Embed Size (px)

Citation preview

AAWW Investor-Analyst DayJune 6, 2014

Leading the Way Forward

Safe Harbor Statement

2

This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Actof 1995 that reflect Atlas Air Worldwide Holdings, Inc.’s (AAWW) current views with respect to certain current and futureevents and financial performance. Such forward-looking statements are and will be, as the case may be, subject to manyrisks, uncertainties and factors relating to the operations and business environments of AAWW and its subsidiaries thatmay cause actual results to be materially different from any future results, express or implied, in such forward-lookingstatements.

For additional information, we refer you to the risk factors set forth in the documents filed by AAWW with the Securitiesand Exchange Commission. Other factors and assumptions not identified above are also involved in the preparation offorward-looking statements, and the failure of such other factors and assumptions to be realized may also cause actualresults to differ materially from those discussed.

AAWW assumes no obligation to update the statements in this presentation to reflect actual results, changes inassumptions, or changes in other factors affecting such estimates, other than as required by law.

This presentation also includes some non-GAAP financial measures. You can find our presentations on the most directlycomparable GAAP financial measures calculated in accordance with accounting principles generally accepted in theUnited States and our reconciliations in our earnings release dated May 1, 2014, which is posted on our Web site atwww.atlasair.com.

Today’s AAWW Attendees

Bill FlynnPresident and Chief Executive Officer

John DietrichEVP and Chief Operating Officer

Spencer SchwartzEVP and Chief Financial Officer

Greg GuillaumeVP, Strategic Development

Edward McGarveyVP and Treasurer

Dan LohSenior Director,Investor Relations

Michael SteenEVP and Chief Commercial Officer

Adam KokasEVP, General Counsel,CHRO and Secretary

Keith MayerVP and Controller

Jeff ZeunikVP, Financial Planning and Analysis

Bonnie RodneySenior Director,Marketing and Communications

3

Today’s Agenda

4

Welcome Adam Kokas

Overview Bill Flynn

Commercial Michael Steen

Operations John Dietrich

Financial Spencer Schwartz

Wrap-Up Bill Flynn

Q&A

Lunch

AAWW Investor-Analyst DayJune 6, 2014

L E A D I N Gthe WAY FORWARDBill Flynn

President and Chief Executive Officer

Overview

A Strong Leader in a Strengthening Industry

6

Global AviationAt center of modern, global economy

Long-term growth industry

Efficient access to markets; catalyst to international trade

Contributes to economic and social development

Drives increased competition and innovation

Strategic supply chain component

Over $6 trillion of goods airfreighted annually; ~35% of total world trade

Committedto

Creating, Enhancing andReturning Value to Shareholders.

AtlasRecognized leader in international aviation outsourcing

Resilient business model focused on long-term growth

Strong customer portfolio; creative partner/advisor able to link customers with opportunities

Business initiatives, investments leading the way forward

Uniquely positioned to identify, secure and sustain growth opportunities

Capacity to develop new organizational capabilities aligned with customers’ needs

Significant upside operating leverage

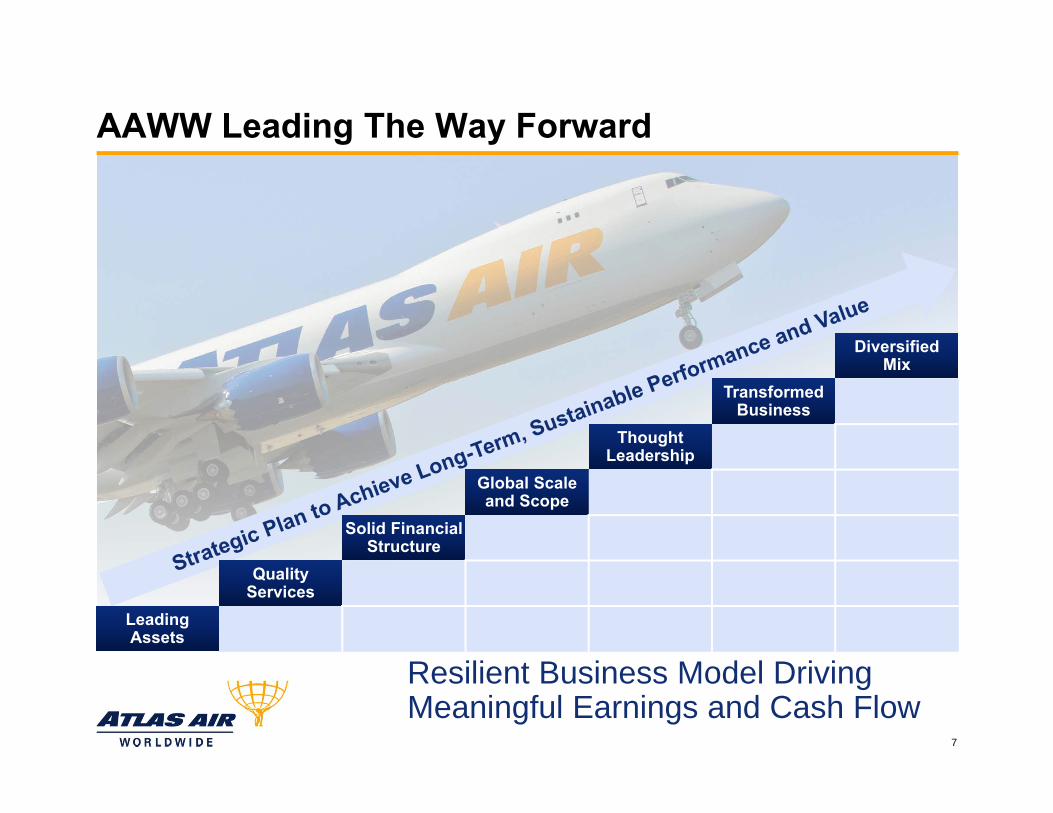

AAWW Leading The Way Forward

Resilient Business Model DrivingMeaningful Earnings and Cash Flow

7

DiversifiedMix

Transformed Business

Thought Leadership

Global Scale and Scope

Solid Financial Structure

Quality Services

LeadingAssets

Key Accomplishments: Foundation for Growth

8

Our BusinessBegins withthe Customer

Meeting/exceeding aggressive objective customer service quality goals Providing superior value-added services An integrated partner, thought leader, advisor – we make customers more profitable

ACMI

Expanded market leadership and customer base, including emerging/expanding markets Added Astral (Africa), Chapman Freeborn (Europe), BST Logistics (Asia);

expanded service with Etihad (Middle East) Placed two returning 747-8Fs in service for DHL Express (Transpacific);

also added 747-400F (Round-the-World)

Dry Leasing Acquired six 777Fs, each with long-term leases with top-tier customers already in place

Added AeroLogic and TNT (Europe) as well as Emirates (Middle East) as customers

CMI Within ACMI, initiated VIP 767 passenger service for MLW Air (U.S.)

Launched two new 767Fs in intra-Asian cargo service for DHL Express

CommercialCharter

Enhanced position as top scheduled charter carrier in South America

Expanded passenger charter operations

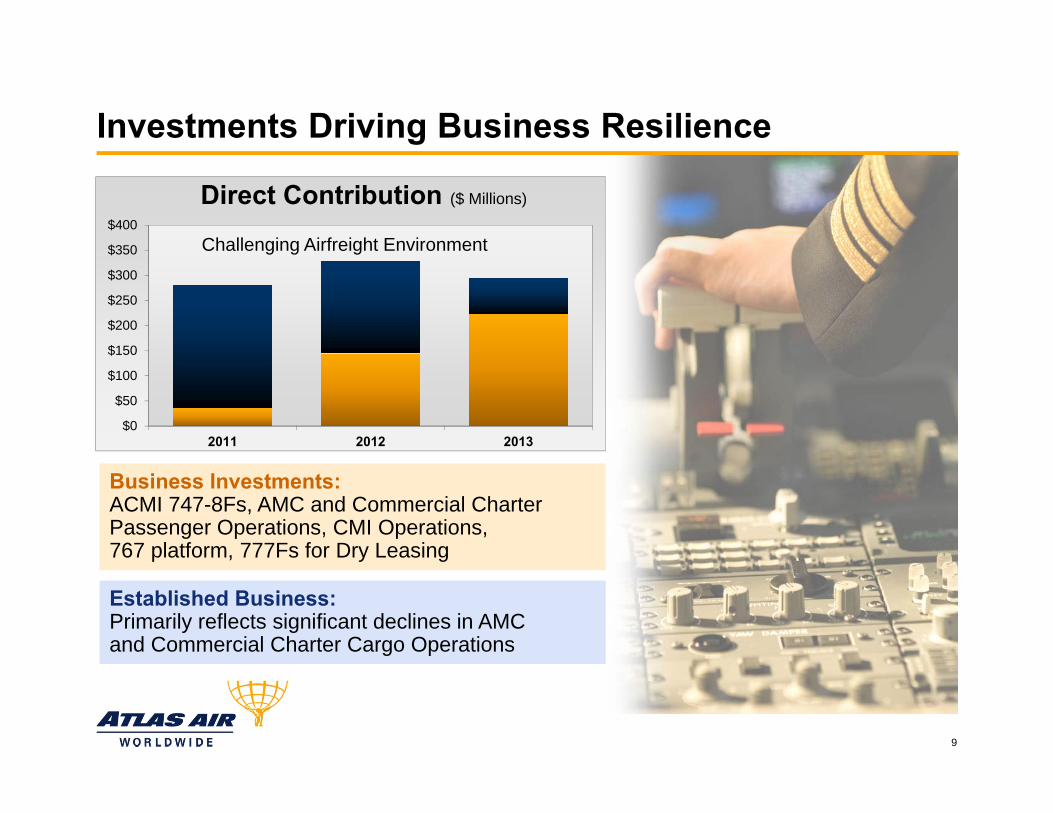

Investments Driving Business Resilience

9

$0

$50

$100

$150

$200

$250

$300

$350

$400

2011 2012 2013

Direct Contribution ($ Millions)

Challenging Airfreight Environment

Business Investments:ACMI 747-8Fs, AMC and Commercial Charter Passenger Operations, CMI Operations,767 platform, 777Fs for Dry Leasing

Business Investments:ACMI 747-8Fs, AMC and Commercial Charter Passenger Operations, CMI Operations,767 platform, 777Fs for Dry Leasing

Established Business:Primarily reflects significant declines in AMCand Commercial Charter Cargo Operations

Established Business:Primarily reflects significant declines in AMCand Commercial Charter Cargo Operations

PACTL –

48.6 49.7 49.2 50.2 51.7

20

30

40

50

60

2010 2011 2012 2013E 2014F

Frei

ght T

onne

s(M

illio

ns)

Total Global Airfreight Tonnage

∆Y-o-Y

Airfreight Demand Growing

10

Source: PACTL, ICAO 2010 – 2011, IATA 2012 – 2014F (IATA – June 2014)

19.2% 2.2% (1.0)% 2.0% 3.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

0

20

40

60

80

100

120

140

Y-o-

Y G

row

th

Frei

ght T

onne

s(T

hous

ands

)

Shanghai Airport Cargo Traffic (PACTL)

Record monthly tonnage March 2014; strongest first quarter ever

Total global airfreight tonnage growing from record levelsInternational freight tonne kilometers (FTKs) to grow 3.6% in 20142013-2017 international FTK CAGR of 5.0%

–––

IATA

2014 Operational Goals and Objectives

Deliver superior service quality to our customers

Expand our ACMI and CMI business

Maximize our AMC and Commercial Charter business opportunities

Achieve Continuous Improvement savingsand efficiencies

Develop Titan (dry leasing) platform

Execute share repurchase program

In other words… Drive Value for Shareholders

11

Off to Good Start in 2014

AAWW results led by investments to strengthenand diversify business mix…

Positive industry demand trends

Expand aircraft and service offerings and develop new customer relationships

Confident about resilience of transformed business model

Well-positioned to capitalize on market improvement, long-term business growth

12

Continuous Improvement – An Ongoing Journey

13

It’s about: Doing things smarter, faster, more

efficiently and at lower cost

Adding value to the customer

Enhancing operating safety

More thoughtful decisions and processes

Differentiating ourselves from the competition – customer service

Building relationships

All leads to being the customer’sfirst choice

Atlas Strategy for Future Growth

14

We have implemented astrategic plan that… Delivers meaningful earnings

Diversifies the business mix

Leverages asset acquisitions

Generates meaningful cash flow

Future growth requires adisciplined plan that… Builds on strength of core model

Invests in appropriate asset portfolio

Balances operation segment risk/reward profiles

Develops new organizational capabilities

Disciplined Approach to Business Growth

Expand asset-lightbusiness Target strategic

opportunities

Expand asset-lightbusiness Target strategic

opportunities

CMICMI

Focus on scale Non-speculative

investments forregional networks

Focus on scale Non-speculative

investments forregional networks

767s767s

Evaluate opportunities for incremental aircraft that… Provide customers most

efficient assets for their needs

Evaluate opportunities for incremental aircraft that… Provide customers most

efficient assets for their needs

FleetFleet

Focus on freighters Invest in quality assets with

lease commitments

Focus on freighters Invest in quality assets with

lease commitments

Dry LeasingDry Leasing

15

Capital Allocation Strategy

Committed to creating, enhancing, returning value to our stockholders

Repurchased 1.7 million shares, 6.5% of outstanding stock, in 2013

Authorization to repurchaseup to $60 million

Cash prioritization:– Balance sheet maintenance– Business investment – Share repurchases

16

ResilientBusiness Model

AAWW Leading The Way Forward

Executing our planIncreasing contributionfrom business investments… Modern fleet: New 747-8Fs Higher ACMI and CMI volumes Added 777Fs for Dry Leasing Expanding 767 platform Added Passenger flying Operating efficiencies Meaningful earnings Return of capital

…In a long-term growth industry

17

A Strong Leader in a Strengthening Industry

AAWW Investor-Analyst DayJune 6, 2014

L E A D I N Gthe WAY FORWARDMichael Steen

Executive Vice President and Chief Commercial Officer

Commercial

Business Developments

19

Placed one 747-8F with BST Logistics Placed two 747-8Fs, additional

747-400F with DHL Express Placed one 747-400F with Astral

Aviation Extended contract for two 747-400Fs

with Qantas

ACMI

CMI Launched 767-200 VIP operation for MLW Air

Increased Boeing LCF flying to3.1 average aircraft in 1Q14 from1.6 aircraft in 1Q13

Initiated Asia-Pacific CMI flying for DHL

AMC Provided thought leadership to CRAF and USTRANSCOMM

Added new members to FedEx Team (American, US Airways)

Positioned to maximize our participation in CRAF program

Business Developments

20

DryLease

Charters Despite weak market, grew Commercial Charter segment revenues by over 10% to $496 million

Participated in severalhi-tech product launches

38 Bowl Game charters

Acquired six 777-200LRFs Long-term leases attached:

– TNT Express (3)– AeroLogic (2)– Emirates (1)

International Global Airfreight:Growth Returning

21

Source: ICAO 2003 – 2011, IATA 2012 – 2014F (IATA – June 2014)

IATA – Total global airfreight tonnage growing from record levels

IATA expects international freight tonne kilometers (FTKs) flown to grow 3.6% in 2014

IATA forecasts 2013-2017 international FTK CAGR of 5.0%

33.6 36.8 37.7

40.1 42.5 41.1 40.8

48.6 49.7 49.2 50.2 51.7

20

30

40

50

60

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014F

Total Global Airfreight Tonnage Growing from Record Levels

Freight Tonnes(Millions)

6.7% 9.6% 2.5% 6.2% 6.2% (3.2)% (0.8)% 19.2% 2.2% (1.0)% 2.0% 3.0%∆Y-o-Y

Airfreight Demand Growing

Source: PACTL, HKIA

22

Y-o-Y Percentage Growth

PACTL – Record monthly tonnage March 2014; strongest first quarter ever

HKIA – Tonnage up 6.0% in 1Q14; 5.6% year-to-date

Dubai, Frankfurt tonnages also growing; Miami steady at high levels

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0

20

40

60

80

100

120

140

Y-o-

Y G

row

th

Frei

ght T

onne

s(T

hous

ands

)

Shanghai Airport Cargo Traffic (PACTL)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0

50

100

150

200

250

300

350

400

450

Y-o-

Y G

row

th

Frei

ght T

onne

s(T

hous

ands

)

Hong Kong International Airport Cargo Traffic (HKIA)

Freight Tonnes (Thousands)

The Key Underlying Express Market is Growing

23

Notes: Weighted average of growth rates in international express package volume reported by these express operators.Weighting is 50% DHL, 25% UPS and 25% FedEx. TNT does not report in sufficient detail to include.1Q 2014 figure shown assumes annualized performance

A substantial amount of Atlas’ business is from serving the International Express market The International Express market is showing robust growth; 6% CAGR since 2010 Express growth:

DHL 5-6% 2011-2020; UPS 4-6% in 2014; FedEx “market continues to grow”

100%

107%

114%

121%

127%

90%

95%

100%

105%

110%

115%

120%

125%

130%

135%

2010 2011 2012 2013 1Q 2014

International Express Market – DHL, FedEx and UPSChange in Package Volume (Base year 2010 - 100%)

Global Airfreight Drivers

24

By Sectors Chart Source: Atlas researchBy Region Chart Source: International Air Transport Association – April 2014

Market Size

By Region

41%

26%

14%

14%

Asia Pacific

Europe

North America

Middle East

Latin America 3%Africa 2%

Percent of International Freight Tonne Kilometers (FTKs)By Sectors

Industry Sectors Served by AAWW Customers

17%

17%

16%11%

10%

6%

11%High-Tech Products

Capital Goods

Apparel

Pharma-ceuticals

Intermediate Materials

Automotive

Other Live, 1%

Perishables

Mail & Express 6%

5%

Products Strategic Choice Specialty ConsiderationAirfreight share:

1.5-2.5% global volume, 35% global value

High-value,time-sensitive items; items with short shelf lives

Products/supply chains withjust-in-time delivery requirements

Products with significant security considerations

Global Airfreight Flows – Major Trade LanesAtlas’ global scale connects manufacturing locations and markets worldwide

Allows the maximizing of stack yields by combining airfreight opportunities across multiple trade lanes

2012-2013 Global Air Freight VolumesFigures in ‘000 tonnes

Industrial / Electrical Machinery, Small packages

Flowers, Fish, Vegetables

743743Industrial / Electrical Machinery, Small packages

Flowers, Fish, Vegetables

743

Machinery

Garments, Perishables

1,4241,424Machinery

Garments, Perishables

1,424

Machinery, Auto Parts, Express Pkgs

Apparel

4,2674,267Machinery, Auto Parts, Express Pkgs

Apparel

4,267

Intermediate goods flows (cross-border supply chains)

6,0006,000 Intermediate goods flows (cross-border supply chains)

6,000

Machinery, Perishables

Apparel, Luxury goods

1,1931,193Machinery, Perishables

Apparel, Luxury goods

1,193

Express, other

1,4001,400Express, other

1,400

Oil & gas equip, Machinery, Small packages

Perishables, Apparel,Auto components

130130Oil & gas equip, Machinery, Small packages

Perishables, Apparel,Auto components

130

3,4313,431Telecom Equip., Apparel, Machinery

Machinery, ChemicalsExpress Pkgs

3,431Telecom Equip., Apparel, Machinery

Machinery, ChemicalsExpress Pkgs

8,5008,500Express, other

8,500Express, other

Machinery

Perishables, Apparel

1,0751,075Machinery

Perishables, Apparel

1,075

1,2291,229Industrial / Electrical Machinery, Small packages

Flowers, Fish, Vegetables

1,229Industrial / Electrical Machinery, Small packages

Flowers, Fish, Vegetables

Machinery, Auto parts, Chemicals, Express Pkgs

2,8392,839Machinery, Auto parts, Chemicals, Express Pkgs

2,839

577577Machinery

Apparel, Pharma

577Machinery

Apparel, Pharma

25

The percentage (by weight) of the top twenty categories of goods shipped by air on transpacific lanes has remained almost constant

Reports of Modal Shift Are Overstated

26

Source: Boeing

Air cargo has maintained its share in the key transpacific cargo market

2.0% 1.8%2.0% 2.0%

2.2%

2.0%

1.7%

2.0%

2.0%

2.3%

2.5%2.2%

2.1%

0

10

20

30

40

50

60

70

80

Tonn

es(m

illion

s)

Air Cargo Market Share in the Transpacific Cargo Market

Ocean Cargo Market Share Air Cargo Market Share

Air vs. Ocean?

27

Air continues to be an essential component of the supply chain

Time Critical Products

Reason for Time Criticality

Current Market Dynamics / Drivers

Current Conditionsor Expectations

Perishables Product life Economic conditions…

Disposable income…

Improving

Increasing

High Value (Electronics)

Value of speed to market

Inventory carryingcost/risk

Obsolescence

Interest rates…

Product refresh cycle…

Inventory velocity…

Increase expected

Continued acceleration

Continued increase

High Margin (Fashion)

Stock-out cost

Speed to market

Trends in fashion/retail

Refresh cycles…

Trend response time…

Continued acceleration

Importance of speed is increasing

Industrial Time Critical

Production costripple effects

Sporadic disruptions… (auto component recallvs. redesign)

Focus on supply chain improvements, but continuing need is expected

Optimal Inventory Management is Key

28

Inventory to sales ratio remains low Last time inventory levels were this low, record demand for airfreight followed

Low inventory levels, combined with an improved economy, drive increased airfreight demand

Large Freighter Supply Trends

29

Source: Atlas (May 2014), Ascend (May 2014), Boeing (April 2014), company reports. Excludes parked aircraft, aircraft inExpress operations, combis and tankers; 747-200F total includes -100s and -300s. Boeing April 2014 777F total includes 40 deliveries to express operators (25 with FedEx, 8 with AeroLogic/DHL, 4 for DHL Express, and 3 with TNT).

32

5870

142

28

72

2046 46

133

48

91

21

41

0

20

40

60

80

100

120

140

160

180

Old Technology Sunsetting

747-200FCurrent Technology

747-400SF 747-400FNew Technology

Deliveries Measured

747-8FMD-11F 777FRecent But Challenged

2012 2012 2012 201205/14 05/14 05/14 05/14 04/1404/14

132

69

20122012

Projected production capacity will grow in line with forecast long-term demand growth of ~4% Older technology is nearly gone MD-11F and 747-400 converted freighter fleets are shrinking Large wide-body freighters will continue to dominate the major trade lanes Belly capacity cannot displace freighters

Main Deck to Belly?

30

Sources: ICAO, IATA, A4A, Boeing, Atlas

Main deck air cargo share is stable at ~60% and forecast to remain steady (belly share ~40%)

57%59%

62% 62% 62% 62% 62% 61%58% 59% 59% 60% 61% 60%

0%

10%

20%

30%

40%

50%

60%

70%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2016 2021

Percentage of World RTKs Carried on Freighters

Key Considerations

10% shift of Trans-Pac market from main deckto Pax belly requires50 incremental aircraft

Limitations on slot and route availability; not enough passenger demand; limited access to aircraft

Global average capacity availability on a 777-300ER is 18-20 tonnes*

New Pax 787s fly point-to-point, e.g. London to Phoenix; good for passengers, not cargo

*Considering 28 tonnes max structural cargo capacity availableafter allocating capacity to bags carried

Access to Best-in-Class Fleet toServe Multiple Market Segments

31

B747-8F: Superior technology platform Highest payload and lowest unit cost freighter Best suited to serve the “trunk routes” of global trade

Transpacific, Transatlantic, Round-the-world, Europe-Asia, North-South Americas

B777F: Superior technology platform Superior range profile Aircraft of choice for express operators Allows Integrators to offer intercontinental next day

delivery services

B767-300ERF: Regional work horse Aircraft of choice for regional trade corridors

(e.g., North America, Intra-Asia) Serves both general freight and express networks Increasing number of freighter conversions are

expected of this aircraft type

Integrated Partnership → Our Value Proposition

32

Operations Excellence World’s most efficient fleet of large- and medium-body aircraft Deliver best-in-class operational performance Flawless implementation and execution Delivering lower total operating cost

Commercial Development Leading market knowledge and cross industry presence Interactive dialogue creating opportunities Best-in-class analysis capabilities and consultancy support Proactive network and route assessment

We Live Our Customers' Values They are market leaders representing the entire industry We represent their brand and deliver on their customer commitments We make their operations more flexible and efficient We continuously focus on delivering increased value

Our Customers Reflect Our Focus on Quality

33

Long-term, profitable relationshipsResilient Business Model and Predictable Revenues

Growth-oriented market leaders High degree of customer integration Focused on continuous development and growth Long-term contractual commitments Covering the entire air cargo supply chain

Our strength

Shippers Forwarders / Brokers Airlines Express

Global Operating Network

34

158,937 Total Block Hours Operated in 201325,571 Flights

430 Airports in 124 Countries711 Charters Completed108 Unique Customers

Asian trade lanes lead market growth

Globalization requiresglobal supply chain solutions

Outsourcing becoming more relevantfor both cargo and passenger operators

Rapid market growth inMiddle East, Africa, South America

Expect to grow key businesses:ACMI, CMI, Charter, Scheduled Charter, Dry Leasing

Delivering Value to DHL

35

Joint analysis and modeling

Added a 747-400F, becoming the 10th 747 in the fleet operating for DHL Express

Added 767-300ERFs to feed long-haul and regional APAC network

Added 747-8F based on its capability; resulted in added capacity to supportDHL Express’ TPAC growth

What How

Focus on continued growth and delivering high-quality service

Delivering Value to Etihad

36

Round-the-world operation with 747-8F

Added new customers to Etihad’s networkAdded new markets to Etihad’s network

Routes selected because they were growingDelivered tangible and immediategrowth to Etihad

Solidified relationship as trusted advisor

Network analytics and customer knowledgeWhat How

Etihad Video

The IndustryThe Industry AtlasAtlas

The Future

38

Modern, reliable, fuel-efficient fleet

Differentiated fleet solutions:747/777/767

747-8Fs performing well

Strong portfolio of long-term customers committed to further expansion

Unique integrated value proposition

High degree of customer collaboration

Airfreight and integrators integralto global trade growth

Over $6 trillion of goods airfreighted annually; ~35% of total world trade

Higher-growth markets demandlarge wide-body assets

High-value, time-sensitive inventories demand airfreight-based supply chain

Airfreight provides a compellingvalue proposition`

Atlas is uniquely positioned for the future.

AAWW Investor-Analyst DayJune 6, 2014

L E A D I N Gthe WAY FORWARDJohn Dietrich

Executive Vice President and Chief Operating Officer

Operations

Deliver globaltime-definite networks

Innovative, outsourcedaviation solutions

Provide operational excellence and deliver customer value

A catalyst for growth!

Operations – A Competitive Advantage

40

Customer focused

Continuous Improvement

Our Business Starts with the Customer

41

Be the customer’sfirst choice… Deliver exceptional performance

Hold ourselves and vendors to the highest standards

Achieve aggressive reliability targets

Seek continuous improvement in everything we do

Be flexible to meet customer needs

Build strong relationships

Global Presence430 destinations around the world…

42

Our Fleet2006

18 Boeing “Classics”

20 Boeing 747-400 Freighters

43

18 Boeing “Classics”

20 Boeing 747-400 Freighters

Our Fleet with Titan Aircraft

22 Boeing 747-400 Freighters21 747-400Fs1 747-400BCF

4 Boeing Large Cargo Freighters (LCFs)Customer-owned

9 Boeing 747-8Fs

4 Boeing 767-200/300ER Passenger3 for AMC and Commercial Charter1 Custom Aircraft (customer-owned)

4 Boeing 747-400 Passenger2 Custom Aircraft (customer-owned)2 Boeing 747-400s for AMC and Commercial Charter

7 Boeing 767-200/300 FreightersFor DHL Express service (customer-owned)

1 Boeing 757-200 FreighterShanghai Airlines Cargo

2 Boeing 737-800 Passenger1 Kenya Airways1 Skymark Airlines

6 Boeing 777-200LRF3 TNT, 2 AeroLogic1 Emirates

1 Boeing 737-300 FreighterChina Postal

44

Leveraging Operations

45

2010(747 Pax CMI)

2011(AMC Pax)(747 & 767) 2012/13

(767 Cargo)Domestic and International

2010(LCF)

Diversification & Growth

Safety and Regulatory Compliance

Culture and commitment to safety

“Tone at the Top”

Robust internal and external audits

Proactive relationship with FAA, DOT, TSA and other regulatory authorities

On IATA Operational Safety Audit (IOSA) Registry since 2007

Zero findings in IOSA andDept. of Defense (DOD) biannual audits

Successful customer audits (e.g., Etihad)

Well-positioned for next DoD audit in August 2014

Flight Data Monitoring Program

Aviation Safety Action Program (ASAP)

Investigation Reporting Systems

Regular safety audits

Reduced aircraft damage and personal injuries

Proactive Safety Management System (SMS)

Safety and Compliance Are Top Corporate Priorities

ConsistentlyPositive Audits

46

Security

Our goal is to protect our people, our assets, our information systems and our customers

Highly experienced security team

Strong commitment to physical and cybersecurity

Security resources that cover more than430 destinations

Threat-based risk management program Implemented in coordination with customers Minimizes threats to personnel, company assets,

high-value cargo

Provide thought leadership to ensurecost-efficient and effective regulatory approach

Highly active in Washington, D.C.on policy and rule making initiatives

47

Continuous Improvement isan ongoing journey: Doing things smarter, faster and more efficiently Program in place since 2008

The focus in 2014 is on process improvements: Implemented enhanced Flight Planning System Fuel Management – "Fuel Wise" Crew Management Improve Maintenance and Engineering Processes Revisiting Insource/Outsource Decisions Information Technology

Continuous Improvement

48

Key Milestones

49

Exceeded customer on-time reliability requirements

Successful new customer start-ups– Astral (Africa), Chapman Freeborn (Europe)– Navitrans (China), Etihad (Middle-East)– DHL (Intra-Asia), MLW – (Domestic VIP)

Peak season flying for all major integrators– DHL, UPS and FedEx

Extended Air Force One training contract– Outstanding survey results

Successful Passenger Charter Operations– Sochi charters for NHL Players Association– College Bowl games– First U.S. carrier Hajj pilgrimage flights in years

Why Atlas?We manage diverse, complex and time-definite global networks

We are customer focused and deliver superior performance

Our global scale and operational capabilities are unparalleled

We possess industry-leading operational and technicalsubject-matter expertise

We collaborate with customersto provide value-added solutions and achieve best-in-class resultsWe are driving Continuous Improvement We are strategically positioned and focused on new opportunities to continue to deliver future growth

50

AAWW Investor-Analyst DayJune 6, 2014

L E A D I N Gthe WAY FORWARDSpencer Schwartz

Executive Vice President and Chief Financial Officer

Financial

Focused on Our Shareholders

52

ShareholdersLong-term sustainable performance and value

Diversified and predictable mix

Expand customer base

Savings through efficiencies

Return of capital

Stop providing guidance for peak season performance so early

Effective corporate governance practices

Committedto

Creating,Enhancing andReturning Valueto Shareholders

AtlasAdded nine 747-8Fs

Grew dry leasing with six 777Fs, developed passengeroperations, added 767 flying, expanding CMI

Several new strategic customers

Continuous Improvement

$72 million share repurchase

2014 earnings framework

Enhanced governance and compensation programs

Operating Revenueup 7%Adjusted* Operating Incomeup 60%ACMIDirect Contributionup 13%Adjusted* Earningsper Share$0.45

Results

1Q 2014

53

* See May 1, 2014 press release for non-GAAP reconciliations

ActivitiesThree 777-200ERFs underlong-term dry lease agreements acquired

Ex-Im bond issued on 9th -8F

Placed 9th -8F with BST Logistics

Two out of three returned -8Fs placed immediately

Continuous Improvement focus

Shifting profile of AMC flying Pax BHs flat;

Cargo BHs down 76% Cargo one-ways still declining

Mixed Charter market Increased demand Yields lag behind

Three -8Fs being returned

Conditions

Business initiatives and investments Have transformed the company to deliver

meaningful earnings in any environment

Seasonal business, majority of earnings generated in second half of the year

Two primary considerations: Military demand is declining Commercial airfreight volumes have

been essentially flat last three years

Block Hour total expected to be a few percentage points lower than 2013

> 70% in ACMI< 10% in AMCBalance in Commercial Charter

If airfreight growth returns: Atlas is positioned to be a prime beneficiary

Dry Leasing growing dramatically

If airfreight growth remains flat: Expect results to approximate 2013,

excluding decline from AMC

Maintenance expense ~ $175-$180 million

Depreciation ~ $115-$120 million

~30% effective income tax rate

2014 Framework

54

Capital Allocation – Last 12 Months

55*Includes cash, cash-equivalents, short-term investments, and restricted cash

1Q14 cash balance*: $302 MillionAll debt secured by an aircraft tail2014 estimated tax rate: 30%

Balance Sheet Maintenance

$72 million share repurchase6.5% of outstanding shares$0.18 immediate EPS accretion

Return of Capital

6 B777Fs2 B747-8FsACMI contribution up 13%Dry Lease contribution up dramatically

Business Investment

Evaluating Opportunities

56

KeyConsiderations

Existing business growth Business diversification Strategic fit Feasibility Implementation risks Hurdle rate Cash generation P&L impact IRR ROIC

Dry Leasing Opportunities

57

Solid CreditworthyMarquee Customers

Long LeasesAttached

Excellent Assets

Low-cost, Asset-backedFinancing

Dry leasing

Passenger

New aircraft types747-8F/777F/767

CMI

M&A

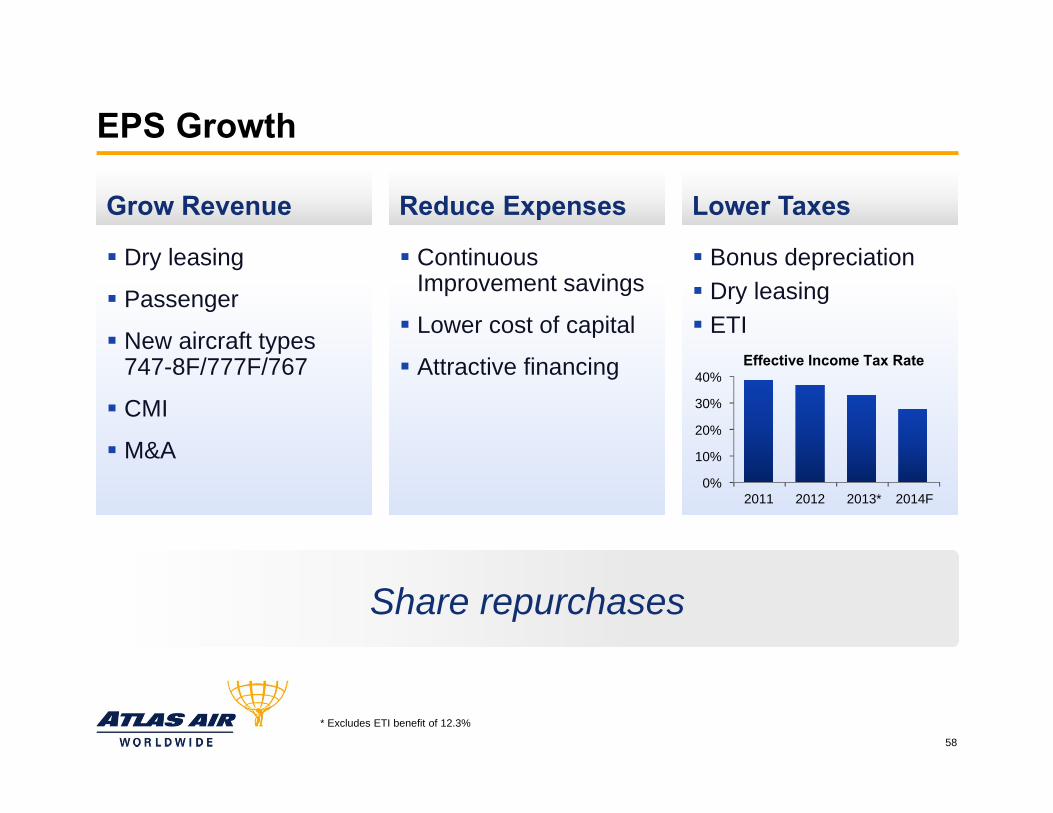

Dry leasing

Passenger

New aircraft types747-8F/777F/767

CMI

M&A

Grow RevenueGrow Revenue

Continuous Improvement savings

Lower cost of capital

Attractive financing

Continuous Improvement savings

Lower cost of capital

Attractive financing

Reduce ExpensesReduce Expenses

Share repurchases

EPS Growth

58

* Excludes ETI benefit of 12.3%

Bonus depreciation Dry leasing ETI

Bonus depreciation Dry leasing ETI

Lower TaxesLower Taxes

0%

10%

20%

30%

40%

2011 2012 2013* 2014F

Effective Income Tax Rate

Earnings Outlook

59

Commercial Earnings are Growing

2012 2013 2014F 2015F

OpportunisticAMC Earnings

2011 2012 2013 2014F 2015F

CoreBusiness Earnings

Recognizedfor Driving Cost-Efficiency and Innovation

Financings and Industry Recognition

60

Nine 747-8Fs financed at under 3%

Six 777Fs financed at 4.4% in tax-efficient structures

AFP Pinnacle Award

AAWW Investor-Analyst DayJune 6, 2014

L E A D I N Gthe WAY FORWARDBill Flynn

President and Chief Executive Officer

Wrap-Up

A Strong Leader in a Strengthening Industry

62

Global AviationAt center of modern, global economy

Long-term growth industry

Efficient access to markets; catalyst to international trade

Contributes to economic and social development

Drives increased competition and innovation

Strategic supply chain component

Over $6 trillion of goods airfreighted annually; ~35% of total world trade

Committedto

Creating, Enhancing andReturning Value to Shareholders.

AtlasRecognized leader in international aviation outsourcing

Resilient business model focused on long-term growth

Strong customer portfolio; creative partner/advisor able to link customers with opportunities

Business initiatives, investments leading the way forward

Uniquely positioned to identify, secure and sustain growth opportunities

Capacity to develop new organizational capabilities aligned with customers’ needs

Significant upside operating leverage

Thank you.The future looks bright.