Embed Size (px)

Citation preview

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 1/37

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 2/37

Derivatives Options and time Writing options Value of options Summary

Derivatives

1 Derivatives

Introduction

Definitions and Terms

2 Options and time

Payoff Diagrams

3 Writing options

Risk

4 Value of options

What is an option worth?

Speculation and Gearing

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 3/37

Derivatives Options and time Writing options Value of options Summary

Overview

1 Derivatives

Introduction

Definitions and Terms

2 Options and time

Payoff Diagrams

3 Writing optionsRisk

4 Value of optionsWhat is an option worth?

Speculation and Gearing

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 4/37

Derivatives Options and time Writing options Value of options Summary

Introduction

This lecture. . .

This lecture consists of

The definition of basic derivatives instruments,options terminology,

no arbitrage and put-call parity,

payoff diagrams,

simple options strategies.

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 5/37

Derivatives Options and time Writing options Value of options Summary

Introduction

Options: the beginning

In 1973 the Chicago Board Options Exchange (CBOE) firstcreated standardized, listed options on an exchange. Putsweren’t even introduced until 1977. Worldwide, there are over

50 exchanges (and growing) on which options are now traded.

Options

The holder of future or forward contracts is obliged to trade atthe maturity of the contract. The holder must take possession

of the commodity, currency,..., regardless of whether the assethas risen or fallen. Options give their holders rights instead ofobligations.

D O S

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 6/37

Derivatives Options and time Writing options Value of options Summary

Introduction

Call options

The simplest option gives the holder the right to trade in the

future at a previously agreed price but takes away theobligation. So if the stock falls, we don’t have to buy it after all.

Definition

A call option is the right to buy a particular asset for an agreed

amount at a specified time in the future.

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 7/37

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 8/37

Derivatives Options and time Writing options Value of options Summary

Introduction

Call options

We exercise the option at expiry if the stock is above the strikeand not if it is below. If we use S to mean the stock price and E

the strike then at expiry the option is worth

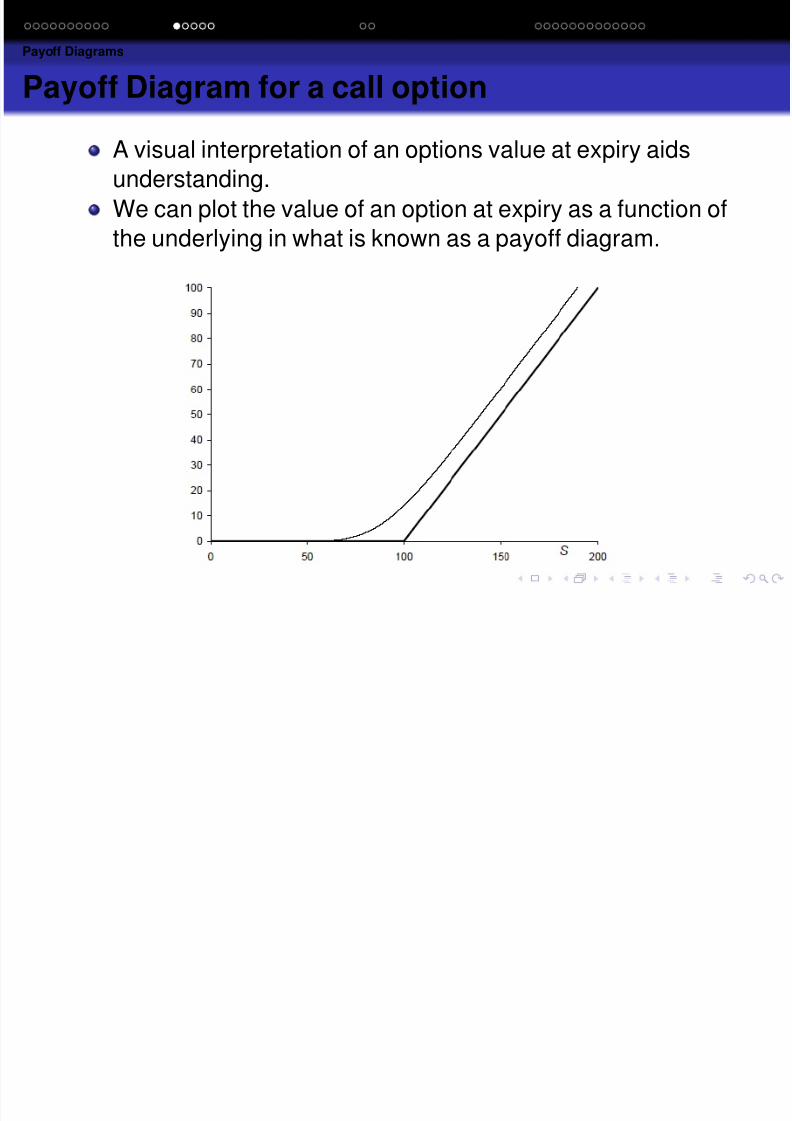

max(S − E , 0).

This function of the underlying asset is called the payoff function . The “max” function represents the optionality.

Why would we buy such an option?

Clearly, if you own a call option you want the stock to rise as

much as possible. Higher stock prices ⇒ greater profit.

Our decision whether to buy it will depend on its price. Theoption has a positive value, i.e. there is no downside to itunlike a future. In our example the option was valued at

$ 0.85. Where did this price come from?

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 9/37

Derivatives Options and time Writing options Value of options Summary

Introduction

Put options

What if you believe that the stock is going to fall, is there acontract that you can buy to benefit from the fall in a stockprice?

Definition

A put option is the right to sell a particular asset for an agreedamount at a specified time in the future

The holder of a put option wants the stock price to fall so that

he can sell the asset for more than it is worth. The payoff

function for a put option is

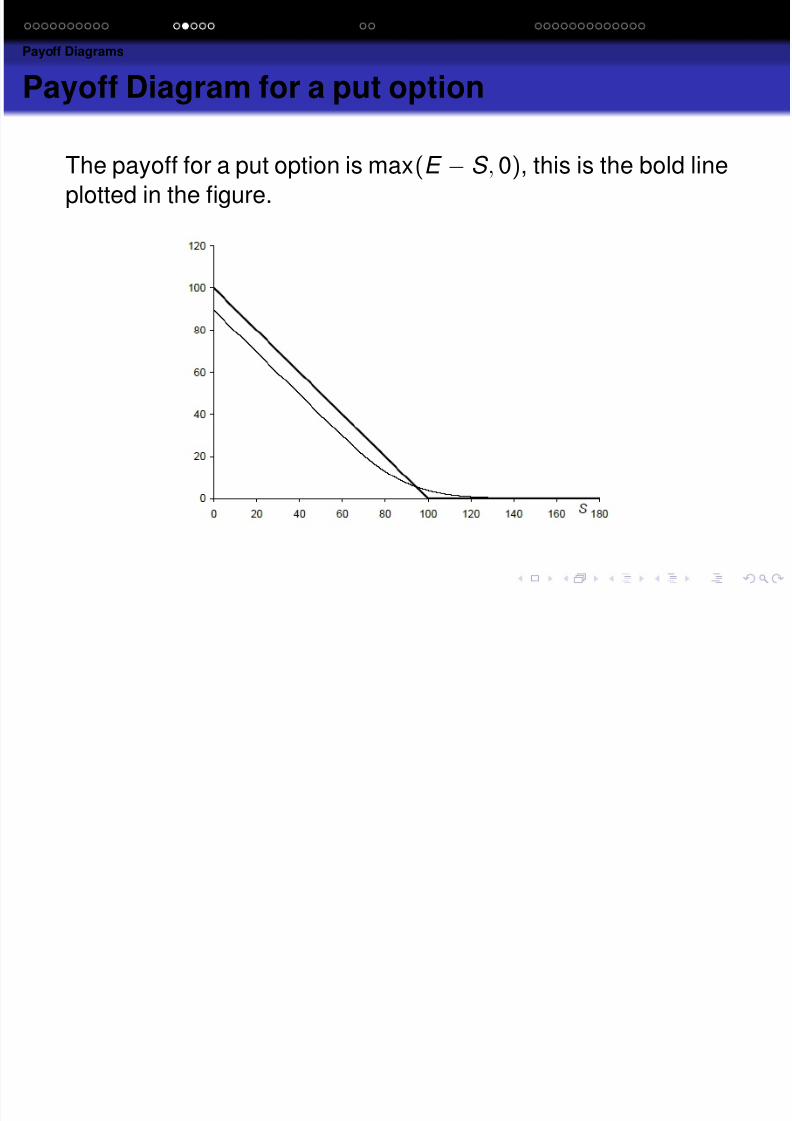

max(E − S , 0).

Now the option is only exercised if the stock falls below the

strike price .

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 10/37

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 11/37

Derivatives Options and time Writing options Value of options Summary

Definitions and Terms

Definitions contd.

Underlying (asset) The financial instrument on which theoption value depends. (Asset values are going to

be denoted by S in this course). The option payoff

is defined as some function of the underlyingasset at expiry.

Strike, or exercise, price The amount for which theunderlying can be bought (call) or sold (put),

denoted by E.

Expiration, or expiry, date Date on which the option can be

exercised or date on which the option ceases toexist or give the holder any rights. This will be

denoted by T .

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 12/37

Derivatives Options and time Writing options Value of options Summary

Definitions and Terms

Definitions contd.

In the money (ITM) An option with positive intrinsic value. A

call option when the asset price is above thestrike, a put option when the asset price is belowthe strike.

Out of the money (OTM) An option with no intrinsic value,only time value. A call option when the asset price

is below the strike, a put option when the asset

price is above the strike.At the money (ATM) A call or put with a strike that is close to

the current asset level.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 13/37

p g p p y

Definitions and Terms

Definitions contd.

Long position A positive amount of a quantity, or a positive

exposure to a quantity.

Short position A negative amount of a quantity, or a negative

exposure to a quantity. Many assets can be soldshort, with some constraints on the length of time

before they must be bought back.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 14/37

p g p p y

Overview

1 DerivativesIntroduction

Definitions and Terms

2 Options and timePayoff Diagrams

3 Writing optionsRisk

4 Value of optionsWhat is an option worth?

Speculation and Gearing

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 15/37

Payoff Diagrams

Payoff Diagram for a call option

A visual interpretation of an options value at expiry aidsunderstanding.

We can plot the value of an option at expiry as a function ofthe underlying in what is known as a payoff diagram.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 16/37

Payoff Diagrams

Payoff Diagram for a put option

The payoff for a put option is max(E − S , 0), this is the bold line

plotted in the figure.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 17/37

Payoff Diagrams

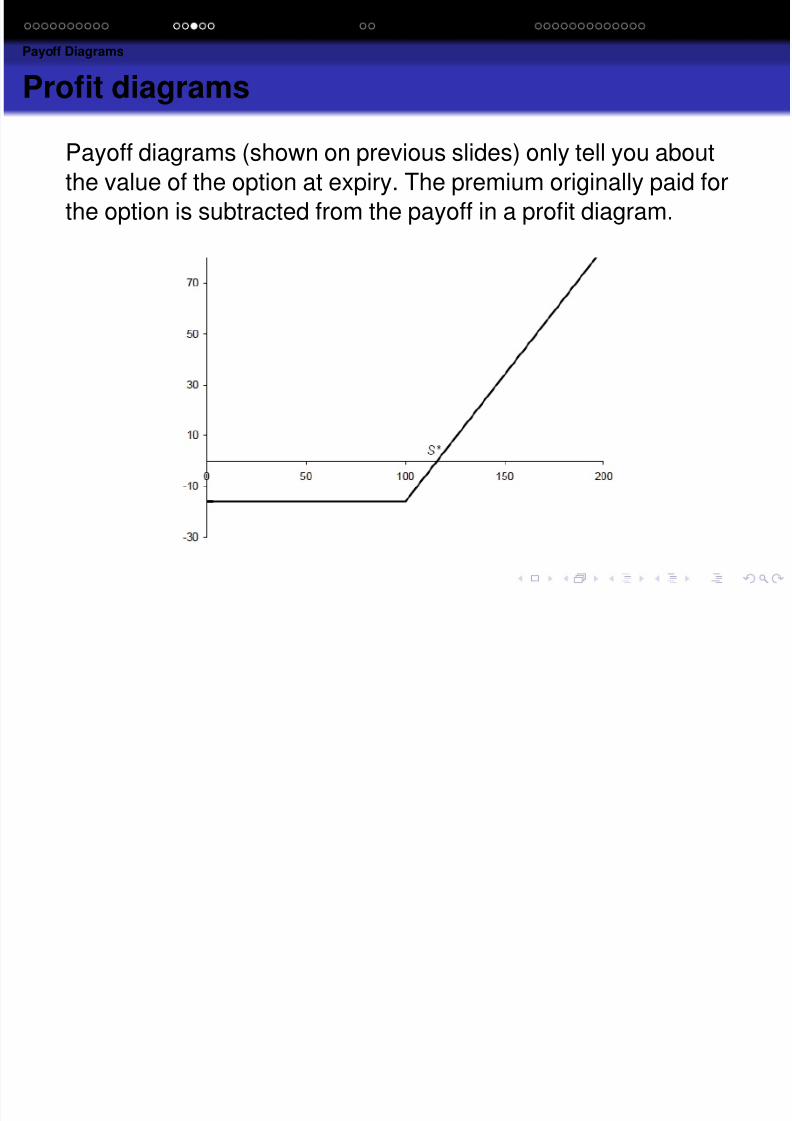

Profit diagrams

Payoff diagrams (shown on previous slides) only tell you aboutthe value of the option at expiry. The premium originally paid forthe option is subtracted from the payoff in a profit diagram.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 18/37

Payoff Diagrams

Profit diagrams contd.

The previous profit diagram takes no account of the time value

of money. The premium is paid up front but the payoff, if any, isonly received at expiry. To be consistent one should eitherdiscount the payoff by multiplying by e −r (T −t ) to valueeverything at the present, or multiply the premium by e r (T −t ) to

value all cashflows at expiry.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 19/37

Payoff Diagrams

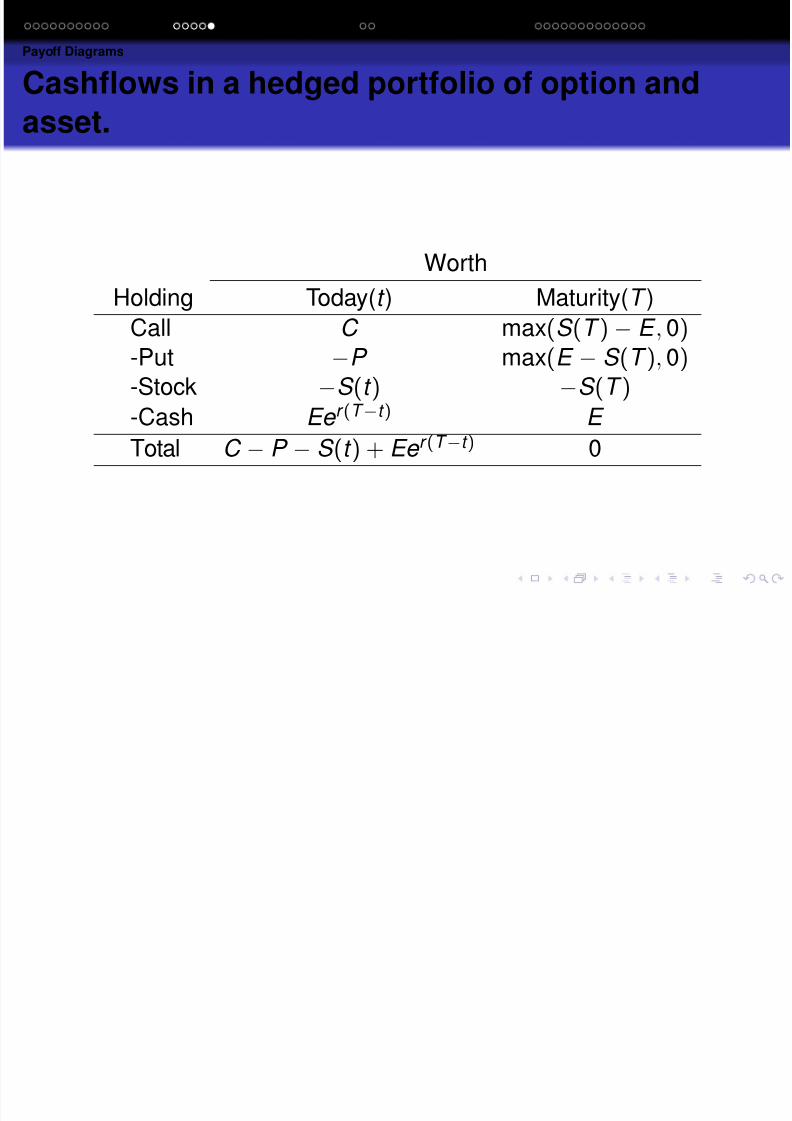

Cashflows in a hedged portfolio of option and

asset.

Worth

Holding Today(t ) Maturity(T )

Call C max(S (T )− E , 0)-Put −P max(E − S (T ), 0)-Stock −S (t ) −S (T )

-Cash Ee r (

T −t ) E

Total C − P − S (t ) + Ee r (T −t ) 0

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 20/37

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 21/37

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 22/37

Risk

Clearing House

The downside of buying an option is just the initialpremium, the upside may be unlimited .

The upside of writing an option is limited, but the downsidecould be huge.

Margin

To cover the risk of default in the event of an unfavorableoutcome, the clearing houses that register and settle options

insist on the deposit of a margin by the writers of options.

Clearing houses act as counterparty to each transaction.

Initial margin is the amount deposited at the initiation of thecontract.

The total amount held as margin must stay above a

prescribed maintenance margin.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 23/37

Overview

1 DerivativesIntroduction

Definitions and Terms

2 Options and timePayoff Diagrams

3 Writing optionsRisk

4 Value of options

What is an option worth?

Speculation and Gearing

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 24/37

What is an option worth?

The value of an option before expiry

We have seen how much calls and puts are worth at expiry, and

drawn these values in payoff diagrams. The question that wecan ask is

“How much is the contract worth now, before expiry?”

You know that there is no downside to owning the option, the

contract gives you specific rights but no obligations.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 25/37

What is an option worth?

Factors

Asset price The higher the underlying asset today, the higherwe might expect the asset to be at expiry of theoption and therefore the more valuable we might

expect a call option to be. On the other hand a putoption might be cheaper by the same reasoning.

Time to expiry The dependence on time to expiry is moresubtle. The longer the time to expiry, the more

time there is for the asset to rise or fall. Is that

good or bad if we own a call option? Furthermore,the longer we have to wait until we get any payoff,

the less valuable will that payoff be simplybecause of the time value of money.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 26/37

What is an option worth?

Some notation

We use V to mean the value of the option, and it will be afunction of the value of the underlying asset S at time t . Thus

we can write V (S , t ) for the value of the contract.

We know the value of the contract at expiry.If we use T to denote the expiry date then at t = T thefunction V is known, it is just the payoff function.

For example if we have a call option then

V (S , T ) = max (S − E , 0).

The fine lines in previous figures are the values of the contracts

V (S , t ) at some time before expiry, plotted against S .

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 27/37

What is an option worth?

Factors affecting options prices

Variables S and t .

Interest rate.

Strike price.Dividends/Foreign interest rate.

Volatility.

Volatility is a measure of how much the asset price fluctuates,

essentially a measure of its randomness. The technicaldefinition of volatility is the “annualized standard deviation of the asset returns .”

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 28/37

What is an option worth?

Volatility

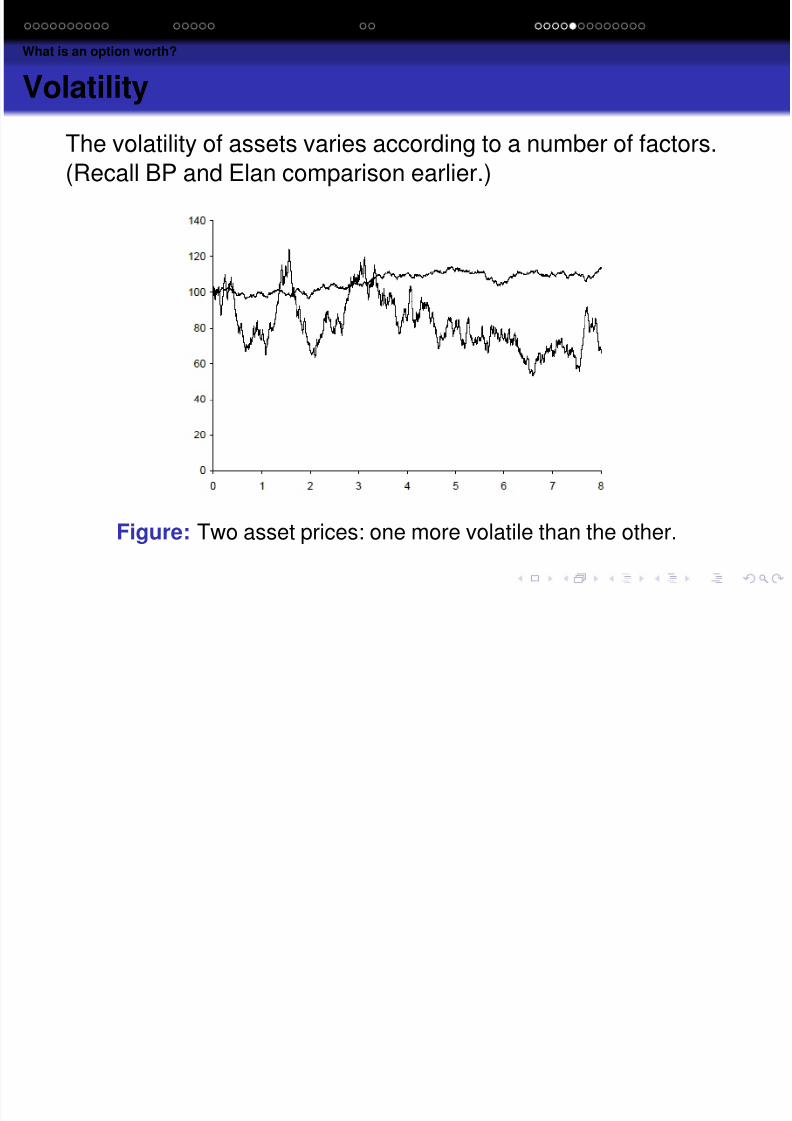

The volatility of assets varies according to a number of factors.(Recall BP and Elan comparison earlier.)

Figure: Two asset prices: one more volatile than the other.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 29/37

Speculation and Gearing

Gearing

If you buy a far out-of-the-money option it may not costvery much, especially if there is not very long until expiry.

If the option expires worthless, then you also haven’t lostvery much.

However, if there is a dramatic move in the underlying, sothat the option expires in the money, you may make a large

profit relative to the amount of the investment.

ExampleToday’s date is September 1st and the price of BP $6.50. The

cost of a $6.80 call option with expiry January 22nd is $0.40.You expect the stock to rise significantly between now andJanuary, how can we profit if you are correct?

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 30/37

Speculation and Gearing

Scenario A: We purchase the stock

Suppose we purchase the stock for $6.50, and that by the

middle of January the stock has risen to $7.30. We will havemade a profit of $0.80 per share. The investment will have risenby

7.30− 6.50

6.50× 100 = 12.3%.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 31/37

Speculation and Gearing

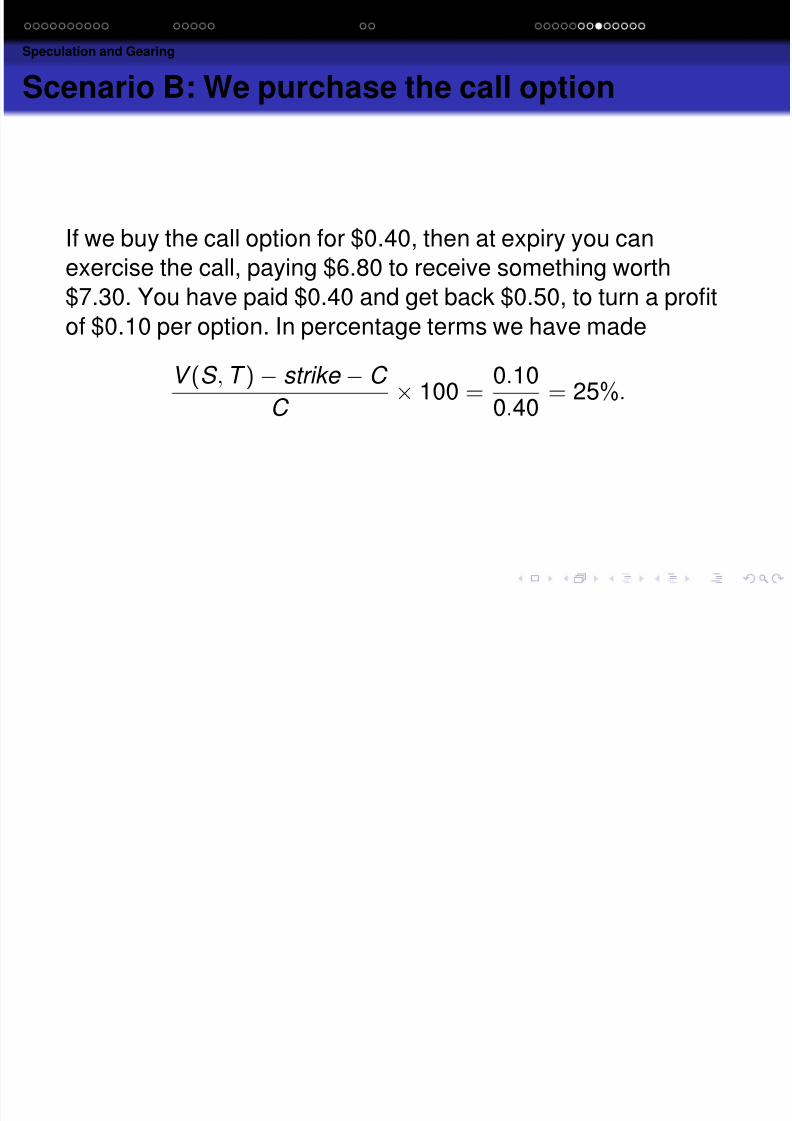

Scenario B: We purchase the call option

If we buy the call option for $0.40, then at expiry you canexercise the call, paying $6.80 to receive something worth$7.30. You have paid $0.40 and get back $0.50, to turn a profit

of $0.10 per option. In percentage terms we have made

V (S , T )− strike −C

C × 100 =

0.10

0.40= 25%.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 32/37

Speculation and Gearing

Gearing or Leverage

This is an example of gearing or leverage. The

out-of-the-money (OTM) option has a high gearing, a possible

high payoff for a small investment. The downside of thisleverage is that the call option is more likely than not to expirecompletely worthless and you will lose all of your investment.

If BP remains at $6.50 then the stock investment has the same

value but the call option experiences a 100% loss.

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 33/37

Derivatives Options and time Writing options Value of options Summary

S l ti d G i

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 34/37

Speculation and Gearing

Put-call parity

Imagine that you buy one European call option with a strike ofE and an expiry of T and that you write a European put option

with the same strike and expiry. The payoff for the portfolio of

the two options is the sum of the individual payoffs:

max(S (T )− E , 0)−max (E − S (T ), 0) = S (T )− E ,

where S (T ) is the value of the underlying asset at time T . The

right-hand side of this expression consists of two parts, theasset and a fixed sum E . Is there another way to get exactlythis payoff?

Derivatives Options and time Writing options Value of options Summary

Speculation and Gearing

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 35/37

Speculation and Gearing

Put-call parity contd.

Yes: If you buy the asset today it will cost S (t ) and be worth

S (T ) at expiry. You don’t know what the value S (T ) will be but

you do know how to guarantee to get that amount, and that is tobuy the asset. What about the E term? To lock in a payment ofE at time T involves a cash flow of Ee −r (T −t ) at time t . Theconclusion is that the portfolio of a long call and a short put

gives exactly the same payoff as a long asset, short cashposition.

Derivatives Options and time Writing options Value of options Summary

Speculation and Gearing

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 36/37

Speculation and Gearing

Put-call parity contd.

The equality of these cashflows is independent of the futurebehaviour of the stock and is model independent:

C − P = S − Ee −r (T −t ),

where C and P are today’s values of the call and the putrespectively. This relationship holds at any time up to expiry

and is known as put-call parity.

Derivatives Options and time Writing options Value of options Summary

8/3/2019 Lecture 2 Derivatives

http://slidepdf.com/reader/full/lecture-2-derivatives 37/37

Summary

Summary

Derivatives, call/put options,

Payoff diagrams,

Hedged portfolio of option and asset,

Writing options,

Value of options,

Gearing.