Embed Size (px)

Citation preview

Lecture 5

Secondary Equity Markets – III

NYSE and NASDAQ

Overview

• Examples:– NYSE

– NASDAQ.

• Tick size and its effects.

• Payment for order flow.

NYSE and Nasdaq

• Understand the evolution of these two major equity markets.

• Evaluate the importance of institutional features, which sometimes are seem quite negligible at first glance.

• Understand the effect of regulatory environment on market performance.

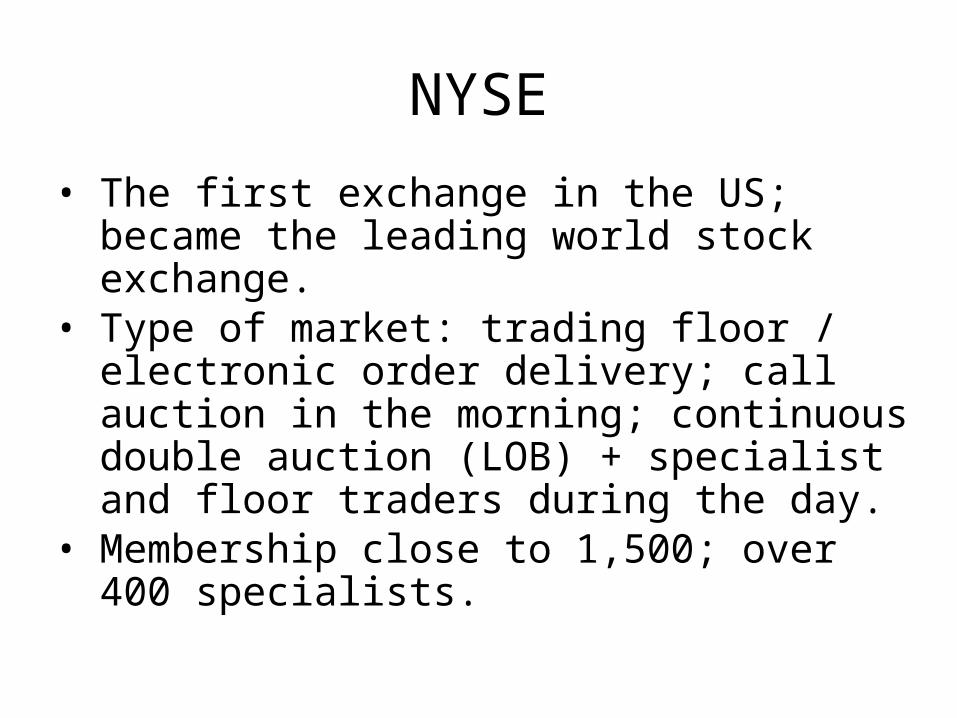

NYSE

• The first exchange in the US; became the leading world stock exchange.

• Type of market: trading floor / electronic order delivery; call auction in the morning; continuous double auction (LOB) + specialist and floor traders during the day.

• Membership close to 1,500; over 400 specialists.

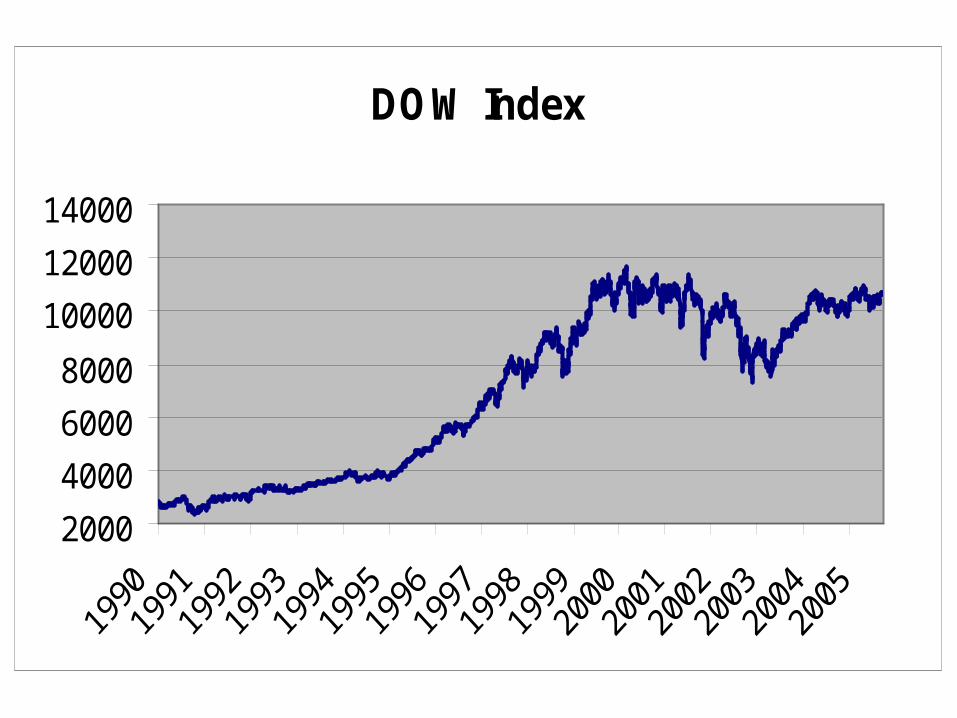

DOW Index

2000

4000

6000

8000

10000

12000

14000

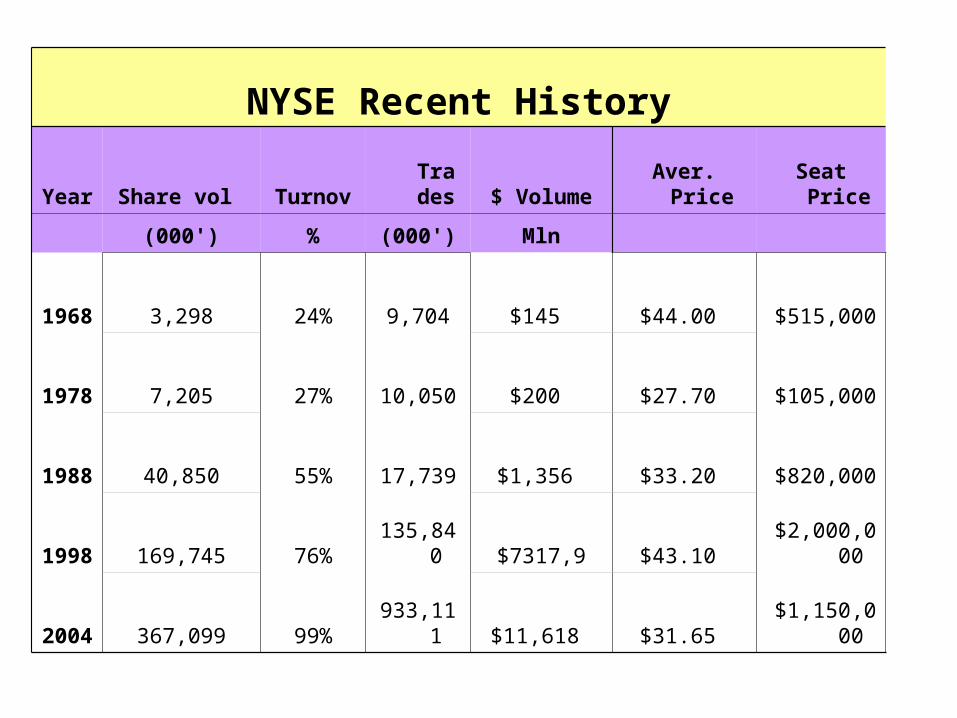

NYSE Recent History

Year Share vol Turnov Trades $ Volume Aver. Price Seat Price

(000') % (000') Mln

1968 3,298 24% 9,704 $145 $44.00 $515,000

1978 7,205 27% 10,050 $200 $27.70 $105,000

1988 40,850 55% 17,739 $1,356 $33.20 $820,000

1998 169,745 76% 135,840 $7317,9 $43.10 $2,000,000

2004 367,099 99% 933,111 $11,618 $31.65 $1,150,000

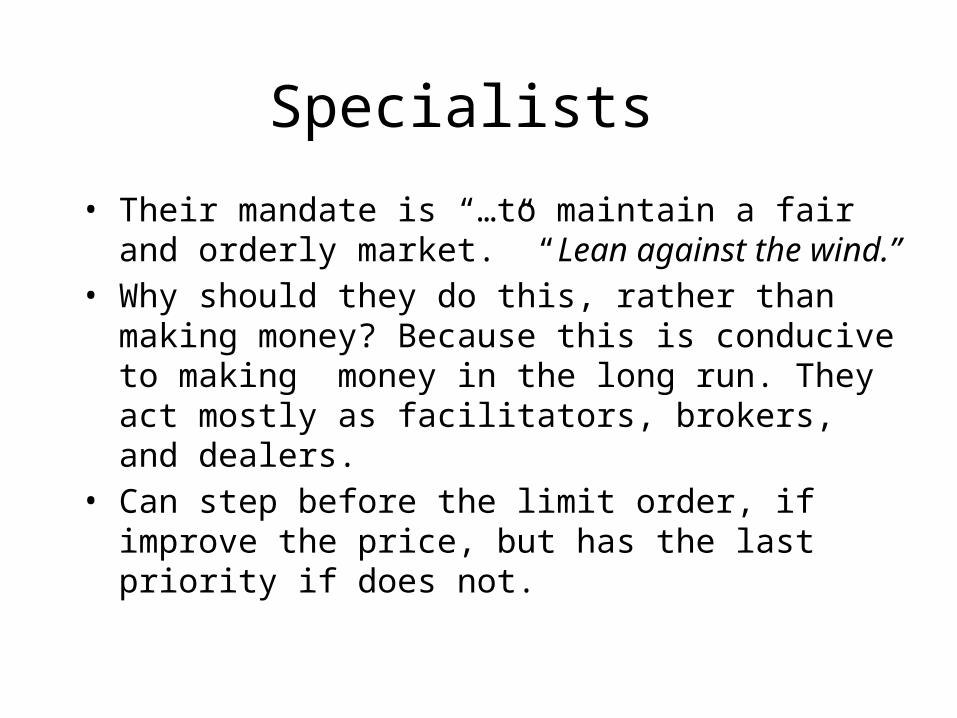

Specialists

• Their mandate is “…to maintain a fair and orderly market.” “Lean against the wind.”

• Why should they do this, rather than making money? Because this is conducive to making money in the long run. They act mostly as facilitators, brokers, and dealers.

• Can step before the limit order, if improve the price, but has the last priority if does not.

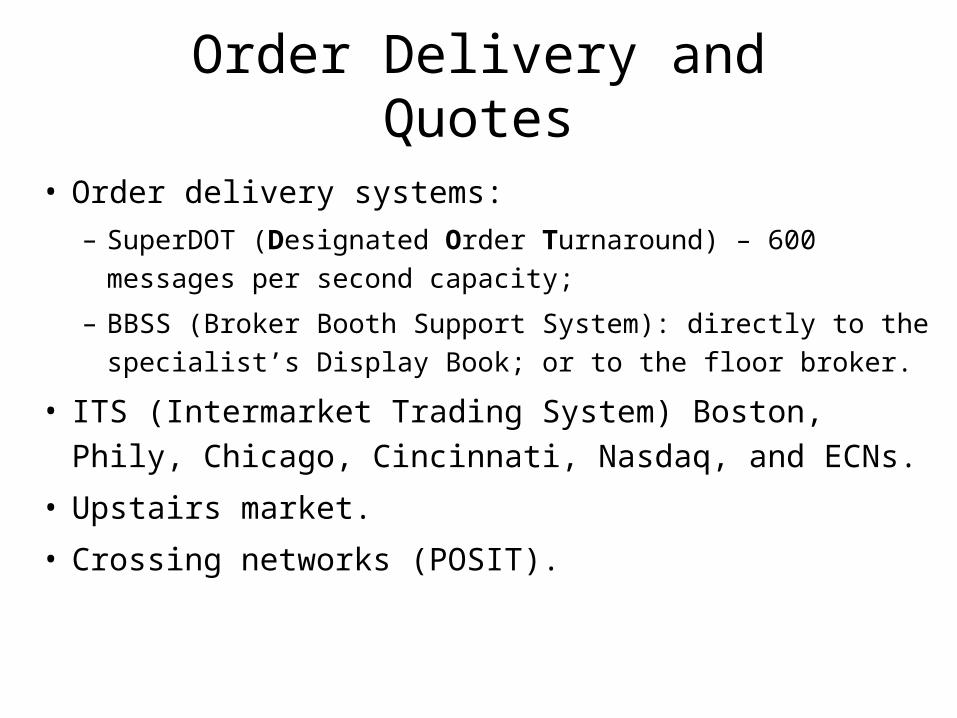

Order Delivery and Quotes

• Order delivery systems:

– SuperDOT (Designated Order Turnaround) – 600 messages per

second capacity;

– BBSS (Broker Booth Support System): directly to the

specialist’s Display Book; or to the floor broker.

• ITS (Intermarket Trading System) Boston, Phily, Chicago,

Cincinnati, Nasdaq, and ECNs.

• Upstairs market.

• Crossing networks (POSIT).

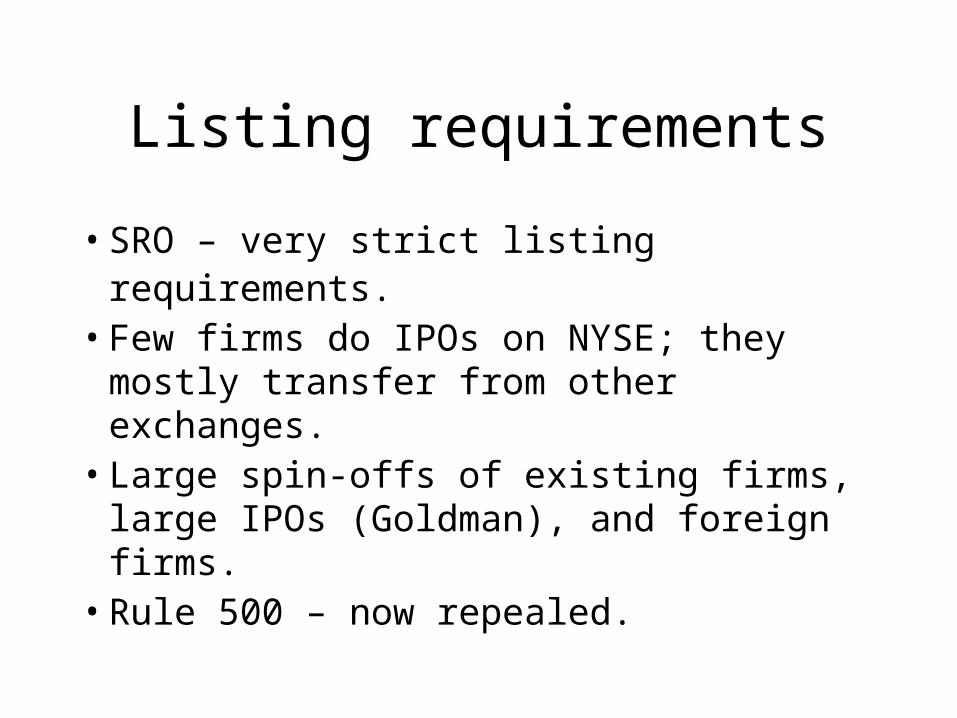

Listing requirements

• SRO – very strict listing requirements.• Few firms do IPOs on NYSE; they

mostly transfer from other exchanges. • Large spin-offs of existing firms, large

IPOs (Goldman), and foreign firms. • Rule 500 – now repealed.

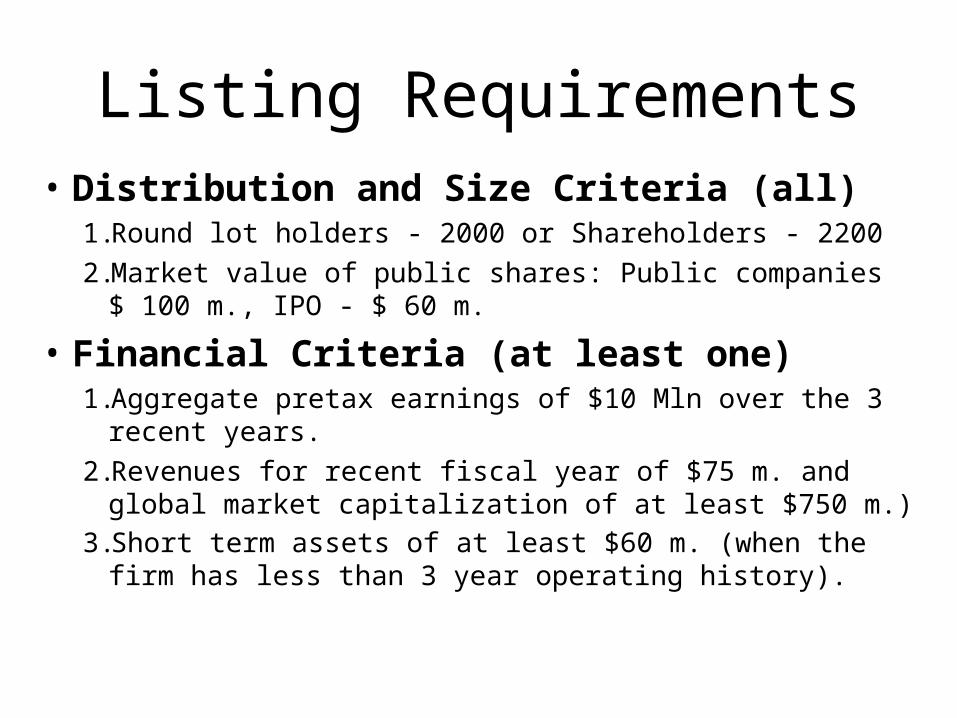

Listing Requirements• Distribution and Size Criteria (all)

1. Round lot holders - 2000 or Shareholders - 2200

2. Market value of public shares: Public companies $ 100 m., IPO - $ 60 m.

• Financial Criteria (at least one)1. Aggregate pretax earnings of $10 Mln over the 3 recent years.

2. Revenues for recent fiscal year of $75 m. and global market capitalization of at least $750 m.)

3. Short term assets of at least $60 m. (when the firm has less than 3 year operating history).

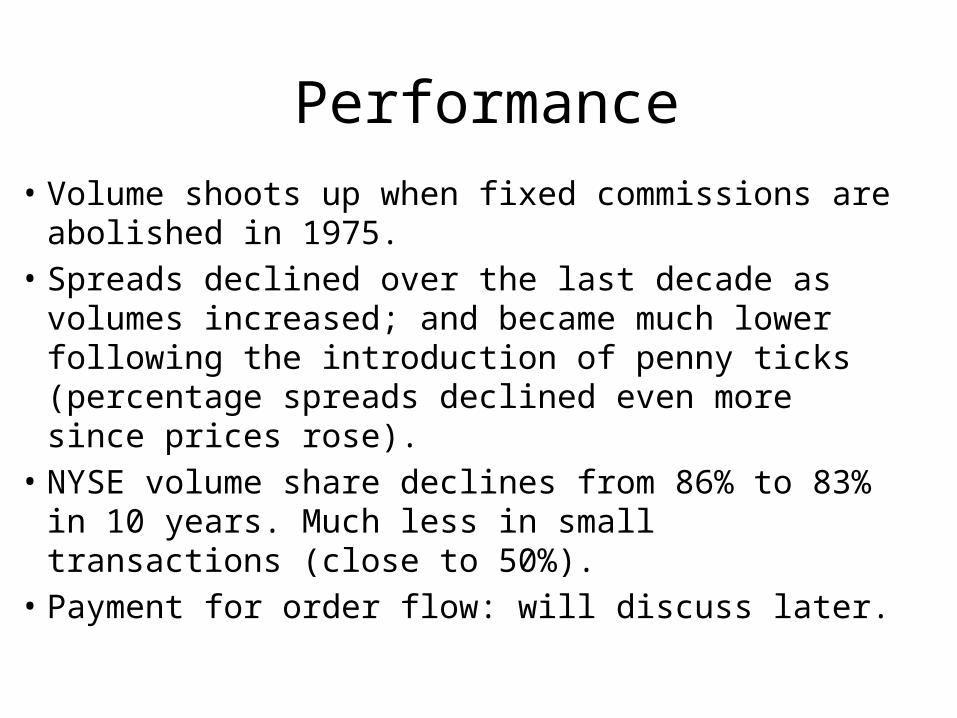

Performance

• Volume shoots up when fixed commissions are abolished in 1975.

• Spreads declined over the last decade as volumes increased; and became much lower following the introduction of penny ticks (percentage spreads declined even more since prices rose).

• NYSE volume share declines from 86% to 83% in 10 years. Much less in small transactions (close to 50%).

• Payment for order flow: will discuss later.

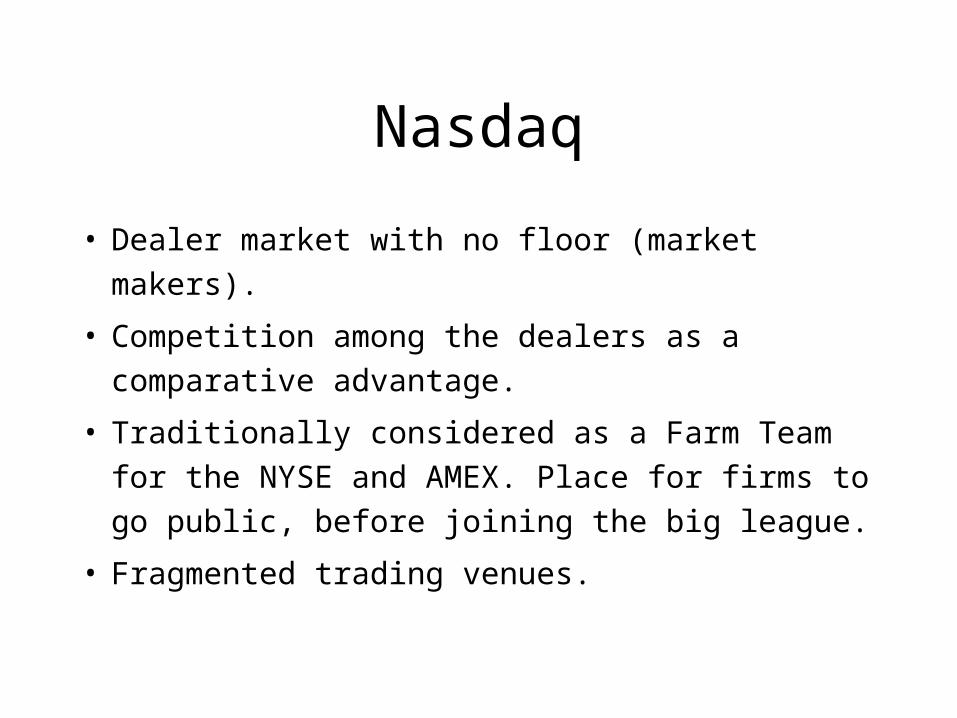

Nasdaq

• Dealer market with no floor (market makers).

• Competition among the dealers as a comparative

advantage.

• Traditionally considered as a Farm Team for the

NYSE and AMEX. Place for firms to go public,

before joining the big league.

• Fragmented trading venues.

Perfect Competition?

• Nasdaq was frequently used in economics classes as an example of a perfectly competitive market:

– homogeneous product – common stock;

– many participants – market makers;

– free entry – easy to become a market maker;

– immediately observable prices, quoted in advance.

• 1994 - 2001 witnessed over 80% decline in spreads, which are the costs of immediacy for small and medium orders. Large orders faired less well.

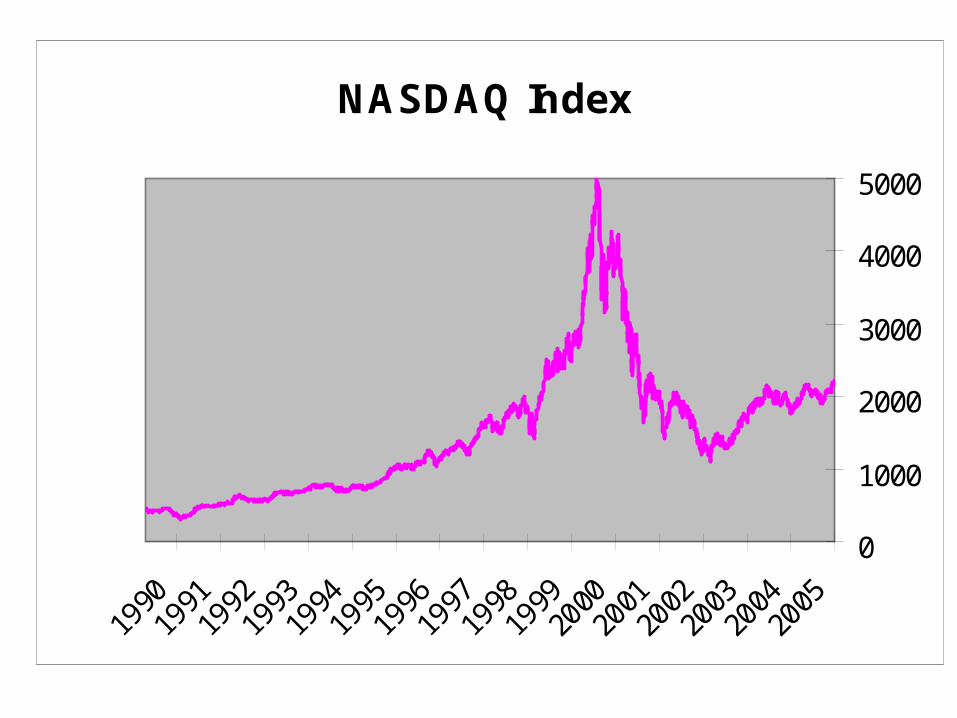

NASDAQ Index

0

1000

2000

3000

4000

5000

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

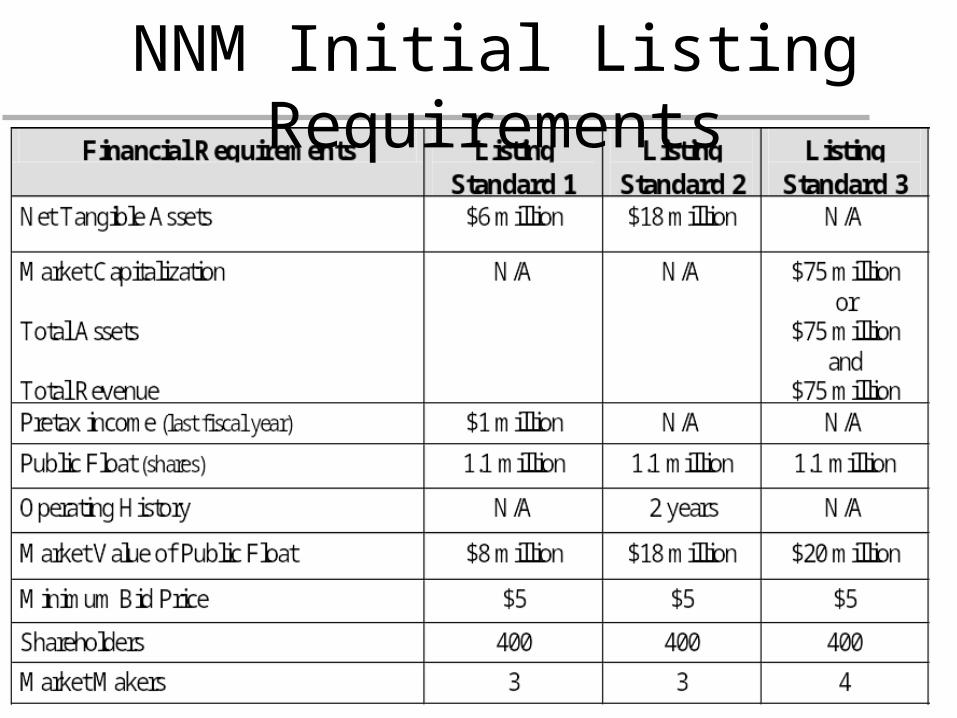

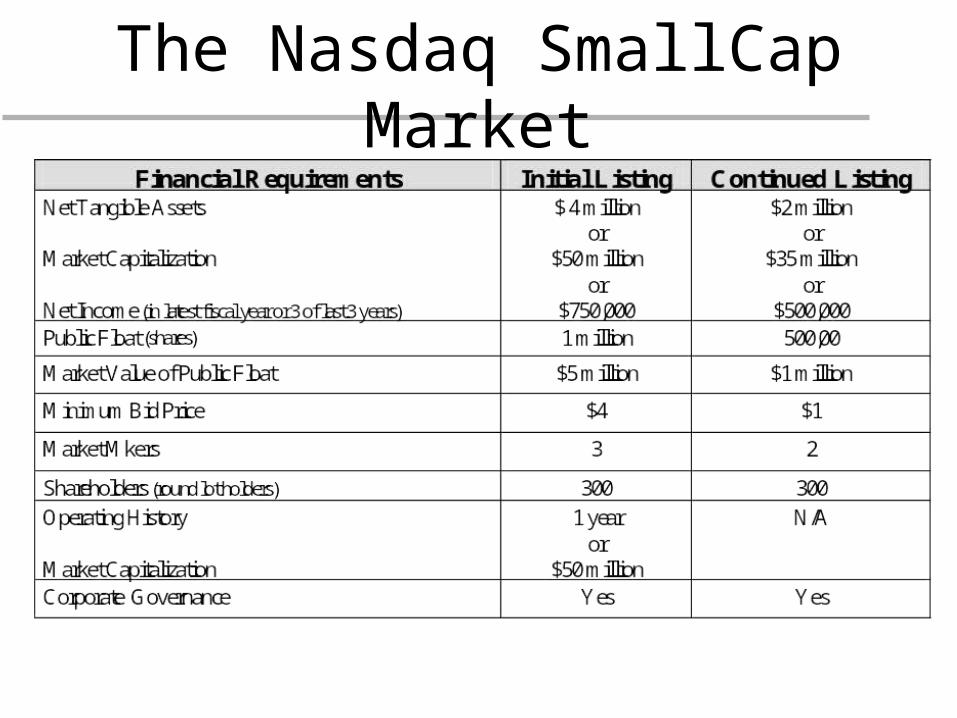

NNM Initial Listing Requirements

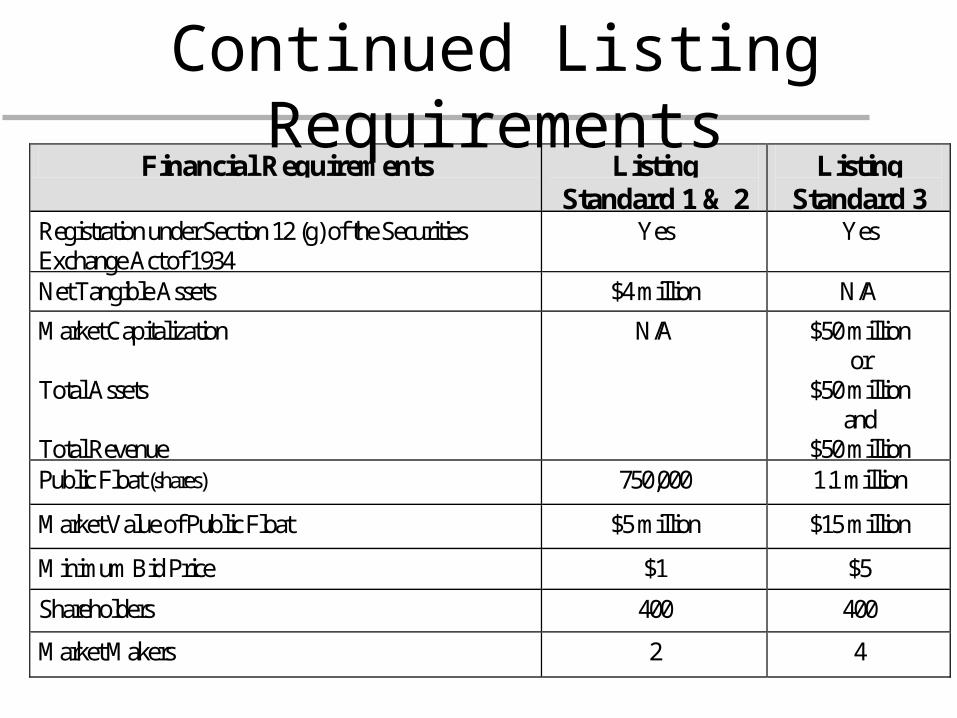

Financial Requirements Listing Standard 1 & 2

Listing Standard 3

Registration under Section 12 (g) of the Securities Exchange Act of 1934

Yes Yes

Net Tangible Assets $4 million N/A

Market Capitalization Total Assets Total Revenue

N/A $50 million or

$50 million and

$50 million Public Float (shares) 750,000 1.1 million

Market Value of Public Float $5 million $15 million

Minimum Bid Price $1 $5

Shareholders 400 400

Market Makers 2 4

Continued Listing Requirements

The Nasdaq SmallCap Market

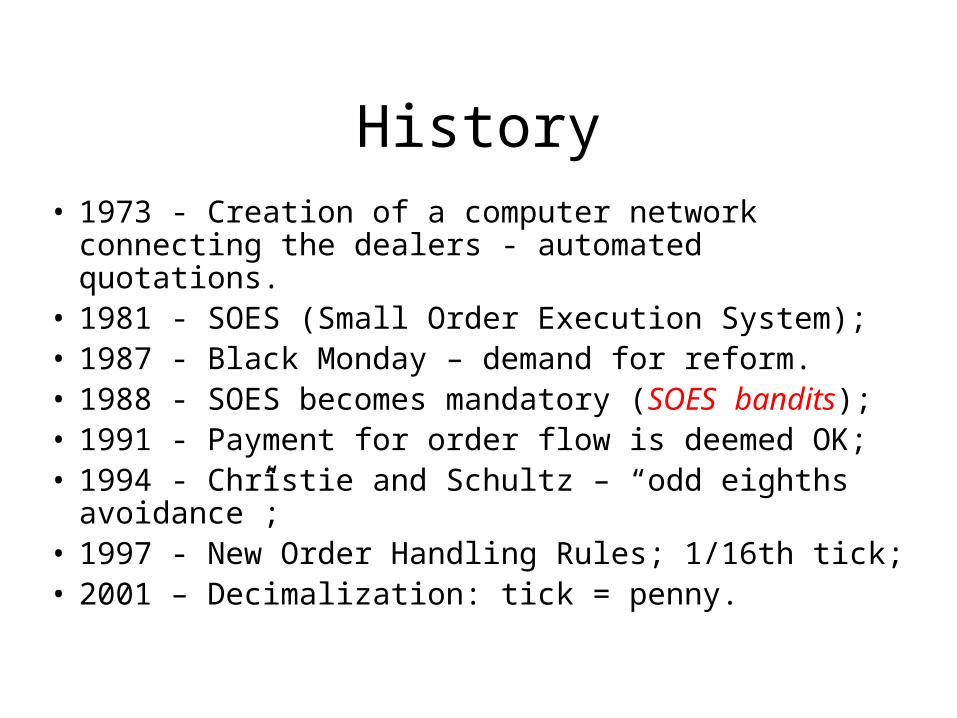

History• 1973 - Creation of a computer network connecting the

dealers - automated quotations.• 1981 - SOES (Small Order Execution System);• 1987 - Black Monday – demand for reform.• 1988 - SOES becomes mandatory (SOES bandits);• 1991 - Payment for order flow is deemed OK;• 1994 - Christie and Schultz – “odd eighths avoidance”;• 1997 - New Order Handling Rules; 1/16th tick;• 2001 – Decimalization: tick = penny.

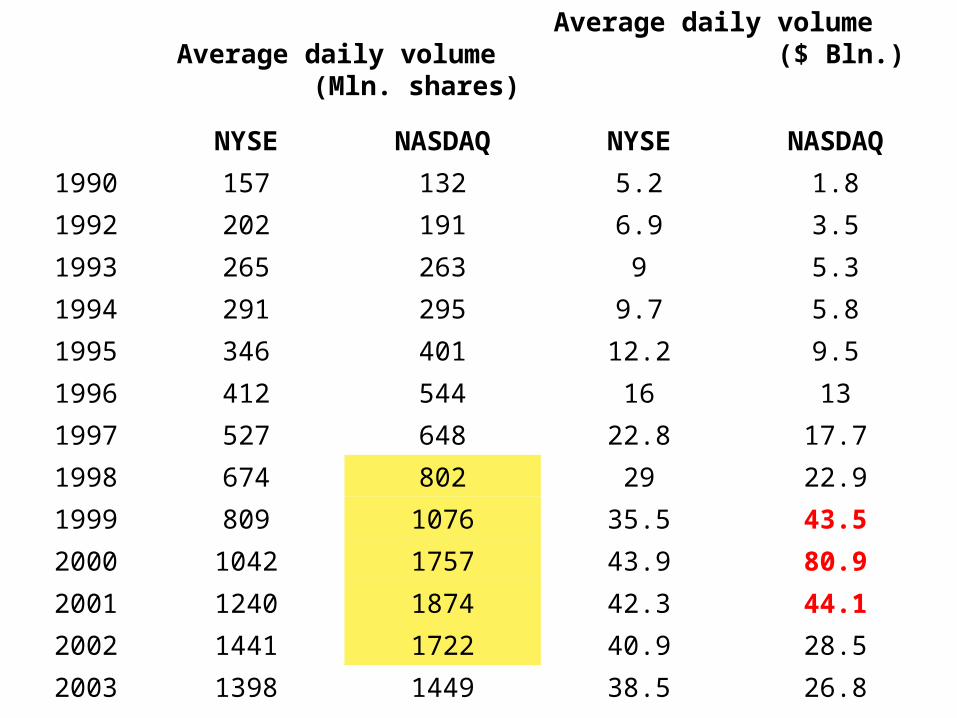

Average daily volume (Mln. shares)

Average daily volume ($ Bln.)

NYSE NASDAQ NYSE NASDAQ

1990 157 132 5.2 1.8

1992 202 191 6.9 3.5

1993 265 263 9 5.3

1994 291 295 9.7 5.8

1995 346 401 12.2 9.5

1996 412 544 16 13

1997 527 648 22.8 17.7

1998 674 802 29 22.9

1999 809 1076 35.5 43.5

2000 1042 1757 43.9 80.9

2001 1240 1874 42.3 44.1

2002 1441 1722 40.9 28.5

2003 1398 1449 38.5 26.8

2004 1457 1259 46.1 27.2

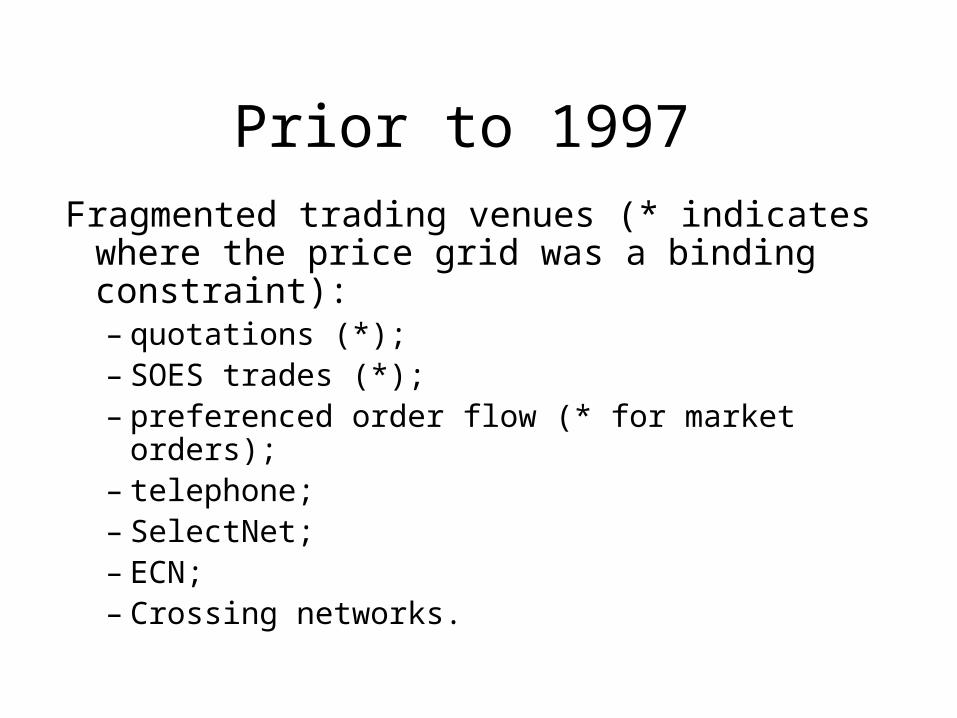

Prior to 1997

Fragmented trading venues (* indicates where the price grid was a binding constraint):– quotations (*);– SOES trades (*);– preferenced order flow (* for market orders);– telephone;– SelectNet;– ECN;– Crossing networks.

Digressions

• Tick size and its effects.

• “Odd eighths avoidance” – not a trivial matter.

• Payment for order flow and its effects on the

markets.

Tick Size

• Minimal price increment imposed by the

exchange. History.

• Constraint on prices.

• Could be beneficial to investors, but in

many cases is detrimental.

• Monopoly versus competition.

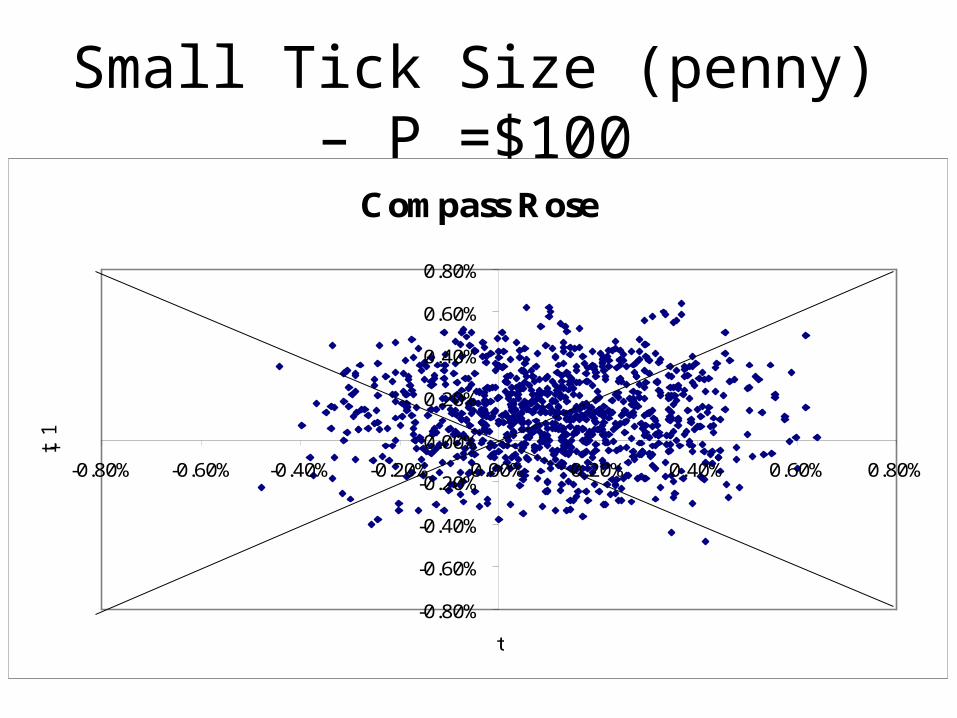

Small Tick Size (penny) – P =$100

Compass Rose

-0.80%

-0.60%

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%

0.80%

-0.80% -0.60% -0.40% -0.20% 0.00% 0.20% 0.40% 0.60% 0.80%

t

t +1

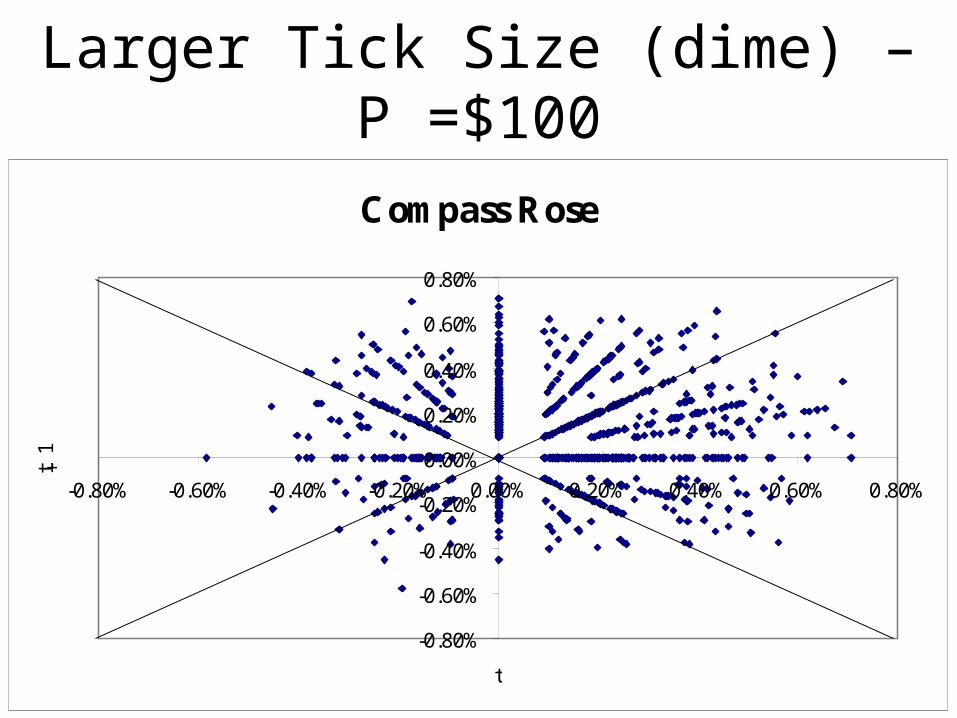

Larger Tick Size (dime) – P =$100

Compass Rose

-0.80%

-0.60%

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%

0.80%

-0.80% -0.60% -0.40% -0.20% 0.00% 0.20% 0.40% 0.60% 0.80%

t

t +1

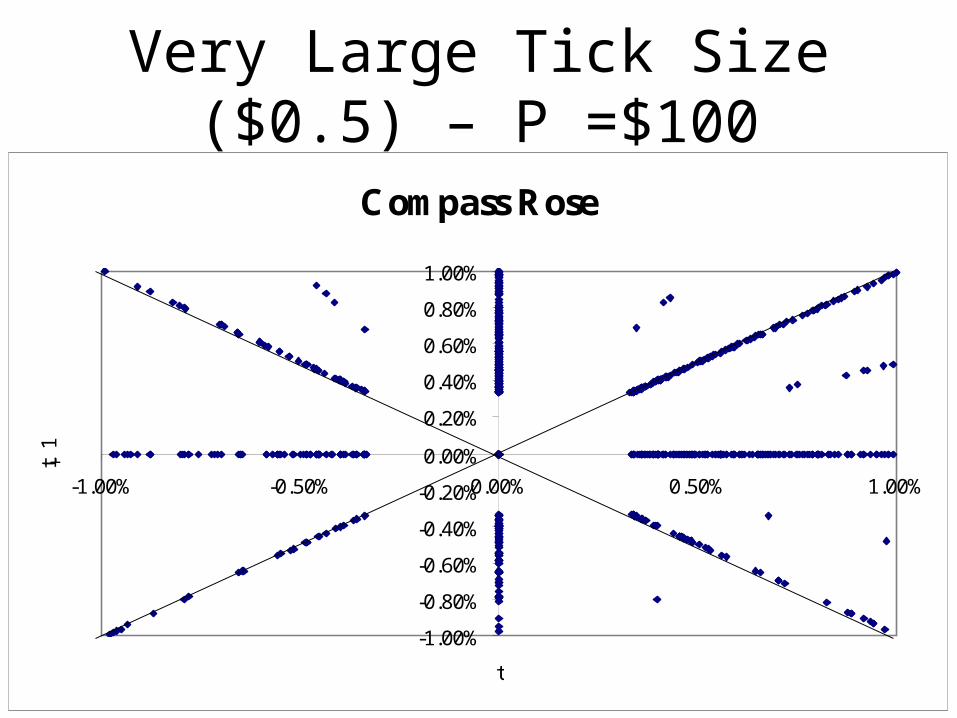

Very Large Tick Size ($0.5) – P =$100

Compass Rose

-1.00%

-0.80%

-0.60%

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

-1.00% -0.50% 0.00% 0.50% 1.00%

t

t +1

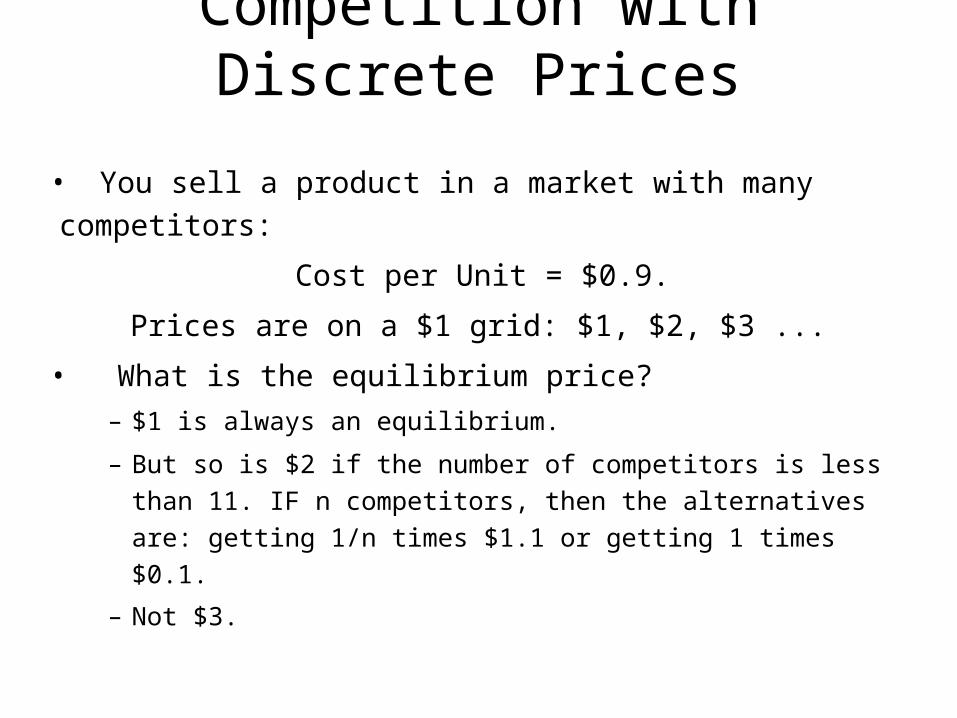

Competition with Discrete Prices

• You sell a product in a market with many competitors:

Cost per Unit = $0.9.

Prices are on a $1 grid: $1, $2, $3 ...

• What is the equilibrium price?

– $1 is always an equilibrium.

– But so is $2 if the number of competitors is less than 11. IF

n competitors, then the alternatives are: getting 1/n times

$1.1 or getting 1 times $0.1.

– Not $3.

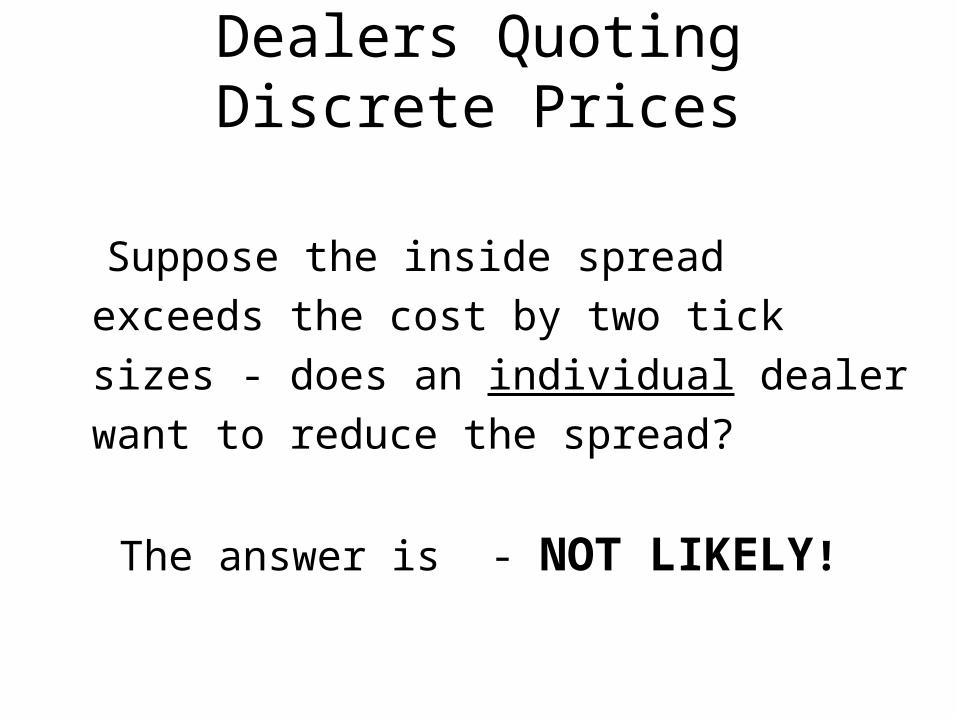

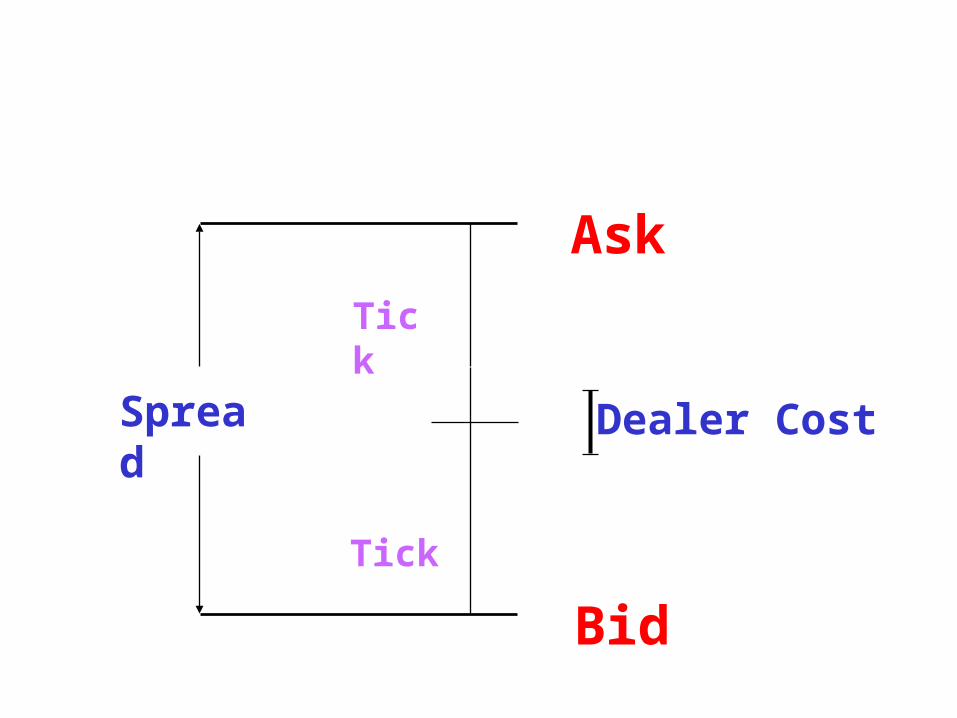

Dealers Quoting Discrete Prices

Suppose the inside spread exceeds the

cost by two tick sizes - does an individual

dealer want to reduce the spread?

The answer is - NOT LIKELY!

Ask

Bid

Dealer Cost

Tick

Tick

Spread

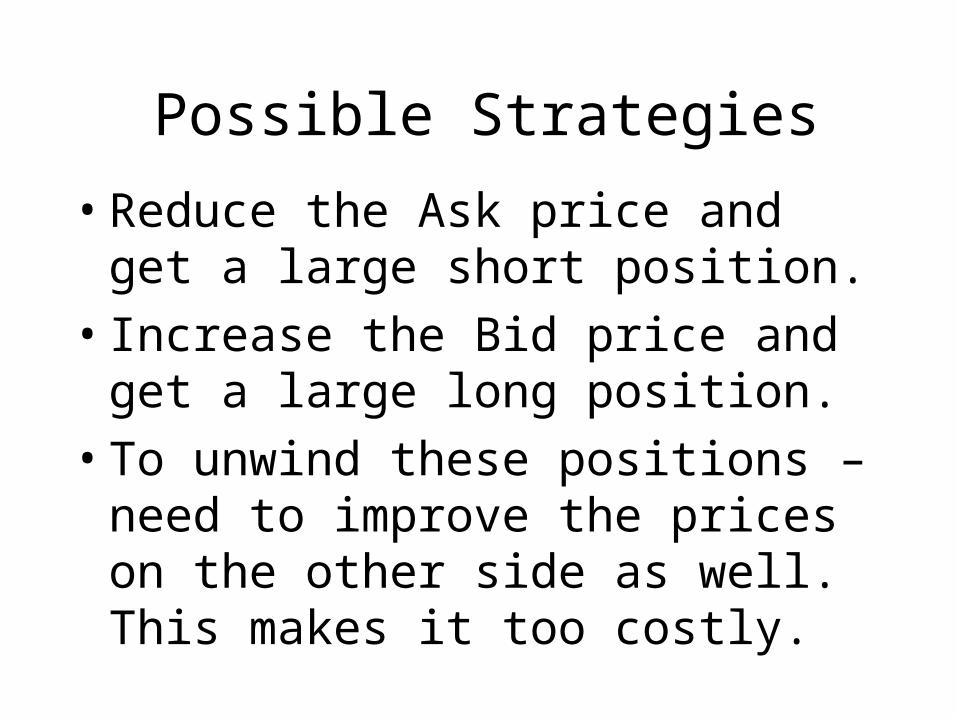

Possible Strategies

• Reduce the Ask price and get a large short position.

• Increase the Bid price and get a large long position.

• To unwind these positions – need to improve the prices on the other side as well. This makes it too costly.

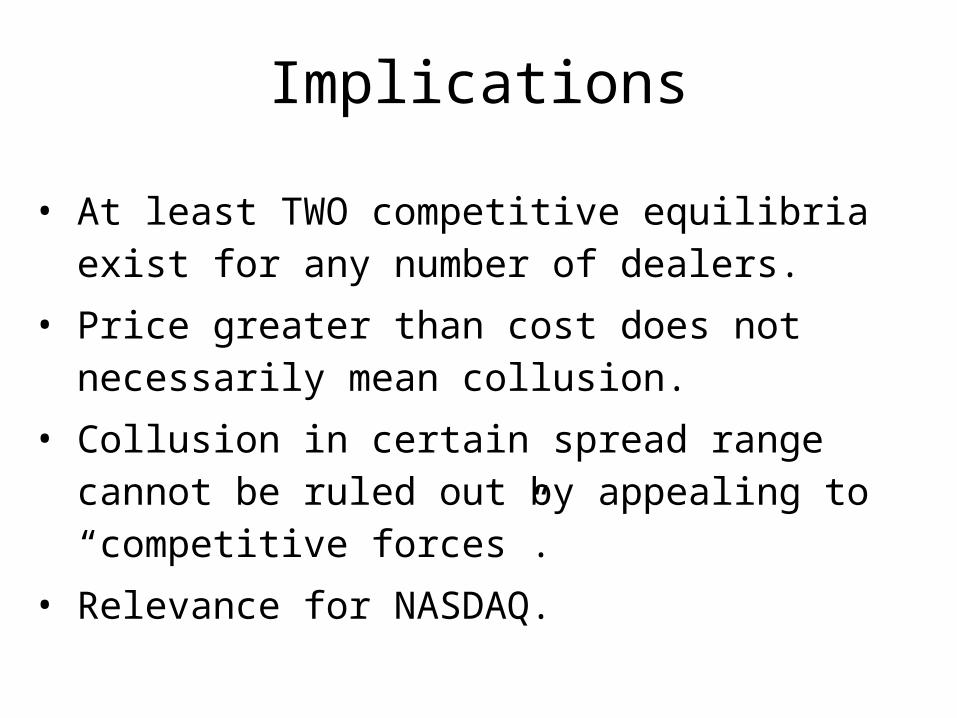

Implications

• At least TWO competitive equilibria exist for any number of dealers.

• Price greater than cost does not necessarily mean collusion.

• Collusion in certain spread range cannot be ruled out by appealing to “competitive forces”.

• Relevance for NASDAQ.

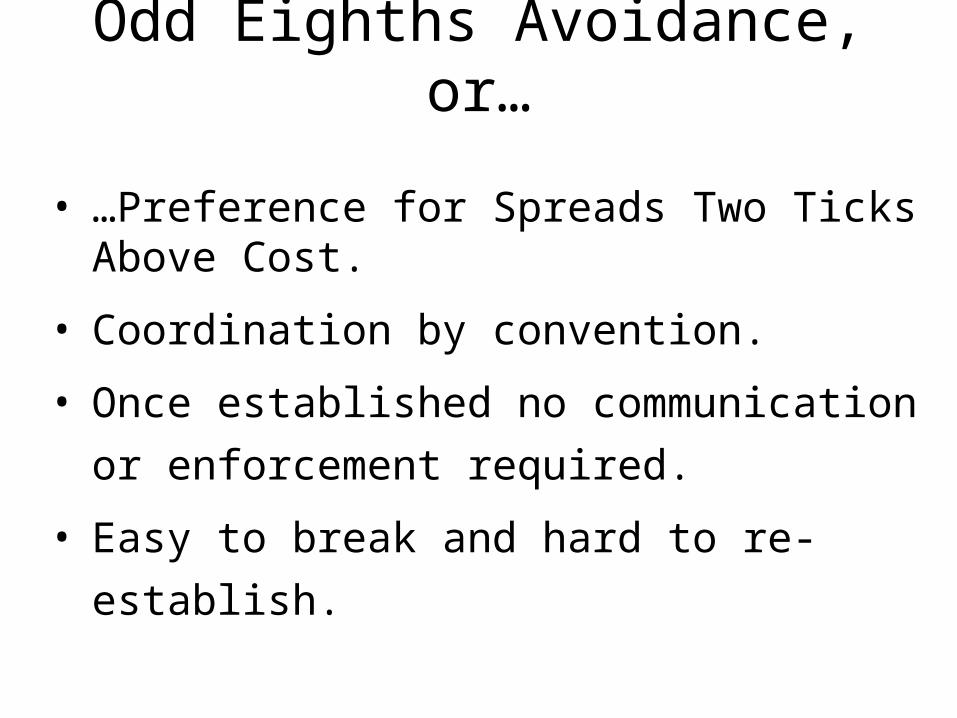

Odd Eighths Avoidance, or…

• …Preference for Spreads Two Ticks Above Cost.

• Coordination by convention.

• Once established no communication or

enforcement required.

• Easy to break and hard to re-establish.

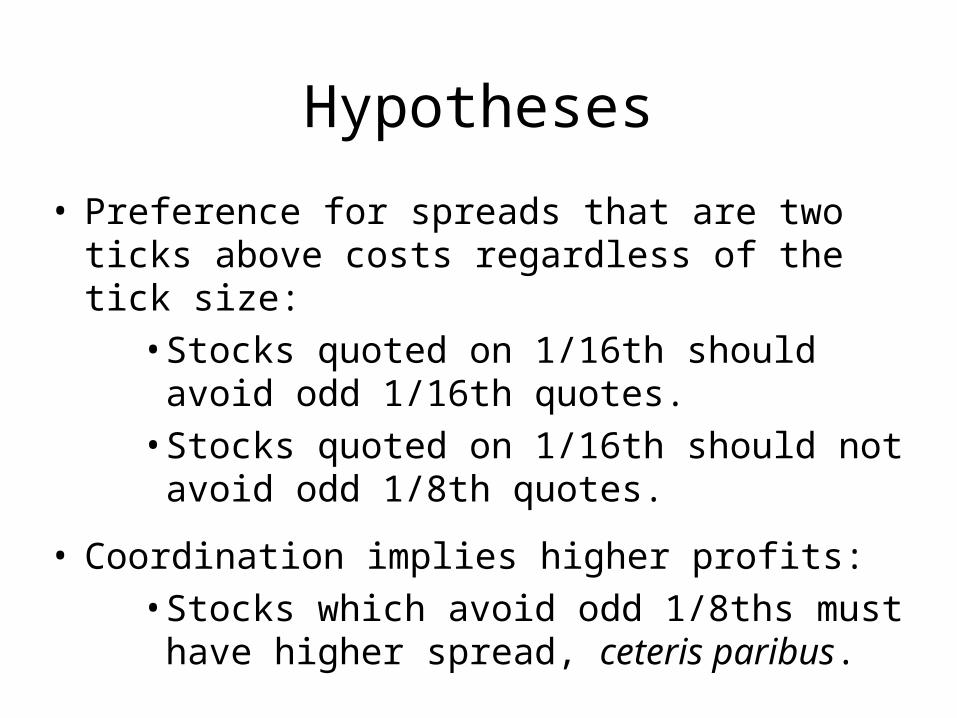

Hypotheses

• Preference for spreads that are two ticks above costs regardless of the tick size:

• Stocks quoted on 1/16th should avoid odd 1/16th quotes.

• Stocks quoted on 1/16th should not avoid odd 1/8th quotes.

• Coordination implies higher profits:• Stocks which avoid odd 1/8ths must have higher

spread, ceteris paribus.

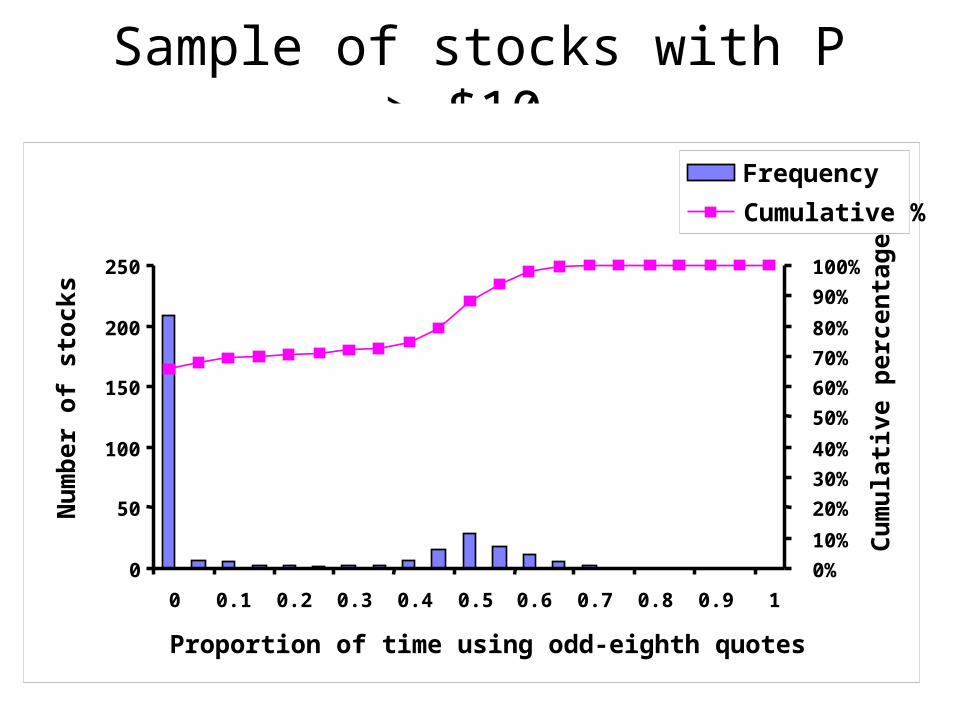

Sample of stocks with P > $10.

0

50

100

150

200

250

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Proportion of time using odd-eighth quotes

Nu

mb

er o

f st

ock

s

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cu

mu

lati

ve p

erce

nta

ge

Frequency

Cumulative %

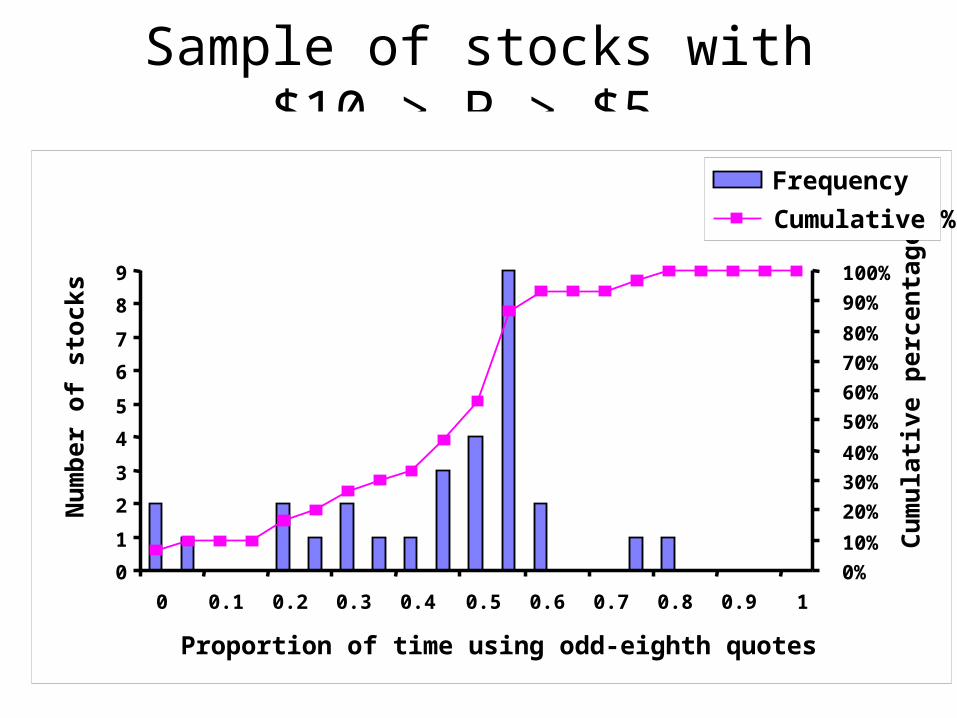

Sample of stocks with $10 > P > $5.

0

1

2

3

4

5

6

7

8

9

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Proportion of time using odd-eighth quotes

Nu

mb

er o

f st

ock

s

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cu

mu

lati

ve p

erce

nta

ge

Frequency

Cumulative %

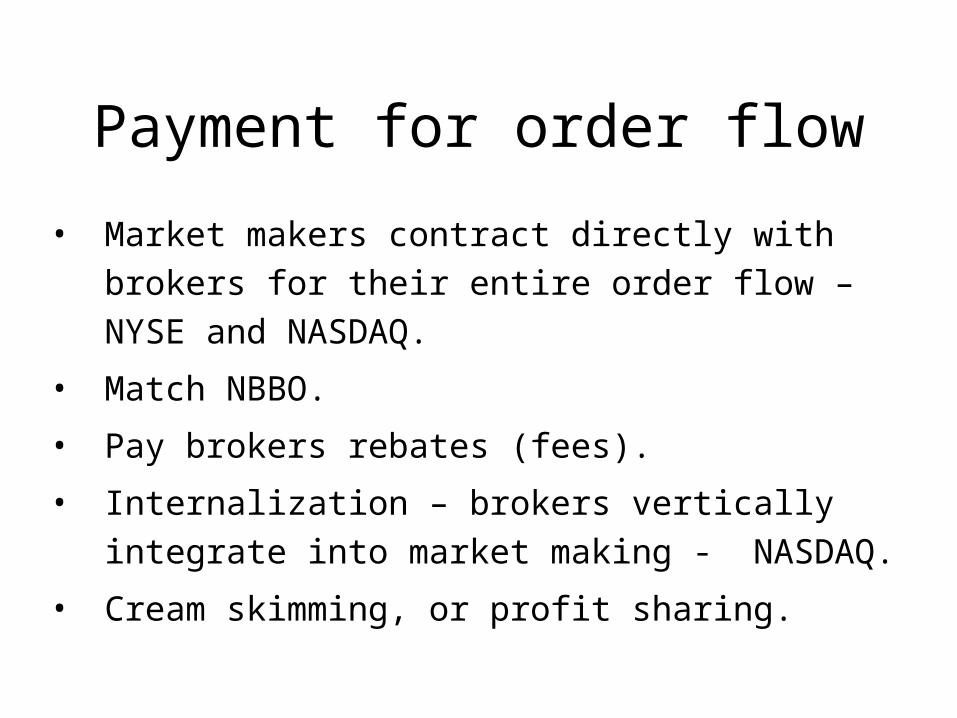

Payment for order flow

• Market makers contract directly with brokers for

their entire order flow – NYSE and NASDAQ.

• Match NBBO.

• Pay brokers rebates (fees).

• Internalization – brokers vertically integrate into

market making - NASDAQ.

• Cream skimming, or profit sharing.

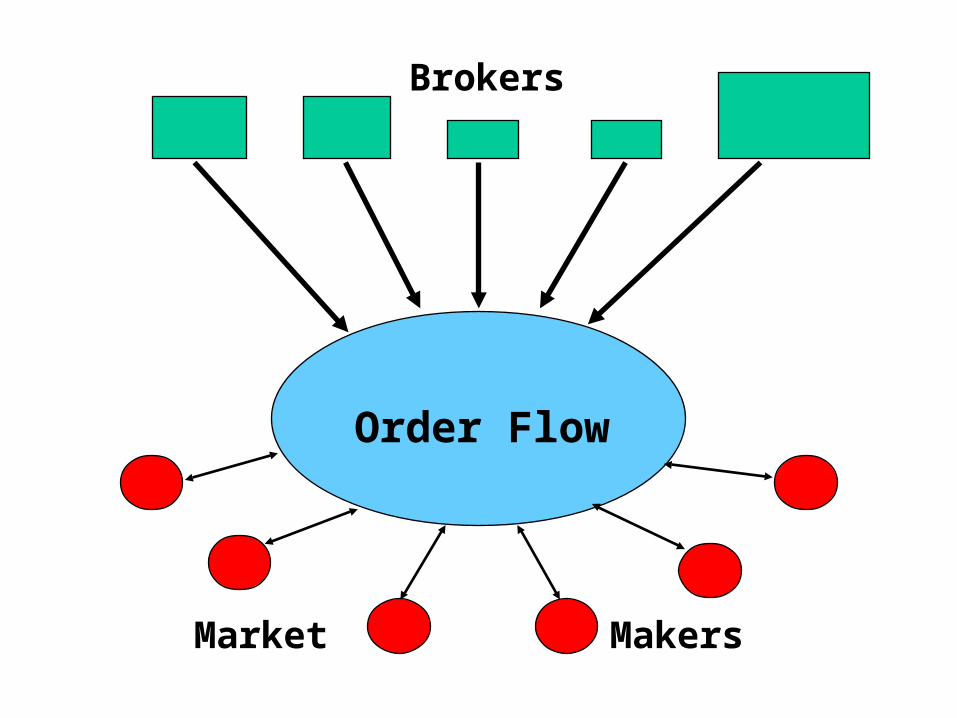

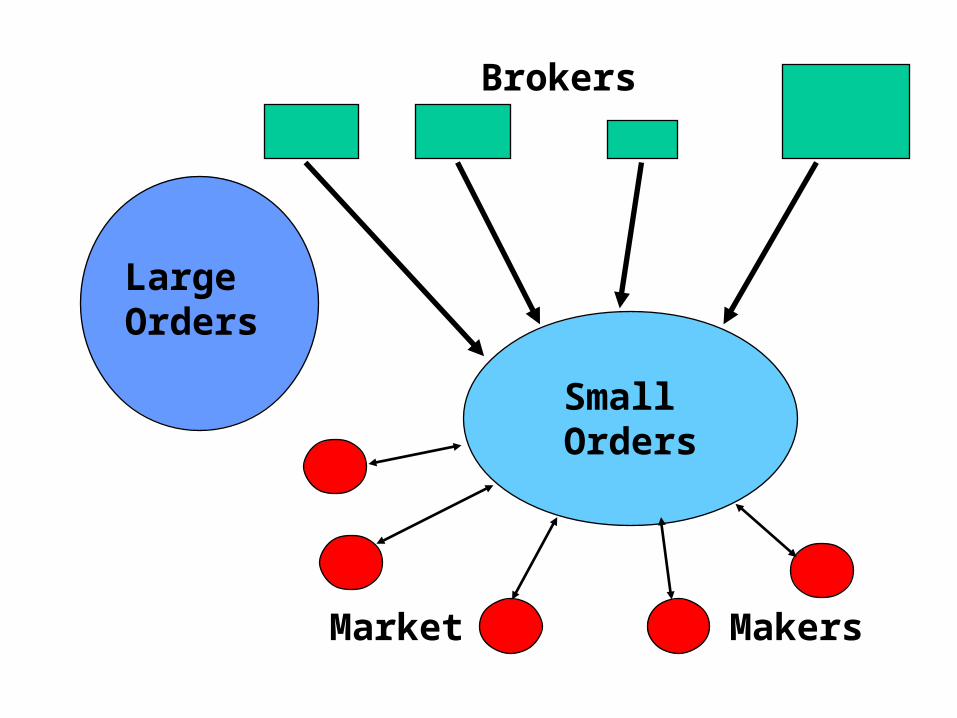

Brokers

Market Makers

Order Flow

Brokers

Market Makers

Large Orders

Small Orders

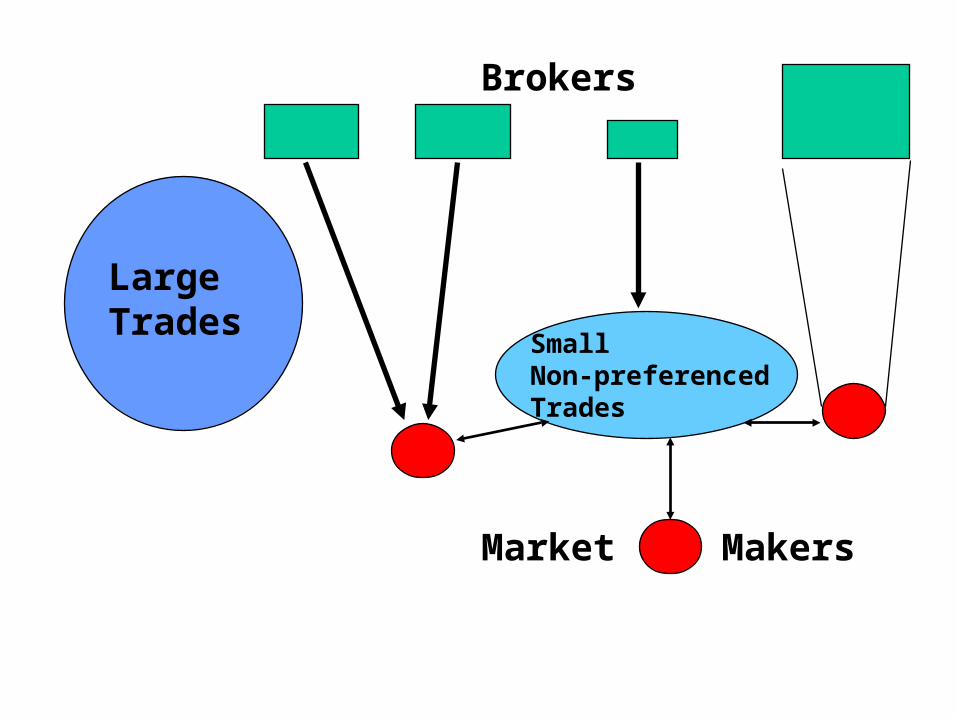

Brokers

Market Makers

Large Trades

Small Non-preferenced Trades

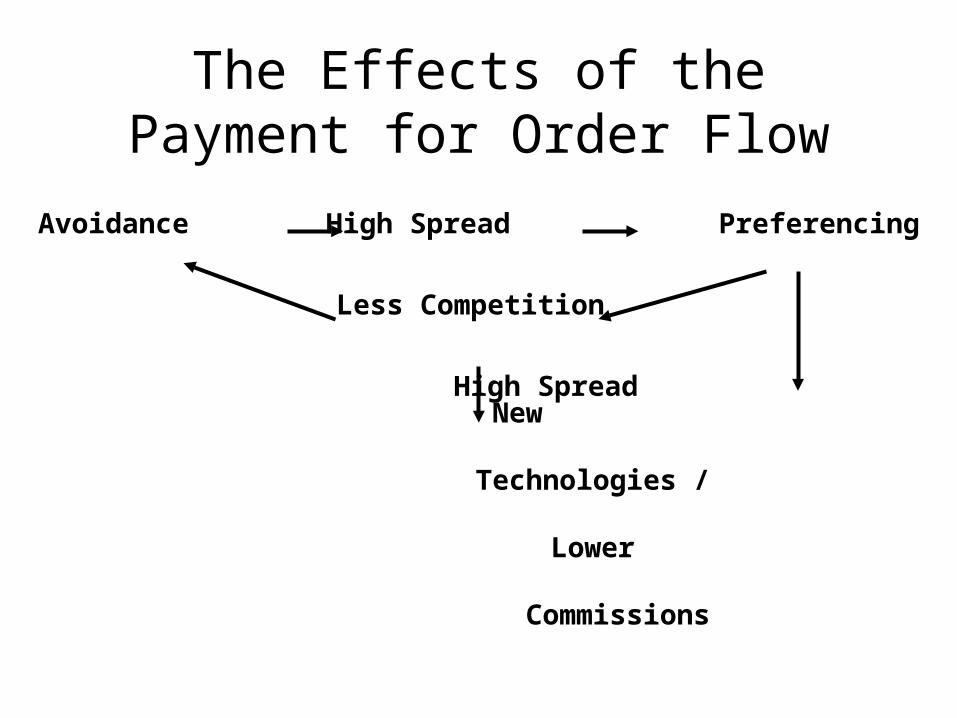

The Effects of the Payment for Order Flow

Avoidance High Spread Preferencing

Less Competition

High Spread New

Technologies /

Lower

Commissions

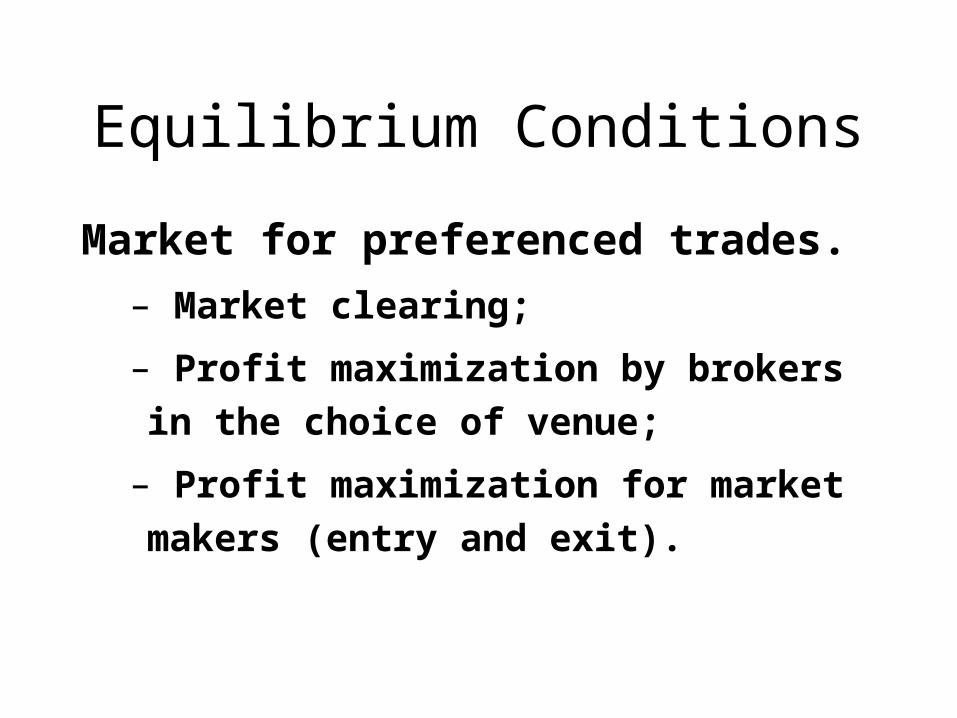

Equilibrium Conditions

Market for preferenced trades.

– Market clearing;

– Profit maximization by brokers in the choice of

venue;

– Profit maximization for market makers (entry

and exit).

Equilibrium

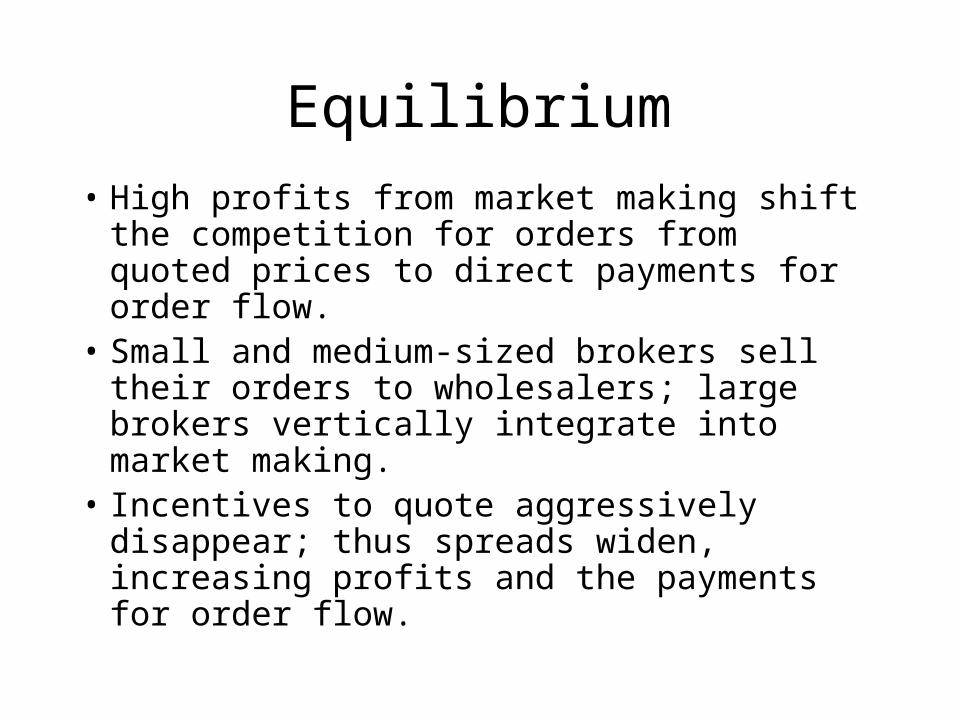

• High profits from market making shift the competition for orders from quoted prices to direct payments for order flow.

• Small and medium-sized brokers sell their orders to wholesalers; large brokers vertically integrate into market making.

• Incentives to quote aggressively disappear; thus spreads widen, increasing profits and the payments for order flow.

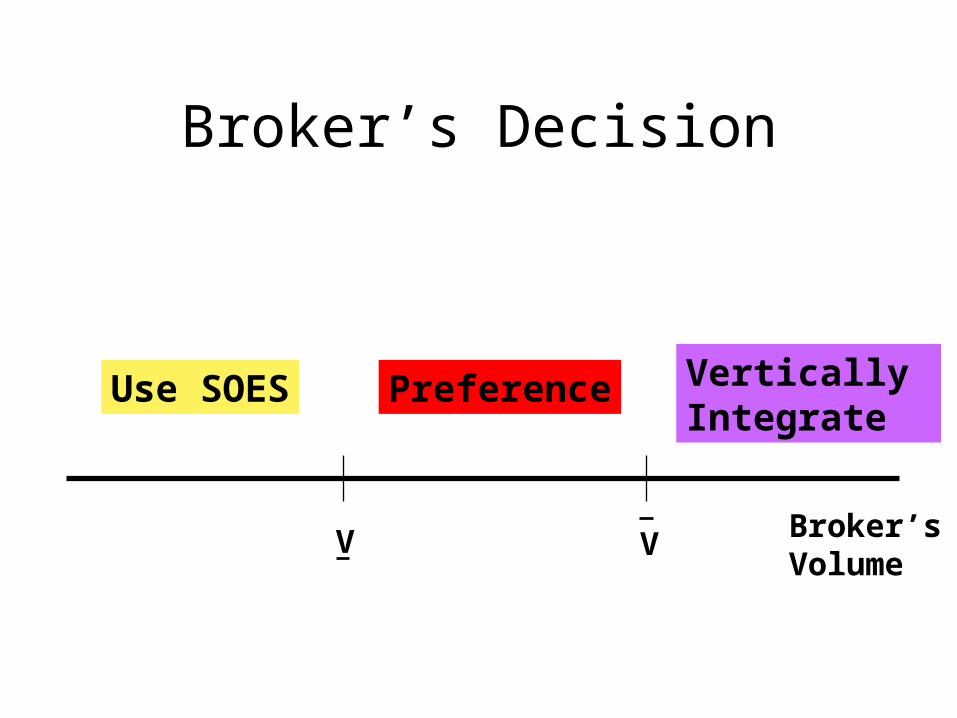

Broker’s Decision

Broker’sVolume

V V

Use SOES Preference Vertically Integrate

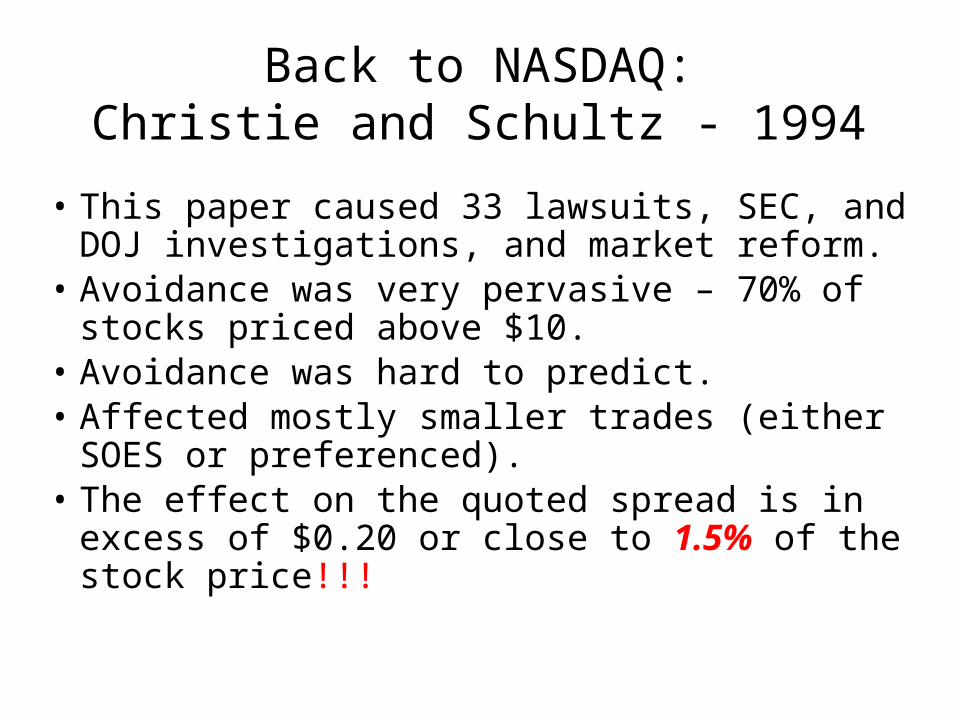

Back to NASDAQ:Christie and Schultz - 1994

• This paper caused 33 lawsuits, SEC, and DOJ investigations, and market reform.

• Avoidance was very pervasive – 70% of stocks priced above $10.

• Avoidance was hard to predict. • Affected mostly smaller trades (either SOES or

preferenced). • The effect on the quoted spread is in excess of

$0.20 or close to 1.5% of the stock price!!!

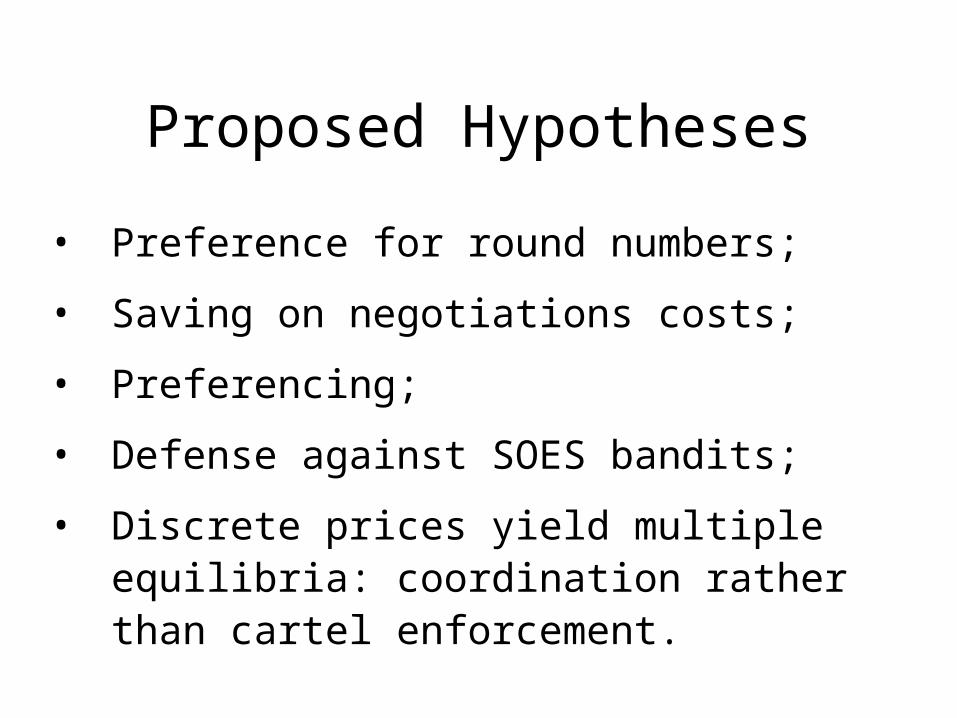

Proposed Hypotheses

• Preference for round numbers;

• Saving on negotiations costs;

• Preferencing;

• Defense against SOES bandits;

• Discrete prices yield multiple equilibria: coordination rather than cartel enforcement.

Day Traders / SOES Bandits

• “Parasitic” traders, that utilize small changes in the price of the stock to make many trades during the day.

• SOES bandits – use technology to make money off the dealer’s quotes.

• Nuisance, but unlikely to account for the odd-eighths avoidance.

Outcome • Settlements:

• DoJ – NASDAQ pays a $100 Mln. Fine and agrees to invest $400 Mln. In the enforcement of Antitrust.

• SEC introduces New Order Handling Rules.

• $1.25Bln in the civil suit.

• New OHR start in Jan 1997:• Limit orders receive preference;

• Dealers other quotes are shown,

• Less market fragmentation,

New Order Handling Rules

• Spreads decline by 27%; • Volume does not change; • Volatility does not change, • The ex post measured cost of trading declines

for all trade sizes. • Conservatively estimated savings for investors:

$2–5 Bln. annually (more, if relative to 1994).

Nasdaq today

• The sponsorship hypothesis.

• NASDAQ as a trading venue or as a listing

platform: two battlefields.

• ECNs as the main competitors to NASDAQ.

• Crossing networks.

• AMEX acquisition.

• INET (Island) acquisition. http://www.island.com/subscribers/emailarchive/2005/20050422.asp

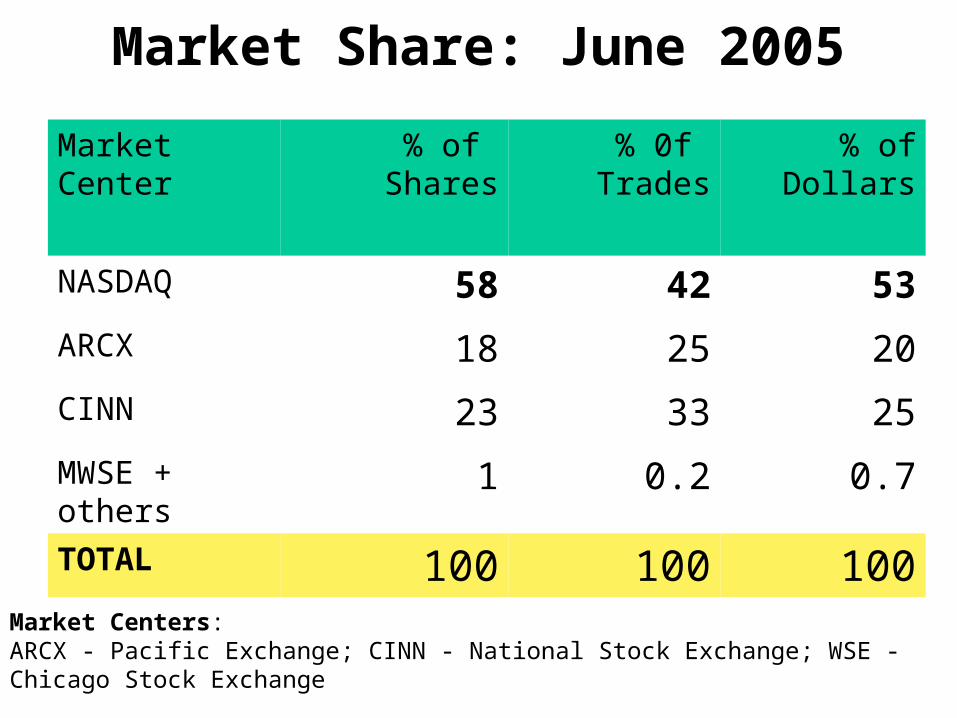

Market Share: June 2005

Market Center

% of Shares

% 0f Trades

% of Dollars

NASDAQ 58 42 53

ARCX 18 25 20

CINN 23 33 25

MWSE + others 1 0.2 0.7

TOTAL 100 100 100

Market Centers: ARCX - Pacific Exchange; CINN - National Stock Exchange; WSE - Chicago Stock Exchange

Conclusions

• Competition is a fragile creature: one must provide it with the right conditions.

• Competition takes many forms.• Very important to pay attention to small

details – they may determine the outcomes.

• Self-regulation sometimes needs help: the reduction of the tick size in 1997 and 2001.

Exercise IV

• Download the evolution of the market share

statistics from the NASDAQ Website:

www.nasdaq.com/newsroom/stats/Performance_Report.stm#item_1

• Provide a brief explanation(s) for the changes

that took place in the NASDAQ market share

over the last couple of years. Be brief.