Embed Size (px)

Citation preview

Dr. Bruce Vanstone

Position Sizing for Traders

Learning from simulations

Bruce Vanstone 2

This material is presented for educational purposes only.

I am not a financial advisor, and this material is not advice.

In many cases, the material represents ongoing research findings.

Disclaimer

Dr. Bruce Vanstone

Part 1 – What are we trying to achieve?◦ Purpose

What this part is (and isn’t!) about Examples are specific to equity trading

◦ 3 parts to developing a system◦ Importance of Position Sizing◦ Types of techniques in common use

‘Standard’ approaches ‘Advanced’ approaches

◦ Requirements of a good position sizing approach

Introduction

Dr. Bruce Vanstone

Part 2 – What we can learn from simulations◦ An ‘example’ system: Trending 101◦ Standard Techniques

Percent of Equity approach Equity Risk Percent approach

◦ Advanced Techniques Martingale / Anti-Martingale Equity Curve approach Monte-Carlo

Introduction

Dr. Bruce Vanstone

Part 3 – Drawing conclusions from the results◦ Overall summary◦ General conclusions

Introduction

Dr. Bruce Vanstone

What this part is (and isn’t!) about

Position Sizing is also often referred to as Money Management – these are the same thing

This part is about the best ways to determine the size of your positions – in other words, how much of your portfolio gets allocated to each stock selected

Part 1 – What are we trying to achieve

Dr. Bruce Vanstone

Interestingly, this is mainly a problem that concerns traders!

◦ From a finance perspective, many investors are interested in self-financing portfolios

This is because in academia, it is understood that the market is efficient. As price movements are thought to be random, there is no reason for preferring (in a position sizing sense) one position over another

Part 1 – a problem for traders

Dr. Bruce Vanstone

A strategy must have an ‘edge’ for you to be ‘successful’ at trading

How ‘successful’ ($ vs risk) you are is determined by how well you can size your positions

The dollar return from a strategy is a factor of the dollar amount traded ◦ Casino blackjack makes a good analogy here

Part 1

Dr. Bruce Vanstone

3 parts to developing a system (Chande)◦ Rules to enter and exit trades◦ Risk control◦ Money Management (Position Sizing)

Important: No Position Sizing strategy can turn a ‘bad’

system ‘good’ A good Position Sizing strategy can make a

‘good’ system ‘better’

Part 1

Dr. Bruce Vanstone

Importance of position sizing

Many traders spend a great deal of time back-testing their entries and exits…◦ Which appears to be of very limited value!

…and almost no time at all on Position Sizing

In terms of ‘Contribution to Success’, the entry and exit rules appear to have only (at best) a minor influence◦ Likely related to when in the cycle they are applied, not what

they are!

Part 1

Dr. Bruce Vanstone

As we shall see, the Position Sizing rules can have a major influence

Research regarding time spent in parts of trading system design shows that Money Management contributes more benefit than entry/exit research (3 Laws of Successful Trading)

Part 1

Dr. Bruce Vanstone

Types of techniques in common use◦ ‘Standard’ Approaches◦ ‘Advanced’ Approaches

Most traders seem content to stop at standard techniques

They normally run a few simulations, change a few position sizing parameters, pick the best one, then get busy…◦ ... Or use that ridiculous 2% risk rule

Part 1

Dr. Bruce Vanstone

This is a ‘poor’ strategy for selecting the most significant determinant of your ‘success’!

We should all be spending a lot more time thinking about position sizing, and a lot less worrying about ‘the market’ and our ‘rules’◦ Focus on things we can control◦ Focus on things with the biggest effect

Part 1

Dr. Bruce Vanstone

Requirements of a ‘good’ position sizing technique

A good position sizing technique relates to◦ 1. Quality of your signal◦ 2. State of the market◦ 3. Amount of your equity

‘Standard’ techniques normally react only to number 3, and occasionally, (in a much lesser way), number 1

Part 1

Dr. Bruce Vanstone

In the next part of this seminar, we will take a simple system, and examine the effect of different position sizing techniques on it

Look, whether at this stage of your trading knowledge you are willing to accept it or not, the rules you use to enter and exit the market are almost inconsequential – they just provide you with a slight edge and help you engage with the market at the right time

Having gone through this process many times, with many, many systems and traders, these results are quite ‘generalizable’

Part 1

Dr. Bruce Vanstone

An example system: ‘Trending 101’ To see the results of different position sizing

techniques, we need a ‘system’ to work with

◦ I typically use a system I call ‘Trending 101’ – its about as simple a trending system as you can imagine, and clearly shows the ‘generalizable’ effect of this work on trend trading strategies

For this system, we are interested in the question ‘What is in the DNA of a ‘longer-term trade?’

Part 2 – What we can learn from Simulations

Dr. Bruce Vanstone

Rules for ‘Trending 101’

Buy: if closing price today is higher than the last 21 days

Sell: if closing price today is lower than the last 21 days

THIS IS AN EXAMPLE ONLY! It is not a recommendation to trade this way!

FOCUS on the DNA idea!

Part 2

Dr. Bruce Vanstone

Part 2

Dr. Bruce Vanstone

What we will now do is look at the return, exposure, and maximum drawdowns of ‘Trending 101’ over prior 10 years in the Australian Stockmarket (ASX200), subject to a variety of position sizing techniques

Our goal is to see the effects of different position sizing techniques on this system, with the aim of understanding how to generalize these effects

Part 2

Dr. Bruce Vanstone

This should enable us to draw sensible conclusions about better ways to size our positions

For simulation purposes, we will assume a starting capital of $100K, and include the effects of transaction costs

Part 2

Dr. Bruce Vanstone

Data

ASX200◦ includes effect of delistings, name changes etc◦ doesn’t need controlling for liquidity

Part 2

Dr. Bruce Vanstone

I have divided position sizing up into two main camps◦ Standard techniques (used by the vast majority of

traders)◦ Advanced techniques (not very common, but

potentially much more powerful)

I will explain each approach within each technique, and assess it according to the three requirements for a good Position sizing strategy.

Then we will see its effect on ‘Trending 101’s DNA

Part 2

Dr. Bruce Vanstone

Remember, we are not focused on the actual values for return, exposure and maximum drawdowns

We are focused on how much as a percentage (and in which directions) these values change, as we examine some different position sizing techniques

Remember that all we are doing is changing the way we bet our money. We are still using the same trades every time.

Part 2

Dr. Bruce Vanstone

Recap!

A good position sizing techniques reacts to◦ 1. Quality of your signal◦ 2. State of the market◦ 3. Amount of your equity

We will monitor changes in◦ Returns (APR%)◦ Exposure (% of time money is in the market)◦ Maximum drawdown (%)

Part 2

Dr. Bruce Vanstone

Standard Techniques◦ Fixed Dollar approach◦ Percent of Equity approach◦ Risk Stop percentage – I won’t even bother!

Part 2

Dr. Bruce Vanstone

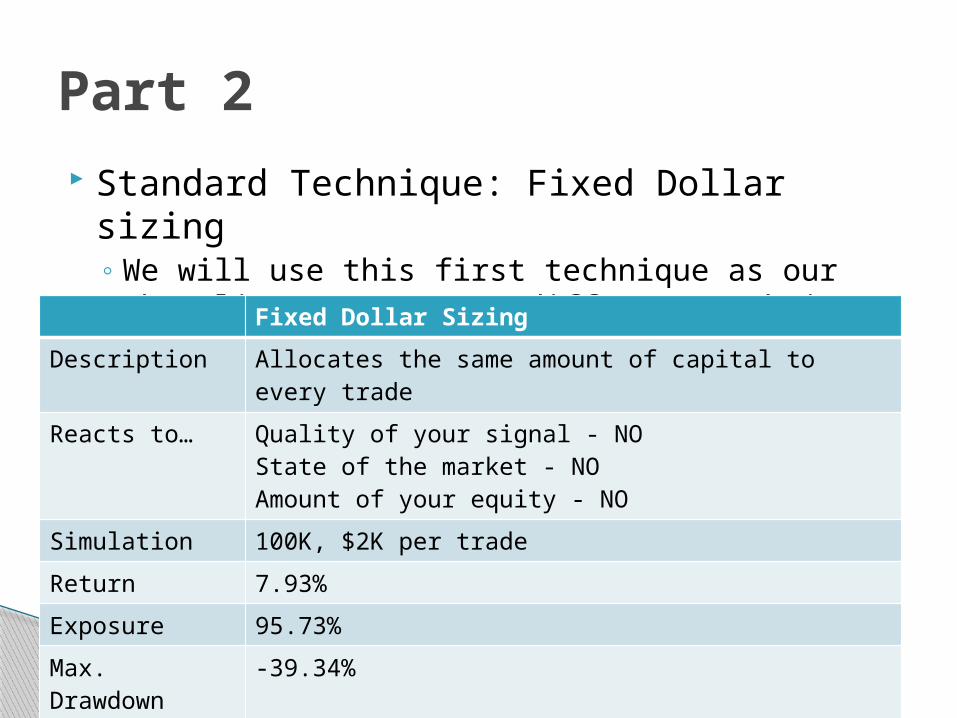

Standard Technique: Fixed Dollar sizing◦ We will use this first technique as our ‘baseline’ to

compare different techniques to

Part 2

Fixed Dollar Sizing

Description Allocates the same amount of capital to every trade

Reacts to… Quality of your signal - NOState of the market - NOAmount of your equity - NO

Simulation 100K, $2K per trade

Return 7.93%

Exposure 95.73%

Max. Drawdown

-39.34%

Dr. Bruce Vanstone

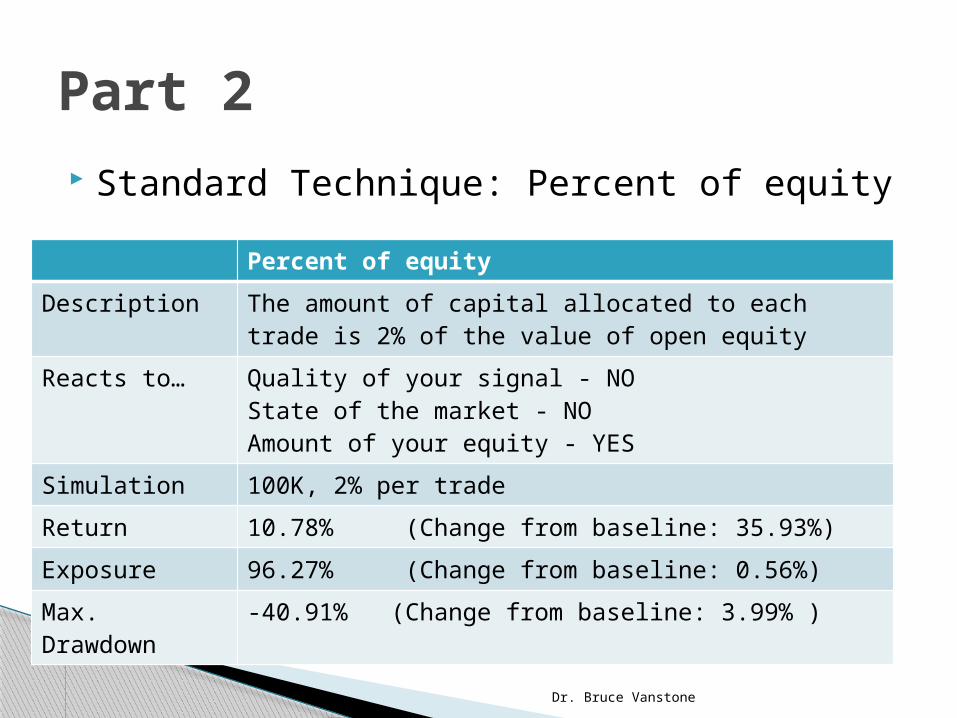

Standard Technique: Percent of equity

Part 2

Percent of equity

Description The amount of capital allocated to each trade is 2% of the value of open equity

Reacts to… Quality of your signal - NOState of the market - NOAmount of your equity - YES

Simulation 100K, 2% per trade

Return 10.78% (Change from baseline: 35.93%)

Exposure 96.27% (Change from baseline: 0.56%)

Max. Drawdown

-40.91% (Change from baseline: 3.99% )

Dr. Bruce Vanstone

Advanced techniques◦ Martingale / Anti-Martingale approach◦ Market driven◦ Equity Curve approach

Part 2

Dr. Bruce Vanstone

To understand where these techniques come from its necessary to revisit basic probability, statistics and a little game theory (sorry!)

Consider the following ‘game’:◦ Toss a fair coin 10 times◦ I can bet $1 on the outcome of each toss◦ If the result is a Head, I get an extra $1◦ If it’s a Tail, I lose my $1

Easy Question: Can I make any money at this game?

Part 2

Dr. Bruce Vanstone

To be honest, we should say NO… but the reason why is important.

Harder question: Why not?

Part 2

Dr. Bruce Vanstone

Its not because the probability of winning is 50:50

We must say NO because the outcome of the next coin toss is not dependant on the last coin toss (coin tosses are statistically independent events)

Part 2

Dr. Bruce Vanstone

Game 1:

H T H H T H T T H T T H H T H T

Game 2:

H H H H H H H H T T T T T T T T

50:50? What about a sequence?

Part 2

Dr. Bruce Vanstone

In academic finance, this is why there is so much debate about Random Walks and Efficient Markets

Its really a debate about whether price changes are statistically independent from each other◦ Which means random!

Part 2

Dr. Bruce Vanstone

Advanced techniques rely on the fact that the trades you generate from your trading system may not all be independent of each other (even though the prices could be)

Or, put differently, the success of your next trade may (in some way?) be determined by your last trade, and/or the state of the market, and/or something else

Part 2

Dr. Bruce Vanstone

This is really important, because many traders treat each individual trade as if it was independent of the last (or of the market), but it is extremely unlikely that this is true.

It is important to understand that in trading, you believe that the probability of winning a given trade is most likely not a statistically independent event

◦ unless your trading rules are actually random, in which case, you have a bigger problem!

Part 2

Dr. Bruce Vanstone

Consider two of our ‘Coin Toss’ games The probability of a win in both games is 50%

Game 1: H,H,T,H,T,T,H,H,T,H,T,T,… Game 2: H,H,T,T,H,H,T,T,H,H,T,T,…

I cannot win Game 1 I cannot lose Game 2 (if I recognize the fact that

the outcome of a toss is not independent of the previous toss)◦ This would mean a ‘crooked’ coin of course!

Part 2

Dr. Bruce Vanstone

So the key to ‘Advanced’ methods relates to finding something which relates to your trade sequence probability

Fortunately, that may not be as hard as it sounds

In statistical terms, this is called finding ‘streaks’, and can be implemented via a ‘runs test’

Part 2

Dr. Bruce Vanstone

However, for many traders, logic also suggests the answer could be related to:◦ The previous trade (or trades)

Most systems go through periods of winning and losing – not random wins/losses

◦ The market For many systems based on trends, the overall

market may help dictate sequences of wins and losses

◦ Unknown Just because we are not sure what it is, doesn’t mean

we can’t use it! Because…. It shows itself in our equity curve

Part 2

Dr. Bruce Vanstone

The previous trade? If the probability of winning is influenced by

the success or failure of the previous trade(s), then this is exploitable

Technique: martingale/anti-martingale

Part 2

Dr. Bruce Vanstone

Martingale betting: increasing bet size after a loss

Anti-Martingale betting: increasing bet size after a win

Martingale strategies for betting were popular in 18th century France, when playing games of chance

Part 2

Dr. Bruce Vanstone

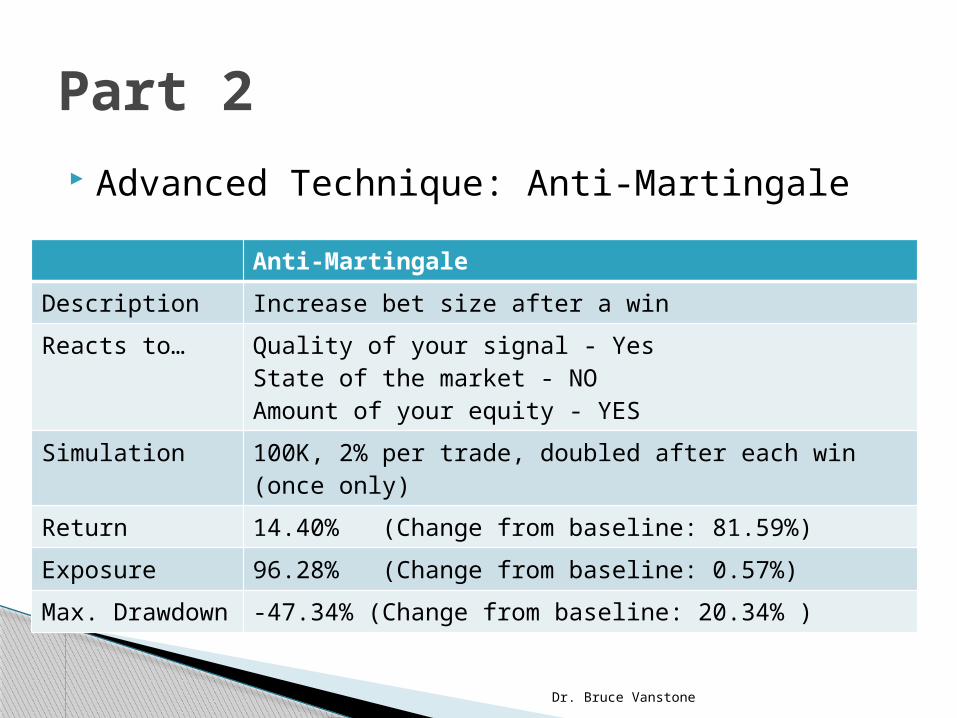

Advanced Technique: Anti-Martingale

Part 2

Anti-Martingale

Description Increase bet size after a win

Reacts to… Quality of your signal - YesState of the market - NOAmount of your equity - YES

Simulation 100K, 2% per trade, doubled after each win (once only)

Return 14.40% (Change from baseline: 81.59%)

Exposure 96.28% (Change from baseline: 0.57%)

Max. Drawdown

-47.34% (Change from baseline: 20.34% )

Dr. Bruce Vanstone

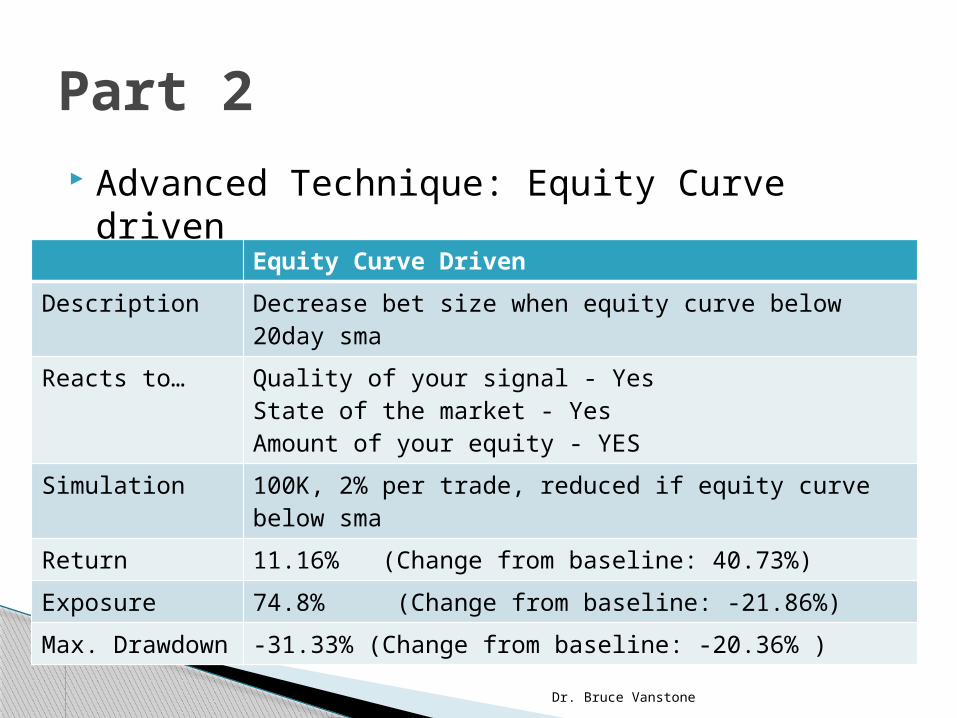

Advanced Technique: Equity Curve driven

Part 2

Equity Curve Driven

Description Decrease bet size when equity curve below 20day sma

Reacts to… Quality of your signal - YesState of the market - YesAmount of your equity - YES

Simulation 100K, 2% per trade, reduced if equity curve below sma

Return 11.16% (Change from baseline: 40.73%)

Exposure 74.8% (Change from baseline: -21.86%)

Max. Drawdown

-31.33% (Change from baseline: -20.36% )

Dr. Bruce Vanstone

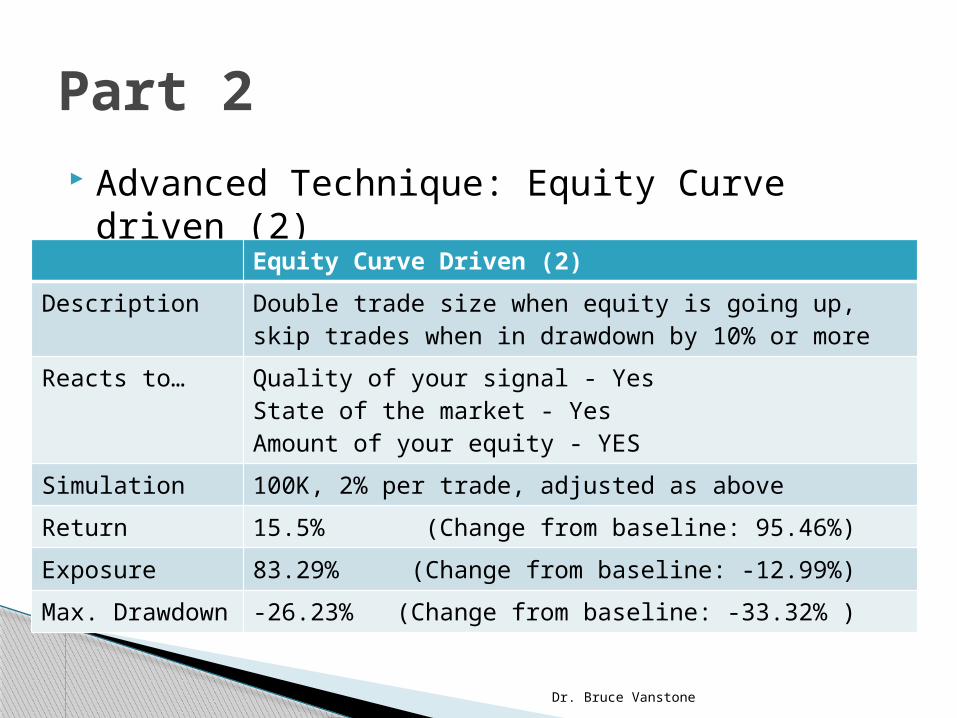

Advanced Technique: Equity Curve driven (2)

Part 2

Equity Curve Driven (2)

Description Double trade size when equity is going up, skip trades when in drawdown by 10% or more

Reacts to… Quality of your signal - YesState of the market - YesAmount of your equity - YES

Simulation 100K, 2% per trade, adjusted as above

Return 15.5% (Change from baseline: 95.46%)

Exposure 83.29% (Change from baseline: -12.99%)

Max. Drawdown

-26.23% (Change from baseline: -33.32% )

Dr. Bruce Vanstone

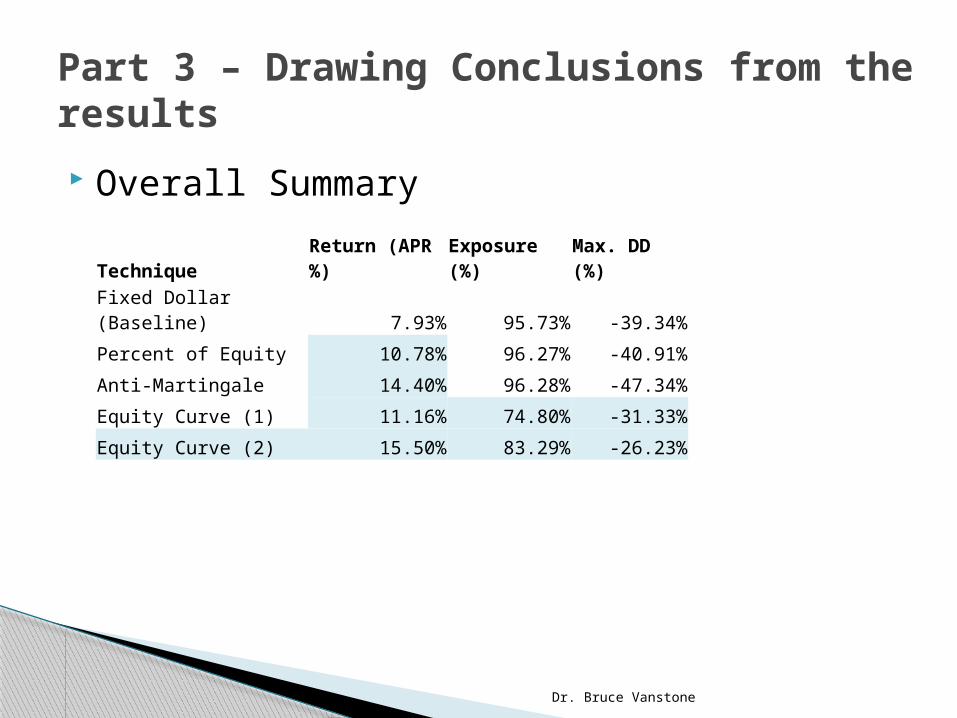

Overall Summary

Part 3 – Drawing Conclusions from the results

Technique Return (APR%) Exposure (%) Max. DD (%)

Fixed Dollar (Baseline) 7.93% 95.73% -39.34%

Percent of Equity 10.78% 96.27% -40.91%

Anti-Martingale 14.40% 96.28% -47.34%

Equity Curve (1) 11.16% 74.80% -31.33%

Equity Curve (2) 15.50% 83.29% -26.23%

Dr. Bruce Vanstone

General Conclusions

Significant improvement can be made to a strategy by changing the way it sizes positions

Overall, the largest improvements in increasing return and decreasing risk appear to come not from your trading signals, but from knowing when to act on your signals…

… and stopping trading as soon as you enter a drawdown period

Part 3

Dr. Bruce Vanstone

The really hard question for tonight: Why?

Part 3

Dr. Bruce Vanstone

Turns out it appears to be a bit of a slap in the face for most traders

Returns increase and drawdown decreases because of when you aren’t trading, NOT because of when you are!

Which relates back to what I was getting at in an earlier slide:◦ (from prior slide) Look, whether at this stage of your trading

knowledge you are willing to accept it or not, the rules you use to enter and exit the market are almost inconsequential – they just provide you with a slight edge and help you engage with the market at the right time

Part 3

Dr. Bruce Vanstone

Returns increase and drawdown decreases because of when you aren’t trading, NOT because of when you are!

The curse of Technical Analysis and back testing software:◦ Makes you wonder why people spend so much time

playing with their entry signals Probably because even though its almost pointless, its

easy and can be fun! Seriously, though... The better the ‘edge’ the more

robust/reliable the systems can be… the better the position sizing, the more lucrative the systems can be

◦

Part 3