Embed Size (px)

Citation preview

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 1/17

UNIT ONE

CHAPTER TWO

INDIAN

FINANCIAL SYSTEM

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 2/17

Lesson no 3

Chapter 2

Indian financial System

Unit 1

Core concepts in financial management

After reading this lesson you will be able to understand the following: -

Concept of ‘Financial System’.

Functions of Financial Markets.

Various criterions of classifying Financial Markets.

Various constituents of financial market, their characteristics and the instruments

used.

Recent changes in ‘Financial System’.

In order to gain an understanding of how firms carry out the finance function, it is

very important for you to understand the financial system of which the firm is a

part. This requires a study of the financial institutions and markets that comprise

the financial system, and the basic sources of long-term finance that are available

to a fund to fund its investments

You might have heard the term financial system what do you think it is?

What is a financial system?

Savings mobilisation and promotion of investment arc functions of the stock and capital

markets, which are a part of the organised financial system in India. The objective of all

economic activity is to promote the well being and standard of living of the people, which

depends on the income and distribution of income in terms of real goods and services in

the economy. The production of output, which is vital to the growth process in the

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 3/17

economy, is a function of the many inputs used in the productive process. These inputs

are material inputs (in the form of physical materials, viz., raw materials, plant,

machinery, etc.), human inputs (in the form of labor and enterprise) and financial inputs

(in the form of capital, cash and credit). The easy availability of financial inputs promotes

the growth process through proper coordination between human and material inputs.

The financial inputs emanate from the financial system, while real goods and services

are part of the real system. The interaction between the real system (goods and services)

and the financial system (money and capital) is necessary for the productive process.

Trading in money and monetary assets constitute the activity in the financial markets and

are referred to as the financial system.

For financial system it is necessary that there is a financial activity, can you comment on

what it is?

What is financial system?

The term "liquidity" is used to refer to cash, money and nearness to cash. Money and

monetary assets are traded in the financial system. Thus, provision of liquidity and

trading in liquidity are the major functions of the financial system. While cash creation is

the function of the RBI, banks do credit creation and financial institutions including the

RBI, banks and term-leading institutions, deal in claims on money or monetary assets.

These institutions are all a part of the financial system.

Besides, the financial system is also geared to the mobilisation of savings and

channelisation of these savings into productive activity. Through appropriate differentials

in the rate of return and other incentives, funds flow from less productive to more

productive activities. The efficient functioning of the financial system facilitates these

flows of funds.

Sector-wise, government and business sectors are the major borrowers whose

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 4/17

investment is always greater than savings. On the other hand, in India the household and

foreign sectors are the net savers, with savings exceeding investment. The financial

system provides the intermediation between investors and helps the process of

specialisation and sophistication in the financial infrastructure, leading to greater

financial development that is pre-requisite for faster economic development.

Now let us move on to functions of financial markets

What are Functions of financial markets?

The primary function of the financial markets is to facilitate the transfer of funds from

surplus sectors (lenders) to deficit sectors (borrowers). Normally, households have excess

of funds or savings, which they lend to borrowers in the corporate and public sectors

whose requirement of funds, exceed their savings. A financial market consists of

investors or buyers, 'sellers, dealers and brokers and does not refer to a physical location.

Formal trading rules and communication networks for originating and trading financial

securities link the participants in the market. The primary market in which public issue of

securities is made through a prospectus is a retail market and there is no physical

location. The investors are reached by direct mailing. On the other hand, the secondary

market or stock exchange where existing securities are traded, is an auction market and

may have a physical location such as the rotunda of the Bombay Stock Exchange or\the

trading floor of Delhi, Ahmedabad and other exchanges where the exchange members

meet to trade securities face-to-face. In the Over-The-Counter (OTCEI) market and

National Stock Exchange, trading in securities is screen-based. The Bombay Stock

Exchange (BOLT) now introduces on-line trading, and other exchanges are in the process

of introducing the same that is screen-based.

Financial markets trade in money and their price is the rate of return the buyer

expects the financial asset to yield. The value of financial assets change with the

investors' expectations on earning or interest rates. Investors seek the highest return for a

given level of risk (by paying the lowest price) and users of funds attempt to borrow at

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 5/17

the lowest rate possible. The aggressive interaction, of investors and users of funds in a

properly functioning capital market ensures the flow of capital to the best user. Investors

receive the highest return and the users obtain funds at the lowest cost.

The three important functions of financial markets are:

1.Financial markets facilitate price discovery. The continual interaction among numerous

buyers and sellers who throng financial markets help in establishing the prices of

financial assets. Well-organised financial markets seem to be remarkably efficient in

price discovery. That is why financial economists say: "If you want to know what is the

value of a financial asset simply look at its price in the financial market"

2. Financial markets provide liquidity to financial assets. Investors can readily sell their

financial assets through the mechanism of financial markets. In the absence of financial

markets, which provide such liquidity, the motivation of investors to hold financial assets

will be considerably diminished. Thanks to negotiability and transferability of securities

through the financial markets, it is possible for companies (and other entities) to raise

long-term funds from investors with short-term and medium-term horizons. While one

investor is substituted by another when a security is transacted, the company is assured of long-term availability of funds.

3. Financial markets considerably reduce the cost of transacting. The two major costs

associated with transacting are search costs and information costs. Search costs comprise

explicit costs such as the expenses incurred on advertising when one wants to buy or sell

an asset and implicit costs such as the effort and time one has to put in to locate a

customer. Information costs refer to costs incurred in evaluating the investment merits of

financial assets.

Did you ever tried to classify financial markets, please do so right now.

How to Classify Financial Markets?

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 6/17

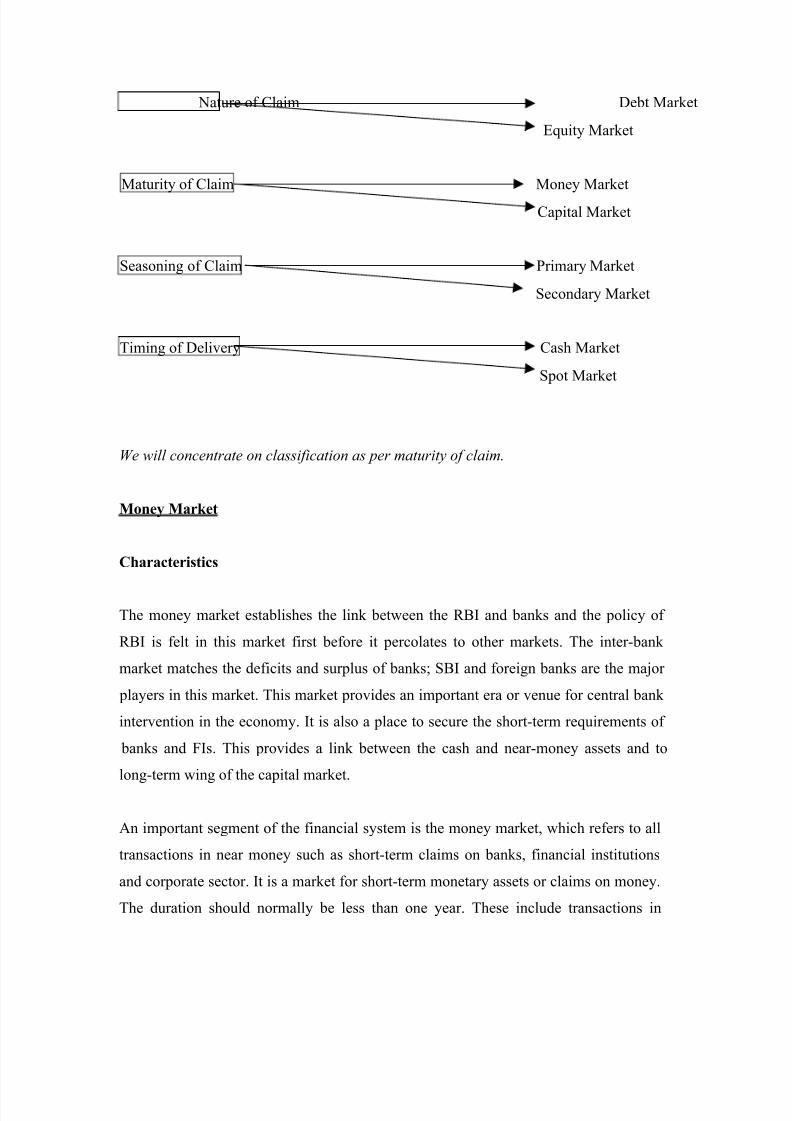

There are different ways of classifying financial markets.

One way is to classify financial markets by the type of financial claim. The debt market

is the financial market for fixed claims (debt instruments) and the equity market is the

financial market for residual claims (equity instruments).

A second way is to classify financial markets by the maturity of claims. The market

for short-term financial claims is referred to as the money market and the market for

long-term financial cli.1ims is called the capital market Traditionally the cut-off

between short-term and long-term financial claims has been one year-though this

dividing line is arbitrary, it is widely accepted. Since short-term financial claims are

almost invariably debt claims, the money market is the market for short-term debt

instruments. The capital market is the market for long-term debt instruments and

equity instruments.

A third way to classify financial markets is based on whether the claims represent new

issues or outstanding issues. The market where issuers sell new claims is referred to as

the primary market and the market where investors trade outstanding securities is called

the secondary market

A fourth way to classify financial markets is by the timing of delivery. A cash or spot

market is one where the delivery occurs immediately and a forward or futures market is

one where the' delivery occurs at a pre-determined time in future

A fifth way to classify financial markets is by the nature of its organisational structure.

An exchange-traded market is characterised by a centralised organisation with

standardised procedures. An over-the counter market is a decentralised market with

customised procedures.

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 7/17

Nature of Claim Debt Market

Equity Market

Maturity of Claim Money Market

Capital Market

Seasoning of Claim Primary Market

Secondary Market

Timing of Delivery Cash Market

Spot Market

We will concentrate on classification as per maturity of claim.

Money Market

Characteristics

The money market establishes the link between the RBI and banks and the policy of

RBI is felt in this market first before it percolates to other markets. The inter-bank

market matches the deficits and surplus of banks; SBI and foreign banks are the major

players in this market. This market provides an important era or venue for central bank

intervention in the economy. It is also a place to secure the short-term requirements of

banks and FIs. This provides a link between the cash and near-money assets and to

long-term wing of the capital market.

An important segment of the financial system is the money market, which refers to all

transactions in near money such as short-term claims on banks, financial institutions

and corporate sector. It is a market for short-term monetary assets or claims on money.

The duration should normally be less than one year. These include transactions in

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 8/17

inter-bank call money (Call money market) and treasury bills issued by the

government and commercial bills issued by the private corporate sector (Bills

market). The money market is the short-term wing of the financial system dealing in

claims on money of a short-term nature, say, of a few days to a few months. Next to

the currency, the most liquid assets are the short-term claims or call money of duration

of up to 15 days. The bills, both of the government and the private corporate sector,

may run for three to six months. But all these instruments would generally be of a few

days to one year and fall into the category of short-term monetary instruments. The

inter-corporate funds market is also a part of this market, which conducts the

borrowing and lending operations among the corporate units in the private sector. The

banks, financial institutions and companies operate in these markets and effect

purchase and sale transactions in these near-money assets.

Instruments in Money Market

Debt instruments, which have a maturity of less than one year at the time of issue, are

called money market instruments. These instruments are highly liquid have negligible

risk. The major money market instruments are Treasury bills, Certificates of deposit,

commercial paper, and repos. Government, financial institutions, banks, and corporates

dominate the money market. Individual investors participate in the money market

directly.

A brief description of money market instruments is given below:

Treasury Bills

Treasury bills are the most important money market instruments. They represent the

obligations of the Government of India, which have a primary tenor like 91 days and 364

days. The Reserve Bank of India sells them on an auction basis every week in certain

minimum denominations. They do not carry an explicit (or coupon rate). Instead, they are

sold at a discount and redeemed at par. Hence the implicit yield of T Bill is a function of

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 9/17

the size of the discount and maturity.

Though the yield on Treasury bills is somewhat low, yet they have following reasons:

(a) these can be transacted readily and there is a secondary market for them. (b) Treasury

bills have nil credit risk and negligible price risk (thanks to their short tenor).

Certificate of Deposits

Certificates of deposits (CDs) represent short-term deposits, which are transferable from, to one

party to another. Banks and financial institutions are the major issuers of CDs. The principal

investors in CDs are banks, financial institutions, Corporates, and mutual funds. CDs are issued in

either bearer or registered form. They generally have a maturity of 3 months to 1 year. CDs are

issued at a discount and redeemed at par.

CDs are a popular form of short-term investment for companies for the following reasons(i)

Banks are normally willing to tailor the denominations and maturities to suit the needs of the

investors. (ii) CDs are generally risk-free. (iii) CDs generally offer Irate of interest than Treasury

bills or term deposits.

Commercial paper

A Commercial Paper is a short term unsecured promissory note issued by the raiser of

debt to the investor. For a corporate to be eligible it must have a tangible net worth of Rs

4 crore or more and have a sanctioned working capital limit sanctioned by a bank/FI. It is

generally companies with very good rating which are active in the CP market, though

RBI permits a minimum credit rating of Crisil-P2. The tenure of CPs can be anything

between 15 days to one year, though the most popular duration is 90 days. These

instruments are offered at a discount to the face value and the rate of interest depends on

the quantum raised, the tenure and the general level of rates besides the credit rating of

the proposed issue. While most of the issuing entities have established working capital

limits with banks, they still prefer to use the CP route for flexibility in interest rates. The

credit ratings for CP are issued by leading rating agencies.

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 10/17

Repos

The term Repo is used as an abbreviation for Repurchase Agreement or Ready Forward.

A Repo involves a simultaneous "sale and repurchase" agreement.

A Repo works as follows. Party A needs short-term funds and Party B wants to make a

short-term investment. Party A sells securities to Party B at a certain price and

simultaneously agrees to repurchase the same after a specified time at a slightly higher

price. The difference between the sale price and the repurchase price represents the

interest cost to Party A and conversely the interest income for Party B.

Repos are a very convenient instrument for short-term investment. They are safe and earn a pre-

determined return

Capital Market

The capital market consists of primary and secondary markets. The primary market deals

with the issue of new instruments by the corporate sector such as equity shares,

preference shares and debentures. The public sector consisting of Central and State

governments, various public sector industrial units (PSU), statutory and other authorities

such as state electricity boards and port trusts also issue bonds and shares especially as a

part of disinvestments of government holdings.

The secondary market consists of 23 stock exchanges, including the National Stock Ex-

change, the Over-the-Counter Exchange of India (OTCEI) and Interconnected Stock

Exchange of India Ltd. (ISEIL) where existing instruments including negotiable debts are

traded. The market value of listed stock on the stock exchanges in India was Rs. 6,83,986

crores in July 2000. Capital formation occurs in the primary market while the secondary

market provides a continuous market for the securities already issued to be bought and

sold in volume with little variation in the current market price. It also provides liquidity

to the initial buyers in the primary market to reoffer the securities to any interested buyer

at any price, if mutually accepted. An active secondary market actually promotes the

growth of the primary market and capital formation because investors in the primary

market are assured of a continuous market and should the occasion arise, they can

liquidate their investments in the stock exchange.

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 11/17

There is a symbiotic relationship between the primary and secondary markets. The major

players in the primary market are the merchant bankers, mutual funds, and financial

institutions. Foreign institutional investors (FIIs) and the anchor of the market, the

individual investors: and in the secondary market, the stockbrokers who are members of

the stock exchanges, the mutual funds, financial institutions, foreign institutional

investors (FIIs), and individual investors.

With a view to protect investors' interest and orderly development of the capital market.

Securities and Exchange Board of India (SEBI) regulates the capital market and

intermediaries.

In the stock and capital markets, there are various types of term-lending institutions, all-

India and state financial corporations and finance companies and development

corporations, which deal in money debt claims. The trading in debt claims of a medium

and long-term nature can be classified into those of the government sector and of the

private sector. The securities of government are traded in the stock market as a separate

component, called gilt-edged market. The securities of the government sector include

those of the Central and State Governments, local bodies, semi -Government bodies and

those guaranteed by the Government. These securities may have a maturity running up to

25 to 30 years. In this market, there are again three types of securities - short, medium

and long-dated government securities, depending upon the maturity period.

Another very important component of the stock exchange deals with trading in corporate

shares, equities, and Deferred and preference shares. When the companies as shares float

equities to the public for the first time, they constitute the new issues market, which is a

component of the Capital market. Besides, there are also further issues that are floated by

the existing companies for additional capital for expansion, modernisation, etc. The new

issues and further issues are the claims of the public on the corporate sector. The claims

on the corporate sector can also take the form of preference shares, which are also of

ownership category.

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 12/17

There are also securities of a debt nature such as bonds/debentures. Debentures may be

convertible or non-convertible, depending on the availability of option for conversion

into equity. Similarly, preference shares, be cumulative or non-cumulative depending

on the provision for accumulation of dividends or not. More recently, convertible

preference shares are also permitted, which can be converted into equity shares at a

later stage.

Efficiency of Financial System.

The real test of development of financial system is its efficiency in operations and

functional roles. The operational efficiency is reflected in the costs of intermediation,

quality of service and its width. The improved operational efficiency during the nineties

is seen from significant reforms in the capital market and stock markets, lowering of

costs of credit and greater flow of bank credit into these markets, lowering of costs

raising funds from the capital market through the route of book building and private

placement. The strengthening of the institutions evidences the Width of Services

Structure and increasing the instruments of mobilising funds, introduction of

technological innovations in the Stock and Capital markets and in the banking system,deregulation, privatization and globalisation of markets and freer flow of funds into and

outside country, etc. The reforms in general and increasing role of technology and

competitive forces in particular have improved the quality of service.

Any financial system can be assessed for its functional efficiency through following

criteria in general

(1) Quantity of funds raised through saving for investment and pattern of allocation

from less to more productive purposes.

(2) Its contribution to economic growth and its impact on real economic variables,

reflected in market capitalisation as a proportion of GDP and the usual ratios, such as

Finance ratio - ratio of total issues to national income; Financial inter-relations ratio -

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 13/17

ratio of total issues to net domestic capital, formation; and financial intermediation ratio -

ratio of secondary issues raised by banks and financial institutions to primary issues in

the market

(3) Information absorption - whether all information an market and economy are fully

reflected in the scrip prices.

(4) Fundamental valuation efficiency - whether the company valuarion_are

reflected in scrip prices.

The non-governmental and non-financial economic units and corporate Sector have two

major sources of funds, namely from banks and financial institution or one hand and

directly from the capital market on the other. There has been an improvement in both

these respects in more recent years due to reforms introduced, since 1985.

LlBERALlSATlON OF THE FINANCIAL SYSTEM

A radical restructuring of the economic system consisting of industrial deregulation,

liberalisation of policies relating to foreign direct investment, public enterprise reforms,

reforms of taxation system, trade liberalisation and financial sector reforms have been

initiated in 1992-93. Financial sector reforms in the area of commercial banking, capital

markets and non-banking finance companies have also been undertaken.

The focus of reforms in the financial markets has been on removing the structural weak-

nesses and developing the markets on sound lines. The money and foreign exchange

market reforms have attempted to broaden and deepen them. Reforms in the government

securities market sought to smoothen the maturity structure of debt, raising of debt at

close-to-market rates and improving the liquidity of government securities by developing

an active secondary market. In the capital market the focus of reforms has been on

strengthening the disclosure standards, developing the market infrastructure and

strengthening the risk management systems at stock exchanges to protect the integrity

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 14/17

and safety of the market. Elements of the structural reforms in various market segments

are introduction of free pricing of financial assets such as interest rate on government

securities, pricing of capital issues and exchange rate, the enlargement of the number of

participants and introduction of new instruments.

Improving financial soundness and credibility of banks is a part of banking reforms

undertaken by the RBI, a regulatory and supervisory agency over commercial banks

under the Banking Companies Regulation Act 1949. The improvement of financial health

of banks is sought to be achieved by capital adequacy norms in relation to the risks to

which banks are exposed, prudential norms for income recognition and provision of bad

debts. The removal of external constraints in norms of pre-emption of funds benefits and

prudential regulation and recapitalisation and writing down of capital base are reflected in

the relatively clean and healthy balance sheets of banks. The reform process has,

however, accentuated the inherent weaknesses of public sector dominated banking

systems. There is a need to further improve financial soundness and to measure up to the

increasing competition that a fast liberalising and globalising economy would bring to the

Indian banking system.

In the area of capital market, the Securities and Exchange Board of India (SEBI) was

set up in 1992 to protect the interests of investors in securities and to promote

development and regulation of the securities market. SEBI has issued guidelines for

primary markets, stipulating access to capital market to improve the quality of public

issues, allotment of shares, private placement, book building, takeover of companies and

venture capital In the area of secondary markets, measures to control volatility and

transparency in dealings by modifying the backend system, laying down insider

regulations to protect integrity of markets, uniform settlement introduction of screen-

based online trading, dematerialising shares by setting up depositor and trading in

derivative securities (stock index futures). There is a sea change in the institutional and

regulatory environment in the capital market area.

In regard to Non-Bank Finance Companies (NBFCs), the Reserve Bank of India has

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 15/17

issued several measures aimed at encouraging disciplined NBFCs, which run on sound

business principles. The measures seek to protect the interests of depositors and provide

more effective, prevision, particularly over those, which accept public deposits. The

regulations stipulate upper limit for public deposits, which NBFCs can accept. This limit

is linked to credit rating an approved rating agency. An upper limit is also placed on the

rate of interest on deposits order to restrain NBFCs from offering incentives and

mobilising excessive deposits, which they may not be able to service. The heterogeneous

nature, number, size, functions (deployment funds) and level of managerial competence

of the NBFCs affect their effective regulation.

Since the liberalisation of the economy in 1992-93 and the initiation of reform

measure the financial system is getting market-oriented. Market efficiency would be

reflected in the wide dissemination of information, reduction of transaction costs and

allocation of capital the most productive users. Further, freeing the financial system from

government interference has been an important element of economic reforms.

INTERPRETING BOND AND STOCK PRICE QUOTATIONS

The financial manager needs to stay abreast of the marker values of the firm's

outstanding bonds and stocks, whether they are traded on an organized exchange,

over the counter, or in international markets. Similarly, existing and prospective

bondholders and stockholders need to monitor the prices of the securities they

own. These prices are important because they represent the current value of their

investment. Information on bonds, stocks, and other securities is contained in

quotations, which include current price data along with statistics on recent price

behavior. Security price quotations are readily available for actively traded bonds

and stocks. The most up-to-date '"quotes" can be obtained electronically, via a personal computer. Price information is available from stockbrokers and is widely

published in news media-both financial and non financial. Popular sources of

daily security price quotations are financial newspapers, such as the Economic

Times and the Business Standard, or the business sections of daily general

newspapers published in most major cities.

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 16/17

8/8/2019 Lecture-03 Indian Fina System

http://slidepdf.com/reader/full/lecture-03-indian-fina-system 17/17

IMPORTANT

To update yourself on regular basis read financial newspapers on regular basis.

Questions

1. Explain the concept of ‘Financial System’?

2. What are the functions of Financial Markets?

3. What are the various criterions of classifying Financial Markets? Discuss in

detail.

4. What are the various instruments under capital market & money market?