thecomparable company as

)4(

Comp

Eq Asset S B

S

)5( )1(

Comp

Eq Asset St B

S

In the presence of the tax, we need to modify (4) as follows.Let t be the tax rate, then the asset beta of the comparablecompany is given by

Since the risk of company of our interest is similar to thiscomparable company, this asset beta should be a goodapproximation to the company of our interest. Finally, plug this asset beta in the CAPM to compute the cost of capital.

This adjusts for the presence of leverage.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 24/30

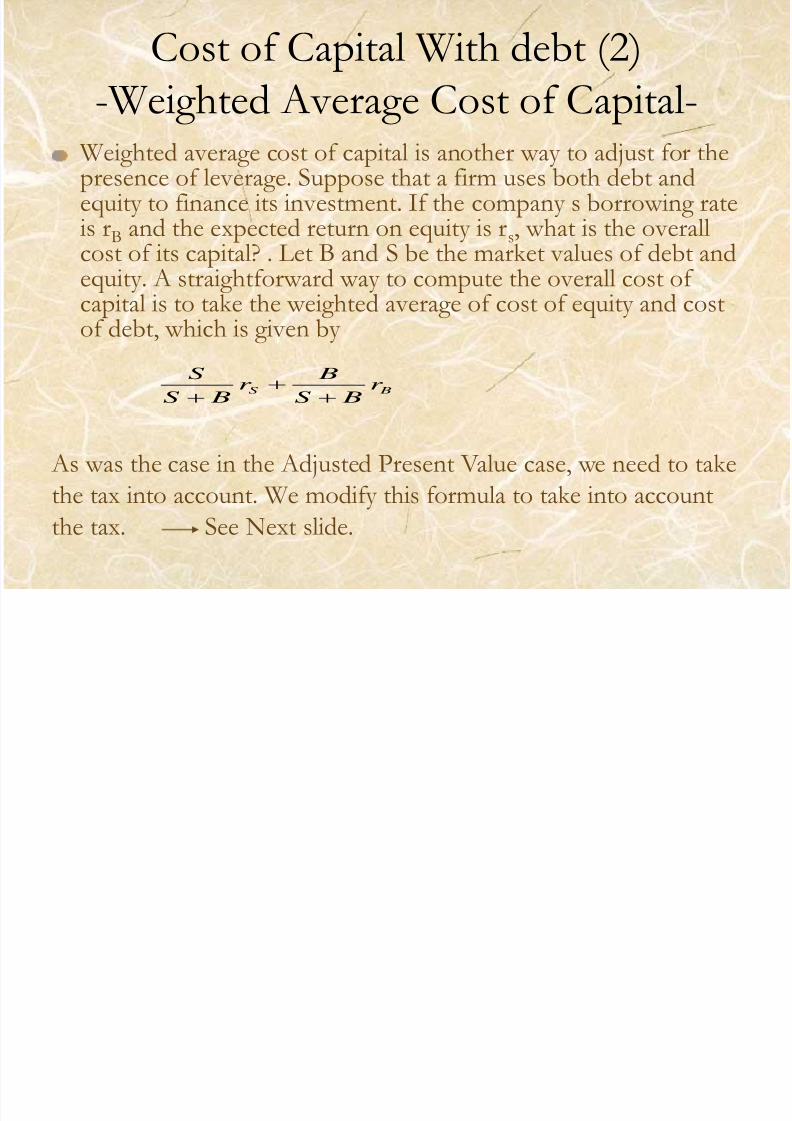

Cost of Capital With debt (2)

-Weighted Average Cost of Capital- Weighted average cost of capital is another way to adjust for thepresence of leverage. Suppose that a firm uses both debt andequity to finance its investment. If the company ’s borrowing rateis rB and the expected return on equity is rs, what is the overallcost of its capital? . Let B and S be the market values of debt and

equity. A straightforward way to compute the overall cost of capital is to take the weighted average of cost of equity and costof debt, which is given by

BSr

BS

Br

BS

S

As was the case in the Adjusted Present Value case, we need to takethe tax into account. We modify this formula to take into accountthe tax. See Next slide.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 25/30

Suppose that expected return on equity is rs. Letrb be the borrowing rate. Since the interest is taxdeductible at corporate rate, after tax return to

the debt holders is rb(1-Tc ) where Tc is thecorporation’s tax rate. In other words, rb(1-Tc ) isthe after tax cost of debt.

See Next Page

Cost of Capital With debt (2)-Weighted Average Cost of Capital with debt-

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 26/30

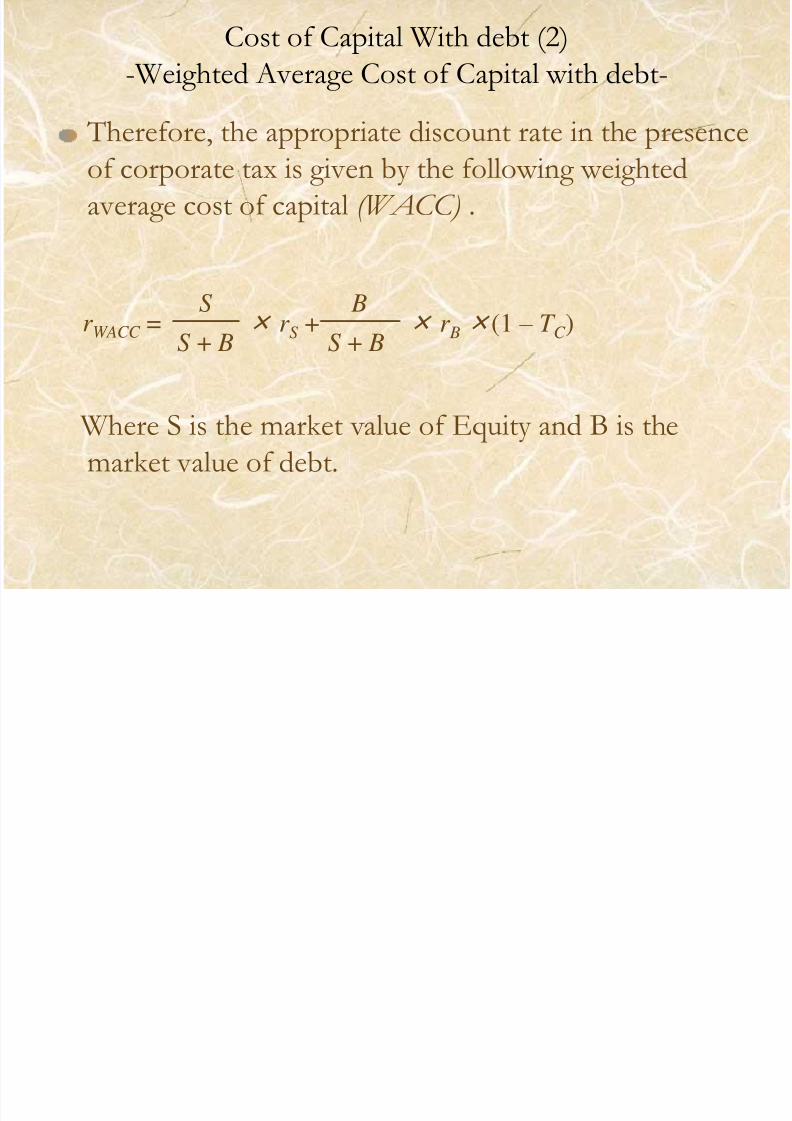

Cost of Capital With debt (2)-Weighted Average Cost of Capital with debt-

Therefore, the appropriate discount rate in the presenceof corporate tax is given by the following weightedaverage cost of capital (WACC) .

Where S is the market value of Equity and B is themarket value of debt.

r WACC

=S + B

S× r

S+S + B

B× r

B×(1 – T

C )

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 27/30

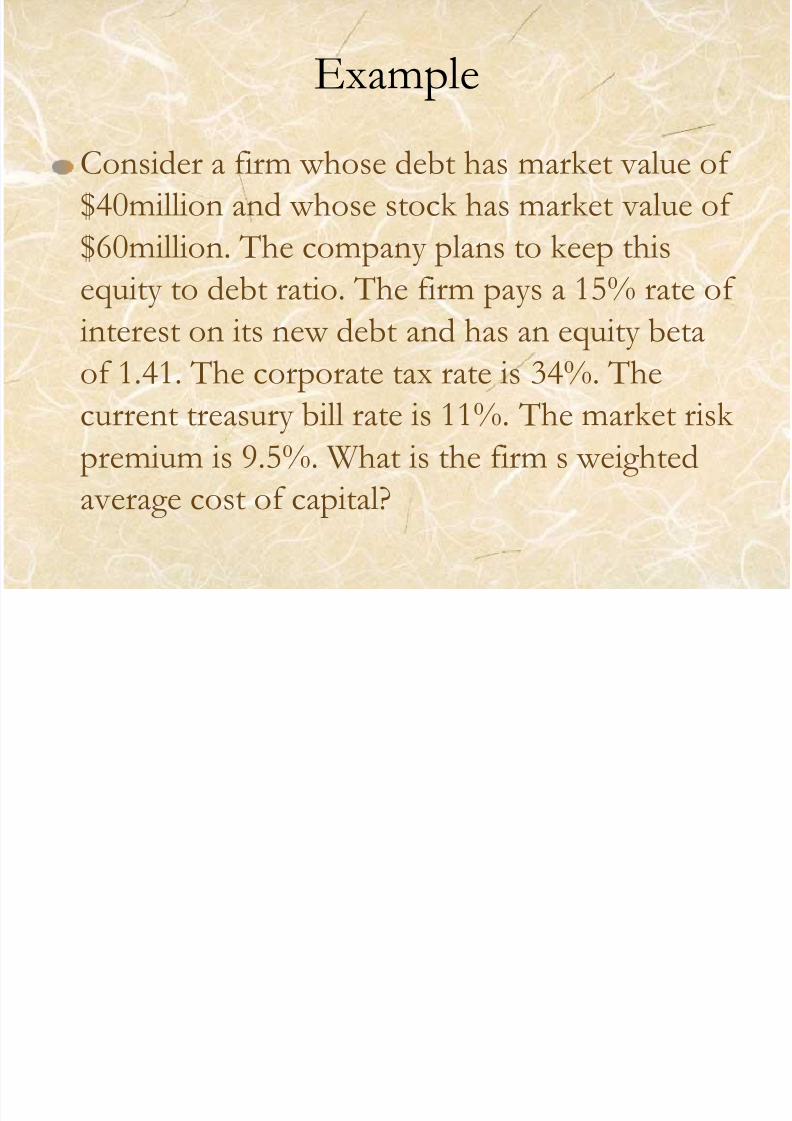

Example

Consider a firm whose debt has market value of $40million and whose stock has market value of $60million. The company plans to keep this

equity to debt ratio. The firm pays a 15% rate of interest on its new debt and has an equity betaof 1.41. The corporate tax rate is 34%. The

current treasury bill rate is 11%. The market risk premium is 9.5%. What is the firm’s weightedaverage cost of capital?

E l E i i I i l

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 28/30

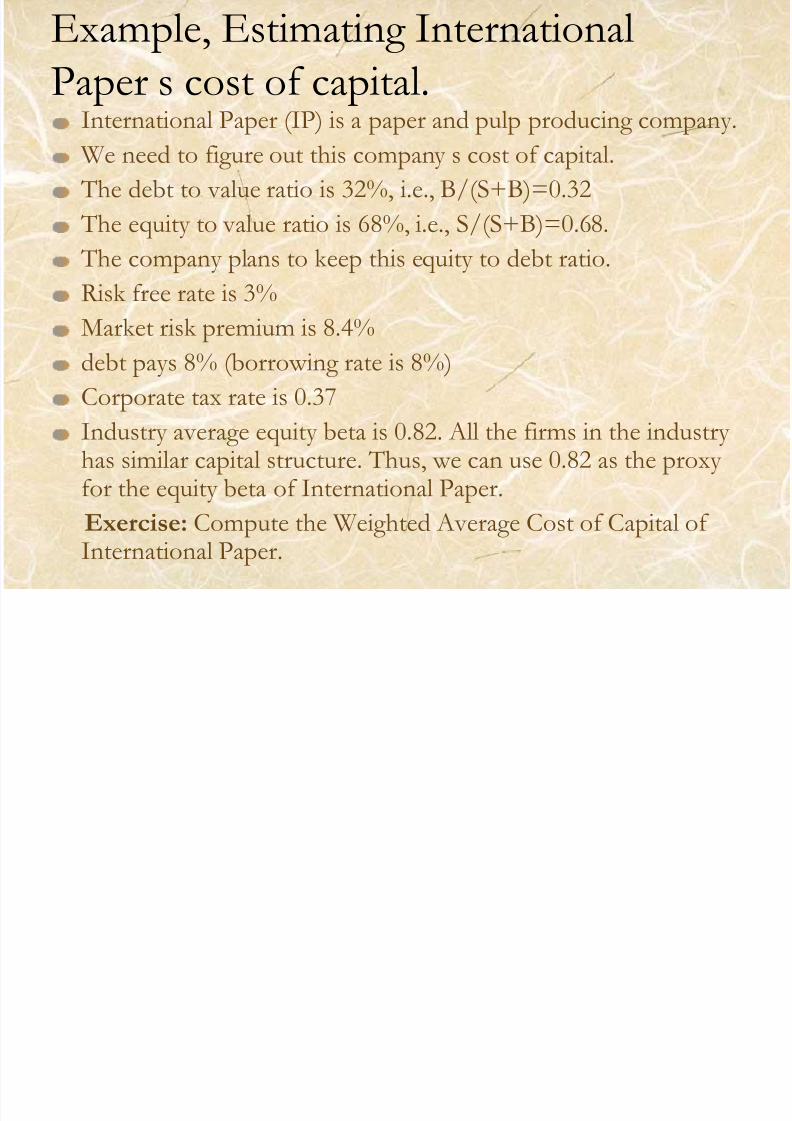

Example, Estimating International

Paper’s cost of capital.International Paper (IP) is a paper and pulp producing company.

We need to figure out this company ’s cost of capital.

The debt to value ratio is 32%, i.e., B/(S+B)=0.32

The equity to value ratio is 68%, i.e., S/(S+B)=0.68.

The company plans to keep this equity to debt ratio.

Risk free rate is 3%

Market risk premium is 8.4%

debt pays 8% (borrowing rate is 8%)

Corporate tax rate is 0.37

Industry average equity beta is 0.82. All the firms in the industry has similar capital structure. Thus, we can use 0.82 as the proxy for the equity beta of International Paper.

Exercise: Compute the Weighted Average Cost of Capital of

International Paper.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 29/30

A note

The firm beta versus project beta

So far, we assumed that the beta for the project is the

same as the beta of the firm. If a company undertakes aproject which is very different from the rest of theprojects, then you should not use the firm’s beta.Instead, use industry beta whose operation is close to

the new project.

See the example in the next slide.

8/4/2019 Lecture Note 9 (Ch12)

http://slidepdf.com/reader/full/lecture-note-9-ch12 30/30

Firm beta v.s. project beta-Example-

D.D. Ronnelley Co, a publisher firm, a publisherfirm, may accept a project in computer software.Noting that computer software companies havehigh betas, the publishing firm views the

software venture as more risky than the rest of its business. Then, it should discount the projectat a rate commensurate with the risk of software

companies.