Embed Size (px)

DESCRIPTION

Managerial ACCT

Citation preview

Lecture 10

Activity Based Costing and Management

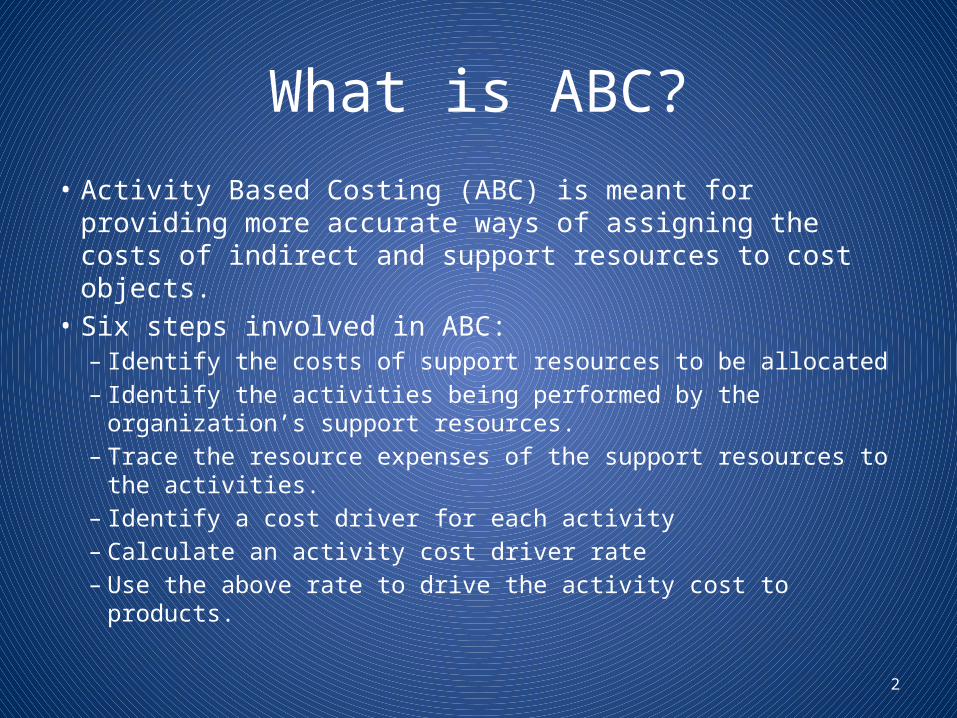

What is ABC?• Activity Based Costing (ABC) is meant for providing more

accurate ways of assigning the costs of indirect and support resources to cost objects.

• Six steps involved in ABC:– Identify the costs of support resources to be allocated– Identify the activities being performed by the organization’s support

resources.– Trace the resource expenses of the support resources to the

activities.– Identify a cost driver for each activity– Calculate an activity cost driver rate– Use the above rate to drive the activity cost to products.

2

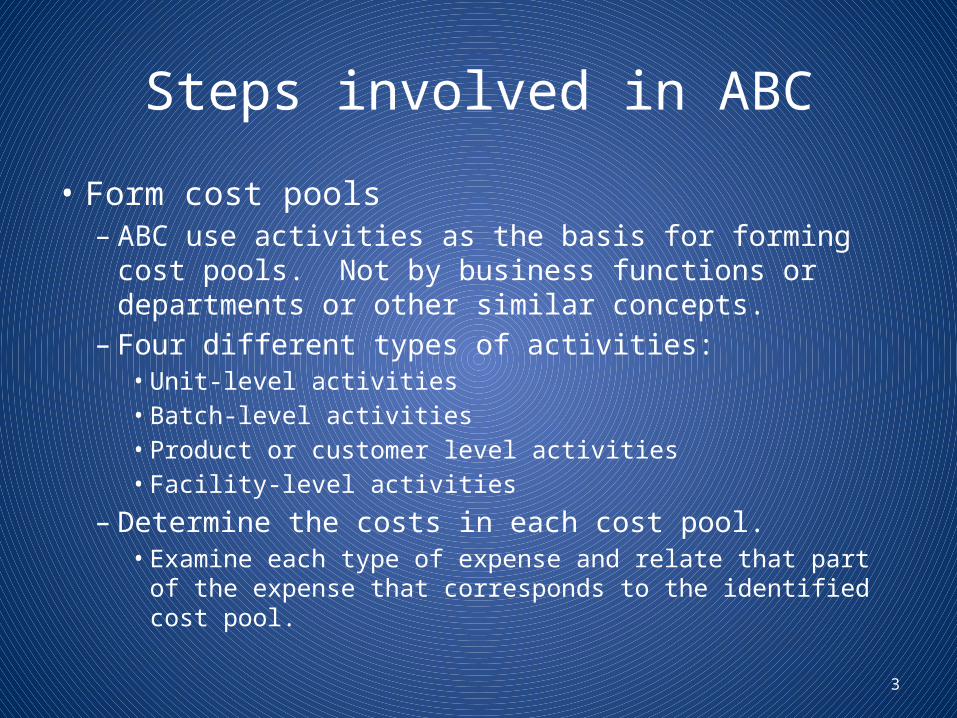

Steps involved in ABC

• Form cost pools– ABC use activities as the basis for forming cost pools. Not by

business functions or departments or other similar concepts.– Four different types of activities:

• Unit-level activities• Batch-level activities• Product or customer level activities• Facility-level activities

– Determine the costs in each cost pool.• Examine each type of expense and relate that part of the expense

that corresponds to the identified cost pool.

3

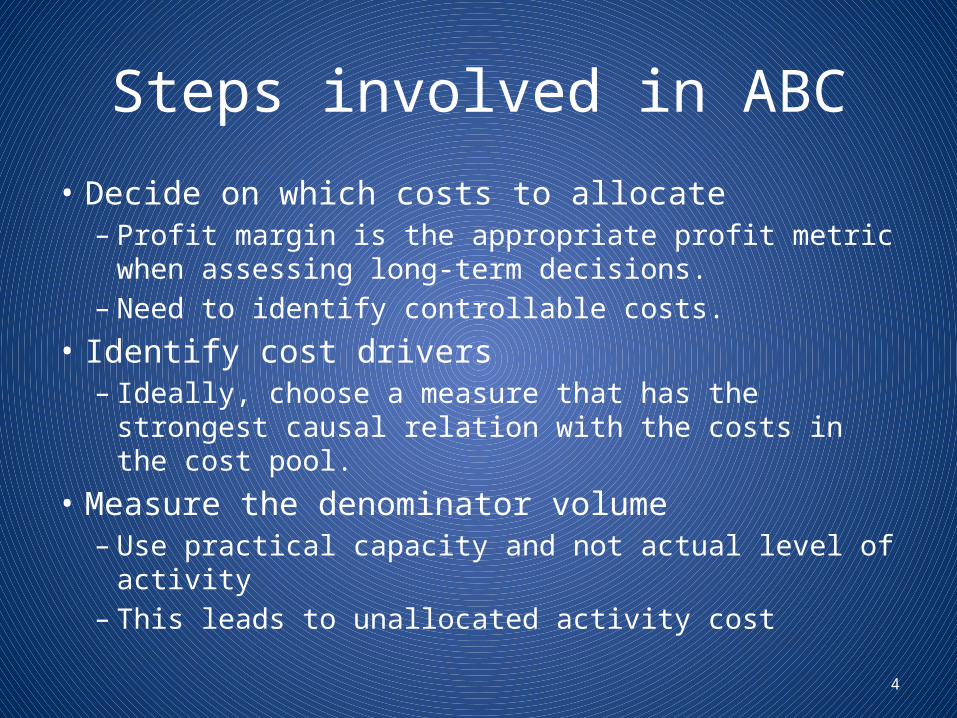

Steps involved in ABC

• Decide on which costs to allocate– Profit margin is the appropriate profit metric when

assessing long-term decisions.– Need to identify controllable costs.

• Identify cost drivers– Ideally, choose a measure that has the strongest causal

relation with the costs in the cost pool.• Measure the denominator volume

– Use practical capacity and not actual level of activity– This leads to unallocated activity cost

4

Designing a good ABC system

• Is ABC just a more complex and expensive way to perform cost allocations?– No! ABC is linked to underlying economic events.

• Stress on cost-and-effect relationship.• Tradeoff between accuracy and cost of

measurement– Activity drivers can be based on transaction,

duration or intensity

5

When does the traditional costing systems fail?

• When a large proportion of activities are at non-unit level• When there is product diversity• When the consumption of common resources are hetrogenous• Some indicators

– Sales are increasing but profits are declining– Complex products are very profitable but simple products are losing money– High profit products are not offered by the competitors– Overhead rates are very high and increasing over time– Direct labor is a small percentage of total costs– Results of bids are difficult to explain– Competitors’ high volume products seem to be priced very low– Line managers/marketing managers ignore costs reported by accountants.

6

Activity Based Management

• Product planning• Customer planning• Resources planning• Product planning

– ABC cost is the floor for setting the price in the long run.

– Refine prices– Refine product mix

7

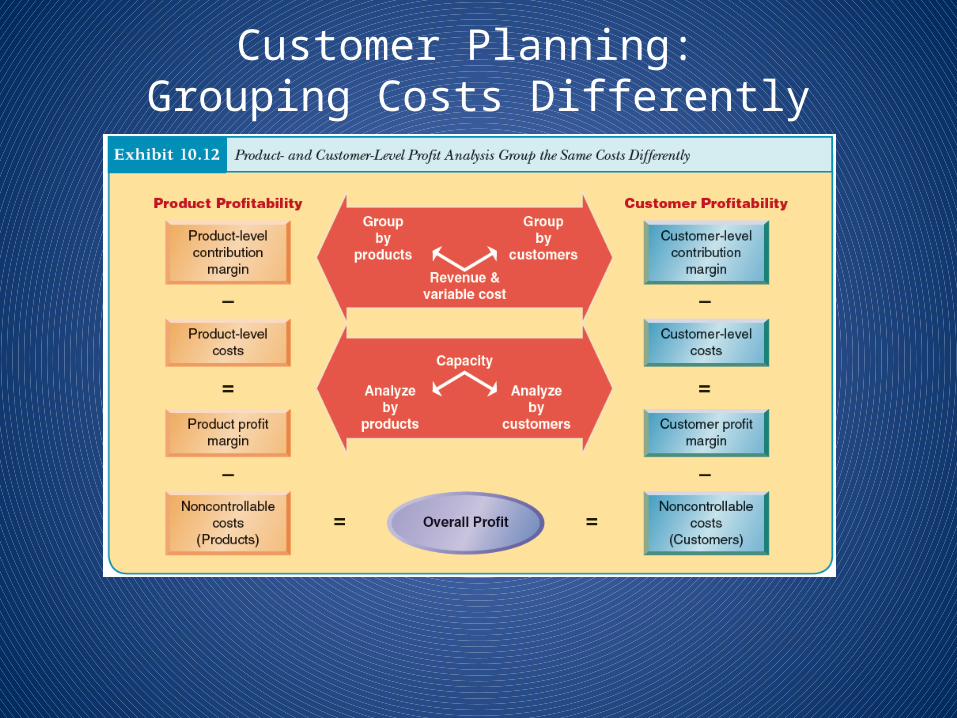

Customer Planning: Grouping Costs Differently

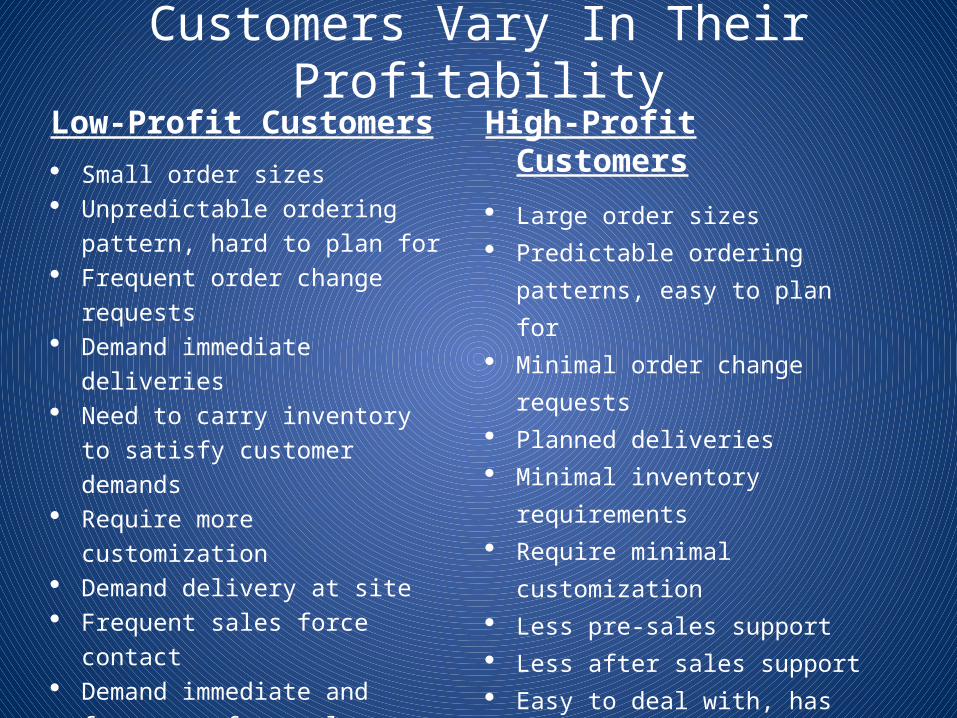

Customers Vary In Their ProfitabilityLow-Profit Customers· Small order sizes· Unpredictable ordering pattern,

hard to plan for· Frequent order change requests· Demand immediate deliveries· Need to carry inventory to satisfy

customer demands· Require more customization· Demand delivery at site· Frequent sales force contact· Demand immediate and frequent

after sales service· Rigid requirements· Not paying on time

High-Profit Customers· Large order sizes· Predictable ordering patterns, easy

to plan for· Minimal order change requests· Planned deliveries· Minimal inventory requirements · Require minimal customization· Less pre-sales support· Less after sales support· Easy to deal with, has well

organized purchase procedures · Flexible relationship· Pays on time

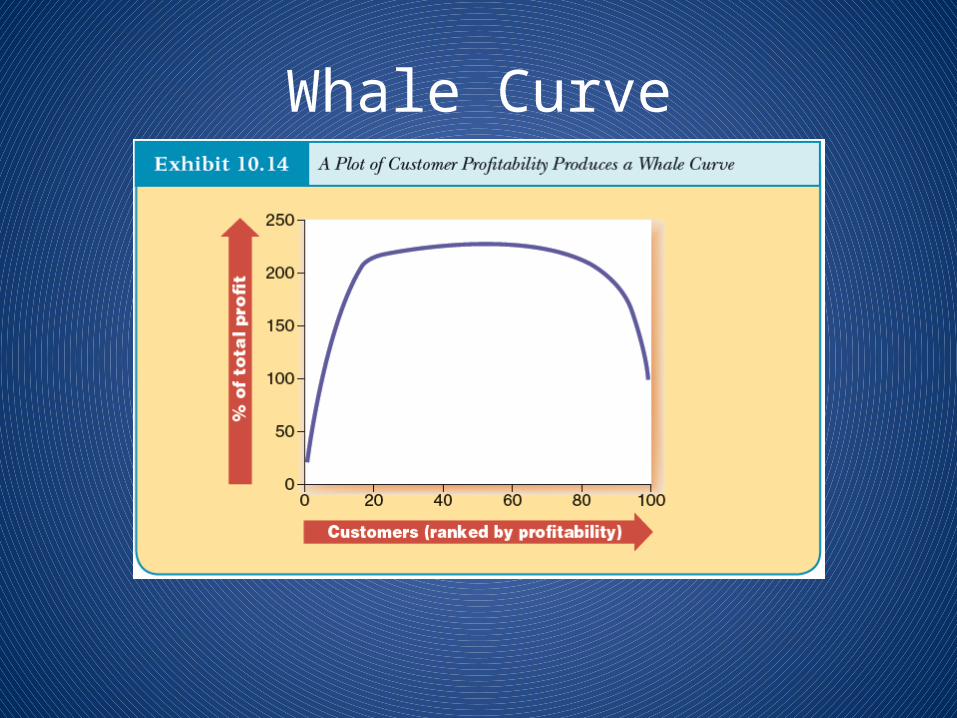

Whale Curve

Activity Based Management

• Customer Planning– Customer profitability analysis– Sales and administration costs are relatively high

in some industries– Classify customers into

• Low cost to serve but generate high profit margins• Low costs to serve and generate low profit margins• High costs to serve and generate high profit margins• High costs to serve but generate low profit margins

11

Activity Based Management

• Resource Planning– ABC creates a “map” of how a product consumes activities

and, thereby, resources– We can use the activity map and production forecasts to

generate the demand for resources• Same as generating the demand for materials or labor

– We can match with supply of resources to reduce unneeded capacity

• Reporting of unused capacity is useful in drawing managerial attention to capacity supplied but not used

12