Embed Size (px)

Citation preview

Lecture 4

Various Interest Rates

Various Interest Rates and Their Relationships An interest rates is the price to exchange

money tomorrow for money today Spot rates, yields, and forward rates are

different ways to express the same information about interest rates We will show that they are equivalent

Yields Spot Rates Forward Rates

Spot Rates “Spot rate” is an interest rate

applicable for a specific time period Use 5-year spot rate if cash flow is in 5

years No intermediate cash flows on CDs

Also called zero coupon rates Zero coupon bonds pay only face value

back at maturity

Spot Rate Example

Find PV(1) $100 to be paid in one year(2) $200 to be paid in three years(3) $300 to be paid each year for two

years

Time Spot Rate

1 year 5.0%

2 years 6.0%

3 years 7.0%

Spot Rate Solutions (p.1)

Discount cash flows to be paid at the end of the first year at the 1-year spot rate If paid in two years, discount using the 2-

year spot rate

71.55206.1

300

05.1

30023 PV

24.9505.1

1001 PV

26.16307.1

20032 PV

Spot Rate Solutions (p.2)

What is the price of a 3-year, 8% annual coupon bond that has a face value of $100?

05.1

8Price

307.1

108

206.1

8 90.102

Yield-to-maturity (YTM)

Used in bond markets Same discount rate applied to ALL

cash flows of a single bond What is the proper discount rate that

equates the present value of cash flows with the observed market price?

YTM example Our example bond had a price of

$102.90 3-year, 8% annual coupon, $100 face value

Determine the yield: solve for y

%9.6

90.1021

108

1

8

1

8321

y

yyy

• Yield on a three-year bond is actually a blend of the spot rates at years 1, 2, and 3

- Cash flows at each time

Determining Spot Rates From Yields

Spot rates are typically available for short maturities

For longer horizons, yields are provided on coupon-paying bonds

Suppose the 1-year spot rate is 8% and the 2-year spot rate is 9.5%

A $10,000 face value, 3-year, 10% annual coupon bond yields 12% Find the 3-year spot rate

Example:Spot Rates from Yields

The yield is the discount rate for all cash flows

63.519,9

12.1

000,10000,1

12.1

000,1

12.1

000,1Price 32

Example: Decompose the coupon bond Note that a 3-year bond is really

three zero coupon bonds

$1,000 $1,000 $10,000+$1,000

Time 1 2 3

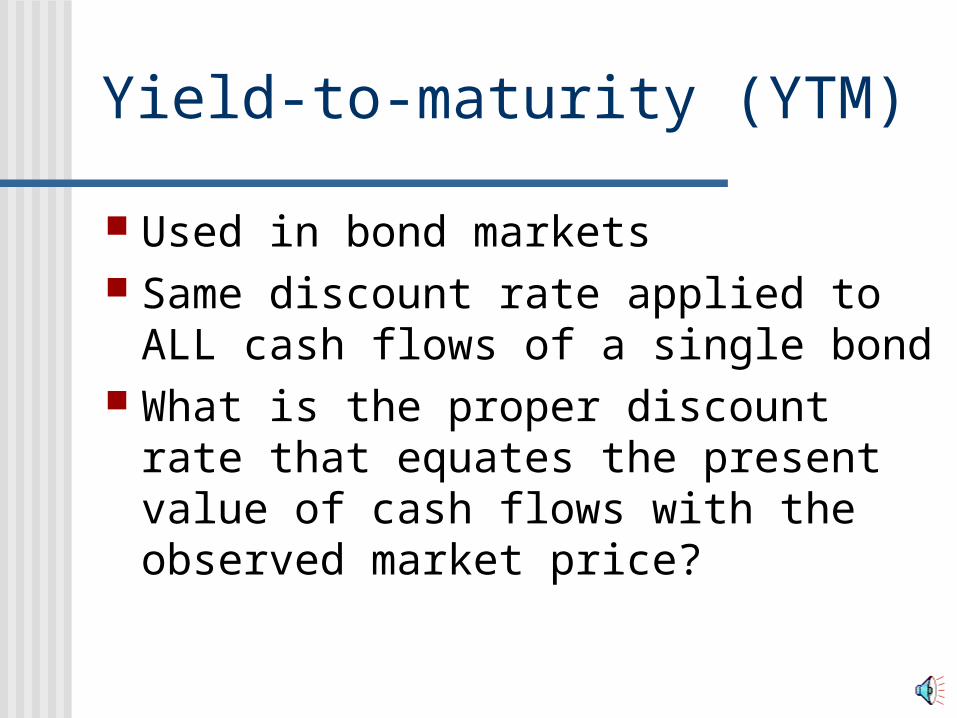

Example: Equating the two pricing approaches

Instead of using the yield to discount, let’s use the zero coupon rates that we know

Find the 3-year zero coupon rate

33)1(

000,11

r

%3.123 r

63.519,9 08.1

000,1 2095.1

000,1

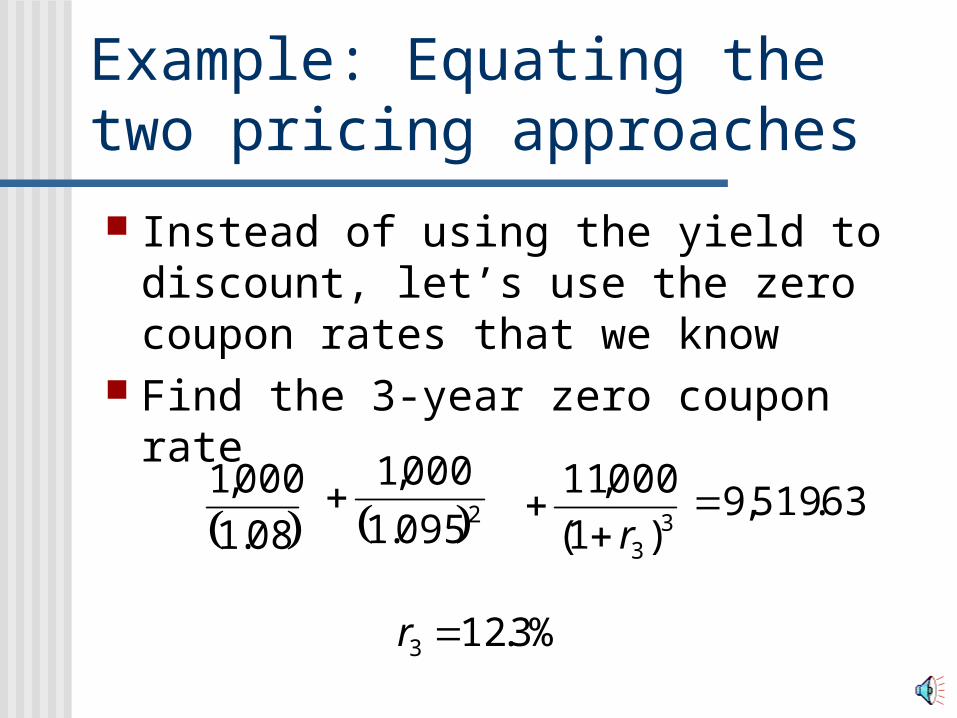

Spot vs. Forward rates

The “spot rate” is the interest rate that is observed today 1 year spot rate, 2 year spot rate, etc

The “forward rate” is a rate that is agreed to today that applies to a future period The one year rate, one year from now The two year rate, three years from

nowyears in starting rate forward year -m n fm n

Spot Rates to Forward Rates Forward rates are implied from the

relationship between spot rates Sometimes called implied forward rates

You are given the following spot rates 1-year is 5%, 2-year is 6%

How can we determine forward rates? Another interpretation: what is the market implying about next year’s rate?

Example (p.2)

Consider two strategies over 2-year horizon

(1)Invest at 2-year spot rate (buy-and-hold)(2)Invest for 1-year, then reinvest proceeds

at end of year

If these strategies are equivalent, what is the market implying about next year’s rate?

)1( 11f

%0095.7or 11 f

)05.1( 2)06.1(

Summary Various types of interest rates

Spot Yield Forward

Relationships between interest rates Make sure that you know what interest

rate is being referenced Be careful about which rates are being

modeled

Which Interest Rates to Model? It depends

Bond traders may prefer models based on yields

Forward rate models have useful mathematical properties

Actuaries may prefer spot rate models Most popular models focus on spot

rates